HI5017: Managerial Accounting Assignment on Cost Concepts and Analysis

VerifiedAdded on 2022/11/26

|17

|4100

|99

Homework Assignment

AI Summary

This managerial accounting assignment presents a detailed analysis of cost concepts, decision-making processes, and the role of management accounting in innovation. Part A focuses on a childcare business, examining fixed, variable, and semi-variable costs, relevant versus irrelevant information for purchasing decisions, and a cost-benefit analysis of different laundering options and hiring additional employees. A letter to a business owner is included, offering advice on whether to rent space or use their existing home for childcare. Part B explores the components of a management accounting system using case studies of Apple Inc. and Canon Inc., emphasizing the importance of innovation and how managerial accounting supports strategic decision-making. The assignment also includes a discussion of lessons learned from an article on innovation management and its implications for management accountants, providing a comprehensive overview of managerial accounting principles and their practical application.

Running head: MANAGERIAL ACCOUNTING

Managerial accounting

Name of the student

Name of the university

Student ID

Author note

Managerial accounting

Name of the student

Name of the university

Student ID

Author note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

MANAGERIAL ACCOUNTING

Table of Contents

Part A:........................................................................................................................................2

Answer to requirement 1:.......................................................................................................2

Answer to requirement 2:.......................................................................................................3

Answer to requirement 3:.......................................................................................................3

Answer to requirement 4:.......................................................................................................5

Answer to requirement 5:.......................................................................................................6

Part B:........................................................................................................................................8

Answer to requirement 1:.......................................................................................................8

Identifying the management accounting system components using the examples

from the case study:................................................................................................................8

Answer to requirement 2:.....................................................................................................11

Contribution of management accounting to innovation process:...................................11

Answer to requirement 3:.....................................................................................................12

Lessons learned from the article and its importance to management accountants:. .12

References and Bibliography list:.......................................................................................14

Table of Contents

Part A:........................................................................................................................................2

Answer to requirement 1:.......................................................................................................2

Answer to requirement 2:.......................................................................................................3

Answer to requirement 3:.......................................................................................................3

Answer to requirement 4:.......................................................................................................5

Answer to requirement 5:.......................................................................................................6

Part B:........................................................................................................................................8

Answer to requirement 1:.......................................................................................................8

Identifying the management accounting system components using the examples

from the case study:................................................................................................................8

Answer to requirement 2:.....................................................................................................11

Contribution of management accounting to innovation process:...................................11

Answer to requirement 3:.....................................................................................................12

Lessons learned from the article and its importance to management accountants:. .12

References and Bibliography list:.......................................................................................14

MANAGERIAL ACCOUNTING

Part A:

Answer to requirement 1:

The case study presented here is about the business of child care that is

owned by a couple who uses their own home for providing services. The costs

involved for running the child care business composed of fixed cost, variable cost

and semi variable costs. Fixed costs are the cost that is incurred irrespective of the

level of production or the service provided and hence it remains fixed. These are the

fixed expenses which the business are required to meet to continue running the

business (Ionescu 2017). Some of the fixed costs that are incurred by the child care

business comprise of insurance cost and the license fee paid by the couple to state.

The couple is required to pay a license fee to take care of maximum six child is $

225 and annual cost incurred for insurance of amount $ 3480 that is charged

annually. The fee paid for license is fixed when maximum of six children are served

and this would increase when there is an increment in the total number of children

that are taken care.

Variable costs are the costs that vary with the variation in level of output and

services provided. There will be change in the variable cost with the increase or

decrease in the service provided or output produced. The child care business has

some variable cost such as total salary payable to employees and utility cost for

running the business (Butler and Ghosh 2015). Therefore, an increase in number of

children taken care would increase the variable cost incurred by child care business.

Semi variable cost are the costs that remains fixed for a particular time period

and thereby it changes with change in level of services provided ( Lawson et al.

Part A:

Answer to requirement 1:

The case study presented here is about the business of child care that is

owned by a couple who uses their own home for providing services. The costs

involved for running the child care business composed of fixed cost, variable cost

and semi variable costs. Fixed costs are the cost that is incurred irrespective of the

level of production or the service provided and hence it remains fixed. These are the

fixed expenses which the business are required to meet to continue running the

business (Ionescu 2017). Some of the fixed costs that are incurred by the child care

business comprise of insurance cost and the license fee paid by the couple to state.

The couple is required to pay a license fee to take care of maximum six child is $

225 and annual cost incurred for insurance of amount $ 3480 that is charged

annually. The fee paid for license is fixed when maximum of six children are served

and this would increase when there is an increment in the total number of children

that are taken care.

Variable costs are the costs that vary with the variation in level of output and

services provided. There will be change in the variable cost with the increase or

decrease in the service provided or output produced. The child care business has

some variable cost such as total salary payable to employees and utility cost for

running the business (Butler and Ghosh 2015). Therefore, an increase in number of

children taken care would increase the variable cost incurred by child care business.

Semi variable cost are the costs that remains fixed for a particular time period

and thereby it changes with change in level of services provided ( Lawson et al.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

MANAGERIAL ACCOUNTING

2015). Therefore it composed of both fixed and variable costs. The child care

business also incurs some semi variable cost such as cost of snack and meal per

day at the amount of $ 3.20. Such cost also includes cost of energy for running dryer

and washer that would increase by $ 145 and $ 120 per year. Hence, the case study

presents three different types of costs.

Answer to requirement 2:

The information that forms the basis of decision to purchase the appliances is

to consider different types of cost that would be required to incur when purchasing

the appliances. Such cost includes the initial investment that is required to be made

by the couple which comprise of cost of installation, cost of dryer and washer and

delivery charges. In addition to this, it is also required to account for the operating

expenses such as travelling charge, laundering charge and cost for supplying the

laundry and energy cost for running the dryer and washer. On other hand, the

information that is not relevant to the decision of purchasing the appliances is the

cost of old appliances and the payment of annual fees to the state (Apostolou et al.

