Managerial Accounting: Assa Abloy Analysis Using PwC Value Framework

VerifiedAdded on 2023/06/03

|43

|5916

|452

Report

AI Summary

This report provides a comprehensive analysis of Assa Abloy's performance using the PwC value framework. It examines external drivers, strategic objectives, business model, governance, risk, remuneration, resources, relationships, and various performance metrics including operational, economic, social, environmental, and segmental aspects. The report critiques the quality of information disclosed in Assa Abloy's annual and sustainability reports, assessing elements such as competitive landscape, regulatory compliance, economic impact, social initiatives, and technological advancements. The analysis concludes with an overall assessment of the company's materiality and reporting practices, highlighting areas of strength and potential improvement. This detailed evaluation offers valuable insights into Assa Abloy's value creation and reporting transparency.

Running head: MANAGERIAL ACCOUNTING

Managerial Accounting

Name of the Student

Name of the University

Authors Note

Course ID

Managerial Accounting

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1MANAGERIAL ACCOUNTING

Executive Summary

The value framework of PwC is depicted with the approach for managing and measuring the

company’s performance and at the same time reporting the important aspects of disclosures.

This excerpt of information is useful in completion of a reporting model which is designated

as per meeting the requirements of investors in a more transparent and detailed manner. The

various sections of the study have made a critical interrogation for the quality of information

published in the annual report of Assa Abloy. This is identified with the important elements

which are outlined by PWC value framework.

Assa Abloy is considered as one of the global leaders in the opening solutions such as

manufacturing of electromechanical locks, digital door locks, mechanical locks, security

doors, hotel security and entrance automation. The consideration of both annual report and

sustainability report are analysed as per individual framework elements which are

commented upon as per quality of performance. The important health elements of

organisation have been conducted with strategy goals objectives, governance, risk and

remission aspects. The organisational performance elements have included segment of

performance, environmental performance and economic performance.

Executive Summary

The value framework of PwC is depicted with the approach for managing and measuring the

company’s performance and at the same time reporting the important aspects of disclosures.

This excerpt of information is useful in completion of a reporting model which is designated

as per meeting the requirements of investors in a more transparent and detailed manner. The

various sections of the study have made a critical interrogation for the quality of information

published in the annual report of Assa Abloy. This is identified with the important elements

which are outlined by PWC value framework.

Assa Abloy is considered as one of the global leaders in the opening solutions such as

manufacturing of electromechanical locks, digital door locks, mechanical locks, security

doors, hotel security and entrance automation. The consideration of both annual report and

sustainability report are analysed as per individual framework elements which are

commented upon as per quality of performance. The important health elements of

organisation have been conducted with strategy goals objectives, governance, risk and

remission aspects. The organisational performance elements have included segment of

performance, environmental performance and economic performance.

2MANAGERIAL ACCOUNTING

Table of Content

s

Introduction................................................................................................................................4

External Drivers: Competitive...................................................................................................4

External Drivers: Regulatory and Geopolitical..........................................................................6

External Drivers: Economic.......................................................................................................7

External Drivers: Social.............................................................................................................9

External Drivers: Technical.....................................................................................................10

Strategy: Strategy objectives....................................................................................................12

Strategy: Business model.........................................................................................................13

Strategy: Governance...............................................................................................................15

Strategy: Risk...........................................................................................................................17

Strategy: Remuneration............................................................................................................18

Resources and Relationships: Financial Assets:......................................................................20

Resource and Relationship: Physical Assets............................................................................22

Resource and Relationship: Customers....................................................................................24

Resource and Relationship: People & Culture.........................................................................25

Resource and Relationship: Innovation – G&S.......................................................................27

Resource and Relationship: Brand & Intellectual Assets........................................................28

Resource and Relationship: Processes & Supply Chain..........................................................29

Table of Content

s

Introduction................................................................................................................................4

External Drivers: Competitive...................................................................................................4

External Drivers: Regulatory and Geopolitical..........................................................................6

External Drivers: Economic.......................................................................................................7

External Drivers: Social.............................................................................................................9

