HI5017 Managerial Accounting: Master Budgets & Abilene Oil and Gas

VerifiedAdded on 2023/04/25

|18

|4273

|140

Report

AI Summary

This report provides a comprehensive analysis of master budgets and their elements, contrasting top-down and bottom-up budgeting approaches. It examines sales budgets, direct labor budgets, manufacturing overhead budgets, production budgets, capital acquisition budgets, cash budgets, and budgeted financial statements. The report includes a comparative assessment of top-down and bottom-up budgeting, focusing on the applicability of these methods to Abilene Oil and Gas Ltd. Furthermore, the study includes a budgeted income statement for Abilene Oil and Gas Ltd for 2019 and a comparative data analysis of actual and budgeted income statements for 2018 & 2019. The report concludes with insights into the suitability of different budgeting approaches for specific organizational contexts.

Running head: MANAGERIAL ACCOUNTING

Managerial Accounting

Name of the Student

Name of the University

Authors Note

Course ID

Managerial Accounting

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1MANAGERIAL ACCOUNTING

Executive Summary:

The study would be focusing on the concepts of master budgets and its elements. To support

the study, a comparative analysis would be performed between the top down budgeting

approach and the bottom down budgeting. The report would further address a comparative

assessment of top down and bottom up approach in the budgeting procedure. On making the

comparative assessments of the top down and the bottom down method the study would

further focus on the applicability of the either one methods in the Abilene Oil and Gas Ltd

being the selected company for this study.

Executive Summary:

The study would be focusing on the concepts of master budgets and its elements. To support

the study, a comparative analysis would be performed between the top down budgeting

approach and the bottom down budgeting. The report would further address a comparative

assessment of top down and bottom up approach in the budgeting procedure. On making the

comparative assessments of the top down and the bottom down method the study would

further focus on the applicability of the either one methods in the Abilene Oil and Gas Ltd

being the selected company for this study.

2MANAGERIAL ACCOUNTING

Table of Contents

Introduction:...............................................................................................................................3

Description of Budgeting Elements:..........................................................................................4

Master Budget:.......................................................................................................................4

Elements of master budgets:......................................................................................................5

Sales budget:..........................................................................................................................5

Direct labour budget:..............................................................................................................6

Manufacturing overhead budget:...........................................................................................6

Production budget:.................................................................................................................6

Capital acquisition budget:.....................................................................................................7

Cash budget:...........................................................................................................................7

Budgeted Financial Statements:.............................................................................................8

Comparison between top down and bottom up budgeting process:...........................................8

Top Down Budgeting in Abilene Oil and Gas Ltd:.................................................................10

Budgeted Income Statement of Abilene Oil and Gas Ltd for 2019:........................................11

Comparative data analysis of Actual and Budgeted Income Statement for 2018 & 2019:......12

Conclusion:..............................................................................................................................13

References:...............................................................................................................................14

Table of Contents

Introduction:...............................................................................................................................3

Description of Budgeting Elements:..........................................................................................4

Master Budget:.......................................................................................................................4

Elements of master budgets:......................................................................................................5

Sales budget:..........................................................................................................................5

Direct labour budget:..............................................................................................................6

Manufacturing overhead budget:...........................................................................................6

Production budget:.................................................................................................................6

Capital acquisition budget:.....................................................................................................7

Cash budget:...........................................................................................................................7

Budgeted Financial Statements:.............................................................................................8

Comparison between top down and bottom up budgeting process:...........................................8

Top Down Budgeting in Abilene Oil and Gas Ltd:.................................................................10

Budgeted Income Statement of Abilene Oil and Gas Ltd for 2019:........................................11

Comparative data analysis of Actual and Budgeted Income Statement for 2018 & 2019:......12

Conclusion:..............................................................................................................................13

References:...............................................................................................................................14

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3MANAGERIAL ACCOUNTING

Introduction:

Budgeting is commonly used by several business as the tool of future financial

planning. The main areas of business for which the budgets are prepared includes the

production, labour, trade receivables, and cash and trade receivables in order to offer a

detailed future plans for a period of next twelve months (Kaplan and Atkinson 2015).

