Managerial Accounting Report: Systems and Budgeting Analysis

VerifiedAdded on 2023/01/11

|13

|3749

|74

Report

AI Summary

This report provides a comprehensive overview of managerial accounting (MA) principles and their application within Let's Grow Ltd, a UK-based manufacturing company. It begins by defining MA and highlighting its role in strategic decision-making, emphasizing the difference between MA and financial accounting. The report then delves into various MA systems, including cost accounting, price optimization, inventory management, and job costing, explaining their significance and benefits. Different types of MA reports, such as budget reports, accounts receivable aging reports, cost managerial accounting reports, and performance reports, are presented, along with their importance in organizational planning, control, and performance evaluation. A detailed cash budget for the upcoming six months is prepared and analyzed. Finally, the report examines the uses and applications of planning tools like cash budgeting and zero-based budgeting in managerial accounting, discussing their advantages and disadvantages, and concludes with an evaluation of the company's financial state based on the forecasted cash budget.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTRODUCTION...........................................................................................................................3

a. Explaining different systems of MA with their significance and benefits...............................3

b. Presenting different types of MA reports and their importance..............................................4

c. Preparing cash budget for upcoming 6 months........................................................................6

d. Analyzing the uses and application of planning tools in managerial accounting....................7

e. Explaining MA systems that helps in resolving financial problems........................................9

f. Evaluating financial state of let’s Grow Ltd based on forecasted cash budget......................10

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................12

a. Explaining different systems of MA with their significance and benefits...............................3

b. Presenting different types of MA reports and their importance..............................................4

c. Preparing cash budget for upcoming 6 months........................................................................6

d. Analyzing the uses and application of planning tools in managerial accounting....................7

e. Explaining MA systems that helps in resolving financial problems........................................9

f. Evaluating financial state of let’s Grow Ltd based on forecasted cash budget......................10

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................12

INTRODUCTION

MA can be defined as a systematic procedure of providing several financial information

and resources to the business managers which helps them in making strategic decision that

further contributes towards the achievement of organizational goals and objectives. Let’s Grow

Ltd is a manufacturing company based in United Kingdom and the current study will emphasize

on the importance of managerial accounting and how it can contribute towards the success and

growth of the organization effectively and efficiently. The report will also include a brief

discussion about tools & techniques of MA that helps in solving business related problems.

a. Explaining different systems of MA with their significance and benefits

Meaning of MA

MA can be defined as the process of developing organizational goals through identifying,

measuring, analyzing, interpreting and sharing the information to business managers. Its main

motive is to extract internal information from multiple sources and then help managers by

making such information available to them (Ghasemi and et.al., 2016). Furthermore, the

information helps the directors and managers to take strategic decisions in regards to pricing,

sales, cost reduction etc. The major difference between managerial and financial accounting is

that the financial accounting involves collection of accounting information for the creation of

financial statements and accounting reports which is then utilized by the external parties whereas

under MA the reports are developed for the internal members of the company to improve the

operations of the business and increase its overall profitability.

Essential requirement of MA systems are as follows-

Cost accounting system- Cost accounting can be defined as the framework used by

companies to decide the cost of its products and services. Once the cost is estimated then the

company can add its profit margin and predict the final price of its goods and services. It is

considered to be as the most important MA system as it directly contributes towards the

profitability and growth of the enterprise. Moreover, the cost accounting system also helps in

predicting the closing value of its materials, work-in-progress and finished goods in order to

prepare correct financial statements. Cost accounting system is further divided into different

types like standard costing, activity-based costing, lean accounting and marginal costing.

MA can be defined as a systematic procedure of providing several financial information

and resources to the business managers which helps them in making strategic decision that

further contributes towards the achievement of organizational goals and objectives. Let’s Grow

Ltd is a manufacturing company based in United Kingdom and the current study will emphasize

on the importance of managerial accounting and how it can contribute towards the success and

growth of the organization effectively and efficiently. The report will also include a brief

discussion about tools & techniques of MA that helps in solving business related problems.

a. Explaining different systems of MA with their significance and benefits

Meaning of MA

MA can be defined as the process of developing organizational goals through identifying,

measuring, analyzing, interpreting and sharing the information to business managers. Its main

motive is to extract internal information from multiple sources and then help managers by

making such information available to them (Ghasemi and et.al., 2016). Furthermore, the

information helps the directors and managers to take strategic decisions in regards to pricing,

sales, cost reduction etc. The major difference between managerial and financial accounting is

that the financial accounting involves collection of accounting information for the creation of

financial statements and accounting reports which is then utilized by the external parties whereas

under MA the reports are developed for the internal members of the company to improve the

operations of the business and increase its overall profitability.

Essential requirement of MA systems are as follows-

Cost accounting system- Cost accounting can be defined as the framework used by

companies to decide the cost of its products and services. Once the cost is estimated then the

company can add its profit margin and predict the final price of its goods and services. It is

considered to be as the most important MA system as it directly contributes towards the

profitability and growth of the enterprise. Moreover, the cost accounting system also helps in

predicting the closing value of its materials, work-in-progress and finished goods in order to

prepare correct financial statements. Cost accounting system is further divided into different

types like standard costing, activity-based costing, lean accounting and marginal costing.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Price optimization system- Price optimization system is concerned with calculating how

the demand of a product or service varies at different price levels and then it includes combining

the data with information about costs and inventory levels to decide new prices that will improve

the future profits of the company (ПАНЧЕНКО, 2018). The optimization system includes three

critical elements like pricing strategy, value of product for both manufacturer and consumer, and

strategies that manage all elements affecting profitability. This system of MA has various

benefits like it helps the firm in making quick decisions, automating the entire process and also

helps in increasing the annual revenue of the company.

