Managerial Accounting Report: Ambertech Limited Budget Analysis

VerifiedAdded on 2023/04/20

|17

|4477

|203

Report

AI Summary

This report provides a comprehensive analysis of managerial accounting principles, focusing on the budgeting process and financial performance evaluation. It begins with an executive summary outlining the significance of budgeting for expense and income detection in the next fiscal year. The report delves into the components of a master budget, essential for preparing future budgets, and then applies these concepts to the financial data of Ambertech Limited for 2018 and 2019. It includes the calculation of a 2019 income statement and a comparison of the 2018 actuals with the forecasted 2019 budget. The report also discusses the elements of the master budget, such as sales, production, direct labor, cash, and various material budgets. Finally, it compares the top-down and bottom-up approaches to budgeting, analyzing their suitability for the company and concluding with insights into the changes made in the forecasted annual report.

Running head: MANAGERIAL ACCOUNTING

Managerial Accounting

Name of the Student:

Name of the University:

Authors Note:

Managerial Accounting

Name of the Student:

Name of the University:

Authors Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

MANAGERIAL ACCOUNTING

1

Executive Summary:

The overall assessment aims in evaluating the significance of budgeting process, which can

be used by organisation for detecting the overall expenses and income that needs to be

incurred in next fiscal year. In addition, the financial performance of the organisation is

mainly evaluated for devising the budgeted, which can adequately support the cash inflows

and outflows during the next fiscal years. Moreover, the components of the master budget are

mainly discussed, which is an essential part of the budgeting process, as it allows the

organisation to prepare an appropriate budget for future fiscal years. The financial budget of

Ambertech Limited is mainly calculated for detecting the overall budget for 2019, which can

help in detecting the incoming and expenses for the organisation. The analysis of the master

budget components directly allows the management to detect the expenses and income that is

estimated for future operations of the organisation. The analysis of the future projected

annual report can eventually help in understanding the measures that has been taken by the

company to generate the required level of income in 2019. Lastly, the comparison of 2018

and forecasted budget for 2019 is mainly conducted in the assessment for detecting the

opinion on the changes, which has been conducted while preparing the forecasted annual

report.

1

Executive Summary:

The overall assessment aims in evaluating the significance of budgeting process, which can

be used by organisation for detecting the overall expenses and income that needs to be

incurred in next fiscal year. In addition, the financial performance of the organisation is

mainly evaluated for devising the budgeted, which can adequately support the cash inflows

and outflows during the next fiscal years. Moreover, the components of the master budget are

mainly discussed, which is an essential part of the budgeting process, as it allows the

organisation to prepare an appropriate budget for future fiscal years. The financial budget of

Ambertech Limited is mainly calculated for detecting the overall budget for 2019, which can

help in detecting the incoming and expenses for the organisation. The analysis of the master

budget components directly allows the management to detect the expenses and income that is

estimated for future operations of the organisation. The analysis of the future projected

annual report can eventually help in understanding the measures that has been taken by the

company to generate the required level of income in 2019. Lastly, the comparison of 2018

and forecasted budget for 2019 is mainly conducted in the assessment for detecting the

opinion on the changes, which has been conducted while preparing the forecasted annual

report.

MANAGERIAL ACCOUNTING

2

Table of Contents

Introduction:...............................................................................................................................3

a. Explanation of the elements of Master Budget:.....................................................................4

b. Discussing about the comparison of top-down and bottom-up approach to the budget

process and analyse, which detecting the most suitable chosen for the company:....................8

c. Producing the budget of Income statement for 2019:..........................................................10

d. Comparing the data and providing relevant opinion on the changes for 2019 budget and

2018 actual income statement:.................................................................................................11

Conclusion:..............................................................................................................................13

Reference and Bibliography:....................................................................................................14

2

Table of Contents

Introduction:...............................................................................................................................3

a. Explanation of the elements of Master Budget:.....................................................................4

b. Discussing about the comparison of top-down and bottom-up approach to the budget

process and analyse, which detecting the most suitable chosen for the company:....................8

c. Producing the budget of Income statement for 2019:..........................................................10

d. Comparing the data and providing relevant opinion on the changes for 2019 budget and

2018 actual income statement:.................................................................................................11

Conclusion:..............................................................................................................................13

Reference and Bibliography:....................................................................................................14

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

MANAGERIAL ACCOUNTING

3

Introduction:

The assessment aims in evaluating the financial performance of Ambertech Limited

for the financial year of 2018 and projecting future income, which can be generated by the

company. In addition, there is further evaluation that has been conducted in the assessment

regarding the top-down and bottom-up approach to the budget process, which can help in

analysing the budget process. Furthermore, the income statement for the financial year of

2019 has been projected, which can help in determining the future incomes of the company.

