Managerial Accounting: Job Order, Process, and CVP Analysis

VerifiedAdded on 2022/11/27

|12

|2739

|237

Homework Assignment

AI Summary

This managerial accounting assignment provides a thorough examination of key concepts within the field. It begins with an overview of managerial accounting, contrasting it with financial accounting, and emphasizing the importance of ethical standards. The assignment then delves into job order costing and process costing, detailing their methodologies and applications. Cost management systems, including activity-based costing and just-in-time systems, are also explored. The document further explains cost-volume-profit (CVP) analysis, variable costing, and absorption costing, highlighting their roles in decision-making. The assignment concludes with discussions on relevant information for decision-making, capital budgeting techniques, and various types of budgets. The content covers a wide array of managerial accounting topics, providing a solid foundation for understanding accounting principles and their application in business management.

Running head: MANAGERIAL ACCOUNTING

Managerial Accounting

Name of the Student

Name of the University

Author’s Note

Managerial Accounting

Name of the Student

Name of the University

Author’s Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1MANAGERIAL ACCOUNTING

Table of Contents

1. Managerial Accounting..........................................................................................................2

2. Job Order Costing..................................................................................................................3

3. Process Order Costing............................................................................................................4

4. Cost Management Systems....................................................................................................5

5. Cost Volume Profit Analysis.................................................................................................6

6. Variable Costing.....................................................................................................................6

7. Decision Making....................................................................................................................7

8. Budgets and Standard Costing...............................................................................................8

References................................................................................................................................10

Table of Contents

1. Managerial Accounting..........................................................................................................2

2. Job Order Costing..................................................................................................................3

3. Process Order Costing............................................................................................................4

4. Cost Management Systems....................................................................................................5

5. Cost Volume Profit Analysis.................................................................................................6

6. Variable Costing.....................................................................................................................6

7. Decision Making....................................................................................................................7

8. Budgets and Standard Costing...............................................................................................8

References................................................................................................................................10

2MANAGERIAL ACCOUNTING

1. Managerial Accounting

Managerial Accounting refers to the process to prepare accounts and reports that

provide the management with timely and accurate financial information for making short-

term and day-to-day business decisions. Managerial accounting is responsible for generating

weekly and monthly reports for the internal users like departmental managers and others

(Kaplan & Atkinson, 2015).

Organizational managers use managerial accounting for extracting the required

financial and statistical data of the business for the purposes of keeping records, planning,

controlling and decision-making.

The primary responsibility of the management accountants is to execute certain tasks

for ensuring financial security of the firms while managing the necessary financial matters for

ensuring the firm’s financial success. These include budgeting, tax handling, aid in strategic

management and managing assets.

The main difference is that financial accounting aims at the preparation of financial

statements of a firm for providing required financial information to the key stakeholders

where managerial accounting aims at providing the necessary financial information to the

management for the purpose of short-term decision-making. Both internal and external users

can use financial management while only internal users can use managerial accounting

(Brewer, Garrison & Noreen, 2015).

The ethical standards of management accountants include maintaining competence,

confidentially, integrity and credibility. In addition, they are needed to follow the ethical

policies and procedures of the organizations for the resolution of any ethical issue.

1. Managerial Accounting

Managerial Accounting refers to the process to prepare accounts and reports that

provide the management with timely and accurate financial information for making short-

term and day-to-day business decisions. Managerial accounting is responsible for generating

weekly and monthly reports for the internal users like departmental managers and others

(Kaplan & Atkinson, 2015).

Organizational managers use managerial accounting for extracting the required

financial and statistical data of the business for the purposes of keeping records, planning,

controlling and decision-making.

The primary responsibility of the management accountants is to execute certain tasks

for ensuring financial security of the firms while managing the necessary financial matters for

ensuring the firm’s financial success. These include budgeting, tax handling, aid in strategic

management and managing assets.

The main difference is that financial accounting aims at the preparation of financial

statements of a firm for providing required financial information to the key stakeholders

where managerial accounting aims at providing the necessary financial information to the

management for the purpose of short-term decision-making. Both internal and external users

can use financial management while only internal users can use managerial accounting

(Brewer, Garrison & Noreen, 2015).