Business are required to plan for the future. Planning is formal in larger companies while for

the smaller business planning tends to be less formal. As a general rule, planning for the

different time scales requires adopting different approaches. For medium and long term a

company would enact wider business objectives while for smaller companies the business

objectives are usually discussed by the managers and owners.

Budgets acts as the medium of co-ordinating the entire business functions as a whole.

While forming budgets, several aspects namely, purchase of raw materials, sales possibilities,

production capacity and labour are balanced and co-ordinated in order to assure that all the

activities proceed in agreement with business purposes (Warren and Jones 2018). Co-

ordination forms the essential part in the process of planning. The interrelation among the

functional budgets is essential as without co-ordination one budget cannot be completed

without the reference to numerous other functions.

The report would be assessing the master budgets elements. The report would further

address a comparative assessment of top down and bottom up approach in the budgeting

procedure. On making the comparative assessments of the top down and the bottom down

method the study would further focus on the applicability of the either one methods in the

Abilene Oil and Gas Ltd being the selected company for this study.

Introduction:

Budgeting is commonly used by several business as the tool of future financial

planning. The main areas of business for which the budgets are prepared includes the

production, labour, trade receivables, and cash and trade receivables in order to offer a

detailed future plans for a period of next twelve months (Kaplan and Atkinson 2015).

Business are required to plan for the future. Planning is formal in larger companies while for

the smaller business planning tends to be less formal. As a general rule, planning for the

different time scales requires adopting different approaches. For medium and long term a

company would enact wider business objectives while for smaller companies the business

objectives are usually discussed by the managers and owners.

Budgets acts as the medium of co-ordinating the entire business functions as a whole.

While forming budgets, several aspects namely, purchase of raw materials, sales possibilities,

production capacity and labour are balanced and co-ordinated in order to assure that all the

activities proceed in agreement with business purposes (Warren and Jones 2018). Co-

ordination forms the essential part in the process of planning. The interrelation among the

functional budgets is essential as without co-ordination one budget cannot be completed

without the reference to numerous other functions.

The report would be assessing the master budgets elements. The report would further

address a comparative assessment of top down and bottom up approach in the budgeting

procedure. On making the comparative assessments of the top down and the bottom down

method the study would further focus on the applicability of the either one methods in the

Abilene Oil and Gas Ltd being the selected company for this study.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4MANAGERIAL ACCOUNTING

Description of Budgeting Elements:

Master Budget:

The entire functional segment in an organization is engaged in the preparation of

budgets for a specific division. The master budget forms the sum of all divisional budgets

which is prepared by the divisions (Morden 2016). The master budget also consists of the

financial planning, cash flow forecast and the budget profit and loss statement and statement

of financial position in an organization. The master budget is prepared by the organizations to

attain a certain level during a particular period of time. Usually master budget is prepared for

one year.

Master budget may be misunderstood as the one big budget for an organization but it

is not the case in actual. Rather, master budget represents the summary of the divisional

budgets. Master budget is a continuous financial planning. The master budget is normally

presented either in the monthly or quarterly format and generally takes into the account an

organizations full financial year (Smith 2017). The master budget may also accompany the

explanatory tool that would serve as the explanation for the organizations strategic directions

and how the master budget would help in meeting particular organizational goals along with

management actions required to meet the budget.

According to Otley (2016) master budget the acts as the tool of central planning

which is used by the management team for directing and co-ordinating the activities of the

organization and to judge whether the responsibilities centres are functioning effectively. As

stated by Lymer (2015) it is necessary for the senior management team to review the number

of iterations relating to master budget and introduce modification until a situation is reached

where the budget allocates the necessary funds to attain the obvious objectives.

Description of Budgeting Elements:

Master Budget:

The entire functional segment in an organization is engaged in the preparation of

budgets for a specific division. The master budget forms the sum of all divisional budgets

which is prepared by the divisions (Morden 2016). The master budget also consists of the

financial planning, cash flow forecast and the budget profit and loss statement and statement

of financial position in an organization. The master budget is prepared by the organizations to

attain a certain level during a particular period of time. Usually master budget is prepared for

one year.

