Managerial Accounting Report: Evaluating Organizational Performance

VerifiedAdded on 2023/01/11

|18

|5588

|54

Report

AI Summary

This report delves into the realm of managerial accounting, exploring its significance in organizational decision-making and performance evaluation. It begins by defining managerial accounting, differentiating it from financial accounting, and outlining essential requirements for various managerial accounting systems, including management styles, organizational structures, and information needs. The report then examines diverse methods of managerial accounting reporting, such as cost schedules, budget reports, performance reports, and variance analysis, emphasizing their roles in cost control, financial planning, and performance assessment. Furthermore, the report delves into cost calculation techniques, including marginal and absorption costing, and their application in preparing income statements. It also addresses the advantages and disadvantages of planning tools used for budgetary control, and how organizations adapt managerial accounting systems to address financial problems. The report concludes by analyzing how managerial accounting can drive sustainable success by effectively responding to financial challenges through the utilization of planning tools. The report uses Creams Ltd. as a case study to illustrate these concepts.

Managerial

Accounting

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...........................................................................................................................................3

LO 1..............................................................................................................................................................4

P1 Explain management accounting and give the essential requirements of different types of

management accounting systems. ..........................................................................................................4

P2 Explain different methods used for management accounting reporting. ..........................................6

M1 Evaluate the benefits of management accounting systems and their application within an

organisational context.............................................................................................................................7

D1 Critically evaluate how management accounting systems and management accounting reporting is

integrated within organisational processes. ...........................................................................................7

LO 2..............................................................................................................................................................8

P3 Calculate costs using appropriate techniques of cost analysis to prepare an income statement using

marginal and absorption costs.................................................................................................................8

M2 Accurately apply a range of management accounting techniques and produce appropriate

financial reporting documents. .............................................................................................................10

D2 Produce financial reports that accurately apply and interpret data for a range of business activities.

...............................................................................................................................................................11

LO 3............................................................................................................................................................11

P4 Explain the advantages and disadvantages of different types of planning tools used for budgetary

control...................................................................................................................................................11

M3 Analyse the use of different planning tools and their application for preparing budgets and

forecasts. ..............................................................................................................................................13

LO 4............................................................................................................................................................13

P5 Compare how organizations are adapting management accounting systems to respond to financial

problems................................................................................................................................................13

M4 Analyse how, in responding to financial problems, management accounting can lead organisations

to sustainable success............................................................................................................................14

D3 Evaluate how planning tools for accounting respond appropriately to solving financial problems to

lead organisations to sustainable success. ............................................................................................14

CONCLUSION.............................................................................................................................................15

REFERENCES..............................................................................................................................................15

INTRODUCTION...........................................................................................................................................3

LO 1..............................................................................................................................................................4

P1 Explain management accounting and give the essential requirements of different types of

management accounting systems. ..........................................................................................................4

P2 Explain different methods used for management accounting reporting. ..........................................6

M1 Evaluate the benefits of management accounting systems and their application within an

organisational context.............................................................................................................................7

D1 Critically evaluate how management accounting systems and management accounting reporting is

integrated within organisational processes. ...........................................................................................7

LO 2..............................................................................................................................................................8

P3 Calculate costs using appropriate techniques of cost analysis to prepare an income statement using

marginal and absorption costs.................................................................................................................8

M2 Accurately apply a range of management accounting techniques and produce appropriate

financial reporting documents. .............................................................................................................10

D2 Produce financial reports that accurately apply and interpret data for a range of business activities.

...............................................................................................................................................................11

LO 3............................................................................................................................................................11

P4 Explain the advantages and disadvantages of different types of planning tools used for budgetary

control...................................................................................................................................................11

M3 Analyse the use of different planning tools and their application for preparing budgets and

forecasts. ..............................................................................................................................................13

LO 4............................................................................................................................................................13

P5 Compare how organizations are adapting management accounting systems to respond to financial

problems................................................................................................................................................13

M4 Analyse how, in responding to financial problems, management accounting can lead organisations

to sustainable success............................................................................................................................14

D3 Evaluate how planning tools for accounting respond appropriately to solving financial problems to

lead organisations to sustainable success. ............................................................................................14

CONCLUSION.............................................................................................................................................15

REFERENCES..............................................................................................................................................15

INTRODUCTION

Managerial accounting which is also known as management accounting is a process of

identifying, analyzing and interpretation of results or output to the managers so that they can

view that result for making decisions for their organization. Managerial accounting reports are

only for the internal people of organization. These reports company does not show to the outer

people as it is totally for the use of organization only. From these reports managers view the

actual performance of their department and this helps them in making better decisions about their

department for future. Managerial accounting helps in showing the true and fair financial as well

as managerial position and soundness of business. For reference purpose, this report has taken an

example of an accounting firm, Creams ltd. Creams Ltd is the multinational company which is

engaged in dealing in ice creams and all. The company is very much famous and operates world

wide.

This report discuss about managerial accounting and its importance to the company along

with the essential requirements of different types of managerial accounting systems. The report

also includes different methods of managerial accounting report. And apart from it, the report

also includes the advantages and disadvantages of planning tools used for budgetary control.

LO 1

P1 Explain management accounting and give the essential requirements of different types of

management accounting systems.

