HI5017 Managerial Accounting: A.P. Eagers Budgeting and Analysis

VerifiedAdded on 2023/04/25

|18

|3867

|475

Report

AI Summary

This report focuses on the budgeting process of A.P. Eagers Limited, an ASX-listed company, including a detailed analysis of the master budget and its elements such as cash budget, inventory and expense, sales and production, and budgeted financial statements. It compares top-down and bottom-up budgeting approaches, recommending the bottom-up approach for A.P. Eagers based on its operations. The report also includes a predicted income statement for A.P. Eagers Limited, based on the company's 2017 income statement, highlighting potential changes and providing a comprehensive overview of the company's financial planning.

Accounting

A.P. Eagers Limited

2/3/2019

A.P. Eagers Limited

2/3/2019

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Accounting 1

Executive Summary

The purpose of the report is to focus on the budget and its process along with the process is

applied to the real-life company. The report requires the selection of the real world, ASX listed

company due to which A.P. Eagers Limited has been selected. The findings of the report include

the detailed analysis of the master budget with the elements which are used for preparing the

budget. Along with this, the major elements which are discussed include cash budget, inventory

and expense, sales and production with the budgeted financial statement. In addition, the top-

down and bottom-up approaches comparison is done with the motive to find the most appropriate

approach for the selected company. The findings show that the bottom-up approach has been

suggested to the company according to the operations. In the end, the predicted income statement

of the ASX Company that is A.P. Eagers Limited is prepared.

Executive Summary

The purpose of the report is to focus on the budget and its process along with the process is

applied to the real-life company. The report requires the selection of the real world, ASX listed

company due to which A.P. Eagers Limited has been selected. The findings of the report include

the detailed analysis of the master budget with the elements which are used for preparing the

budget. Along with this, the major elements which are discussed include cash budget, inventory

and expense, sales and production with the budgeted financial statement. In addition, the top-

down and bottom-up approaches comparison is done with the motive to find the most appropriate

approach for the selected company. The findings show that the bottom-up approach has been

suggested to the company according to the operations. In the end, the predicted income statement

of the ASX Company that is A.P. Eagers Limited is prepared.

Accounting 2

Contents

Introduction......................................................................................................................................3

Background of the company............................................................................................................4

Master budget elements...................................................................................................................4

Sales and production budget........................................................................................................5

Inventory and expense budget.....................................................................................................5

Cash budget.................................................................................................................................6

Budgeted financial statements.....................................................................................................6

Top-down approach and a bottom-up approach..............................................................................6

Top-down budgeting....................................................................................................................7

Bottom-up budgeting...................................................................................................................7

Comparisons of approaches.........................................................................................................8

Suitable approach.......................................................................................................................11

Budgeted Income statement of the company.................................................................................11

Changes in the income statement..............................................................................................12

Conclusion.....................................................................................................................................14

References......................................................................................................................................15

Contents

Introduction......................................................................................................................................3

Background of the company............................................................................................................4

Master budget elements...................................................................................................................4

Sales and production budget........................................................................................................5

Inventory and expense budget.....................................................................................................5

Cash budget.................................................................................................................................6

Budgeted financial statements.....................................................................................................6

Top-down approach and a bottom-up approach..............................................................................6

Top-down budgeting....................................................................................................................7

Bottom-up budgeting...................................................................................................................7

Comparisons of approaches.........................................................................................................8

Suitable approach.......................................................................................................................11

Budgeted Income statement of the company.................................................................................11

Changes in the income statement..............................................................................................12

Conclusion.....................................................................................................................................14

References......................................................................................................................................15

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Accounting 3

Introduction

The aim of the report is to throw the light on the budgeted income statement of the ASX

Company who is operating the business operations in the Australian market. The budgeted

income statement of the company reflects the forecasting of the increase in the revenue and

expenses of the company for the future. The report require to prepare the budget for real life

company due to which A.P. Eagers Limited ASX listed company has been selected and the

company is operating their business in the Australian market. The report majorly focuses on the

budget and the approaches which are used by the company while preparing the budgets of the

company. The discussion related to the elements of the master budget will be stated. The major

components of the master budget and the way to prepare it have been discussed. The major

differences in the approaches of budgeting will be explained. A.P. Eagers Limited needs to

implement one of the approaches while preparing the budget. The income statement for 2019

(budgeted) of the A.P. Eagers Limited has been prepared with the help of 2017 income statement

of the company.

