Managerial Accounting Report: Costing Systems in Contemporary Business

VerifiedAdded on 2023/01/16

|13

|4057

|89

Report

AI Summary

This report provides an in-depth analysis of managerial accounting, focusing on the features and applications of standard costing as a planning and control system. It explores standard costing within the context of a real-life case company, Beximco Pharmaceuticals Ltd, highlighting its relevance in the pharmaceutical industry. The report further delves into a comparative analysis of target costing and standard costing, discussing the former's relevance in today's competitive and uncertain business environment. It outlines the target costing process and its significance in cost management. The report concludes by recommending appropriate systems of management accounting for contemporary organizations, emphasizing the importance of effective controls and planning processes. The report also discusses the limitations of standard costing and its relevance in today's manufacturing world.

Managerial Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ABSTRACT

This report summarises different aspects of managerial accounting in context of

contemporary business. It demonstrates key characteristics of standard costing and its use in

managerial controlling and organisation's planning processes. Report also provides

recommendations about appropriate systems of management accounting and relevancy in

contemporary business organisations. It helps to understand the adoption of these systems with

regards to establishing effective controls.

This report summarises different aspects of managerial accounting in context of

contemporary business. It demonstrates key characteristics of standard costing and its use in

managerial controlling and organisation's planning processes. Report also provides

recommendations about appropriate systems of management accounting and relevancy in

contemporary business organisations. It helps to understand the adoption of these systems with

regards to establishing effective controls.

Table of Contents

ABSTRACT.....................................................................................................................................2

Table of Contents.............................................................................................................................3

INTRODUCTION...........................................................................................................................4

TASK...............................................................................................................................................4

(1). Features of standard costing as a planning and control system:...........................................4

(2.) Standard costing as a planning and control system in your real-life case company:............5

(3.) Discussion on target costing and comparison and contrast it from standard costing............7

(4.) Target costing’s relevancy in today’s competitive and in uncertain business environment: 9

(5.) Systems for contemporary organisations to use for planning purpose:..............................10

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

ABSTRACT.....................................................................................................................................2

Table of Contents.............................................................................................................................3

INTRODUCTION...........................................................................................................................4

TASK...............................................................................................................................................4

(1). Features of standard costing as a planning and control system:...........................................4

(2.) Standard costing as a planning and control system in your real-life case company:............5

(3.) Discussion on target costing and comparison and contrast it from standard costing............7

(4.) Target costing’s relevancy in today’s competitive and in uncertain business environment: 9

(5.) Systems for contemporary organisations to use for planning purpose:..............................10

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Managerial accounting implies to the mechanism and practices for developing records

and reports for supporting managing officials in the corporation's decision-making functions. It is

a wider filed which also involves techniques and approaches to support managerial and

accounting practices (Pettersson and Segerstedt, 2013). This study involves explanation about

features of standard costing with regards to planning and controlling system, comparison

between target costing and standard costing. It also contains discussion on target costing

relevancy in present uncertain and competitive business environment, and recommendation for

contemporary organisations to apply for planning objectives in context of ASL Plc.

TASK

(1). Features of standard costing as a planning and control system:

Standard cost control (first being a budgetary regulation) is one of the most advanced cost

accounting enhancements. traditional costing is a cost management technique. due to the

drawbacks of traditional costing, standard costing has been ado0pted in many sectors. Traditional

costing, which relates to the costs estimation after it has taken place, reports the evaluation of

what has taken place (Hilton and Platt, 2013). Management considers control by means of

standards and standard costing as an innovative system, which determines whether or not

company's funds are utilized appropriately. During budgetary control cycle the standardized

costs are generally calculated because they are effective in planning flexible strategies and

assessing performance. This allows us to create competitive prices as well as to define the

production costs which must be controlled in relation to standard costs. Various models

demonstrate how negative patterns can be reversed correctly evaluated. When the different costs

controls are taken very carefully immediately, a good standard costing program enables to

manage costs and reduce costs. One objective of the standards is to establish a goal, and this can

gain inspiration. An inadequately-implemented standard costing framework could have a

humorous impact on individuals. this could be retorted, that norms should enable executives to

exercise freedom without apprehension of resentment in order to fulfil their role efficiently. The

practical challenge with this approach is to balance the requisite independence of management

with poor performance. The principal aim of the standard costing is to remind management about

everyday operational control. Predetermined expenditures are normal costs, which provide a

Managerial accounting implies to the mechanism and practices for developing records

and reports for supporting managing officials in the corporation's decision-making functions. It is

a wider filed which also involves techniques and approaches to support managerial and

accounting practices (Pettersson and Segerstedt, 2013). This study involves explanation about

features of standard costing with regards to planning and controlling system, comparison

between target costing and standard costing. It also contains discussion on target costing

relevancy in present uncertain and competitive business environment, and recommendation for

contemporary organisations to apply for planning objectives in context of ASL Plc.