The ethical standards of management accountants include maintaining competence,

confidentially, integrity and credibility. In addition, they are needed to follow the ethical

policies and procedures of the organizations for the resolution of any ethical issue.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3MANAGERIAL ACCOUNTING

Product Costs

Raw Materials

Direct Labour

Manufacturing

overhead

Balance Sheet

Raw Material Inventory

(Direct Materials used in

production)

Work-in-Process Inventory

(Goods completed-cost of

manufactured goods)

Finished Goods Inventory

Period Costs

Selling and

Administrative

Overheads

Income

Statement

Cost of Goods

Sold

Selling and

Administrative

Expenses

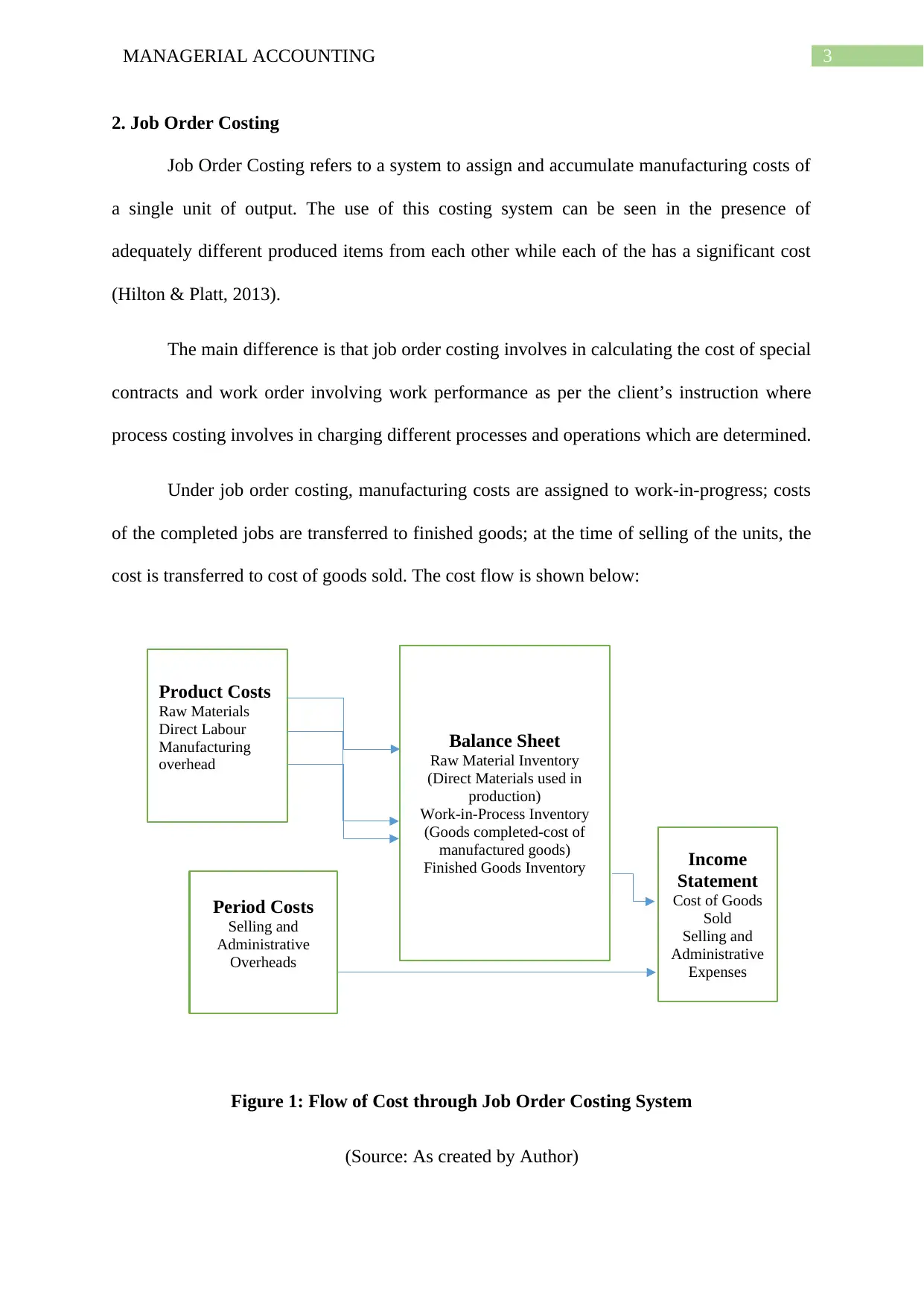

2. Job Order Costing

Job Order Costing refers to a system to assign and accumulate manufacturing costs of

a single unit of output. The use of this costing system can be seen in the presence of

adequately different produced items from each other while each of the has a significant cost

(Hilton & Platt, 2013).

