Managerial Accounting: Financial Analysis & Floppy Disc Inc. Report

VerifiedAdded on 2023/06/08

|11

|1403

|496

Report

AI Summary

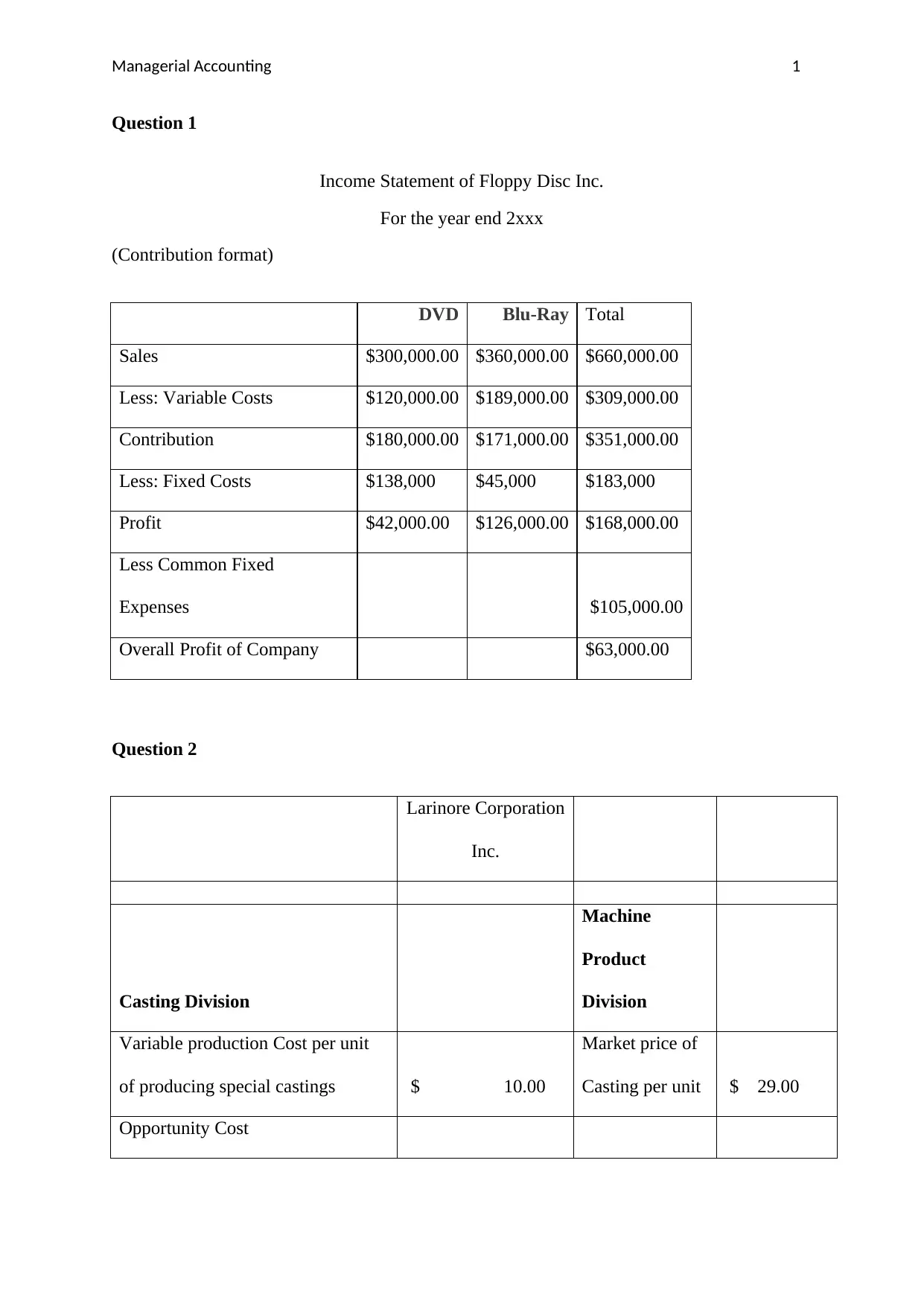

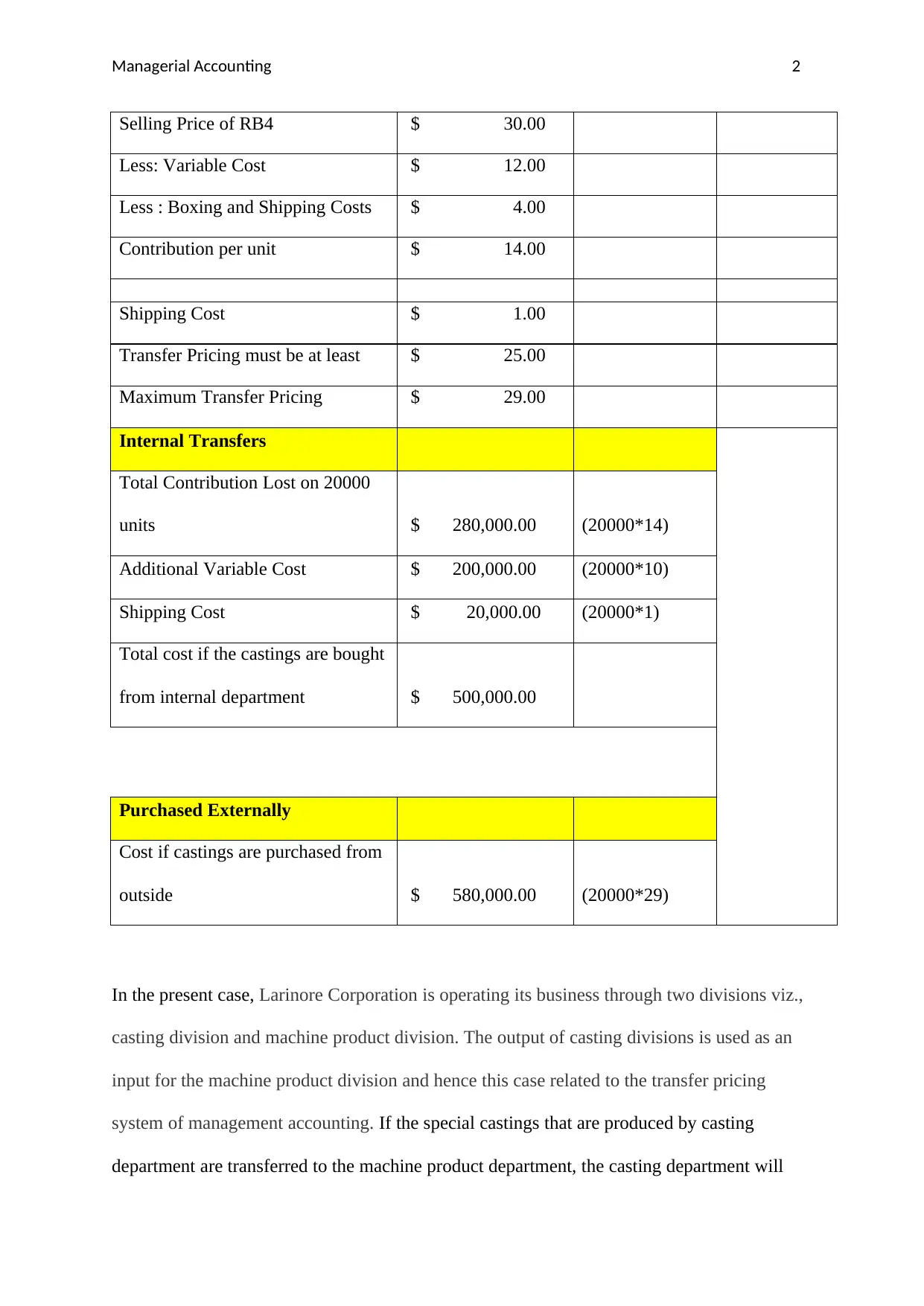