External Drivers: Technical.....................................................................................................10

Strategy: Strategy objectives....................................................................................................12

Strategy: Business model.........................................................................................................13

Strategy: Governance...............................................................................................................15

Strategy: Risk...........................................................................................................................17

Strategy: Remuneration............................................................................................................18

Resources and Relationships: Financial Assets:......................................................................20

Resource and Relationship: Physical Assets............................................................................22

Resource and Relationship: Customers....................................................................................24

Resource and Relationship: People & Culture.........................................................................25

Resource and Relationship: Innovation – G&S.......................................................................27

Resource and Relationship: Brand & Intellectual Assets........................................................28

Resource and Relationship: Processes & Supply Chain..........................................................29

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3MANAGERIAL ACCOUNTING

Performance: Operational........................................................................................................31

Performance: Economic Performance......................................................................................33

Performance: Social Performance:...........................................................................................34

Performance: Environmental...................................................................................................36

Performance: Segmental..........................................................................................................37

Materiality................................................................................................................................39

Conclusion................................................................................................................................41

References................................................................................................................................42

Performance: Operational........................................................................................................31

Performance: Economic Performance......................................................................................33

Performance: Social Performance:...........................................................................................34

Performance: Environmental...................................................................................................36

Performance: Segmental..........................................................................................................37

Materiality................................................................................................................................39

Conclusion................................................................................................................................41

References................................................................................................................................42

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4MANAGERIAL ACCOUNTING

Introduction

The present content of the report has been stated in terms of the PWC value

framework applied for Assa Abloy. The main experts of the study will examine the different

types of the areas pertaining to the activates such as sourcing of the information from the

strategic objectives, stakeholder relationship, performance and resources. The important

considerations of the report will also include the various types of the other extent of the

discussions which will be focused in terms of aligning the decision-making framework of the

organization with the use of the appropriate accountability concepts.