Introduction

The aim of the report is to throw the light on the budgeted income statement of the ASX

Company who is operating the business operations in the Australian market. The budgeted

income statement of the company reflects the forecasting of the increase in the revenue and

expenses of the company for the future. The report require to prepare the budget for real life

company due to which A.P. Eagers Limited ASX listed company has been selected and the

company is operating their business in the Australian market. The report majorly focuses on the

budget and the approaches which are used by the company while preparing the budgets of the

company. The discussion related to the elements of the master budget will be stated. The major

components of the master budget and the way to prepare it have been discussed. The major

differences in the approaches of budgeting will be explained. A.P. Eagers Limited needs to

implement one of the approaches while preparing the budget. The income statement for 2019

(budgeted) of the A.P. Eagers Limited has been prepared with the help of 2017 income statement

of the company.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Accounting 4

Background of the company

A.P. Eagers Limited is owned and operates the motor vehicle dealership in the Australia market.

The company majorly operates the business in the four segments which include car retailing,

truck retailing, property and the investments (Freedman, 2018). The company majorly sells the

new and used motor vehicles with this it distributes and sells the parts with the accessories and

many other aftermarket products. The company is also indulged in the auctions of the motor

vehicle with this its operations are majorly present in Southern and central Queensland,

Adelaide. The company was formed by Edward Eager with his son Frederic in the year 1913

(Bloomberg, 2018). Since then, the company is continuing as the wholly-owned subsidiary of the

A.P. Eagers Limited (Freedman, 2018).

Master budget elements

Master budget is stated as the accumulation of the organisation lower-level budgets which are

prepared due to various areas of the functions presents (Freedman, 2018). The master budget is

the estimation of the operational and functional activities of the company. In order to completely

prepare the master budget, it is must for the company to achieve the sub-budgets that contribute

up to the master budget. The term master budget itself define that it is the combination of the

different sub-budgets and these sub-budgets are considered as the elements of master budget.

The detailed explanations of these elements are: -

Sales and production budget

The preparation of the master budget by the companies begins with the sales budget because this

budget provides the guidance to the rest of the budgeting process which is conducted by the

Background of the company

A.P. Eagers Limited is owned and operates the motor vehicle dealership in the Australia market.

The company majorly operates the business in the four segments which include car retailing,

truck retailing, property and the investments (Freedman, 2018). The company majorly sells the

new and used motor vehicles with this it distributes and sells the parts with the accessories and

many other aftermarket products. The company is also indulged in the auctions of the motor

vehicle with this its operations are majorly present in Southern and central Queensland,

Adelaide. The company was formed by Edward Eager with his son Frederic in the year 1913

(Bloomberg, 2018). Since then, the company is continuing as the wholly-owned subsidiary of the

A.P. Eagers Limited (Freedman, 2018).

Master budget elements

Master budget is stated as the accumulation of the organisation lower-level budgets which are

prepared due to various areas of the functions presents (Freedman, 2018). The master budget is

the estimation of the operational and functional activities of the company. In order to completely

prepare the master budget, it is must for the company to achieve the sub-budgets that contribute

up to the master budget. The term master budget itself define that it is the combination of the

different sub-budgets and these sub-budgets are considered as the elements of master budget.

The detailed explanations of these elements are: -

Sales and production budget

The preparation of the master budget by the companies begins with the sales budget because this

budget provides the guidance to the rest of the budgeting process which is conducted by the

Accounting 5

company. This budget is considered as the guiding budget as it guides the rest of the process of

budgeting because of the level of production which is direct links with the forecasting of the

sales of the company. To proceed with the sales budget of the company, the management usually

makes use of the current and prior year sales for initiating to make the educated guess on the

following year's sales figures (Chen, Weikart and Williams, 2014). Once the company make the

prediction for the level of sales, the information is going to be converted into the units of the

sales which help in determining the amount of the units that are required majorly to meet the

projected sales. Moreover, in the production budget, the amount of figures gets adjusted by the

amount of the inventory that is maintained by the company. This amount is adjusted with the

motive to identify the amount of inventory that is required to be produced (Accounting tools,

2018).

Inventory and expense budget

The formation of the master budget needs the inventory budgets which are made up of the direct

materials, labour and the manufacturing overhead budget which provide the assistance to the

company to determine the material, labour and overhead amount of products which will be

required to the company at the time of manufacturing the products for the selling it into the

market (Cox, 2014). Further, this budget contributes effectively in identifying the related sales

and administrative expenses which will be faced by the company in the near future. Thus, it

becomes essential for the company to accumulate the sub-budgets to form the master budget.

