Managerial Accounting Report: PWC Value-Framework Analysis

VerifiedAdded on 2020/03/28

|34

|2200

|465

Report

AI Summary

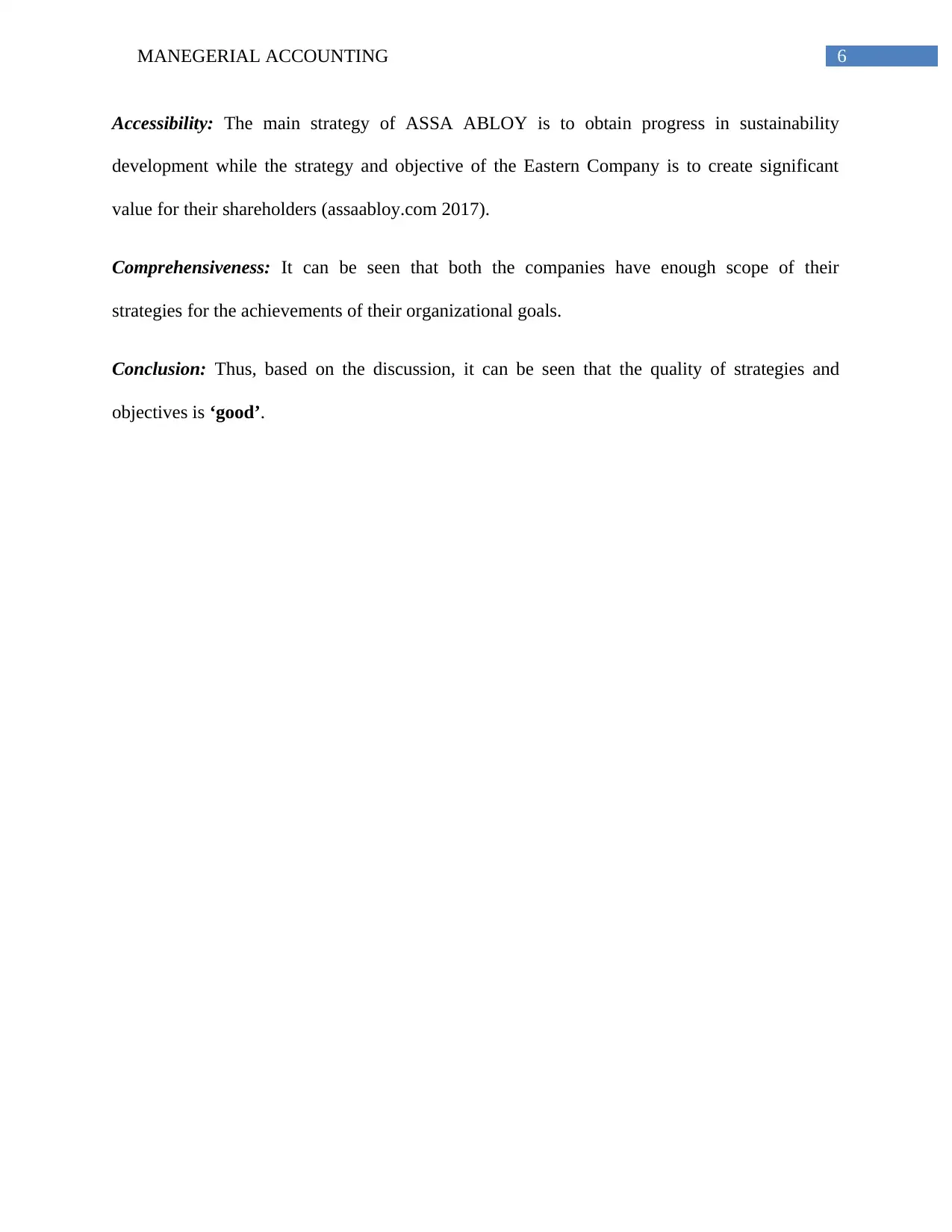

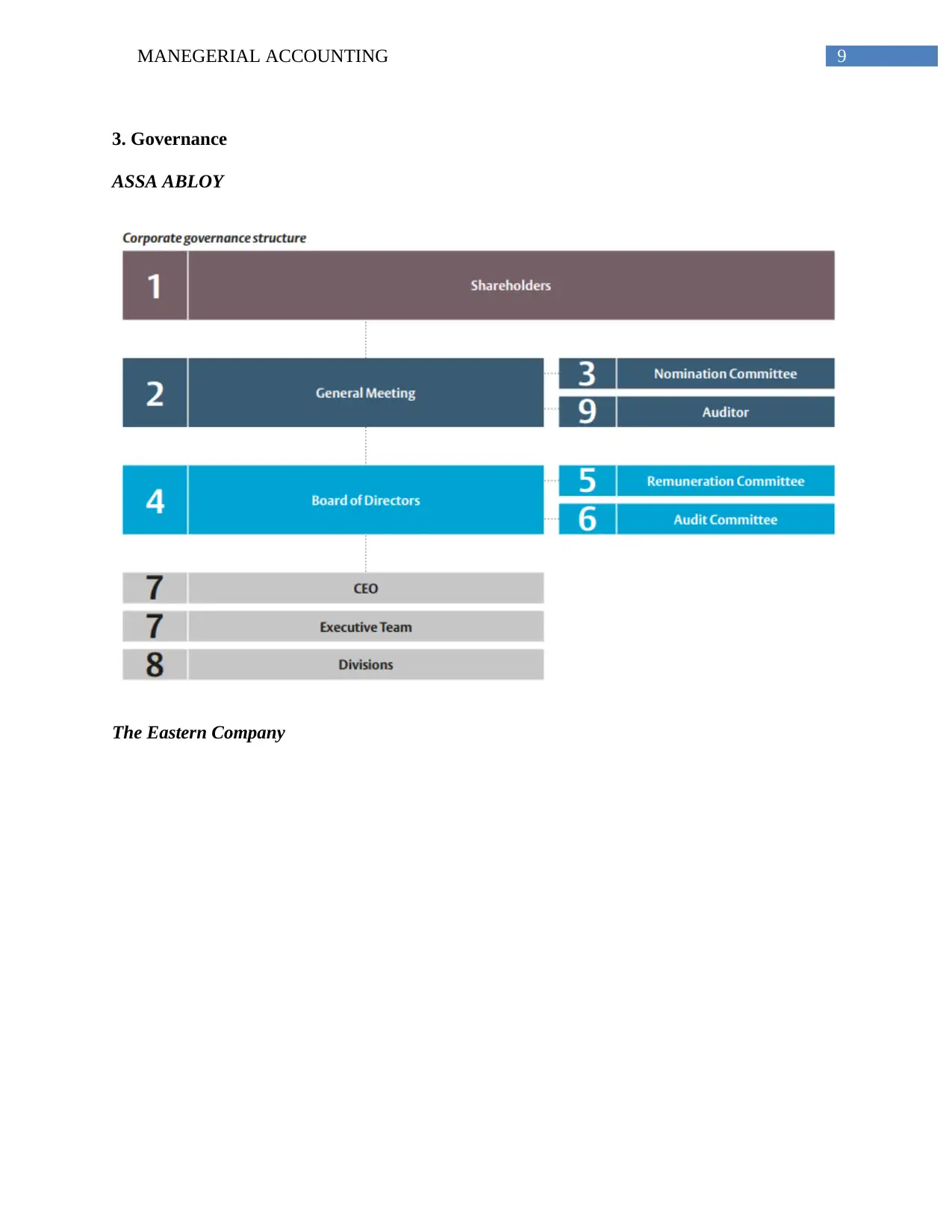

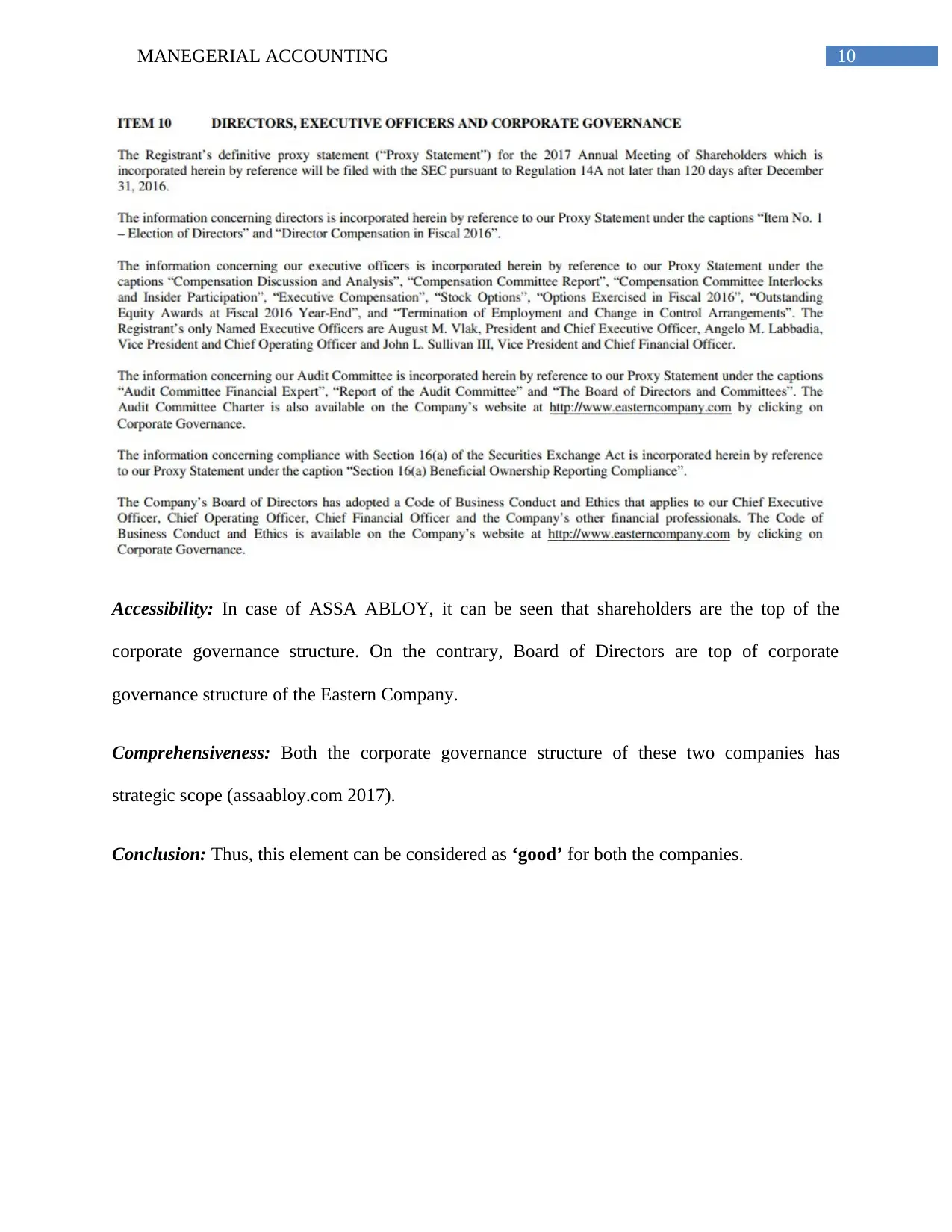

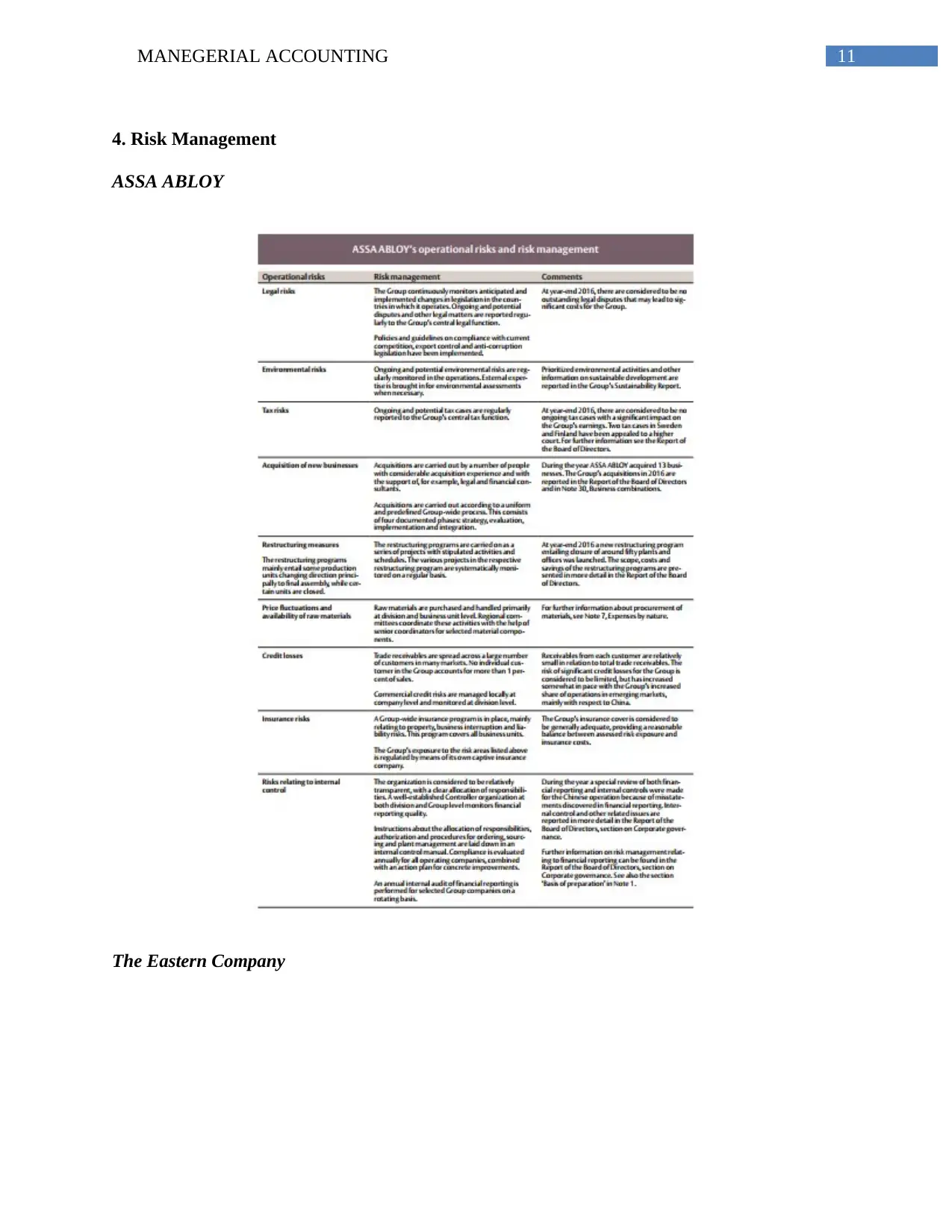

This report offers a comprehensive analysis of managerial accounting, focusing on the application of the PWC Value-Framework to assess the business performance of ASSA ABLOY and The Eastern Company. The report dissects seventeen key elements of the PWC Value-Framework, including strategy and objectives, business models, governance, risk management, remuneration, financial and physical assets, customer relations, people and culture, innovation, intellectual assets, processes and supply chains, operational, economic, social, and environmental performance, as well as segmental reporting. Each element is evaluated based on accessibility, comprehensiveness, and overall conclusion. The analysis highlights the strengths and weaknesses of both companies across these different areas, providing insights into their strategic approaches and operational effectiveness. The report also examines the reporting of material matters for both companies, detailing their methods for identifying and addressing potential misstatements in financial reports. The findings provide a comparative perspective on the companies' management accounting practices and their alignment with the PWC Value-Framework principles.

1 out of 34

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.