Master budget may be misunderstood as the one big budget for an organization but it

is not the case in actual. Rather, master budget represents the summary of the divisional

budgets. Master budget is a continuous financial planning. The master budget is normally

presented either in the monthly or quarterly format and generally takes into the account an

organizations full financial year (Smith 2017). The master budget may also accompany the

explanatory tool that would serve as the explanation for the organizations strategic directions

and how the master budget would help in meeting particular organizational goals along with

management actions required to meet the budget.

According to Otley (2016) master budget the acts as the tool of central planning

which is used by the management team for directing and co-ordinating the activities of the

organization and to judge whether the responsibilities centres are functioning effectively. As

stated by Lymer (2015) it is necessary for the senior management team to review the number

of iterations relating to master budget and introduce modification until a situation is reached

where the budget allocates the necessary funds to attain the obvious objectives.

5MANAGERIAL ACCOUNTING

The master budget is held as the most vital tool for planning in an organization. At the

time of planning the management at top level discusses the profitability, assets and liability

position of the company. Preparation of master budget requires due co-ordination of several

budgets which covers the entire parts of a business and makes the master budget appear more

accurate.

Elements of master budgets:

The master budget elements are given below;

I. Sales budget

II. Direct labour budget

III. Manufacturing overhead budgets

IV. Production budgets

V. Capital acquisition budgets

VI. Cash budgets

VII. Budgeted financial statements

Sales budget:

The sales budget is regarded as the foundation of the master budget. All the

requirements relating to staff, administrative costs and purchase are based on sales. Under

this budget the first step is to determine the number of units to be sold and price per is

obtained. Based on this the sales value is computed (Huikku, Hyvönen and Järvinen 2017).

Preparation of the sales budget is based on the certain factors such as estimation of market

demand, capacity of production or facility for infrastructure, present supply facility and

analysis of industry. The market demand the production capacity is ascertain through the

marketing and production division.

The master budget is held as the most vital tool for planning in an organization. At the

time of planning the management at top level discusses the profitability, assets and liability

position of the company. Preparation of master budget requires due co-ordination of several

budgets which covers the entire parts of a business and makes the master budget appear more

accurate.

Elements of master budgets:

The master budget elements are given below;

I. Sales budget

II. Direct labour budget

III. Manufacturing overhead budgets

IV. Production budgets

V. Capital acquisition budgets

VI. Cash budgets

VII. Budgeted financial statements

Sales budget:

The sales budget is regarded as the foundation of the master budget. All the

requirements relating to staff, administrative costs and purchase are based on sales. Under

this budget the first step is to determine the number of units to be sold and price per is

obtained. Based on this the sales value is computed (Huikku, Hyvönen and Järvinen 2017).

Preparation of the sales budget is based on the certain factors such as estimation of market

demand, capacity of production or facility for infrastructure, present supply facility and

analysis of industry. The market demand the production capacity is ascertain through the

marketing and production division.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6MANAGERIAL ACCOUNTING

Direct labour budget:

The direct labour budget is useful in computing number of labour hours that would be

required to manufacture the itemized units in the production budget. A highly complex direct

labour budget would not only compute the total number of hours required but would also

provide information by breaking the category of labour required (Giuriato, Cepparulo and

Barberi 2016). The direct labour budget is helpful in determining the number of employees

that would be required to staff the area of manufacturing all through the period of budgeting.

This would enable the management to expect the need of hiring along with the schedule of

overtime and when it is most likely to layoff. The direct labor budget helps in giving useful

information regarding the aggregate level and it is not characteristically used for specific

purpose of hiring and requirements relating to layoff.

Manufacturing overhead budget:

The manufacturing overhead comprises of information relating to all the cost of

manufacturing apart from the cost of direct materials and direct labor. The information

provided in the manufacturing overhead budget forms the part of cost of sales line of items in

the master budget (Koochakpour and Tarokh 2017). Furthermore, the total costs of all the

overhead budget is transformed into per unit overhead distribution that is put into use to

obtain the cost of closing finished goods inventory and the same is later incorporated into the

budgeted balance sheet. The information that is provided in this budget forms the most vital

element for all the departmental budgeting models since it comprises of bigger part of total

amount of the organization expenses.