Cash budget

The cash budget is considered as one of the important sub-budgets which are created by the

company at the starting of the financial year. The budget is useful for the company in order to

predict the revenue that the company will receive and the expenses that company has to pay

company. This budget is considered as the guiding budget as it guides the rest of the process of

budgeting because of the level of production which is direct links with the forecasting of the

sales of the company. To proceed with the sales budget of the company, the management usually

makes use of the current and prior year sales for initiating to make the educated guess on the

following year's sales figures (Chen, Weikart and Williams, 2014). Once the company make the

prediction for the level of sales, the information is going to be converted into the units of the

sales which help in determining the amount of the units that are required majorly to meet the

projected sales. Moreover, in the production budget, the amount of figures gets adjusted by the

amount of the inventory that is maintained by the company. This amount is adjusted with the

motive to identify the amount of inventory that is required to be produced (Accounting tools,

2018).

Inventory and expense budget

The formation of the master budget needs the inventory budgets which are made up of the direct

materials, labour and the manufacturing overhead budget which provide the assistance to the

company to determine the material, labour and overhead amount of products which will be

required to the company at the time of manufacturing the products for the selling it into the

market (Cox, 2014). Further, this budget contributes effectively in identifying the related sales

and administrative expenses which will be faced by the company in the near future. Thus, it

becomes essential for the company to accumulate the sub-budgets to form the master budget.

Cash budget

The cash budget is considered as one of the important sub-budgets which are created by the

company at the starting of the financial year. The budget is useful for the company in order to

predict the revenue that the company will receive and the expenses that company has to pay

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Accounting 6

(Shcherbina and Tamulevičienė, 2016). This has been found that a cash budget helps the

company in predicting the receipts and payments. Further, for some of the companies, the cash

budget reflects the end of the process of budgeting and the other companies go on to the

complete budget financial statements.

Budgeted financial statements

The prediction or estimation of the financial statements needs the predicted amount present in the

income statement with the balance sheet which is majorly used by the company (Yılmaz, 2018).

The use of the financial statement is to review the position of the company in the market so that

they can work effectively to improve the same. After finalizing, the budget information of the

business is approved over into the budget field for every line item in the financial statement

within a business accounting software (Accounting tools, 2018). The budgeted financial

statement is essential for the company in predicting the financial positions, results, and the cash

flows of a business as the various dates in the near future.

Top-down approach and a bottom-up approach

In the budget preparation, the accountant of the company ensures that budgeting approach is

utilized effectively which can be both top-down approach and the bottom-up approach. A budget

is one of the financial plans for the saving, borrowing and spending money. A budget helps the

company in identifying whether it can operate based on the estimated income and expenses for a

particular period of time (Garrison, Noreen, Brewer and McGowan, 2010). There are several

types of budget approaches which include: - Zero-based budgeting, Top-down budgeting,

Flexible budgeting and Bottom-up budgeting

(Shcherbina and Tamulevičienė, 2016). This has been found that a cash budget helps the

company in predicting the receipts and payments. Further, for some of the companies, the cash

budget reflects the end of the process of budgeting and the other companies go on to the

complete budget financial statements.

Budgeted financial statements

The prediction or estimation of the financial statements needs the predicted amount present in the

income statement with the balance sheet which is majorly used by the company (Yılmaz, 2018).

The use of the financial statement is to review the position of the company in the market so that

they can work effectively to improve the same. After finalizing, the budget information of the

business is approved over into the budget field for every line item in the financial statement

within a business accounting software (Accounting tools, 2018). The budgeted financial

statement is essential for the company in predicting the financial positions, results, and the cash

flows of a business as the various dates in the near future.

Top-down approach and a bottom-up approach

In the budget preparation, the accountant of the company ensures that budgeting approach is

utilized effectively which can be both top-down approach and the bottom-up approach. A budget

is one of the financial plans for the saving, borrowing and spending money. A budget helps the

company in identifying whether it can operate based on the estimated income and expenses for a

particular period of time (Garrison, Noreen, Brewer and McGowan, 2010). There are several

types of budget approaches which include: - Zero-based budgeting, Top-down budgeting,

Flexible budgeting and Bottom-up budgeting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Accounting 7

Top-down budgeting

In this approach of budgeting, the top management forms the budgets for the departments that

are based on the combination of the predicting for the future expenses and revenue with the

previous year’s actual budget results and send the money down to the university pipeline. This

shows that it begins with top and ends at the lower department within the organisation. This

budgeting process can be effective for the lower management because they do not have to spend

the time to form the budget for the company and its related operations (Hilton and Platt, 2013).