2018. Therefore, the relevant information for purchasing the appliances is associated

with the cost of running dryer and washer along with the depreciation factor which

should also be accounted for.

Answer to requirement 3:

For laundering the clothes, couple has three options and the option incurring

the minimal outflow of cost and annual expenses would be the feasible option for

laundering the clothes. The first option available to the couple is the rental service

from dry cleaning and laundry service provider. The total cost outflow under this

option is $ 624 and the total expense incorporate only operating expense and there

2015). Therefore it composed of both fixed and variable costs. The child care

business also incurs some semi variable cost such as cost of snack and meal per

day at the amount of $ 3.20. Such cost also includes cost of energy for running dryer

and washer that would increase by $ 145 and $ 120 per year. Hence, the case study

presents three different types of costs.

Answer to requirement 2:

The information that forms the basis of decision to purchase the appliances is

to consider different types of cost that would be required to incur when purchasing

the appliances. Such cost includes the initial investment that is required to be made

by the couple which comprise of cost of installation, cost of dryer and washer and

delivery charges. In addition to this, it is also required to account for the operating

expenses such as travelling charge, laundering charge and cost for supplying the

laundry and energy cost for running the dryer and washer. On other hand, the

information that is not relevant to the decision of purchasing the appliances is the

cost of old appliances and the payment of annual fees to the state (Apostolou et al.

2018. Therefore, the relevant information for purchasing the appliances is associated

with the cost of running dryer and washer along with the depreciation factor which

should also be accounted for.

Answer to requirement 3:

For laundering the clothes, couple has three options and the option incurring

the minimal outflow of cost and annual expenses would be the feasible option for

laundering the clothes. The first option available to the couple is the rental service

from dry cleaning and laundry service provider. The total cost outflow under this

option is $ 624 and the total expense incorporate only operating expense and there

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

MANAGERIAL ACCOUNTING

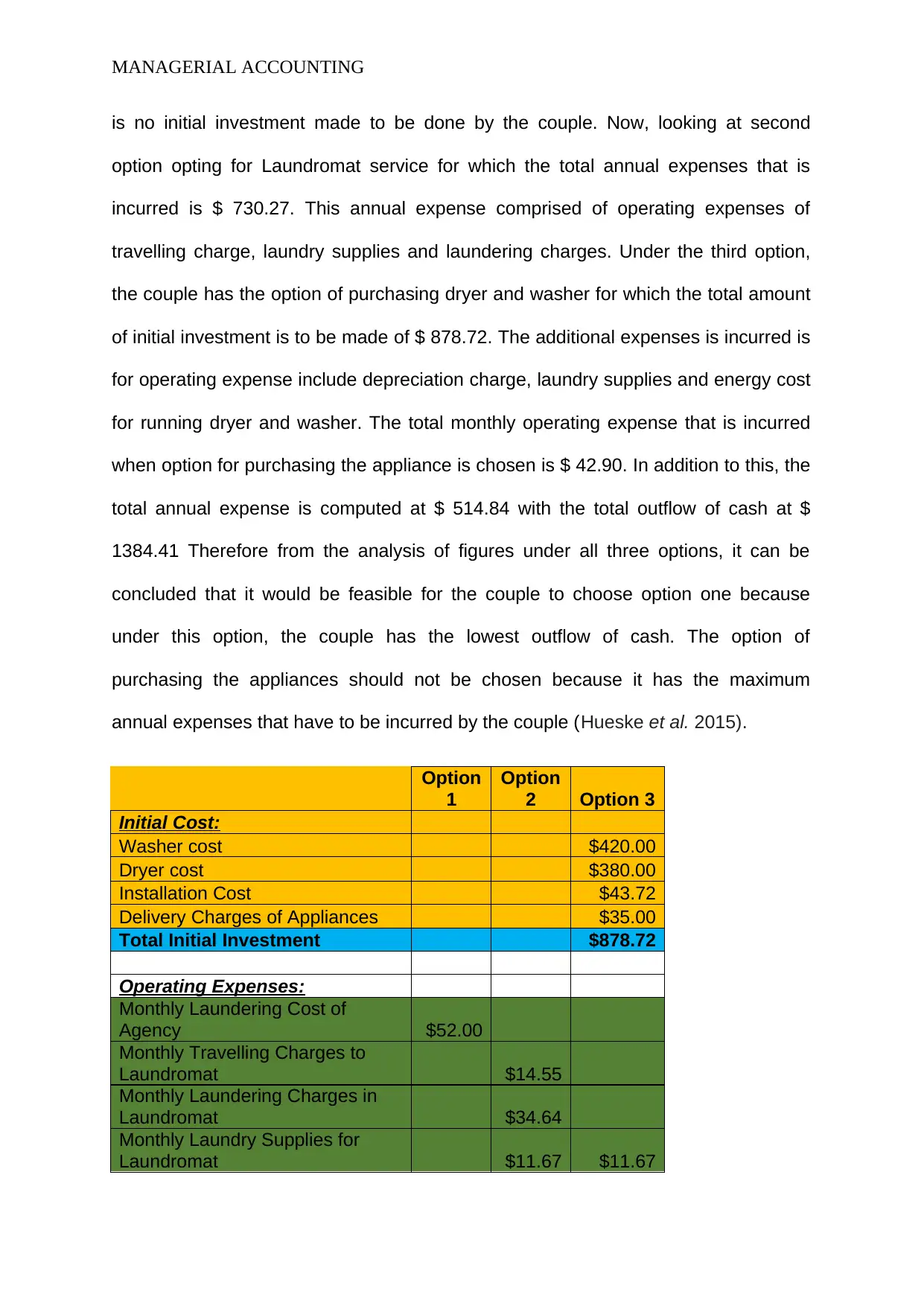

is no initial investment made to be done by the couple. Now, looking at second

option opting for Laundromat service for which the total annual expenses that is

incurred is $ 730.27. This annual expense comprised of operating expenses of

travelling charge, laundry supplies and laundering charges. Under the third option,

the couple has the option of purchasing dryer and washer for which the total amount

of initial investment is to be made of $ 878.72. The additional expenses is incurred is

for operating expense include depreciation charge, laundry supplies and energy cost

for running dryer and washer. The total monthly operating expense that is incurred

when option for purchasing the appliance is chosen is $ 42.90. In addition to this, the

total annual expense is computed at $ 514.84 with the total outflow of cash at $

1384.41 Therefore from the analysis of figures under all three options, it can be

concluded that it would be feasible for the couple to choose option one because

under this option, the couple has the lowest outflow of cash. The option of

purchasing the appliances should not be chosen because it has the maximum

annual expenses that have to be incurred by the couple (Hueske et al. 2015).