Inventory management system- The inventory management system can be defined as the

combination of technology and processes to ensure the adequate monitoring and maintenance of

raw materials, finished goods and company assets. It is imperative for every organization to have

an integrated inventory management system so that it can maintain a track record of every

inventory item and ensure complete transparency in the business. Inventory management system

not only helps in improving the cash flow system of the business but also ensures better reporting

and prediction of sales of goods & services (Taylor and Scapens, 2016). Furthermore, it

minimizes the storage costs, labor costs, dead stock and also improves the firm’s relationship

with its vendors and suppliers. Thus, it is recommended for every enterprise to have an

integrated & efficient inventory management system.

Job costing system- The job costing system is an imperative tool of MA as it is

concerned with accumulating the costs associated with several jobs within the organization. Such

information is important as it helps in determining the accuracy of company’s system which

helps in quoting prices that allow a reasonable amount of profit. The job costing system also

provides relevant information about direct materials, direct labor and overheads.

b. Presenting different types of MA reports and their importance

The managerial accounting report is used for the purpose of planning, regulating,

decision making and for measuring the business performance. These reports are very important

for the growth of the organization and managers analyze these reports to study the overall

performance of enterprise and how it can be improved through improved coordination and

cooperation between the members of the company.

the demand of a product or service varies at different price levels and then it includes combining

the data with information about costs and inventory levels to decide new prices that will improve

the future profits of the company (ПАНЧЕНКО, 2018). The optimization system includes three

critical elements like pricing strategy, value of product for both manufacturer and consumer, and

strategies that manage all elements affecting profitability. This system of MA has various

benefits like it helps the firm in making quick decisions, automating the entire process and also

helps in increasing the annual revenue of the company.

Inventory management system- The inventory management system can be defined as the

combination of technology and processes to ensure the adequate monitoring and maintenance of

raw materials, finished goods and company assets. It is imperative for every organization to have

an integrated inventory management system so that it can maintain a track record of every

inventory item and ensure complete transparency in the business. Inventory management system

not only helps in improving the cash flow system of the business but also ensures better reporting

and prediction of sales of goods & services (Taylor and Scapens, 2016). Furthermore, it

minimizes the storage costs, labor costs, dead stock and also improves the firm’s relationship

with its vendors and suppliers. Thus, it is recommended for every enterprise to have an

integrated & efficient inventory management system.

Job costing system- The job costing system is an imperative tool of MA as it is

concerned with accumulating the costs associated with several jobs within the organization. Such

information is important as it helps in determining the accuracy of company’s system which

helps in quoting prices that allow a reasonable amount of profit. The job costing system also

provides relevant information about direct materials, direct labor and overheads.

b. Presenting different types of MA reports and their importance

The managerial accounting report is used for the purpose of planning, regulating,

decision making and for measuring the business performance. These reports are very important

for the growth of the organization and managers analyze these reports to study the overall

performance of enterprise and how it can be improved through improved coordination and

cooperation between the members of the company.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Different types of MA reports are as follows:

Budget reports: Budget MA reports play a crucial role in measuring the success of an

organization as it helps in monitoring the overall performance of the business, department wise

to get a closer and detailed look about the way operations are performed. A budget report is

always prepared on the basis of past experiences and mistakes so that the company can

acknowledge in case any problem arises (Shevelev, Sheveleva and Gvozdev, 2017). The main

objective of budget reports is to measure the actual performance of the company with its

budgeted performance and then identify the deviations so that the company can take corrective

actions in the future. Such reports also guide the managers to provide better incentive to

employees, cut costs and perform better negotiation with the suppliers and other key partners.

Account receivable Aging reports: Accounts receivable reports are critical for every

business that heavily relies on extending credit facilities to other parties. Systematic breaking

down of remaining balance of firm’s clients helps the managers in identifying the defaulters as

well as find problems in the collection process of company. If the company has a large number

of defaulters then it needs to implement tighter credit policies because it is imperative for every

business to have regular cash flow so that the day to day activities can be performed easily.

However, there is always some amount of bad debts that a company needs to write off annually,

but it cannot become a regular habit (Shields and Shelleman, 2016). With the help of Account

receivable Aging reports, managers have complete information about who owes the business

what.

Cost Managerial Accounting reports: The cost managerial accounting reports computes

the final cost of all the goods and service manufactured by the organization over a period of time.

It includes the cost of all raw materials, overheads, labor and other costs taken into consideration.

The report helps the managers in making easy comparisons between the cost & price of the

product and monitoring the profit margin accordingly. Moreover, the cost accountants and the

production managers also interpret the cost of different items that have incurred during the

production and whether it can be eliminated or minimized to a certain extent so that the business

can escalate its profits accordingly. Thus, cost managerial accounting report plays a critical role

in reducing the inventory waste, overhead and labor costs which further leads to optimum

utilization of resources within all the departments of the corporation.