This approach saves the time for lower management who are majorly involved in the process of

operations rather than the overall strategic plan. Though, the approach also has a disadvantage

which shows that the budget is formed by those who directly indulge in the daily operations of

the department and may not be aware of the specific expense that is linked to the department

(Kaplan and Atkinson, 2015).

Bottom-up budgeting

The bottom-up budgeting starts at the bottom of an organisation and gets approved by the top

management. The budget is decided by the lower level management and it is further presented to

the top level management majorly for the approval (Noreen, Brewer and Garrison, 2014). The

top-level management review the budget and then approve the budget which is proposed or send

it back down to the lower management with the motive to review and modify the same. The

bottom-up budgeting is a good thing for the lower management employees of the company

because it is based on the needs of the specific department because they are more familiar with

the needs that are required like labour, capital, suppliers to meet the goals (Pilbeam, 2018).

Though, this approach also leaves a disadvantage for the company because they remain unaware

of the strategic plan of the company. Further, the approach is flexible enough as the departments

Top-down budgeting

In this approach of budgeting, the top management forms the budgets for the departments that

are based on the combination of the predicting for the future expenses and revenue with the

previous year’s actual budget results and send the money down to the university pipeline. This

shows that it begins with top and ends at the lower department within the organisation. This

budgeting process can be effective for the lower management because they do not have to spend

the time to form the budget for the company and its related operations (Hilton and Platt, 2013).

This approach saves the time for lower management who are majorly involved in the process of

operations rather than the overall strategic plan. Though, the approach also has a disadvantage

which shows that the budget is formed by those who directly indulge in the daily operations of

the department and may not be aware of the specific expense that is linked to the department

(Kaplan and Atkinson, 2015).

Bottom-up budgeting

The bottom-up budgeting starts at the bottom of an organisation and gets approved by the top

management. The budget is decided by the lower level management and it is further presented to

the top level management majorly for the approval (Noreen, Brewer and Garrison, 2014). The

top-level management review the budget and then approve the budget which is proposed or send

it back down to the lower management with the motive to review and modify the same. The

bottom-up budgeting is a good thing for the lower management employees of the company

because it is based on the needs of the specific department because they are more familiar with

the needs that are required like labour, capital, suppliers to meet the goals (Pilbeam, 2018).

Though, this approach also leaves a disadvantage for the company because they remain unaware

of the strategic plan of the company. Further, the approach is flexible enough as the departments

Accounting 8

of the companies are not supposed to think for the top level management plans with the planning

of resources. This means that in this approach the departments of the companies doesn’t think for

the capital investment.

