Evaluating Activity-Based Costing in Managerial Accounting HI5017

VerifiedAdded on 2023/06/04

|18

|3905

|206

Report

AI Summary

This report evaluates the implications of the activity-based costing (ABC) system from a business perspective, utilizing two journal articles from different industries to assess its effectiveness in enhancing cost reporting. The study compares the traditional costing system with the ABC system, highlighting the benefits and challenges of implementing ABC in both public and service sectors. Key research questions address the implementation of ABC in public firms, its applicability to organizations with limited size and product lines, and the advantages gained by applying the ABC system. The analysis identifies similarities and differences between the two studies, focusing on improvements in cost projections and the elimination of loopholes in traditional costing methods. The report concludes with specific outcomes and recommendations for Australian management accountants to improve their management accounting procedures.

Running head: MANAGERIAL ACCOUNTING

Managerial Accounting

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Managerial Accounting

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1MANAGERIAL ACCOUNTING

Executive Summary:

The goal of this report is to evaluate the implications of the activity-based costing system

from the viewpoint of the business organisations. For effective evaluation of the topic, the

report has considered selecting two journal articles on different organisations belonging to

different industries. The two journal articles include the application of the activity-based

costing system in an organisation and the ways through which it enhances the cost

reporting structure. The significant outcomes obtained after evaluation are recommended

to the Australian management accountants so that they could improve the management

accounting procedures in place.

Executive Summary:

The goal of this report is to evaluate the implications of the activity-based costing system

from the viewpoint of the business organisations. For effective evaluation of the topic, the

report has considered selecting two journal articles on different organisations belonging to

different industries. The two journal articles include the application of the activity-based

costing system in an organisation and the ways through which it enhances the cost

reporting structure. The significant outcomes obtained after evaluation are recommended

to the Australian management accountants so that they could improve the management

accounting procedures in place.

2MANAGERIAL ACCOUNTING

Table of Contents

Introduction:..............................................................................................................................3

a. Explanation of activity-based costing (ABC) system:.............................................................3

b. Purpose of the two studies and research questions set out for topic exploration:..............4

c. Similarities and differences in the findings of the two studies:.............................................9

d. Four specific outcomes useful for the Australian management accountants:....................10

Conclusion:...............................................................................................................................13

References:...............................................................................................................................14

Table of Contents

Introduction:..............................................................................................................................3

a. Explanation of activity-based costing (ABC) system:.............................................................3

b. Purpose of the two studies and research questions set out for topic exploration:..............4

c. Similarities and differences in the findings of the two studies:.............................................9

d. Four specific outcomes useful for the Australian management accountants:....................10

Conclusion:...............................................................................................................................13

References:...............................................................................................................................14

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3MANAGERIAL ACCOUNTING

Introduction:

With the increasing speed of globalisation, all business organisations are focused

towards raising their profits. Under such condition, when there is increase in sales revenue,

the variable costs tend to rise as well. Hence, this has mandated the need for the

organisations to select a suitable costing method having the ability of recording and

analysing the business costs (Chenhall and Moers 2015). In the current modernisation era,

many business organisations are using activity-based costing (ABC) system in order to

identify and allocate costs. This is because the traditional costing systems fail to assist the

organisations to cope up with the varying business environment. As a result, ABC system has

evolved over time to assist the organisations in overcoming the loopholes inherent in

traditional costing system so that effective business decisions could be undertaken.

ABC system enables the organisations in allocating indirect business costs effectively

based on the activities for manufacturing the various products. ABC system could be applied

to organisations involved in manufacturing various products (Christ and Burritt 2015).

Moreover, the system helps the management of an organisation in identifying the costs and

its related activities and accordingly, allocation could be made. The working procedure of

the ABC system is distinctive in nature compared to traditional costing systems, as it takes

into account machine hours as the base for cost allocation of the organisations. In this

system, the nature of the activity is taken into account and then the organisation identifies

the respective cost unit.

Introduction:

With the increasing speed of globalisation, all business organisations are focused

towards raising their profits. Under such condition, when there is increase in sales revenue,

the variable costs tend to rise as well. Hence, this has mandated the need for the

organisations to select a suitable costing method having the ability of recording and

analysing the business costs (Chenhall and Moers 2015). In the current modernisation era,

many business organisations are using activity-based costing (ABC) system in order to

identify and allocate costs. This is because the traditional costing systems fail to assist the

organisations to cope up with the varying business environment. As a result, ABC system has

evolved over time to assist the organisations in overcoming the loopholes inherent in

traditional costing system so that effective business decisions could be undertaken.