Managerial accounting refers to the identifying, measuring, analyzing and delivering the

information about the performance of the company to the managers so that they can better and

rational decisions. The managerial accounting is different from financial accounting as financial

accounting is shown to the outer people also but managerial accounting is for the internal use

only. People working within the organization get the information for the managerial accounting

reports. These reports helps the organization in better decision making and these decisions are

made by rationally by the better understanding of the performance and financial soundness of the

business. The techniques which are used in managerial accounting are not as same which is

directed in financial accounting, they are different. Also the presentation of managerial

accounting can be modified according to the use and want of the managers. These managerial

accounting reports show the performances of the departments which can help the managers in

detecting the defects into their working. After detecting the loop holes managers can make

decisions accordingly which can help him in the attainment of the specific or desired objectives

(Bargate, 2012). It includes many other elements such as costing, budgeting, forecasting, and

other financial analysis. The managerial accounting is important for the following reasons:

Managerial accounting which is also known as management accounting is a process of

identifying, analyzing and interpretation of results or output to the managers so that they can

view that result for making decisions for their organization. Managerial accounting reports are

only for the internal people of organization. These reports company does not show to the outer

people as it is totally for the use of organization only. From these reports managers view the

actual performance of their department and this helps them in making better decisions about their

department for future. Managerial accounting helps in showing the true and fair financial as well

as managerial position and soundness of business. For reference purpose, this report has taken an

example of an accounting firm, Creams ltd. Creams Ltd is the multinational company which is

engaged in dealing in ice creams and all. The company is very much famous and operates world

wide.

This report discuss about managerial accounting and its importance to the company along

with the essential requirements of different types of managerial accounting systems. The report

also includes different methods of managerial accounting report. And apart from it, the report

also includes the advantages and disadvantages of planning tools used for budgetary control.

LO 1

P1 Explain management accounting and give the essential requirements of different types of

management accounting systems.

Managerial accounting refers to the identifying, measuring, analyzing and delivering the

information about the performance of the company to the managers so that they can better and

rational decisions. The managerial accounting is different from financial accounting as financial

accounting is shown to the outer people also but managerial accounting is for the internal use

only. People working within the organization get the information for the managerial accounting

reports. These reports helps the organization in better decision making and these decisions are

made by rationally by the better understanding of the performance and financial soundness of the

business. The techniques which are used in managerial accounting are not as same which is

directed in financial accounting, they are different. Also the presentation of managerial

accounting can be modified according to the use and want of the managers. These managerial

accounting reports show the performances of the departments which can help the managers in

detecting the defects into their working. After detecting the loop holes managers can make

decisions accordingly which can help him in the attainment of the specific or desired objectives

(Bargate, 2012). It includes many other elements such as costing, budgeting, forecasting, and

other financial analysis. The managerial accounting is important for the following reasons:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Decision making: The managerial accounting is useful in better decision making for the

department or for the organization. After analyzing the reports or information, a manger go

through it and makes rational decisions. It has been said that a good decision is which when

taken after undertaking the whole performance and information because after this a manger has a

more better understanding about the position at which his department is in.

Setting objectives: The managerial accounting also used in setting the objectives for the

business. The objective for a department or for an organization is set only after going through its

previous performance. Through managerial accounting reports a manager can go through the

performances of his department and can set its objectives accordingly. The set objectives should

be such that it could be attain by the people or department. It should not be made by irrational

assumptions.

The main purpose of the managerial accounting is to extract the internal information

about the company’s performance and financial soundness with the help of various sources and

then available that information to managers. The information provided helps the mangers in

taking the critical decisions which is related to price, cost, budget, strategies and much more. The

essential requirements of managerial accounting system include:

Management Style: The system which is adopted by the organization do affects the managerial

accounting style (Brewer, Garrison and Noreen, 2015). It is very much necessary to follow a

certain type of managerial style as it indicates what and to whom the information needs to get

transfer for decisions or for future process. Management style can be of two types:

Autocratic Style: In this type of style, the information is passed to only those people who

make the decisions. These people are generally top level of management. These people take the

decisions by themselves without involving other people ideas or opinions.

Democratic Style: In this type of style, the information is passed to all the people and not

only top level management people takes the decisions but they involve the other people also in

contributing in decision making process by putting their own thoughts and opinions upon that

topic. This style also includes the people from lower level of management.

Organization Structure: The structure of organization also defines the managerial accounting.

The managerial accounting style should be apt for organization structure. The organization

structure can be of two types:

Functional Structure: In this structure, the mangers are provided with the information

which is only related to his department or functional area (Butler and Ghosh, 2015). No extra or

other information is provided to him.

department or for the organization. After analyzing the reports or information, a manger go

through it and makes rational decisions. It has been said that a good decision is which when

taken after undertaking the whole performance and information because after this a manger has a

more better understanding about the position at which his department is in.

Setting objectives: The managerial accounting also used in setting the objectives for the

business. The objective for a department or for an organization is set only after going through its

previous performance. Through managerial accounting reports a manager can go through the

performances of his department and can set its objectives accordingly. The set objectives should

be such that it could be attain by the people or department. It should not be made by irrational

assumptions.