TASK

(1). Features of standard costing as a planning and control system:

Standard cost control (first being a budgetary regulation) is one of the most advanced cost

accounting enhancements. traditional costing is a cost management technique. due to the

drawbacks of traditional costing, standard costing has been ado0pted in many sectors. Traditional

costing, which relates to the costs estimation after it has taken place, reports the evaluation of

what has taken place (Hilton and Platt, 2013). Management considers control by means of

standards and standard costing as an innovative system, which determines whether or not

company's funds are utilized appropriately. During budgetary control cycle the standardized

costs are generally calculated because they are effective in planning flexible strategies and

assessing performance. This allows us to create competitive prices as well as to define the

production costs which must be controlled in relation to standard costs. Various models

demonstrate how negative patterns can be reversed correctly evaluated. When the different costs

controls are taken very carefully immediately, a good standard costing program enables to

manage costs and reduce costs. One objective of the standards is to establish a goal, and this can

gain inspiration. An inadequately-implemented standard costing framework could have a

humorous impact on individuals. this could be retorted, that norms should enable executives to

exercise freedom without apprehension of resentment in order to fulfil their role efficiently. The

practical challenge with this approach is to balance the requisite independence of management

with poor performance. The principal aim of the standard costing is to remind management about

everyday operational control. Predetermined expenditures are normal costs, which provide a

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

foundation for successful cost control. The costs of criteria reflect the criterion for evaluating it.

Following is summary of all the discussed key features of Standard Costing relevant for

establishing effective planning and control processes, as follows:

Standard costing is structured to asses’ costs of outputs supported on previous period

experiences as well as future trends.

Cost comparison. In it actual expenses/costs are compared to standard/budgeted costs.

Control over different-variances: comparing standards and actual expenses to assess and

control variances.

Recognise key areas: Variances identified in standard costing help to allocate key areas which

are threat in planning and managerial controlling (Maher, Stickney and Weil, 2012).

(2.) Standard costing as a planning and control system in your real-life case company:

Here in study real life company named Beximco Pharmaceuticals Ltd which is

pharmaceutical company working in Bangladesh. Beximco Pharma is a rapidly growing generic

player of drugs undertaken to offering access to inexpensive drugs. The state-of-the-art

production services of company have been licensed by regulatory bodies in USA, Australia,

European Union and Brazil, and this is currently focusing on establishing presence in several

developing and established markets all over the globe. manufacturing operations of Beximco

Pharma are situated over around 20 acre (81,000 m2) area in Dhaka,Bangladesh. The projects are

comprised of a variety of intent-built plants such as a new plant for Oral Solid Dosage (OSD).

The plant contains fabrication facilities, research labs as well as no. of factories. The plants and

equipment were built, assembled and assembled, amongst others, by collaborators from Italy,

Germany, Sweden, Switzerland and UK. One of key industries of Bangladesh's national

economy field is pharmaceuticals and chemicals companies. The pharmaceutical sector achieves

around 97 per cent of regional market's total drug requirements. It hires around 115,000 workers,

market size is around BDT 117 billion. According to figures from Bangladesh's Manager-

General of Drug Affairs, the overall number of companies manufacturing medication is:

allopathic around 258, unani around 268, homeopathic around 79, ayurvedic around 201, and

Herbal around 17. There are over 100 corporations in Bangladesh which manufacture different

chemicals. Standard costing is best suited for activities involving a variety of unusual or repeated

operations. Procedures are often repeated in organizations and thus standard costing of such

organizations is important. For non-producing industries where the processes are routine,

Following is summary of all the discussed key features of Standard Costing relevant for

establishing effective planning and control processes, as follows:

Standard costing is structured to asses’ costs of outputs supported on previous period

experiences as well as future trends.

Cost comparison. In it actual expenses/costs are compared to standard/budgeted costs.

Control over different-variances: comparing standards and actual expenses to assess and

control variances.

Recognise key areas: Variances identified in standard costing help to allocate key areas which

are threat in planning and managerial controlling (Maher, Stickney and Weil, 2012).