Budget reports: Budget MA reports play a crucial role in measuring the success of an

organization as it helps in monitoring the overall performance of the business, department wise

to get a closer and detailed look about the way operations are performed. A budget report is

always prepared on the basis of past experiences and mistakes so that the company can

acknowledge in case any problem arises (Shevelev, Sheveleva and Gvozdev, 2017). The main

objective of budget reports is to measure the actual performance of the company with its

budgeted performance and then identify the deviations so that the company can take corrective

actions in the future. Such reports also guide the managers to provide better incentive to

employees, cut costs and perform better negotiation with the suppliers and other key partners.

Account receivable Aging reports: Accounts receivable reports are critical for every

business that heavily relies on extending credit facilities to other parties. Systematic breaking

down of remaining balance of firm’s clients helps the managers in identifying the defaulters as

well as find problems in the collection process of company. If the company has a large number

of defaulters then it needs to implement tighter credit policies because it is imperative for every

business to have regular cash flow so that the day to day activities can be performed easily.

However, there is always some amount of bad debts that a company needs to write off annually,

but it cannot become a regular habit (Shields and Shelleman, 2016). With the help of Account

receivable Aging reports, managers have complete information about who owes the business

what.

Cost Managerial Accounting reports: The cost managerial accounting reports computes

the final cost of all the goods and service manufactured by the organization over a period of time.

It includes the cost of all raw materials, overheads, labor and other costs taken into consideration.

The report helps the managers in making easy comparisons between the cost & price of the

product and monitoring the profit margin accordingly. Moreover, the cost accountants and the

production managers also interpret the cost of different items that have incurred during the

production and whether it can be eliminated or minimized to a certain extent so that the business

can escalate its profits accordingly. Thus, cost managerial accounting report plays a critical role

in reducing the inventory waste, overhead and labor costs which further leads to optimum

utilization of resources within all the departments of the corporation.

Performance reports: The performance reports are created for the singular objective of

reviewing the performance of the company and its employees both collectively and individually

at the end of annual year.The following information is used by business managers to identify the

strengths and weaknesses of the employees and then provide those tasks accordingly. Moreover,

the top-level management also provide training & development to the team members to ensure

better growth of employees which ultimately contributes towards the accomplishment of goals

and objectives of the business effectively and efficiently. The members are also awarded for their

commitment and dedication towards the enterprise which increase their motivation and work

productivity systematically. Thus, it can be said that the role of performance reports is crucial for

every organization as it helps in keeping an accurate measure of their implemented strategies and

ideas towards the set targets.

Other managerial accounting reports: Other MA reports include project reports,

competitor’s analysis, supplier performance and inventory management reports. In most cases

these reports are outsourced to professionals instead of internally producing as it helps the

business to focus on its core activities (Amara and Benelifa, 2017). Also, the ideal choice for the

company is to let professionals make the reports as they can use there skills and knowledge

adequately to prepare accurate and authentic reports.

c. Preparing cash budget for upcoming 6 months

Particulars March April May June July August

Revenue (received in

same month) 30000 36000 24000 28000 32000 34000

Revenue (received in

following month) 96000 120000 144000 96000 112000 128000

Total Revenue 126000 156000 168000 124000 144000 162000

Less: expenses

Purchases 50000 50000 70000 80000 90000 100000

wages 30000 30000 30000 30000 30000 30000

Rent (paid quarterly) 12000 12000

Depreciation 2000 2000 2000 2000 2000 2000

Variable overheads 10000 15000 18000 12000 14000 16000

Fixed overhead 30000 30000 30000 30000 30000 30000

Total expenses 134000 127000 150000 166000 166000 178000

Cash surplus / deficit -8000 29000 18000 -42000 -22000 -16000

Opening cash balance 20000 12000 41000 59000 17000 -5000

reviewing the performance of the company and its employees both collectively and individually

at the end of annual year.The following information is used by business managers to identify the

strengths and weaknesses of the employees and then provide those tasks accordingly. Moreover,

the top-level management also provide training & development to the team members to ensure

better growth of employees which ultimately contributes towards the accomplishment of goals

and objectives of the business effectively and efficiently. The members are also awarded for their

commitment and dedication towards the enterprise which increase their motivation and work

productivity systematically. Thus, it can be said that the role of performance reports is crucial for

every organization as it helps in keeping an accurate measure of their implemented strategies and

ideas towards the set targets.