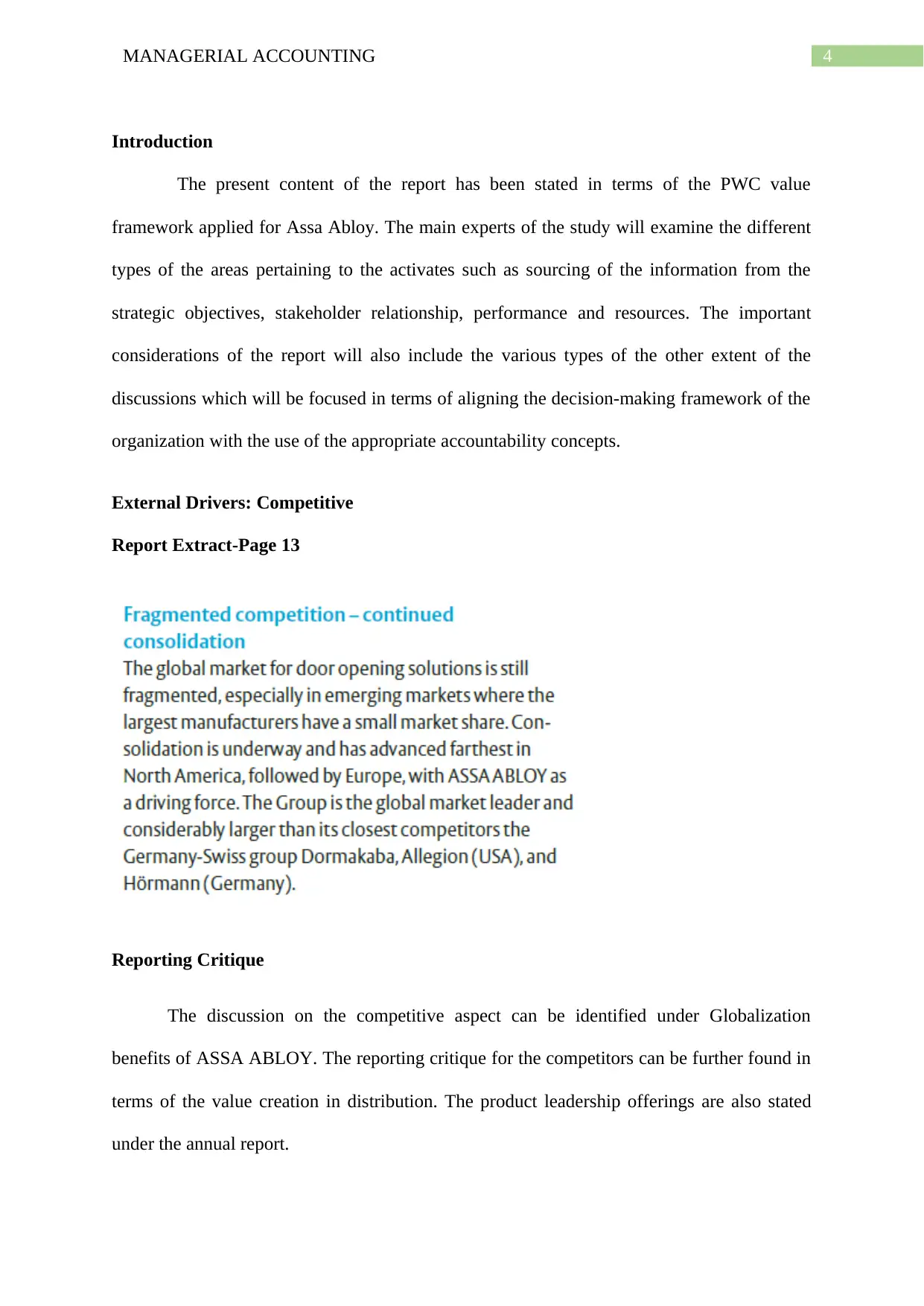

External Drivers: Competitive

Report Extract-Page 13

Reporting Critique

The discussion on the competitive aspect can be identified under Globalization

benefits of ASSA ABLOY. The reporting critique for the competitors can be further found in

terms of the value creation in distribution. The product leadership offerings are also stated

under the annual report.

Introduction

The present content of the report has been stated in terms of the PWC value

framework applied for Assa Abloy. The main experts of the study will examine the different

types of the areas pertaining to the activates such as sourcing of the information from the

strategic objectives, stakeholder relationship, performance and resources. The important

considerations of the report will also include the various types of the other extent of the

discussions which will be focused in terms of aligning the decision-making framework of the

organization with the use of the appropriate accountability concepts.

External Drivers: Competitive

Report Extract-Page 13

Reporting Critique

The discussion on the competitive aspect can be identified under Globalization

benefits of ASSA ABLOY. The reporting critique for the competitors can be further found in

terms of the value creation in distribution. The product leadership offerings are also stated

under the annual report.

5MANAGERIAL ACCOUNTING

Accessibility

The accessibility of such an information can be depicted under the markets overhead

stated with markets under page 13 of the annual report. The information on the product

leadership can be depicted in terms of the product leadership heading which is shown under

page 30 of the annual report.

Comprehensiveness

The comprehensiveness can be depicted in terms of the local presence in terms of the

competitive advantages. The similar concept is also applicable to the globalization trend of

ASSA ABLOY for promoting the various aspects of smart and cost-effective approach. The

competitiveness in terms of the product leadership can be depicted with the offering of the

new products pertaining to the high innovation rate. The launching of the new products has

further accounted for 25% of the overall sales.

Overall Conclusion

ASSA ABLOY is discerned to carry out the competitor’s risk analysis on both social

and local level. Moreover, it has considered significant disclosures on the global scope of

competition associated with the company thereby making the overall disclosure process as

good.

Accessibility

The accessibility of such an information can be depicted under the markets overhead

stated with markets under page 13 of the annual report. The information on the product

leadership can be depicted in terms of the product leadership heading which is shown under

page 30 of the annual report.

Comprehensiveness

The comprehensiveness can be depicted in terms of the local presence in terms of the

competitive advantages. The similar concept is also applicable to the globalization trend of

ASSA ABLOY for promoting the various aspects of smart and cost-effective approach. The

competitiveness in terms of the product leadership can be depicted with the offering of the

new products pertaining to the high innovation rate. The launching of the new products has

further accounted for 25% of the overall sales.