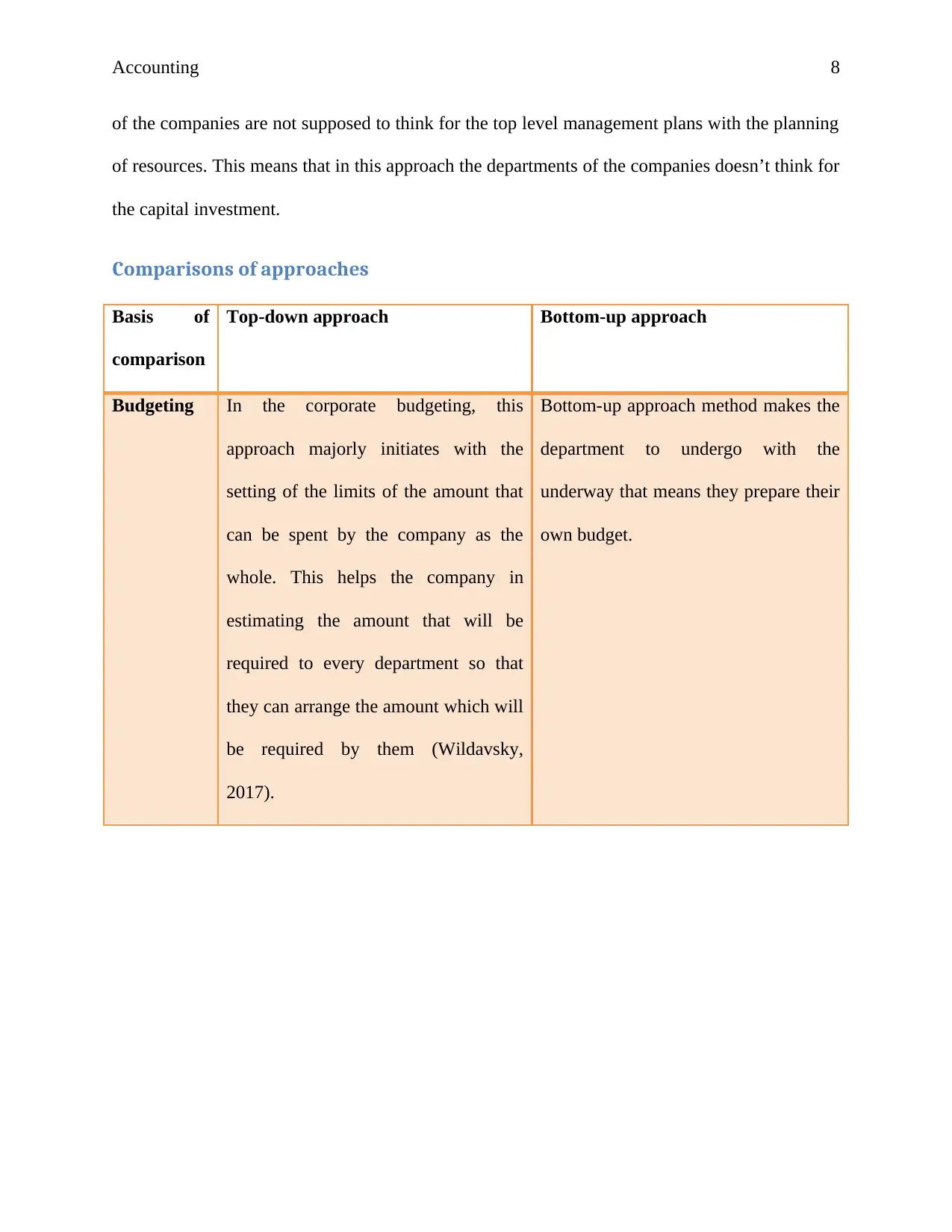

Comparisons of approaches

Basis of

comparison

Top-down approach Bottom-up approach

Budgeting In the corporate budgeting, this

approach majorly initiates with the

setting of the limits of the amount that

can be spent by the company as the

whole. This helps the company in

estimating the amount that will be

required to every department so that

they can arrange the amount which will

be required by them (Wildavsky,

2017).

Bottom-up approach method makes the

department to undergo with the

underway that means they prepare their

own budget.

of the companies are not supposed to think for the top level management plans with the planning

of resources. This means that in this approach the departments of the companies doesn’t think for

the capital investment.

Comparisons of approaches

Basis of

comparison

Top-down approach Bottom-up approach

Budgeting In the corporate budgeting, this

approach majorly initiates with the

setting of the limits of the amount that

can be spent by the company as the

whole. This helps the company in

estimating the amount that will be

required to every department so that

they can arrange the amount which will

be required by them (Wildavsky,

2017).