The main difference is that job order costing involves in calculating the cost of special

contracts and work order involving work performance as per the client’s instruction where

process costing involves in charging different processes and operations which are determined.

Under job order costing, manufacturing costs are assigned to work-in-progress; costs

of the completed jobs are transferred to finished goods; at the time of selling of the units, the

cost is transferred to cost of goods sold. The cost flow is shown below:

Figure 1: Flow of Cost through Job Order Costing System

(Source: As created by Author)

Product Costs

Raw Materials

Direct Labour

Manufacturing

overhead

Balance Sheet

Raw Material Inventory

(Direct Materials used in

production)

Work-in-Process Inventory

(Goods completed-cost of

manufactured goods)

Finished Goods Inventory

Period Costs

Selling and

Administrative

Overheads

Income

Statement

Cost of Goods

Sold

Selling and

Administrative

Expenses

2. Job Order Costing

Job Order Costing refers to a system to assign and accumulate manufacturing costs of

a single unit of output. The use of this costing system can be seen in the presence of

adequately different produced items from each other while each of the has a significant cost

(Hilton & Platt, 2013).

The main difference is that job order costing involves in calculating the cost of special

contracts and work order involving work performance as per the client’s instruction where

process costing involves in charging different processes and operations which are determined.

Under job order costing, manufacturing costs are assigned to work-in-progress; costs

of the completed jobs are transferred to finished goods; at the time of selling of the units, the

cost is transferred to cost of goods sold. The cost flow is shown below:

Figure 1: Flow of Cost through Job Order Costing System

(Source: As created by Author)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4MANAGERIAL ACCOUNTING

Direct Materials

Direct Labour

Manufacturing

Overhead

Processing

Department Finished Goods

Costs of Goods

Sold

Manufacturing overheads are the indirect factory-associated costs and these re

incurred at the time of manufacturing products. This is applied by dividing the total overhead

by the number of direct labour hours (Novák & Popesko, 2014).

The main reason for adjusting the manufacturing overhead account at the end of the

period is to avoid the over application or under application of this.