Adequate analysis of each elements of the master budget has been conducted for determining

the impacts, which can be conducted on the financial performance. The analysis of the master

budget components directly allows the management to detect the expenses and income that is

estimated for future operations of the organisation. The analysis of the future projected

annual report can eventually help in understanding the measures that has been taken by the

company to generate the required level of income in 2019. Lastly, the comparison of 2018

and forecasted budget for 2019 is mainly conducted in the assessment for detecting the

opinion on the changes, which has been conducted while preparing the forecasted annual

report.

3

Introduction:

The assessment aims in evaluating the financial performance of Ambertech Limited

for the financial year of 2018 and projecting future income, which can be generated by the

company. In addition, there is further evaluation that has been conducted in the assessment

regarding the top-down and bottom-up approach to the budget process, which can help in

analysing the budget process. Furthermore, the income statement for the financial year of

2019 has been projected, which can help in determining the future incomes of the company.

Adequate analysis of each elements of the master budget has been conducted for determining

the impacts, which can be conducted on the financial performance. The analysis of the master

budget components directly allows the management to detect the expenses and income that is

estimated for future operations of the organisation. The analysis of the future projected

annual report can eventually help in understanding the measures that has been taken by the

company to generate the required level of income in 2019. Lastly, the comparison of 2018

and forecasted budget for 2019 is mainly conducted in the assessment for detecting the

opinion on the changes, which has been conducted while preparing the forecasted annual