Bottom-up approach method makes the

department to undergo with the

underway that means they prepare their

own budget.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

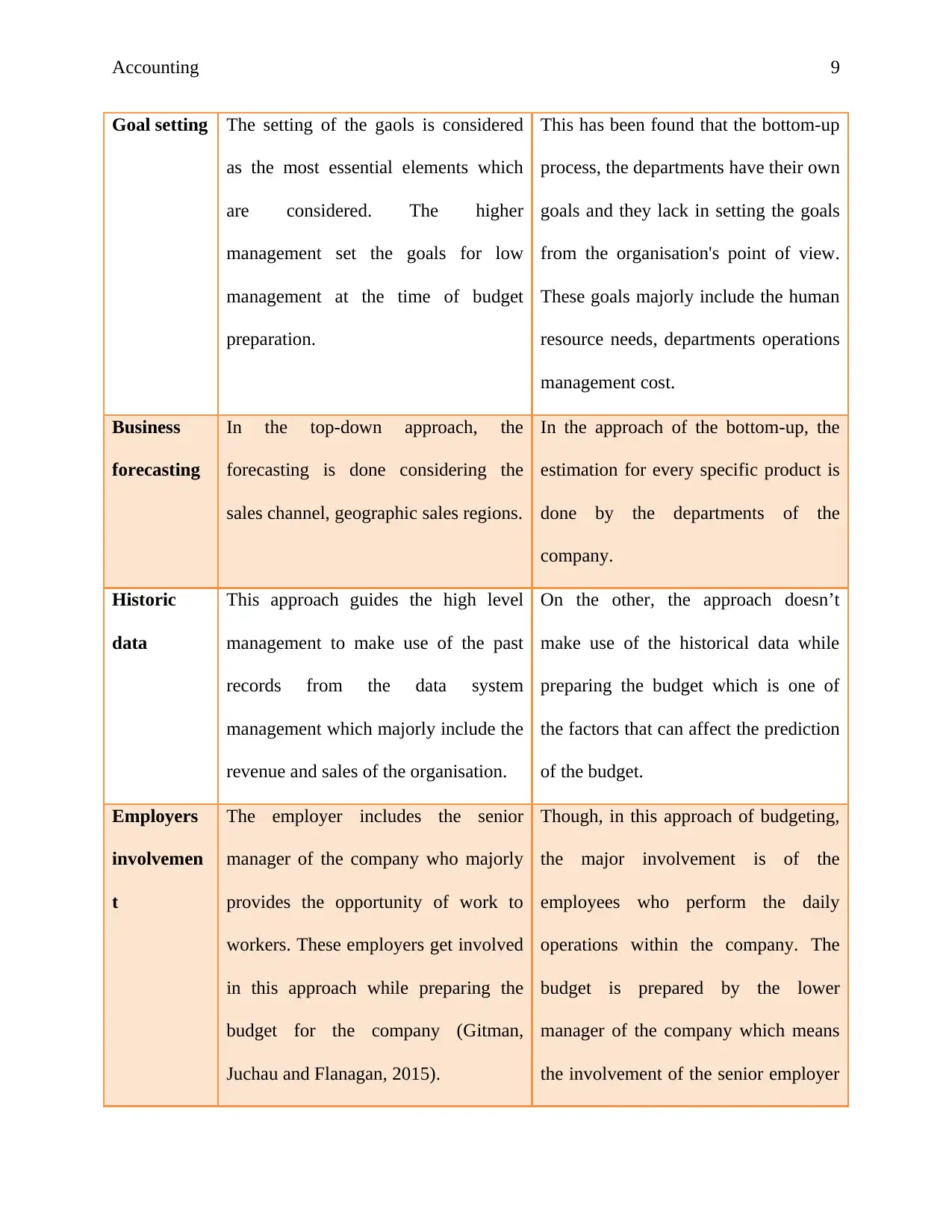

Accounting 9

Goal setting The setting of the gaols is considered

as the most essential elements which

are considered. The higher

management set the goals for low

management at the time of budget

preparation.

This has been found that the bottom-up

process, the departments have their own

goals and they lack in setting the goals

from the organisation's point of view.

These goals majorly include the human

resource needs, departments operations

management cost.

Business

forecasting

In the top-down approach, the

forecasting is done considering the

sales channel, geographic sales regions.

In the approach of the bottom-up, the

estimation for every specific product is

done by the departments of the

company.

Historic

data

This approach guides the high level

management to make use of the past

records from the data system

management which majorly include the

revenue and sales of the organisation.

On the other, the approach doesn’t

make use of the historical data while

preparing the budget which is one of

the factors that can affect the prediction

of the budget.

Employers

involvemen

t

The employer includes the senior

manager of the company who majorly

provides the opportunity of work to

workers. These employers get involved

in this approach while preparing the

budget for the company (Gitman,

Juchau and Flanagan, 2015).

Though, in this approach of budgeting,

the major involvement is of the

employees who perform the daily

operations within the company. The

budget is prepared by the lower

manager of the company which means

the involvement of the senior employer

Goal setting The setting of the gaols is considered

as the most essential elements which

are considered. The higher

management set the goals for low

management at the time of budget

preparation.

This has been found that the bottom-up

process, the departments have their own

goals and they lack in setting the goals

from the organisation's point of view.

These goals majorly include the human

resource needs, departments operations

management cost.

Business

forecasting

In the top-down approach, the

forecasting is done considering the

sales channel, geographic sales regions.

In the approach of the bottom-up, the

estimation for every specific product is

done by the departments of the

company.

Historic

data

This approach guides the high level

management to make use of the past

records from the data system

management which majorly include the

revenue and sales of the organisation.