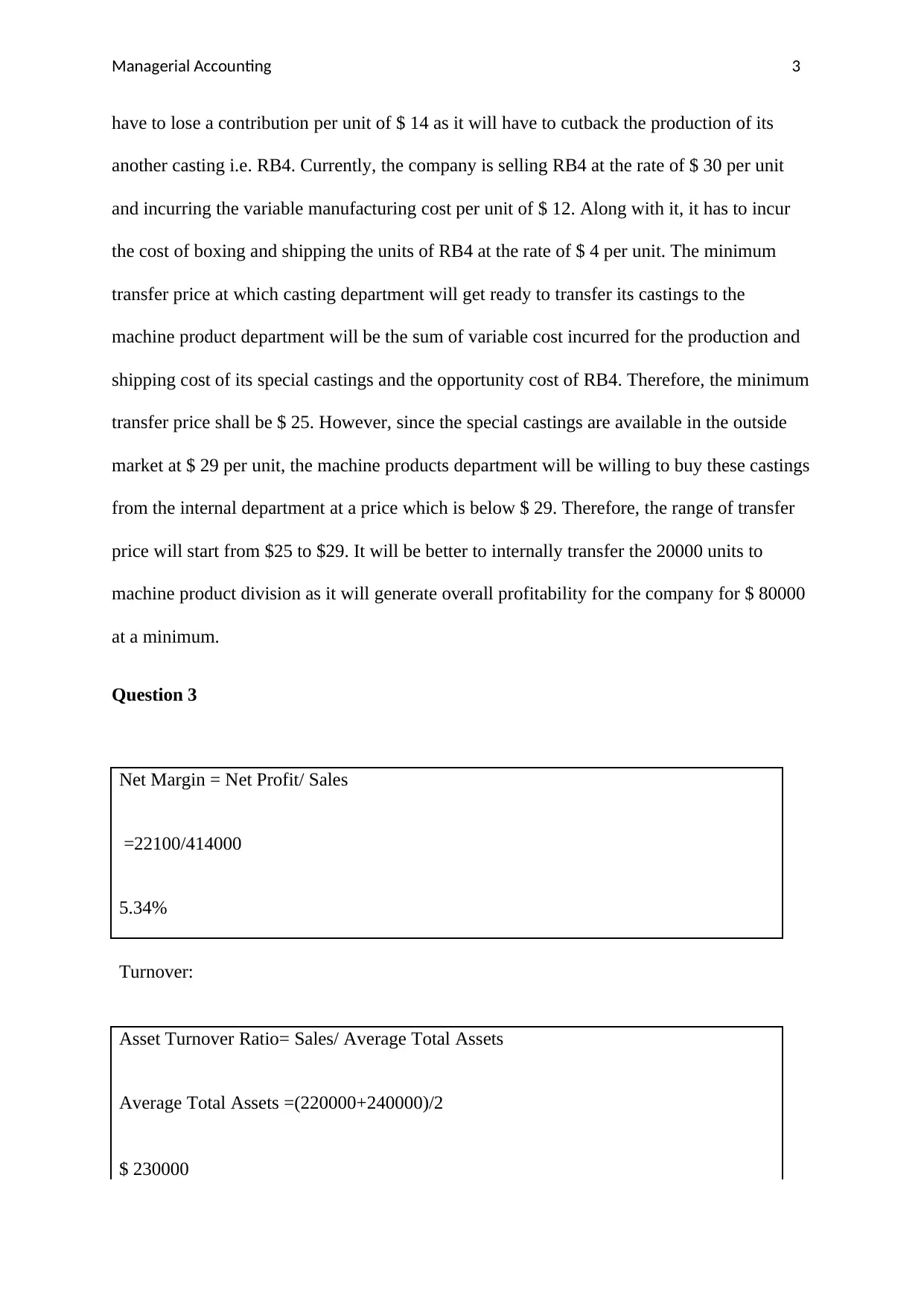

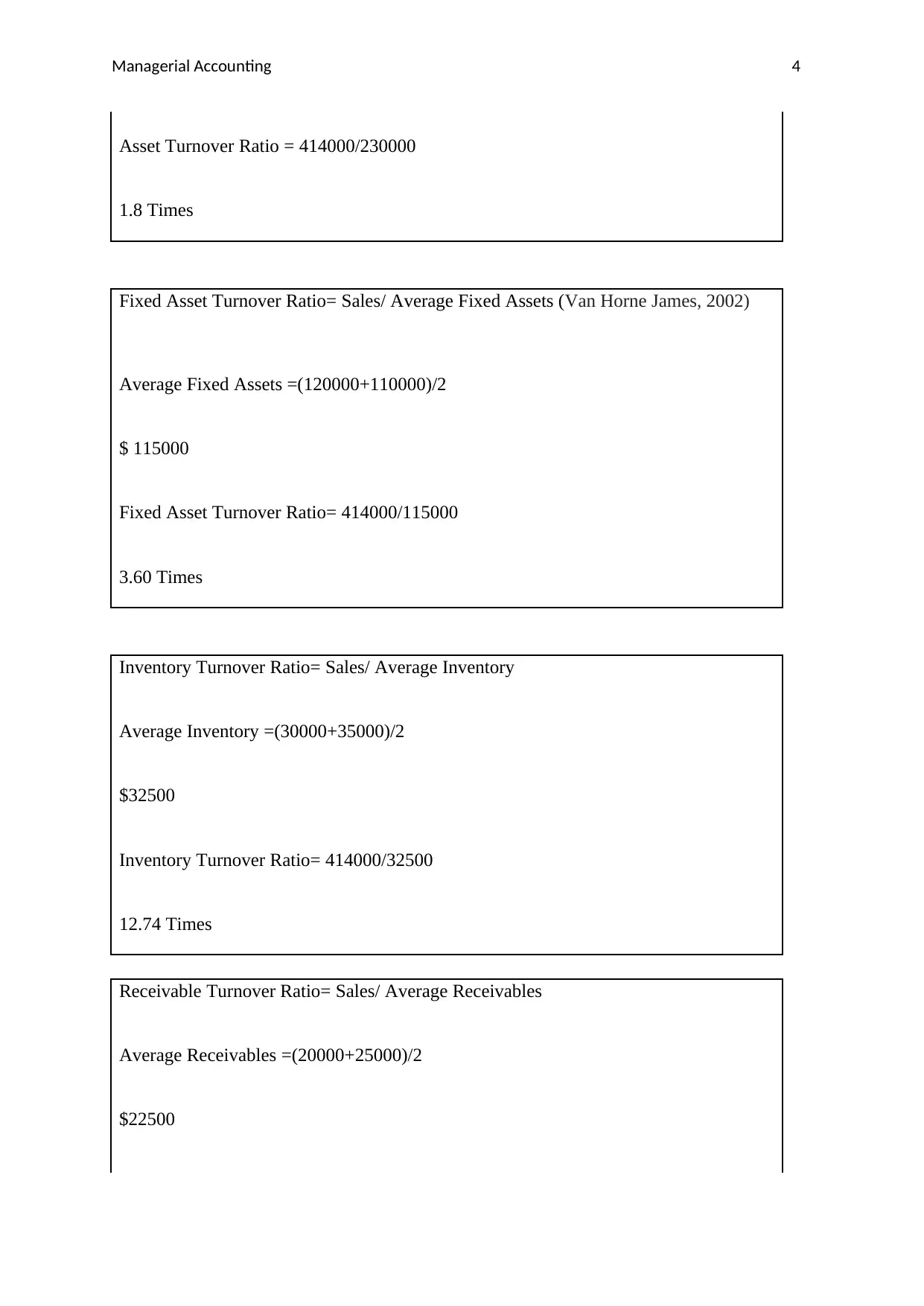

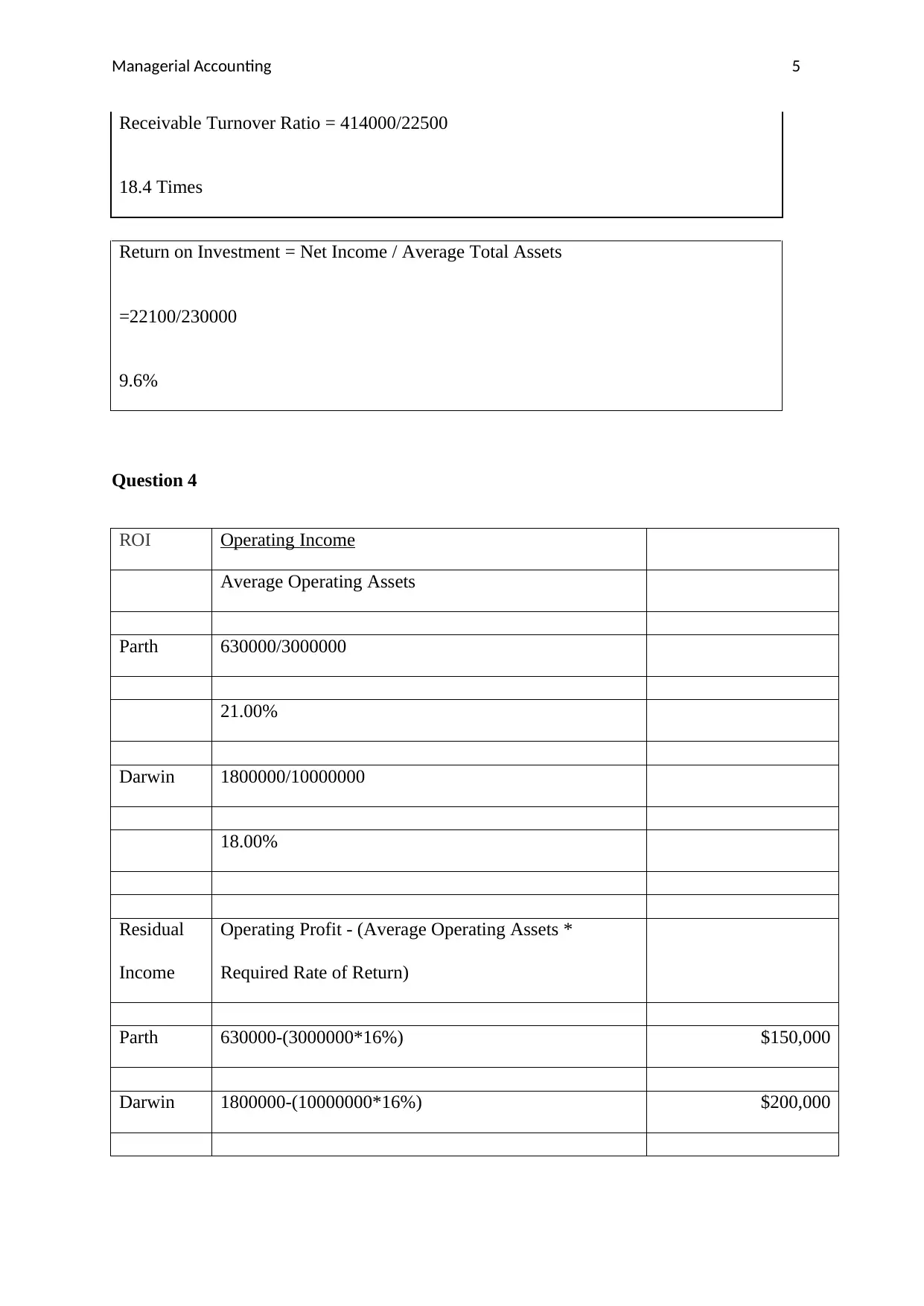

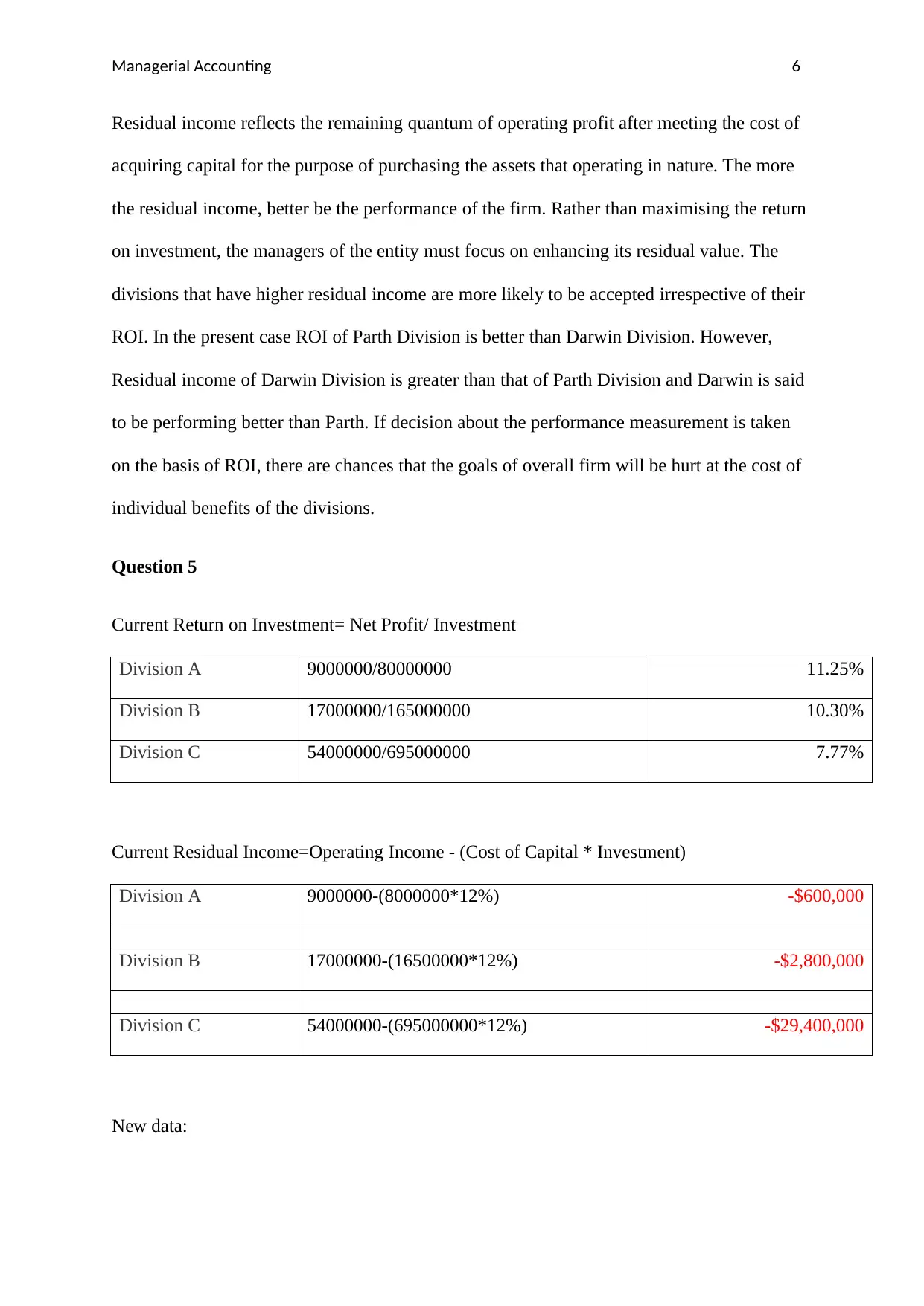

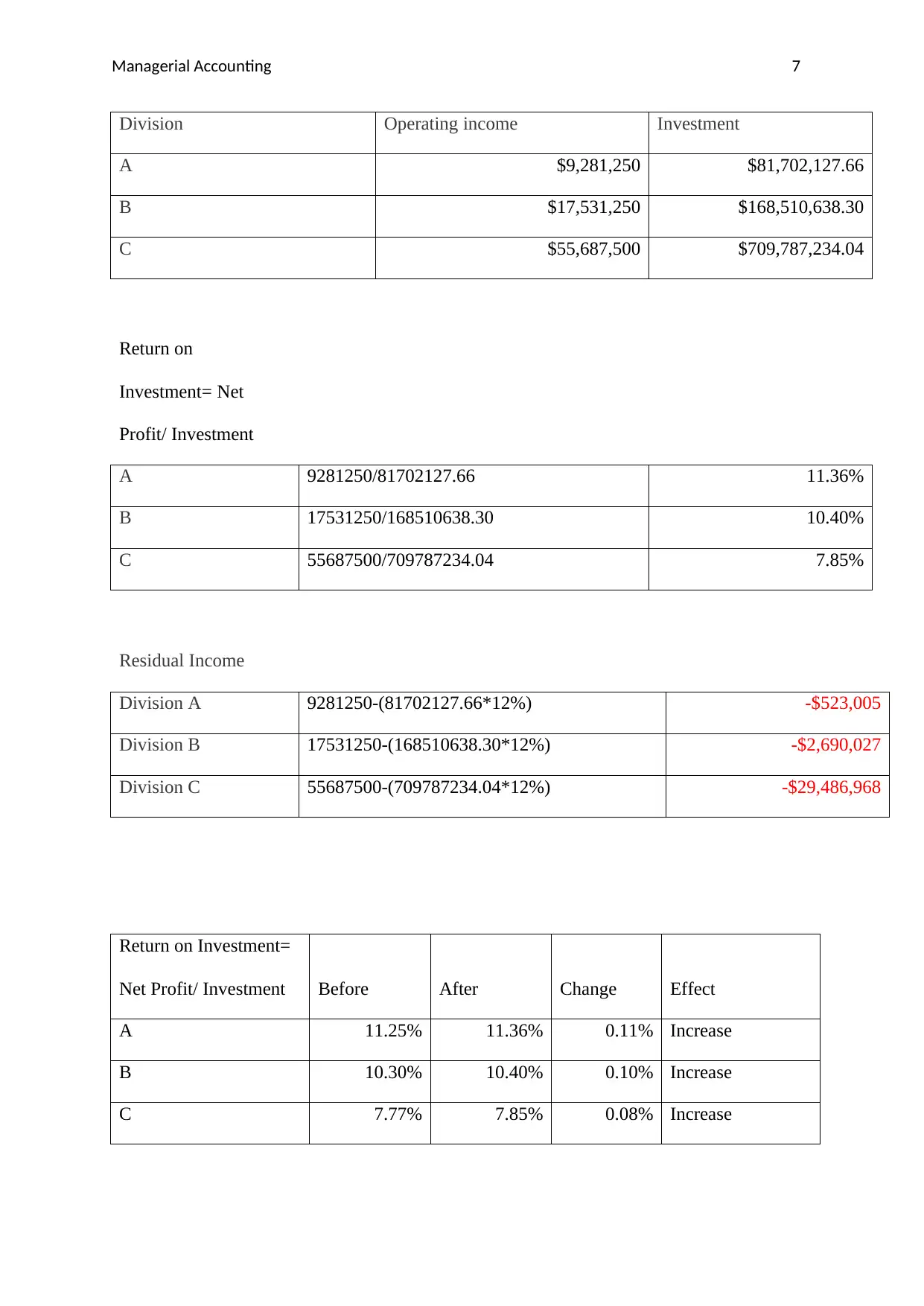