ABC system enables the organisations in allocating indirect business costs effectively

based on the activities for manufacturing the various products. ABC system could be applied

to organisations involved in manufacturing various products (Christ and Burritt 2015).

Moreover, the system helps the management of an organisation in identifying the costs and

its related activities and accordingly, allocation could be made. The working procedure of

the ABC system is distinctive in nature compared to traditional costing systems, as it takes

into account machine hours as the base for cost allocation of the organisations. In this

system, the nature of the activity is taken into account and then the organisation identifies

the respective cost unit.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4MANAGERIAL ACCOUNTING

a. Explanation of activity-based costing (ABC) system:

ABC system is an effective method of cost allocation to various cost drivers of the

organisations, which would help in effective decision-making. The role of the ABC system is

significant in setting the selling prices of the products, which are manufactured by the

organisations. More precisely, in this system, the costs incurred are categorised based on

short-term costs as well as long-term costs (Cooper, Ezzamel and Qu 2017). The short-term

business costs are allocated basically based on the volume-related business cost drivers. For

instance, few volume-related cost drivers include labour hours, machine hours and costs of

direct materials. For long-term variable costs, the initial step is to detect and assess the

nature of costs and their activities incurring the costs (Cooper 2017).

The objectives of the ABC system in a business environment are described briefly as

follows:

ABC system intends to rectify the deficiencies of the traditional costing method,

which is associated with record of business cost (Hopper and Bui 2016).

This system has the objective of enhancing cost allocation, which could be associated

by relating the costs incurred by the organisation to its respective activities.

The system concentrates on assisting the management of an organisation to

undertake decisions appropriately about the business costs and decide the selling

prices of the products (Dale and Plunkett 2017).

ABC system leads to more suitable cost disclosures of the organisations and

therefore, the cost structure could be improved further.

a. Explanation of activity-based costing (ABC) system:

ABC system is an effective method of cost allocation to various cost drivers of the

organisations, which would help in effective decision-making. The role of the ABC system is

significant in setting the selling prices of the products, which are manufactured by the

organisations. More precisely, in this system, the costs incurred are categorised based on

short-term costs as well as long-term costs (Cooper, Ezzamel and Qu 2017). The short-term

business costs are allocated basically based on the volume-related business cost drivers. For

instance, few volume-related cost drivers include labour hours, machine hours and costs of

direct materials. For long-term variable costs, the initial step is to detect and assess the

nature of costs and their activities incurring the costs (Cooper 2017).

The objectives of the ABC system in a business environment are described briefly as

follows:

ABC system intends to rectify the deficiencies of the traditional costing method,

which is associated with record of business cost (Hopper and Bui 2016).

This system has the objective of enhancing cost allocation, which could be associated

by relating the costs incurred by the organisation to its respective activities.

The system concentrates on assisting the management of an organisation to

undertake decisions appropriately about the business costs and decide the selling

prices of the products (Dale and Plunkett 2017).

ABC system leads to more suitable cost disclosures of the organisations and

therefore, the cost structure could be improved further.

5MANAGERIAL ACCOUNTING

b. Purpose of the two studies and research questions set out for topic exploration:

For effective evaluation of the ABC system, various research articles have been taken

into consideration. Two articles are selected, which would assist in further explanation of

the application and benefits of the system in an organisation. The articles selected are listed

as follows:

Article 1: “Activity based costing (ABC) in the public sector: Benefits and challenges”

Article 2: “Activity Based Costing in Services Industry: A Conceptual Framework for

Entrepreneurs”

The above two journals are focused on organisations functioning in different

industries. These articles highlight and provide meaningful insights into the ABC system

Analysis of Article 1:

This journal article aims to show the difference between the traditional costing

system and the ABC system at the time of application in business organisations. Moreover, it

highlights the benefits related to the ABC system. Furthermore, the article reflects the

implementation of the ABC system in a public sector organisation.