The main purpose of the managerial accounting is to extract the internal information

about the company’s performance and financial soundness with the help of various sources and

then available that information to managers. The information provided helps the mangers in

taking the critical decisions which is related to price, cost, budget, strategies and much more. The

essential requirements of managerial accounting system include:

Management Style: The system which is adopted by the organization do affects the managerial

accounting style (Brewer, Garrison and Noreen, 2015). It is very much necessary to follow a

certain type of managerial style as it indicates what and to whom the information needs to get

transfer for decisions or for future process. Management style can be of two types:

Autocratic Style: In this type of style, the information is passed to only those people who

make the decisions. These people are generally top level of management. These people take the

decisions by themselves without involving other people ideas or opinions.

Democratic Style: In this type of style, the information is passed to all the people and not

only top level management people takes the decisions but they involve the other people also in

contributing in decision making process by putting their own thoughts and opinions upon that

topic. This style also includes the people from lower level of management.

Organization Structure: The structure of organization also defines the managerial accounting.

The managerial accounting style should be apt for organization structure. The organization

structure can be of two types:

Functional Structure: In this structure, the mangers are provided with the information

which is only related to his department or functional area (Butler and Ghosh, 2015). No extra or

other information is provided to him.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Flat Structure: In this type of structure, the wide range of information is provided to the

managers so that they can take decisions by identifying the critical information of the

organization.

Information: They say information is the key. Information or data helps the organization for

better understanding of things and performances. Through getting true and fair information

managers can take the further steps or decisions. But information also should be classified into

some categories which are as follows:

What, who, How: This refers to what information is needing to a person, does he want

the performance information about his department or does he want the information about his

team members and the like. Who wants the information, is manager wants the information or

executive director wants the information and How refers to the purpose of getting the

information.

Sources: Sources refers to the place from where the information is get extracted. This

may include the primary or secondary sources.

Relevancy: The information provided should be relevant to the need of person. The

information would be useful only and only if it will be relevant to the user.

Accuracy: The information provided should be accurate enough that a person can rely

upon it (Datar and Rajan, 2014).

P2 Explain different methods used for management accounting reporting.

Generally, a budget is a financial statement which says about the future financial

requirements into a project or for attaining any particular target. Financial document includes

both the income and expenses. For example if Hart’s bakery wants to produce the cakes and their

other bakery item so for that they will first make the rational assumptions about the sales which

they will going to have in a particular time period. Along with this they would calculate the

production which they need to undertake which satisfies their assumed sales. When the

production level is decided, the company will make a fair list consisting of resources they would

be needing along with the prices associated with them. Through this the company can a budget

of their financial requirements. Budget includes the cost of raw materials, labor costs and other

over heads which gives a true and fair look to companies about their budget under which they

need to complete their whole task (Demski, 2013). The departments try their best to complete the

task or project within the budget allotted to them and they sometime also tries to save amount

from budgets allotted. Budget helps the organization in making the comparison between the

actual cost or income and standard cost or income.

There are various methods which is used for management accounting reporting and some are

included as follows:

managers so that they can take decisions by identifying the critical information of the

organization.

Information: They say information is the key. Information or data helps the organization for

better understanding of things and performances. Through getting true and fair information

managers can take the further steps or decisions. But information also should be classified into

some categories which are as follows:

What, who, How: This refers to what information is needing to a person, does he want

the performance information about his department or does he want the information about his

team members and the like. Who wants the information, is manager wants the information or

executive director wants the information and How refers to the purpose of getting the

information.

Sources: Sources refers to the place from where the information is get extracted. This

may include the primary or secondary sources.

Relevancy: The information provided should be relevant to the need of person. The

information would be useful only and only if it will be relevant to the user.

Accuracy: The information provided should be accurate enough that a person can rely

upon it (Datar and Rajan, 2014).

P2 Explain different methods used for management accounting reporting.

Generally, a budget is a financial statement which says about the future financial

requirements into a project or for attaining any particular target. Financial document includes

both the income and expenses. For example if Hart’s bakery wants to produce the cakes and their

other bakery item so for that they will first make the rational assumptions about the sales which

they will going to have in a particular time period. Along with this they would calculate the

production which they need to undertake which satisfies their assumed sales. When the

production level is decided, the company will make a fair list consisting of resources they would

be needing along with the prices associated with them. Through this the company can a budget

of their financial requirements. Budget includes the cost of raw materials, labor costs and other

over heads which gives a true and fair look to companies about their budget under which they

need to complete their whole task (Demski, 2013). The departments try their best to complete the

task or project within the budget allotted to them and they sometime also tries to save amount

from budgets allotted. Budget helps the organization in making the comparison between the

actual cost or income and standard cost or income.

There are various methods which is used for management accounting reporting and some are

included as follows:

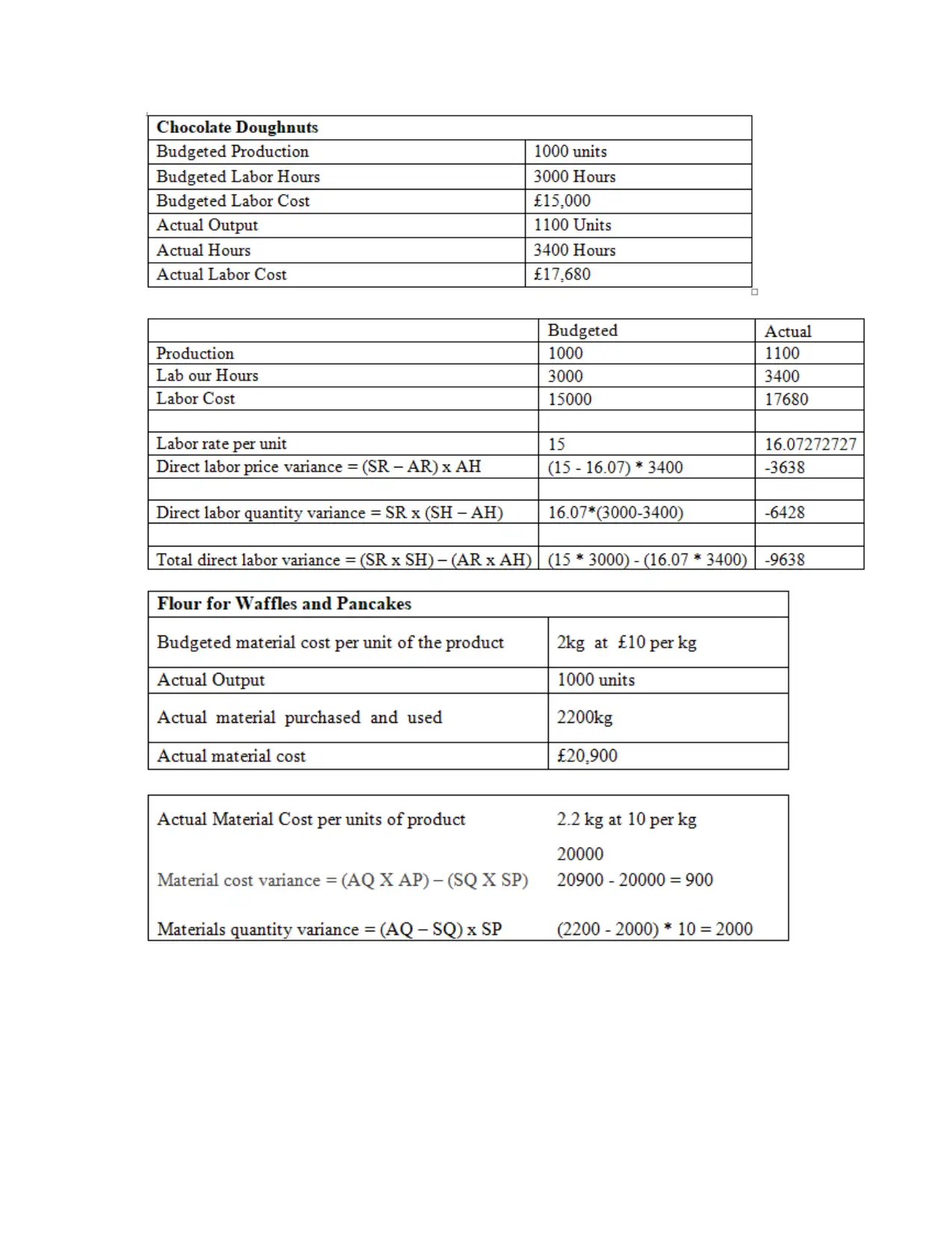

Cost Schedules: Budgets are usually based on the standard costs. In this the cost of raw material

per unit is estimated and then the total cost of whole the production is evaluated. Here standard

cost refers to the cost which is calculated by the company by estimating the cost of per unit.

Whereas actual cost refers to the cost which is actually incurred to the company production unit.

If the actual cost is more than the standard cost then the company should review their budget

review and necessary control measures should be taken by the managers. But if the actual budget

is equal or less than the standard budget then there is no need to get worry as it is said to be ar n

ideal situation for the company. In the case where actual budget is more than the standard

budget, the manager should evaluate the difference. When the difference is more or big then

necessary steps or control measures should be taken. But if the gap is under margin then the

company need not to get worry (Greenberg and Wilner, 2015).

Costing and budgets are getting prepared according to the marginal cost and budgets. The

basic aim of the company is to cover the costs because once the cost is covered the rest is

company’s profit.

Budget reports: Budget refers to the planning of activities which needs to be undertaken by an

organization along with their associated cost. Here the price or the cost plays an important role

into the budget. Before starting of any project or financial term, Hart’s Bakery make their

budgets on a quarterly basis. In the budget they make up the cost which he would be needing for

carrying out the activities such as production, marketing, supply chain, transport, raw materials,

labor and so on. The budgets are very important for any business. Budget sets a framework

within which organization carries their activities or operations.

Performance report: Performance report is the report which tells about the performances or

work of the organization which they have achieved so far or in a particular time period. From

performance report, an organization can evaluates the true and fair financial health and

soundness of the business. Performance report can be also of employees performance. In this the

performance or the contribution which is makes by the employees is included. From such report

a manager can make out about which employees has perform good or excellent and which

employee has not even performed up to the mark (Jiambalvo, 2019). From such reports a

manager can make the required decisions about training and development programs, promotions,

reward, appreciations, skills and knowledge program and the so forth which needs to given to

employees.

Variance analysis: Variance analysis refers to the attainment of the difference between the

actual and standard budgets or performances. As in the case with Hart’s bakery there variance

can be calculated by the taking out the differences between the actual cost and standard cost.