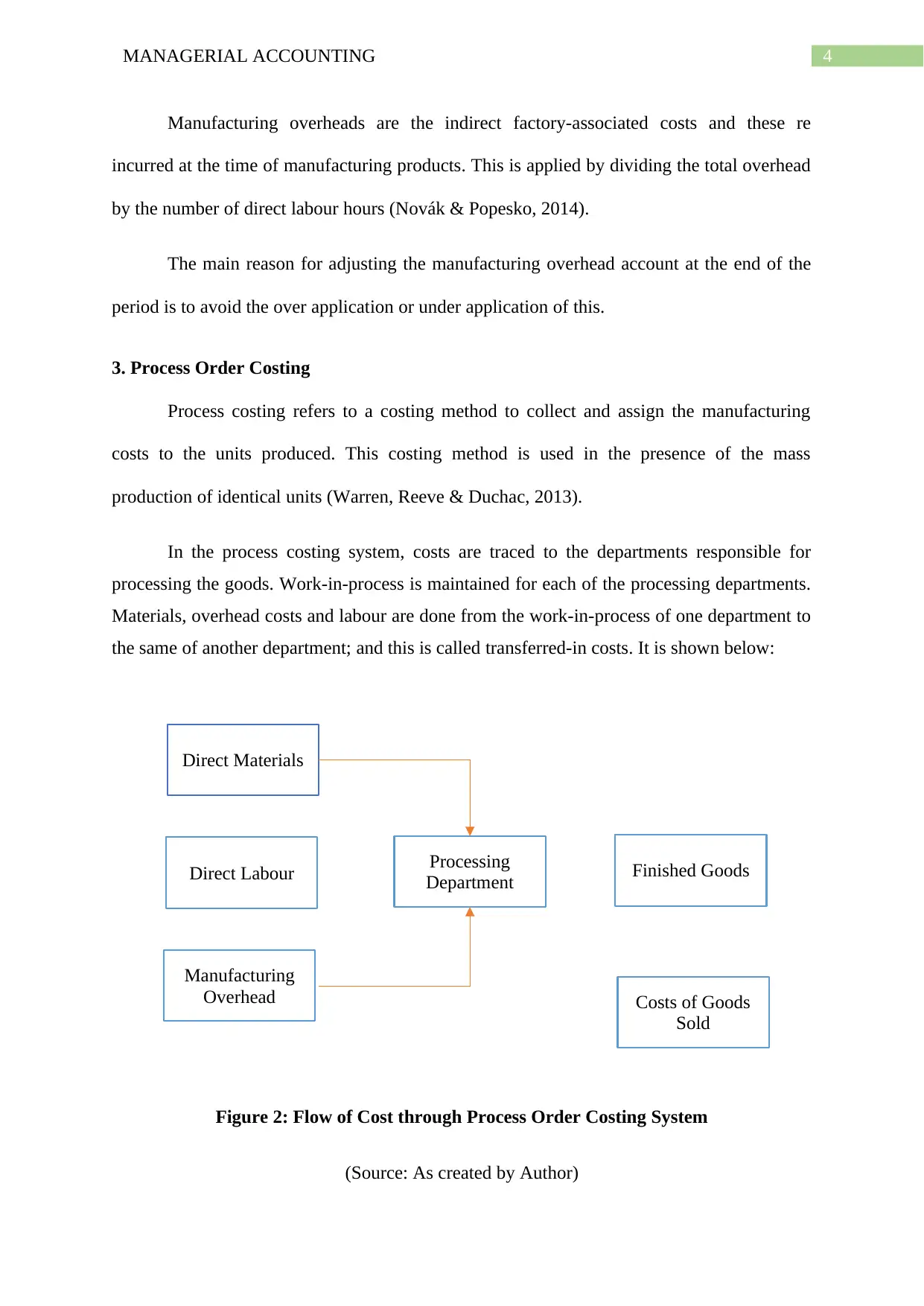

3. Process Order Costing

Process costing refers to a costing method to collect and assign the manufacturing

costs to the units produced. This costing method is used in the presence of the mass

production of identical units (Warren, Reeve & Duchac, 2013).

In the process costing system, costs are traced to the departments responsible for

processing the goods. Work-in-process is maintained for each of the processing departments.

Materials, overhead costs and labour are done from the work-in-process of one department to

the same of another department; and this is called transferred-in costs. It is shown below:

Figure 2: Flow of Cost through Process Order Costing System

(Source: As created by Author)

Direct Materials

Direct Labour

Manufacturing

Overhead

Processing

Department Finished Goods

Costs of Goods

Sold

Manufacturing overheads are the indirect factory-associated costs and these re

incurred at the time of manufacturing products. This is applied by dividing the total overhead

by the number of direct labour hours (Novák & Popesko, 2014).

The main reason for adjusting the manufacturing overhead account at the end of the

period is to avoid the over application or under application of this.

3. Process Order Costing

Process costing refers to a costing method to collect and assign the manufacturing

costs to the units produced. This costing method is used in the presence of the mass

production of identical units (Warren, Reeve & Duchac, 2013).

In the process costing system, costs are traced to the departments responsible for

processing the goods. Work-in-process is maintained for each of the processing departments.

Materials, overhead costs and labour are done from the work-in-process of one department to

the same of another department; and this is called transferred-in costs. It is shown below:

Figure 2: Flow of Cost through Process Order Costing System

(Source: As created by Author)

5MANAGERIAL ACCOUNTING

Equivalent units of production refers to an item’s number of completed units that a

firm could have produced theoretically, given the amount of incurred direct labour, direct

materials and manufacturing overhead costs during the period. It is calculated with the help

of the following formula:

Equivalent Units of Production = Number of Partially Completed Units × Percentage of

Completion

Production report is considered as a very useful tool for the organizational managers

because it assists them in making informed business decisions about the products. Production

reports provide the managers with the required financial and costing information that is

needed for the purpose of decision-making (Needles, Powers & Crosson, 2013).

