Managerial Accounting: Performance Measures, Remuneration & Motivation

VerifiedAdded on 2023/04/23

|15

|4424

|60

Report

AI Summary

This report delves into the application of managerial accounting tools and concepts for measuring employee performance and determining remuneration, with a focus on cost management within organizations. It evaluates both financial and non-financial performance measures to optimize individual and corporate rewards, referencing management control theories applicable to organizational settings. Using Amaysim Australia as a case study, the report explores how performance measurement impacts ethical behavior and contributes to achieving organizational goals through effective remuneration strategies, including financial incentives and long-term variable pay methods.

Managerial Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Executive Summary.........................................................................................................................1

Introduction......................................................................................................................................2

Review of topic and review of literature..........................................................................................2

Company review and analysis.........................................................................................................7

Comparison of remuneration methods used to the research............................................................9

Conclusion.....................................................................................................................................10

Referencing....................................................................................................................................12

Executive Summary.........................................................................................................................1

Introduction......................................................................................................................................2

Review of topic and review of literature..........................................................................................2

Company review and analysis.........................................................................................................7

Comparison of remuneration methods used to the research............................................................9

Conclusion.....................................................................................................................................10

Referencing....................................................................................................................................12

Executive Summary

This report emphasis on how the performance of the employees can be measures through

various different accounting tools, also the role of cost management in an organisation through

analysis of different accounting tools and methods has been done. The reader of this report

would be able to evaluate the financial and non-financial performance measures and tools so as

to reward the individual and corporate. Management control theory and concepts which apply to

organisational settings would be checked to generate the accounting and organisational reports.

This report concludes that how performance measurement measures affects the ethical behaviour

of the organisation and how the evaluation of financial and non-financial measures helps in

achieving the desirable gaols.

This report emphasis on how the performance of the employees can be measures through

various different accounting tools, also the role of cost management in an organisation through

analysis of different accounting tools and methods has been done. The reader of this report

would be able to evaluate the financial and non-financial performance measures and tools so as

to reward the individual and corporate. Management control theory and concepts which apply to

organisational settings would be checked to generate the accounting and organisational reports.

This report concludes that how performance measurement measures affects the ethical behaviour

of the organisation and how the evaluation of financial and non-financial measures helps in

achieving the desirable gaols.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Introduction

Managerial accounting in other words also known as the cost accounting is a process of

measuring, identifying, interpreting and communicating the information to the managers so that

an effective decision could be taken to achieve the overall goal of the organisation. This

accounting helps the management in achieving the target of financial leverage for the company

and also helps them setting the employees remunerations by analysing the profit. The company

taken for the purpose of the study is Amaysim Australia which is the leading provider of

subscription based mobile service plans and Australia’s fourth largest mobile service provider.

This report focuses on how the concepts and tools of accounting which helps in analysing the

roles of cost and management in the organisation. Also evaluation of financial and nonfinancial

performance of the company would be checked so remuneration of the employees can be fixed.

At last the report would focus on measuring the performance and reward effort of the employees

so as to achieve the target objectives smoothly.

Review of topic and review of literature

Management accounting is the process of measuring and reporting financial performance

of the company so that it becomes easy for the company to implement the remuneration on the

basis of performance done by the employees of the organisation. It covers all fields of accounting

which is aimed at forming the management of business (Ahmed and Duellman, 2013). The

management accountants use the information that is relating to the cost of the company so that a

fixed remuneration can be set for the employees which would make the company earn maximum

profit without hampering the actual expense. Budgets are used by the company so that it

becomes easy for them to allocate the amount for operations of the business. This is also used so

that planning, performance, evaluation and operational control of management can be achieved.

Planning: it is the management process to analyse and decide as to which product to be made and

where and when it should be made (Maher and et. al., 2012). The management has to determine

the materials, labour, and various other resources that would be used to achieve the desired

output.

Performance evaluation: it is the function of the cost manager to determine the plan with

help of the accounting tools that will fix the remuneration on the basis of performance of

2

Managerial accounting in other words also known as the cost accounting is a process of

measuring, identifying, interpreting and communicating the information to the managers so that

an effective decision could be taken to achieve the overall goal of the organisation. This

accounting helps the management in achieving the target of financial leverage for the company

and also helps them setting the employees remunerations by analysing the profit. The company

taken for the purpose of the study is Amaysim Australia which is the leading provider of

subscription based mobile service plans and Australia’s fourth largest mobile service provider.

This report focuses on how the concepts and tools of accounting which helps in analysing the

roles of cost and management in the organisation. Also evaluation of financial and nonfinancial

performance of the company would be checked so remuneration of the employees can be fixed.

At last the report would focus on measuring the performance and reward effort of the employees

so as to achieve the target objectives smoothly.

Review of topic and review of literature

Management accounting is the process of measuring and reporting financial performance

of the company so that it becomes easy for the company to implement the remuneration on the

basis of performance done by the employees of the organisation. It covers all fields of accounting

which is aimed at forming the management of business (Ahmed and Duellman, 2013). The

management accountants use the information that is relating to the cost of the company so that a

fixed remuneration can be set for the employees which would make the company earn maximum

profit without hampering the actual expense. Budgets are used by the company so that it

becomes easy for them to allocate the amount for operations of the business. This is also used so

that planning, performance, evaluation and operational control of management can be achieved.

