Managerial Accounting Report: Arsenal FC's Operating Expenses Analysis

VerifiedAdded on 2023/04/20

|10

|1696

|382

Report

AI Summary

This report delves into the managerial accounting practices of football clubs, using Arsenal FC as a case study. It examines the operating expenses, including staff costs, player registrations, and depreciation, and how these are impacted by the club's decision to build a new stadium. The report analyzes the financial statements of Arsenal FC, comparing data from 2016 and 2017, and projects the extended operating expenses associated with increasing stadium capacity. It explores the implications of stadium development on the cost of revenue and highlights the importance of stadiums for football clubs' commercial strategies. The report includes tables and figures illustrating the financial data and provides insights into how stadium improvements can lead to increased revenue and profit. The analysis covers various aspects of financial performance, including operating profit, and discusses the relationship between operating expenses and the cost of revenue within the context of stadium expansion.

Running head: MANAGERIAL ACCOUNTING 1

Managerial Accounting

Managerial Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

MANAGERIAL ACCOUNTING 2

Table of Contents

Operating expenses of football clubs...............................................................................................3

Importance of new stadiums............................................................................................................3

Extension of operating expenses for building new stadiums...........................................................4

Implications on cost of revenue.......................................................................................................6

References........................................................................................................................................7

Table of Contents

Operating expenses of football clubs...............................................................................................3

Importance of new stadiums............................................................................................................3

Extension of operating expenses for building new stadiums...........................................................4

Implications on cost of revenue.......................................................................................................6

References........................................................................................................................................7

MANAGERIAL ACCOUNTING 3

Operating expenses of football clubs

Operating expenses are those expenses which are not directly related to the goods and

services’ production (Hilton & Platt, 2014). These expenses usually include the general,

administrative and selling expenses in the form of separate line item. The general, administrative

and selling expenses are the ones which are not directly related to a particular product like the

costs of overhead. The operating expenditures of the football clubs include expenses such as rent,

utilities, legal costs, sports supplies, marketing and sales expenses, insurance costs, payrolls and

salaries. The Arsenal football club is a professional football club which plays in the Premier

League and is based in London, England (Arsenal, 2018a). The operating expenses of the

renowned football club Arsenal FC include amortization of goodwill, player registrations’

amortization, player registrations’ impairment, impairment and depreciation charges, staff costs,

property sales costs, etc. The total operating expenses of the club for the year 2016 was $340,050

(Arsenal, 2018b).

Importance of new stadiums

Stadiums these days have become increasingly important for football clubs and their

commercial and marketing strategies. High amount of efforts are being put towards building

bigger stadiums, in order to gather a larger audience and gather more income. The first instance

was the move of Arsenal from Highbury stadium to the Emirates Stadium in the year 2006

(Walters, 2011). The Highbury needed a rework due to the Taylor report on the disaster of

Hillsborough that took place in 1989. Highbury was known for being the most closely packed

stadium and only had a capacity of 38,000. This naturally posed issues for Arsenal and its fans,

especially when they were looking forward at challenging their rivalry, Manchester United

Operating expenses of football clubs

Operating expenses are those expenses which are not directly related to the goods and

services’ production (Hilton & Platt, 2014). These expenses usually include the general,

administrative and selling expenses in the form of separate line item. The general, administrative

and selling expenses are the ones which are not directly related to a particular product like the

costs of overhead. The operating expenditures of the football clubs include expenses such as rent,

utilities, legal costs, sports supplies, marketing and sales expenses, insurance costs, payrolls and

salaries. The Arsenal football club is a professional football club which plays in the Premier

League and is based in London, England (Arsenal, 2018a). The operating expenses of the

renowned football club Arsenal FC include amortization of goodwill, player registrations’

amortization, player registrations’ impairment, impairment and depreciation charges, staff costs,

property sales costs, etc. The total operating expenses of the club for the year 2016 was $340,050

(Arsenal, 2018b).