report.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

MANAGERIAL ACCOUNTING

4

Ending

finished goods

budget

Sale budget

Production

Budget

Direct labour

budget

Cash Budget

Direct

Material

Budget

Selling and

administrative

budget

Manufacturing

overhead budget

Budgeted Financial Statements

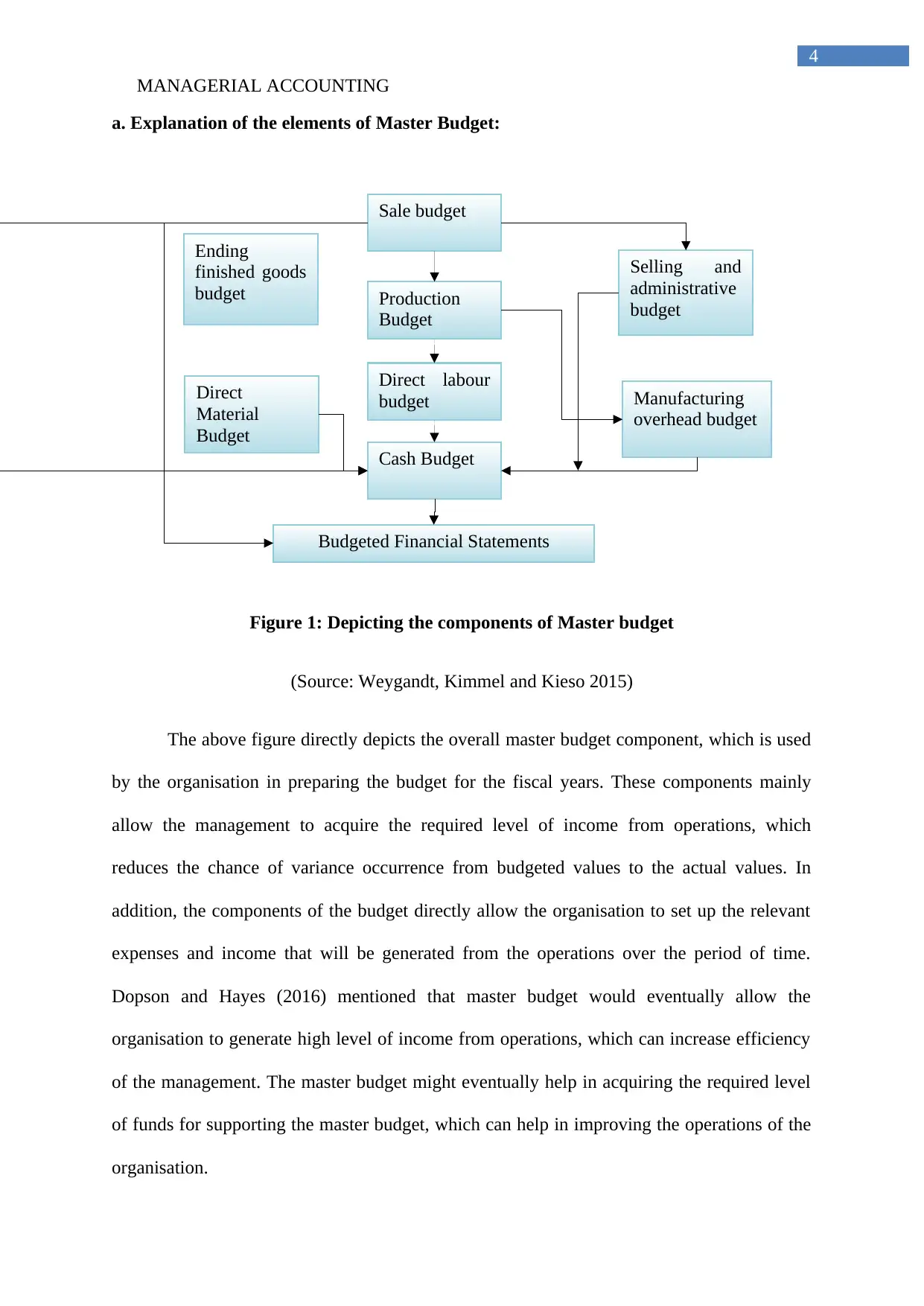

a. Explanation of the elements of Master Budget:

Figure 1: Depicting the components of Master budget

(Source: Weygandt, Kimmel and Kieso 2015)

The above figure directly depicts the overall master budget component, which is used

by the organisation in preparing the budget for the fiscal years. These components mainly

allow the management to acquire the required level of income from operations, which

reduces the chance of variance occurrence from budgeted values to the actual values. In

addition, the components of the budget directly allow the organisation to set up the relevant

expenses and income that will be generated from the operations over the period of time.

Dopson and Hayes (2016) mentioned that master budget would eventually allow the

organisation to generate high level of income from operations, which can increase efficiency

of the management. The master budget might eventually help in acquiring the required level

of funds for supporting the master budget, which can help in improving the operations of the

organisation.

4

Ending

finished goods

budget

Sale budget

Production

Budget

Direct labour

budget

Cash Budget

Direct

Material

Budget

Selling and

administrative

budget

Manufacturing

overhead budget

Budgeted Financial Statements

a. Explanation of the elements of Master Budget:

Figure 1: Depicting the components of Master budget

(Source: Weygandt, Kimmel and Kieso 2015)

The above figure directly depicts the overall master budget component, which is used

by the organisation in preparing the budget for the fiscal years. These components mainly

allow the management to acquire the required level of income from operations, which

reduces the chance of variance occurrence from budgeted values to the actual values. In

addition, the components of the budget directly allow the organisation to set up the relevant

expenses and income that will be generated from the operations over the period of time.

Dopson and Hayes (2016) mentioned that master budget would eventually allow the

organisation to generate high level of income from operations, which can increase efficiency

of the management. The master budget might eventually help in acquiring the required level

of funds for supporting the master budget, which can help in improving the operations of the

organisation.

MANAGERIAL ACCOUNTING

5

The elements of master budget are depicted as follows.

Sales budget:

Sales budget is considered the basic component of the master budget, which allows

the organisation to detect the level of sales units that will be incurred from the operations.

The overall expected price per units and the number of units sold for the future fiscal years is

mainly estimated in the sales budget. Moreover, the sales budget values are identified from

the historical growth in sales values that has been generated by the organisation. The sales

budget directly influences the other components of the master budget, as rising sales units

will alter the production and expense needs of the organisation (Noreen, Brewer and Garrison

2014).

Production budget:

The production budget is mainly used by the organisation for detecting the level of

planned production, which needs to be conducted by the management for supporting their

products demand. In addition, the production budget would be beneficial for the organisation

to determine the required level of raw materials and other purchases that needs to be

conducted for smoothly conducting their operations. The production budget ensures the

organisation to determine the level of activities, which will be needed for supporting the sales

demand from customers.

Direct labour budget:

The direct labour budget is influenced directly by the sales budget prepared by the

organisation. This high level of output needed by the sales budget will directly affect the

needs of direct labour in the production system. Hence, the direct labour budget would allow

the organisation to determine the level of workers needed in the production function to

5

The elements of master budget are depicted as follows.

