Managerial Accounting Case Study: Costing Methods Comparison

VerifiedAdded on 2023/01/18

|15

|1931

|90

Project

AI Summary

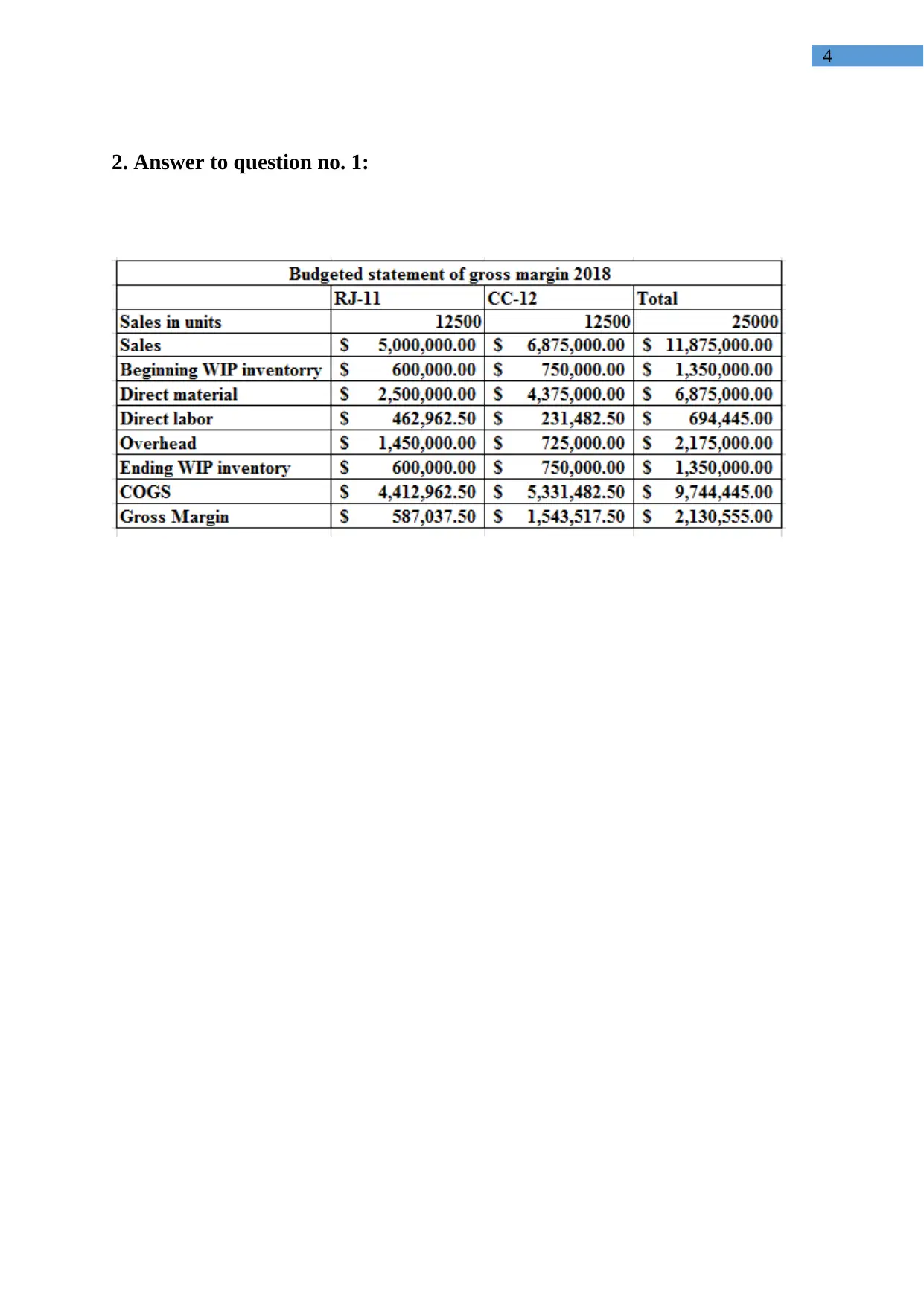

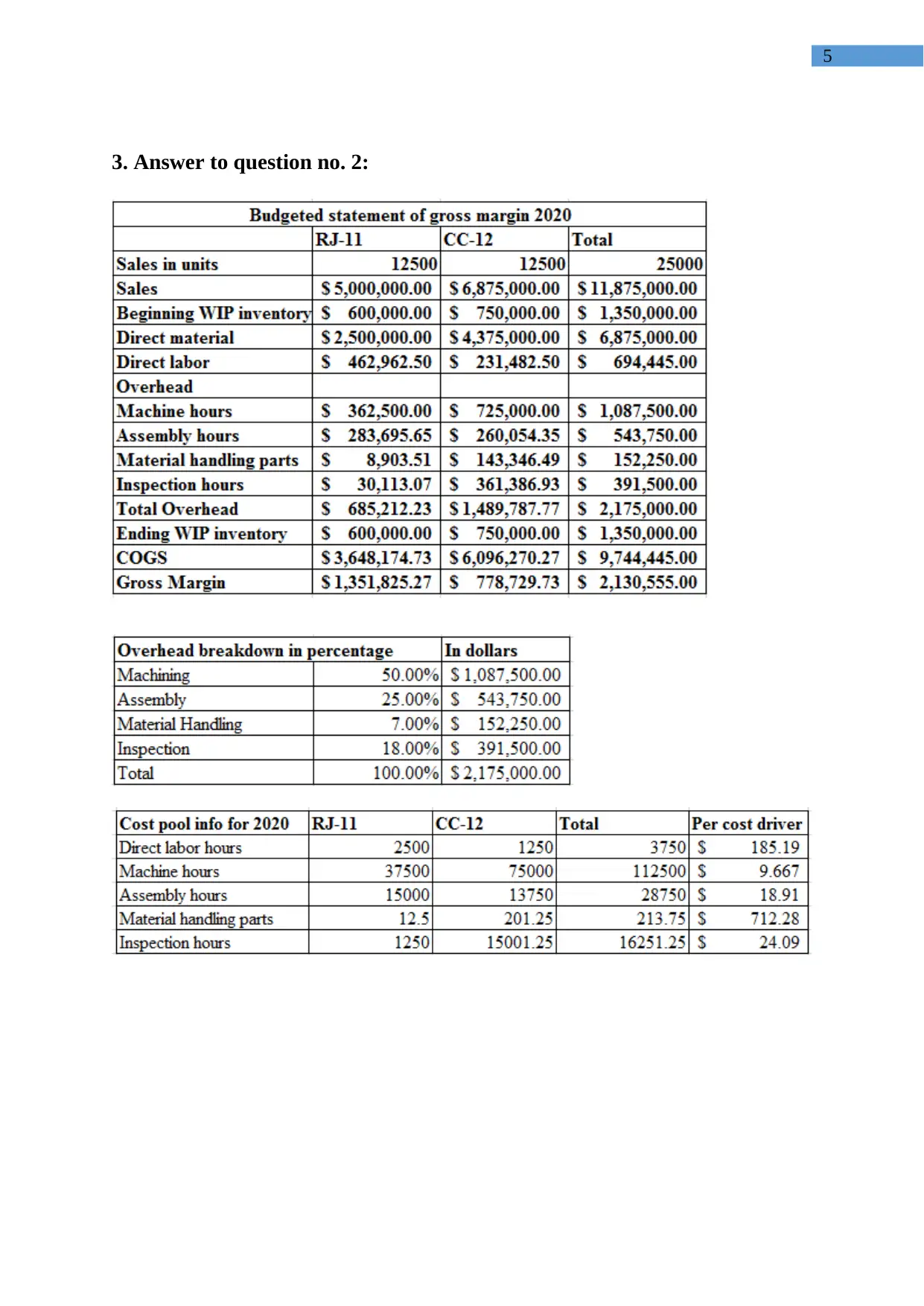

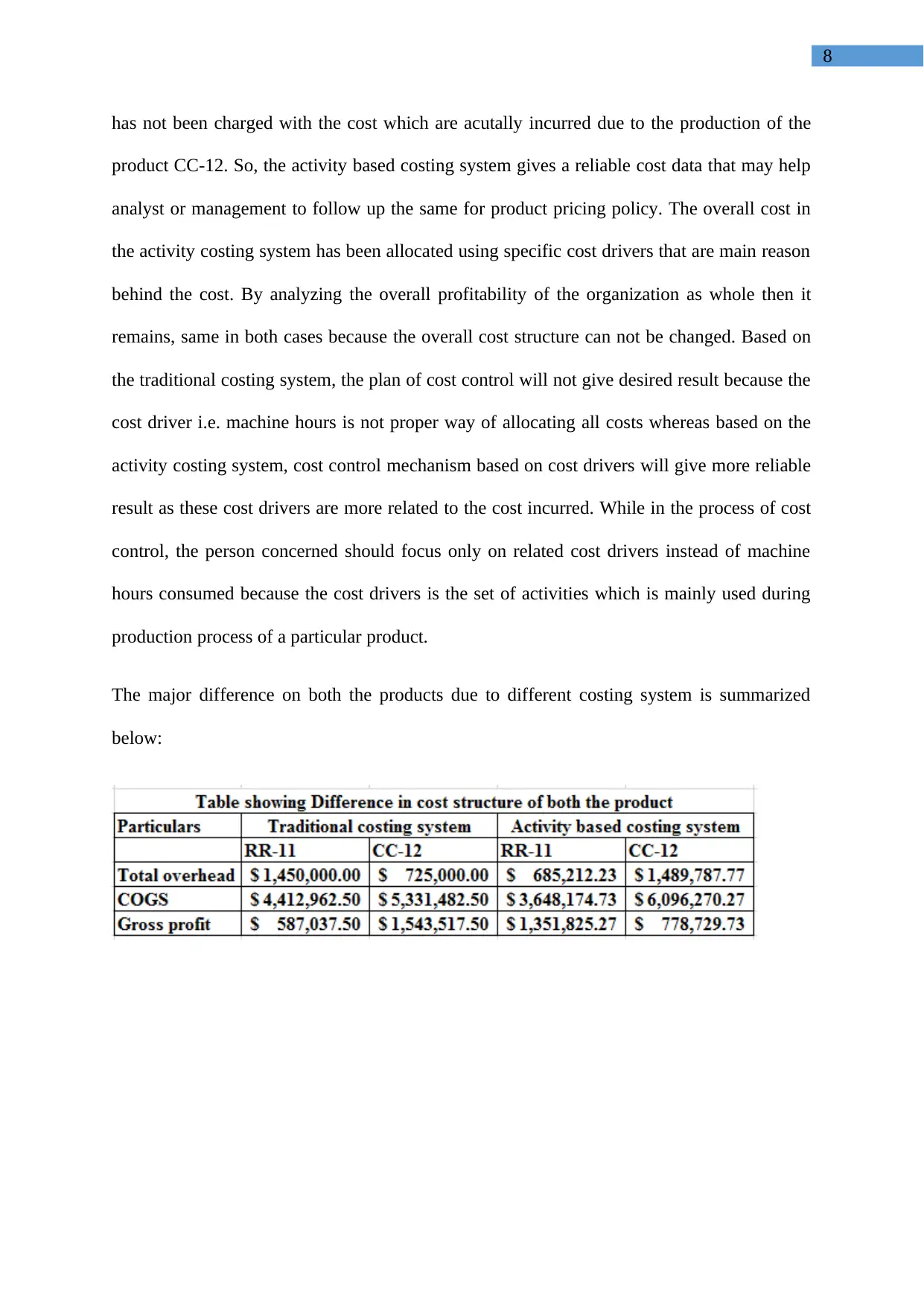