Importance of new stadiums

Stadiums these days have become increasingly important for football clubs and their

commercial and marketing strategies. High amount of efforts are being put towards building

bigger stadiums, in order to gather a larger audience and gather more income. The first instance

was the move of Arsenal from Highbury stadium to the Emirates Stadium in the year 2006

(Walters, 2011). The Highbury needed a rework due to the Taylor report on the disaster of

Hillsborough that took place in 1989. Highbury was known for being the most closely packed

stadium and only had a capacity of 38,000. This naturally posed issues for Arsenal and its fans,

especially when they were looking forward at challenging their rivalry, Manchester United

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

MANAGERIAL ACCOUNTING 4

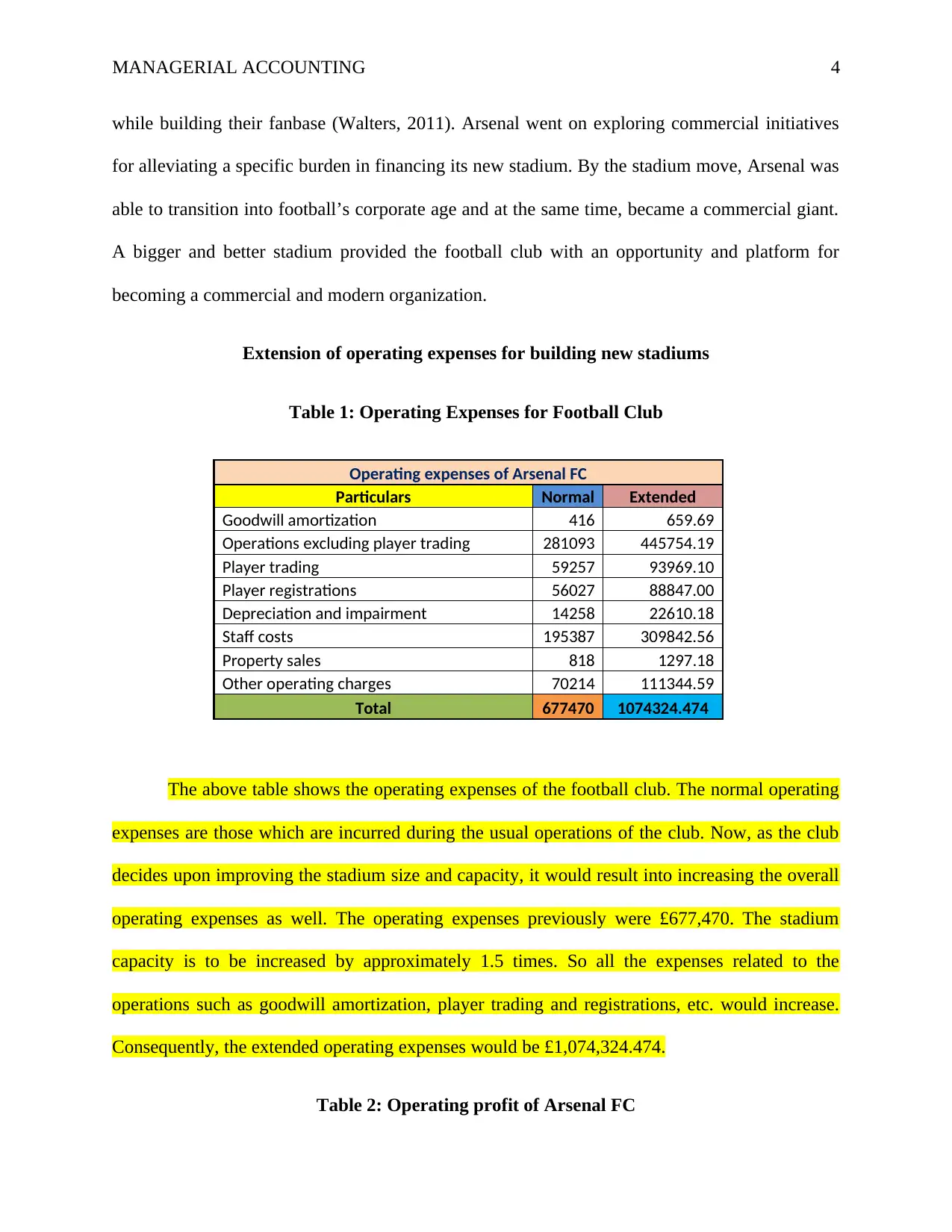

while building their fanbase (Walters, 2011). Arsenal went on exploring commercial initiatives

for alleviating a specific burden in financing its new stadium. By the stadium move, Arsenal was

able to transition into football’s corporate age and at the same time, became a commercial giant.

A bigger and better stadium provided the football club with an opportunity and platform for

becoming a commercial and modern organization.

Extension of operating expenses for building new stadiums

Table 1: Operating Expenses for Football Club

Operating expenses of Arsenal FC

Particulars Normal Extended

Goodwill amortization 416 659.69

Operations excluding player trading 281093 445754.19

Player trading 59257 93969.10

Player registrations 56027 88847.00

Depreciation and impairment 14258 22610.18

Staff costs 195387 309842.56

Property sales 818 1297.18

Other operating charges 70214 111344.59

Total 677470 1074324.474

The above table shows the operating expenses of the football club. The normal operating

expenses are those which are incurred during the usual operations of the club. Now, as the club

decides upon improving the stadium size and capacity, it would result into increasing the overall

operating expenses as well. The operating expenses previously were £677,470. The stadium

capacity is to be increased by approximately 1.5 times. So all the expenses related to the

operations such as goodwill amortization, player trading and registrations, etc. would increase.

Consequently, the extended operating expenses would be £1,074,324.474.

Table 2: Operating profit of Arsenal FC

while building their fanbase (Walters, 2011). Arsenal went on exploring commercial initiatives