4. Cost Management Systems

In case of the production of one unit, it is easy to assign costs. However, it is not easy

to assign overhead cost like utilities and labour to one unit and thus, the prices are allocated.

It is not possible to know overhead costs and these calculations are needed to be projected.

Based on these estimation and projection, allocation is estimated. Accurate projection

depends on accurate allocation.

Activity based costing assists in the allocation of costs to each produced products and

the activity based management utilizes this allocation for making manufacturing as well as

cost decisions (Cooper, 2017). Activity based management assists in analysing the

fluctuations in materials, labour costs and overhead costs for adjusting pricing. This provides

the scope in adjusting in costs for the purpose of effective decision-making.

Just in Time system helps in manufacturing products for meeting demand in order to

keep the inventory and overhead costs in minimum level and to ensure there is not any

storage of materials and the overheads are required only for manufacturing the products

Equivalent units of production refers to an item’s number of completed units that a

firm could have produced theoretically, given the amount of incurred direct labour, direct

materials and manufacturing overhead costs during the period. It is calculated with the help

of the following formula:

Equivalent Units of Production = Number of Partially Completed Units × Percentage of

Completion

Production report is considered as a very useful tool for the organizational managers

because it assists them in making informed business decisions about the products. Production

reports provide the managers with the required financial and costing information that is

needed for the purpose of decision-making (Needles, Powers & Crosson, 2013).

4. Cost Management Systems

In case of the production of one unit, it is easy to assign costs. However, it is not easy

to assign overhead cost like utilities and labour to one unit and thus, the prices are allocated.

It is not possible to know overhead costs and these calculations are needed to be projected.

Based on these estimation and projection, allocation is estimated. Accurate projection

depends on accurate allocation.

Activity based costing assists in the allocation of costs to each produced products and

the activity based management utilizes this allocation for making manufacturing as well as

cost decisions (Cooper, 2017). Activity based management assists in analysing the

fluctuations in materials, labour costs and overhead costs for adjusting pricing. This provides

the scope in adjusting in costs for the purpose of effective decision-making.

Just in Time system helps in manufacturing products for meeting demand in order to

keep the inventory and overhead costs in minimum level and to ensure there is not any

storage of materials and the overheads are required only for manufacturing the products

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6MANAGERIAL ACCOUNTING

(Aradhye & Kallurkar, 2014). However, the quality management system helps in dividing

costs into certain categories; they are appraisal and internal as well as external failure

prevention. Unlike activity based costing, this needs major investment for the reduction of

costly errors in future.

5. Cost Volume Profit Analysis

There are three kinds of costs; they are fixed cost and variable cost. Fixed costs are

those costs that do not change with the change in activity level. Variable costs change in

direct proportion with the production level; it implies total variable costs increases and

decrease due to the increase and decrease in produced units respectively (Drury, 2013).

Contribution margin can be defined as an amount or ration of revenue and this can be

obtained by subtracting the variable expenses from the revenue. Contribution margin plays a

crucial role in computing operating income because operating income is obtained by

subtracting the total fixed costs from the contribution margin since both of their presence can

be seen in the contribution income statement.

The Cost Volume Profit Analysis refers to a planning mechanism used by the

management for predicting the future volume of activity, incurred costs, sales made and

received profit. Organizational managers use the cost volume profit analysis for making

informed decision regarding products or services sold by them. It assists the managers in

breaking down the costs into fixed and variables and this provides an effective insight into

their product’s or service’s profitability (Abdullahi et al., 2017). This helps the managers in

large manner.

6. Variable Costing

Both variable costing and absorption costing are costing methods used by large

number of companies. The inclusion of all costs including production related fixed costs can

(Aradhye & Kallurkar, 2014). However, the quality management system helps in dividing

costs into certain categories; they are appraisal and internal as well as external failure

prevention. Unlike activity based costing, this needs major investment for the reduction of

costly errors in future.

5. Cost Volume Profit Analysis

There are three kinds of costs; they are fixed cost and variable cost. Fixed costs are

those costs that do not change with the change in activity level. Variable costs change in

direct proportion with the production level; it implies total variable costs increases and

decrease due to the increase and decrease in produced units respectively (Drury, 2013).