As per the research paper, the problem statement reveals the opinion of numerous

academicians and researchers, in which they stated that the ABC system is useful in business

organisations, which have large size and big operating scales or those organisations offering

multiple products and services to the customers. However, Oseifuah (2014) cited that the

ABC system is used more extensively than the initial portrayal. This research aims to

consider a public listed organisation involved in offering services to the general public. These

b. Purpose of the two studies and research questions set out for topic exploration:

For effective evaluation of the ABC system, various research articles have been taken

into consideration. Two articles are selected, which would assist in further explanation of

the application and benefits of the system in an organisation. The articles selected are listed

as follows:

Article 1: “Activity based costing (ABC) in the public sector: Benefits and challenges”

Article 2: “Activity Based Costing in Services Industry: A Conceptual Framework for

Entrepreneurs”

The above two journals are focused on organisations functioning in different

industries. These articles highlight and provide meaningful insights into the ABC system

Analysis of Article 1:

This journal article aims to show the difference between the traditional costing

system and the ABC system at the time of application in business organisations. Moreover, it

highlights the benefits related to the ABC system. Furthermore, the article reflects the

implementation of the ABC system in a public sector organisation.

As per the research paper, the problem statement reveals the opinion of numerous

academicians and researchers, in which they stated that the ABC system is useful in business

organisations, which have large size and big operating scales or those organisations offering

multiple products and services to the customers. However, Oseifuah (2014) cited that the

ABC system is used more extensively than the initial portrayal. This research aims to

consider a public listed organisation involved in offering services to the general public. These

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6MANAGERIAL ACCOUNTING

services are classified as overhead intensive and hence, the researcher believes that the ABC

system is the best alternative for the sector.

According to the researcher, the implementation of ABC system would result in

accountability and transparency of the organisation. The research is carried out by taking

into account the public listed organisations having operations in South Africa and they are

considered to be one of the essential backbones to service delivery in the nation. Therefore,

the research intends to analyse the ways through which the implementation of ABC system

could be enforced effectively in the public organisations operating in South Africa.

This journal paper describes the traditional costing method and the ways through

which it could be applied in organisations. The traditional costing system is implemented

and developed in organisations, which has either process costing or job costing method in

place. The costs are apportioned and they are segregated based on products, which have

direct costs and based on period having indirect expenses. The cost allocation is conducted

based on the volume cost drivers, which might be the machine hours (Eldenburg

et al.

2016). Moreover, the article sheds light on identifying the loopholes inherent in the

traditional costing method.

services are classified as overhead intensive and hence, the researcher believes that the ABC

system is the best alternative for the sector.

According to the researcher, the implementation of ABC system would result in

accountability and transparency of the organisation. The research is carried out by taking

into account the public listed organisations having operations in South Africa and they are

considered to be one of the essential backbones to service delivery in the nation. Therefore,

the research intends to analyse the ways through which the implementation of ABC system

could be enforced effectively in the public organisations operating in South Africa.

This journal paper describes the traditional costing method and the ways through

which it could be applied in organisations. The traditional costing system is implemented

and developed in organisations, which has either process costing or job costing method in

place. The costs are apportioned and they are segregated based on products, which have

direct costs and based on period having indirect expenses. The cost allocation is conducted

based on the volume cost drivers, which might be the machine hours (Eldenburg

et al.

2016). Moreover, the article sheds light on identifying the loopholes inherent in the

traditional costing method.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7MANAGERIAL ACCOUNTING