Planning: it is the management process to analyse and decide as to which product to be made and

where and when it should be made (Maher and et. al., 2012). The management has to determine

the materials, labour, and various other resources that would be used to achieve the desired

output.

Performance evaluation: it is the function of the cost manager to determine the plan with

help of the accounting tools that will fix the remuneration on the basis of performance of

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

the employees. It also includes the relative contribution of different managers and

different parts of the organisation.

Operations control function: it is the duty of the cost manager to check the operational

functions of the organisation such as knowing the work in progress which is remaining to

be done.

Monitoring and controlling: it is the function of the management to monitor and control

the accounting system by defining the standards against which performance may be

measured through standard cost and budgets that are developed by them (Noreen, Brewer

and Garrison, 2014). The actual results and targets should be measured so that if any

variance that arise between them can be corrected by the different actions taken by them.

Management accounting plays a significant role in the monitoring and control of cost and

efficiency of the routine processes.

Accountability: management accounting plays a significant emphasis on the

accountability through the effective performance measurement. This is done by setting

the targets for the business units and as well as different units.

Budgeting: It is the function of the cost and the management accountant to check that if

the expenses that are done are under the budget of which are allocated to them. It should

be checked that the remuneration that are paid to the employees does not exceed the

remuneration that is budgeted (Otley and Emmanuel, 2013).Various budgets such as cost

budget and the budgets related to operations of the business should be defined and

checked.

Managerial accounting usually collects the information that is financial in nature but

sometimes it collects and reports the non financial information as well.

The role of cost and management in the operation of business is a very vast in nature. The

management is the main body in an organisation on the decision of whom the organisation works

(Altintas an et. al., 2014). It is the body that helps the company to determine the functions and

the ways in which it will achieve the target as prescribed. It is the role of management to plan,

direct and control the business of the organisation so that it is able to achieve maximum profits.

It is the function of the management to take decisions and plan it in a way so that they are able to

achieve the targeted profits. Various accounting tools are used by the management and cost

3

different parts of the organisation.

Operations control function: it is the duty of the cost manager to check the operational

functions of the organisation such as knowing the work in progress which is remaining to

be done.

Monitoring and controlling: it is the function of the management to monitor and control

the accounting system by defining the standards against which performance may be

measured through standard cost and budgets that are developed by them (Noreen, Brewer

and Garrison, 2014). The actual results and targets should be measured so that if any

variance that arise between them can be corrected by the different actions taken by them.

Management accounting plays a significant role in the monitoring and control of cost and

efficiency of the routine processes.

Accountability: management accounting plays a significant emphasis on the

accountability through the effective performance measurement. This is done by setting

the targets for the business units and as well as different units.

Budgeting: It is the function of the cost and the management accountant to check that if

the expenses that are done are under the budget of which are allocated to them. It should

be checked that the remuneration that are paid to the employees does not exceed the

remuneration that is budgeted (Otley and Emmanuel, 2013).Various budgets such as cost

budget and the budgets related to operations of the business should be defined and

checked.

Managerial accounting usually collects the information that is financial in nature but

sometimes it collects and reports the non financial information as well.

The role of cost and management in the operation of business is a very vast in nature. The

management is the main body in an organisation on the decision of whom the organisation works

(Altintas an et. al., 2014). It is the body that helps the company to determine the functions and

the ways in which it will achieve the target as prescribed. It is the role of management to plan,

direct and control the business of the organisation so that it is able to achieve maximum profits.

It is the function of the management to take decisions and plan it in a way so that they are able to

achieve the targeted profits. Various accounting tools are used by the management and cost

3

accountant so that they are able to make work culture in the organisation at a level that is best for

its employees. these tools include the following:

Financial planning: it is the main tool of the management as it includes the ways that will

help in achieving the maximum profit for the organisation (Mihăilă, 2014). By planning the

objectives of the organisation it would be able to achieve the success.

Financial statement analysis: it is the function and the role of the cost and management

accountant to analyse the financial statement of the entity so that it becomes easy for

them to achieve the target of maintaining the profits and the sales and also to prepare a

budget that has to be achieved in the near future.

Fund flow analysis: this is the statement which shows the flow of funds that is being

generated by the organisation so as to achieve the success (Wickramasinghe and

Alawattage, 2012). By analysing the funds flow the management can decide the areas

where the investment is required and the areas where investment can be blocked.

Budgetary control: this is the main function of cost accountant to manage the budgets of

the enterprise so as to achieve maximum profits (Otley, D., 2016). The management

should check and control the remuneration of the employees on the regular basis so that

the employees are paid according to work done by them. They should also fix the

budgets for a specified department which will help in achieving the targeted profits.

Performance management and measurement: it is the function of the management ot

check and evaluate the performance of the employees in the organisation so that it can

be seen who are the employees who are better for the organisation and who are not

(Weygandt, Kimmeland Kieso, 2015). This can be done by key performance indicator

of the employee. As this is used to reflect the organisation success in relation to a

specified goal.