Variance is very easy in its calculations and can help the organization in finding out the area in

which the company has its loop hole. That loop hole can get filled by taking corrective actions

and detecting the place where the organization is making mistake while making their budget

reports.

per unit is estimated and then the total cost of whole the production is evaluated. Here standard

cost refers to the cost which is calculated by the company by estimating the cost of per unit.

Whereas actual cost refers to the cost which is actually incurred to the company production unit.

If the actual cost is more than the standard cost then the company should review their budget

review and necessary control measures should be taken by the managers. But if the actual budget

is equal or less than the standard budget then there is no need to get worry as it is said to be ar n

ideal situation for the company. In the case where actual budget is more than the standard

budget, the manager should evaluate the difference. When the difference is more or big then

necessary steps or control measures should be taken. But if the gap is under margin then the

company need not to get worry (Greenberg and Wilner, 2015).

Costing and budgets are getting prepared according to the marginal cost and budgets. The

basic aim of the company is to cover the costs because once the cost is covered the rest is

company’s profit.

Budget reports: Budget refers to the planning of activities which needs to be undertaken by an

organization along with their associated cost. Here the price or the cost plays an important role

into the budget. Before starting of any project or financial term, Hart’s Bakery make their

budgets on a quarterly basis. In the budget they make up the cost which he would be needing for

carrying out the activities such as production, marketing, supply chain, transport, raw materials,

labor and so on. The budgets are very important for any business. Budget sets a framework

within which organization carries their activities or operations.

Performance report: Performance report is the report which tells about the performances or

work of the organization which they have achieved so far or in a particular time period. From

performance report, an organization can evaluates the true and fair financial health and

soundness of the business. Performance report can be also of employees performance. In this the

performance or the contribution which is makes by the employees is included. From such report

a manager can make out about which employees has perform good or excellent and which

employee has not even performed up to the mark (Jiambalvo, 2019). From such reports a

manager can make the required decisions about training and development programs, promotions,

reward, appreciations, skills and knowledge program and the so forth which needs to given to

employees.

Variance analysis: Variance analysis refers to the attainment of the difference between the

actual and standard budgets or performances. As in the case with Hart’s bakery there variance

can be calculated by the taking out the differences between the actual cost and standard cost.

Variance is very easy in its calculations and can help the organization in finding out the area in

which the company has its loop hole. That loop hole can get filled by taking corrective actions

and detecting the place where the organization is making mistake while making their budget

reports.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

These are some methods which is used in managerial accounting system in an

organization.

M1 Evaluate the benefits of management accounting systems and their application within an

organisational context.

The benefits of management according system are as follows:

Cost Schedules: The cost schedules helps an organization in staying at the track. From the cost

schedules the organization have an idea about their activities that they need to undertake for the

completion of project. It is a table which shows all the costs associated with activities.

Budget Report: The preparation of budget report helps the organization in the identification of

any sort of error. Through the identification corrective actions can be taken with time.

Performance Report: The performance reports has many benefits, such as, the organization has

the accountability for employee’s performance, help in examining the current situation,

transparency, good governance of activities and the so on.

D1 Critically evaluate how management accounting systems and management accounting

reporting is integrated within organisational processes.

Different organization adopt different management accounting system. As the ocst

accounting system regulations helps the organization in the integration of management

accounting system. The cost accounting system refers to a framework which is used by the

company for estimating the cost for their product for the purpose of profitability analysis,

inventory analysis and cost control.The regulations which are stated in it are given by an

authorized body which make sure that it has the capability for proper management accounting

reporting. The Cost accounting system helps the organization in integrating the financial as well

as managerial activities undertaken by them.