Other managerial accounting reports: Other MA reports include project reports,

competitor’s analysis, supplier performance and inventory management reports. In most cases

these reports are outsourced to professionals instead of internally producing as it helps the

business to focus on its core activities (Amara and Benelifa, 2017). Also, the ideal choice for the

company is to let professionals make the reports as they can use there skills and knowledge

adequately to prepare accurate and authentic reports.

c. Preparing cash budget for upcoming 6 months

Particulars March April May June July August

Revenue (received in

same month) 30000 36000 24000 28000 32000 34000

Revenue (received in

following month) 96000 120000 144000 96000 112000 128000

Total Revenue 126000 156000 168000 124000 144000 162000

Less: expenses

Purchases 50000 50000 70000 80000 90000 100000

wages 30000 30000 30000 30000 30000 30000

Rent (paid quarterly) 12000 12000

Depreciation 2000 2000 2000 2000 2000 2000

Variable overheads 10000 15000 18000 12000 14000 16000

Fixed overhead 30000 30000 30000 30000 30000 30000

Total expenses 134000 127000 150000 166000 166000 178000

Cash surplus / deficit -8000 29000 18000 -42000 -22000 -16000

Opening cash balance 20000 12000 41000 59000 17000 -5000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

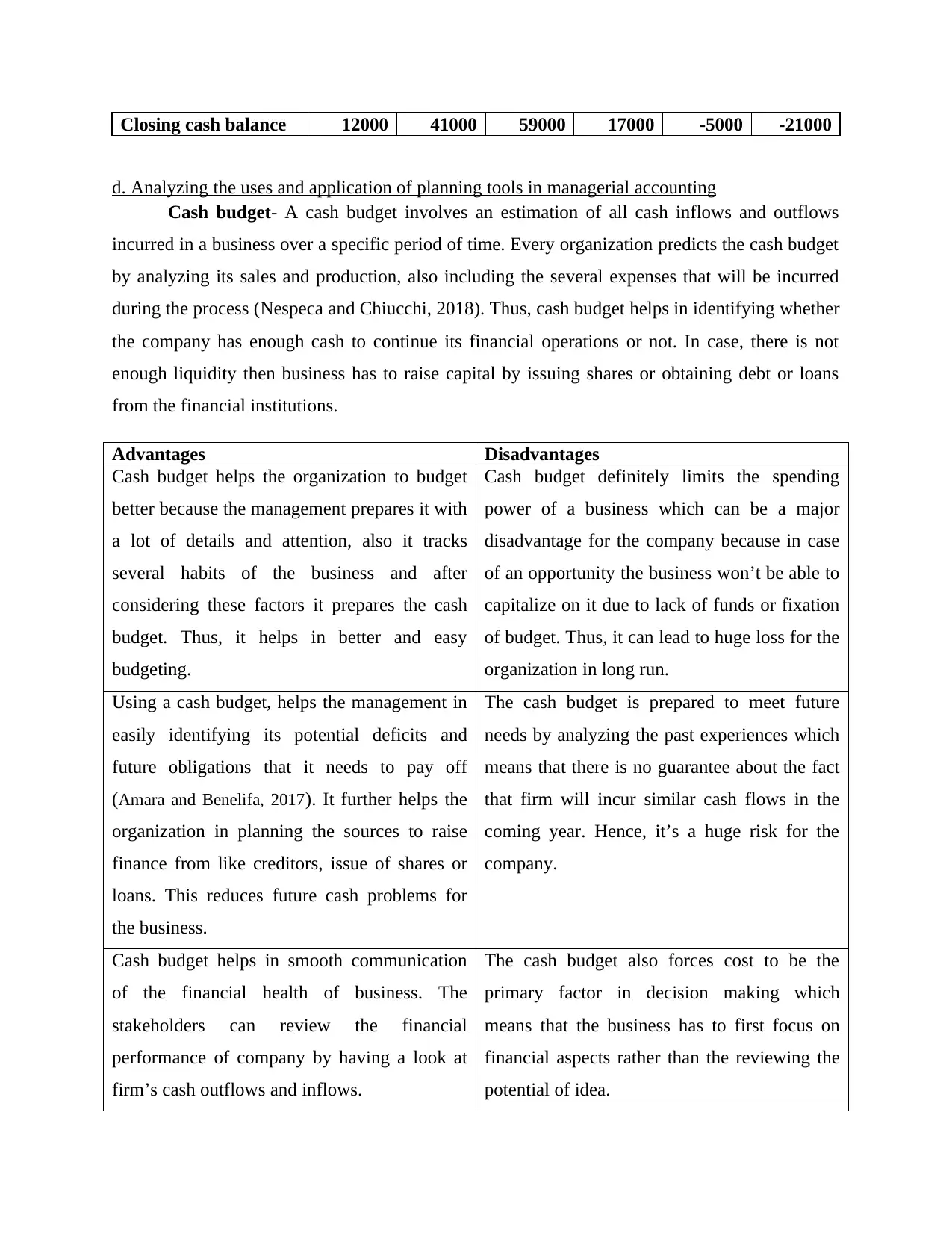

Closing cash balance 12000 41000 59000 17000 -5000 -21000

d. Analyzing the uses and application of planning tools in managerial accounting

Cash budget- A cash budget involves an estimation of all cash inflows and outflows

incurred in a business over a specific period of time. Every organization predicts the cash budget

by analyzing its sales and production, also including the several expenses that will be incurred

during the process (Nespeca and Chiucchi, 2018). Thus, cash budget helps in identifying whether

the company has enough cash to continue its financial operations or not. In case, there is not

enough liquidity then business has to raise capital by issuing shares or obtaining debt or loans

from the financial institutions.

Advantages Disadvantages

Cash budget helps the organization to budget

better because the management prepares it with

a lot of details and attention, also it tracks

several habits of the business and after

considering these factors it prepares the cash

budget. Thus, it helps in better and easy

budgeting.

