Managerial Accounting: Financial Analysis of Angel Seafood Holdings

VerifiedAdded on 2023/04/21

|20

|4415

|121

Report

AI Summary

This report provides a financial performance analysis of Angel Seafood Holdings Limited for 2018, including estimations of future performance and an evaluation of top-down and bottom-up budgeting approaches. It includes a budgeted income statement for 2019 and a comparison with the actual 2018 statement. The report assesses the elements of a master budget and concludes that a top-down approach is more suitable for Angel Seafood Holdings, enabling the firm to develop necessary budgets to support its operations and formulate required income levels.

Running head: MANAGERIAL ACCOUNTING

Managerial Accounting

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Managerial Accounting

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1MANAGERIAL ACCOUNTING

Executive Summary:

The report has emphasised on analysing the financial performance of Angel Seafood Holdings

Limited for the year 2018 along with estimating future performance based on certain

assumptions that could be generated by the organisation. Moreover, there has been further

analysis conducted for evaluation of the bottom-up approach and top-down approach to the

budget process. The income statement budget of Angel Seafood Holdings Limited is computed

mainly for identifying the expected income and expenses in the upcoming year. From the

pertinent analysis of the bottom-up approach and top-down approach, it has been found that

the organisation could formulate the necessary budgets in order to support its business

operations. The elements of the above-stated two approaches are analysed primarily for

identifying the suitable budgeting approach, which could be utilised on the part of Angel

Seafood Holdings Limited. The evaluation of financial performance could be carried out in the

assessment, which would assist in identifying the improvement level to be conducted by the

organisation. Finally, it has been evaluated that the top-down approach would be more suitable

for Angel Seafood Holdings Limited,

Executive Summary:

The report has emphasised on analysing the financial performance of Angel Seafood Holdings

Limited for the year 2018 along with estimating future performance based on certain

assumptions that could be generated by the organisation. Moreover, there has been further

analysis conducted for evaluation of the bottom-up approach and top-down approach to the

budget process. The income statement budget of Angel Seafood Holdings Limited is computed

mainly for identifying the expected income and expenses in the upcoming year. From the

pertinent analysis of the bottom-up approach and top-down approach, it has been found that

the organisation could formulate the necessary budgets in order to support its business

operations. The elements of the above-stated two approaches are analysed primarily for

identifying the suitable budgeting approach, which could be utilised on the part of Angel

Seafood Holdings Limited. The evaluation of financial performance could be carried out in the

assessment, which would assist in identifying the improvement level to be conducted by the

organisation. Finally, it has been evaluated that the top-down approach would be more suitable

for Angel Seafood Holdings Limited,

2MANAGERIAL ACCOUNTING

Table of Contents

Introduction:....................................................................................................................................3

a. Elements of the master budget:..................................................................................................4

b. Top down and bottom up approach to the budget process:......................................................8

c. Budgeted income statement of Angel Seafood Holdings for 2019:..........................................10

d. Comparison of the actual income statement and budgeted income statement:.....................13

Conclusion:....................................................................................................................................15

References:....................................................................................................................................17

Table of Contents

Introduction:....................................................................................................................................3

a. Elements of the master budget:..................................................................................................4

b. Top down and bottom up approach to the budget process:......................................................8

c. Budgeted income statement of Angel Seafood Holdings for 2019:..........................................10

d. Comparison of the actual income statement and budgeted income statement:.....................13

Conclusion:....................................................................................................................................15

References:....................................................................................................................................17

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3MANAGERIAL ACCOUNTING

Introduction:

The report intends to analyse the financial performance of Angel Seafood Holdings

Limited for the year 2018 along with estimating future performance based on certain

assumptions that could be generated by the organisation. Moreover, there has been further

analysis conducted for evaluation of the bottom-up approach and top-down approach to the

budget process. Along with this, the income statement for the year 2019 has been anticipated,

which could assist in ascertaining the future income of the organisation. Considerable

assessment of the elements of master budget is carried out to find out the effects, which could

be conducted on financial performance. The evaluation of the elements of master budget

directly enables the management in identifying the expenses and income, which is projected for

future business operations. By analysing the future estimated income statement, it could assist

in undertaking the measures adapted by the organisation in generating the needed income

level in 2019. Finally, the actual income statement of 2018 has been contrasted with the

projected income statement of 2019 for providing opinion on the changes while developing the

forecasted annual report.