(2.) Standard costing as a planning and control system in your real-life case company:

Here in study real life company named Beximco Pharmaceuticals Ltd which is

pharmaceutical company working in Bangladesh. Beximco Pharma is a rapidly growing generic

player of drugs undertaken to offering access to inexpensive drugs. The state-of-the-art

production services of company have been licensed by regulatory bodies in USA, Australia,

European Union and Brazil, and this is currently focusing on establishing presence in several

developing and established markets all over the globe. manufacturing operations of Beximco

Pharma are situated over around 20 acre (81,000 m2) area in Dhaka,Bangladesh. The projects are

comprised of a variety of intent-built plants such as a new plant for Oral Solid Dosage (OSD).

The plant contains fabrication facilities, research labs as well as no. of factories. The plants and

equipment were built, assembled and assembled, amongst others, by collaborators from Italy,

Germany, Sweden, Switzerland and UK. One of key industries of Bangladesh's national

economy field is pharmaceuticals and chemicals companies. The pharmaceutical sector achieves

around 97 per cent of regional market's total drug requirements. It hires around 115,000 workers,

market size is around BDT 117 billion. According to figures from Bangladesh's Manager-

General of Drug Affairs, the overall number of companies manufacturing medication is:

allopathic around 258, unani around 268, homeopathic around 79, ayurvedic around 201, and

Herbal around 17. There are over 100 corporations in Bangladesh which manufacture different

chemicals. Standard costing is best suited for activities involving a variety of unusual or repeated

operations. Procedures are often repeated in organizations and thus standard costing of such

organizations is important. For non-producing industries where the processes are routine,

standard costing methods can be implemented. Furthermore, non-repetitive practices can not

readily be carried out, because there is no foundation for repetitive procedures to be observed,

and standards could therefore not have been established. The research showed that around 75

percent (21 out of 28) of the organizations still employ standard costing with various objectives

in their businesses. It shows that despite the emergence of new modern managerial accounting

techniques such as ABC, Lean manufacturing, six sigma etc., traditional costs in Bangladesh

didn't lose their attraction to this field. The explanation for respondent's selection of this form is

simplicity. A standard costing mechanism can be applied in organizations which manufacture a

large number of distinct products and generate several common activities. Standard costs

for actual output for just a specific duration in this costing system may attributed to the

executives of management centres who are really in charge of different activities. For actual

costs for that same duration, the accountability centres are often paid. Both cost rates are then

measured, the normal and the real, and the difference between two becomes reported.

Managers need guidance to examine where the discrepancies have emerged. Accountants

can support management in this process, but in practice to carry out an effective audit, it is

crucial that they do so with the accountable management. The explanation for the variation is

readily identified through doing that together. There are many benefits in terms of requirements,

such as simpler measurements, efficient liability as well as performance controls efficiency.

Since after the industrial revolutions, standard costs have become an important factor in the

world of management materials. They have been evolved and been using when production

circumstances were stable for organisations, huge series of standardized goods were

manufactured as well as the costs associated with job and materials were the main costs, i.e. a

fundamentally different working environment (Matherly and Burney, 2013). Standards may be

seen as a guideline to be followed and/or preserved and thus do not comply with constantly

improving efforts. There's no impetus for any further progress when the targets are met. it is

quite critical to track and control real actions over time while looking for continual improvement.

Price levels can also compete directly against improved quality efforts. It is logical for an

individual to try to identify the best prices when making purchases. In order to accomplish

positive variations, it could be straightforward to comply with the rules on standard quality, but

poor quality in material bought may result, for instance, in increased costs due to various

increased distraction and cassation. Reliability-in-quality and performance must always be the

readily be carried out, because there is no foundation for repetitive procedures to be observed,

and standards could therefore not have been established. The research showed that around 75

percent (21 out of 28) of the organizations still employ standard costing with various objectives

in their businesses. It shows that despite the emergence of new modern managerial accounting

techniques such as ABC, Lean manufacturing, six sigma etc., traditional costs in Bangladesh

didn't lose their attraction to this field. The explanation for respondent's selection of this form is

simplicity. A standard costing mechanism can be applied in organizations which manufacture a

large number of distinct products and generate several common activities. Standard costs

for actual output for just a specific duration in this costing system may attributed to the

executives of management centres who are really in charge of different activities. For actual

costs for that same duration, the accountability centres are often paid. Both cost rates are then

measured, the normal and the real, and the difference between two becomes reported.

Managers need guidance to examine where the discrepancies have emerged. Accountants

can support management in this process, but in practice to carry out an effective audit, it is

crucial that they do so with the accountable management. The explanation for the variation is

readily identified through doing that together. There are many benefits in terms of requirements,

such as simpler measurements, efficient liability as well as performance controls efficiency.

