Holmes Institute HI5017 Managerial Accounting Case Studies Report

VerifiedAdded on 2023/03/17

|19

|4971

|81

Report

AI Summary

This report presents a comprehensive analysis of a managerial accounting case study, focusing on cost concepts and their application in a service-based business. The assignment delves into the identification and classification of various cost types, including fixed, variable, and semi-variable costs, within the context of a childcare facility. It evaluates relevant and irrelevant information for decision-making, such as purchasing appliances. The report also includes a detailed cost-benefit analysis for hiring additional employees and evaluating the feasibility of renting new spaces. Furthermore, the report incorporates calculations for net profit margins under different scenarios, offering recommendations based on financial analysis. The document also explores components of managerial accounting and evaluates their relevance in decision-making and the contribution of management accounting in the process of innovation. Finally, the report includes findings from a relevant article and its usefulness to management accountants in Australian companies.

Running head: MANAGERIAL ACCOUNTING

Managerial accounting

Name of the student

Name of the university

Student ID

Author note

Managerial accounting

Name of the student

Name of the university

Student ID

Author note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

MANAGERIAL ACCOUNTING

Table of Contents

Part A:........................................................................................................................................3

Answer to requirement 1:.......................................................................................................3

Answer to requirement 2:.......................................................................................................4

Answer to requirement 3:.......................................................................................................5

Answer to requirement 4:.......................................................................................................6

Answer to requirement 5:.......................................................................................................7

Part B:......................................................................................................................................10

Answer to requirement 1:.....................................................................................................10

Identifying components of managerial accounting of the companies and evaluating

their relevance in the decision making process:...............................................................10

Answer to requirement 2:.....................................................................................................12

Evaluating the contribution of management accounting in the process of innovation:

..................................................................................................................................................12

Answer to requirement 3:.....................................................................................................13

Findings from the article and its usefulness to the management accountants to the

Australian companies:..........................................................................................................13

References and Bibliography list:.......................................................................................17

Table of Contents

Part A:........................................................................................................................................3

Answer to requirement 1:.......................................................................................................3

Answer to requirement 2:.......................................................................................................4

Answer to requirement 3:.......................................................................................................5

Answer to requirement 4:.......................................................................................................6

Answer to requirement 5:.......................................................................................................7

Part B:......................................................................................................................................10

Answer to requirement 1:.....................................................................................................10

Identifying components of managerial accounting of the companies and evaluating

their relevance in the decision making process:...............................................................10

Answer to requirement 2:.....................................................................................................12

Evaluating the contribution of management accounting in the process of innovation:

..................................................................................................................................................12

Answer to requirement 3:.....................................................................................................13

Findings from the article and its usefulness to the management accountants to the

Australian companies:..........................................................................................................13

References and Bibliography list:.......................................................................................17

MANAGERIAL ACCOUNTING

Part A:

Answer to requirement 1:

The case study talks about running of child care business and different types

of cost that is involved in running the child care facility. The components and the

concepts of cost forms an integral part of accounting system as it determines the

feasibility of carrying out business activities. In general, there are three types of cost

that is incurred by business activities such as fixed cost, variable cost and semi

variable cost. Fixed costs are the fixed expenses that are incurred by business

regardless of the services provided and total number of output produced (Joshi & Li,

2016). It can be therefore said such costs are inured even when the business

product level is zero and such costs are incurred on monthly or daily basis. From the

given case study, fixed expenses are the cost of insurance and the license fee that

are being paid to state. The state charges license fee of $ 225 for running the child

care facility for which the permit is limited to provide service to maximum of six

children. In addition to this, they are also required to pay insurance that costs them

amount of $ 3840 on annual basis.

Variable costs on other hand are the costs that vary in proportion to the level

of output produced and services provided. This means the cost vary with change in

the level of output produced that is it increases or decreases with expanding or

falling production. Hence, business is not required to incur any variable cost when

the level of output produced is zero. Some of the variable costs are the salaries paid

to employees and cost of meal and snacks per day per children. The cost of meal

Part A:

Answer to requirement 1:

The case study talks about running of child care business and different types

of cost that is involved in running the child care facility. The components and the

concepts of cost forms an integral part of accounting system as it determines the

feasibility of carrying out business activities. In general, there are three types of cost

that is incurred by business activities such as fixed cost, variable cost and semi

variable cost. Fixed costs are the fixed expenses that are incurred by business

regardless of the services provided and total number of output produced (Joshi & Li,

2016). It can be therefore said such costs are inured even when the business

product level is zero and such costs are incurred on monthly or daily basis. From the

given case study, fixed expenses are the cost of insurance and the license fee that

are being paid to state. The state charges license fee of $ 225 for running the child

care facility for which the permit is limited to provide service to maximum of six

children. In addition to this, they are also required to pay insurance that costs them

amount of $ 3840 on annual basis.

Variable costs on other hand are the costs that vary in proportion to the level

of output produced and services provided. This means the cost vary with change in

the level of output produced that is it increases or decreases with expanding or

falling production. Hence, business is not required to incur any variable cost when

the level of output produced is zero. Some of the variable costs are the salaries paid

to employees and cost of meal and snacks per day per children. The cost of meal

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

MANAGERIAL ACCOUNTING

and snacks for children per day is $ 3.20 and the salary paid to employee is $ 9 per

hour which would increase with increase in number of children that are provided

service.