Introduction:

The report intends to analyse the financial performance of Angel Seafood Holdings

Limited for the year 2018 along with estimating future performance based on certain

assumptions that could be generated by the organisation. Moreover, there has been further

analysis conducted for evaluation of the bottom-up approach and top-down approach to the

budget process. Along with this, the income statement for the year 2019 has been anticipated,

which could assist in ascertaining the future income of the organisation. Considerable

assessment of the elements of master budget is carried out to find out the effects, which could

be conducted on financial performance. The evaluation of the elements of master budget

directly enables the management in identifying the expenses and income, which is projected for

future business operations. By analysing the future estimated income statement, it could assist

in undertaking the measures adapted by the organisation in generating the needed income

level in 2019. Finally, the actual income statement of 2018 has been contrasted with the

projected income statement of 2019 for providing opinion on the changes while developing the

forecasted annual report.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4MANAGERIAL ACCOUNTING

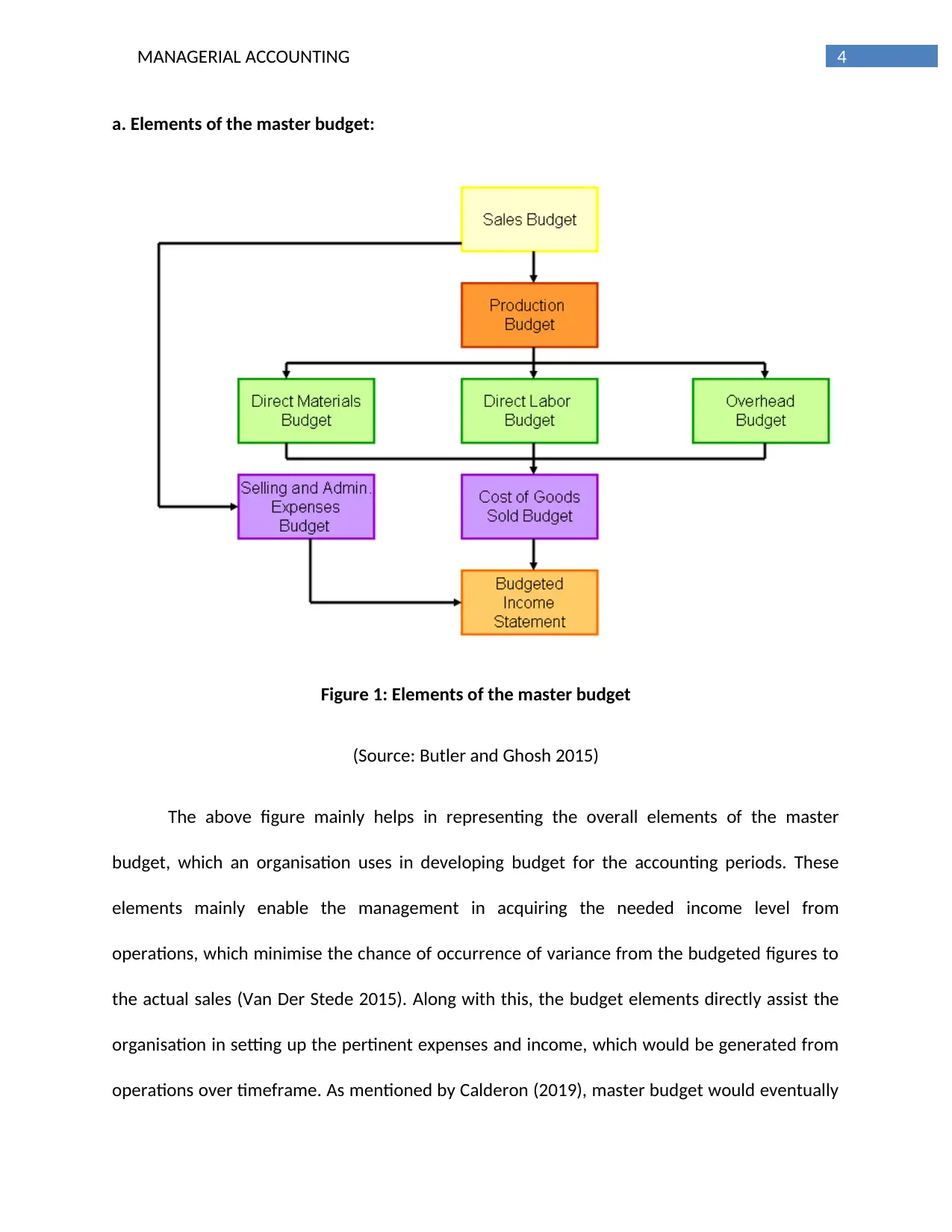

a. Elements of the master budget:

Figure 1: Elements of the master budget

(Source: Butler and Ghosh 2015)

The above figure mainly helps in representing the overall elements of the master

budget, which an organisation uses in developing budget for the accounting periods. These

elements mainly enable the management in acquiring the needed income level from

operations, which minimise the chance of occurrence of variance from the budgeted figures to

the actual sales (Van Der Stede 2015). Along with this, the budget elements directly assist the

organisation in setting up the pertinent expenses and income, which would be generated from

operations over timeframe. As mentioned by Calderon (2019), master budget would eventually

a. Elements of the master budget:

Figure 1: Elements of the master budget

(Source: Butler and Ghosh 2015)

The above figure mainly helps in representing the overall elements of the master

budget, which an organisation uses in developing budget for the accounting periods. These

elements mainly enable the management in acquiring the needed income level from

operations, which minimise the chance of occurrence of variance from the budgeted figures to

the actual sales (Van Der Stede 2015). Along with this, the budget elements directly assist the

organisation in setting up the pertinent expenses and income, which would be generated from

operations over timeframe. As mentioned by Calderon (2019), master budget would eventually

5MANAGERIAL ACCOUNTING

enable the organisation in generating high income level from operations, which could increase

overall management efficiency. The master budget would eventually assist in gaining the

needed fund level in order to support the master budget, which could assist in enhancing the

overall business operations. The significant elements of the master budget are represented as

follows:

Sales budget:

Sales budget is deemed to be the primary component of the master budget, which

enables the organisation in identifying the level of selling units, which would be incurred from

operations. The estimated price per unit and the total number of units sold for the future years

are estimated in sales budget. Along with this, the values in the sales budget are detected from

the past growth in selling values, which are generated by the organisation. The other elements

of the master budget are affected direct[y by the sales budget, since increasing selling units

would affect expenditure as well as production needs of the organisation (Carlsson-Wall, Kraus

and Lind 2015).

Production budget:

The business organisations mainly use the production budget for identifying the planned

production level, which the management needs to carry out for supporting the demand of the

products (Weygandt, Kimmel and Kieso 2015). Moreover, the production budget carries

increased value for the organisations in ascertaining the needed requirement of raw materials

and other purchases, which are required to be carried out for smooth conduction of business

operations. With the help of production budget, the organisations could ascertain the level of

enable the organisation in generating high income level from operations, which could increase

overall management efficiency. The master budget would eventually assist in gaining the

needed fund level in order to support the master budget, which could assist in enhancing the

overall business operations. The significant elements of the master budget are represented as

follows:

Sales budget:

Sales budget is deemed to be the primary component of the master budget, which

enables the organisation in identifying the level of selling units, which would be incurred from

operations. The estimated price per unit and the total number of units sold for the future years

are estimated in sales budget. Along with this, the values in the sales budget are detected from

the past growth in selling values, which are generated by the organisation. The other elements

of the master budget are affected direct[y by the sales budget, since increasing selling units

would affect expenditure as well as production needs of the organisation (Carlsson-Wall, Kraus

and Lind 2015).

Production budget:

The business organisations mainly use the production budget for identifying the planned

production level, which the management needs to carry out for supporting the demand of the

products (Weygandt, Kimmel and Kieso 2015). Moreover, the production budget carries

increased value for the organisations in ascertaining the needed requirement of raw materials

and other purchases, which are required to be carried out for smooth conduction of business

operations. With the help of production budget, the organisations could ascertain the level of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6MANAGERIAL ACCOUNTING

activities, which would be required in order to support sales demand from the customers

(Pavlatos and Kostakis 2015).

Cash budget:

The main reason behind the preparation of cash budget is to ascertain the level of

income and expenses expected to be generated from operations. The cash budget helps in

depicting the cash position that the organisation would generate in the accounting period.

Along with this, the cash budget enables the organisation in identifying increased level of cash

inflows as well as outflows, which would be carried out from operations (Shields 2015). The

formulation of cash budget is made after the preparation of sales budget and production

budget, which would enable the management in ascertaining the net cash flows, which would

rise over a specific timeframe.