Cash budget definitely limits the spending

power of a business which can be a major

disadvantage for the company because in case

of an opportunity the business won’t be able to

capitalize on it due to lack of funds or fixation

of budget. Thus, it can lead to huge loss for the

organization in long run.

Using a cash budget, helps the management in

easily identifying its potential deficits and

future obligations that it needs to pay off

(Amara and Benelifa, 2017). It further helps the

organization in planning the sources to raise

finance from like creditors, issue of shares or

loans. This reduces future cash problems for

the business.

The cash budget is prepared to meet future

needs by analyzing the past experiences which

means that there is no guarantee about the fact

that firm will incur similar cash flows in the

coming year. Hence, it’s a huge risk for the

company.

Cash budget helps in smooth communication

of the financial health of business. The

stakeholders can review the financial

performance of company by having a look at

firm’s cash outflows and inflows.

The cash budget also forces cost to be the

primary factor in decision making which

means that the business has to first focus on

financial aspects rather than the reviewing the

potential of idea.

d. Analyzing the uses and application of planning tools in managerial accounting

Cash budget- A cash budget involves an estimation of all cash inflows and outflows

incurred in a business over a specific period of time. Every organization predicts the cash budget

by analyzing its sales and production, also including the several expenses that will be incurred

during the process (Nespeca and Chiucchi, 2018). Thus, cash budget helps in identifying whether

the company has enough cash to continue its financial operations or not. In case, there is not

enough liquidity then business has to raise capital by issuing shares or obtaining debt or loans

from the financial institutions.

Advantages Disadvantages

Cash budget helps the organization to budget

better because the management prepares it with

a lot of details and attention, also it tracks

several habits of the business and after

considering these factors it prepares the cash

budget. Thus, it helps in better and easy

budgeting.

Cash budget definitely limits the spending

power of a business which can be a major

disadvantage for the company because in case

of an opportunity the business won’t be able to

capitalize on it due to lack of funds or fixation

of budget. Thus, it can lead to huge loss for the

organization in long run.

Using a cash budget, helps the management in

easily identifying its potential deficits and

future obligations that it needs to pay off

(Amara and Benelifa, 2017). It further helps the

organization in planning the sources to raise

finance from like creditors, issue of shares or

loans. This reduces future cash problems for

the business.

The cash budget is prepared to meet future

needs by analyzing the past experiences which

means that there is no guarantee about the fact

that firm will incur similar cash flows in the

coming year. Hence, it’s a huge risk for the

company.

Cash budget helps in smooth communication

of the financial health of business. The

stakeholders can review the financial

performance of company by having a look at

firm’s cash outflows and inflows.