Semi variable costs are the costs that involve the components of both fixed

and variable cost. For a given level of production, the cost will remain fixed and after

the production level exceeds a certain level, the cost will also start increasing

proportionately. Some of the utility costs that are incurred by business are utility cost

that would increase. In addition to this, energy cost for running the washer and dryer

increases every year by $ 120 and $ 145 respectively. The license fee paid by

couple is for providing service to maximum of six children. If the couple intends to

provide services to additional number of children, the license fees paid would also

increase.

Answer to requirement 2:

The couple is required to make decision about purchasing of appliances for

laundering of the soiled clothes of children. They are thinking of purchasing the

appliances that would help them in laundering the clothes. Hence, some of the

relevant information that is required to be considered by the couple for purchasing

the appliances is cost of washer and cost of dryer. Cost of installing the machine is

information that should be considered by the couple along with the appliance

delivery charges. In addition to this, couple is also required account for operational

expenses that would be incurred by the couple. For determining the total operating

expenses, couple is required to collect information about the depreciation, energy

cost of washer and dryer. The information that is not relevant for the couple when

and snacks for children per day is $ 3.20 and the salary paid to employee is $ 9 per

hour which would increase with increase in number of children that are provided

service.

Semi variable costs are the costs that involve the components of both fixed

and variable cost. For a given level of production, the cost will remain fixed and after

the production level exceeds a certain level, the cost will also start increasing

proportionately. Some of the utility costs that are incurred by business are utility cost

that would increase. In addition to this, energy cost for running the washer and dryer

increases every year by $ 120 and $ 145 respectively. The license fee paid by

couple is for providing service to maximum of six children. If the couple intends to

provide services to additional number of children, the license fees paid would also

increase.

Answer to requirement 2:

The couple is required to make decision about purchasing of appliances for

laundering of the soiled clothes of children. They are thinking of purchasing the

appliances that would help them in laundering the clothes. Hence, some of the

relevant information that is required to be considered by the couple for purchasing

the appliances is cost of washer and cost of dryer. Cost of installing the machine is

information that should be considered by the couple along with the appliance

delivery charges. In addition to this, couple is also required account for operational

expenses that would be incurred by the couple. For determining the total operating

expenses, couple is required to collect information about the depreciation, energy

cost of washer and dryer. The information that is not relevant for the couple when

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

MANAGERIAL ACCOUNTING

deciding the purchase of appliances is the cost of old appliances, license fees and

insurance cost (Robson & Bottausci, 2018).