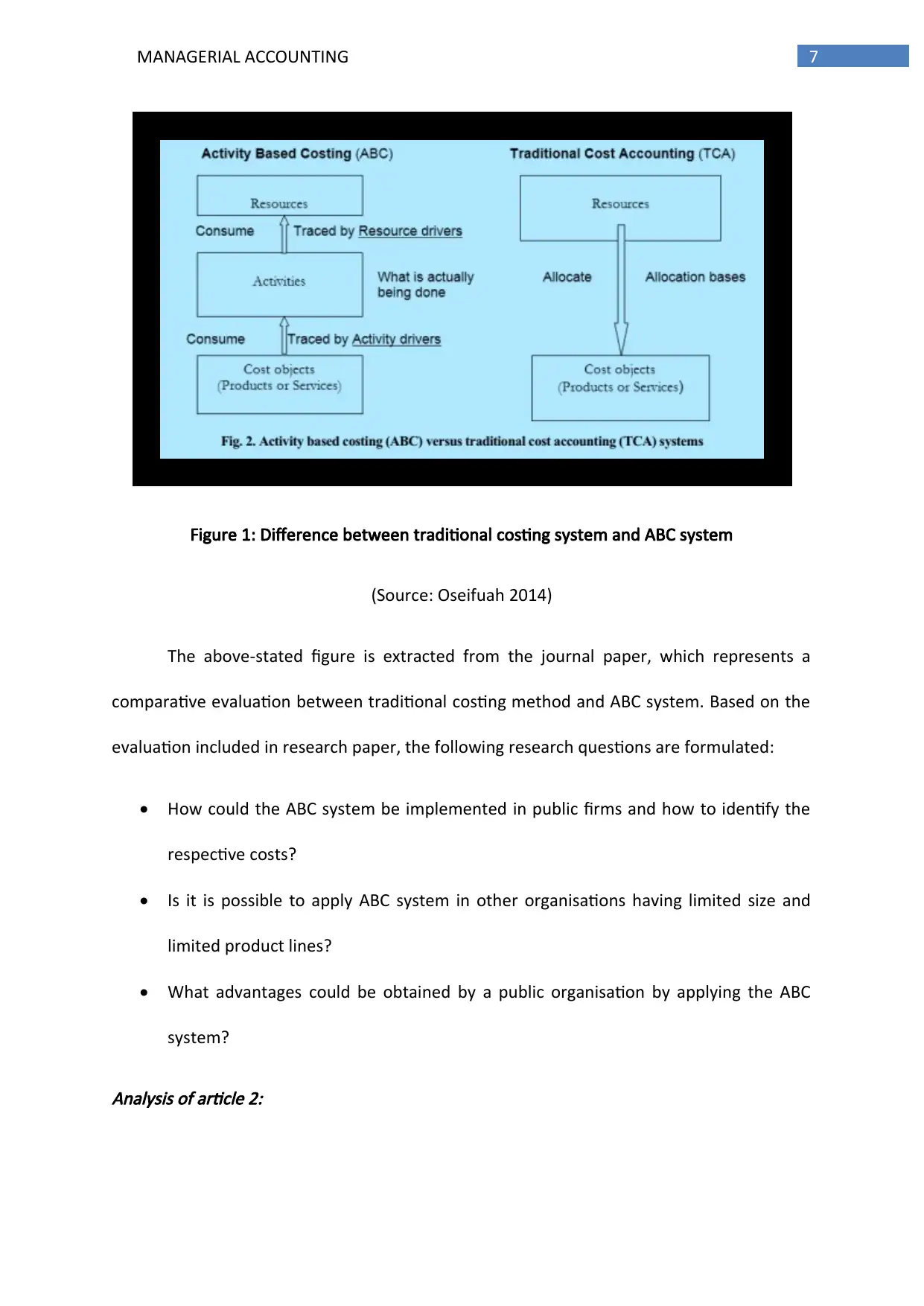

Figure 1: Difference between traditional costing system and ABC system

(Source: Oseifuah 2014)

The above-stated figure is extracted from the journal paper, which represents a

comparative evaluation between traditional costing method and ABC system. Based on the

evaluation included in research paper, the following research questions are formulated:

How could the ABC system be implemented in public firms and how to identify the

respective costs?

Is it is possible to apply ABC system in other organisations having limited size and

limited product lines?

What advantages could be obtained by a public organisation by applying the ABC

system?

Analysis of article 2:

Figure 1: Difference between traditional costing system and ABC system

(Source: Oseifuah 2014)

The above-stated figure is extracted from the journal paper, which represents a

comparative evaluation between traditional costing method and ABC system. Based on the

evaluation included in research paper, the following research questions are formulated:

How could the ABC system be implemented in public firms and how to identify the

respective costs?

Is it is possible to apply ABC system in other organisations having limited size and

limited product lines?

What advantages could be obtained by a public organisation by applying the ABC

system?

Analysis of article 2:

8MANAGERIAL ACCOUNTING

According to this paper, the researchers have focused on service sector. It has been

observed that both manufacturing and service organisations have managed to attain growth

in the current periods. The researchers have detected that in the varying environment, the

overall rise in operating scale leads to massive hike in costs related to business operations.

Majority of the business organisations encounter problems to handle the profit levels and

business costs (Frazier 2014). Hence, it has become necessary for the organisations to

choose an effective system of cost management, which could reflect the costs incurred

during the year correctly and appropriately.