Sales budget:

Sales budget is considered the basic component of the master budget, which allows

the organisation to detect the level of sales units that will be incurred from the operations.

The overall expected price per units and the number of units sold for the future fiscal years is

mainly estimated in the sales budget. Moreover, the sales budget values are identified from

the historical growth in sales values that has been generated by the organisation. The sales

budget directly influences the other components of the master budget, as rising sales units

will alter the production and expense needs of the organisation (Noreen, Brewer and Garrison

2014).

Production budget:

The production budget is mainly used by the organisation for detecting the level of

planned production, which needs to be conducted by the management for supporting their

products demand. In addition, the production budget would be beneficial for the organisation

to determine the required level of raw materials and other purchases that needs to be

conducted for smoothly conducting their operations. The production budget ensures the

organisation to determine the level of activities, which will be needed for supporting the sales

demand from customers.

Direct labour budget:

The direct labour budget is influenced directly by the sales budget prepared by the

organisation. This high level of output needed by the sales budget will directly affect the

needs of direct labour in the production system. Hence, the direct labour budget would allow

the organisation to determine the level of workers needed in the production function to

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

MANAGERIAL ACCOUNTING

6

support the production output and comply with the sales budget. The direct labour budget is

prepared after the preparation of the production units, which determines the level of labour

input that will be needed for the next fiscal year (Butler and Ghosh 2015).

Cash budget:

Cash budget is mainly prepared after determining the level of expenses and income

that will be generated from the operations. The cash budget directly indicates the level of

cash position that will be generated by the organisation during the fiscal year. In addition, the

cash budget relevantly allows the organisation to detect high level of cash inflows and

outflows, which will be conducted from the operations. The preparation of cash budget is

mainly conducted after preparing the sales and production budget, which allows the

management to determine the level of net cash flow that will be increased over the period of

time.

Ending finished good budget:

The ending finished goods budget is determined are the prepared of the overall

material budget and the production budget. This component of the master budget relevantly

allows the management to determine the level of units that will be needed by the organisation

to support the ending finished goods for the fiscal year. In addition, the determination of the

finished good budget would eventually help in generating high level of income from

operations.

Direct material budget:

The direct material budget is prepared after the completion of the production budget

and sales budget, which help in determining the level of materials that will be needed to

support the sales demand from customers. In addition, the direct material budget would

6

support the production output and comply with the sales budget. The direct labour budget is

prepared after the preparation of the production units, which determines the level of labour

input that will be needed for the next fiscal year (Butler and Ghosh 2015).

Cash budget:

Cash budget is mainly prepared after determining the level of expenses and income

that will be generated from the operations. The cash budget directly indicates the level of

cash position that will be generated by the organisation during the fiscal year. In addition, the

cash budget relevantly allows the organisation to detect high level of cash inflows and

outflows, which will be conducted from the operations. The preparation of cash budget is

mainly conducted after preparing the sales and production budget, which allows the

management to determine the level of net cash flow that will be increased over the period of

time.

Ending finished good budget:

The ending finished goods budget is determined are the prepared of the overall

material budget and the production budget. This component of the master budget relevantly

allows the management to determine the level of units that will be needed by the organisation

to support the ending finished goods for the fiscal year. In addition, the determination of the

finished good budget would eventually help in generating high level of income from

operations.

Direct material budget:

The direct material budget is prepared after the completion of the production budget

and sales budget, which help in determining the level of materials that will be needed to

support the sales demand from customers. In addition, the direct material budget would

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

MANAGERIAL ACCOUNTING

7

eventually help in determining the level of expenses, which is needed by the organisation to

support their production needs. The material budget also allows the organisation to

understand the requirements of material after analysing the inventory currently held for

production (Epure 2016).

Selling and administrative budget:

The managers for analysing the planned operations expenses use the selling and

administrative budget and other manufacturing costs incurred during the fiscal year. In

addition, the evaluation also helps in determining the selling expenses and administrative

expenses, which needs to be incurred by the company for supporting the future operations.

The selling and administrative expenses would eventually help in determining the level of

spending which needs to be conducted by the company for supporting the operations during

the fiscal year by analysing the output.