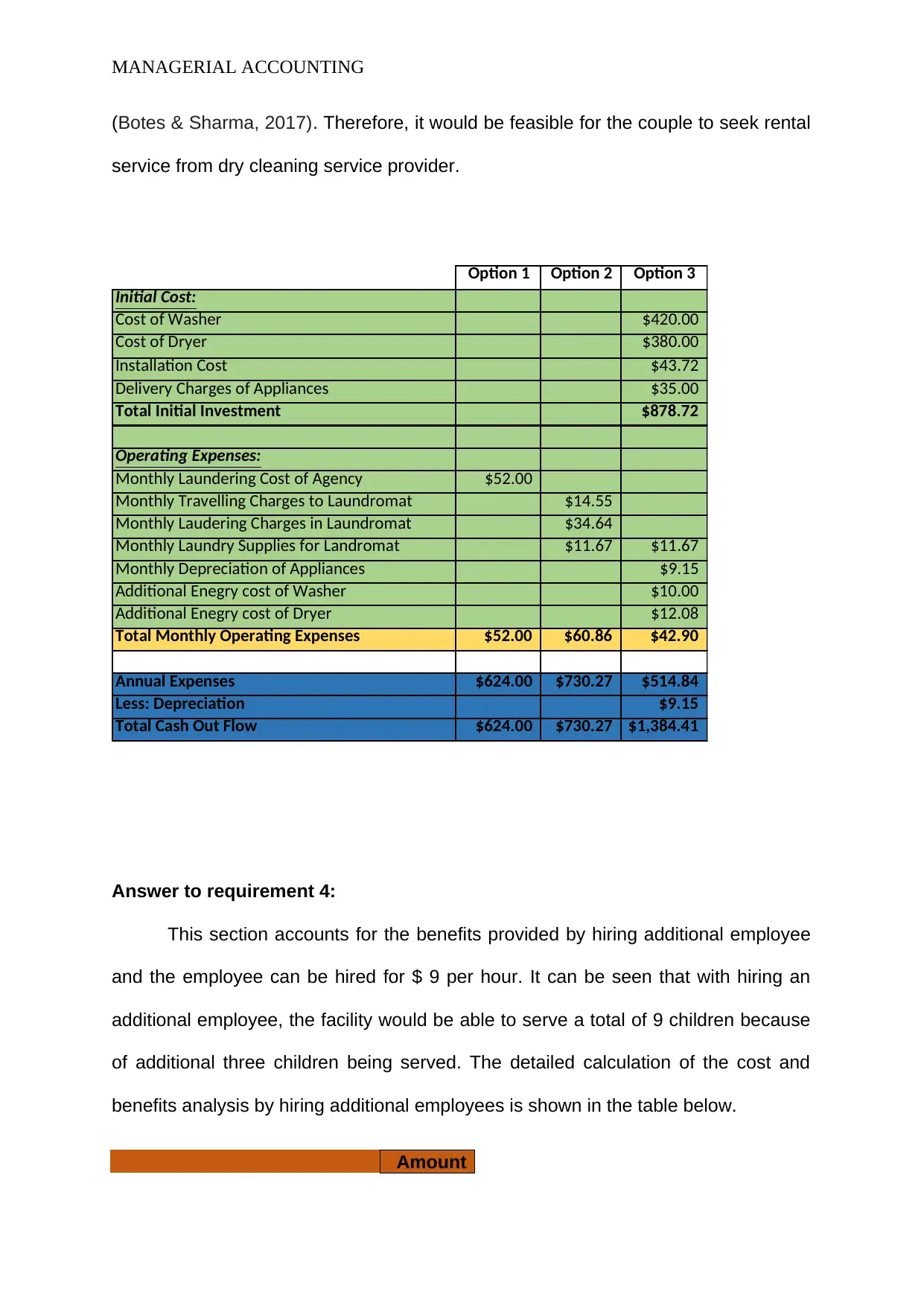

Answer to requirement 3:

For laundering the clothes, couple is required to evaluate the benefits and

costs provided by each of the options. The first option available to the customer is to

seek rental service from dry cleaning and red oak laundry. There is no initial cost of

investment in this option and the total operating expenses for seeking renting service

is computed at $ 52 which the makes the total outflow of cash of amount $ 624. The

second option available to the customer is opt for Laundromat services for which the

operating expenses are incurred for laundry supplies, laundry charges and travelling

charges. Total amount of operating expenses on monthly basis comes to $ 60.86

and the total amount of annual expenses is recorded at $ 730.27. The last option is

to purchase their own dryer and washer for washing the clothes for which the couple

is required to incur initial cost and operating expenses. The total amount of initial

investment includes the components such as cost of washer and dryer, delivery

charges of appliances and installation cost at the value of $ 878.72. In addition to

this, the operating expenses include energy cost for washer and dryer along with

depreciation at amount of $ 42.90. After taking into account all the components, the

total expenses of purchasing the new appliances would be $ 1384.41. From the

analysis of computed figures, it is observed that the total outflow of cash is highest

when the couple opts to purchase the washer and dryer compared to renting service

and Laundromat services. However, one point that should be taken into account is

the annual expense which is lowest when the couple is purchasing the appliances

deciding the purchase of appliances is the cost of old appliances, license fees and

insurance cost (Robson & Bottausci, 2018).

Answer to requirement 3:

For laundering the clothes, couple is required to evaluate the benefits and

costs provided by each of the options. The first option available to the customer is to

seek rental service from dry cleaning and red oak laundry. There is no initial cost of

investment in this option and the total operating expenses for seeking renting service

is computed at $ 52 which the makes the total outflow of cash of amount $ 624. The

second option available to the customer is opt for Laundromat services for which the

operating expenses are incurred for laundry supplies, laundry charges and travelling

charges. Total amount of operating expenses on monthly basis comes to $ 60.86

and the total amount of annual expenses is recorded at $ 730.27. The last option is

to purchase their own dryer and washer for washing the clothes for which the couple

is required to incur initial cost and operating expenses. The total amount of initial

investment includes the components such as cost of washer and dryer, delivery

charges of appliances and installation cost at the value of $ 878.72. In addition to

this, the operating expenses include energy cost for washer and dryer along with

depreciation at amount of $ 42.90. After taking into account all the components, the

total expenses of purchasing the new appliances would be $ 1384.41. From the

analysis of computed figures, it is observed that the total outflow of cash is highest

when the couple opts to purchase the washer and dryer compared to renting service

and Laundromat services. However, one point that should be taken into account is

the annual expense which is lowest when the couple is purchasing the appliances

MANAGERIAL ACCOUNTING

(Botes & Sharma, 2017). Therefore, it would be feasible for the couple to seek rental

service from dry cleaning service provider.

Option 1 Option 2 Option 3

Initial Cost:

Cost of Washer $420.00

Cost of Dryer $380.00

Installation Cost $43.72

Delivery Charges of Appliances $35.00

Total Initial Investment $878.72

Operating Expenses:

Monthly Laundering Cost of Agency $52.00

Monthly Travelling Charges to Laundromat $14.55

Monthly Laudering Charges in Laundromat $34.64

Monthly Laundry Supplies for Landromat $11.67 $11.67

Monthly Depreciation of Appliances $9.15

Additional Enegry cost of Washer $10.00

Additional Enegry cost of Dryer $12.08

Total Monthly Operating Expenses $52.00 $60.86 $42.90

Annual Expenses $624.00 $730.27 $514.84

Less: Depreciation $9.15

Total Cash Out Flow $624.00 $730.27 $1,384.41

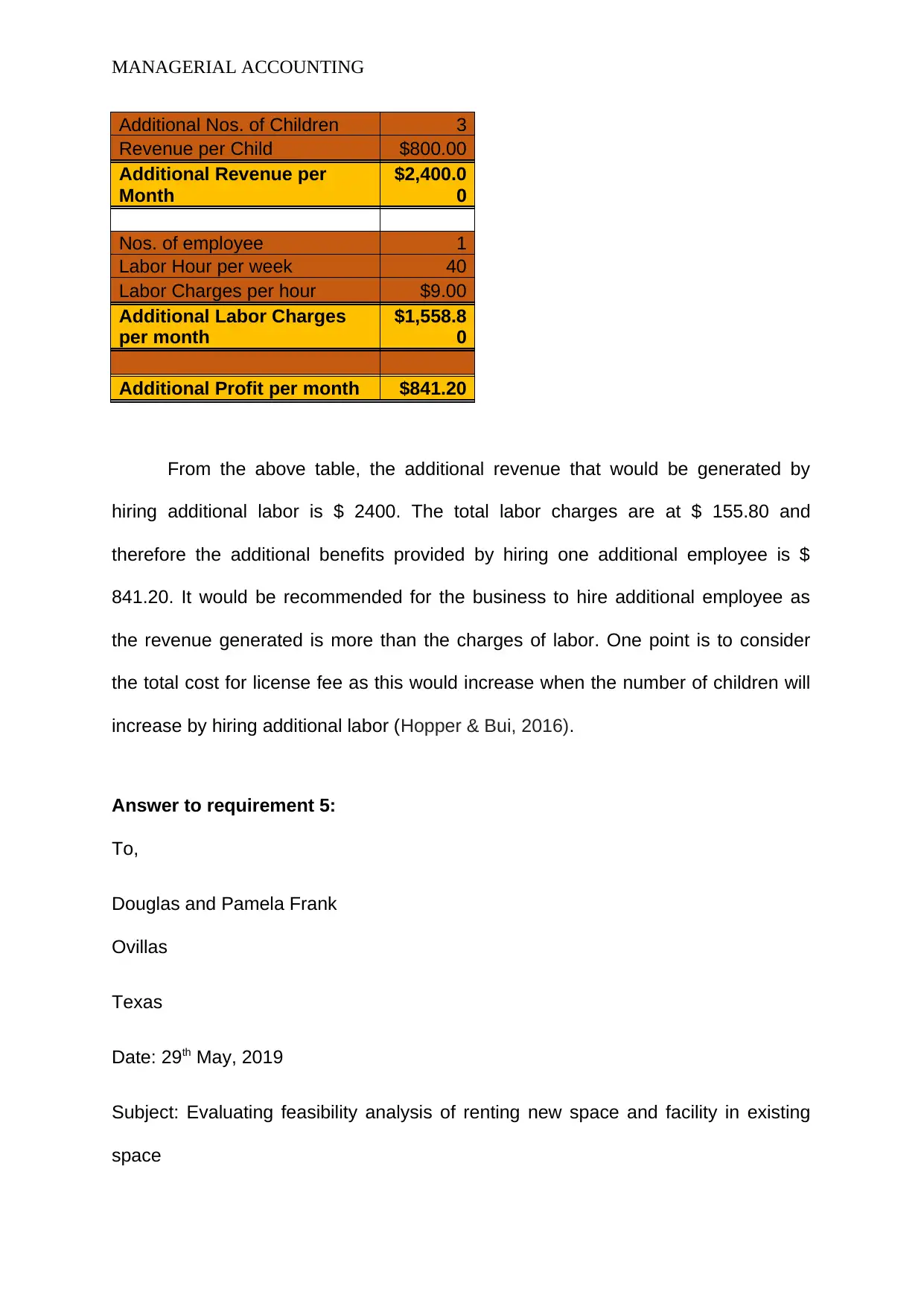

Answer to requirement 4:

This section accounts for the benefits provided by hiring additional employee

and the employee can be hired for $ 9 per hour. It can be seen that with hiring an

additional employee, the facility would be able to serve a total of 9 children because

of additional three children being served. The detailed calculation of the cost and

benefits analysis by hiring additional employees is shown in the table below.

Amount

(Botes & Sharma, 2017). Therefore, it would be feasible for the couple to seek rental

service from dry cleaning service provider.

Option 1 Option 2 Option 3

Initial Cost:

Cost of Washer $420.00

Cost of Dryer $380.00

Installation Cost $43.72

Delivery Charges of Appliances $35.00

Total Initial Investment $878.72

Operating Expenses:

Monthly Laundering Cost of Agency $52.00

Monthly Travelling Charges to Laundromat $14.55

Monthly Laudering Charges in Laundromat $34.64

Monthly Laundry Supplies for Landromat $11.67 $11.67

Monthly Depreciation of Appliances $9.15

Additional Enegry cost of Washer $10.00

Additional Enegry cost of Dryer $12.08

Total Monthly Operating Expenses $52.00 $60.86 $42.90

Annual Expenses $624.00 $730.27 $514.84

Less: Depreciation $9.15

Total Cash Out Flow $624.00 $730.27 $1,384.41

Answer to requirement 4:

This section accounts for the benefits provided by hiring additional employee

and the employee can be hired for $ 9 per hour. It can be seen that with hiring an

additional employee, the facility would be able to serve a total of 9 children because

of additional three children being served. The detailed calculation of the cost and

benefits analysis by hiring additional employees is shown in the table below.