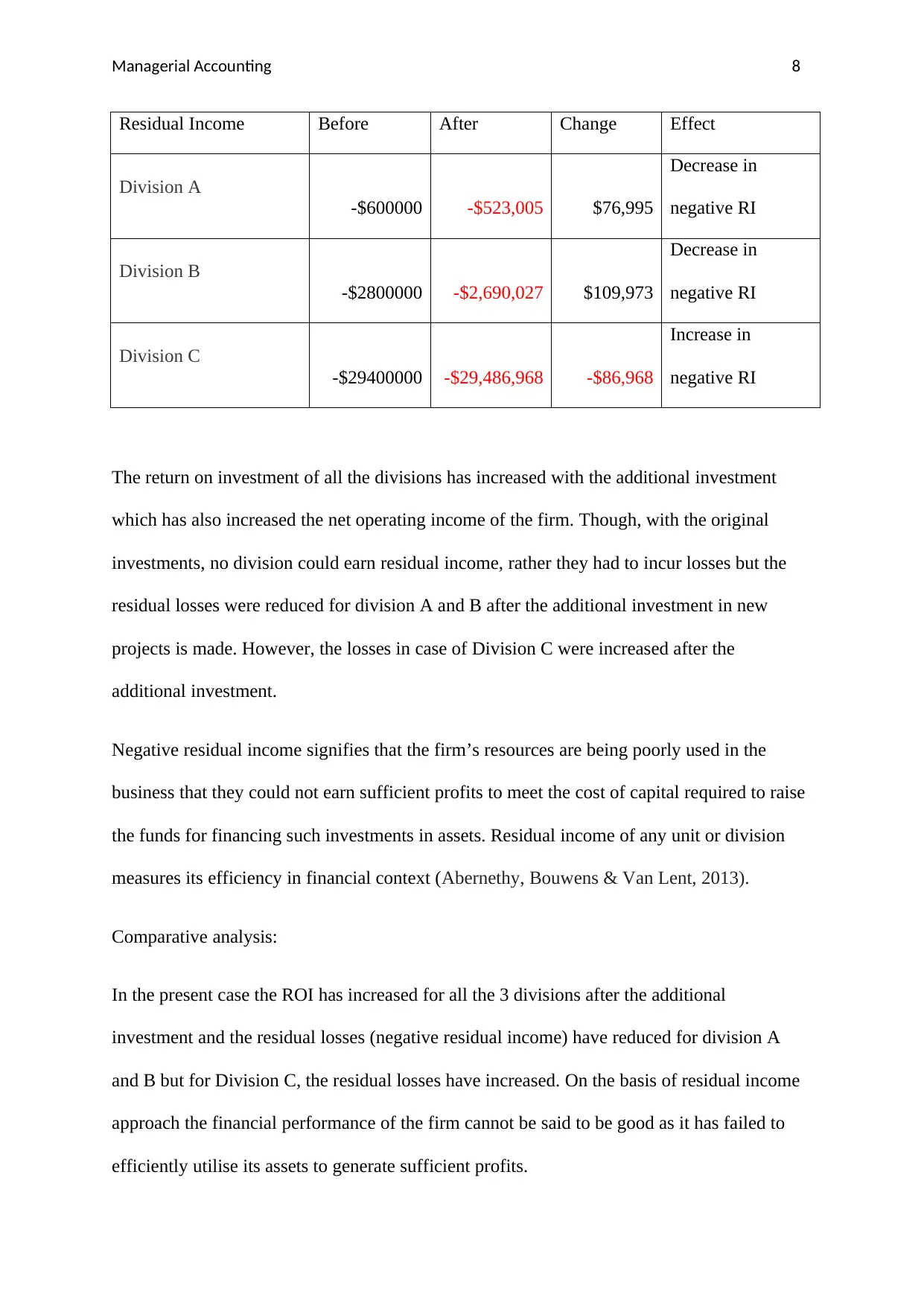

This document presents a detailed solution to a managerial accounting assignment, encompassing several key areas of financial analysis. It includes an income statement for Floppy Disc Inc., segmented by product lines (DVD and Blu-Ray), utilizing a contribution format to assess profitability. The assignment also delves into transfer pricing strategies within Larinore Corporation, evaluating the optimal transfer price between its Casting and Machine Products Divisions, considering variable costs, opportunity costs, and external market prices. Furthermore, it calculates and interprets various financial ratios such as net margin, asset turnover, fixed asset turnover, inventory turnover, receivable turnover, and return on investment (ROI) for a given company. The report extends to performance evaluation using ROI and residual income, comparing the performance of different divisions (Parth and Darwin) and analyzing the impact of additional investments on divisional performance, highlighting the importance of efficient asset utilization. Desklib offers a wealth of resources, including similar solved assignments and study tools, to support students in mastering managerial accounting concepts.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.