Overall Conclusion

ASSA ABLOY is discerned to carry out the competitor’s risk analysis on both social

and local level. Moreover, it has considered significant disclosures on the global scope of

competition associated with the company thereby making the overall disclosure process as

good.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6MANAGERIAL ACCOUNTING

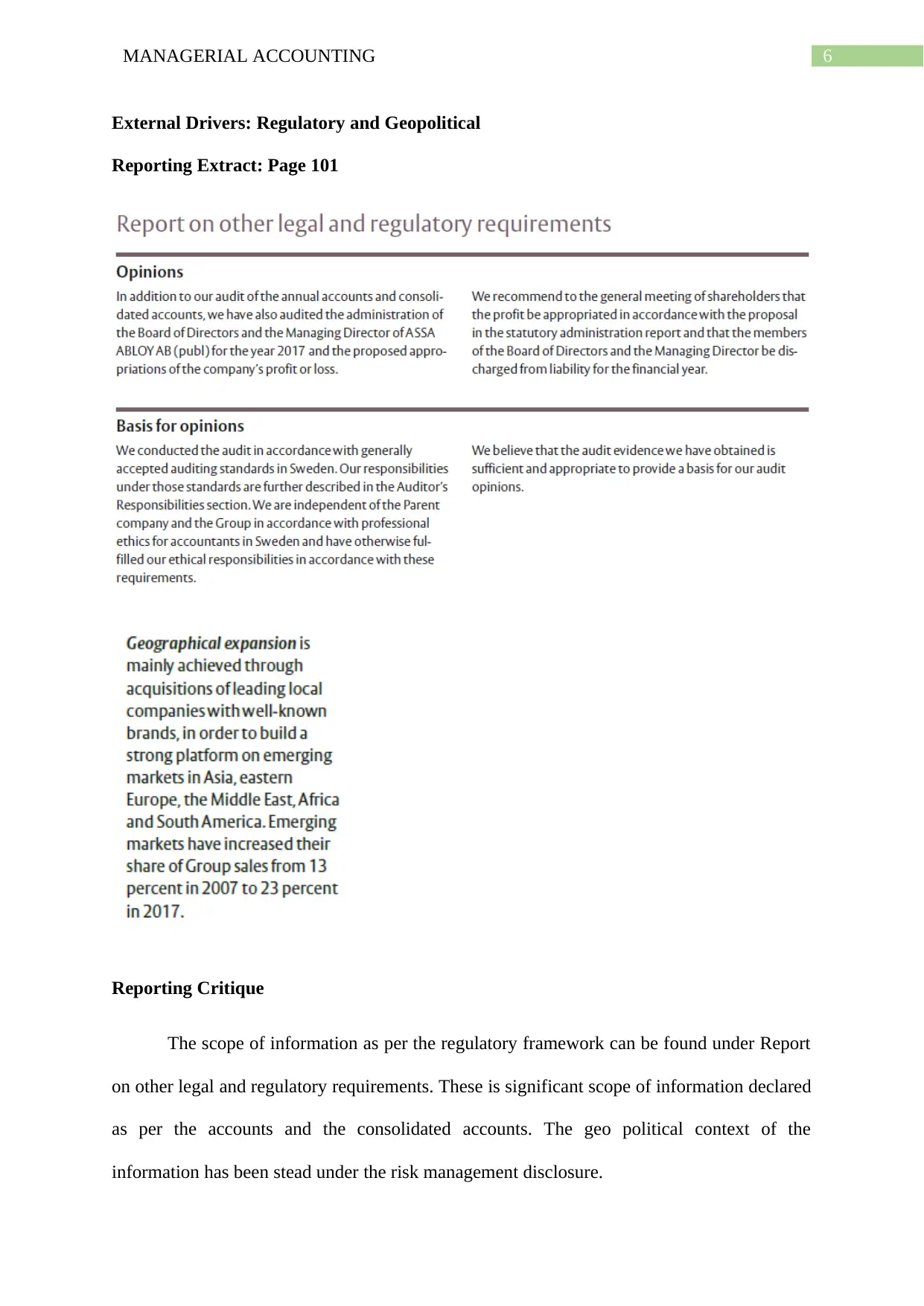

External Drivers: Regulatory and Geopolitical

Reporting Extract: Page 101

Reporting Critique

The scope of information as per the regulatory framework can be found under Report

on other legal and regulatory requirements. These is significant scope of information declared

as per the accounts and the consolidated accounts. The geo political context of the

information has been stead under the risk management disclosure.