Performance measurement is considered as the function of the organisation that is used to

evaluate both individual and organisational performance (Aly, 2016). Nowadays companies are

focusing on measuring the financial as well as non financial performance of the employees so

that they are able to fix the rewards on the basis of performance. It is the seen that the impact of

performance measurement process helps the company to achieve the participation of the

employees as well as achieving the satisfaction level among them. If the employees participate in

the decision making, then it would provide a base for the management to evaluate the

4

its employees. these tools include the following:

Financial planning: it is the main tool of the management as it includes the ways that will

help in achieving the maximum profit for the organisation (Mihăilă, 2014). By planning the

objectives of the organisation it would be able to achieve the success.

Financial statement analysis: it is the function and the role of the cost and management

accountant to analyse the financial statement of the entity so that it becomes easy for

them to achieve the target of maintaining the profits and the sales and also to prepare a

budget that has to be achieved in the near future.

Fund flow analysis: this is the statement which shows the flow of funds that is being

generated by the organisation so as to achieve the success (Wickramasinghe and

Alawattage, 2012). By analysing the funds flow the management can decide the areas

where the investment is required and the areas where investment can be blocked.

Budgetary control: this is the main function of cost accountant to manage the budgets of

the enterprise so as to achieve maximum profits (Otley, D., 2016). The management

should check and control the remuneration of the employees on the regular basis so that

the employees are paid according to work done by them. They should also fix the

budgets for a specified department which will help in achieving the targeted profits.

Performance management and measurement: it is the function of the management ot

check and evaluate the performance of the employees in the organisation so that it can

be seen who are the employees who are better for the organisation and who are not

(Weygandt, Kimmeland Kieso, 2015). This can be done by key performance indicator

of the employee. As this is used to reflect the organisation success in relation to a

specified goal.

Performance measurement is considered as the function of the organisation that is used to

evaluate both individual and organisational performance (Aly, 2016). Nowadays companies are

focusing on measuring the financial as well as non financial performance of the employees so

that they are able to fix the rewards on the basis of performance. It is the seen that the impact of

performance measurement process helps the company to achieve the participation of the

employees as well as achieving the satisfaction level among them. If the employees participate in

the decision making, then it would provide a base for the management to evaluate the

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

performance of the employees. For this the company should make a performance measurement

system that would play a key role as a source of information about the financial outcomes and

the internal operations which is seen in the company (Miller and Power, 2013). It is the

management thinking to select the performance measurement objectives, it can be selected by the

people who are involved in the organisation. There are various nonfinancial performance

measurement tools that helps in analysing the performance of the employees. These includes the

following:

Key performance indicators: it is the indicator that is used to reflect the company’s

progress in relation to the overall objectives. The purpose of this is to monitor the progress that is

done towards accomplishing the plans that are developed by the management in their strategy

plans (Arruñada, and Hansen, 2015)

These are typically included in reporting the scorecards which enables the

management and the board to focus on the metrics which are most important so as to

achieve the organisational goals (Walther, 2013). These are also based on the

financial key performance activities of the organisation such as income statement,

balance sheets etc. also the non financial performance indicators include the

measures that relates to customer satisfaction, supply chain management of the

organisation etc.

It is seen that if the performance of the company is good and the employees are

contributing to make the company achieve its objective then company has to plan a

way that will reward the employees and the organisation as a whole.

There are various ways through which the financial and non financial performance of the

employees can be rewarded and be better implemented so as to motivate the employees to

perform in a better way (Datar, Rajan, and Horngren, 2013).

As financial techniques refer to a monetary reward that are given to the employees. It is

the incentives that are paid to them so as to motivate them. It should include the direct

relationship between the efforts and the rewards of the employees.

Reward strategy of the company to give reward to the key managerial person of the

company includes attracting and retaining the best person so that annual targets can be achieved.

These are only applicable in the case of key managerial persons (Needles, and et. al., 2013.).

Apart from the fixed remuneration that is to be paid to the employee the company should

5

system that would play a key role as a source of information about the financial outcomes and

the internal operations which is seen in the company (Miller and Power, 2013). It is the

management thinking to select the performance measurement objectives, it can be selected by the

people who are involved in the organisation. There are various nonfinancial performance

measurement tools that helps in analysing the performance of the employees. These includes the

following:

Key performance indicators: it is the indicator that is used to reflect the company’s

progress in relation to the overall objectives. The purpose of this is to monitor the progress that is

done towards accomplishing the plans that are developed by the management in their strategy

plans (Arruñada, and Hansen, 2015)

These are typically included in reporting the scorecards which enables the

management and the board to focus on the metrics which are most important so as to

achieve the organisational goals (Walther, 2013). These are also based on the

financial key performance activities of the organisation such as income statement,

balance sheets etc. also the non financial performance indicators include the

measures that relates to customer satisfaction, supply chain management of the

organisation etc.

It is seen that if the performance of the company is good and the employees are

contributing to make the company achieve its objective then company has to plan a

way that will reward the employees and the organisation as a whole.