for alleviating a specific burden in financing its new stadium. By the stadium move, Arsenal was

able to transition into football’s corporate age and at the same time, became a commercial giant.

A bigger and better stadium provided the football club with an opportunity and platform for

becoming a commercial and modern organization.

Extension of operating expenses for building new stadiums

Table 1: Operating Expenses for Football Club

Operating expenses of Arsenal FC

Particulars Normal Extended

Goodwill amortization 416 659.69

Operations excluding player trading 281093 445754.19

Player trading 59257 93969.10

Player registrations 56027 88847.00

Depreciation and impairment 14258 22610.18

Staff costs 195387 309842.56

Property sales 818 1297.18

Other operating charges 70214 111344.59

Total 677470 1074324.474

The above table shows the operating expenses of the football club. The normal operating

expenses are those which are incurred during the usual operations of the club. Now, as the club

decides upon improving the stadium size and capacity, it would result into increasing the overall

operating expenses as well. The operating expenses previously were £677,470. The stadium

capacity is to be increased by approximately 1.5 times. So all the expenses related to the

operations such as goodwill amortization, player trading and registrations, etc. would increase.

Consequently, the extended operating expenses would be £1,074,324.474.

Table 2: Operating profit of Arsenal FC

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

MANAGERIAL ACCOUNTING 5

2017 2016

Operations

excluding

player

trading

£’000

Player

trading

£’000

Total

£’000

Operations

excluding

player

trading

£’000

Player

trading

£’000

Total

£’000

Operating

profit/(loss)

122,180 (70,194) 51,986 69,216 (56,027) 13,189

The above table shows the operating profit of Arsenal FC for the two financial years,

2016 and 2017. The operating profit is earned out of operations related to as well as excluding

the player trading. In 2016, the operations excluding player trading earned the firm an operating

profit of £69,216. However, an operating loss of £56,027 was incurred by player trading for the

same year. The total operating profit earned was £13,189. In the year 2017, the operations

excluding player trading earned the firm an operating profit of £122,180 which was way higher

than that of the previous year. However, again an operating loss of £70,194 was incurred by

player trading for the same year. The total operating profit earned stood to be £51,986.