Manufacturing overhead budget:

The manufacturing overhead budget directly provides the details regarding

manufacturing costs, which needs to be incurred by the organisation leaving the direct

material and direct labour cost. The information represented in the manufacturing overhead

budget cost is directly linked with the cost of goods sold by the organisation. This eventually

helps in determining the level of expenses that needs to be incurred by the company to

support the future sales units of the company. The budget is considered significant in nature,

as it contains large portion of the expenses, which needs to be conducted by the organisation

to accommodate the targeted sales.

Budgeted financial statements:

7

eventually help in determining the level of expenses, which is needed by the organisation to

support their production needs. The material budget also allows the organisation to

understand the requirements of material after analysing the inventory currently held for

production (Epure 2016).

Selling and administrative budget:

The managers for analysing the planned operations expenses use the selling and

administrative budget and other manufacturing costs incurred during the fiscal year. In

addition, the evaluation also helps in determining the selling expenses and administrative

expenses, which needs to be incurred by the company for supporting the future operations.

The selling and administrative expenses would eventually help in determining the level of

spending which needs to be conducted by the company for supporting the operations during

the fiscal year by analysing the output.

Manufacturing overhead budget:

The manufacturing overhead budget directly provides the details regarding

manufacturing costs, which needs to be incurred by the organisation leaving the direct

material and direct labour cost. The information represented in the manufacturing overhead

budget cost is directly linked with the cost of goods sold by the organisation. This eventually

helps in determining the level of expenses that needs to be incurred by the company to

support the future sales units of the company. The budget is considered significant in nature,

as it contains large portion of the expenses, which needs to be conducted by the organisation

to accommodate the targeted sales.

Budgeted financial statements:

MANAGERIAL ACCOUNTING

8

Budgeted financial statements is prepared by the organisation after completing the

above components of the master budget, as it helps in preparing the income statement and

balance sheet for the fiscal year. In addition, the budgeted financial statement would

eventually help in determining the projected incomes, which will be generated by the

company over the next fiscal years. This would eventually help in determining the level of

income and expenses that will be incurred during the fiscal year (Warren, Moffitt and Byrnes

2015).

b. Discussing about the comparison of top-down and bottom-up approach to the budget

process and analyse, which detecting the most suitable chosen for the company:

There are significant differences between the top-down and bottom-up approach,

which can be used by the organisation, while preparing the budget. In addition, the

comparison would eventually help in detecting the most viable budgeting process, which can

be used by the organisation for preparing the budge, which can support their future

operations. Top-down and bottom-up approach is mainly used in different areas of the

business, which helps the management to make relevant decisions regarding the operations.

The top down approach mainly evaluates the situation from general perspective to specific,

while the bottom-up approach focuses on specific conditions and then moves to general

attributes. Furthermore, there is specific difference between the top-down and bottom up

approach of the budget process, which indicates the alternative measure that is taken by each

process (Kaplan and Atkinson 2015).

The top managements mainly set top down budget, which does not allow the ultimate

budget holders to have the opportunity for participating in the budgeting process. In addition,

the top management directly creates the budget, where adequate allocation of resources is

conducted as per the discretion of the high officials. The department heads in this process is

8

Budgeted financial statements is prepared by the organisation after completing the

above components of the master budget, as it helps in preparing the income statement and

balance sheet for the fiscal year. In addition, the budgeted financial statement would

eventually help in determining the projected incomes, which will be generated by the

company over the next fiscal years. This would eventually help in determining the level of

income and expenses that will be incurred during the fiscal year (Warren, Moffitt and Byrnes

2015).

b. Discussing about the comparison of top-down and bottom-up approach to the budget

process and analyse, which detecting the most suitable chosen for the company:

There are significant differences between the top-down and bottom-up approach,

which can be used by the organisation, while preparing the budget. In addition, the

comparison would eventually help in detecting the most viable budgeting process, which can

be used by the organisation for preparing the budge, which can support their future

operations. Top-down and bottom-up approach is mainly used in different areas of the

business, which helps the management to make relevant decisions regarding the operations.

The top down approach mainly evaluates the situation from general perspective to specific,

while the bottom-up approach focuses on specific conditions and then moves to general

attributes. Furthermore, there is specific difference between the top-down and bottom up

approach of the budget process, which indicates the alternative measure that is taken by each

process (Kaplan and Atkinson 2015).