LO 2

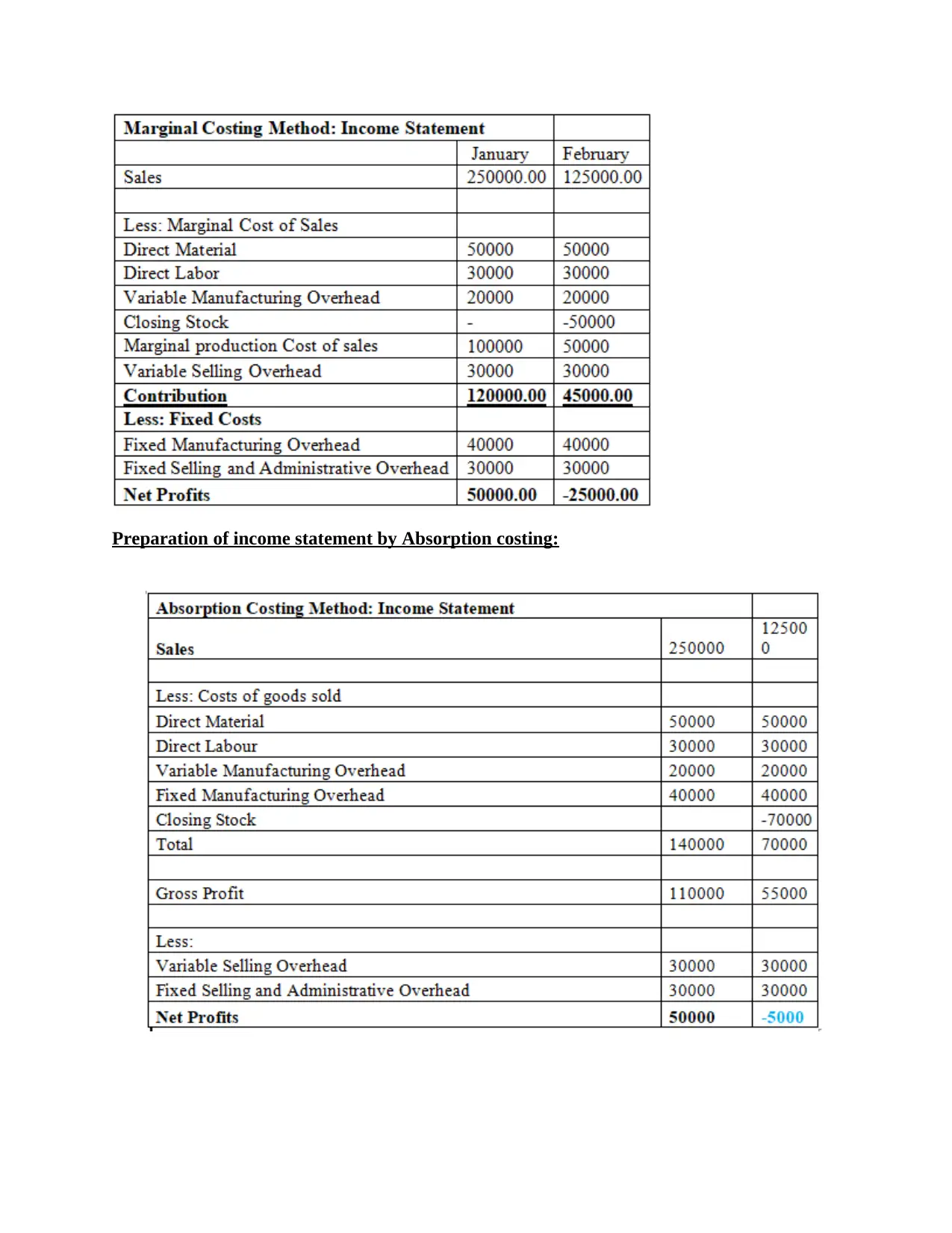

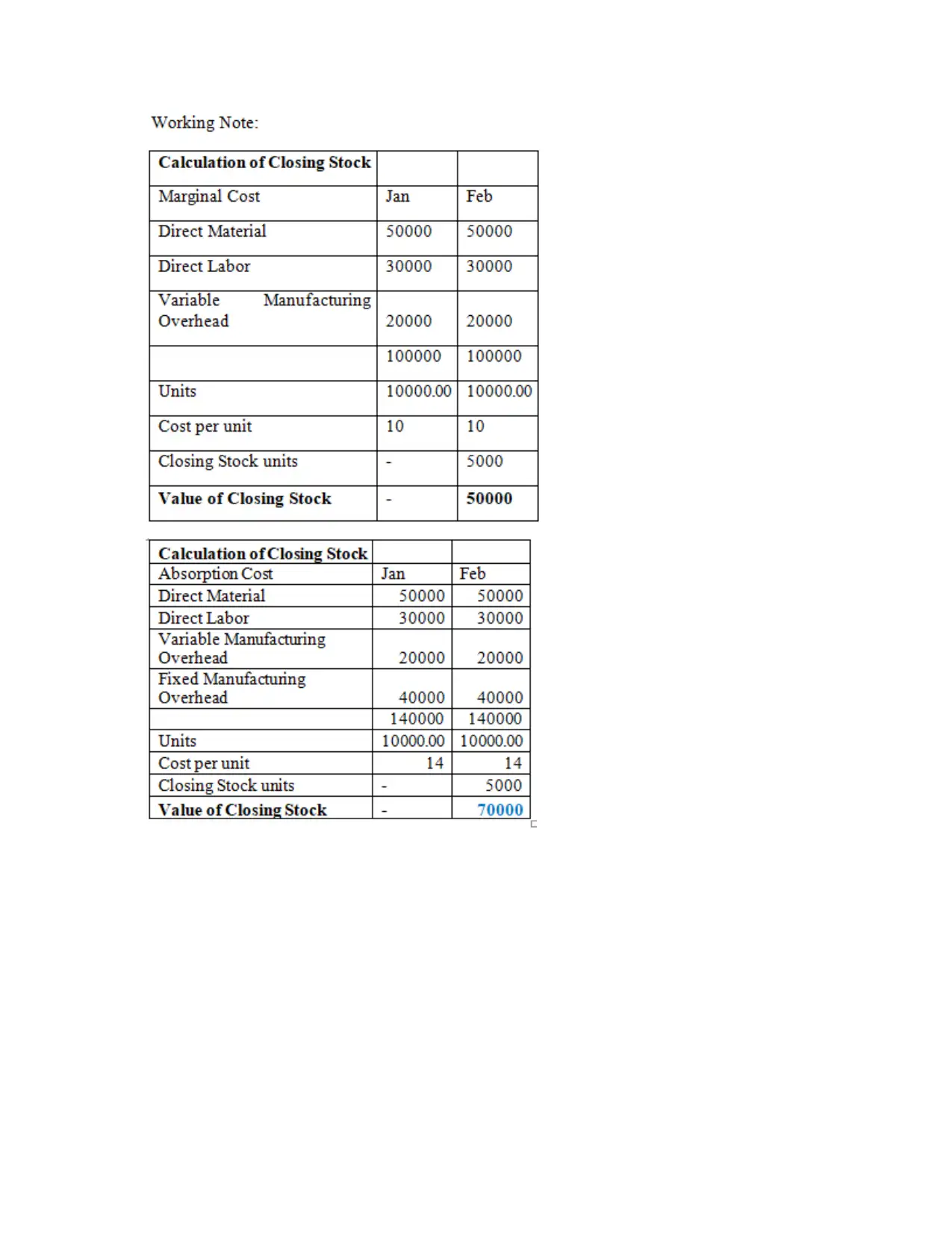

P3 Calculate costs using appropriate techniques of cost analysis to prepare an income statement

using marginal and absorption costs.

