Managerial Accounting Report: Hawthorn Leisure Works - Fee Analysis

VerifiedAdded on 2023/04/04

|6

|1307

|72

Report

AI Summary

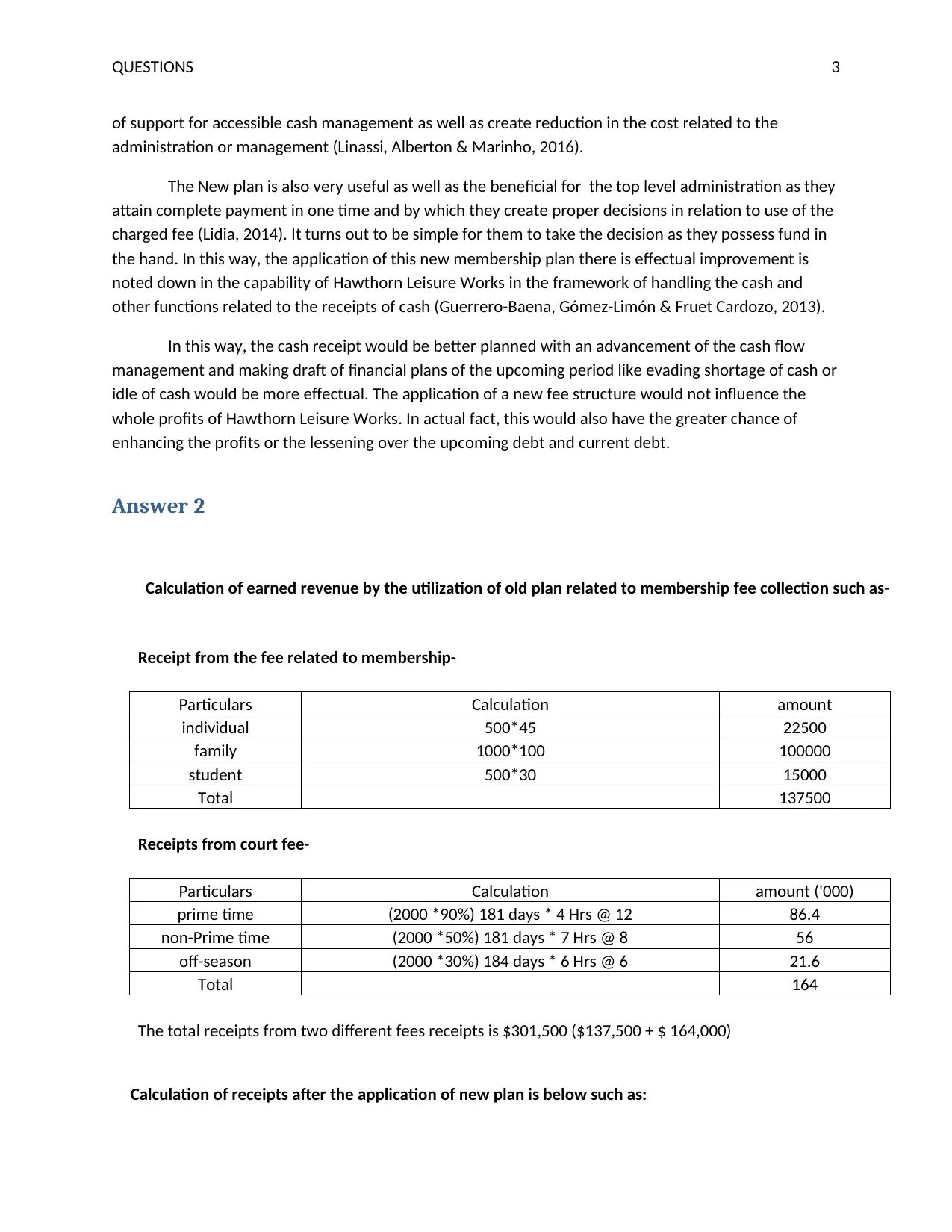

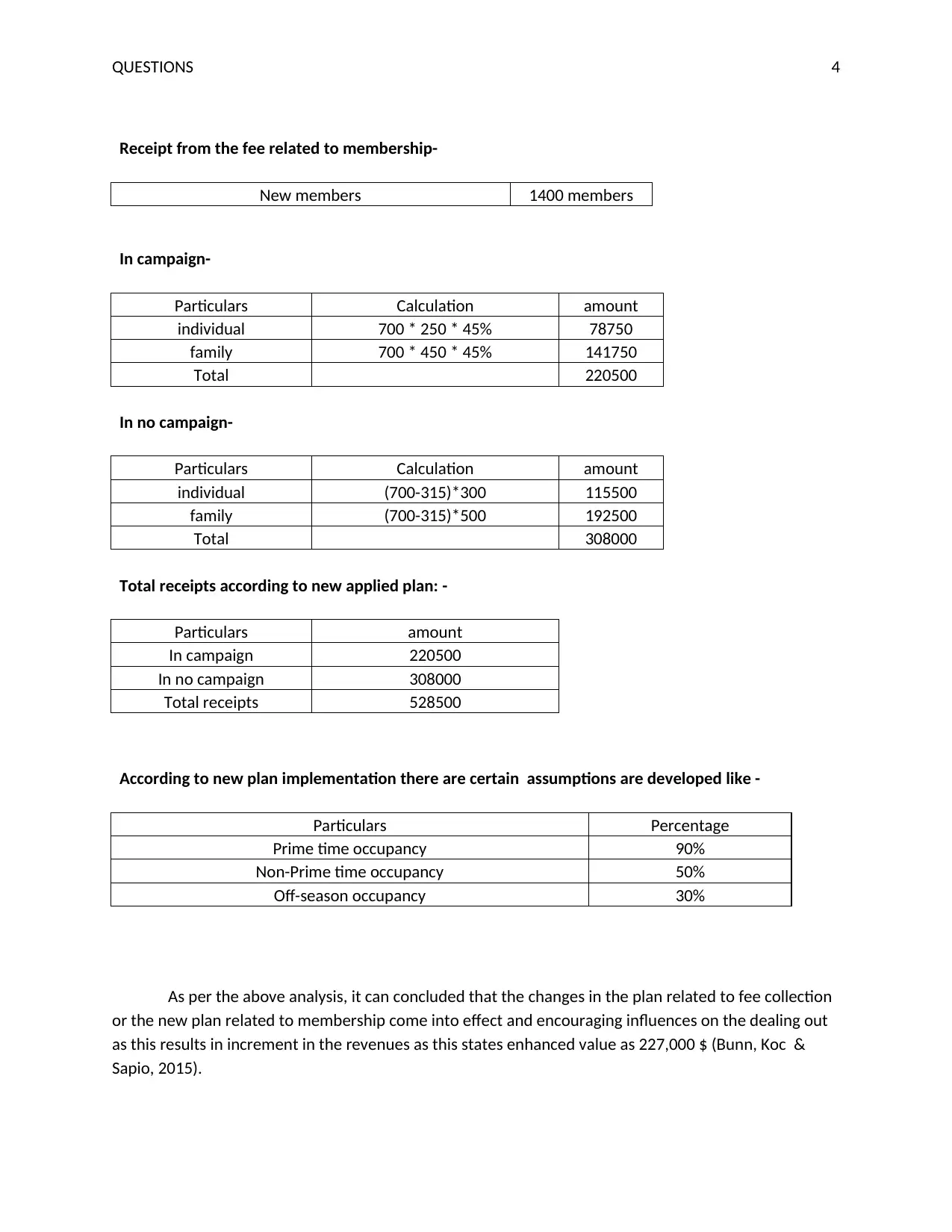

This managerial accounting report examines Hawthorn Leisure Works (HLW) and its fee structure, focusing on the impact of different fee models (hourly court fees vs. annual membership fees) on cash receipts and revenue. The report analyzes the financial implications of a new membership plan introduced by HLW, which shifts from hourly court fees to advance annual membership fees. It calculates earned revenue under both the old and new plans, considering factors like prime and non-prime time occupancy and campaign participation. The analysis highlights the changes in revenue and potential improvements in cash flow management resulting from the new plan. The report also discusses the application of activity-based costing and the importance of volume analysis in pricing decisions, as well as the role of cash flow statements in enhancing profitability. The report concludes by summarizing the benefits of the new fee structure for HLW.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.