The article sheds light on the different costing systems, which are utilised in a

business environment and the ways through which they could be reported. Based on such

reporting, the organisations could undertake suitable decisions. The paper critically explains

the ABC system and the significant steps that the organisations follow to identify the cost

elements and main cost drivers. Moreover, this paper would reveal the ways through which

the ABC system and traditional costing system do not resemble each other (Onat, Anitsal

and Anitsal 2014). Certain loopholes are inherent in traditional costing system, which

include inability to consider non-financial factors impacting business operations and

incorrect cost information. Therefore, this paper sets out the fact that traditional costing

system is unsuitable for any organisation involved in the service sector. This automatically

leads to the opinion of adopting the ABC system for effective cost treatment in the context

of the service sector organisations. The researchers have discussed a number of benefits

associated with the implementation of the ABC system in service organisations. This is

because the system provides accurate depiction of business costs, cost minimisations,

According to this paper, the researchers have focused on service sector. It has been

observed that both manufacturing and service organisations have managed to attain growth

in the current periods. The researchers have detected that in the varying environment, the

overall rise in operating scale leads to massive hike in costs related to business operations.

Majority of the business organisations encounter problems to handle the profit levels and

business costs (Frazier 2014). Hence, it has become necessary for the organisations to

choose an effective system of cost management, which could reflect the costs incurred

during the year correctly and appropriately.

The article sheds light on the different costing systems, which are utilised in a

business environment and the ways through which they could be reported. Based on such

reporting, the organisations could undertake suitable decisions. The paper critically explains

the ABC system and the significant steps that the organisations follow to identify the cost

elements and main cost drivers. Moreover, this paper would reveal the ways through which

the ABC system and traditional costing system do not resemble each other (Onat, Anitsal

and Anitsal 2014). Certain loopholes are inherent in traditional costing system, which

include inability to consider non-financial factors impacting business operations and

incorrect cost information. Therefore, this paper sets out the fact that traditional costing

system is unsuitable for any organisation involved in the service sector. This automatically

leads to the opinion of adopting the ABC system for effective cost treatment in the context

of the service sector organisations. The researchers have discussed a number of benefits

associated with the implementation of the ABC system in service organisations. This is

because the system provides accurate depiction of business costs, cost minimisations,

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9MANAGERIAL ACCOUNTING

enhances product costing and assists in decision-making procedure of the organisations

(Fullerton, Kennedy and Widener 2014).

Hence, the above discussion reflects the merits of the ABC system effectively

compared to traditional costing method. The researchers have explicitly mentioned the

benefits of the ABC system along with the reasons of implementing the same within the

service sector organisations. The evaluation depicts the application of the ABC system from

the business context. Therefore, the following research questions are framed based on the

evaluation of the research paper:

What contributions do the ABC systems make in undertaking useful decisions?

What are the differences between an organisation using traditional costing system

and one using the ABC system?

What cost drivers are necessary for the service sector organisations?

c. Similarities and differences in the findings of the two studies:

After critical evaluation of the two studies, certain similarities and differences are

inherent between them and they are described as follows:

Similarities:

Both the research papers have focused on applying the ABC system in different

industries and the ways through which it could fetch enhancements in their

reporting framework. It has been analysed that the system would result in

improvements and correct projections in relation to different types of costs

(Langfield-Smith

et al. 2017).

enhances product costing and assists in decision-making procedure of the organisations

(Fullerton, Kennedy and Widener 2014).

Hence, the above discussion reflects the merits of the ABC system effectively

compared to traditional costing method. The researchers have explicitly mentioned the

benefits of the ABC system along with the reasons of implementing the same within the

service sector organisations. The evaluation depicts the application of the ABC system from

the business context. Therefore, the following research questions are framed based on the

evaluation of the research paper:

What contributions do the ABC systems make in undertaking useful decisions?

What are the differences between an organisation using traditional costing system

and one using the ABC system?

What cost drivers are necessary for the service sector organisations?

c. Similarities and differences in the findings of the two studies:

After critical evaluation of the two studies, certain similarities and differences are

inherent between them and they are described as follows:

Similarities:

Both the research papers have focused on applying the ABC system in different

industries and the ways through which it could fetch enhancements in their

reporting framework. It has been analysed that the system would result in

improvements and correct projections in relation to different types of costs

(Langfield-Smith

et al. 2017).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10MANAGERIAL ACCOUNTING

Both the articles have focused on identifying the loopholes present in the traditional

costing system and the ways through which the ABC system could be applied for

eliminating these loopholes. Moreover, these articles have discussed the major

differences between the ABC system and traditional costing system, as the former is

deemed to provide certain business improvements.