There are various ways through which the financial and non financial performance of the

employees can be rewarded and be better implemented so as to motivate the employees to

perform in a better way (Datar, Rajan, and Horngren, 2013).

As financial techniques refer to a monetary reward that are given to the employees. It is

the incentives that are paid to them so as to motivate them. It should include the direct

relationship between the efforts and the rewards of the employees.

Reward strategy of the company to give reward to the key managerial person of the

company includes attracting and retaining the best person so that annual targets can be achieved.

These are only applicable in the case of key managerial persons (Needles, and et. al., 2013.).

Apart from the fixed remuneration that is to be paid to the employee the company should

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

formulate a plan such as STI plan that would enable them to achieve the organisational goals. It

should be linked to the performance of the organisation as if the company performs in a better

way the better would be the key managerial person remuneration will be.

It is investigated that relationship between the executive remuneration and the company’s

performance helps the company to achieve the target in a better way. As the STI framework

helps the managers to achieve maximum remuneration that is based on the performance of the

company. It includes the scorecard that gives the data on both the financial and nonfinancial

performance of the company and on the basis of which the incentive of the key managerial

person is fixed (Demerjian, and et. al., 2012)

The higher the scorecard the higher the remuneration of the employee. It is equally

important to have a link between the STI design and the STI payment methods. Payments should

be done on the basis of both overall and the individual performance. it should focus more on the

whole company performance.

The other method that is implanted to pay the employees is the long term variable pay

method. It should be designed in a way that it helps in incorporating the performance measures

and reflects the company’s needs (Lohr, 2012). This helps in bringing the similarity in long term

strategy across the majority of the companies. It can also reflect different performance focus

depending on the group selected and the way the performance is measured. These are the various

ways through which the rewards in the organisation can be given to employees while evaluating

their financial performance.

Organisational control is an issue that arise in front of the managers so that they are able

to achieve the target of socio political and corporate governance. It is important also as if there is

failure in the management control than it can lead to financial loss and reputation damage of the

company (Demski, 2013). So the management should at times check the overall financial

performance of the organisation. With the help of analysing the financial documents of the

company they can set the target for the future. They would be able to fix the required amount of

sales that they desire so that the maximum profit could be achieved accordingly. The

management control has two basic control functions which includes the following:

Strategic control: this is the process of monitoring whether the various strategies that

are adopted by the organisation are helping in achieving the organisational goals or

not.

6

should be linked to the performance of the organisation as if the company performs in a better

way the better would be the key managerial person remuneration will be.

It is investigated that relationship between the executive remuneration and the company’s

performance helps the company to achieve the target in a better way. As the STI framework

helps the managers to achieve maximum remuneration that is based on the performance of the

company. It includes the scorecard that gives the data on both the financial and nonfinancial

performance of the company and on the basis of which the incentive of the key managerial

person is fixed (Demerjian, and et. al., 2012)

The higher the scorecard the higher the remuneration of the employee. It is equally

important to have a link between the STI design and the STI payment methods. Payments should

be done on the basis of both overall and the individual performance. it should focus more on the

whole company performance.

The other method that is implanted to pay the employees is the long term variable pay

method. It should be designed in a way that it helps in incorporating the performance measures

and reflects the company’s needs (Lohr, 2012). This helps in bringing the similarity in long term

strategy across the majority of the companies. It can also reflect different performance focus

depending on the group selected and the way the performance is measured. These are the various

ways through which the rewards in the organisation can be given to employees while evaluating

their financial performance.

Organisational control is an issue that arise in front of the managers so that they are able

to achieve the target of socio political and corporate governance. It is important also as if there is

failure in the management control than it can lead to financial loss and reputation damage of the

company (Demski, 2013). So the management should at times check the overall financial

performance of the organisation. With the help of analysing the financial documents of the

company they can set the target for the future. They would be able to fix the required amount of

sales that they desire so that the maximum profit could be achieved accordingly. The

management control has two basic control functions which includes the following:

Strategic control: this is the process of monitoring whether the various strategies that

are adopted by the organisation are helping in achieving the organisational goals or

not.

6

Management control: this is the function that includes the planning and organising

the operations so as to achieve organisations target on time.

Management controls are necessary to safeguard against possibilities that external environment

does against the organization.

Company review and analysis

Amaysim Australia is a leading provider of subscription based mobile service plans. It was

founded in the year 2010 and id the fourth largest service provider in Australia. The revenue of

the company in the year 2018 was around 212.6$ Mn which is a benchmark for various other

companies (Dierynck, Landsman and Renders, 2012). It is the public registered company with

number of employees around 130. The CEO of the company is Peter 0’Connell. The company

was listed on the Australian securities exchange on 15th July 2015 and has obtained a solid

growth since then. It was discovered that the companies KMP earned 60% if their maximum

remuneration that was given them as an opportunity from STI method. The directors of the

company involve the following

Andrew Reitzer Chairman

Julian Ogrin Chief Executive Officer and Managing Director

Rolf Hansen Non-independent* Non-Executive Director

Thorsten Kraemer Independent Non-Executive Director

Maria Martin Independent Non-Executive Director

Peter O’Connell Non-independent* Non-Executive Director

Jodie Sangster Independent Non-Executive Director

The report of the company includes the remuneration that is paid to the KMP who are

directly or indirectly responsible for planning and directing and controlling the functions of the

organisation. The company has formed a strategy to reward the members through the STI and

LTI programme. The KMP of the company would be entitled to receive the fixed remuneration

which includes the following;

Basic salary

Superannuation

Non-monetary benefits

7

the operations so as to achieve organisations target on time.

