Managerial Accounting: Evaluating Departmental Financial Performance

VerifiedAdded on 2023/05/28

|9

|2015

|249

Homework Assignment

AI Summary

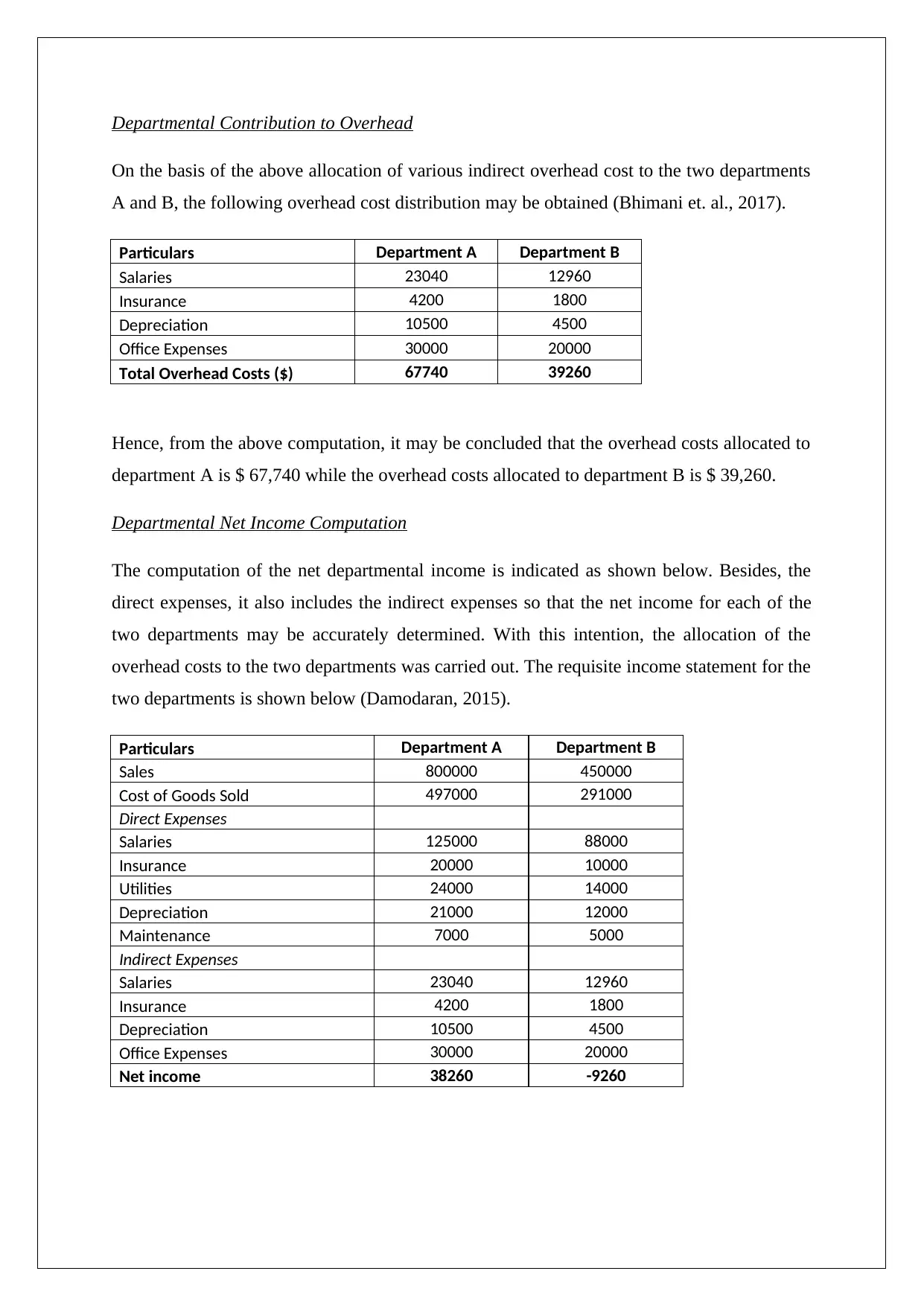

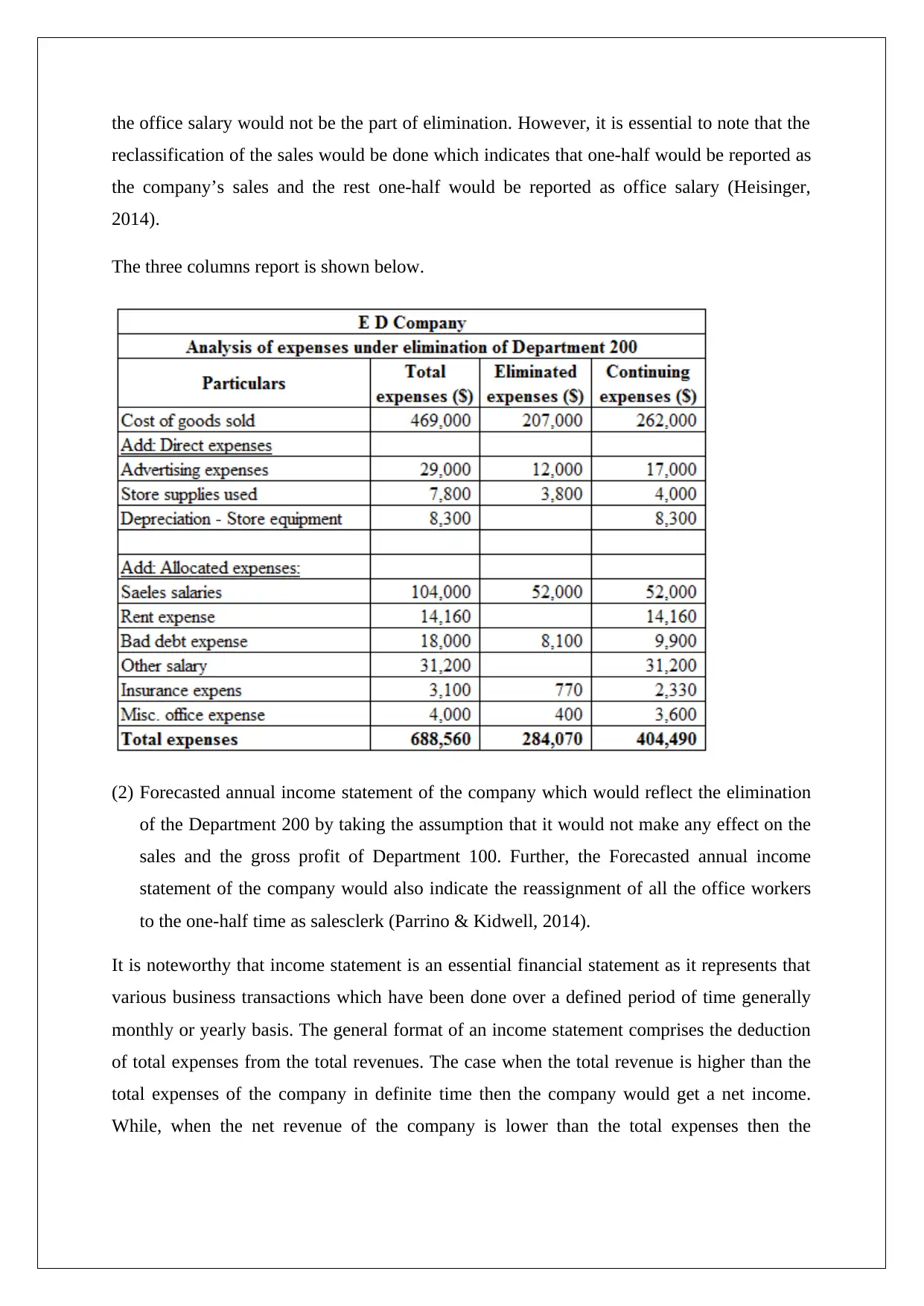

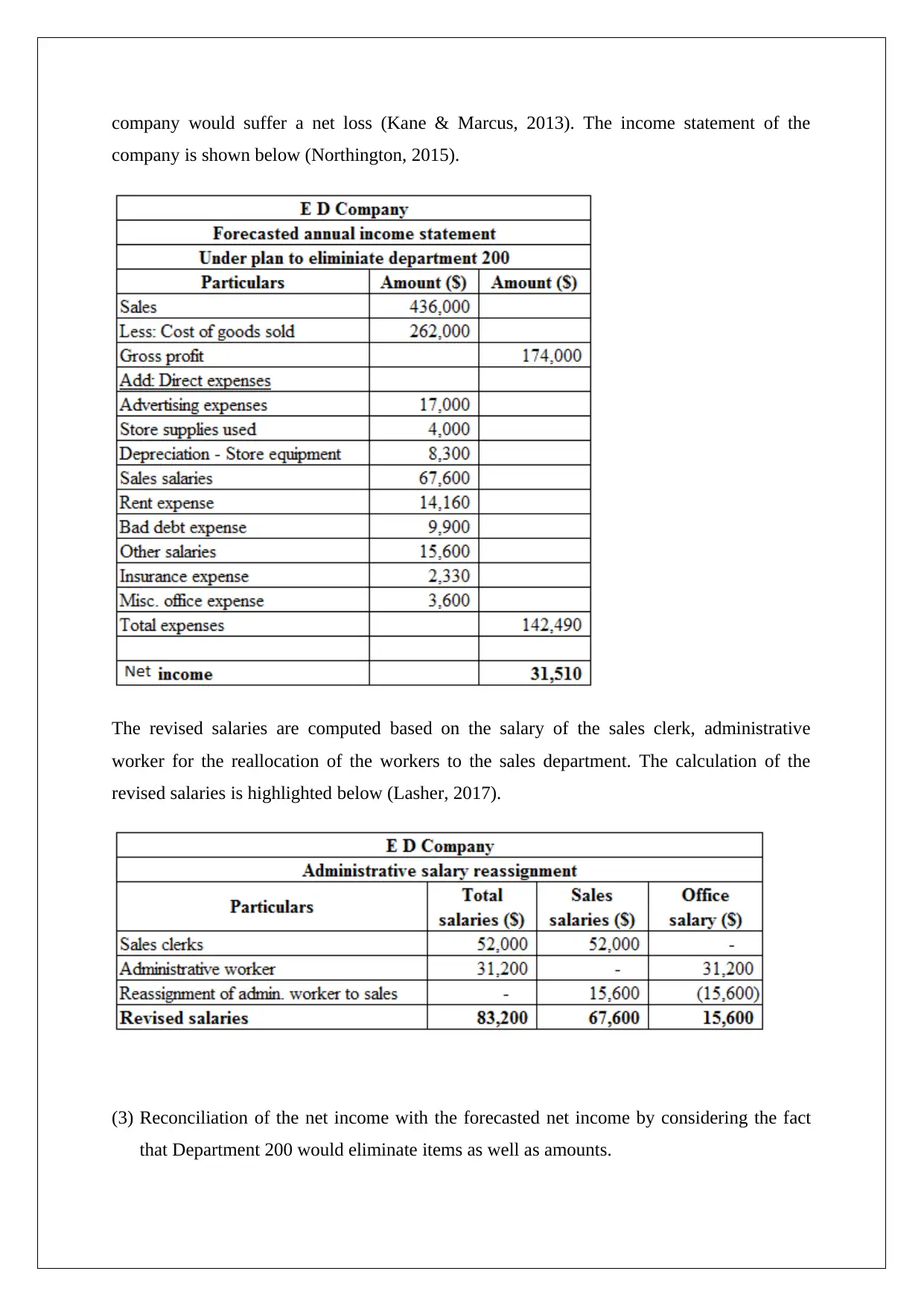

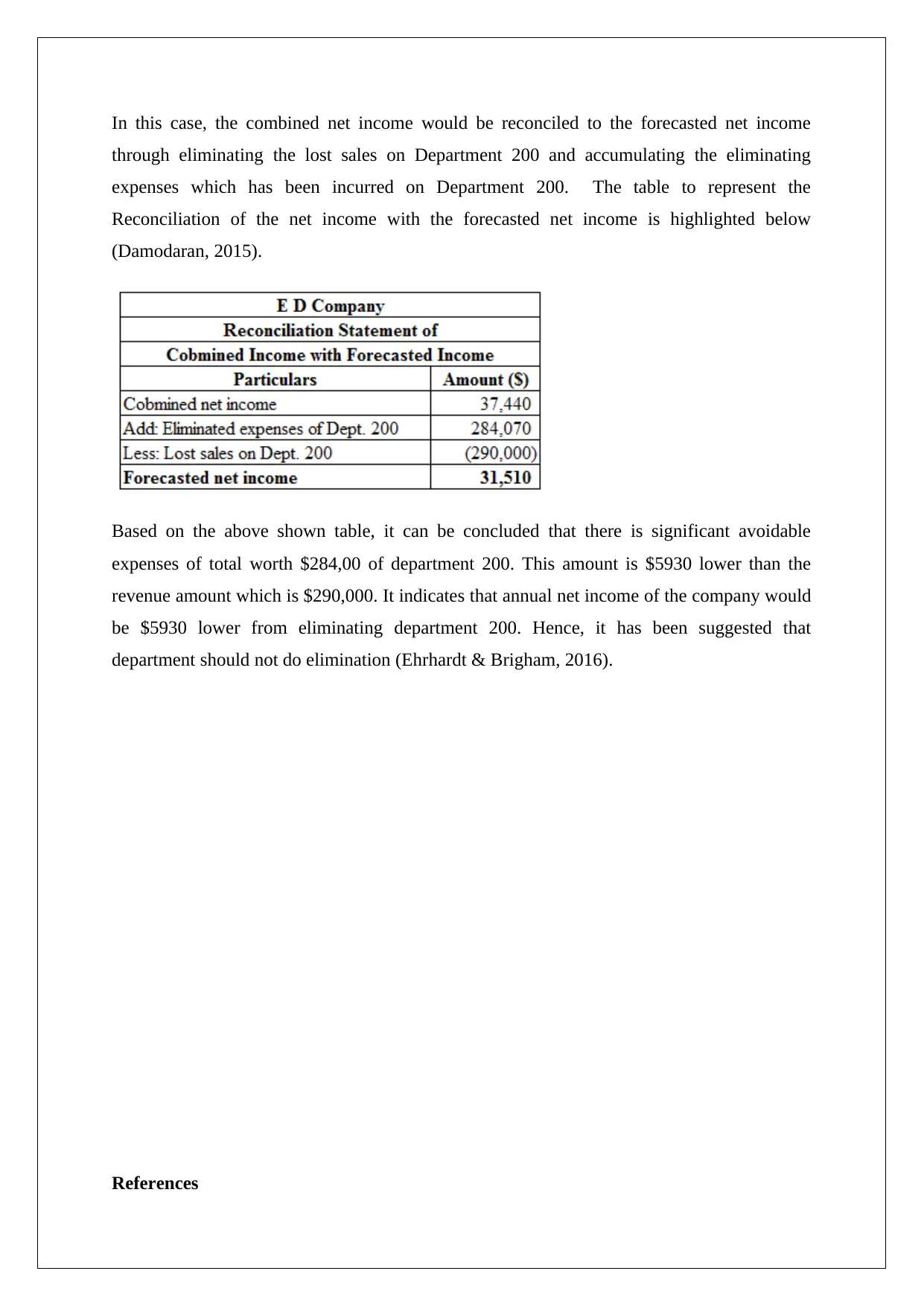

This assignment solution addresses managerial accounting principles through two primary problems. The first problem involves allocating indirect expenses to two departments based on specified criteria, such as sales and square footage, to determine each department's net income and assess profitability. It concludes that while one department shows a net loss, discontinuing it may not be beneficial due to the absorption of indirect expenses. The second problem focuses on a three-column report analyzing expenses, a forecasted income statement reflecting the elimination of a department, and a reconciliation of net income, ultimately advising against the department's elimination due to avoidable expenses exceeding lost revenue. The assignment utilizes various accounting techniques and financial analyses to evaluate departmental performance and inform strategic decisions.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.