The benefits of the ABC system as a costing method are mentioned in both the

research papers. Both papers have been focused on boosting the analysis with the

advantages related to the ABC system.

Dissimilarities:

After evaluation of the two research papers, it is apparent that the organisations

selected belong to different business sectors. This is identified as the major

difference between the two papers, since the business structure and the cost items

would be different for the organisations operating in different industrial sectors

(Lavia López and Hiebl 2014). In the first article, public sector organisations are

provided with utmost priority. On the other hand, the service sector organisations

are emphasised in the second article.

The organisations considered in both the articles are involved in providing diversified

services and moreover, the nations where the organisations operate are not same.

Instead, the organisations selected in the research papers belong to different

nations.

Both the articles have focused on identifying the loopholes present in the traditional

costing system and the ways through which the ABC system could be applied for

eliminating these loopholes. Moreover, these articles have discussed the major

differences between the ABC system and traditional costing system, as the former is

deemed to provide certain business improvements.

The benefits of the ABC system as a costing method are mentioned in both the

research papers. Both papers have been focused on boosting the analysis with the

advantages related to the ABC system.

Dissimilarities:

After evaluation of the two research papers, it is apparent that the organisations

selected belong to different business sectors. This is identified as the major

difference between the two papers, since the business structure and the cost items

would be different for the organisations operating in different industrial sectors

(Lavia López and Hiebl 2014). In the first article, public sector organisations are

provided with utmost priority. On the other hand, the service sector organisations

are emphasised in the second article.

The organisations considered in both the articles are involved in providing diversified

services and moreover, the nations where the organisations operate are not same.

Instead, the organisations selected in the research papers belong to different

nations.

11MANAGERIAL ACCOUNTING

d. Four specific outcomes useful for the Australian management accountants:

The assessment of the two journal articles constructed above effectively depicts the

benefits of the ABC system in business organisations. Certain positive outcomes are learnt

from the analysis of the two papers, which could be advised to the management

accountants working in the Australian organisations. Such knowledge would help them in

making significant improvements in the business structures of their organisations (Messner

2016). The four specific outcomes learned from the research papers, which are deemed to

be valuable for the Australian management accountants are enumerated as follows:

Advantages of the ABC system over the traditional costing system:

It has been identified that there are numerous Australian organisations that follow

traditional costing system for cost allocation (Mitra 2016). This requires revision and the

system needs to be substituted with the ABC system. The reason is that the ABC system

could result in useful changes in the reporting framework followed by the Australian

organisations (Noreen, Brewer and Garrison 2014). Hence, the organisations having

business operations in Australia with large operational scales and multiple product lines are

advised to adopt the ABC system for better cost allocation. Moreover, it is estimated that

the adoption of this system could lead to improved reporting for all types of costs incurred

by the business organisations (Otley 2016). Along with this, the papers evaluated highlight

the deficiencies evident in the traditional costing system and the ways through which the

implementation of the ABC system would help in dealing with those deficiencies.

Furthermore, the assessment has identified few other issues related to the traditional

costing system and hence, this mandates the need of replacing the same with the popular

ABC system.

d. Four specific outcomes useful for the Australian management accountants:

The assessment of the two journal articles constructed above effectively depicts the

benefits of the ABC system in business organisations. Certain positive outcomes are learnt

from the analysis of the two papers, which could be advised to the management

accountants working in the Australian organisations. Such knowledge would help them in

making significant improvements in the business structures of their organisations (Messner

2016). The four specific outcomes learned from the research papers, which are deemed to

be valuable for the Australian management accountants are enumerated as follows:

Advantages of the ABC system over the traditional costing system:

It has been identified that there are numerous Australian organisations that follow

traditional costing system for cost allocation (Mitra 2016). This requires revision and the

system needs to be substituted with the ABC system. The reason is that the ABC system

could result in useful changes in the reporting framework followed by the Australian

organisations (Noreen, Brewer and Garrison 2014). Hence, the organisations having

business operations in Australia with large operational scales and multiple product lines are

advised to adopt the ABC system for better cost allocation. Moreover, it is estimated that

the adoption of this system could lead to improved reporting for all types of costs incurred

by the business organisations (Otley 2016). Along with this, the papers evaluated highlight

the deficiencies evident in the traditional costing system and the ways through which the

implementation of the ABC system would help in dealing with those deficiencies.

Furthermore, the assessment has identified few other issues related to the traditional

costing system and hence, this mandates the need of replacing the same with the popular

ABC system.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.