External Drivers: Regulatory and Geopolitical

Reporting Extract: Page 101

Reporting Critique

The scope of information as per the regulatory framework can be found under Report

on other legal and regulatory requirements. These is significant scope of information declared

as per the accounts and the consolidated accounts. The geo political context of the

information has been stead under the risk management disclosure.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7MANAGERIAL ACCOUNTING

Accessibility

The expert of information on Report on other legal and regulatory requirements can

be sourced in page 101 of the annual report. Moreover, there is significant nature of the

information leading to the geo-political changes in the business which can be duly referred in

pages 10, pages 13 and page 26 of the annual report.

Comprehensiveness

The geo political context of the information has been further stated with the exposure

to the various types of information pertaining to the strategic, operational and

financial risks.

The regulatory requirements as per the annual report is stated with the opinions audit

of the annual accounts as per the ASSA.

The main basis of the opinions has been further depicted with the conduction of the

audit as per the generally accepted auditing standards in Sweden

Overall Conclusion

It can be seen that despite of the sufficient nature of the disclosure on the Report on

the legal and regulatory requirements in terms of the Responsibilities of the Board of

Directors and the Managing Director and Auditor’s responsibility. However, there is a

significant gap of information pertaining to the geo political changes. Therefore, such a

disclosure pertaining to this information can be seen to be bad.

External Drivers: Economic

Reporting Extract: Page 70

Accessibility

The expert of information on Report on other legal and regulatory requirements can

be sourced in page 101 of the annual report. Moreover, there is significant nature of the

information leading to the geo-political changes in the business which can be duly referred in

pages 10, pages 13 and page 26 of the annual report.

Comprehensiveness

The geo political context of the information has been further stated with the exposure

to the various types of information pertaining to the strategic, operational and

financial risks.

The regulatory requirements as per the annual report is stated with the opinions audit

of the annual accounts as per the ASSA.

The main basis of the opinions has been further depicted with the conduction of the

audit as per the generally accepted auditing standards in Sweden

Overall Conclusion

It can be seen that despite of the sufficient nature of the disclosure on the Report on

the legal and regulatory requirements in terms of the Responsibilities of the Board of

Directors and the Managing Director and Auditor’s responsibility. However, there is a

significant gap of information pertaining to the geo political changes. Therefore, such a

disclosure pertaining to this information can be seen to be bad.