Option

1

Option

2 Option 3

Initial Cost:

Washer cost $420.00

Dryer cost $380.00

Installation Cost $43.72

Delivery Charges of Appliances $35.00

Total Initial Investment $878.72

Operating Expenses:

Monthly Laundering Cost of

Agency $52.00

Monthly Travelling Charges to

Laundromat $14.55

Monthly Laundering Charges in

Laundromat $34.64

Monthly Laundry Supplies for

Laundromat $11.67 $11.67

is no initial investment made to be done by the couple. Now, looking at second

option opting for Laundromat service for which the total annual expenses that is

incurred is $ 730.27. This annual expense comprised of operating expenses of

travelling charge, laundry supplies and laundering charges. Under the third option,

the couple has the option of purchasing dryer and washer for which the total amount

of initial investment is to be made of $ 878.72. The additional expenses is incurred is

for operating expense include depreciation charge, laundry supplies and energy cost

for running dryer and washer. The total monthly operating expense that is incurred

when option for purchasing the appliance is chosen is $ 42.90. In addition to this, the

total annual expense is computed at $ 514.84 with the total outflow of cash at $

1384.41 Therefore from the analysis of figures under all three options, it can be

concluded that it would be feasible for the couple to choose option one because

under this option, the couple has the lowest outflow of cash. The option of

purchasing the appliances should not be chosen because it has the maximum

annual expenses that have to be incurred by the couple (Hueske et al. 2015).

Option

1

Option

2 Option 3

Initial Cost:

Washer cost $420.00

Dryer cost $380.00

Installation Cost $43.72

Delivery Charges of Appliances $35.00

Total Initial Investment $878.72

Operating Expenses:

Monthly Laundering Cost of

Agency $52.00

Monthly Travelling Charges to

Laundromat $14.55

Monthly Laundering Charges in

Laundromat $34.64

Monthly Laundry Supplies for

Laundromat $11.67 $11.67

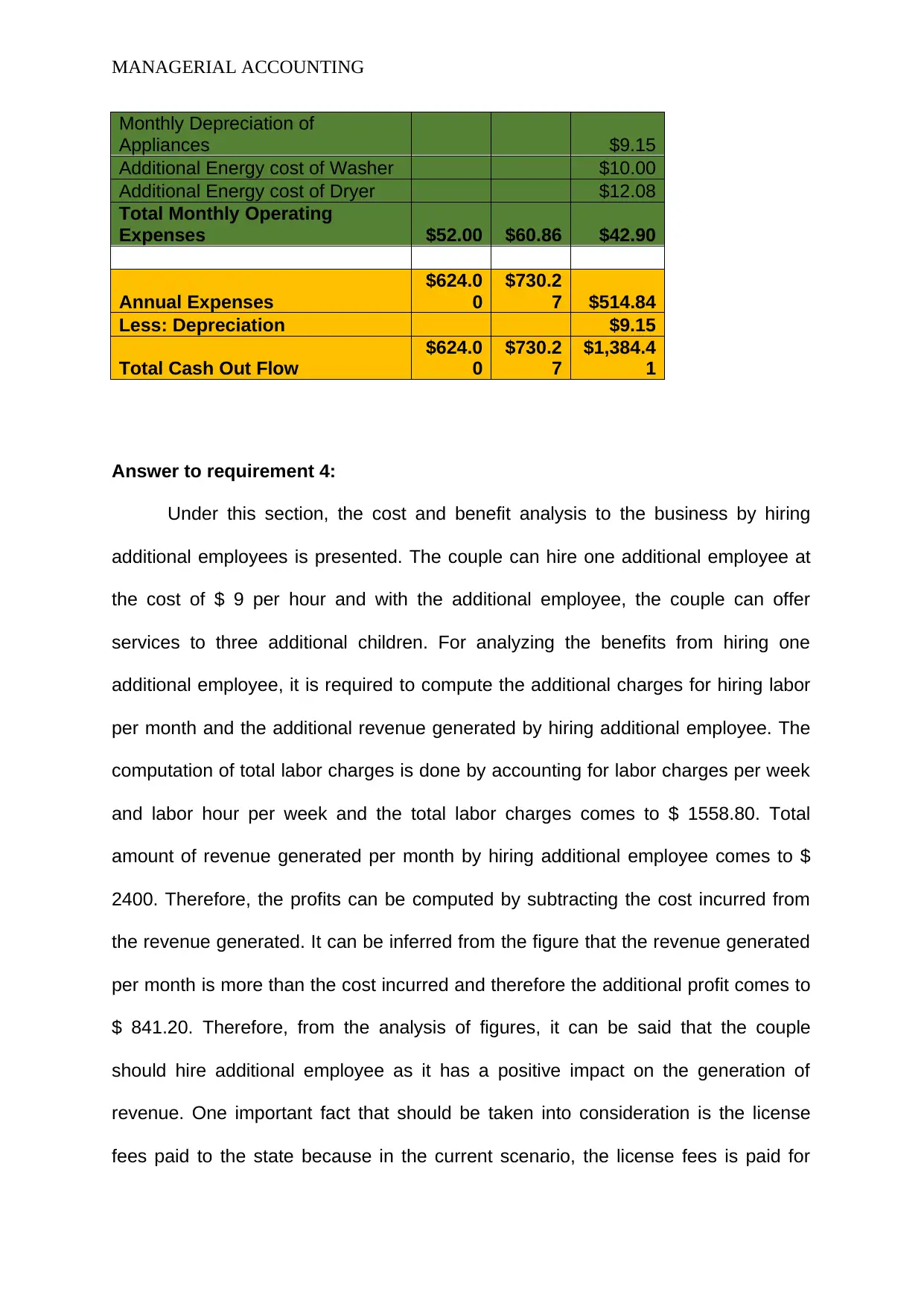

MANAGERIAL ACCOUNTING

Monthly Depreciation of

Appliances $9.15

Additional Energy cost of Washer $10.00

Additional Energy cost of Dryer $12.08

Total Monthly Operating

Expenses $52.00 $60.86 $42.90

Annual Expenses

$624.0

0

$730.2

7 $514.84

Less: Depreciation $9.15

Total Cash Out Flow

$624.0

0

$730.2

7

$1,384.4

1

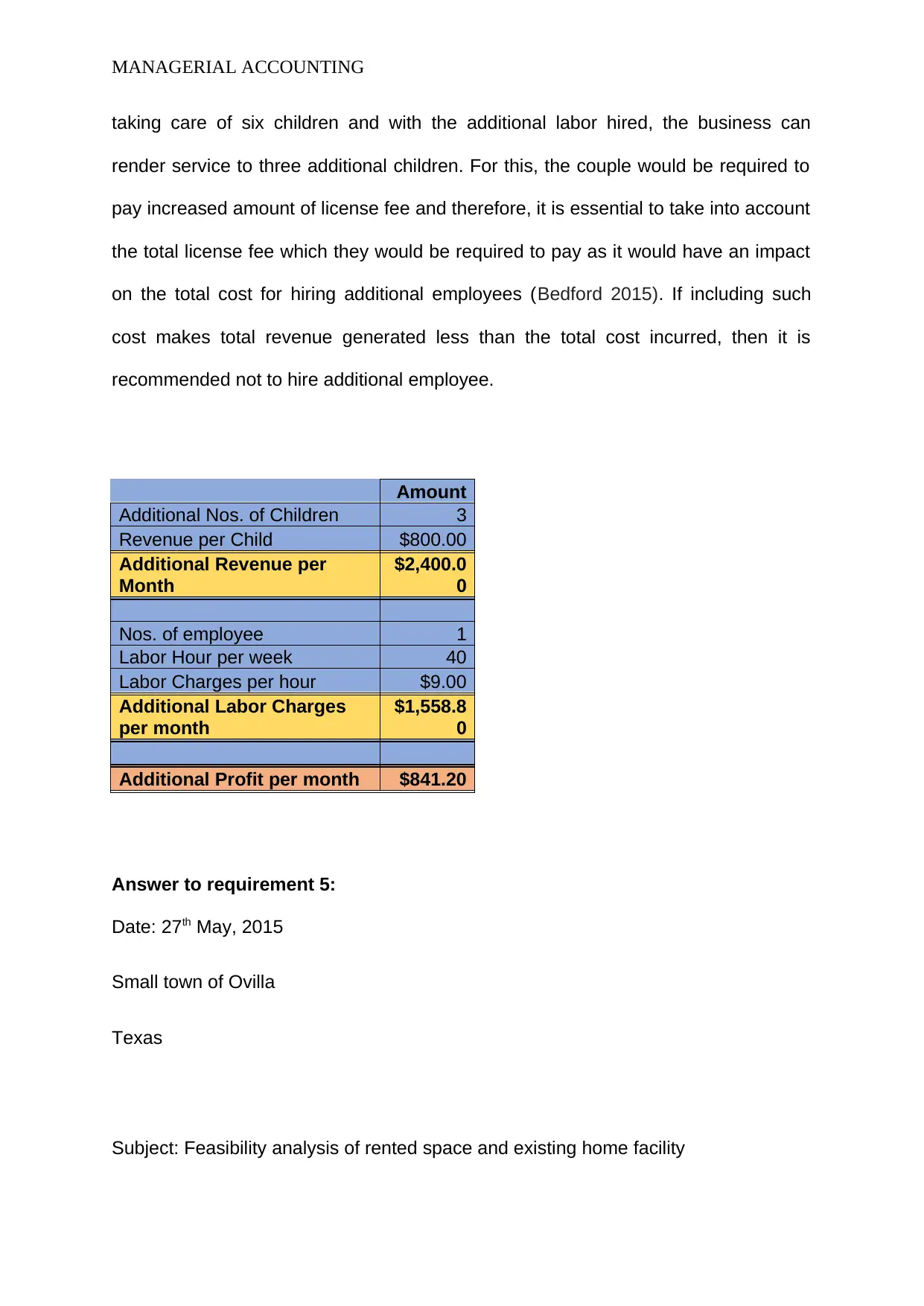

Answer to requirement 4:

Under this section, the cost and benefit analysis to the business by hiring

additional employees is presented. The couple can hire one additional employee at

the cost of $ 9 per hour and with the additional employee, the couple can offer

services to three additional children. For analyzing the benefits from hiring one

additional employee, it is required to compute the additional charges for hiring labor

per month and the additional revenue generated by hiring additional employee. The

computation of total labor charges is done by accounting for labor charges per week

and labor hour per week and the total labor charges comes to $ 1558.80. Total

amount of revenue generated per month by hiring additional employee comes to $

2400. Therefore, the profits can be computed by subtracting the cost incurred from

the revenue generated. It can be inferred from the figure that the revenue generated

per month is more than the cost incurred and therefore the additional profit comes to

$ 841.20. Therefore, from the analysis of figures, it can be said that the couple

should hire additional employee as it has a positive impact on the generation of

revenue. One important fact that should be taken into consideration is the license

fees paid to the state because in the current scenario, the license fees is paid for