Direct labour budget:

The sales budget has direct effect on the direct labour budget generated by the

organisation. The increased output level that is required on the part of the sales budget would

have direct impact on the direct labour needs in the system of production (Maskell, Baggaley

and Grasso 2016). Therefore, with the help of direct labour budget, the organisation would be

able to ascertain the level of staffs required in the function of production for assisting the

production output along with adherence to the sales budget. The formulation of direct labour

budget is made after the production units are prepared and this ascertains the labour input

level required for the next accounting period (Cokins 2014).

activities, which would be required in order to support sales demand from the customers

(Pavlatos and Kostakis 2015).

Cash budget:

The main reason behind the preparation of cash budget is to ascertain the level of

income and expenses expected to be generated from operations. The cash budget helps in

depicting the cash position that the organisation would generate in the accounting period.

Along with this, the cash budget enables the organisation in identifying increased level of cash

inflows as well as outflows, which would be carried out from operations (Shields 2015). The

formulation of cash budget is made after the preparation of sales budget and production

budget, which would enable the management in ascertaining the net cash flows, which would

rise over a specific timeframe.

Direct labour budget:

The sales budget has direct effect on the direct labour budget generated by the

organisation. The increased output level that is required on the part of the sales budget would

have direct impact on the direct labour needs in the system of production (Maskell, Baggaley

and Grasso 2016). Therefore, with the help of direct labour budget, the organisation would be

able to ascertain the level of staffs required in the function of production for assisting the

production output along with adherence to the sales budget. The formulation of direct labour

budget is made after the production units are prepared and this ascertains the labour input

level required for the next accounting period (Cokins 2014).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7MANAGERIAL ACCOUNTING

Direct materials budget:

After preparation of the sales budget and production budget, the direct materials

budget is prepared, which assist in ascertaining the material level required for supporting the

sales demand from the customers. Moreover, the direct materials budget would eventually

assist in ascertaining the level of expenses, which the organisation requires so that it could

support its production requirements. Furthermore, with the help of direct materials budget, it

is possible to gain an insight of the material requirements after evaluation of stock presently

held for production (Cooper, Ezzamel and Qu 2017).

Manufacturing overhead budget:

With the help of this budget, the organisation could gain an overview of the

manufacturing expenses, which the organisation has to incur apart from direct materials and

direct labour costs. The information provided in the budget cost has direct association with the

cost of revenue of the organisation. This has assisted in ascertaining the expense level, which

the organisation has to incur so that the future selling units could be supported adequately. The

manufacturing overhead budget is deemed to be significant in nature, since it includes a vast

proportion of expenses, which the organisation has to spend for accommodating the targeted

sales (Dekker 2016).

Selling and administrative expense budget:

In order to analyse the planned expenses for operations, the managers of a business

organisation utilise selling and administrative expense budget as well as other manufacturing

Direct materials budget:

After preparation of the sales budget and production budget, the direct materials

budget is prepared, which assist in ascertaining the material level required for supporting the

sales demand from the customers. Moreover, the direct materials budget would eventually

assist in ascertaining the level of expenses, which the organisation requires so that it could

support its production requirements. Furthermore, with the help of direct materials budget, it

is possible to gain an insight of the material requirements after evaluation of stock presently

held for production (Cooper, Ezzamel and Qu 2017).

Manufacturing overhead budget:

With the help of this budget, the organisation could gain an overview of the

manufacturing expenses, which the organisation has to incur apart from direct materials and

direct labour costs. The information provided in the budget cost has direct association with the

cost of revenue of the organisation. This has assisted in ascertaining the expense level, which

the organisation has to incur so that the future selling units could be supported adequately. The

manufacturing overhead budget is deemed to be significant in nature, since it includes a vast

proportion of expenses, which the organisation has to spend for accommodating the targeted

sales (Dekker 2016).

Selling and administrative expense budget:

In order to analyse the planned expenses for operations, the managers of a business

organisation utilise selling and administrative expense budget as well as other manufacturing

8MANAGERIAL ACCOUNTING

costs spent in the accounting period. Moreover, the analysis assists in ascertaining the selling

and administrative costs, which the organisation has to understand so that its future operations

could be supported adequately. With the help of these expenses, the spending level could be

ascertained that the organisation has to perform to support its operations in the accounting

period by assessing the results (Smith 2017).