Amount

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

MANAGERIAL ACCOUNTING

Additional Nos. of Children 3

Revenue per Child $800.00

Additional Revenue per

Month

$2,400.0

0

Nos. of employee 1

Labor Hour per week 40

Labor Charges per hour $9.00

Additional Labor Charges

per month

$1,558.8

0

Additional Profit per month $841.20

From the above table, the additional revenue that would be generated by

hiring additional labor is $ 2400. The total labor charges are at $ 155.80 and

therefore the additional benefits provided by hiring one additional employee is $

841.20. It would be recommended for the business to hire additional employee as

the revenue generated is more than the charges of labor. One point is to consider

the total cost for license fee as this would increase when the number of children will

increase by hiring additional labor (Hopper & Bui, 2016).

Answer to requirement 5:

To,

Douglas and Pamela Frank

Ovillas

Texas

Date: 29th May, 2019

Subject: Evaluating feasibility analysis of renting new space and facility in existing

space

Additional Nos. of Children 3

Revenue per Child $800.00

Additional Revenue per

Month

$2,400.0

0

Nos. of employee 1

Labor Hour per week 40

Labor Charges per hour $9.00

Additional Labor Charges

per month

$1,558.8

0

Additional Profit per month $841.20

From the above table, the additional revenue that would be generated by

hiring additional labor is $ 2400. The total labor charges are at $ 155.80 and

therefore the additional benefits provided by hiring one additional employee is $

841.20. It would be recommended for the business to hire additional employee as

the revenue generated is more than the charges of labor. One point is to consider

the total cost for license fee as this would increase when the number of children will

increase by hiring additional labor (Hopper & Bui, 2016).

Answer to requirement 5:

To,

Douglas and Pamela Frank

Ovillas

Texas

Date: 29th May, 2019

Subject: Evaluating feasibility analysis of renting new space and facility in existing