External Drivers: Economic

Reporting Extract: Page 70

8MANAGERIAL ACCOUNTING

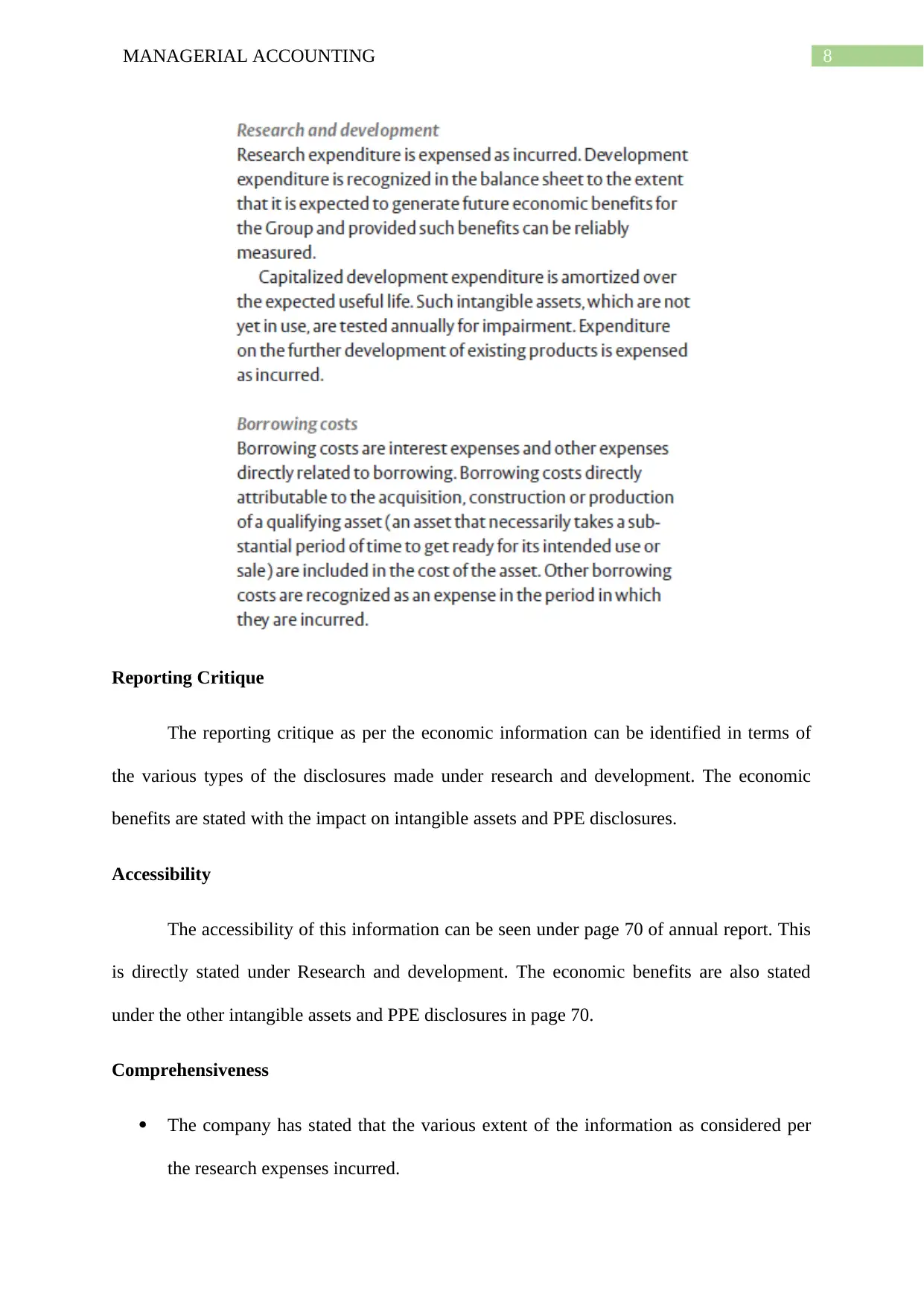

Reporting Critique

The reporting critique as per the economic information can be identified in terms of

the various types of the disclosures made under research and development. The economic

benefits are stated with the impact on intangible assets and PPE disclosures.

Accessibility

The accessibility of this information can be seen under page 70 of annual report. This

is directly stated under Research and development. The economic benefits are also stated

under the other intangible assets and PPE disclosures in page 70.

Comprehensiveness

The company has stated that the various extent of the information as considered per

the research expenses incurred.

Reporting Critique

The reporting critique as per the economic information can be identified in terms of

the various types of the disclosures made under research and development. The economic

benefits are stated with the impact on intangible assets and PPE disclosures.

Accessibility

The accessibility of this information can be seen under page 70 of annual report. This

is directly stated under Research and development. The economic benefits are also stated

under the other intangible assets and PPE disclosures in page 70.

Comprehensiveness

The company has stated that the various extent of the information as considered per

the research expenses incurred.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9MANAGERIAL ACCOUNTING

Moreover, the developmental expenditures are recognised as per the information

given in the balance sheet of the company with the main extent of information

pertaining to generate the future economic benefits.