The top managements mainly set top down budget, which does not allow the ultimate

budget holders to have the opportunity for participating in the budgeting process. In addition,

the top management directly creates the budget, where adequate allocation of resources is

conducted as per the discretion of the high officials. The department heads in this process is

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

MANAGERIAL ACCOUNTING

9

not being used by the organisation for determining the budgeted values that is needed by the

organisation. The top-down budget process directly allows the manager to create the budget

within the confines of the desired budgeted values. This type of approach has certain

significance, which reduces the lead-time for completing the production process, as top

management are responsible for the preparation of budget. Hence, the timesaving’s can be

conducted in this method, which can reduce the involvement of persons who are responsible

for the day-to-day work of the organisation. However, there are certain disadvantages to the

method, which directly relates to the non-involvements of individual who can detect the

specific expenses that might incur during the operations. This might result in low

performance of the budget, as high-level individuals cannot accommodate adequate expenses

that will be incurred in the department (Eker and Aytaç 2016).

The bottom-up approach of budgeting is mainly a system, where budget holders are

able to participate in their own budgets. This type of budgeting process directly involves the

managers of the department in preparing the overall budget and send to the top management

for approval. This type of budgeting process mainly requires the managers of the department

to prepare the budget in accordance with their needs and expenses. This type of approach has

specific significance, where the estimated expenses are adequately accommodated by the

budget. However, there are specific disadvantages of the bottom-up approach, which the

expenses that might be conducted by the management due to the higher spending target of the

departments. Therefore, the bottom-up approach will directly raise the level of expenses that

is needed for each department, as the budget will accommodate the expense requirement of

all the relevant department managers (Vladychyn 2017).

Both the top-bottom and bottom-up budgeting approach has advantages and

disadvantages, which can negatively affect the prepared budget of the organisation. However,

top-bottom approach is mainly selected for Ambertech Limited, as it will allow the

9

not being used by the organisation for determining the budgeted values that is needed by the

organisation. The top-down budget process directly allows the manager to create the budget

within the confines of the desired budgeted values. This type of approach has certain

significance, which reduces the lead-time for completing the production process, as top

management are responsible for the preparation of budget. Hence, the timesaving’s can be

conducted in this method, which can reduce the involvement of persons who are responsible

for the day-to-day work of the organisation. However, there are certain disadvantages to the

method, which directly relates to the non-involvements of individual who can detect the

specific expenses that might incur during the operations. This might result in low

performance of the budget, as high-level individuals cannot accommodate adequate expenses

that will be incurred in the department (Eker and Aytaç 2016).

The bottom-up approach of budgeting is mainly a system, where budget holders are

able to participate in their own budgets. This type of budgeting process directly involves the

managers of the department in preparing the overall budget and send to the top management

for approval. This type of budgeting process mainly requires the managers of the department

to prepare the budget in accordance with their needs and expenses. This type of approach has

specific significance, where the estimated expenses are adequately accommodated by the

budget. However, there are specific disadvantages of the bottom-up approach, which the

expenses that might be conducted by the management due to the higher spending target of the

departments. Therefore, the bottom-up approach will directly raise the level of expenses that

is needed for each department, as the budget will accommodate the expense requirement of

all the relevant department managers (Vladychyn 2017).

Both the top-bottom and bottom-up budgeting approach has advantages and

disadvantages, which can negatively affect the prepared budget of the organisation. However,

top-bottom approach is mainly selected for Ambertech Limited, as it will allow the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

MANAGERIAL ACCOUNTING

10

organisation to prepare the adequate budget for supporting their operations. The top-bottom

approach would eventually help in designing the adequate level of expenses and income for

the organisation, which can be incurred during the fiscal year.