space

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

MANAGERIAL ACCOUNTING

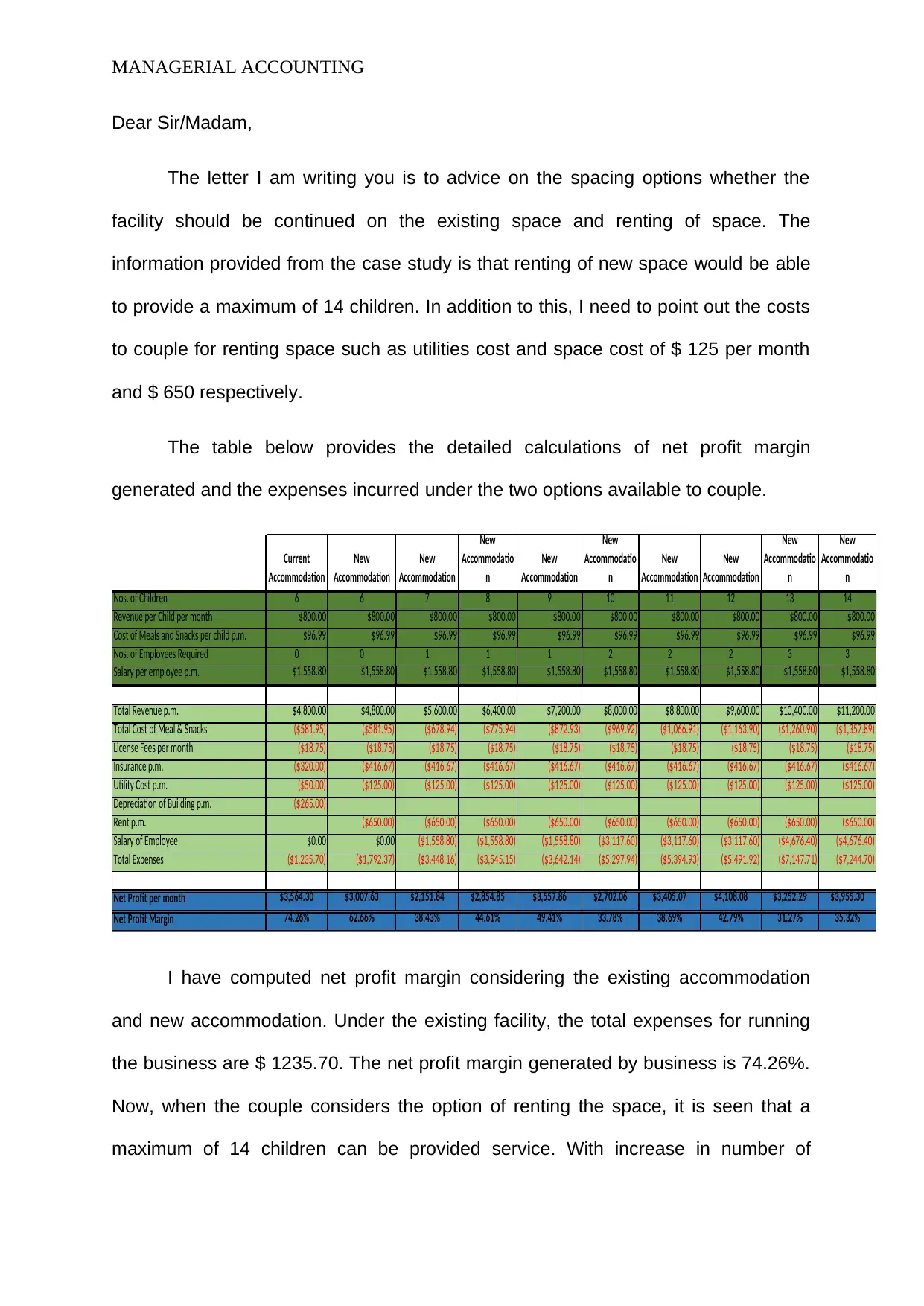

Dear Sir/Madam,

The letter I am writing you is to advice on the spacing options whether the

facility should be continued on the existing space and renting of space. The

information provided from the case study is that renting of new space would be able

to provide a maximum of 14 children. In addition to this, I need to point out the costs

to couple for renting space such as utilities cost and space cost of $ 125 per month

and $ 650 respectively.

The table below provides the detailed calculations of net profit margin

generated and the expenses incurred under the two options available to couple.

Current

Accommodation

New

Accommodation

New

Accommodation

New

Accommodatio

n

New

Accommodation

New

Accommodatio

n

New

Accommodation

New

Accommodation

New

Accommodatio

n

New

Accommodatio

n

Nos. of Children 6 6 7 8 9 10 11 12 13 14

Revenue per Child per month $800.00 $800.00 $800.00 $800.00 $800.00 $800.00 $800.00 $800.00 $800.00 $800.00

Cost of Meals and Snacks per child p.m. $96.99 $96.99 $96.99 $96.99 $96.99 $96.99 $96.99 $96.99 $96.99 $96.99

Nos. of Employees Required 0 0 1 1 1 2 2 2 3 3

Salary per employee p.m. $1,558.80 $1,558.80 $1,558.80 $1,558.80 $1,558.80 $1,558.80 $1,558.80 $1,558.80 $1,558.80 $1,558.80

Total Revenue p.m. $4,800.00 $4,800.00 $5,600.00 $6,400.00 $7,200.00 $8,000.00 $8,800.00 $9,600.00 $10,400.00 $11,200.00

Total Cost of Meal & Snacks ($581.95) ($581.95) ($678.94) ($775.94) ($872.93) ($969.92) ($1,066.91) ($1,163.90) ($1,260.90) ($1,357.89)

License Fees per month ($18.75) ($18.75) ($18.75) ($18.75) ($18.75) ($18.75) ($18.75) ($18.75) ($18.75) ($18.75)

Insurance p.m. ($320.00) ($416.67) ($416.67) ($416.67) ($416.67) ($416.67) ($416.67) ($416.67) ($416.67) ($416.67)

Utility Cost p.m. ($50.00) ($125.00) ($125.00) ($125.00) ($125.00) ($125.00) ($125.00) ($125.00) ($125.00) ($125.00)

Depreciation of Building p.m. ($265.00)

Rent p.m. ($650.00) ($650.00) ($650.00) ($650.00) ($650.00) ($650.00) ($650.00) ($650.00) ($650.00)

Salary of Employee $0.00 $0.00 ($1,558.80) ($1,558.80) ($1,558.80) ($3,117.60) ($3,117.60) ($3,117.60) ($4,676.40) ($4,676.40)

Total Expenses ($1,235.70) ($1,792.37) ($3,448.16) ($3,545.15) ($3,642.14) ($5,297.94) ($5,394.93) ($5,491.92) ($7,147.71) ($7,244.70)

Net Profit per month $3,564.30 $3,007.63 $2,151.84 $2,854.85 $3,557.86 $2,702.06 $3,405.07 $4,108.08 $3,252.29 $3,955.30

Net Profit Margin 74.26% 62.66% 38.43% 44.61% 49.41% 33.78% 38.69% 42.79% 31.27% 35.32%

I have computed net profit margin considering the existing accommodation

and new accommodation. Under the existing facility, the total expenses for running

the business are $ 1235.70. The net profit margin generated by business is 74.26%.

Now, when the couple considers the option of renting the space, it is seen that a

maximum of 14 children can be provided service. With increase in number of

Dear Sir/Madam,

The letter I am writing you is to advice on the spacing options whether the

facility should be continued on the existing space and renting of space. The

information provided from the case study is that renting of new space would be able

to provide a maximum of 14 children. In addition to this, I need to point out the costs

to couple for renting space such as utilities cost and space cost of $ 125 per month

and $ 650 respectively.

The table below provides the detailed calculations of net profit margin

generated and the expenses incurred under the two options available to couple.