The information on the intangible assets is also seen with a non-acquisition related

economic benefits for the assets associated with the group. Such an asset is depicted

under the initial recognition cost and amortization.

The comprehensiveness of the reporting has been further seen with the

Overall Conclusion

The overall depictions of the information show that there is significant nature of

reporting for the economic impacts there is considerable number of sources included by the

company in their annual report with the implication on intangible assets and PPE. Therefore,

such a reporting of information can be stated as good in nature.

External Drivers: Social

Reporting Extract: Page 7

Reporting Critique

In the section of goals and outcomes it can be seen that there is significant disclosure

of the information considered with the social KPI.

Moreover, the developmental expenditures are recognised as per the information

given in the balance sheet of the company with the main extent of information

pertaining to generate the future economic benefits.

The information on the intangible assets is also seen with a non-acquisition related

economic benefits for the assets associated with the group. Such an asset is depicted

under the initial recognition cost and amortization.

The comprehensiveness of the reporting has been further seen with the

Overall Conclusion

The overall depictions of the information show that there is significant nature of

reporting for the economic impacts there is considerable number of sources included by the

company in their annual report with the implication on intangible assets and PPE. Therefore,

such a reporting of information can be stated as good in nature.

External Drivers: Social

Reporting Extract: Page 7

Reporting Critique

In the section of goals and outcomes it can be seen that there is significant disclosure

of the information considered with the social KPI.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10MANAGERIAL ACCOUNTING

Accessibility

The social KPI information can be extracted from page 7 of the annual report.

Comprehensiveness

The social KPI is portrayed from the information associated with the injury rate and

role of women in management positions.

The company has set a social target of reducing the injury rate by 55% from 2015 to

2020.

The main target of the company has been depicted in terms of the initiatives taken by

the company pertaining to allocating 30% of the management positions to be held

women’s

Overall Conclusion

The company has stated about various sources of the information pertaining to the

information associated with the injury rate and role of women in management positions. In

addition to this, there is considerable amount of disclosure pertaining to the initiatives taken

by the company to allocate noteworthy position to be held by women. Due to large variety of

information available pertaining to social initiatives this disclosure can be depicted as good.

External Drivers: Technical

Reporting Extract: Page 58

Accessibility

The social KPI information can be extracted from page 7 of the annual report.

Comprehensiveness

The social KPI is portrayed from the information associated with the injury rate and

role of women in management positions.

The company has set a social target of reducing the injury rate by 55% from 2015 to

2020.

The main target of the company has been depicted in terms of the initiatives taken by

the company pertaining to allocating 30% of the management positions to be held

women’s

Overall Conclusion

The company has stated about various sources of the information pertaining to the

information associated with the injury rate and role of women in management positions. In

addition to this, there is considerable amount of disclosure pertaining to the initiatives taken

by the company to allocate noteworthy position to be held by women. Due to large variety of

information available pertaining to social initiatives this disclosure can be depicted as good.