Income statement under Marginal costing method for month of May & June

organization.

M1 Evaluate the benefits of management accounting systems and their application within an

organisational context.

The benefits of management according system are as follows:

Cost Schedules: The cost schedules helps an organization in staying at the track. From the cost

schedules the organization have an idea about their activities that they need to undertake for the

completion of project. It is a table which shows all the costs associated with activities.

Budget Report: The preparation of budget report helps the organization in the identification of

any sort of error. Through the identification corrective actions can be taken with time.

Performance Report: The performance reports has many benefits, such as, the organization has

the accountability for employee’s performance, help in examining the current situation,

transparency, good governance of activities and the so on.

D1 Critically evaluate how management accounting systems and management accounting

reporting is integrated within organisational processes.

Different organization adopt different management accounting system. As the ocst

accounting system regulations helps the organization in the integration of management

accounting system. The cost accounting system refers to a framework which is used by the

company for estimating the cost for their product for the purpose of profitability analysis,

inventory analysis and cost control.The regulations which are stated in it are given by an

authorized body which make sure that it has the capability for proper management accounting

reporting. The Cost accounting system helps the organization in integrating the financial as well

as managerial activities undertaken by them.

LO 2

P3 Calculate costs using appropriate techniques of cost analysis to prepare an income statement

using marginal and absorption costs.

Income statement under Marginal costing method for month of May & June

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Preparation of income statement by Absorption costing:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

M2 Accurately apply a range of management accounting techniques and produce appropriate

financial reporting documents.

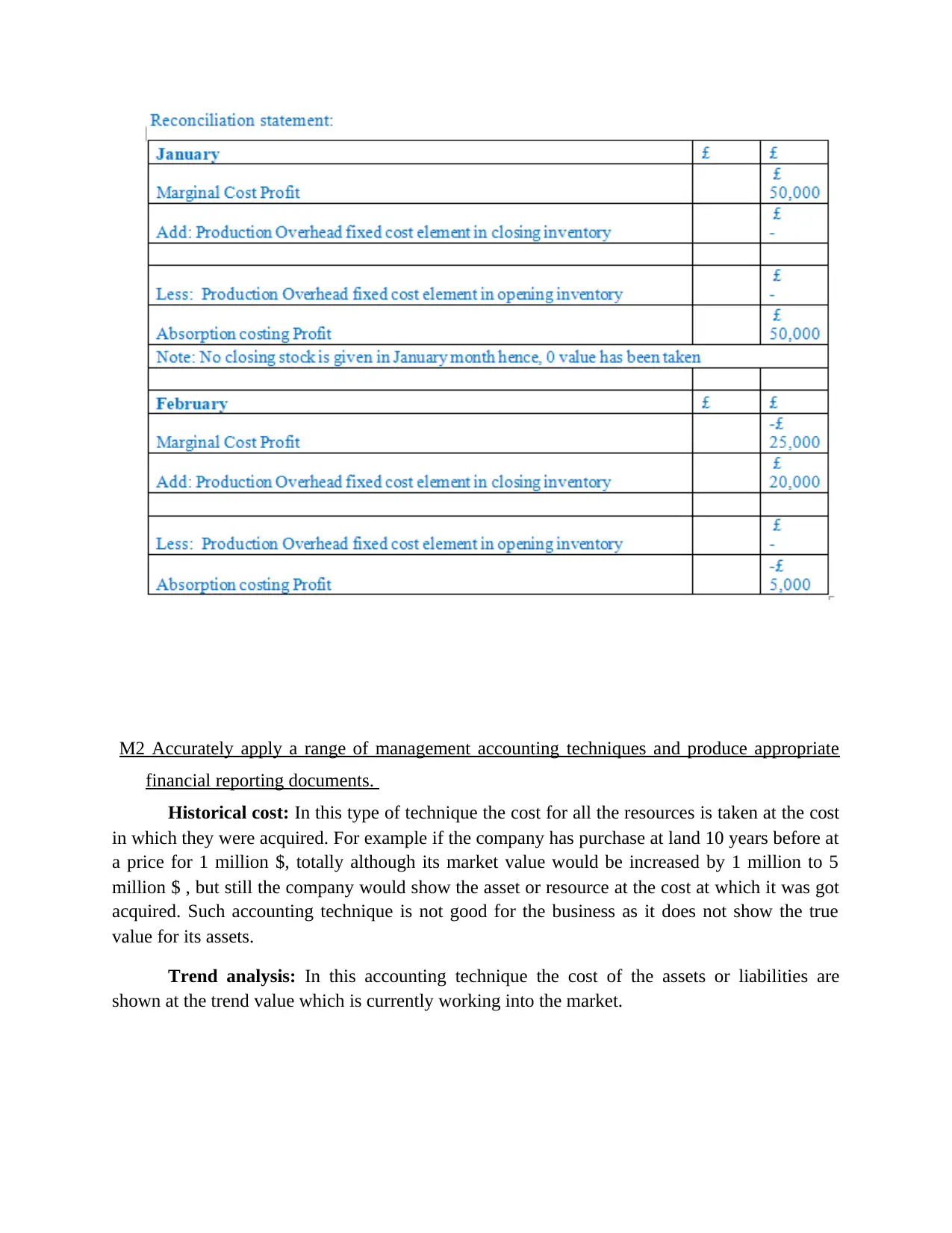

Historical cost: In this type of technique the cost for all the resources is taken at the cost