Monthly Depreciation of

Appliances $9.15

Additional Energy cost of Washer $10.00

Additional Energy cost of Dryer $12.08

Total Monthly Operating

Expenses $52.00 $60.86 $42.90

Annual Expenses

$624.0

0

$730.2

7 $514.84

Less: Depreciation $9.15

Total Cash Out Flow

$624.0

0

$730.2

7

$1,384.4

1

Answer to requirement 4:

Under this section, the cost and benefit analysis to the business by hiring

additional employees is presented. The couple can hire one additional employee at

the cost of $ 9 per hour and with the additional employee, the couple can offer

services to three additional children. For analyzing the benefits from hiring one

additional employee, it is required to compute the additional charges for hiring labor

per month and the additional revenue generated by hiring additional employee. The

computation of total labor charges is done by accounting for labor charges per week

and labor hour per week and the total labor charges comes to $ 1558.80. Total

amount of revenue generated per month by hiring additional employee comes to $

2400. Therefore, the profits can be computed by subtracting the cost incurred from

the revenue generated. It can be inferred from the figure that the revenue generated

per month is more than the cost incurred and therefore the additional profit comes to

$ 841.20. Therefore, from the analysis of figures, it can be said that the couple

should hire additional employee as it has a positive impact on the generation of

revenue. One important fact that should be taken into consideration is the license

fees paid to the state because in the current scenario, the license fees is paid for

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

MANAGERIAL ACCOUNTING

taking care of six children and with the additional labor hired, the business can

render service to three additional children. For this, the couple would be required to

pay increased amount of license fee and therefore, it is essential to take into account

the total license fee which they would be required to pay as it would have an impact

on the total cost for hiring additional employees (Bedford 2015). If including such

cost makes total revenue generated less than the total cost incurred, then it is

recommended not to hire additional employee.

Amount

Additional Nos. of Children 3

Revenue per Child $800.00

Additional Revenue per

Month

$2,400.0

0

Nos. of employee 1

Labor Hour per week 40

Labor Charges per hour $9.00

Additional Labor Charges

per month

$1,558.8

0

Additional Profit per month $841.20

Answer to requirement 5:

Date: 27th May, 2015

Small town of Ovilla

Texas

Subject: Feasibility analysis of rented space and existing home facility

taking care of six children and with the additional labor hired, the business can

render service to three additional children. For this, the couple would be required to

pay increased amount of license fee and therefore, it is essential to take into account

the total license fee which they would be required to pay as it would have an impact

on the total cost for hiring additional employees (Bedford 2015). If including such

cost makes total revenue generated less than the total cost incurred, then it is

recommended not to hire additional employee.

Amount

Additional Nos. of Children 3

Revenue per Child $800.00

Additional Revenue per

Month

$2,400.0

0

Nos. of employee 1

Labor Hour per week 40

Labor Charges per hour $9.00

Additional Labor Charges

per month

$1,558.8

0

Additional Profit per month $841.20

Answer to requirement 5:

Date: 27th May, 2015

Small town of Ovilla

Texas

Subject: Feasibility analysis of rented space and existing home facility

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

MANAGERIAL ACCOUNTING

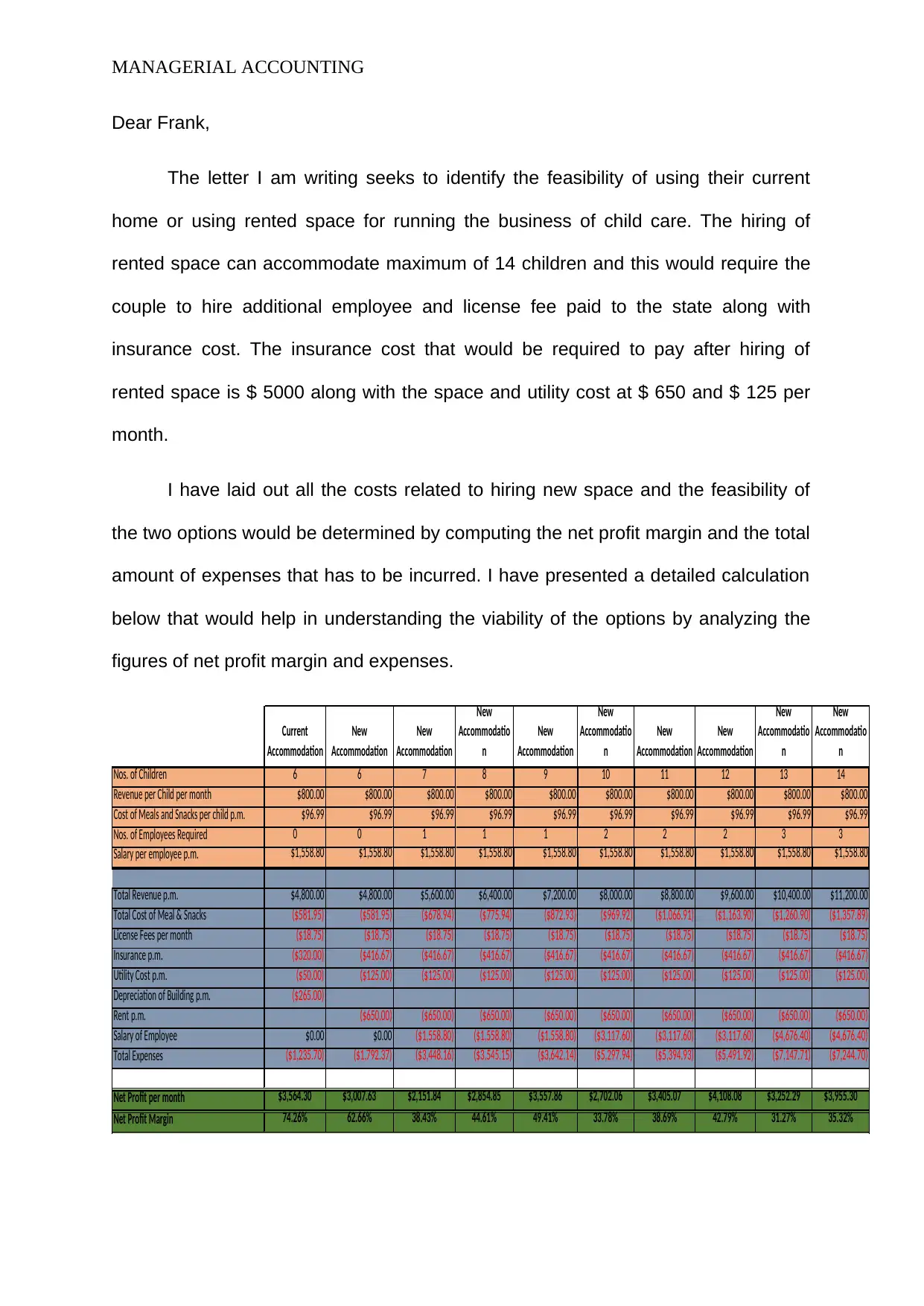

Dear Frank,

The letter I am writing seeks to identify the feasibility of using their current

home or using rented space for running the business of child care. The hiring of

rented space can accommodate maximum of 14 children and this would require the

couple to hire additional employee and license fee paid to the state along with

insurance cost. The insurance cost that would be required to pay after hiring of

rented space is $ 5000 along with the space and utility cost at $ 650 and $ 125 per

month.

I have laid out all the costs related to hiring new space and the feasibility of

the two options would be determined by computing the net profit margin and the total

amount of expenses that has to be incurred. I have presented a detailed calculation

below that would help in understanding the viability of the options by analyzing the

figures of net profit margin and expenses.

Current

Accommodation

New

Accommodation

New

Accommodation

New

Accommodatio

n

New

Accommodation

New

Accommodatio

n

New

Accommodation

New

Accommodation

New

Accommodatio

n

New

Accommodatio

n

Nos. of Children 6 6 7 8 9 10 11 12 13 14

Revenue per Child per month $800.00 $800.00 $800.00 $800.00 $800.00 $800.00 $800.00 $800.00 $800.00 $800.00

Cost of Meals and Snacks per child p.m. $96.99 $96.99 $96.99 $96.99 $96.99 $96.99 $96.99 $96.99 $96.99 $96.99

Nos. of Employees Required 0 0 1 1 1 2 2 2 3 3

Salary per employee p.m. $1,558.80 $1,558.80 $1,558.80 $1,558.80 $1,558.80 $1,558.80 $1,558.80 $1,558.80 $1,558.80 $1,558.80

Total Revenue p.m. $4,800.00 $4,800.00 $5,600.00 $6,400.00 $7,200.00 $8,000.00 $8,800.00 $9,600.00 $10,400.00 $11,200.00

Total Cost of Meal & Snacks ($581.95) ($581.95) ($678.94) ($775.94) ($872.93) ($969.92) ($1,066.91) ($1,163.90) ($1,260.90) ($1,357.89)

License Fees per month ($18.75) ($18.75) ($18.75) ($18.75) ($18.75) ($18.75) ($18.75) ($18.75) ($18.75) ($18.75)

Insurance p.m. ($320.00) ($416.67) ($416.67) ($416.67) ($416.67) ($416.67) ($416.67) ($416.67) ($416.67) ($416.67)

Utility Cost p.m. ($50.00) ($125.00) ($125.00) ($125.00) ($125.00) ($125.00) ($125.00) ($125.00) ($125.00) ($125.00)

Depreciation of Building p.m. ($265.00)

Rent p.m. ($650.00) ($650.00) ($650.00) ($650.00) ($650.00) ($650.00) ($650.00) ($650.00) ($650.00)

Salary of Employee $0.00 $0.00 ($1,558.80) ($1,558.80) ($1,558.80) ($3,117.60) ($3,117.60) ($3,117.60) ($4,676.40) ($4,676.40)

Total Expenses ($1,235.70) ($1,792.37) ($3,448.16) ($3,545.15) ($3,642.14) ($5,297.94) ($5,394.93) ($5,491.92) ($7,147.71) ($7,244.70)

Net Profit per month $3,564.30 $3,007.63 $2,151.84 $2,854.85 $3,557.86 $2,702.06 $3,405.07 $4,108.08 $3,252.29 $3,955.30

Net Profit Margin 74.26% 62.66% 38.43% 44.61% 49.41% 33.78% 38.69% 42.79% 31.27% 35.32%

Dear Frank,

The letter I am writing seeks to identify the feasibility of using their current

home or using rented space for running the business of child care. The hiring of

rented space can accommodate maximum of 14 children and this would require the

couple to hire additional employee and license fee paid to the state along with

insurance cost. The insurance cost that would be required to pay after hiring of

rented space is $ 5000 along with the space and utility cost at $ 650 and $ 125 per

month.

I have laid out all the costs related to hiring new space and the feasibility of

the two options would be determined by computing the net profit margin and the total

amount of expenses that has to be incurred. I have presented a detailed calculation

below that would help in understanding the viability of the options by analyzing the

figures of net profit margin and expenses.