Production budget:

The production budget is helpful in computing the total number of units of a certain

product needs to be produced and it is obtained from the combination of sales forecast and

planned sum of finished goods inventory to have in hand. The main reason for preparing the

Direct labour budget:

The direct labour budget is useful in computing number of labour hours that would be

required to manufacture the itemized units in the production budget. A highly complex direct

labour budget would not only compute the total number of hours required but would also

provide information by breaking the category of labour required (Giuriato, Cepparulo and

Barberi 2016). The direct labour budget is helpful in determining the number of employees

that would be required to staff the area of manufacturing all through the period of budgeting.

This would enable the management to expect the need of hiring along with the schedule of

overtime and when it is most likely to layoff. The direct labor budget helps in giving useful

information regarding the aggregate level and it is not characteristically used for specific

purpose of hiring and requirements relating to layoff.

Manufacturing overhead budget:

The manufacturing overhead comprises of information relating to all the cost of

manufacturing apart from the cost of direct materials and direct labor. The information

provided in the manufacturing overhead budget forms the part of cost of sales line of items in

the master budget (Koochakpour and Tarokh 2017). Furthermore, the total costs of all the

overhead budget is transformed into per unit overhead distribution that is put into use to

obtain the cost of closing finished goods inventory and the same is later incorporated into the

budgeted balance sheet. The information that is provided in this budget forms the most vital

element for all the departmental budgeting models since it comprises of bigger part of total

amount of the organization expenses.

Production budget:

The production budget is helpful in computing the total number of units of a certain

product needs to be produced and it is obtained from the combination of sales forecast and

planned sum of finished goods inventory to have in hand. The main reason for preparing the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7MANAGERIAL ACCOUNTING

production budget is to boost the system of manufacturing as used in the requirements of

material planning (Lowe and Tinker 2015). Presentation of production budget is generally

done either in the monthly or quarterly format. It may be difficult in creating a

comprehensive production budget which incorporates the forecast for each variation in the

product that an organization sells. Therefore, it becomes necessary to aggregate the projection

data into wider categories of products that are having identical characteristics.

Capital acquisition budget:

The property, plant and equipment need monthly maintenance and periodical

replacement as well. If the targeted amount of sales is higher than the previous period then

new there is a need for introducing the new plants and machineries. As a result, careful

planning of the capital asset should be done. The capital acquisition budget usually consists

of two notional categories (Abor 2017). Namely, the fund is set apart for meeting the

committed business liabilities based on the signing of contracts for earlier years and funds

that would be needed to make payment in relation to the new acquisition based on which the

contracts are signed during the present year. In most of the situations the delivery period for

capital assets usually ranges for over number of years. However, only advance payment

which is made throughout the year is associated to pre-defined milestone and stages.

Cash budget:

For each of the divisional budgets every organization would require cash. The cash

budget assures an organization that all through the financial year a business does not runs out

of cash because of inappropriate planning in the preparation of the budget. Based on the

production and sales budget, it is ascertained what would be the anticipated cash receipts and

the amounts that are anticipated to be paid (Miller-Nobles, Mattison and Matsumura 2016).

The receipts and payments of the customer cycle as well as supplier cycle should be

determined. While preparing the cash budget the organization makes the decision whether it

production budget is to boost the system of manufacturing as used in the requirements of

material planning (Lowe and Tinker 2015). Presentation of production budget is generally

done either in the monthly or quarterly format. It may be difficult in creating a

comprehensive production budget which incorporates the forecast for each variation in the

product that an organization sells. Therefore, it becomes necessary to aggregate the projection

data into wider categories of products that are having identical characteristics.

Capital acquisition budget:

The property, plant and equipment need monthly maintenance and periodical

replacement as well. If the targeted amount of sales is higher than the previous period then

new there is a need for introducing the new plants and machineries. As a result, careful

planning of the capital asset should be done. The capital acquisition budget usually consists

of two notional categories (Abor 2017). Namely, the fund is set apart for meeting the

committed business liabilities based on the signing of contracts for earlier years and funds

that would be needed to make payment in relation to the new acquisition based on which the

contracts are signed during the present year. In most of the situations the delivery period for

capital assets usually ranges for over number of years. However, only advance payment

which is made throughout the year is associated to pre-defined milestone and stages.