Since after the industrial revolutions, standard costs have become an important factor in the

world of management materials. They have been evolved and been using when production

circumstances were stable for organisations, huge series of standardized goods were

manufactured as well as the costs associated with job and materials were the main costs, i.e. a

fundamentally different working environment (Matherly and Burney, 2013). Standards may be

seen as a guideline to be followed and/or preserved and thus do not comply with constantly

improving efforts. There's no impetus for any further progress when the targets are met. it is

quite critical to track and control real actions over time while looking for continual improvement.

Price levels can also compete directly against improved quality efforts. It is logical for an

individual to try to identify the best prices when making purchases. In order to accomplish

positive variations, it could be straightforward to comply with the rules on standard quality, but

poor quality in material bought may result, for instance, in increased costs due to various

increased distraction and cassation. Reliability-in-quality and performance must always be the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

focal point. Standard costs improve the cost accounting process for valuing inventories. Where

standard costing framework is not being applied, the true costs within each particular material

object in inventory must be kept recorded Real costs shall also be retained to assess the cost

including inventory of manufactured goods. A company does not need to hold store reports and

products cost at their real cost into well-working standard costing framework. There are three

major factors in standard costing which affects decisions of managers, first one is size of

variances, controllability of variances and cost of examining variances. Alternatively, records are

kept at standard costs, transformation to true cost happens by marking off all differences as the

cost of any duration (Lohr, 2012). There are still a range of deficiencies in standard costing

which pose the issue of its sustained use in contemporary production environments. As per

journal's study, almost all respondent companies (52.38 percent) claim that standards established

by the organisations are increasingly becoming obsolete as internal operating circumstances and

external context also shift. Industries are also recording high automation of processes, bypassing

quality progress and shortage of detailed information (14.29 percent each) as shortcomings of

standard costing method.

The persistence of standard costing confirms its effectiveness and dominance in today

manufacturing world. Through the usage of McDonaldization as well as diligent and practical

standard setting procedure, the deficiencies identified by the study may be minimized or

removed. Because of socio-economic facilities and scarcity of qualified technicians in such

regard, use of ABC, lean manufacturing, six sigma etc, is still not common amongst local

companies.

standard costing framework is not being applied, the true costs within each particular material

object in inventory must be kept recorded Real costs shall also be retained to assess the cost

including inventory of manufactured goods. A company does not need to hold store reports and

products cost at their real cost into well-working standard costing framework. There are three

major factors in standard costing which affects decisions of managers, first one is size of

variances, controllability of variances and cost of examining variances. Alternatively, records are

kept at standard costs, transformation to true cost happens by marking off all differences as the

cost of any duration (Lohr, 2012). There are still a range of deficiencies in standard costing

which pose the issue of its sustained use in contemporary production environments. As per

journal's study, almost all respondent companies (52.38 percent) claim that standards established

by the organisations are increasingly becoming obsolete as internal operating circumstances and

external context also shift. Industries are also recording high automation of processes, bypassing

quality progress and shortage of detailed information (14.29 percent each) as shortcomings of

standard costing method.

The persistence of standard costing confirms its effectiveness and dominance in today

manufacturing world. Through the usage of McDonaldization as well as diligent and practical

standard setting procedure, the deficiencies identified by the study may be minimized or

removed. Because of socio-economic facilities and scarcity of qualified technicians in such

regard, use of ABC, lean manufacturing, six sigma etc, is still not common amongst local

companies.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

(3.) Discussion on target costing and comparison and contrast it from standard costing.

The target-costing is not only a costing tool, but a planning strategy, whereby costs

depend on market situation and take into consideration a variety of variables, including

homogeneous goods, competition rates, no / lower cost adjustments for the end user and so on. If

these considerations are raised, management needs to regulate the prices, since they have limited

or no influence over the sales price. Target costing is a mechanism whereby a corporation plans

its price levels, products cost, and profitability it hopes to accomplish for a fresh product in

advance Unless a product can be developed at these anticipated levels the development process

will be discontinued absolutely. A management department has a valuable mechanism of target

costing to constantly track items from the point they reach the development phase and further

across its product life processes. This is seen as one of the first and most essential tools

throughout the production environment for sustained productivity (Demski, 2013).

In this method, any costs of the item or procedure are designed and controlled earlier in

the implementation period, such as production or layout, rather than in the later stage of design

and marketing. Target Costing relates to current and successive product cycles. This starts with a

detailed understanding of business and a desire to meet consumer expectations regarding the

standard of product, functionality, promptness and value.