Contribution margin can be defined as an amount or ration of revenue and this can be

obtained by subtracting the variable expenses from the revenue. Contribution margin plays a

crucial role in computing operating income because operating income is obtained by

subtracting the total fixed costs from the contribution margin since both of their presence can

be seen in the contribution income statement.

The Cost Volume Profit Analysis refers to a planning mechanism used by the

management for predicting the future volume of activity, incurred costs, sales made and

received profit. Organizational managers use the cost volume profit analysis for making

informed decision regarding products or services sold by them. It assists the managers in

breaking down the costs into fixed and variables and this provides an effective insight into

their product’s or service’s profitability (Abdullahi et al., 2017). This helps the managers in

large manner.

6. Variable Costing

Both variable costing and absorption costing are costing methods used by large

number of companies. The inclusion of all costs including production related fixed costs can

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7MANAGERIAL ACCOUNTING

be seen in absorption costing while the inclusion of only variable costs can be seen in

variable costing. For this reason, the companies using variable costing maintains separate

fixed-cost operating expenses from the production costs. Absorption costing involves the

allocation of fixed overhead costs leads to the combination of all fixed overhead costs as a

single line charged against the net income. However, variable costing considers only those

expenses which are directly related to the production (Drury, 2013).

Manufacturing companies involve in manufacturing and selling products; thus they

have inventory. For this reason, variable costing allocates the variable costs to the inventory;

and thus, all overhead costs are charged to the incurred expenses while the variable overhead

and direct material costs are charged to the inventory. However, in case of a service

company, there is not any selling or producing any product. For this reason, no costs are

allocated to the inventory. Thus, a service company can report as well as analyse the

contribution margin as the difference between revenue and variable costs. This is the main

difference of the use of variable costing in a manufacturing company and a service company

(Joshi et al., 2013).

7. Decision Making

Managers use the relevant information for decision-making and relevant information

is considered as expected future data and it differs among the alternatives. In addition, the

relevant non-financial information also has crucial role in short-term decision making.

Relevant information provides the managers insight about the performance of the products

which is helpful in decision-making. Pricing is considered as another crucial aspect having

impact on the short-term decision-making process. Target pricing helps the managers in

determining the target full product cost by subtracting the desired profit from target pricing.

This helps in managers in deciding between the strategies of price taker and price setter.

be seen in absorption costing while the inclusion of only variable costs can be seen in

variable costing. For this reason, the companies using variable costing maintains separate

fixed-cost operating expenses from the production costs. Absorption costing involves the

allocation of fixed overhead costs leads to the combination of all fixed overhead costs as a

single line charged against the net income. However, variable costing considers only those

expenses which are directly related to the production (Drury, 2013).

Manufacturing companies involve in manufacturing and selling products; thus they

have inventory. For this reason, variable costing allocates the variable costs to the inventory;

and thus, all overhead costs are charged to the incurred expenses while the variable overhead

and direct material costs are charged to the inventory. However, in case of a service

company, there is not any selling or producing any product. For this reason, no costs are

allocated to the inventory. Thus, a service company can report as well as analyse the

contribution margin as the difference between revenue and variable costs. This is the main

difference of the use of variable costing in a manufacturing company and a service company

(Joshi et al., 2013).

7. Decision Making

Managers use the relevant information for decision-making and relevant information

is considered as expected future data and it differs among the alternatives. In addition, the

relevant non-financial information also has crucial role in short-term decision making.

Relevant information provides the managers insight about the performance of the products

which is helpful in decision-making. Pricing is considered as another crucial aspect having

impact on the short-term decision-making process. Target pricing helps the managers in

determining the target full product cost by subtracting the desired profit from target pricing.

This helps in managers in deciding between the strategies of price taker and price setter.

8MANAGERIAL ACCOUNTING

Capital budgeting is considered as a planning mechanism that is utilized for

determining the worth of an organization’s long-term investment and this has a great

significant on selection of capital projects. The capital budgeting techniques are discussed

below.

Payback Method – Payback period is considered as the needed time to earn back the

investment amount in an asset from its net cash flows. This refers to a simple method for

evaluating the risk connected to a proposed project (Lane & Rosewall, 2015).