Cash budget:

For each of the divisional budgets every organization would require cash. The cash

budget assures an organization that all through the financial year a business does not runs out

of cash because of inappropriate planning in the preparation of the budget. Based on the

production and sales budget, it is ascertained what would be the anticipated cash receipts and

the amounts that are anticipated to be paid (Miller-Nobles, Mattison and Matsumura 2016).

The receipts and payments of the customer cycle as well as supplier cycle should be

determined. While preparing the cash budget the organization makes the decision whether it

8MANAGERIAL ACCOUNTING

would require any additional external borrowing or not. At this stage all the administrative

expenditure are to be taken into account while preparing the cash budget.

Budgeted Financial Statements:

The budgeted financial statements includes the full set of financial reports namely;

a. The income statements

b. Statement of financial position

c. Statement of cash flow

d. Statement of retained earnings

The budgeted financial statement is derived from the annual model of business

budgeting. They budgeted financial statement is treated as the useful projection of the

financial results, financial position and cash flow statement of an organization for several

future dates (Lawson et al. 2015). This budget helps in creating new model of budgets where

the management can understand the effect of adjusting the model of budgeting in financial

reports. The administration team of an organization at the time of preparing the budgeting

model brings forward the financial statements which is in accordance with the financial

anticipation and what an organization is ultimately capable of doing.

Comparison between top down and bottom up budgeting process:

Under the top down method of budgeting, the budgets are created at executive

management level and then it passes down to numerous departments. Most often, this budget

is not based on any facts or projections but how an organization can afford every operational

function (Weygandt, Kimmel and Kieso 2015). The most commonly used method of top

down budgeting is the affordable method, percentage sales method, allocation method, return

on investment and competitive parity method.

would require any additional external borrowing or not. At this stage all the administrative

expenditure are to be taken into account while preparing the cash budget.

Budgeted Financial Statements:

The budgeted financial statements includes the full set of financial reports namely;

a. The income statements

b. Statement of financial position

c. Statement of cash flow

d. Statement of retained earnings

The budgeted financial statement is derived from the annual model of business

budgeting. They budgeted financial statement is treated as the useful projection of the

financial results, financial position and cash flow statement of an organization for several

future dates (Lawson et al. 2015). This budget helps in creating new model of budgets where

the management can understand the effect of adjusting the model of budgeting in financial

reports. The administration team of an organization at the time of preparing the budgeting

model brings forward the financial statements which is in accordance with the financial

anticipation and what an organization is ultimately capable of doing.

Comparison between top down and bottom up budgeting process:

Under the top down method of budgeting, the budgets are created at executive

management level and then it passes down to numerous departments. Most often, this budget

is not based on any facts or projections but how an organization can afford every operational

function (Weygandt, Kimmel and Kieso 2015). The most commonly used method of top

down budgeting is the affordable method, percentage sales method, allocation method, return

on investment and competitive parity method.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9MANAGERIAL ACCOUNTING

The decision makers are viewed as the main role players as they are responsible in

formulating a well-organized order that helps in suiting to the types of current problems

(Nazarova et al. 2016). In order to increase the degree of effectiveness the theorists of top

down approach have demanded for clear and consistent statement of policy goals as the

means of reducing the number of engaged actors with the objective of finding policy makers

so that they can guarantee the applications of new statute.

The top down budgeting approach may face the criticism due to its only emphasis on

the formed statute. It disappears the process of discussion that has happened prior to the

agreement on one solution and treats the process of implementation as if there are no

alternative opinion or not political feature relating to problems solutions that may result in

bitterness amid the implementers that have favoured alternative solution (Horngren and

Harrison 2015). The top down approach evidently favours the decision makers since they as

are the key role players and hardly pays any attention towards the administrative staff that

performs the legal act.