The cash budget also forces cost to be the

primary factor in decision making which

means that the business has to first focus on

financial aspects rather than the reviewing the

potential of idea.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

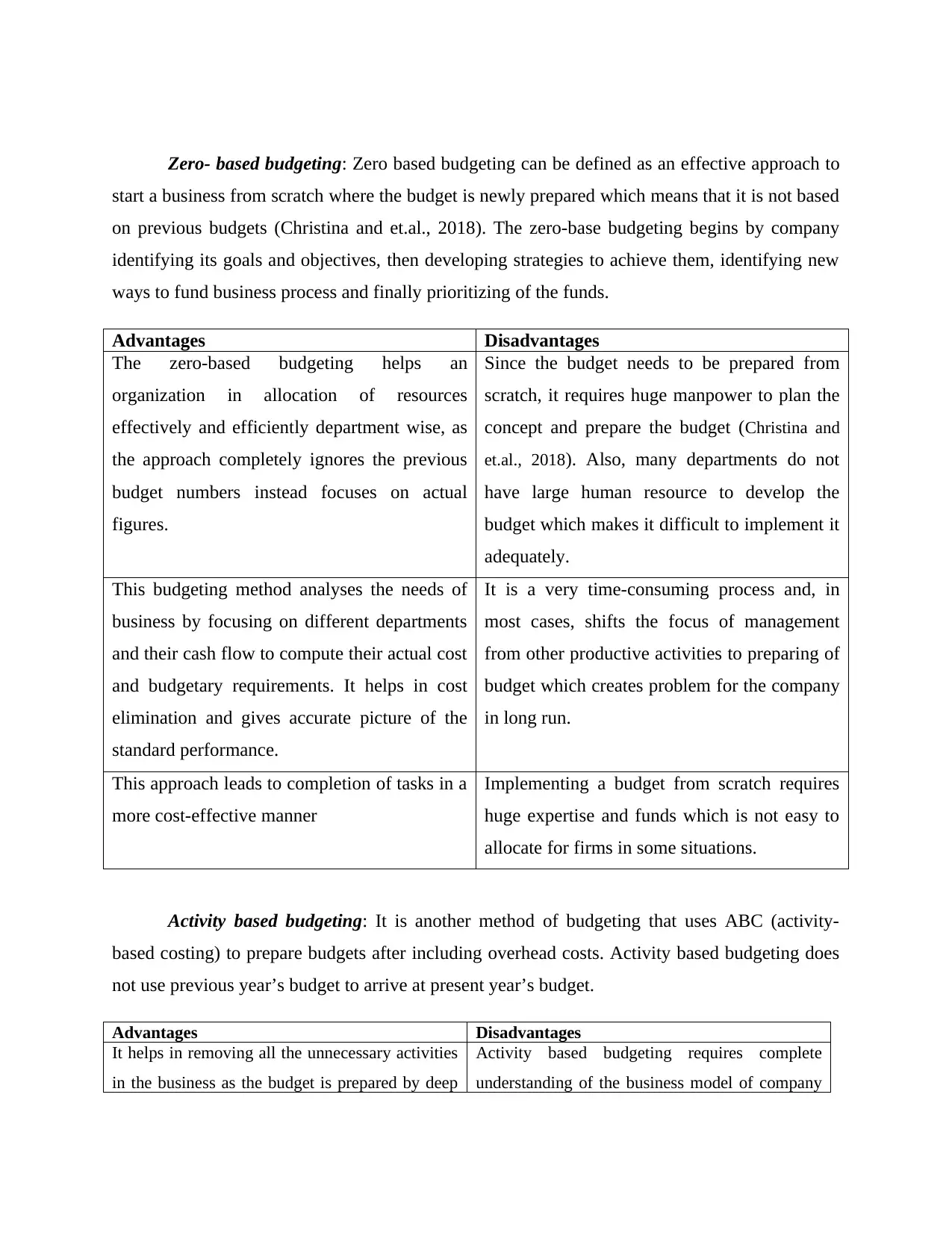

Zero- based budgeting: Zero based budgeting can be defined as an effective approach to

start a business from scratch where the budget is newly prepared which means that it is not based

on previous budgets (Christina and et.al., 2018). The zero-base budgeting begins by company

identifying its goals and objectives, then developing strategies to achieve them, identifying new

ways to fund business process and finally prioritizing of the funds.

Advantages Disadvantages

The zero-based budgeting helps an

organization in allocation of resources

effectively and efficiently department wise, as

the approach completely ignores the previous

budget numbers instead focuses on actual

figures.

Since the budget needs to be prepared from

scratch, it requires huge manpower to plan the

concept and prepare the budget (Christina and

et.al., 2018). Also, many departments do not

have large human resource to develop the

budget which makes it difficult to implement it

adequately.

This budgeting method analyses the needs of

business by focusing on different departments

and their cash flow to compute their actual cost

and budgetary requirements. It helps in cost

elimination and gives accurate picture of the

standard performance.

It is a very time-consuming process and, in

most cases, shifts the focus of management

from other productive activities to preparing of

budget which creates problem for the company

in long run.

This approach leads to completion of tasks in a

more cost-effective manner

Implementing a budget from scratch requires

huge expertise and funds which is not easy to

allocate for firms in some situations.

Activity based budgeting: It is another method of budgeting that uses ABC (activity-

based costing) to prepare budgets after including overhead costs. Activity based budgeting does

not use previous year’s budget to arrive at present year’s budget.

Advantages Disadvantages

It helps in removing all the unnecessary activities

in the business as the budget is prepared by deep

Activity based budgeting requires complete

understanding of the business model of company

start a business from scratch where the budget is newly prepared which means that it is not based

on previous budgets (Christina and et.al., 2018). The zero-base budgeting begins by company

identifying its goals and objectives, then developing strategies to achieve them, identifying new

ways to fund business process and finally prioritizing of the funds.

Advantages Disadvantages

The zero-based budgeting helps an

organization in allocation of resources

effectively and efficiently department wise, as

the approach completely ignores the previous

budget numbers instead focuses on actual

figures.

Since the budget needs to be prepared from

scratch, it requires huge manpower to plan the

concept and prepare the budget (Christina and

et.al., 2018). Also, many departments do not

have large human resource to develop the

budget which makes it difficult to implement it

adequately.

This budgeting method analyses the needs of

business by focusing on different departments

and their cash flow to compute their actual cost

and budgetary requirements. It helps in cost

elimination and gives accurate picture of the

standard performance.

It is a very time-consuming process and, in

most cases, shifts the focus of management

from other productive activities to preparing of

budget which creates problem for the company

in long run.

This approach leads to completion of tasks in a

more cost-effective manner

Implementing a budget from scratch requires

huge expertise and funds which is not easy to

allocate for firms in some situations.

Activity based budgeting: It is another method of budgeting that uses ABC (activity-

based costing) to prepare budgets after including overhead costs. Activity based budgeting does

not use previous year’s budget to arrive at present year’s budget.

Advantages Disadvantages

It helps in removing all the unnecessary activities

in the business as the budget is prepared by deep

Activity based budgeting requires complete

understanding of the business model of company

research and analysis. Thus, it saves firm’s funds

through removing all the bottlenecks.

and if the budget manager is not able to

understand it completely then it can lead to failure

of budgeting method.

Removing of bottlenecks leads to reduction in

price of goods and services which further

improves the company’s relationship with its

customers and also increases its market segment

in the industry.

The cost involved in implementing activity based

budgeting is high as it requires a lot of skilled

employees and the company has to bear the

expense of their training and development which

is very high and it has an adverse effect on the

other financial activities of business.