Target Costing Process:

Ascertain the sales value for new product-item then forecast the industry evaluation

performance as well as the targeted profits.

Finding the targeted cost by subtracting the profits from value of a product-item.

For particular elements and procedures, functional cost benefit analysis.

Determine the predicted cost of the product-item.

Comparing the projected cost to the targeted cost.

When the predicted cost exceeds the intended targeted cost, perform the cost benefit

analysis to minimize the predicted costs.

The ultimate decision on launch of product-item should be made once the projected

costs are on track (Warren, Moffitt and Byrnes, 2015).

Cost management during manufacturing.

The costs specifically affected by it is prioritised throughout the target costing mechanism,

that involves material including purchase components, tooling costs, production costs,

The target-costing is not only a costing tool, but a planning strategy, whereby costs

depend on market situation and take into consideration a variety of variables, including

homogeneous goods, competition rates, no / lower cost adjustments for the end user and so on. If

these considerations are raised, management needs to regulate the prices, since they have limited

or no influence over the sales price. Target costing is a mechanism whereby a corporation plans

its price levels, products cost, and profitability it hopes to accomplish for a fresh product in

advance Unless a product can be developed at these anticipated levels the development process

will be discontinued absolutely. A management department has a valuable mechanism of target

costing to constantly track items from the point they reach the development phase and further

across its product life processes. This is seen as one of the first and most essential tools

throughout the production environment for sustained productivity (Demski, 2013).

In this method, any costs of the item or procedure are designed and controlled earlier in

the implementation period, such as production or layout, rather than in the later stage of design

and marketing. Target Costing relates to current and successive product cycles. This starts with a

detailed understanding of business and a desire to meet consumer expectations regarding the

standard of product, functionality, promptness and value.

Target Costing Process:

Ascertain the sales value for new product-item then forecast the industry evaluation

performance as well as the targeted profits.

Finding the targeted cost by subtracting the profits from value of a product-item.

For particular elements and procedures, functional cost benefit analysis.

Determine the predicted cost of the product-item.

Comparing the projected cost to the targeted cost.

When the predicted cost exceeds the intended targeted cost, perform the cost benefit

analysis to minimize the predicted costs.

The ultimate decision on launch of product-item should be made once the projected

costs are on track (Warren, Moffitt and Byrnes, 2015).

Cost management during manufacturing.

The costs specifically affected by it is prioritised throughout the target costing mechanism,

that involves material including purchase components, tooling costs, production costs,

expenditures for growth and depreciation. It is, however, a systematic cost control strategy, so it

takes into consideration all of those expenses and assets that are affected by the original

determinations on product's planning.