The bottom up approach on the other hand is viewed as the build-up approach. At the

time of advertisement and promotions, this approach helps in taking into the account the

overall objectives of the companies that are necessary in meeting the desired objectives.

There are numerous methods related with this approach of budgeting. The most commonly

used method of bottom up approach is the objective and task method (Arora 2016). The

bottom up approach assigns exactly where the top down budgeting represents its biggest

failures by identifying the work of actual implementers. Based on this point of view at the

macro-implementation levels the centrally located actors implements government programs

that react at the macro level plans, develops and implements their own programs.

The decision makers are viewed as the main role players as they are responsible in

formulating a well-organized order that helps in suiting to the types of current problems

(Nazarova et al. 2016). In order to increase the degree of effectiveness the theorists of top

down approach have demanded for clear and consistent statement of policy goals as the

means of reducing the number of engaged actors with the objective of finding policy makers

so that they can guarantee the applications of new statute.

The top down budgeting approach may face the criticism due to its only emphasis on

the formed statute. It disappears the process of discussion that has happened prior to the

agreement on one solution and treats the process of implementation as if there are no

alternative opinion or not political feature relating to problems solutions that may result in

bitterness amid the implementers that have favoured alternative solution (Horngren and

Harrison 2015). The top down approach evidently favours the decision makers since they as

are the key role players and hardly pays any attention towards the administrative staff that

performs the legal act.

The bottom up approach on the other hand is viewed as the build-up approach. At the

time of advertisement and promotions, this approach helps in taking into the account the

overall objectives of the companies that are necessary in meeting the desired objectives.

There are numerous methods related with this approach of budgeting. The most commonly

used method of bottom up approach is the objective and task method (Arora 2016). The

bottom up approach assigns exactly where the top down budgeting represents its biggest

failures by identifying the work of actual implementers. Based on this point of view at the

macro-implementation levels the centrally located actors implements government programs

that react at the macro level plans, develops and implements their own programs.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10MANAGERIAL ACCOUNTING

In contrary to the top down theorist, the bottom up approach theorists have

acknowledged the fact that the implementers at the micro-level think regarding their work

and create their own opinion regarding the task they receive and change the given programs

so that they can enhance them and adopt them better to the real circumstances (Obi 2015).

The theory bottom up theory not only identify this behaviour but also state that the even

positive development of the entire project as worker who is associated with the real state of

affairs can judge better than the policy makers who hardly have the identical information as

the project worker has.

Top Down Budgeting in Abilene Oil and Gas Ltd:

The top down budgeting approach is more appropriate for the Abilene Oil and Gas

Ltd. The main arguments that favours the application of this budgeting approach is that it

would help in introducing the financial sustainability considerations towards the forefront of

the budgeting procedure (Milojević, Andžić and Vladisavljević 2018). The application of top

down budgeting approach in Abilene Oil and Gas Ltd would help in promoting more

informed decision regarding the aggregate expense level for an estimated revenue. Rather

than making huge amount of expenses, Abilene Oil and Gas Ltd can aggregate the total

expenses that would help in automating the consideration associated to the budget size.

Following the automation, Abilene Oil and Gas Ltd can distribute the aggregate expenses

among the important segments.

Implementing the top down budgeting would help the Abilene Oil and Gas Ltd in

projecting its sales towards wide ranging segments of its products by moving out of narrow

categories to much wider line of items (Abilene.com.au 2019). The application of top down

method would enable the company in addressing the business factors namely the channel of

sales, geographical sales regions, customer categories and even the specific customers which

may considerably back the profitability of the company.

In contrary to the top down theorist, the bottom up approach theorists have

acknowledged the fact that the implementers at the micro-level think regarding their work

and create their own opinion regarding the task they receive and change the given programs

so that they can enhance them and adopt them better to the real circumstances (Obi 2015).

The theory bottom up theory not only identify this behaviour but also state that the even

positive development of the entire project as worker who is associated with the real state of

affairs can judge better than the policy makers who hardly have the identical information as

the project worker has.