in which they were acquired. For example if the company has purchase at land 10 years before at

a price for 1 million $, totally although its market value would be increased by 1 million to 5

million $ , but still the company would show the asset or resource at the cost at which it was got

acquired. Such accounting technique is not good for the business as it does not show the true

value for its assets.

Trend analysis: In this accounting technique the cost of the assets or liabilities are

shown at the trend value which is currently working into the market.

financial reporting documents.

Historical cost: In this type of technique the cost for all the resources is taken at the cost

in which they were acquired. For example if the company has purchase at land 10 years before at

a price for 1 million $, totally although its market value would be increased by 1 million to 5

million $ , but still the company would show the asset or resource at the cost at which it was got

acquired. Such accounting technique is not good for the business as it does not show the true

value for its assets.

Trend analysis: In this accounting technique the cost of the assets or liabilities are

shown at the trend value which is currently working into the market.

D2 Produce financial reports that accurately apply and interpret data for a range of business

activities.

From the income statement shown above, we can clearly evaluate that the sales for the

company has definitely increased. As in the month of may the Net profit for the company Hart’s

Bakery was 1050 but by the end of June month it was 9794.4. The Bakery shows much profit

which is a very significant sign for it. Apart from this the company has maintain its cost for

labor, resources, manufacturing and other variable cost. The cost has remained constant for the

company and with this constant cost, it has increases its profit margin, according to the income

statement for these two months.

LO 3

P4 Explain the advantages and disadvantages of different types of planning tools used for

budgetary control.

Budgets are in quantitative form which is mandatory for the business to continue for their

operations. Budgets are set in a view to make an advance framework about the finance that

would need for carrying out the activities or operations. Budgets helps the making the

managerial and accounting functions properly. By preparations of budgets company can carry

out its managerial activities with accordance to the framework set. And also the accounting

activities are carrying within the specified or allotted budget. There are many reasons for the

preparations of budgets and some are as follows:

To make sure that the company should meet its planned goals and objectives. Therefore it is a

way for aligning the activities of the business so that every department knows about its job and

target (Jones, Atkinson, Lorenz and Harris, 2012). When the departments are very well aware

about their job responsibility they would make their plans about how they can achieve the goal or

objective given to them.

It is also works as an incentive of the managers, as they know that what performance they

had in past and they have a chance to improve the performance for their department. So

that they can prove themselves.

The budget helps the organization in aligning the activities of the different departments.

The company, as in the case with Hart’z Bakery, prepares two budgets, one for every

departments which sets as a target for them which they have to achieve and second is the

overall budget which includes the goals and objective of whole organization. First the

organizational budget is prepared then this budget is divided into other functional area

which works as a target for the functional departments. Functional departments may

include, production department, marketing department, sales department, financial

department, human resource department and much more.

activities.

From the income statement shown above, we can clearly evaluate that the sales for the

company has definitely increased. As in the month of may the Net profit for the company Hart’s

Bakery was 1050 but by the end of June month it was 9794.4. The Bakery shows much profit

which is a very significant sign for it. Apart from this the company has maintain its cost for

labor, resources, manufacturing and other variable cost. The cost has remained constant for the

company and with this constant cost, it has increases its profit margin, according to the income

statement for these two months.

LO 3

P4 Explain the advantages and disadvantages of different types of planning tools used for

budgetary control.

Budgets are in quantitative form which is mandatory for the business to continue for their

operations. Budgets are set in a view to make an advance framework about the finance that

would need for carrying out the activities or operations. Budgets helps the making the

managerial and accounting functions properly. By preparations of budgets company can carry

out its managerial activities with accordance to the framework set. And also the accounting

activities are carrying within the specified or allotted budget. There are many reasons for the

preparations of budgets and some are as follows:

To make sure that the company should meet its planned goals and objectives. Therefore it is a

way for aligning the activities of the business so that every department knows about its job and

target (Jones, Atkinson, Lorenz and Harris, 2012). When the departments are very well aware

about their job responsibility they would make their plans about how they can achieve the goal or

objective given to them.

It is also works as an incentive of the managers, as they know that what performance they

had in past and they have a chance to improve the performance for their department. So

that they can prove themselves.

The budget helps the organization in aligning the activities of the different departments.

The company, as in the case with Hart’z Bakery, prepares two budgets, one for every

departments which sets as a target for them which they have to achieve and second is the

overall budget which includes the goals and objective of whole organization. First the

organizational budget is prepared then this budget is divided into other functional area

which works as a target for the functional departments. Functional departments may

include, production department, marketing department, sales department, financial

department, human resource department and much more.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.