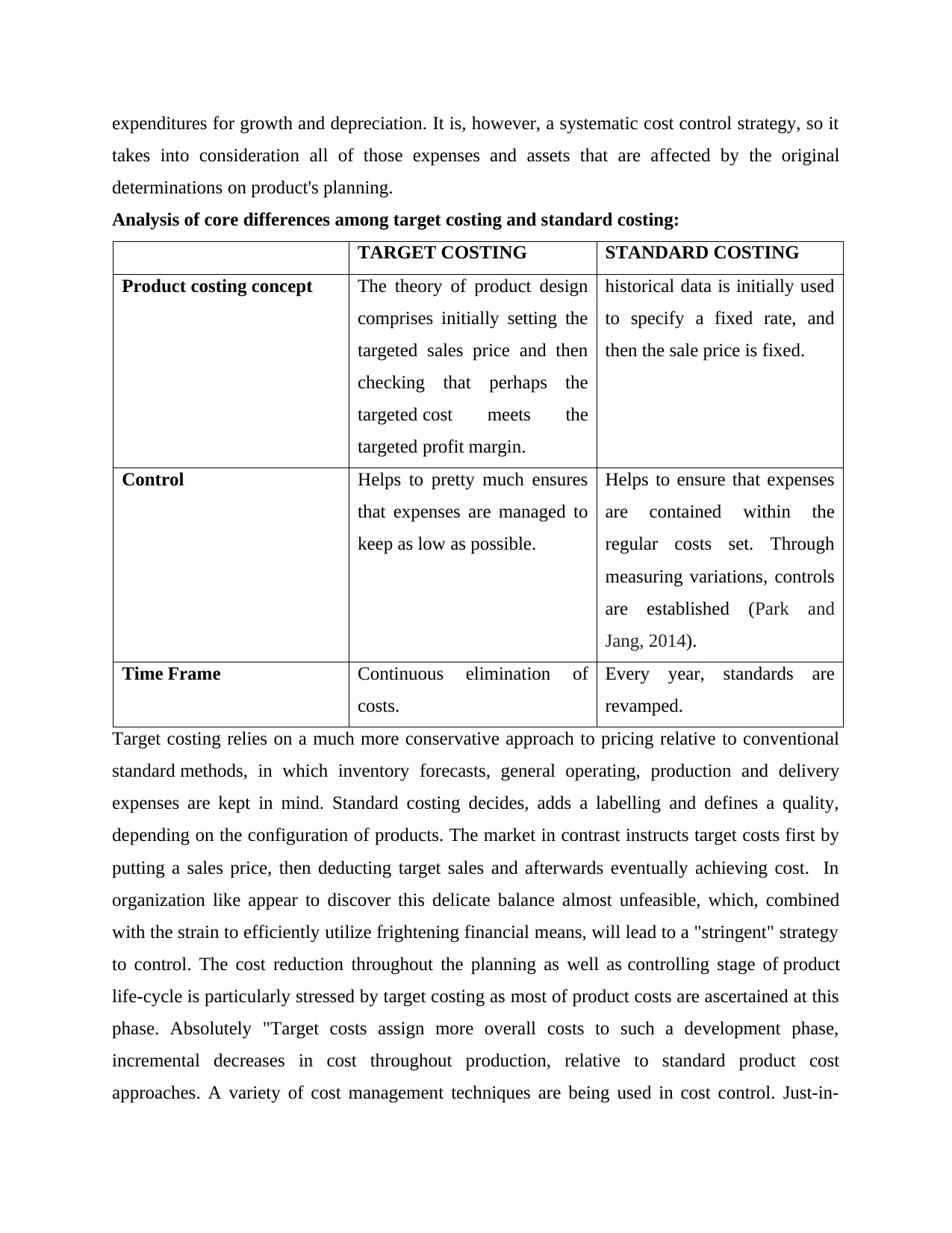

Analysis of core differences among target costing and standard costing:

TARGET COSTING STANDARD COSTING

Product costing concept The theory of product design

comprises initially setting the

targeted sales price and then

checking that perhaps the

targeted cost meets the

targeted profit margin.

historical data is initially used

to specify a fixed rate, and

then the sale price is fixed.

Control Helps to pretty much ensures

that expenses are managed to

keep as low as possible.

Helps to ensure that expenses

are contained within the

regular costs set. Through

measuring variations, controls

are established (Park and

Jang, 2014).

Time Frame Continuous elimination of

costs.

Every year, standards are

revamped.

Target costing relies on a much more conservative approach to pricing relative to conventional

standard methods, in which inventory forecasts, general operating, production and delivery

expenses are kept in mind. Standard costing decides, adds a labelling and defines a quality,

depending on the configuration of products. The market in contrast instructs target costs first by

putting a sales price, then deducting target sales and afterwards eventually achieving cost. In

organization like appear to discover this delicate balance almost unfeasible, which, combined

with the strain to efficiently utilize frightening financial means, will lead to a "stringent" strategy

to control. The cost reduction throughout the planning as well as controlling stage of product

life-cycle is particularly stressed by target costing as most of product costs are ascertained at this

phase. Absolutely "Target costs assign more overall costs to such a development phase,

incremental decreases in cost throughout production, relative to standard product cost

approaches. A variety of cost management techniques are being used in cost control. Just-in-

takes into consideration all of those expenses and assets that are affected by the original

determinations on product's planning.

Analysis of core differences among target costing and standard costing:

TARGET COSTING STANDARD COSTING

Product costing concept The theory of product design

comprises initially setting the

targeted sales price and then

checking that perhaps the

targeted cost meets the

targeted profit margin.

historical data is initially used

to specify a fixed rate, and

then the sale price is fixed.

Control Helps to pretty much ensures

that expenses are managed to

keep as low as possible.

Helps to ensure that expenses

are contained within the

regular costs set. Through

measuring variations, controls

are established (Park and

Jang, 2014).

Time Frame Continuous elimination of

costs.

Every year, standards are

revamped.