Top Down Budgeting in Abilene Oil and Gas Ltd:

The top down budgeting approach is more appropriate for the Abilene Oil and Gas

Ltd. The main arguments that favours the application of this budgeting approach is that it

would help in introducing the financial sustainability considerations towards the forefront of

the budgeting procedure (Milojević, Andžić and Vladisavljević 2018). The application of top

down budgeting approach in Abilene Oil and Gas Ltd would help in promoting more

informed decision regarding the aggregate expense level for an estimated revenue. Rather

than making huge amount of expenses, Abilene Oil and Gas Ltd can aggregate the total

expenses that would help in automating the consideration associated to the budget size.

Following the automation, Abilene Oil and Gas Ltd can distribute the aggregate expenses

among the important segments.

Implementing the top down budgeting would help the Abilene Oil and Gas Ltd in

projecting its sales towards wide ranging segments of its products by moving out of narrow

categories to much wider line of items (Abilene.com.au 2019). The application of top down

method would enable the company in addressing the business factors namely the channel of

sales, geographical sales regions, customer categories and even the specific customers which

may considerably back the profitability of the company.

11MANAGERIAL ACCOUNTING

The top down approach is very much suitable for the Abilene Oil and Gas Ltd as it

would help in forecasting the wider aggregate of GDP and make use of historical data to gain

a better understanding of the consumption expenditure (Jaafar, Bakar and Awaludin 2016).

Abilene Oil and Gas Ltd can consider the application of top down approach as the means of

macroeconomic pointers to project the volume of sales and profitability. The adoption of top

down budgeting approach would be more helpful for the Abilene Oil and Gas Ltd as it would

help in streamlining the role of finance department to centrally emphasise on monitoring of

aggregate expenses.

For Abilene Oil and Gas Ltd it is necessary to formally set a limit on the total

expenses at the very early stage of budget preparation. The application of the top down

approach would help in establishing limits by binding on the medium term aggregate expense

ceilings (Vanderbeck and Mitchell 2015). Even though not obtained directly from the concept

of top down approach, a medium term approach towards fiscal policy formulation and

budgeting would be important for Abilene Oil and Gas Ltd in assuring the aggregate level of

expense limit serve the intended purpose of the company.