Budgeted financial statements:

The organisations prepare the budgeted financial statements after completion of the

above-stated elements of the master budget. This is because they aid in developing the income

statement and the balance sheet statement for the accounting period (Fullerton, Kennedy and

Widener 2014). Moreover, the budgeted financial statements would assist in ascertaining the

estimated incomes, which the organisations would generate over the upcoming financial years.

As a result, the level of income earned and expenses made could be ascertained in the

accounting period (Horngren and Harrison 2015).

b. Top down and bottom up approach to the budget process:

Considerable differences could be observed between the bottom-up approach and top-

down approach, which the organisations could use for budget preparation. Moreover, the

contrast would assist in identifying the feasible process of budgeting, which the organisation

could use for budget preparation to support its future operations. The above two approaches

are used primarily in various business areas, which assist the management in undertaking

significant decisions about the business operations. With the help of top down approach, it is

costs spent in the accounting period. Moreover, the analysis assists in ascertaining the selling

and administrative costs, which the organisation has to understand so that its future operations

could be supported adequately. With the help of these expenses, the spending level could be

ascertained that the organisation has to perform to support its operations in the accounting

period by assessing the results (Smith 2017).

Budgeted financial statements:

The organisations prepare the budgeted financial statements after completion of the

above-stated elements of the master budget. This is because they aid in developing the income

statement and the balance sheet statement for the accounting period (Fullerton, Kennedy and

Widener 2014). Moreover, the budgeted financial statements would assist in ascertaining the

estimated incomes, which the organisations would generate over the upcoming financial years.

As a result, the level of income earned and expenses made could be ascertained in the

accounting period (Horngren and Harrison 2015).

b. Top down and bottom up approach to the budget process:

Considerable differences could be observed between the bottom-up approach and top-

down approach, which the organisations could use for budget preparation. Moreover, the

contrast would assist in identifying the feasible process of budgeting, which the organisation

could use for budget preparation to support its future operations. The above two approaches

are used primarily in various business areas, which assist the management in undertaking

significant decisions about the business operations. With the help of top down approach, it is

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9MANAGERIAL ACCOUNTING

possible to analyse a scenario from general to particular perspective, while the bottom up

approach concentrates on particular conditions after which it moves to general features. Along

with this, a particular difference is inherent between the bottom-up approach and top down

approach of the budget process that denotes the alternative measures undertaken by all the

processes (Kravet 2014).

The top down budget is set mainly by the top management, which restricts the final

budget holders in having the opportunity to participate in the budgeting procedure. Moreover,

the higher-level management assists in developing the budget directly, in which considerable

resource allocation is carried out in accordance with the discretion of the top officials. The

organisation is not involved in using the departmental heads in this procedure in order to

ascertain the budgeted figures. The top down budgeting procedure enables the managers in

developing the budget within the limits of the desired budgeted figures. This kind of approach

is extremely beneficial, which minimises the lead time for completion of the production

process, since the higher-level management is accountable to prepare the needed budgets. This

assists in saving time, which could minimise the association of the individuals responsible for

carrying out the daily activities of the organisation (Suomala, Lyly-Yrjänäinen and Lukka 2014).

However, there are a number of drawbacks in this method, which is associated with the non-

engagement of the individual identifying the particular expenses that could occur during

business operations. As a result, the budget would not be able to meet up to the expectations,

since the high-level individuals would fail to take into account the expense, which would be

incurred within the department (McLaney and Atrill 2014).

possible to analyse a scenario from general to particular perspective, while the bottom up

approach concentrates on particular conditions after which it moves to general features. Along

with this, a particular difference is inherent between the bottom-up approach and top down

approach of the budget process that denotes the alternative measures undertaken by all the

processes (Kravet 2014).

The top down budget is set mainly by the top management, which restricts the final

budget holders in having the opportunity to participate in the budgeting procedure. Moreover,

the higher-level management assists in developing the budget directly, in which considerable

resource allocation is carried out in accordance with the discretion of the top officials. The

organisation is not involved in using the departmental heads in this procedure in order to

ascertain the budgeted figures. The top down budgeting procedure enables the managers in

developing the budget within the limits of the desired budgeted figures. This kind of approach

is extremely beneficial, which minimises the lead time for completion of the production

process, since the higher-level management is accountable to prepare the needed budgets. This

assists in saving time, which could minimise the association of the individuals responsible for

carrying out the daily activities of the organisation (Suomala, Lyly-Yrjänäinen and Lukka 2014).