Management controls are necessary to safeguard against possibilities that external environment

does against the organization.

Company review and analysis

Amaysim Australia is a leading provider of subscription based mobile service plans. It was

founded in the year 2010 and id the fourth largest service provider in Australia. The revenue of

the company in the year 2018 was around 212.6$ Mn which is a benchmark for various other

companies (Dierynck, Landsman and Renders, 2012). It is the public registered company with

number of employees around 130. The CEO of the company is Peter 0’Connell. The company

was listed on the Australian securities exchange on 15th July 2015 and has obtained a solid

growth since then. It was discovered that the companies KMP earned 60% if their maximum

remuneration that was given them as an opportunity from STI method. The directors of the

company involve the following

Andrew Reitzer Chairman

Julian Ogrin Chief Executive Officer and Managing Director

Rolf Hansen Non-independent* Non-Executive Director

Thorsten Kraemer Independent Non-Executive Director

Maria Martin Independent Non-Executive Director

Peter O’Connell Non-independent* Non-Executive Director

Jodie Sangster Independent Non-Executive Director

The report of the company includes the remuneration that is paid to the KMP who are

directly or indirectly responsible for planning and directing and controlling the functions of the

organisation. The company has formed a strategy to reward the members through the STI and

LTI programme. The KMP of the company would be entitled to receive the fixed remuneration

which includes the following;

Basic salary

Superannuation

Non-monetary benefits

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

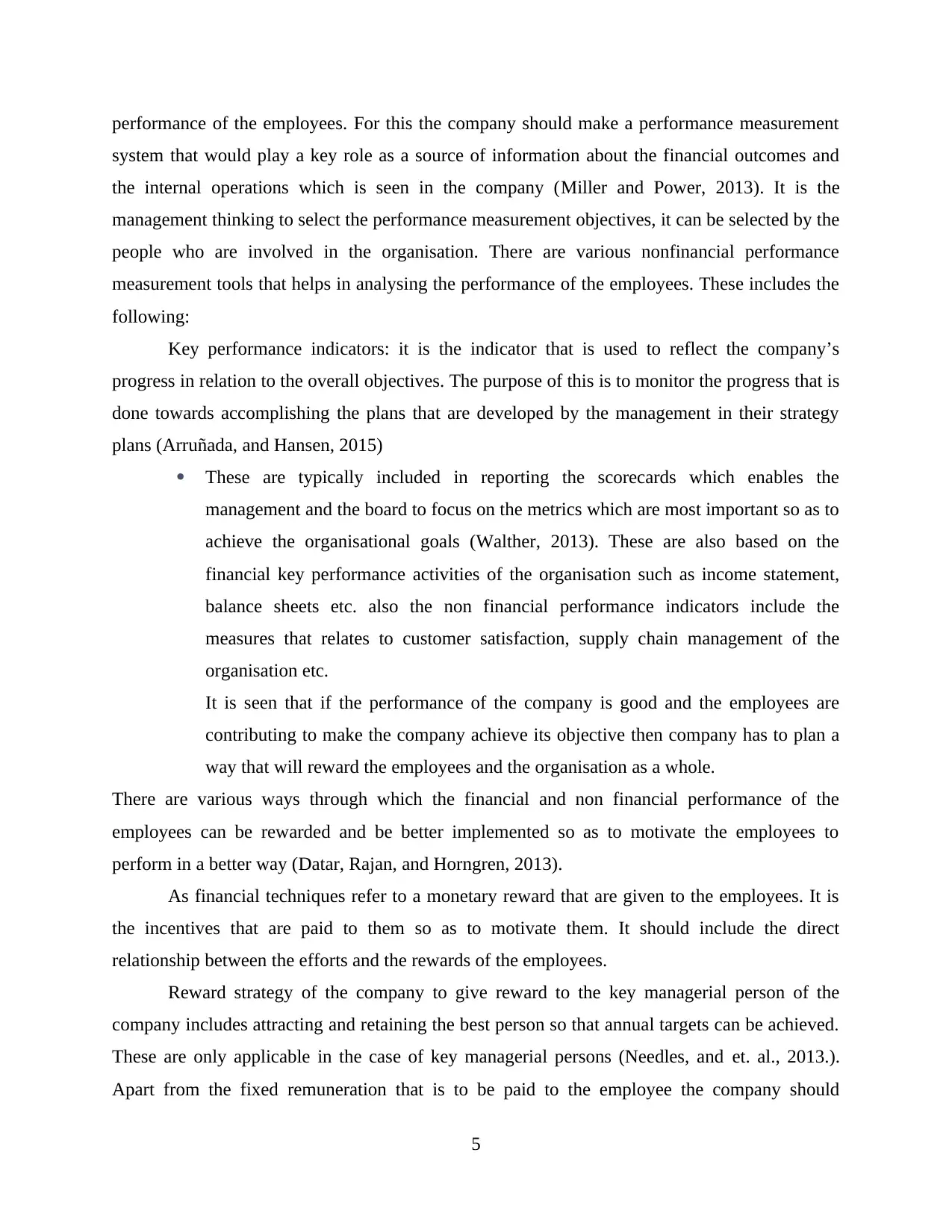

Illustration 1: Remuneration mix

They also are entitled to receive STI which would be on the basis of annual performance

relative to financial and non-financial KPI’s. Also LTI would be delivers as options. For LTI the

performance would be measured over three four and five-year period.