Current

Accommodation

New

Accommodation

New

Accommodation

New

Accommodatio

n

New

Accommodation

New

Accommodatio

n

New

Accommodation

New

Accommodation

New

Accommodatio

n

New

Accommodatio

n

Nos. of Children 6 6 7 8 9 10 11 12 13 14

Revenue per Child per month $800.00 $800.00 $800.00 $800.00 $800.00 $800.00 $800.00 $800.00 $800.00 $800.00

Cost of Meals and Snacks per child p.m. $96.99 $96.99 $96.99 $96.99 $96.99 $96.99 $96.99 $96.99 $96.99 $96.99

Nos. of Employees Required 0 0 1 1 1 2 2 2 3 3

Salary per employee p.m. $1,558.80 $1,558.80 $1,558.80 $1,558.80 $1,558.80 $1,558.80 $1,558.80 $1,558.80 $1,558.80 $1,558.80

Total Revenue p.m. $4,800.00 $4,800.00 $5,600.00 $6,400.00 $7,200.00 $8,000.00 $8,800.00 $9,600.00 $10,400.00 $11,200.00

Total Cost of Meal & Snacks ($581.95) ($581.95) ($678.94) ($775.94) ($872.93) ($969.92) ($1,066.91) ($1,163.90) ($1,260.90) ($1,357.89)

License Fees per month ($18.75) ($18.75) ($18.75) ($18.75) ($18.75) ($18.75) ($18.75) ($18.75) ($18.75) ($18.75)

Insurance p.m. ($320.00) ($416.67) ($416.67) ($416.67) ($416.67) ($416.67) ($416.67) ($416.67) ($416.67) ($416.67)

Utility Cost p.m. ($50.00) ($125.00) ($125.00) ($125.00) ($125.00) ($125.00) ($125.00) ($125.00) ($125.00) ($125.00)

Depreciation of Building p.m. ($265.00)

Rent p.m. ($650.00) ($650.00) ($650.00) ($650.00) ($650.00) ($650.00) ($650.00) ($650.00) ($650.00)

Salary of Employee $0.00 $0.00 ($1,558.80) ($1,558.80) ($1,558.80) ($3,117.60) ($3,117.60) ($3,117.60) ($4,676.40) ($4,676.40)

Total Expenses ($1,235.70) ($1,792.37) ($3,448.16) ($3,545.15) ($3,642.14) ($5,297.94) ($5,394.93) ($5,491.92) ($7,147.71) ($7,244.70)

Net Profit per month $3,564.30 $3,007.63 $2,151.84 $2,854.85 $3,557.86 $2,702.06 $3,405.07 $4,108.08 $3,252.29 $3,955.30

Net Profit Margin 74.26% 62.66% 38.43% 44.61% 49.41% 33.78% 38.69% 42.79% 31.27% 35.32%

MANAGERIAL ACCOUNTING

It is clearly observable from the calculations presented above that with

increase in total number of children that are provided service; the total amount of

expense is increasing. In addition to this, the net profit margin is declining

continuously under the present accommodation to hiring new accommodation and

with increasing number of children. However, the total amount of revenue generated

has increased and this increase in revenue is offset by increase in the total amount

of expenses (Caglio and Ditillo 2017). Therefore, it would be advisable for the couple

not to hire the rented space and continue providing service using their own home.

Hence, they should continue to operate the facility at their home. If the existing

facility is run, then a maximum of six children should be accepted and it is not

required to hire any employee as the couple themselves is efficient to provide

services.

Regards,

Accountant

Part B:

Answer to requirement 1:

Identifying the management accounting system components using the

examples from the case study:

In this section, the components of management accounting system are

depicted using the case of Apple Inc and Canon Inc. Management accounting

system comprise of the components such as controlling, planning and strategy that

helps in the process of making decision at different levels. One of the aspects of

It is clearly observable from the calculations presented above that with

increase in total number of children that are provided service; the total amount of

expense is increasing. In addition to this, the net profit margin is declining

continuously under the present accommodation to hiring new accommodation and

with increasing number of children. However, the total amount of revenue generated

has increased and this increase in revenue is offset by increase in the total amount

of expenses (Caglio and Ditillo 2017). Therefore, it would be advisable for the couple

not to hire the rented space and continue providing service using their own home.

Hence, they should continue to operate the facility at their home. If the existing

facility is run, then a maximum of six children should be accepted and it is not

required to hire any employee as the couple themselves is efficient to provide

services.

Regards,

Accountant

Part B:

Answer to requirement 1:

Identifying the management accounting system components using the

examples from the case study:

In this section, the components of management accounting system are

depicted using the case of Apple Inc and Canon Inc. Management accounting

system comprise of the components such as controlling, planning and strategy that

helps in the process of making decision at different levels. One of the aspects of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

MANAGERIAL ACCOUNTING

creating information is to develop the process of new innovation within the circles of

quality control. It is required by the firm to create new products, new ways of

manufacturing, selling and distribution for remaining competitive. Planning stage of

organization incorporates the assessment of quality and cost groups. One of the

important parts of the management accounting system is the development of the

strategy that helps in creating linkage between the strategic attempts and daily

activities of business (Gureva et al. 2016).

The process of product development by the organizations mentioned in the

case study that is Apple Inc and Canon Inc incorporate innovation that assisted in

generating new information and enabled the managers to make efficient and

effective decisions. In the case of Canon Inc, the market for plain paper copier was

reconceptualized for making the maintenance cost essentially zero. The existing

inverse relationship between the reliability and costs for the mini copier was

contradicted and the manager sought to handle this contradiction by actualization of

the mini copier. This actualization was done by incorporating the control factor of the

managerial accounting system and it was ascertained that it is required to make an

improvement in the drums and cleaner durability. After producing certain number of

copies, the producer would discard the drum so that the copier does not incur any

maintenance cost. Such innovation was introduced because of in depth

understanding and this subsequently added to the capacity of the company

(Carlsson et al. 2018).

Assessing the cost and quality was another component of managerial

accounting system at Canon Inc. It was required to formulate the quality standard for

the different acts associated with the mini copier. It was found that the cartridge was

the new developed fact that was the base of knowledge and was applicable to the

creating information is to develop the process of new innovation within the circles of

quality control. It is required by the firm to create new products, new ways of

manufacturing, selling and distribution for remaining competitive. Planning stage of

organization incorporates the assessment of quality and cost groups. One of the

important parts of the management accounting system is the development of the

strategy that helps in creating linkage between the strategic attempts and daily

activities of business (Gureva et al. 2016).

