MA515 Managerial Accounting Report: Analysis of HLW Membership Plans

VerifiedAdded on 2022/11/28

|8

|814

|410

Report

AI Summary

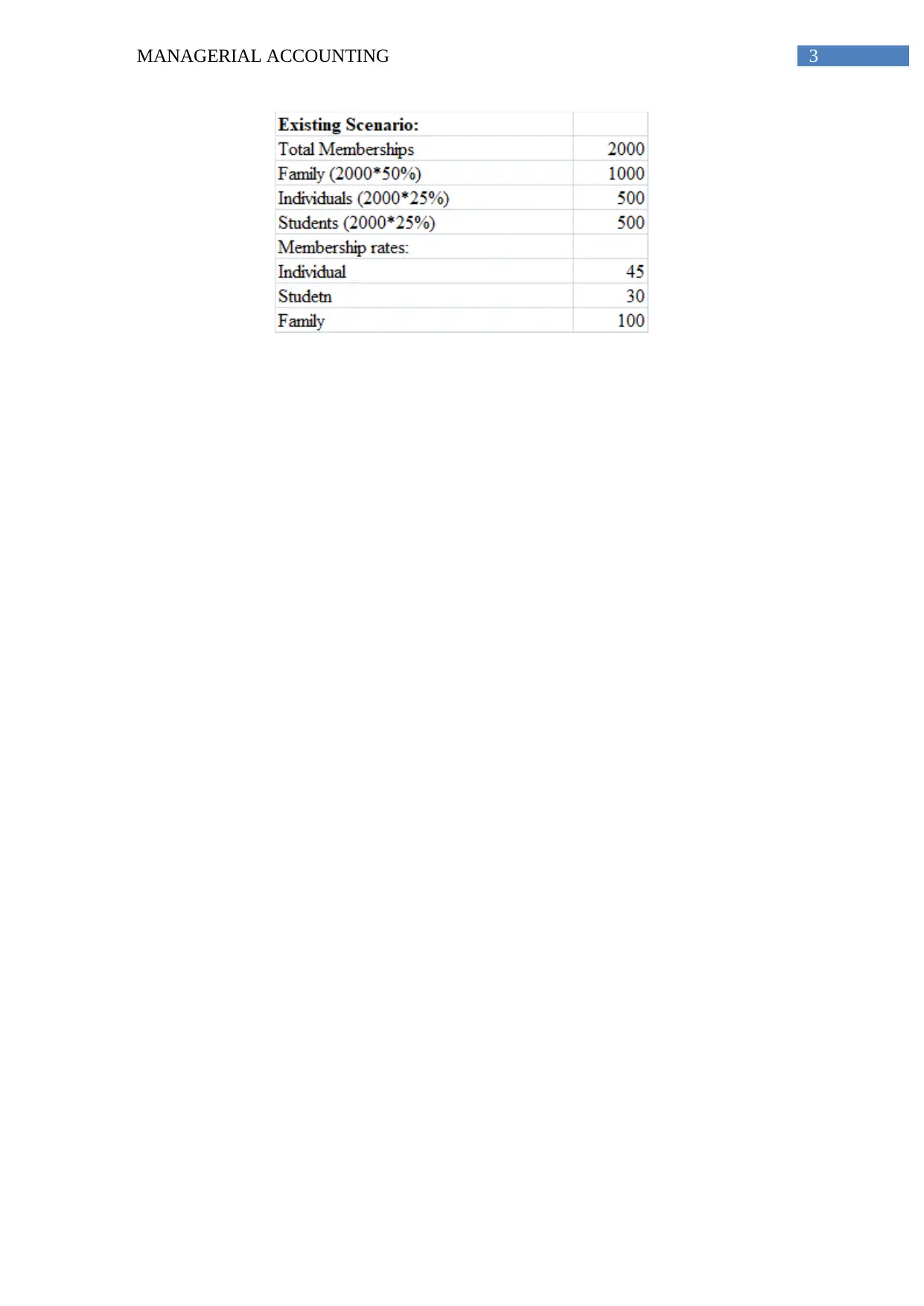

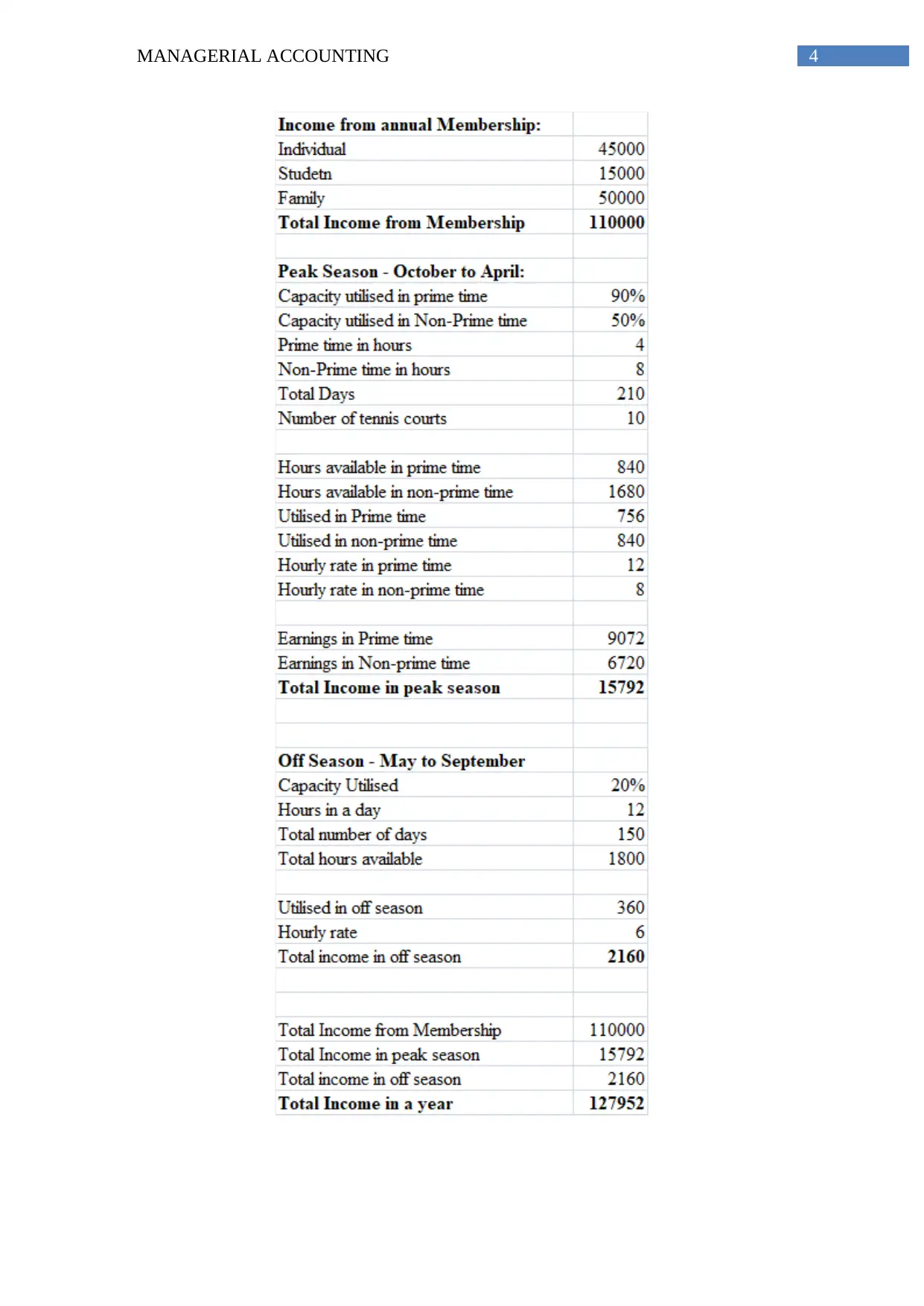

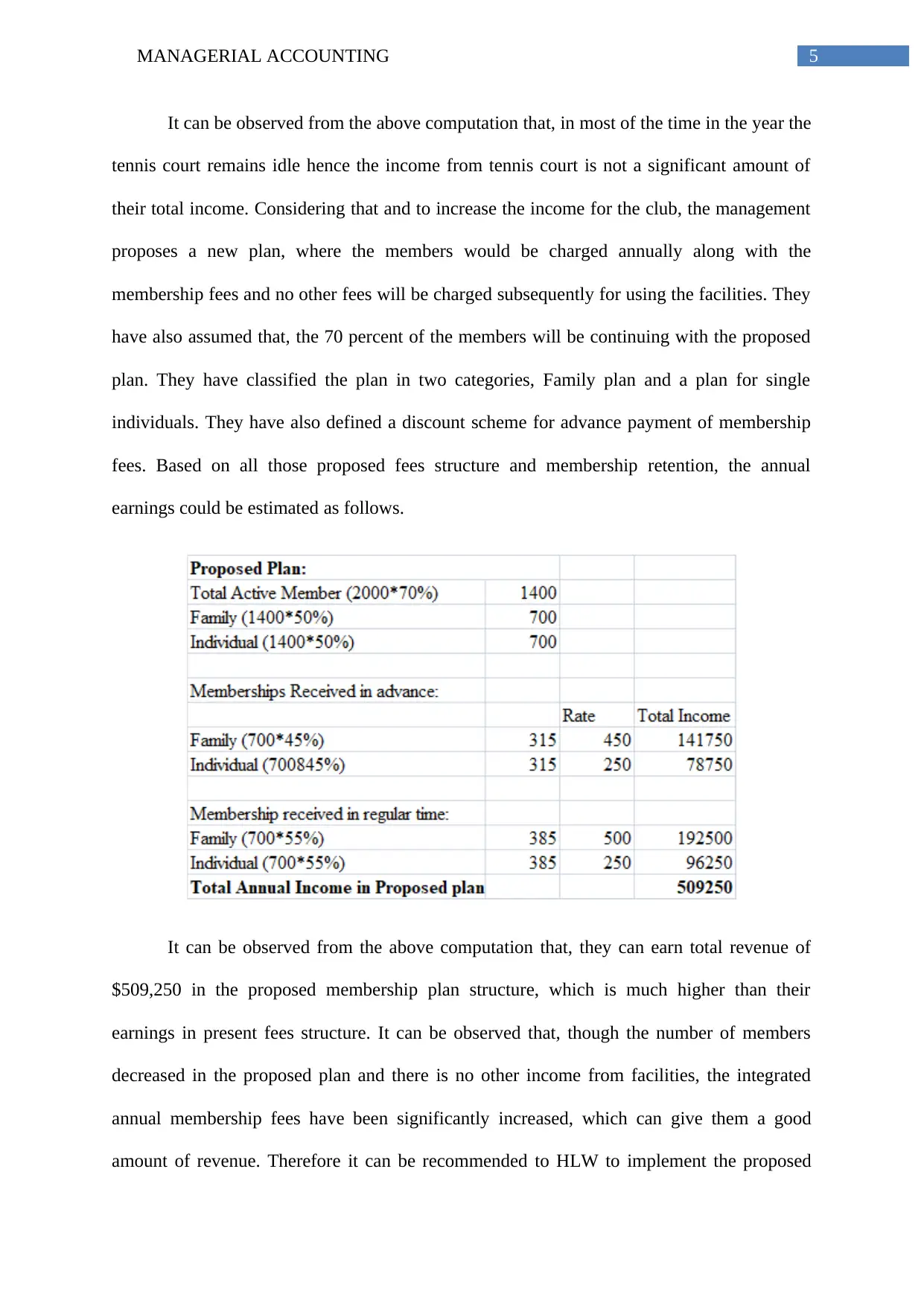

This report presents a managerial accounting analysis of Hawthorn Leisure Works (HLW), a fitness club offering tennis courts and other services. The analysis focuses on evaluating HLW's current and proposed membership plans, considering factors such as membership fees, facility usage, and revenue generation. The report computes the total annual income under both scenarios, highlighting the impact of different pricing strategies. The current plan charges members separately for services, while the proposed plan integrates fees into an annual membership. The analysis reveals that, although the proposed plan may result in fewer members, it leads to increased total revenue due to integrated pricing. The report concludes with a recommendation for HLW to adopt the proposed membership plan, supported by a detailed discussion of the financial implications. The report uses computations and comparisons to support its findings, and it adheres to the guidelines of the assignment brief.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.