The chart above explains the maximum remuneration that would be paid to the KMP. It is

the chart of remuneration mix that would underlie the remuneration payable to the employee.

For STI plan eligibility is only to executive KMP (Hilton, and Platt, 2013). This is the

plan that has been developed to motivate and reward executive KMP for the achievement of

annual performance targets. This has been done as maximum STI opportunity is set for each

Executive KMP based on the executive’s role and responsibilities. For FY17 the CEO’s

maximum STI opportunity was 75% of fixed remuneration, and 30-50% of fixed remuneration

for other Executive KMP. The performance was assessed through the CEO’s performance

relative to annual KPIs is assessed by the Chair of the Board, in conjunction with the

Remuneration and Nomination Committee (Kanellou and Spathis, 2013). The CEO’s STI award

(if any) is approved by the Amaysim Board. The performance of all other Executive KMP is

assessed by the CEO, for recommendation to the Remuneration and Nomination Committee and

approval by the Amaysim Board.

Also the LTI was introduces so as to retain the executive talent and align the interests of

the executive KMP with shareholders and to incentivise the executives KMP to deliver the

8

They also are entitled to receive STI which would be on the basis of annual performance

relative to financial and non-financial KPI’s. Also LTI would be delivers as options. For LTI the

performance would be measured over three four and five-year period.

The chart above explains the maximum remuneration that would be paid to the KMP. It is

the chart of remuneration mix that would underlie the remuneration payable to the employee.

For STI plan eligibility is only to executive KMP (Hilton, and Platt, 2013). This is the

plan that has been developed to motivate and reward executive KMP for the achievement of

annual performance targets. This has been done as maximum STI opportunity is set for each

Executive KMP based on the executive’s role and responsibilities. For FY17 the CEO’s

maximum STI opportunity was 75% of fixed remuneration, and 30-50% of fixed remuneration

for other Executive KMP. The performance was assessed through the CEO’s performance

relative to annual KPIs is assessed by the Chair of the Board, in conjunction with the

Remuneration and Nomination Committee (Kanellou and Spathis, 2013). The CEO’s STI award

(if any) is approved by the Amaysim Board. The performance of all other Executive KMP is

assessed by the CEO, for recommendation to the Remuneration and Nomination Committee and

approval by the Amaysim Board.

Also the LTI was introduces so as to retain the executive talent and align the interests of

the executive KMP with shareholders and to incentivise the executives KMP to deliver the