Target costing relies on a much more conservative approach to pricing relative to conventional

standard methods, in which inventory forecasts, general operating, production and delivery

expenses are kept in mind. Standard costing decides, adds a labelling and defines a quality,

depending on the configuration of products. The market in contrast instructs target costs first by

putting a sales price, then deducting target sales and afterwards eventually achieving cost. In

organization like appear to discover this delicate balance almost unfeasible, which, combined

with the strain to efficiently utilize frightening financial means, will lead to a "stringent" strategy

to control. The cost reduction throughout the planning as well as controlling stage of product

life-cycle is particularly stressed by target costing as most of product costs are ascertained at this

phase. Absolutely "Target costs assign more overall costs to such a development phase,

incremental decreases in cost throughout production, relative to standard product cost

approaches. A variety of cost management techniques are being used in cost control. Just-in-

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

time, full performance control inventory specifications and quality management are among the

strategies advocated by target costing (Nitzl and Chin, 2017).

(4.) Target costing’s relevancy in today’s competitive and in uncertain business environment:

Target costing is widely advantageous as competition increased intensely and profits were

reduced, as rates were dictated progressively by market pressures instead of simply settling costs

with adequate benefit. Participants of value chain, like manufacturers and suppliers, can often be

helpful. To attempt to foster their innovation and cost management, demands from the industry

can be carried on to expanded firms. Target costing is part of a process of product development.

It begins by comprehending the needs, requirements, and rates for product and the combination

of product, of the user sections in directed competitive markets. The client will show the profit to

be paid for the commodity and its versions. the highest sustainable cost. Margin must be

sustainable throughout the entire life cycle of the company (Bargate, 2012).

ASL is driven to utilize target costing by several considerations. Firstly, it can help

business to define manufacturing costs, which are calculated throughout the design phase in

order to optimize the opportunity for reducing costs by utilizing target costing. In addition, the

cost goal often includes evaluating other issues that may contribute to even more general

management problems. The pace of the competitiveness has become one of the variables which

directly affect industry-driven costs. The magnitude of a company's goal cost increases with the

strength of competition. ASL has continued to distinguish the products from its rivals cantered

on its outstanding functionality. As a result of the decreased competitive pressure, ASL has a

somewhat complex costing mechanism than other businesses. Moreover, when targeted

costing are applied to ASL Company, they are less advantageous than other companies since

each newer generation of ASL products has a greater level of growth. Still, with up-front

investment items, ASL does not need a life-cycle analytical method. If expenditures at the start

are high, the advantages of cost target are smaller. In addition, many factors affecting target

costing processes are detrimental to ASL. Because of its advanced manufacturing, the business

has also built a competitive edge, which allows it to design products which are practically up to

date. Instead of being a market boss, the organization is labelled engineering leader. In fact,

target costing is also an aspect in which market research and costing intersect. Branding and

marketing roles use the cost goal to define the characteristics and sales price of a product. ASL

can regulate all operations with the target costs under this framework. All managers of the

strategies advocated by target costing (Nitzl and Chin, 2017).

(4.) Target costing’s relevancy in today’s competitive and in uncertain business environment:

Target costing is widely advantageous as competition increased intensely and profits were

reduced, as rates were dictated progressively by market pressures instead of simply settling costs

with adequate benefit. Participants of value chain, like manufacturers and suppliers, can often be

helpful. To attempt to foster their innovation and cost management, demands from the industry

can be carried on to expanded firms. Target costing is part of a process of product development.

It begins by comprehending the needs, requirements, and rates for product and the combination

of product, of the user sections in directed competitive markets. The client will show the profit to

be paid for the commodity and its versions. the highest sustainable cost. Margin must be

sustainable throughout the entire life cycle of the company (Bargate, 2012).

ASL is driven to utilize target costing by several considerations. Firstly, it can help

business to define manufacturing costs, which are calculated throughout the design phase in

order to optimize the opportunity for reducing costs by utilizing target costing. In addition, the

cost goal often includes evaluating other issues that may contribute to even more general

management problems. The pace of the competitiveness has become one of the variables which

directly affect industry-driven costs. The magnitude of a company's goal cost increases with the

strength of competition. ASL has continued to distinguish the products from its rivals cantered

on its outstanding functionality. As a result of the decreased competitive pressure, ASL has a

somewhat complex costing mechanism than other businesses. Moreover, when targeted

costing are applied to ASL Company, they are less advantageous than other companies since

each newer generation of ASL products has a greater level of growth. Still, with up-front

investment items, ASL does not need a life-cycle analytical method. If expenditures at the start

are high, the advantages of cost target are smaller. In addition, many factors affecting target

costing processes are detrimental to ASL. Because of its advanced manufacturing, the business

has also built a competitive edge, which allows it to design products which are practically up to

date. Instead of being a market boss, the organization is labelled engineering leader. In fact,

target costing is also an aspect in which market research and costing intersect. Branding and

marketing roles use the cost goal to define the characteristics and sales price of a product. ASL

can regulate all operations with the target costs under this framework. All managers of the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

company participate in the designing and production of the item at target cost (Ibarrondo-Dávila,

López-Alonso and Rubio-Gámez, 2015).