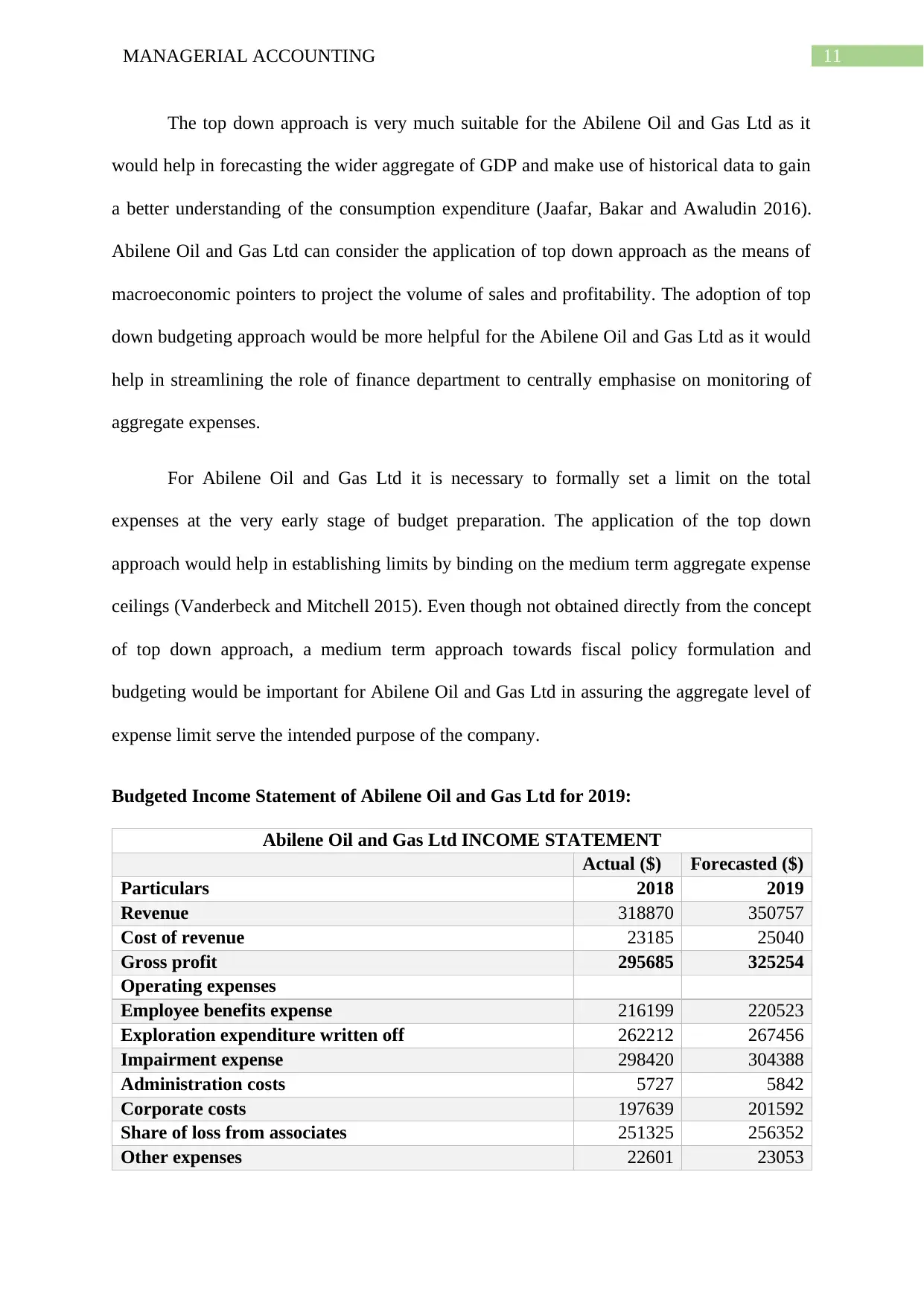

Budgeted Income Statement of Abilene Oil and Gas Ltd for 2019:

Abilene Oil and Gas Ltd INCOME STATEMENT

Actual ($) Forecasted ($)

Particulars 2018 2019

Revenue 318870 350757

Cost of revenue 23185 25040

Gross profit 295685 325254

Operating expenses

Employee benefits expense 216199 220523

Exploration expenditure written off 262212 267456

Impairment expense 298420 304388

Administration costs 5727 5842

Corporate costs 197639 201592

Share of loss from associates 251325 256352

Other expenses 22601 23053

The top down approach is very much suitable for the Abilene Oil and Gas Ltd as it

would help in forecasting the wider aggregate of GDP and make use of historical data to gain

a better understanding of the consumption expenditure (Jaafar, Bakar and Awaludin 2016).

Abilene Oil and Gas Ltd can consider the application of top down approach as the means of

macroeconomic pointers to project the volume of sales and profitability. The adoption of top

down budgeting approach would be more helpful for the Abilene Oil and Gas Ltd as it would

help in streamlining the role of finance department to centrally emphasise on monitoring of

aggregate expenses.

For Abilene Oil and Gas Ltd it is necessary to formally set a limit on the total

expenses at the very early stage of budget preparation. The application of the top down

approach would help in establishing limits by binding on the medium term aggregate expense

ceilings (Vanderbeck and Mitchell 2015). Even though not obtained directly from the concept

of top down approach, a medium term approach towards fiscal policy formulation and

budgeting would be important for Abilene Oil and Gas Ltd in assuring the aggregate level of

expense limit serve the intended purpose of the company.

Budgeted Income Statement of Abilene Oil and Gas Ltd for 2019:

Abilene Oil and Gas Ltd INCOME STATEMENT

Actual ($) Forecasted ($)

Particulars 2018 2019

Revenue 318870 350757

Cost of revenue 23185 25040

Gross profit 295685 325254

Operating expenses

Employee benefits expense 216199 220523

Exploration expenditure written off 262212 267456

Impairment expense 298420 304388

Administration costs 5727 5842

Corporate costs 197639 201592

Share of loss from associates 251325 256352

Other expenses 22601 23053

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.