Accounting Rate of Return (ARR) Method – ARR refers to an investment’s rate of return

in percentage as compared to the cost of initial investment. It divides the average revenue of

an asset by the initial investment for getting the rate of return.

Discounted Cash Flow (DCF) Method – DCF is considered as a valuation method that is

utilized in order to estimate the value of an investment on the basis of future cash flows

(Mellichamp, 2013).

8. Budgets and Standard Costing

The types of budgets are discussed below:

Master Budget – A master budget refers to the total of a firm’s budgets including fund

allocation to different activities of the business.

Operating Budget – Operating budget involves the costs associated in the operational

activities which are production cost, manufacturing cost, overhead cost, administrative cost,

labour cost and others; and the sales are considered as the income flow.

Financial Budget – This is the kind of budget that makes it sure the availability of correct

types of funds for the business.

Capital budgeting is considered as a planning mechanism that is utilized for

determining the worth of an organization’s long-term investment and this has a great

significant on selection of capital projects. The capital budgeting techniques are discussed

below.

Payback Method – Payback period is considered as the needed time to earn back the

investment amount in an asset from its net cash flows. This refers to a simple method for

evaluating the risk connected to a proposed project (Lane & Rosewall, 2015).

Accounting Rate of Return (ARR) Method – ARR refers to an investment’s rate of return

in percentage as compared to the cost of initial investment. It divides the average revenue of

an asset by the initial investment for getting the rate of return.

Discounted Cash Flow (DCF) Method – DCF is considered as a valuation method that is

utilized in order to estimate the value of an investment on the basis of future cash flows

(Mellichamp, 2013).

8. Budgets and Standard Costing

The types of budgets are discussed below:

Master Budget – A master budget refers to the total of a firm’s budgets including fund

allocation to different activities of the business.

Operating Budget – Operating budget involves the costs associated in the operational

activities which are production cost, manufacturing cost, overhead cost, administrative cost,

labour cost and others; and the sales are considered as the income flow.

Financial Budget – This is the kind of budget that makes it sure the availability of correct

types of funds for the business.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9MANAGERIAL ACCOUNTING

Cash Flow Budget – This budget helps in determining whether the company is dealing with

the accounts payable and receivable in timely manner.

Static Budget – This budget remains the same even after alteration in the factors affecting

the preparation of budget (Miller, 2018).

In a manufacturing company, an operating budget is prepared by preparing the

budgets for sales, operating costs, income and cash flows. Both the short and long-term

projects are considered for the preparation of this budget. In the same company, the

preparation of financial budgets needs to consider the projection of all the future financial

income and expenses of the same company. This help in preparing these budgets.

A budget is considered as a financial plan concerning the revenues and costs of a firm

which provides the required co-ordination and direction for controlling the business activities

so that business objective can be achieved. Standard cost is considered as a predetermined

measure of what a cost should be. This helps in controlling the costs while ensuring the

achievement of business goals.

The determination of variance is done through differentiating between the standard

cost and actual cost. The use of this variance can be seen in monitoring the incurred cost by a

business.

Cash Flow Budget – This budget helps in determining whether the company is dealing with

the accounts payable and receivable in timely manner.

Static Budget – This budget remains the same even after alteration in the factors affecting

the preparation of budget (Miller, 2018).

In a manufacturing company, an operating budget is prepared by preparing the

budgets for sales, operating costs, income and cash flows. Both the short and long-term

projects are considered for the preparation of this budget. In the same company, the

preparation of financial budgets needs to consider the projection of all the future financial

income and expenses of the same company. This help in preparing these budgets.

A budget is considered as a financial plan concerning the revenues and costs of a firm

which provides the required co-ordination and direction for controlling the business activities

so that business objective can be achieved. Standard cost is considered as a predetermined

measure of what a cost should be. This helps in controlling the costs while ensuring the

achievement of business goals.

The determination of variance is done through differentiating between the standard

cost and actual cost. The use of this variance can be seen in monitoring the incurred cost by a

business.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10MANAGERIAL ACCOUNTING

References

Abdullahi, S. R., Bello, S., Mukhtar, I. S., & Musa, M. H. (2017). Cost-Volume-Profit

Analysis as a Management Tool for Decision Making In Small Business Enterprise

within Bayero University, Kano. IOSR Journal of Business and Management (IOSR-

JBM), 19(2), 40-45.