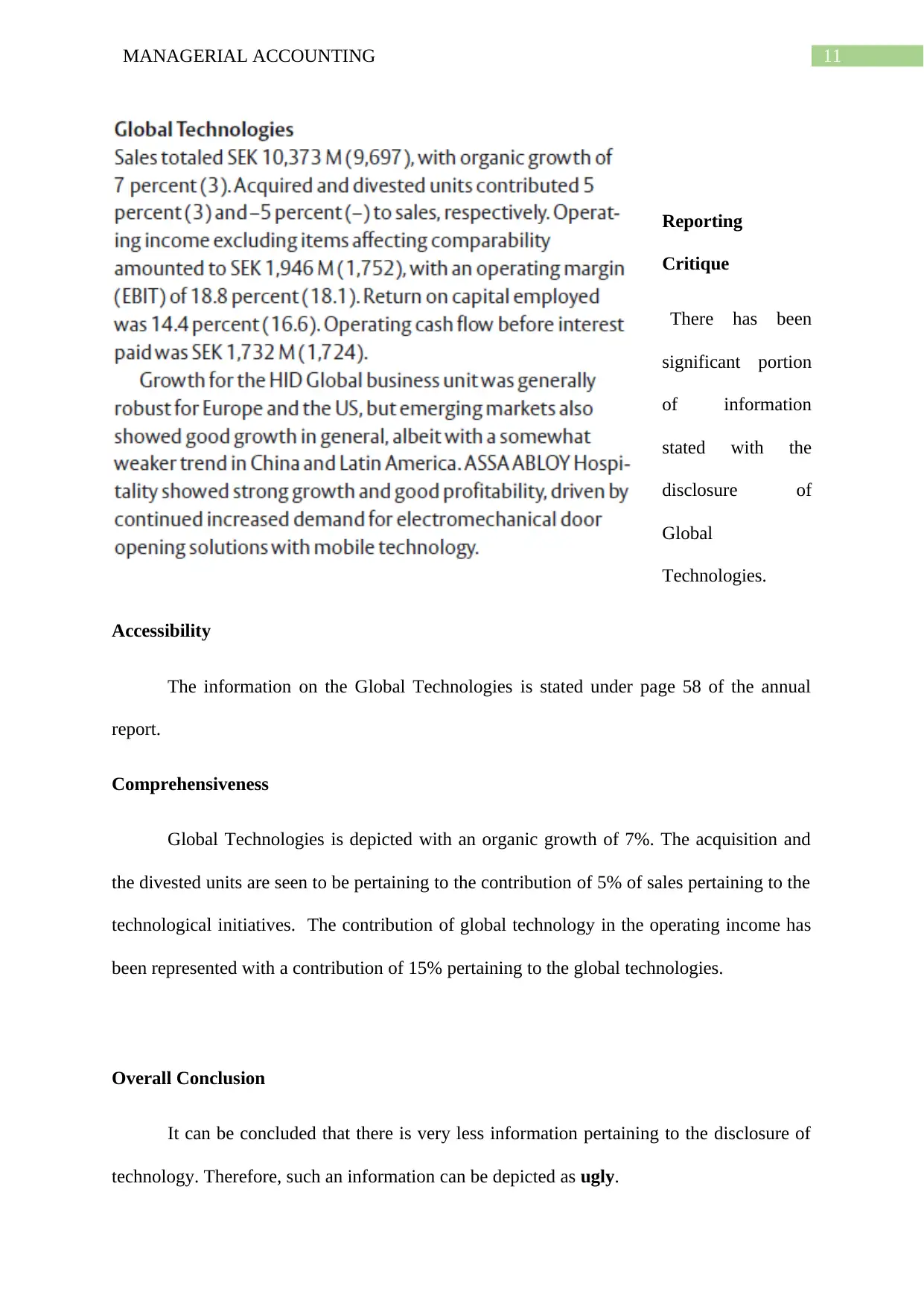

External Drivers: Technical

Reporting Extract: Page 58

11MANAGERIAL ACCOUNTING

Reporting

Critique

There has been

significant portion

of information

stated with the

disclosure of

Global

Technologies.

Accessibility

The information on the Global Technologies is stated under page 58 of the annual

report.

Comprehensiveness

Global Technologies is depicted with an organic growth of 7%. The acquisition and

the divested units are seen to be pertaining to the contribution of 5% of sales pertaining to the

technological initiatives. The contribution of global technology in the operating income has

been represented with a contribution of 15% pertaining to the global technologies.

Overall Conclusion

It can be concluded that there is very less information pertaining to the disclosure of

technology. Therefore, such an information can be depicted as ugly.

Reporting

Critique

There has been

significant portion

of information

stated with the

disclosure of

Global

Technologies.

Accessibility

The information on the Global Technologies is stated under page 58 of the annual

report.

Comprehensiveness

Global Technologies is depicted with an organic growth of 7%. The acquisition and

the divested units are seen to be pertaining to the contribution of 5% of sales pertaining to the

technological initiatives. The contribution of global technology in the operating income has

been represented with a contribution of 15% pertaining to the global technologies.

Overall Conclusion

It can be concluded that there is very less information pertaining to the disclosure of

technology. Therefore, such an information can be depicted as ugly.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 43

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.