(5.) Systems for contemporary organisations to use for planning purpose:

There are different systems in managerial accounting field and each system has its own

significance and limitations. But based on above discussion and ASL case study, following are

some key systems relevant for planning as well as control, as follows:

Cost Accounting System: It provides a systemic set of standards in which costs of manufacturing

products are tracked and disclosed in depth information in the totality. They include ways in

which such costs are acknowledged, classed, assigned, collated and disclosed and contrasted to

standard costs. The ultimate aim is to inform managers about how to improve business methods

and procedures centred on cost effectiveness and strength. Cost accounting gives details on the

costs of the processes and the long term planning controls for managing. It helps in developing a

framework for effective planning and controls (Halbouni and Hassan, 2012).

Budgeting System: This can function in a number of ways and therefore many methods can be

applied. Budgets may be employed as a predictive and strategic planning tool. This system's

implementation could also be utilized for a motivational mechanism. The system can be

applied as an analysis and monitoring performance and as a data for decision-making tool. In

conjunction to planning or reviewing financial reports and comparing them to actual fiscal

reports, several different methods to budgeting process can also be used according to the

intended purpose of the Organization. For illustration, Breakeven review measures the sales

volume necessary to cover costs for a fresh product.

Control is indeed a key managerial feature. The significance is evident when

company understand that it is important for all management tasks. Command monitors failures

and advises how to handle or face significant obstacles. The organization's success therefore

depends on efficient management. For planning purpose both systems would be efficient for

respective company. While budgeting system is more focused on establishing control over all the

operational activities. Here it has been recommended to ASL that company should adopt these

above discussed systems with aims to establishing efficient proper planning processes and

developing controlling effective framework (Braun, 2013). Adoption of such system will lead to

boost in overall performance of corporation.

López-Alonso and Rubio-Gámez, 2015).

(5.) Systems for contemporary organisations to use for planning purpose:

There are different systems in managerial accounting field and each system has its own

significance and limitations. But based on above discussion and ASL case study, following are

some key systems relevant for planning as well as control, as follows:

Cost Accounting System: It provides a systemic set of standards in which costs of manufacturing

products are tracked and disclosed in depth information in the totality. They include ways in

which such costs are acknowledged, classed, assigned, collated and disclosed and contrasted to

standard costs. The ultimate aim is to inform managers about how to improve business methods

and procedures centred on cost effectiveness and strength. Cost accounting gives details on the

costs of the processes and the long term planning controls for managing. It helps in developing a

framework for effective planning and controls (Halbouni and Hassan, 2012).

Budgeting System: This can function in a number of ways and therefore many methods can be

applied. Budgets may be employed as a predictive and strategic planning tool. This system's

implementation could also be utilized for a motivational mechanism. The system can be

applied as an analysis and monitoring performance and as a data for decision-making tool. In

conjunction to planning or reviewing financial reports and comparing them to actual fiscal

reports, several different methods to budgeting process can also be used according to the

intended purpose of the Organization. For illustration, Breakeven review measures the sales

volume necessary to cover costs for a fresh product.

Control is indeed a key managerial feature. The significance is evident when

company understand that it is important for all management tasks. Command monitors failures

and advises how to handle or face significant obstacles. The organization's success therefore

depends on efficient management. For planning purpose both systems would be efficient for

respective company. While budgeting system is more focused on establishing control over all the

operational activities. Here it has been recommended to ASL that company should adopt these

above discussed systems with aims to establishing efficient proper planning processes and

developing controlling effective framework (Braun, 2013). Adoption of such system will lead to

boost in overall performance of corporation.

CONCLUSION

From above study it has been evaluated that standard costing is still in current environment

is useful however its relevance has been decreased due to target costing. But presently

companies are applying both methods simultaneously to boost their performance by establishing

effective controlling and planning. Moreover, there are several other methods which contributes

in organisational planning and managerial controlling task. One or more systems can be

simultaneously used in a business organisation according to their managerial structure and issues

facing in current market environment.

From above study it has been evaluated that standard costing is still in current environment

is useful however its relevance has been decreased due to target costing. But presently

companies are applying both methods simultaneously to boost their performance by establishing

effective controlling and planning. Moreover, there are several other methods which contributes

in organisational planning and managerial controlling task. One or more systems can be

simultaneously used in a business organisation according to their managerial structure and issues

facing in current market environment.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.