The process of product development by the organizations mentioned in the

case study that is Apple Inc and Canon Inc incorporate innovation that assisted in

generating new information and enabled the managers to make efficient and

effective decisions. In the case of Canon Inc, the market for plain paper copier was

reconceptualized for making the maintenance cost essentially zero. The existing

inverse relationship between the reliability and costs for the mini copier was

contradicted and the manager sought to handle this contradiction by actualization of

the mini copier. This actualization was done by incorporating the control factor of the

managerial accounting system and it was ascertained that it is required to make an

improvement in the drums and cleaner durability. After producing certain number of

copies, the producer would discard the drum so that the copier does not incur any

maintenance cost. Such innovation was introduced because of in depth

understanding and this subsequently added to the capacity of the company

(Carlsson et al. 2018).

Assessing the cost and quality was another component of managerial

accounting system at Canon Inc. It was required to formulate the quality standard for

the different acts associated with the mini copier. It was found that the cartridge was

the new developed fact that was the base of knowledge and was applicable to the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

MANAGERIAL ACCOUNTING

other products as well. The task force and the team contributed to the reduction of

time between the planning of developing the products and the till the time products

can be completed. There were added benefits of the reconceptualization of the

market of mini copier such as assembly automation, miniaturization and reduction in

the weight. The development of mini copier was associated with the cooperation

between the development of product and manufacturing of technology. Therefore,

with the enhancing of the organization capability brought many benefits and expands

the base of knowledge (Hopper and Bui 2016).

Now, considering the case of Apple Inc that incorporated the planning and

strategizing components of managerial accounting in the process of product

development. The creation process of Apple Inc for development of Macintosh by

way of revolutionized Mac came with the advantages and disadvantages. The new

ideas and features emerged due to constant interaction between the members of

team of Mac during the period of its revolution that intended to produce Mac at lower

price. Such team became self organization that was brought due to the constant

interaction between different teams comprising hardware and software people

(Bogoviz and Mezhov 2015).

Controlling component was used by the management accounting system of

Apple that resulted in setting up of factory so that Mac can be produced

inexpensively at lower cost. However, the process of developing the product was

critical because of the criticality of the role of the chief executive officer of Apple Inc.

It has been found that the role of leader acted as a facilitator and catalyst in the

process of decision making and the process was further enhanced because the final

arbiter of decision was taken by Steve. From the analysis of facts, it is inferred that

other products as well. The task force and the team contributed to the reduction of

time between the planning of developing the products and the till the time products

can be completed. There were added benefits of the reconceptualization of the

market of mini copier such as assembly automation, miniaturization and reduction in

the weight. The development of mini copier was associated with the cooperation

between the development of product and manufacturing of technology. Therefore,

with the enhancing of the organization capability brought many benefits and expands

the base of knowledge (Hopper and Bui 2016).

Now, considering the case of Apple Inc that incorporated the planning and

strategizing components of managerial accounting in the process of product

development. The creation process of Apple Inc for development of Macintosh by

way of revolutionized Mac came with the advantages and disadvantages. The new

ideas and features emerged due to constant interaction between the members of

team of Mac during the period of its revolution that intended to produce Mac at lower

price. Such team became self organization that was brought due to the constant

interaction between different teams comprising hardware and software people

(Bogoviz and Mezhov 2015).

Controlling component was used by the management accounting system of

Apple that resulted in setting up of factory so that Mac can be produced

inexpensively at lower cost. However, the process of developing the product was

critical because of the criticality of the role of the chief executive officer of Apple Inc.

It has been found that the role of leader acted as a facilitator and catalyst in the

process of decision making and the process was further enhanced because the final

arbiter of decision was taken by Steve. From the analysis of facts, it is inferred that

MANAGERIAL ACCOUNTING

the development process of Macintosh incorporated the controlling and decision

making components of the managerial accounting system.

Answer to requirement 2:

Contribution of management accounting to innovation process:

The role of management accounting in the process of innovation is

demonstrated in this section by analyzing the case of two companies which

incorporated innovation in the product development process. An organization

intending to innovate its product by introducing new ideas has higher chances of

success when it is backed by the management accounting system as it helps in

facilitating the decision making prices due to proper planning and controlling.

Innovation creates differentiation between the organizations brought by the

development of the techniques of management accounting. Furthermore, it is

interesting to mention that the traditional and old method of management accounting

results in eradication of the freedom and flexibility that is required by the innovation

and such facilitation is done because of the command culture and control features of

the managerial accounting (Shields 2015).

Innovation at Apple and Canon Inc was facilitated by way of social interaction

that helped information creation for innovation. The controlling and planning

component of management accounting contributes to the facilitate innovation of the

product. Furthermore, the organizations relied on the concept of managerial

accounting that was done for the return on investment and analysis of profit center.

It is the human activity at Canon Inc that formed the basis of entire plain paper

copier reconceptualization and such activities not based on deduction or induction.

the development process of Macintosh incorporated the controlling and decision

making components of the managerial accounting system.

Answer to requirement 2:

Contribution of management accounting to innovation process:

The role of management accounting in the process of innovation is

demonstrated in this section by analyzing the case of two companies which

incorporated innovation in the product development process. An organization

intending to innovate its product by introducing new ideas has higher chances of

success when it is backed by the management accounting system as it helps in

facilitating the decision making prices due to proper planning and controlling.

Innovation creates differentiation between the organizations brought by the

development of the techniques of management accounting. Furthermore, it is

interesting to mention that the traditional and old method of management accounting

results in eradication of the freedom and flexibility that is required by the innovation

and such facilitation is done because of the command culture and control features of

the managerial accounting (Shields 2015).

Innovation at Apple and Canon Inc was facilitated by way of social interaction

that helped information creation for innovation. The controlling and planning

component of management accounting contributes to the facilitate innovation of the

product. Furthermore, the organizations relied on the concept of managerial

accounting that was done for the return on investment and analysis of profit center.

It is the human activity at Canon Inc that formed the basis of entire plain paper

copier reconceptualization and such activities not based on deduction or induction.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.