Current

Accommodation

New

Accommodation

New

Accommodation

New

Accommodatio

n

New

Accommodation

New

Accommodatio

n

New

Accommodation

New

Accommodation

New

Accommodatio

n

New

Accommodatio

n

Nos. of Children 6 6 7 8 9 10 11 12 13 14

Revenue per Child per month $800.00 $800.00 $800.00 $800.00 $800.00 $800.00 $800.00 $800.00 $800.00 $800.00

Cost of Meals and Snacks per child p.m. $96.99 $96.99 $96.99 $96.99 $96.99 $96.99 $96.99 $96.99 $96.99 $96.99

Nos. of Employees Required 0 0 1 1 1 2 2 2 3 3

Salary per employee p.m. $1,558.80 $1,558.80 $1,558.80 $1,558.80 $1,558.80 $1,558.80 $1,558.80 $1,558.80 $1,558.80 $1,558.80

Total Revenue p.m. $4,800.00 $4,800.00 $5,600.00 $6,400.00 $7,200.00 $8,000.00 $8,800.00 $9,600.00 $10,400.00 $11,200.00

Total Cost of Meal & Snacks ($581.95) ($581.95) ($678.94) ($775.94) ($872.93) ($969.92) ($1,066.91) ($1,163.90) ($1,260.90) ($1,357.89)

License Fees per month ($18.75) ($18.75) ($18.75) ($18.75) ($18.75) ($18.75) ($18.75) ($18.75) ($18.75) ($18.75)

Insurance p.m. ($320.00) ($416.67) ($416.67) ($416.67) ($416.67) ($416.67) ($416.67) ($416.67) ($416.67) ($416.67)

Utility Cost p.m. ($50.00) ($125.00) ($125.00) ($125.00) ($125.00) ($125.00) ($125.00) ($125.00) ($125.00) ($125.00)

Depreciation of Building p.m. ($265.00)

Rent p.m. ($650.00) ($650.00) ($650.00) ($650.00) ($650.00) ($650.00) ($650.00) ($650.00) ($650.00)

Salary of Employee $0.00 $0.00 ($1,558.80) ($1,558.80) ($1,558.80) ($3,117.60) ($3,117.60) ($3,117.60) ($4,676.40) ($4,676.40)

Total Expenses ($1,235.70) ($1,792.37) ($3,448.16) ($3,545.15) ($3,642.14) ($5,297.94) ($5,394.93) ($5,491.92) ($7,147.71) ($7,244.70)

Net Profit per month $3,564.30 $3,007.63 $2,151.84 $2,854.85 $3,557.86 $2,702.06 $3,405.07 $4,108.08 $3,252.29 $3,955.30

Net Profit Margin 74.26% 62.66% 38.43% 44.61% 49.41% 33.78% 38.69% 42.79% 31.27% 35.32%

I have computed net profit margin considering the existing accommodation

and new accommodation. Under the existing facility, the total expenses for running

the business are $ 1235.70. The net profit margin generated by business is 74.26%.

Now, when the couple considers the option of renting the space, it is seen that a

maximum of 14 children can be provided service. With increase in number of

MANAGERIAL ACCOUNTING

children taken care of, it is observable that the total expense for the couple is

increasing continuously. This increase in total expenses is attributable to increase in

total cost of meal and snacks and increase in salary paid to employees.

Furthermore, the net profit margin is declining with increase in additional number of

children being provided service. Therefore, from the analysis of the figures, it is

inferred that it would be viable to continue running the facility in the existing space

that is they should run the business in their home. Since, it is deduced from the

analysis that the couple should run the facility at home and under existing facility, a

maximum of 6 children can be provided service (Dierynck & Labro, 2018). Thus,

from the detailed evaluation of figure, it is said that couple should serve 6 children.

Under current accommodation, couple is not required to hire additional employee.

I hope the calculations provided by me regarding the option to rent space and

running the existing facility at home would address the queries and assist you in the

decision making process.

Thanking You,

Yours sincerely

Name

[Accountant]

children taken care of, it is observable that the total expense for the couple is

increasing continuously. This increase in total expenses is attributable to increase in

total cost of meal and snacks and increase in salary paid to employees.

Furthermore, the net profit margin is declining with increase in additional number of

children being provided service. Therefore, from the analysis of the figures, it is

inferred that it would be viable to continue running the facility in the existing space

that is they should run the business in their home. Since, it is deduced from the

analysis that the couple should run the facility at home and under existing facility, a

maximum of 6 children can be provided service (Dierynck & Labro, 2018). Thus,

from the detailed evaluation of figure, it is said that couple should serve 6 children.

Under current accommodation, couple is not required to hire additional employee.

I hope the calculations provided by me regarding the option to rent space and

running the existing facility at home would address the queries and assist you in the

decision making process.

Thanking You,

Yours sincerely

Name

[Accountant]

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

MANAGERIAL ACCOUNTING

Part B:

Answer to requirement 1:

Identifying components of managerial accounting of the companies and

evaluating their relevance in the decision making process:

Management accounting can be defined as the procedure by which the

financial data such as costs are analyzed and the same is communicated to the

managers for undertaking the decisions. Basically, there are three components of

management accounting that include planning, decision making and controlling.

Controlling refers to evaluating the outcome by determining the factor such as cost

and measurement processes are within inside and outside the range. Strategy

development for enhancing the process of decision making also forms an important

components along with the planning that happens at all the level such as the plan to

maximize the profits of organization (Quattrone, 2016).

The journal article titled “Toward a new theory of innovation management: A

case study comparing Canon Inc and Apple Computer Inc” examines the

incorporation of the components of the management accounting in the product

development process at different levels. From the given article, it is observed that

both the organizations that is Apple and Canon have performed the application of the

components of management accounting in the development of Macintosh computers

and Mini copier respectively. The case of these two companies reflects upon the

Part B:

Answer to requirement 1:

Identifying components of managerial accounting of the companies and

evaluating their relevance in the decision making process:

Management accounting can be defined as the procedure by which the

financial data such as costs are analyzed and the same is communicated to the

managers for undertaking the decisions. Basically, there are three components of

management accounting that include planning, decision making and controlling.