On the other, the approach doesn’t

make use of the historical data while

preparing the budget which is one of

the factors that can affect the prediction

of the budget.

Employers

involvemen

t

The employer includes the senior

manager of the company who majorly

provides the opportunity of work to

workers. These employers get involved

in this approach while preparing the

budget for the company (Gitman,

Juchau and Flanagan, 2015).

Though, in this approach of budgeting,

the major involvement is of the

employees who perform the daily

operations within the company. The

budget is prepared by the lower

manager of the company which means

the involvement of the senior employer

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Accounting 10

is missing is this approach of the

budget.

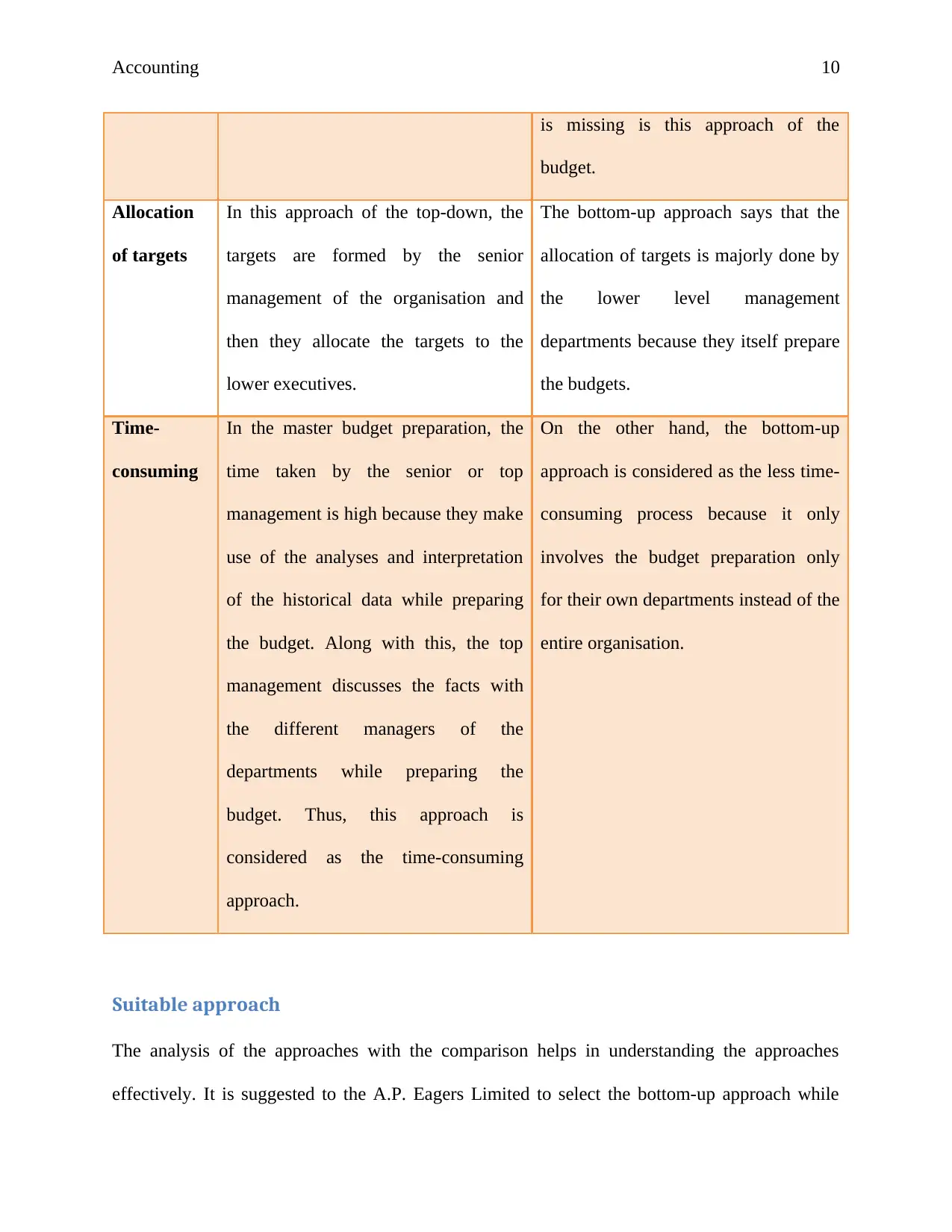

Allocation

of targets

In this approach of the top-down, the

targets are formed by the senior

management of the organisation and

then they allocate the targets to the

lower executives.