Table 3: Operating Expenses of Arsenal FC

Operating expenses

comprise:

2017

£’000

2016

£’000

Amortization of goodwill 416 416

2017 2016

Operations

excluding

player

trading

£’000

Player

trading

£’000

Total

£’000

Operations

excluding

player

trading

£’000

Player

trading

£’000

Total

£’000

Operating

profit/(loss)

122,180 (70,194) 51,986 69,216 (56,027) 13,189

The above table shows the operating profit of Arsenal FC for the two financial years,

2016 and 2017. The operating profit is earned out of operations related to as well as excluding

the player trading. In 2016, the operations excluding player trading earned the firm an operating

profit of £69,216. However, an operating loss of £56,027 was incurred by player trading for the

same year. The total operating profit earned was £13,189. In the year 2017, the operations

excluding player trading earned the firm an operating profit of £122,180 which was way higher

than that of the previous year. However, again an operating loss of £70,194 was incurred by

player trading for the same year. The total operating profit earned stood to be £51,986.

Table 3: Operating Expenses of Arsenal FC

Operating expenses

comprise:

2017

£’000

2016

£’000

Amortization of goodwill 416 416

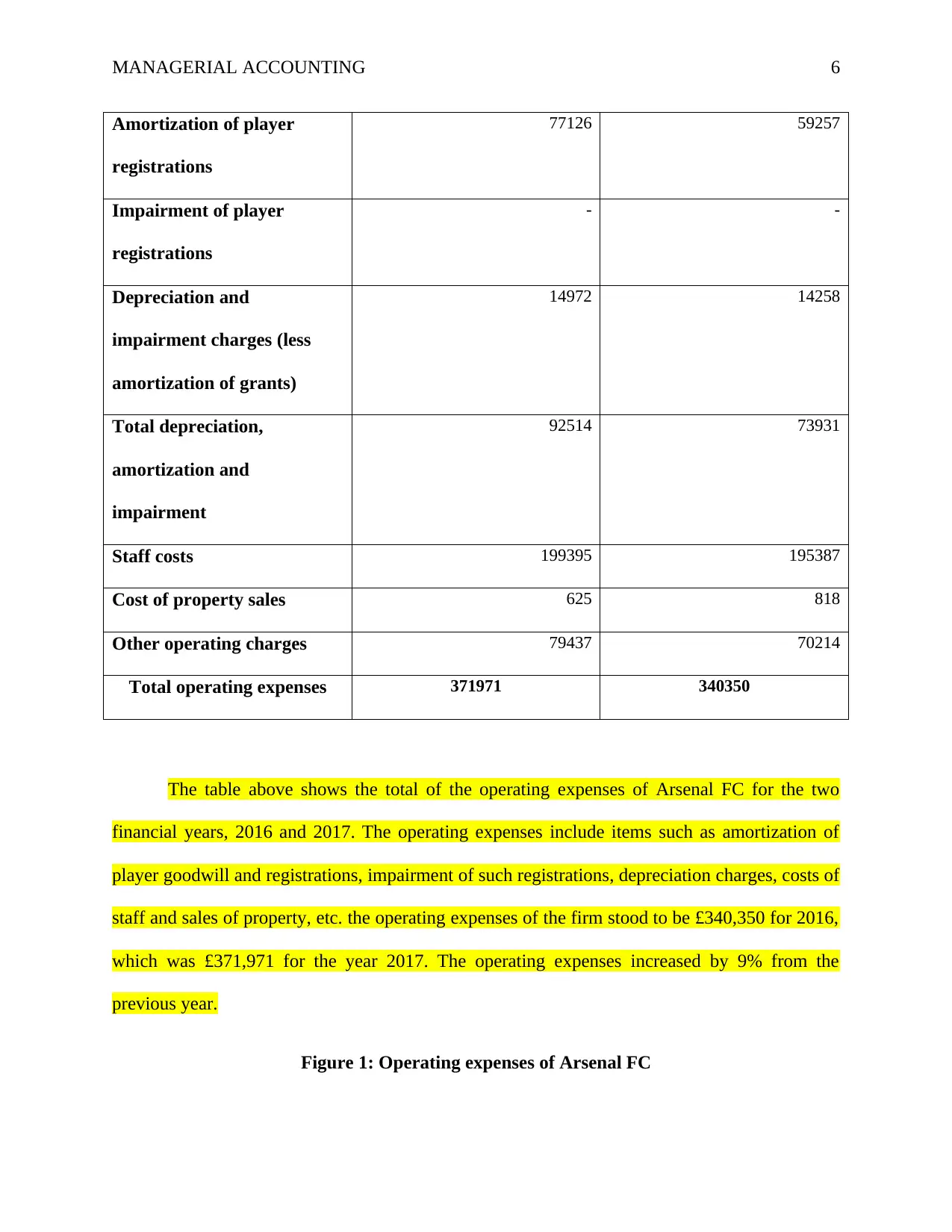

MANAGERIAL ACCOUNTING 6

Amortization of player

registrations

77126 59257

Impairment of player

registrations

- -

Depreciation and

impairment charges (less

amortization of grants)

14972 14258

Total depreciation,

amortization and