Controlling refers to evaluating the outcome by determining the factor such as cost

and measurement processes are within inside and outside the range. Strategy

development for enhancing the process of decision making also forms an important

components along with the planning that happens at all the level such as the plan to

maximize the profits of organization (Quattrone, 2016).

The journal article titled “Toward a new theory of innovation management: A

case study comparing Canon Inc and Apple Computer Inc” examines the

incorporation of the components of the management accounting in the product

development process at different levels. From the given article, it is observed that

both the organizations that is Apple and Canon have performed the application of the

components of management accounting in the development of Macintosh computers

and Mini copier respectively. The case of these two companies reflects upon the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

MANAGERIAL ACCOUNTING

dynamics of the process of information creation and the lessons it generated for the

management.

The development of mini copier was done by reconceptualizing the entire

market of plain paper copier and for the actualization of the mini copier; the

organization formed a feasibility study team. This feasibility team comprised of

personnel from different departments such as production, technical department,

research and development, product design and marketing personnel. Cost and

reliability was the two factors that were required to be fundamentally managed by the

team and they intended to resolve the contradiction between these two facts. For

addressing the issue, a change in the concept was made by engaging the team in

heated arguments and the new concept emerged that would make copier

maintenance free (Gow et al., 2016).

Some of the management accounting components such as planning and

decision-making was also incorporated in the development of Macintosh computers

by Apple Inc. For the purpose of producing the product at lower cost, a Macintosh

group was formed that would examine the feasibility of developing an extremely low

cost computer for the people. Creation of the team resulted in emergence of new

ideas and features due to the constant and intense interaction among the team

members (Makrygiannakis & Jack, 2016). It was found that the manufacturing

managers in the team formed an integral part of the project team of development of

Macintosh.

Therefore, from the analysis of the given case of Apple and Canon, it is

inferred that the creation of team with personnel from different departments resulted

dynamics of the process of information creation and the lessons it generated for the

management.

The development of mini copier was done by reconceptualizing the entire

market of plain paper copier and for the actualization of the mini copier; the

organization formed a feasibility study team. This feasibility team comprised of

personnel from different departments such as production, technical department,

research and development, product design and marketing personnel. Cost and

reliability was the two factors that were required to be fundamentally managed by the

team and they intended to resolve the contradiction between these two facts. For

addressing the issue, a change in the concept was made by engaging the team in

heated arguments and the new concept emerged that would make copier

maintenance free (Gow et al., 2016).

Some of the management accounting components such as planning and

decision-making was also incorporated in the development of Macintosh computers

by Apple Inc. For the purpose of producing the product at lower cost, a Macintosh

group was formed that would examine the feasibility of developing an extremely low

cost computer for the people. Creation of the team resulted in emergence of new

ideas and features due to the constant and intense interaction among the team

members (Makrygiannakis & Jack, 2016). It was found that the manufacturing

managers in the team formed an integral part of the project team of development of

Macintosh.

Therefore, from the analysis of the given case of Apple and Canon, it is

inferred that the creation of team with personnel from different departments resulted

MANAGERIAL ACCOUNTING

in creating new ideas and features that contributed to the development of product by

way of innovation.

Answer to requirement 2:

Evaluating the contribution of management accounting in the process of

innovation:

The system of management accounting within organizations and its

associated components contributes to the process of innovation in the development

of products. In the current paper, it is argued that information can be regarded as the

process of creating information which helps in concretizing of the products that helps

in meeting the changing demand of people. Innovation in an organization can

emerge by breaking and challenging the staid and bureaucratic structures. The

process of innovation can be well understood when personnel working in

organization are conceptualized as creator of information rather than information

processor (Messner, 2016). The innovation in an organization has become a way

forward with the development of the techniques and concept of management

accounting as the incorporation of the techniques contributes to the development of

product in terms of the products uniqueness, technological competencies and

competitive pressures. The traditional method of management accounting that

includes the command culture and control would be eliminated by the freedom and

flexibility required in the innovation process (Trantopoulos et al., 2017).

in creating new ideas and features that contributed to the development of product by

way of innovation.

Answer to requirement 2:

Evaluating the contribution of management accounting in the process of

innovation:

The system of management accounting within organizations and its

associated components contributes to the process of innovation in the development

of products. In the current paper, it is argued that information can be regarded as the

process of creating information which helps in concretizing of the products that helps

in meeting the changing demand of people. Innovation in an organization can

emerge by breaking and challenging the staid and bureaucratic structures. The

process of innovation can be well understood when personnel working in

organization are conceptualized as creator of information rather than information

processor (Messner, 2016). The innovation in an organization has become a way

forward with the development of the techniques and concept of management

accounting as the incorporation of the techniques contributes to the development of

product in terms of the products uniqueness, technological competencies and

competitive pressures. The traditional method of management accounting that

includes the command culture and control would be eliminated by the freedom and

flexibility required in the innovation process (Trantopoulos et al., 2017).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.