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

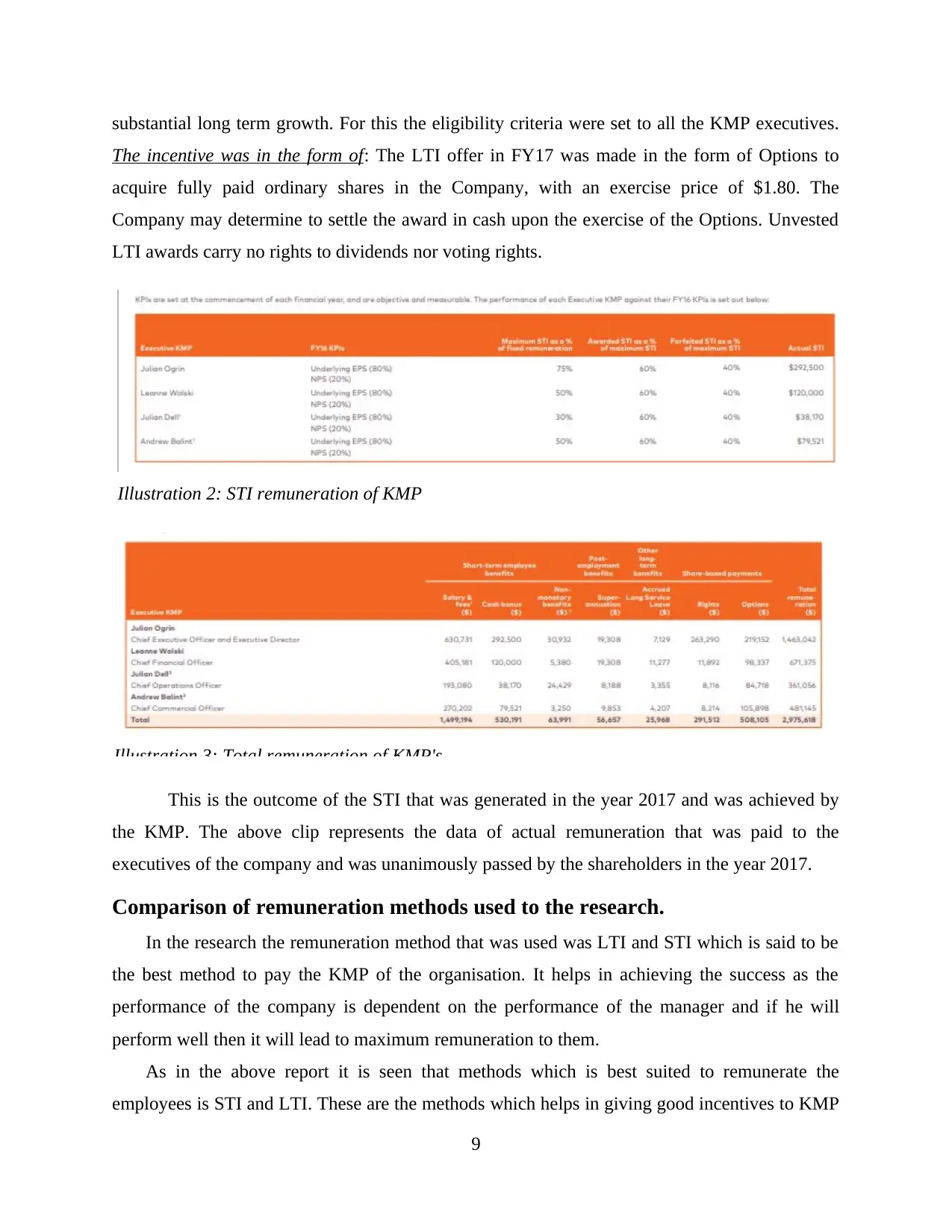

Illustration 2: STI remuneration of KMP

Illustration 3: Total remuneration of KMP's

substantial long term growth. For this the eligibility criteria were set to all the KMP executives.

The incentive was in the form of: The LTI offer in FY17 was made in the form of Options to

acquire fully paid ordinary shares in the Company, with an exercise price of $1.80. The

Company may determine to settle the award in cash upon the exercise of the Options. Unvested

LTI awards carry no rights to dividends nor voting rights.

This is the outcome of the STI that was generated in the year 2017 and was achieved by

the KMP. The above clip represents the data of actual remuneration that was paid to the

executives of the company and was unanimously passed by the shareholders in the year 2017.

Comparison of remuneration methods used to the research.

In the research the remuneration method that was used was LTI and STI which is said to be

the best method to pay the KMP of the organisation. It helps in achieving the success as the

performance of the company is dependent on the performance of the manager and if he will

perform well then it will lead to maximum remuneration to them.

As in the above report it is seen that methods which is best suited to remunerate the

employees is STI and LTI. These are the methods which helps in giving good incentives to KMP

9

Illustration 3: Total remuneration of KMP's

substantial long term growth. For this the eligibility criteria were set to all the KMP executives.

The incentive was in the form of: The LTI offer in FY17 was made in the form of Options to

acquire fully paid ordinary shares in the Company, with an exercise price of $1.80. The

Company may determine to settle the award in cash upon the exercise of the Options. Unvested

LTI awards carry no rights to dividends nor voting rights.

This is the outcome of the STI that was generated in the year 2017 and was achieved by

the KMP. The above clip represents the data of actual remuneration that was paid to the

executives of the company and was unanimously passed by the shareholders in the year 2017.

Comparison of remuneration methods used to the research.

In the research the remuneration method that was used was LTI and STI which is said to be

the best method to pay the KMP of the organisation. It helps in achieving the success as the

performance of the company is dependent on the performance of the manager and if he will

perform well then it will lead to maximum remuneration to them.

As in the above report it is seen that methods which is best suited to remunerate the

employees is STI and LTI. These are the methods which helps in giving good incentives to KMP

9

through which the performance of organisation can be increased (Songini, Gnan, and Malmi,

2013). As it can be seen from the report that if the managers are paid incentives according the

STI or LTI model then it leads to increase the profitability for the stakeholders.

In the context of the company they have also chosen the method of LTI and STI to pay

incentives to the employees therefore it is the considered to be the best method for the

remuneration (Krapp, Nebel and Sahamie, 2013). They have given the employees performance

measurement and vesting options as same discussed in the report. The performance that is

assessed against key performance indicators to ensure that the company’s growth strategy and

financial objectives are achieved in a better way. They have used the EPS scheme has been

selected by the organisation so as to metric the performance of the employees. This incorporates

the executives KMP can control and allows the board to measure operational management of the

company.

They have also taken NPS as a measure to analyse the performance of the mangers. It is

done by analysing the external environment of the firms (Kravet, 2014). They have made a plan

that would conduct four NPS survey during the financial year. Every KPI operates independently

and is expressed in a manner that helps in achieving the maximum STI for the KMP.