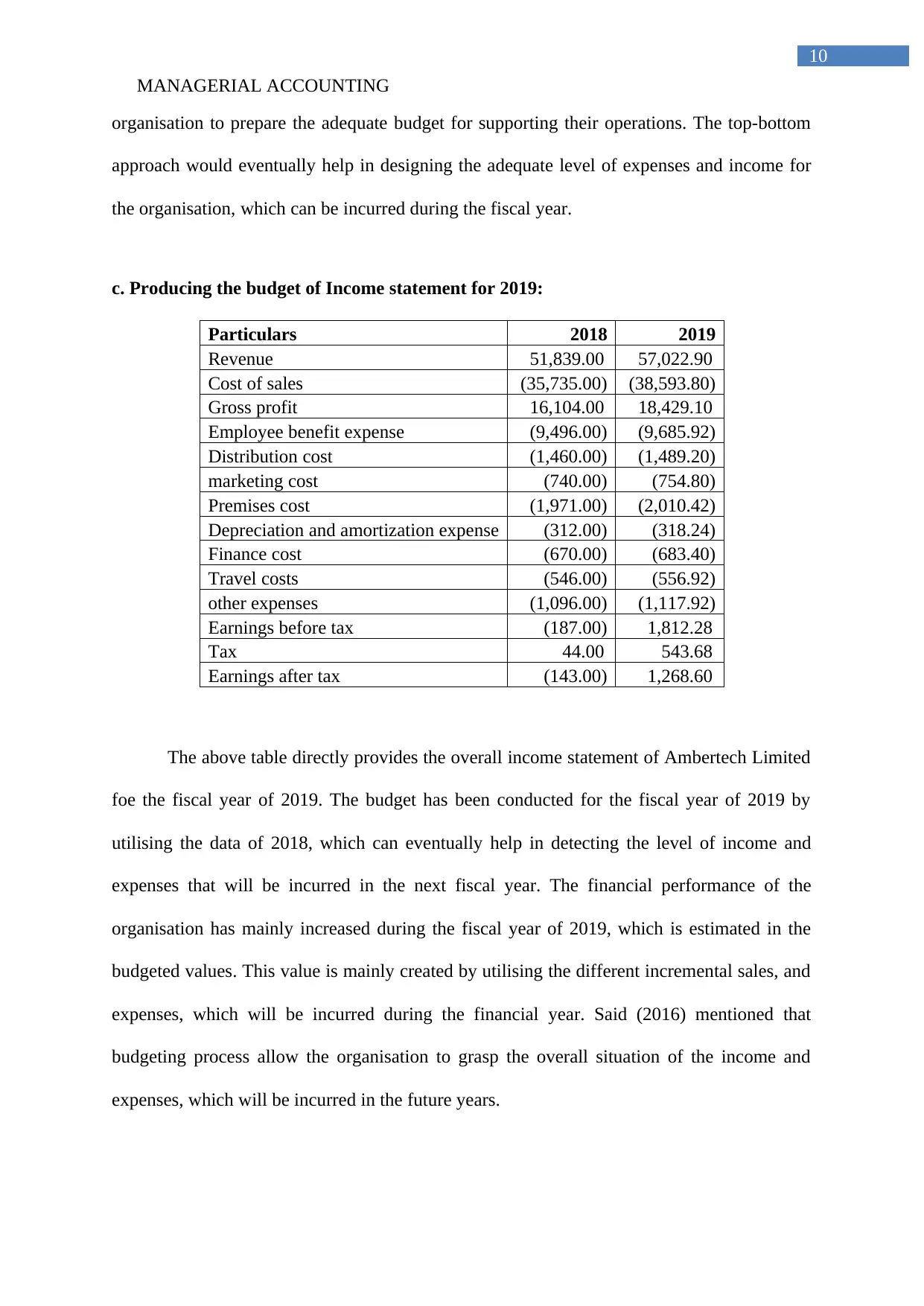

c. Producing the budget of Income statement for 2019:

Particulars 2018 2019

Revenue 51,839.00 57,022.90

Cost of sales (35,735.00) (38,593.80)

Gross profit 16,104.00 18,429.10

Employee benefit expense (9,496.00) (9,685.92)

Distribution cost (1,460.00) (1,489.20)

marketing cost (740.00) (754.80)

Premises cost (1,971.00) (2,010.42)

Depreciation and amortization expense (312.00) (318.24)

Finance cost (670.00) (683.40)

Travel costs (546.00) (556.92)

other expenses (1,096.00) (1,117.92)

Earnings before tax (187.00) 1,812.28

Tax 44.00 543.68

Earnings after tax (143.00) 1,268.60

The above table directly provides the overall income statement of Ambertech Limited

foe the fiscal year of 2019. The budget has been conducted for the fiscal year of 2019 by

utilising the data of 2018, which can eventually help in detecting the level of income and

expenses that will be incurred in the next fiscal year. The financial performance of the

organisation has mainly increased during the fiscal year of 2019, which is estimated in the

budgeted values. This value is mainly created by utilising the different incremental sales, and

expenses, which will be incurred during the financial year. Said (2016) mentioned that

budgeting process allow the organisation to grasp the overall situation of the income and

expenses, which will be incurred in the future years.