The budgeting method evaluates each and every

aspect of cost carefully to reduce the operational

cost and thus increase the profitability of business.

It focuses on short term goals and objectives

therefore it is not suitable for a company that has

a long term visions and objectives to achieve.

e. Explaining MA systems that helps in resolving financial problems

Key performance indicator-The key performance indicator can be defined as a

measurable value that showcases the effectiveness and efficiency of a company in accomplishing

its business goals and objectives. KPI’s are heavily used by companies at multiple levels to

evaluate their current position and success to reach the set targets (Curry, Hersinger and Nilsson,

2019). There are two types of KPI’s used by the companies like High-level KPI’s that focus on

the entire performance of the business and low level KPI’s that has its emphasis on specific

departments like sales, marketing and finance. The main objective of KPI’s is to provide

information about a set of things that an organization needs to do right to execute its strategy.

Variance analysis- Variance analysis is a systematic study of comparing the actual

performance of the company with standard performance and then identifying the deviations and

taking corrective actions accordingly. This is mainly done to rectify the errors and ensure that the

organization follows the budget blueprint and achieves its target goals.

Benchmarking- It is a process of measuring the overall performance of company’s

products and services against the best products in the same industry (Taylor and Scapens, 2016).

Benchmarking involves comparing the actual product produced by the company with standard

industry product, analyzing the differences and then implementing the changes in firm’s products

to improve the performance.

through removing all the bottlenecks.

and if the budget manager is not able to

understand it completely then it can lead to failure

of budgeting method.

Removing of bottlenecks leads to reduction in

price of goods and services which further

improves the company’s relationship with its

customers and also increases its market segment

in the industry.

The cost involved in implementing activity based

budgeting is high as it requires a lot of skilled

employees and the company has to bear the

expense of their training and development which

is very high and it has an adverse effect on the

other financial activities of business.

The budgeting method evaluates each and every

aspect of cost carefully to reduce the operational

cost and thus increase the profitability of business.

It focuses on short term goals and objectives

therefore it is not suitable for a company that has

a long term visions and objectives to achieve.

e. Explaining MA systems that helps in resolving financial problems

Key performance indicator-The key performance indicator can be defined as a

measurable value that showcases the effectiveness and efficiency of a company in accomplishing

its business goals and objectives. KPI’s are heavily used by companies at multiple levels to

evaluate their current position and success to reach the set targets (Curry, Hersinger and Nilsson,

2019). There are two types of KPI’s used by the companies like High-level KPI’s that focus on

the entire performance of the business and low level KPI’s that has its emphasis on specific

departments like sales, marketing and finance. The main objective of KPI’s is to provide

information about a set of things that an organization needs to do right to execute its strategy.

Variance analysis- Variance analysis is a systematic study of comparing the actual

performance of the company with standard performance and then identifying the deviations and

taking corrective actions accordingly. This is mainly done to rectify the errors and ensure that the

organization follows the budget blueprint and achieves its target goals.

Benchmarking- It is a process of measuring the overall performance of company’s

products and services against the best products in the same industry (Taylor and Scapens, 2016).

Benchmarking involves comparing the actual product produced by the company with standard

industry product, analyzing the differences and then implementing the changes in firm’s products

to improve the performance.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Balanced scorecard- It is a strategic performance scale to identify and then improve the

internal functions of business which results in better performance of the company. It is mainly

used to provide feedback to the organization which helps them in making better informed

decisions.

Financial governance- Financial governance can be defined as the manner through

which an organization collects, manages reviews and controls the financial information of

company (Shields and Shelleman, 2016). It is stated to be a singular most important system for

all financial procedures from close to disclosure.

ABC Ltd Lets Grow Ltd.

This company adopts key performance

indicator tool and financial governance in order

to overcome the challenges of problems

relating to funds. These techniques help the

firm in increasing the efficiency and

effectiveness of the business operations.

On the other hand, it makes use of

benchmarking and balanced scorecard in order

to achieve competitive edge against its rivalry

and also focusing on main perspectives of the

business which in turn helps the company in

gaining success.

f. Evaluating financial state of let’s Grow Ltd based on forecasted cash budget

It has been analyzed from the cash budget that in the coming six months, 4 months the

company will be earning profits as it is having sufficient cash balance and profits as compared to

its expenses. However, in last two months, the firm would result or incurring a loss as its

expenses will increase with a higher value than its total revenue. This shows that financial

position of Lets grow Ltd will be seen as getting poor with the passage of the months due to rise

in expenses with greater value.

CONCLUSION

From the above study it can be concluded that managerial accounting is indeed a critical

as well as crucial tool for the success of every organization. It not only helps in the better

working of internal management but also contributes towards strategic decision making that

further helps the business in achievement of its goals and objectives systematically. The above

report provided complete information about the financial performance of Let’s Grow limited

internal functions of business which results in better performance of the company. It is mainly

used to provide feedback to the organization which helps them in making better informed

decisions.

Financial governance- Financial governance can be defined as the manner through

which an organization collects, manages reviews and controls the financial information of

company (Shields and Shelleman, 2016). It is stated to be a singular most important system for

all financial procedures from close to disclosure.

ABC Ltd Lets Grow Ltd.