Aradhye, A. S., & Kallurkar, S. P. (2014). A case study of just-in-time system in service

industry. Procedia Engineering, 97, 2232-2237.

Brewer, P. C., Garrison, R. H., & Noreen, E. W. (2015). Introduction to managerial

accounting. McGraw-Hill Education.

Cooper, R. (2017). Target costing and value engineering. Routledge.

Drury, C. (2013). Costing: an introduction. Springer.

DRURY, C. M. (2013). Management and cost accounting. Springer.

Hilton, R. W., & Platt, D. E. (2013). Managerial accounting: creating value in a dynamic

business environment. McGraw-Hill Education.

Joshi, D., Nepal, B., Rathore, A. P. S., & Sharma, D. (2013). On supply chain

competitiveness of Indian automotive component manufacturing

industry. International Journal of Production Economics, 143(1), 151-161.

Kaplan, R. S., & Atkinson, A. A. (2015). Advanced management accounting. PHI Learning.

Lane, K., & Rosewall, T. (2015). Firms’ investment decisions and interest rates. Firms’

Investment Decisions and Interest Rates 1 Why Is Wage Growth So Low? 9

Developments in Thermal Coal Markets 19 Potential Growth and Rebalancing in

China 29 Banking Fees in Australia 39, 1.

References

Abdullahi, S. R., Bello, S., Mukhtar, I. S., & Musa, M. H. (2017). Cost-Volume-Profit

Analysis as a Management Tool for Decision Making In Small Business Enterprise

within Bayero University, Kano. IOSR Journal of Business and Management (IOSR-

JBM), 19(2), 40-45.

Aradhye, A. S., & Kallurkar, S. P. (2014). A case study of just-in-time system in service

industry. Procedia Engineering, 97, 2232-2237.

Brewer, P. C., Garrison, R. H., & Noreen, E. W. (2015). Introduction to managerial

accounting. McGraw-Hill Education.

Cooper, R. (2017). Target costing and value engineering. Routledge.

Drury, C. (2013). Costing: an introduction. Springer.

DRURY, C. M. (2013). Management and cost accounting. Springer.

Hilton, R. W., & Platt, D. E. (2013). Managerial accounting: creating value in a dynamic

business environment. McGraw-Hill Education.

Joshi, D., Nepal, B., Rathore, A. P. S., & Sharma, D. (2013). On supply chain

competitiveness of Indian automotive component manufacturing

industry. International Journal of Production Economics, 143(1), 151-161.

Kaplan, R. S., & Atkinson, A. A. (2015). Advanced management accounting. PHI Learning.

Lane, K., & Rosewall, T. (2015). Firms’ investment decisions and interest rates. Firms’

Investment Decisions and Interest Rates 1 Why Is Wage Growth So Low? 9

Developments in Thermal Coal Markets 19 Potential Growth and Rebalancing in

China 29 Banking Fees in Australia 39, 1.

11MANAGERIAL ACCOUNTING

Mellichamp, D. A. (2013). New discounted cash flow method: Estimating plant profitability

at the conceptual design level while compensating for business

risk/uncertainty. Computers & Chemical Engineering, 48, 251-263.

Miller, G. (2018). Performance based budgeting. Routledge.

Needles, B. E., Powers, M., & Crosson, S. V. (2013). Principles of accounting. Cengage

Learning.

Novák, P., & Popesko, B. (2014). Cost variability and cost behaviour in manufacturing

enterprises. Economics and Sociology.

Warren, C., Reeve, J. M., & Duchac, J. (2013). Financial & managerial accounting. Cengage

learning.

Mellichamp, D. A. (2013). New discounted cash flow method: Estimating plant profitability

at the conceptual design level while compensating for business

risk/uncertainty. Computers & Chemical Engineering, 48, 251-263.

Miller, G. (2018). Performance based budgeting. Routledge.

Needles, B. E., Powers, M., & Crosson, S. V. (2013). Principles of accounting. Cengage

Learning.

Novák, P., & Popesko, B. (2014). Cost variability and cost behaviour in manufacturing

enterprises. Economics and Sociology.

Warren, C., Reeve, J. M., & Duchac, J. (2013). Financial & managerial accounting. Cengage

learning.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.