impairment

92514 73931

Staff costs 199395 195387

Cost of property sales 625 818

Other operating charges 79437 70214

Total operating expenses 371971 340350

The table above shows the total of the operating expenses of Arsenal FC for the two

financial years, 2016 and 2017. The operating expenses include items such as amortization of

player goodwill and registrations, impairment of such registrations, depreciation charges, costs of

staff and sales of property, etc. the operating expenses of the firm stood to be £340,350 for 2016,

which was £371,971 for the year 2017. The operating expenses increased by 9% from the

previous year.

Figure 1: Operating expenses of Arsenal FC

Amortization of player

registrations

77126 59257

Impairment of player

registrations

- -

Depreciation and

impairment charges (less

amortization of grants)

14972 14258

Total depreciation,

amortization and

impairment

92514 73931

Staff costs 199395 195387

Cost of property sales 625 818

Other operating charges 79437 70214

Total operating expenses 371971 340350

The table above shows the total of the operating expenses of Arsenal FC for the two

financial years, 2016 and 2017. The operating expenses include items such as amortization of

player goodwill and registrations, impairment of such registrations, depreciation charges, costs of

staff and sales of property, etc. the operating expenses of the firm stood to be £340,350 for 2016,

which was £371,971 for the year 2017. The operating expenses increased by 9% from the

previous year.