This company adopts key performance

indicator tool and financial governance in order

to overcome the challenges of problems

relating to funds. These techniques help the

firm in increasing the efficiency and

effectiveness of the business operations.

On the other hand, it makes use of

benchmarking and balanced scorecard in order

to achieve competitive edge against its rivalry

and also focusing on main perspectives of the

business which in turn helps the company in

gaining success.

f. Evaluating financial state of let’s Grow Ltd based on forecasted cash budget

It has been analyzed from the cash budget that in the coming six months, 4 months the

company will be earning profits as it is having sufficient cash balance and profits as compared to

its expenses. However, in last two months, the firm would result or incurring a loss as its

expenses will increase with a higher value than its total revenue. This shows that financial

position of Lets grow Ltd will be seen as getting poor with the passage of the months due to rise

in expenses with greater value.

CONCLUSION

From the above study it can be concluded that managerial accounting is indeed a critical

as well as crucial tool for the success of every organization. It not only helps in the better

working of internal management but also contributes towards strategic decision making that

further helps the business in achievement of its goals and objectives systematically. The above

report provided complete information about the financial performance of Let’s Grow limited

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

through its cash budget and also gave details regarding how it can be improved by implementing

management accounting tools like cost accounting, inventory management and job costing.

There are certain systems that can also be used by Let’s Grow ltd to improve its financial

performance like use of Key performance indicators, Variance analysis and Benchmarking.

Thus, at the end it can be stated that Management accounting is an essential system that

considers both qualitative and quantitative factors to improve the overall performance of an

enterprise.

management accounting tools like cost accounting, inventory management and job costing.

There are certain systems that can also be used by Let’s Grow ltd to improve its financial

performance like use of Key performance indicators, Variance analysis and Benchmarking.

Thus, at the end it can be stated that Management accounting is an essential system that

considers both qualitative and quantitative factors to improve the overall performance of an

enterprise.

REFERENCES

Books and journal

Amara, T. and Benelifa, S., 2017. The impact of external and internal factors on the MA

practices. International Journal of Finance and Accounting. 6(2). pp.46-58.

Christina, V. and et.al., 2018. Business Ethics Perception as Moderating Variable on the

Influence of MA System to Managerial Performance (Study at PT Bank Mandiri

(Persero), Tbk.). International Journal of Engineering & Technology. 7(4.34). pp.277-

280.

Curry, A., Hersinger, A. and Nilsson, K., 2019. Operations managers’ use of (ir) relevant MA

information: A mixed-methods approach. The Nordic Journal of Business. 68(1).

Ghasemi, R. and et.al., 2016. The mediating effect of MA system on the relationship between

competition and managerial performance. International Journal of Accounting and

Information Management.

Nespeca, A. and Chiucchi, M.S., 2018. The impact of business intelligence systems on MA

systems: The consultant’s perspective. In Network, smart and open (pp. 283-297).

Springer, Cham.

Shevelev, A. E., Sheveleva, E. V. and Gvozdev, M. Y., 2017. Methods of internal control in

integrated MA system of the enterprise. In SHS Web of Conferences (Vol. 35. p. 01115).

EDP Sciences.

Shields, J. and Shelleman, J. M., 2016. MA systems in micro-SMEs. Journal of Applied

Management and Entrepreneurship. 21(1). p.19.

Taylor, L. C. and Scapens, R. W., 2016. The role of identity and image in shaping MA

change. Accounting, Auditing & Accountability Journal.

ПАНЧЕНКО, О., 2018. Place and role of MA in the general accounting system. Облiк i

фiнанси. (3). pp.75-82.

Books and journal

Amara, T. and Benelifa, S., 2017. The impact of external and internal factors on the MA

practices. International Journal of Finance and Accounting. 6(2). pp.46-58.

Christina, V. and et.al., 2018. Business Ethics Perception as Moderating Variable on the

Influence of MA System to Managerial Performance (Study at PT Bank Mandiri

(Persero), Tbk.). International Journal of Engineering & Technology. 7(4.34). pp.277-

280.

Curry, A., Hersinger, A. and Nilsson, K., 2019. Operations managers’ use of (ir) relevant MA

information: A mixed-methods approach. The Nordic Journal of Business. 68(1).

Ghasemi, R. and et.al., 2016. The mediating effect of MA system on the relationship between

competition and managerial performance. International Journal of Accounting and

Information Management.

Nespeca, A. and Chiucchi, M.S., 2018. The impact of business intelligence systems on MA

systems: The consultant’s perspective. In Network, smart and open (pp. 283-297).

Springer, Cham.

Shevelev, A. E., Sheveleva, E. V. and Gvozdev, M. Y., 2017. Methods of internal control in

integrated MA system of the enterprise. In SHS Web of Conferences (Vol. 35. p. 01115).

EDP Sciences.

Shields, J. and Shelleman, J. M., 2016. MA systems in micro-SMEs. Journal of Applied

Management and Entrepreneurship. 21(1). p.19.

Taylor, L. C. and Scapens, R. W., 2016. The role of identity and image in shaping MA

change. Accounting, Auditing & Accountability Journal.

ПАНЧЕНКО, О., 2018. Place and role of MA in the general accounting system. Облiк i

фiнанси. (3). pp.75-82.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.