The bottom-up approach says that the

allocation of targets is majorly done by

the lower level management

departments because they itself prepare

the budgets.

Time-

consuming

In the master budget preparation, the

time taken by the senior or top

management is high because they make

use of the analyses and interpretation

of the historical data while preparing

the budget. Along with this, the top

management discusses the facts with

the different managers of the

departments while preparing the

budget. Thus, this approach is

considered as the time-consuming

approach.

On the other hand, the bottom-up

approach is considered as the less time-

consuming process because it only

involves the budget preparation only

for their own departments instead of the

entire organisation.

Suitable approach

The analysis of the approaches with the comparison helps in understanding the approaches

effectively. It is suggested to the A.P. Eagers Limited to select the bottom-up approach while

is missing is this approach of the

budget.

Allocation

of targets

In this approach of the top-down, the

targets are formed by the senior

management of the organisation and

then they allocate the targets to the

lower executives.

The bottom-up approach says that the

allocation of targets is majorly done by

the lower level management

departments because they itself prepare

the budgets.

Time-

consuming

In the master budget preparation, the

time taken by the senior or top

management is high because they make

use of the analyses and interpretation

of the historical data while preparing

the budget. Along with this, the top

management discusses the facts with

the different managers of the

departments while preparing the

budget. Thus, this approach is

considered as the time-consuming

approach.

On the other hand, the bottom-up

approach is considered as the less time-

consuming process because it only

involves the budget preparation only

for their own departments instead of the

entire organisation.

Suitable approach

The analysis of the approaches with the comparison helps in understanding the approaches

effectively. It is suggested to the A.P. Eagers Limited to select the bottom-up approach while

Accounting 11

preparing the budget for the organisation. The reason behind suggesting this approach is that the

company deals the operations majorly in the four different segments due to which they need to

maintain the different departments of various business units. The implementation of the bottom-

up approach provides the benefit to the company as they don’t prepare the budget as every

department will prepare their own budgets. All these budgets need to approve by the top level

management so they can easily find the differences and can improve the same (Trotman and

Carson, 2018). Along with this, the budget formation will not take the time which will lead to the

quick and effective decision by the company. Further, the employees will be able to attain the

different skills which will help them in bringing personal development. The bottom-up approach

is found suitable according to business operations.

Budgeted Income statement of the company

A.P. Eagers Limited budgeted income statement for the year 2019 is prepared based on 2017

data. Though, this has been found that 2018 income statement of the company is not disclosed

due to which the budgeted income statement has been prepared with the help of 2017 income

statement (A.P. Eagers Limited, 2018). These adjustments are related to the sales, expenses and

the cost of goods sold by the company.

Statement of Profit or loss of A.P. Eagers Limited

Actual Budgeted Variance

Particulars 2,017

2,0

19

$ $

Revenue 4,058,779.00

4,464,656.

90 -10%

Other Gains 17,934.00

19,727.

40 -10%

The share of net profits of associate 407 407 0%

Changes in inventories of finished goods and work in 27,645.00 29,856. -8%

preparing the budget for the organisation. The reason behind suggesting this approach is that the

company deals the operations majorly in the four different segments due to which they need to

maintain the different departments of various business units. The implementation of the bottom-

up approach provides the benefit to the company as they don’t prepare the budget as every

department will prepare their own budgets. All these budgets need to approve by the top level

management so they can easily find the differences and can improve the same (Trotman and

Carson, 2018). Along with this, the budget formation will not take the time which will lead to the

quick and effective decision by the company. Further, the employees will be able to attain the

different skills which will help them in bringing personal development. The bottom-up approach

is found suitable according to business operations.

Budgeted Income statement of the company

A.P. Eagers Limited budgeted income statement for the year 2019 is prepared based on 2017

data. Though, this has been found that 2018 income statement of the company is not disclosed

due to which the budgeted income statement has been prepared with the help of 2017 income

statement (A.P. Eagers Limited, 2018). These adjustments are related to the sales, expenses and

the cost of goods sold by the company.

Statement of Profit or loss of A.P. Eagers Limited

Actual Budgeted Variance

Particulars 2,017

2,0

19

$ $

Revenue 4,058,779.00

4,464,656.

90 -10%

Other Gains 17,934.00

19,727.

40 -10%

The share of net profits of associate 407 407 0%

Changes in inventories of finished goods and work in 27,645.00 29,856. -8%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.