However, there are a number of drawbacks in this method, which is associated with the non-

engagement of the individual identifying the particular expenses that could occur during

business operations. As a result, the budget would not be able to meet up to the expectations,

since the high-level individuals would fail to take into account the expense, which would be

incurred within the department (McLaney and Atrill 2014).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10MANAGERIAL ACCOUNTING

The bottom-up budgeting approach is primarily a budgeting method, in which the

budget holders are able to engage in their own budgets. This process has direct engagement

with the departmental managers for developing the budget in line with their expenses and

requirements. The approach is deemed to be significant, since the anticipated expenses are

accommodated effectively within the budget. However, the bottom-up approach has a certain

number of drawbacks, as the expenses would be managed owing to the increased target of

spending of the departments. Hence, the bottom-up approach would assist in increasing the

expense level, which is required for each department. This is because the budget would

consider the expense needs of all the pertinent managers of the department (Messner 2016).

In case of both approaches, there are a number of benefits and limitations, which could

have unfavourable effects on the developed budgets of the business organisations. However,

the top-down approach would be more suitable for Angel Seafood Holdings Limited, since it

would enable the firm in developing the needed budgets to support its business operations.

Moreover, with the help of this approach, the organisation could formulate the required level

of income and expenses to be earned and incurred in a particular period.

c. Budgeted income statement of Angel Seafood Holdings for 2019:

Particulars 2018 2019

Revenue:

Sales revenue $ 1,458,916 $ 1,604,808

Other revenue $ 51,595 $ 51,595

Other income $ 1,632,213 $ 1,632,213

The bottom-up budgeting approach is primarily a budgeting method, in which the

budget holders are able to engage in their own budgets. This process has direct engagement

with the departmental managers for developing the budget in line with their expenses and

requirements. The approach is deemed to be significant, since the anticipated expenses are

accommodated effectively within the budget. However, the bottom-up approach has a certain

number of drawbacks, as the expenses would be managed owing to the increased target of

spending of the departments. Hence, the bottom-up approach would assist in increasing the

expense level, which is required for each department. This is because the budget would

consider the expense needs of all the pertinent managers of the department (Messner 2016).

In case of both approaches, there are a number of benefits and limitations, which could

have unfavourable effects on the developed budgets of the business organisations. However,

the top-down approach would be more suitable for Angel Seafood Holdings Limited, since it

would enable the firm in developing the needed budgets to support its business operations.

Moreover, with the help of this approach, the organisation could formulate the required level

of income and expenses to be earned and incurred in a particular period.

c. Budgeted income statement of Angel Seafood Holdings for 2019:

Particulars 2018 2019

Revenue:

Sales revenue $ 1,458,916 $ 1,604,808

Other revenue $ 51,595 $ 51,595

Other income $ 1,632,213 $ 1,632,213

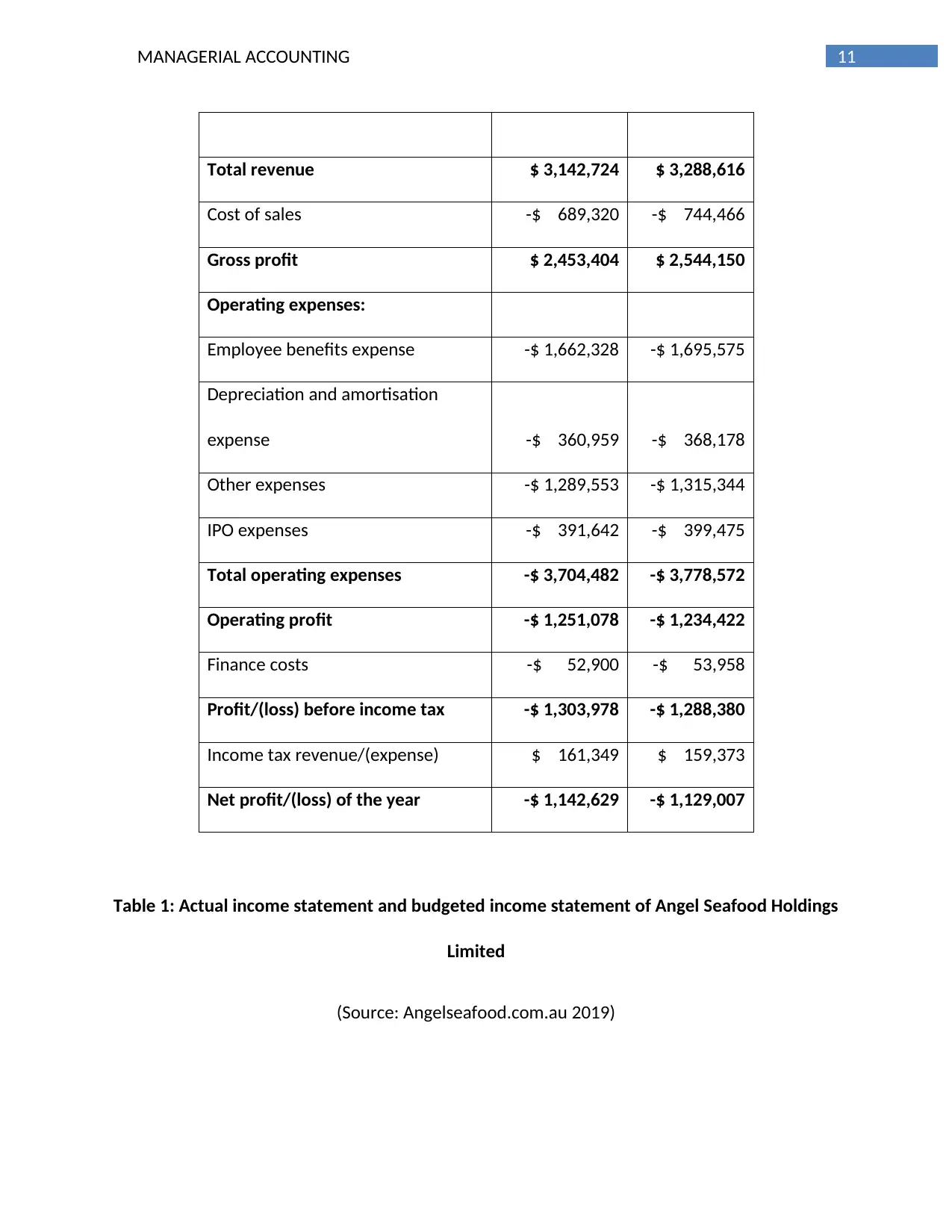

11MANAGERIAL ACCOUNTING

Total revenue $ 3,142,724 $ 3,288,616

Cost of sales -$ 689,320 -$ 744,466

Gross profit $ 2,453,404 $ 2,544,150

Operating expenses:

Employee benefits expense -$ 1,662,328 -$ 1,695,575

Depreciation and amortisation

expense -$ 360,959 -$ 368,178

Other expenses -$ 1,289,553 -$ 1,315,344

IPO expenses -$ 391,642 -$ 399,475

Total operating expenses -$ 3,704,482 -$ 3,778,572

Operating profit -$ 1,251,078 -$ 1,234,422

Finance costs -$ 52,900 -$ 53,958

Profit/(loss) before income tax -$ 1,303,978 -$ 1,288,380

Income tax revenue/(expense) $ 161,349 $ 159,373

Net profit/(loss) of the year -$ 1,142,629 -$ 1,129,007

Table 1: Actual income statement and budgeted income statement of Angel Seafood Holdings

Limited

(Source: Angelseafood.com.au 2019)

Total revenue $ 3,142,724 $ 3,288,616

Cost of sales -$ 689,320 -$ 744,466

Gross profit $ 2,453,404 $ 2,544,150

Operating expenses:

Employee benefits expense -$ 1,662,328 -$ 1,695,575

Depreciation and amortisation

expense -$ 360,959 -$ 368,178

Other expenses -$ 1,289,553 -$ 1,315,344

IPO expenses -$ 391,642 -$ 399,475

Total operating expenses -$ 3,704,482 -$ 3,778,572

Operating profit -$ 1,251,078 -$ 1,234,422

Finance costs -$ 52,900 -$ 53,958

Profit/(loss) before income tax -$ 1,303,978 -$ 1,288,380

Income tax revenue/(expense) $ 161,349 $ 159,373

Net profit/(loss) of the year -$ 1,142,629 -$ 1,129,007

Table 1: Actual income statement and budgeted income statement of Angel Seafood Holdings

Limited

(Source: Angelseafood.com.au 2019)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.