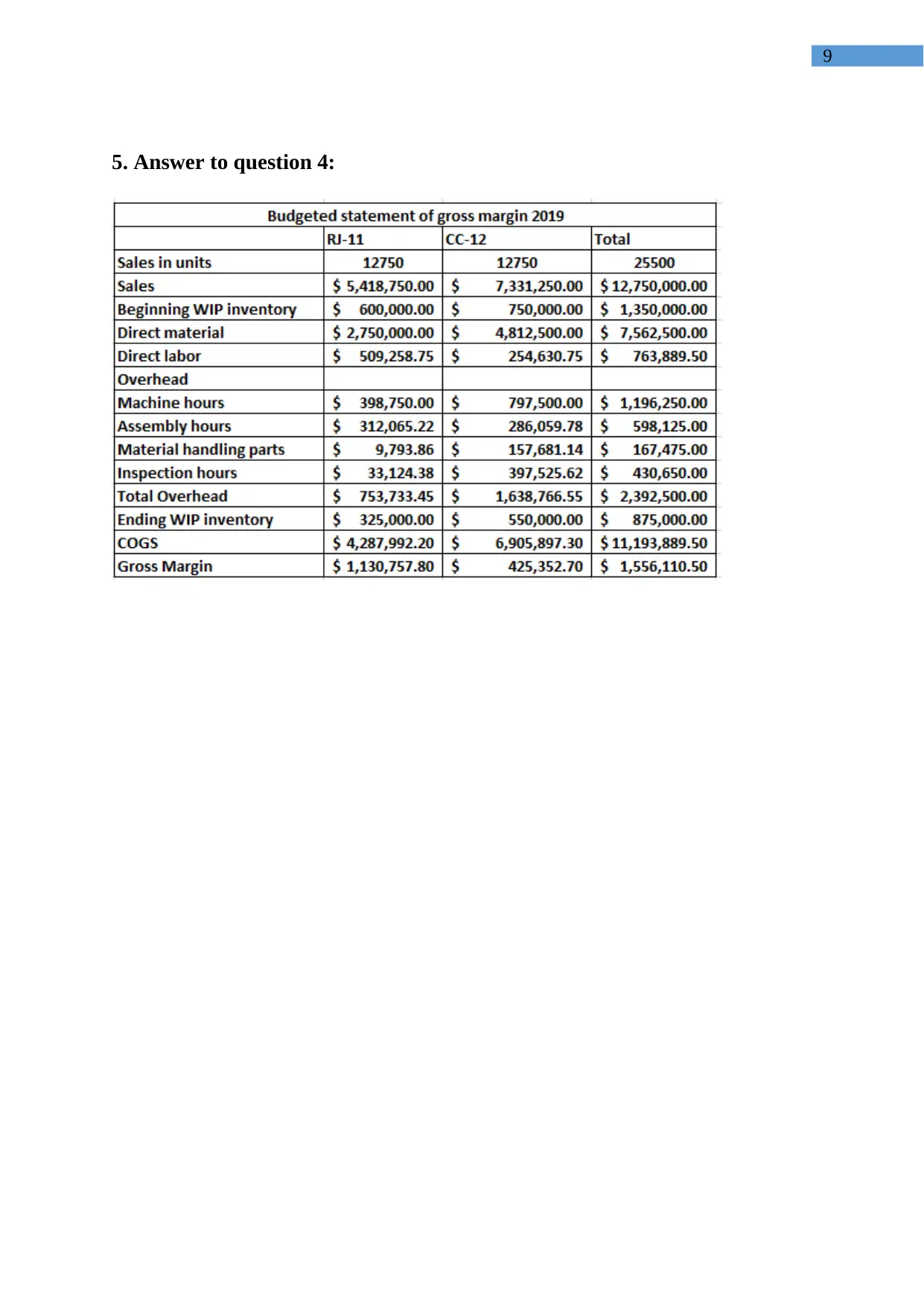

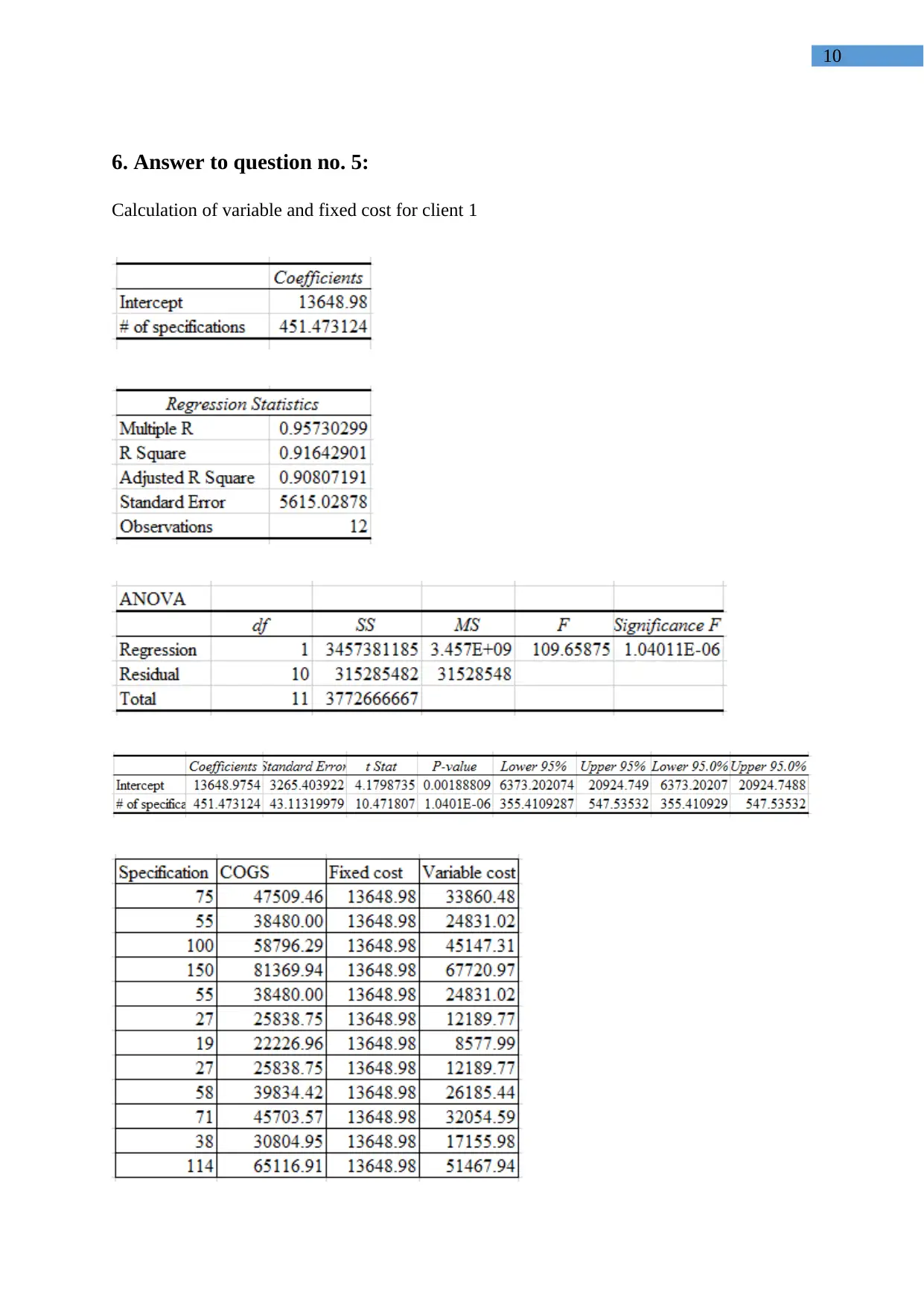

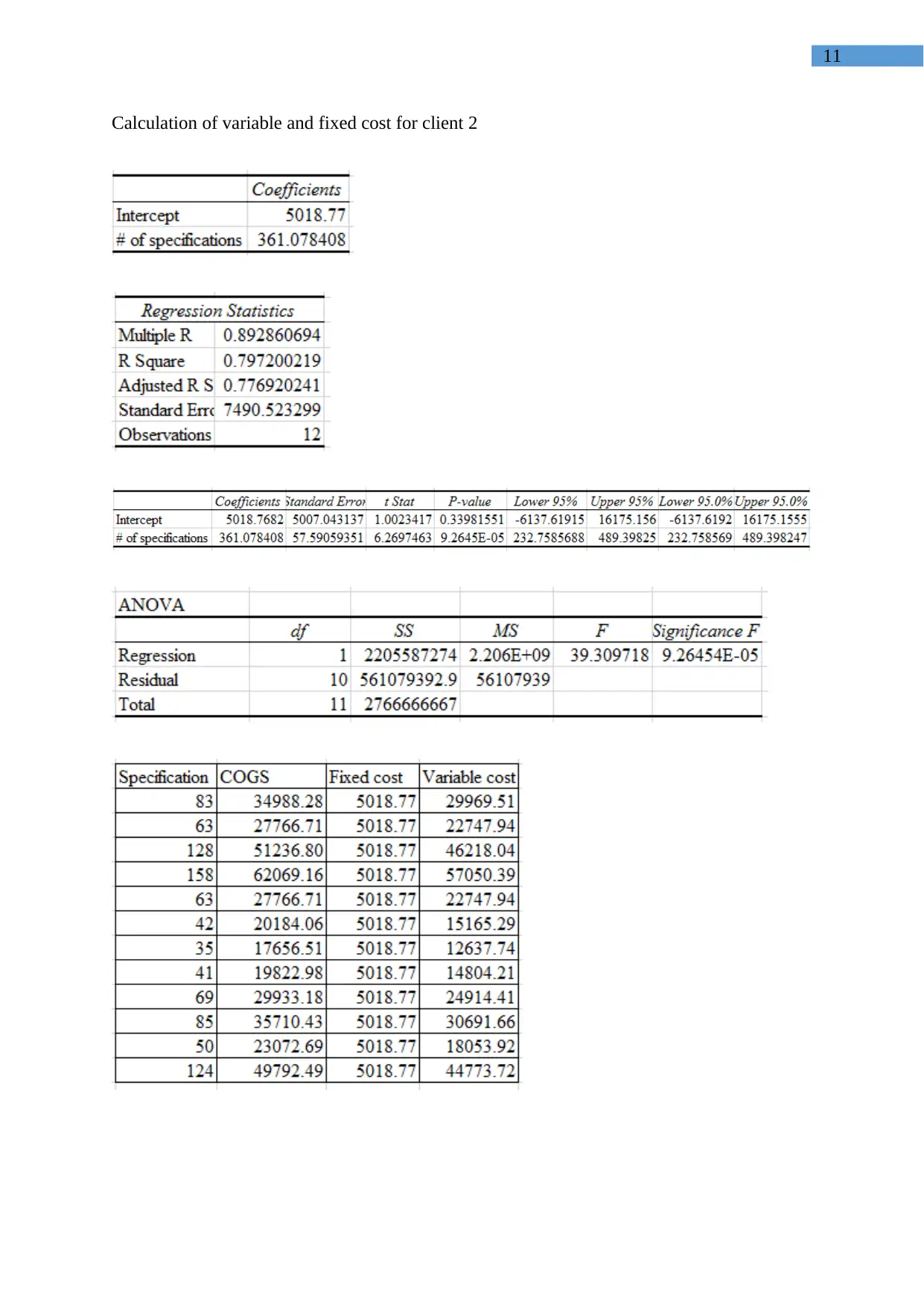

This report analyzes a managerial accounting case study involving Harvard Square Inc., a manufacturing company with traditional and modern product lines. The report compares traditional costing and activity-based costing (ABC) methods, detailing the allocation of overhead costs using machine hour rates and various cost drivers, respectively. It examines the impact of these costing systems on product profitability, highlighting how ABC provides a more accurate cost structure by assigning costs based on activities. Furthermore, the report incorporates regression analysis to determine fixed and variable costs for different clients, illustrating how cost behavior varies based on product specifications. The analysis covers the calculation of gross profit margins, the influence of different costing methods on product profitability, and the implications for cost control and management decision-making. The case study emphasizes the importance of choosing the appropriate costing system for accurate product costing and effective cost management, supported by references to relevant academic literature.

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.