10

organisation to prepare the adequate budget for supporting their operations. The top-bottom

approach would eventually help in designing the adequate level of expenses and income for

the organisation, which can be incurred during the fiscal year.

c. Producing the budget of Income statement for 2019:

Particulars 2018 2019

Revenue 51,839.00 57,022.90

Cost of sales (35,735.00) (38,593.80)

Gross profit 16,104.00 18,429.10

Employee benefit expense (9,496.00) (9,685.92)

Distribution cost (1,460.00) (1,489.20)

marketing cost (740.00) (754.80)

Premises cost (1,971.00) (2,010.42)

Depreciation and amortization expense (312.00) (318.24)

Finance cost (670.00) (683.40)

Travel costs (546.00) (556.92)

other expenses (1,096.00) (1,117.92)

Earnings before tax (187.00) 1,812.28

Tax 44.00 543.68

Earnings after tax (143.00) 1,268.60

The above table directly provides the overall income statement of Ambertech Limited

foe the fiscal year of 2019. The budget has been conducted for the fiscal year of 2019 by

utilising the data of 2018, which can eventually help in detecting the level of income and

expenses that will be incurred in the next fiscal year. The financial performance of the

organisation has mainly increased during the fiscal year of 2019, which is estimated in the

budgeted values. This value is mainly created by utilising the different incremental sales, and

expenses, which will be incurred during the financial year. Said (2016) mentioned that

budgeting process allow the organisation to grasp the overall situation of the income and

expenses, which will be incurred in the future years.

MANAGERIAL ACCOUNTING

11

From the evaluation of the above calculation, it can be detected that the relevant

increment in the overall expenses of the organisation is estimated at the levels of 10%, which

has increased the revenues for the fiscal year of 2019. This increment has mainly allowed the

gross profit to increase in the budgeted values of 2019. The cost of goods sold is estimated to

increase at the levels of 8%, which has provided a positive gross profit margin for the

budgeted period of 2019. However, the other expense that has been incurred by the company

has only increased at the levels of 2%, which has made a positive net profit for the budgeted

financial year of 2019. The evaluation of financial performance can be conducted with the

help of above figure and determine the level of incomes, which can be generated from

operations. Mihaila (2014) indicated that budget preparation is conducted with the help of

adequate assumptions, as it allows the organization to detect the future operational needs that

must be met by the management.

The budgeted revenues can be achieved by the organization after implementing

adequate marketing strategies and increasing the demand for its products. The increment in

overall revenues of the organization is mainly essential, as it will allow the management to

acquire the adequate cash inflow to support the cash outflow. The budgeted income statement

for 2019 is relatively positive for Ambertech Limited, which was not previously incurred

during the fiscal year of 2018. Fry and Fiedler (2014) argued that budget process could

negatively affect the operations of the organization if adequate research is not conducted

while preparing the master budget.

d. Comparing the data and providing relevant opinion on the changes for 2019 budget

and 2018 actual income statement:

The above table directly represents the overall budgeted income statement of the

organization for the fiscal year of 2019, which is prepared in accordance with the financial

11

From the evaluation of the above calculation, it can be detected that the relevant

increment in the overall expenses of the organisation is estimated at the levels of 10%, which

has increased the revenues for the fiscal year of 2019. This increment has mainly allowed the

gross profit to increase in the budgeted values of 2019. The cost of goods sold is estimated to

increase at the levels of 8%, which has provided a positive gross profit margin for the

budgeted period of 2019. However, the other expense that has been incurred by the company

has only increased at the levels of 2%, which has made a positive net profit for the budgeted

financial year of 2019. The evaluation of financial performance can be conducted with the

help of above figure and determine the level of incomes, which can be generated from

operations. Mihaila (2014) indicated that budget preparation is conducted with the help of

adequate assumptions, as it allows the organization to detect the future operational needs that

must be met by the management.

The budgeted revenues can be achieved by the organization after implementing

adequate marketing strategies and increasing the demand for its products. The increment in

overall revenues of the organization is mainly essential, as it will allow the management to

acquire the adequate cash inflow to support the cash outflow. The budgeted income statement

for 2019 is relatively positive for Ambertech Limited, which was not previously incurred

during the fiscal year of 2018. Fry and Fiedler (2014) argued that budget process could

negatively affect the operations of the organization if adequate research is not conducted

while preparing the master budget.

d. Comparing the data and providing relevant opinion on the changes for 2019 budget

and 2018 actual income statement:

The above table directly represents the overall budgeted income statement of the

organization for the fiscal year of 2019, which is prepared in accordance with the financial

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.