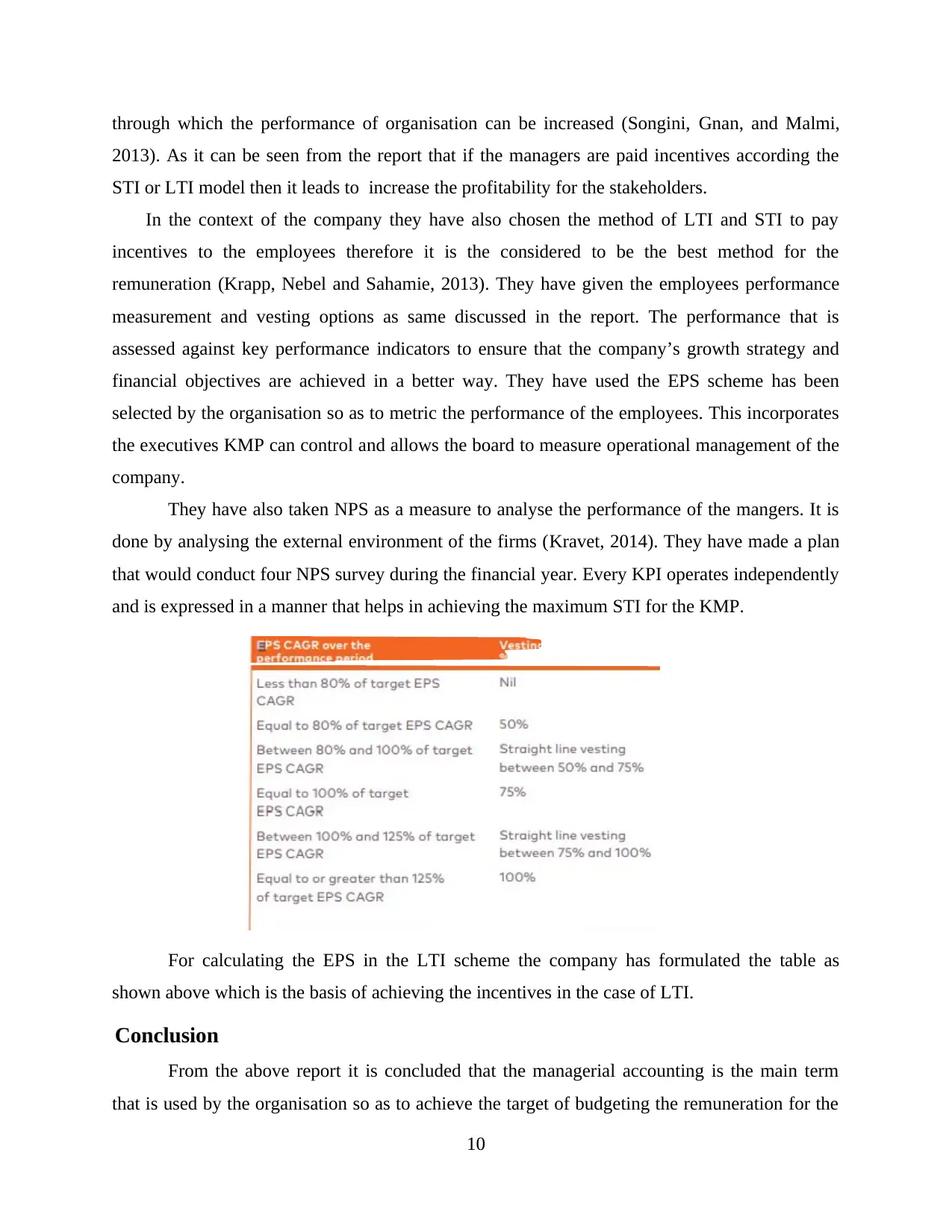

For calculating the EPS in the LTI scheme the company has formulated the table as

shown above which is the basis of achieving the incentives in the case of LTI.

Conclusion

From the above report it is concluded that the managerial accounting is the main term

that is used by the organisation so as to achieve the target of budgeting the remuneration for the

10

2013). As it can be seen from the report that if the managers are paid incentives according the

STI or LTI model then it leads to increase the profitability for the stakeholders.

In the context of the company they have also chosen the method of LTI and STI to pay

incentives to the employees therefore it is the considered to be the best method for the

remuneration (Krapp, Nebel and Sahamie, 2013). They have given the employees performance

measurement and vesting options as same discussed in the report. The performance that is

assessed against key performance indicators to ensure that the company’s growth strategy and

financial objectives are achieved in a better way. They have used the EPS scheme has been

selected by the organisation so as to metric the performance of the employees. This incorporates

the executives KMP can control and allows the board to measure operational management of the

company.

They have also taken NPS as a measure to analyse the performance of the mangers. It is

done by analysing the external environment of the firms (Kravet, 2014). They have made a plan

that would conduct four NPS survey during the financial year. Every KPI operates independently

and is expressed in a manner that helps in achieving the maximum STI for the KMP.

For calculating the EPS in the LTI scheme the company has formulated the table as

shown above which is the basis of achieving the incentives in the case of LTI.

Conclusion

From the above report it is concluded that the managerial accounting is the main term

that is used by the organisation so as to achieve the target of budgeting the remuneration for the

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.