Figure 1: Operating expenses of Arsenal FC

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

MANAGERIAL ACCOUNTING 7

0

100000

200000

300000

400000

2017

2016

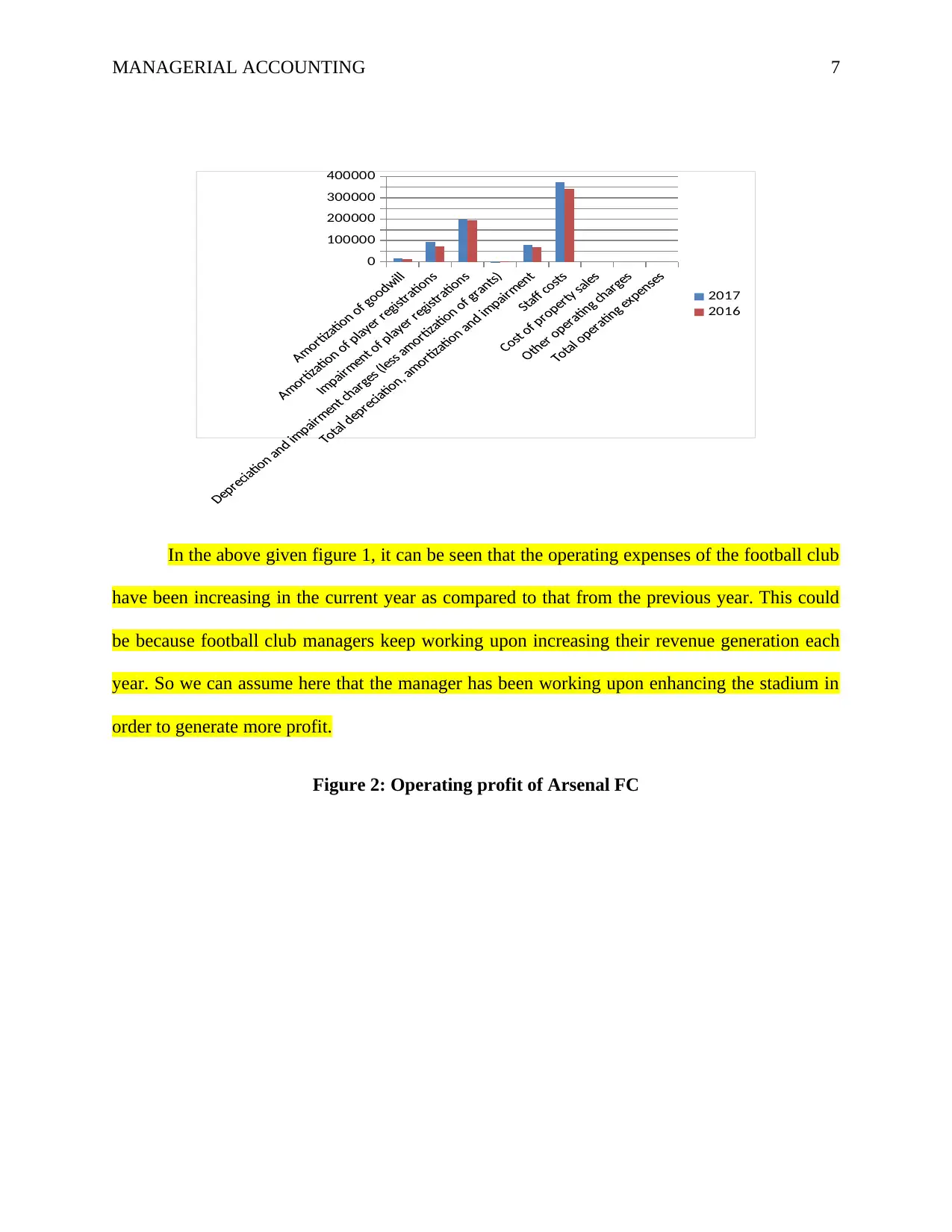

In the above given figure 1, it can be seen that the operating expenses of the football club

have been increasing in the current year as compared to that from the previous year. This could

be because football club managers keep working upon increasing their revenue generation each

year. So we can assume here that the manager has been working upon enhancing the stadium in

order to generate more profit.

Figure 2: Operating profit of Arsenal FC

0

100000

200000

300000

400000

2017

2016

In the above given figure 1, it can be seen that the operating expenses of the football club

have been increasing in the current year as compared to that from the previous year. This could

be because football club managers keep working upon increasing their revenue generation each

year. So we can assume here that the manager has been working upon enhancing the stadium in

order to generate more profit.

Figure 2: Operating profit of Arsenal FC

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

MANAGERIAL ACCOUNTING 8

Operations

excluding

player

trading

Player

trading Total Operations

excluding

player

trading

Player

trading Total

2017 2016

-100,000

-50,000

0

50,000

100,000

150,000

Operating Profit

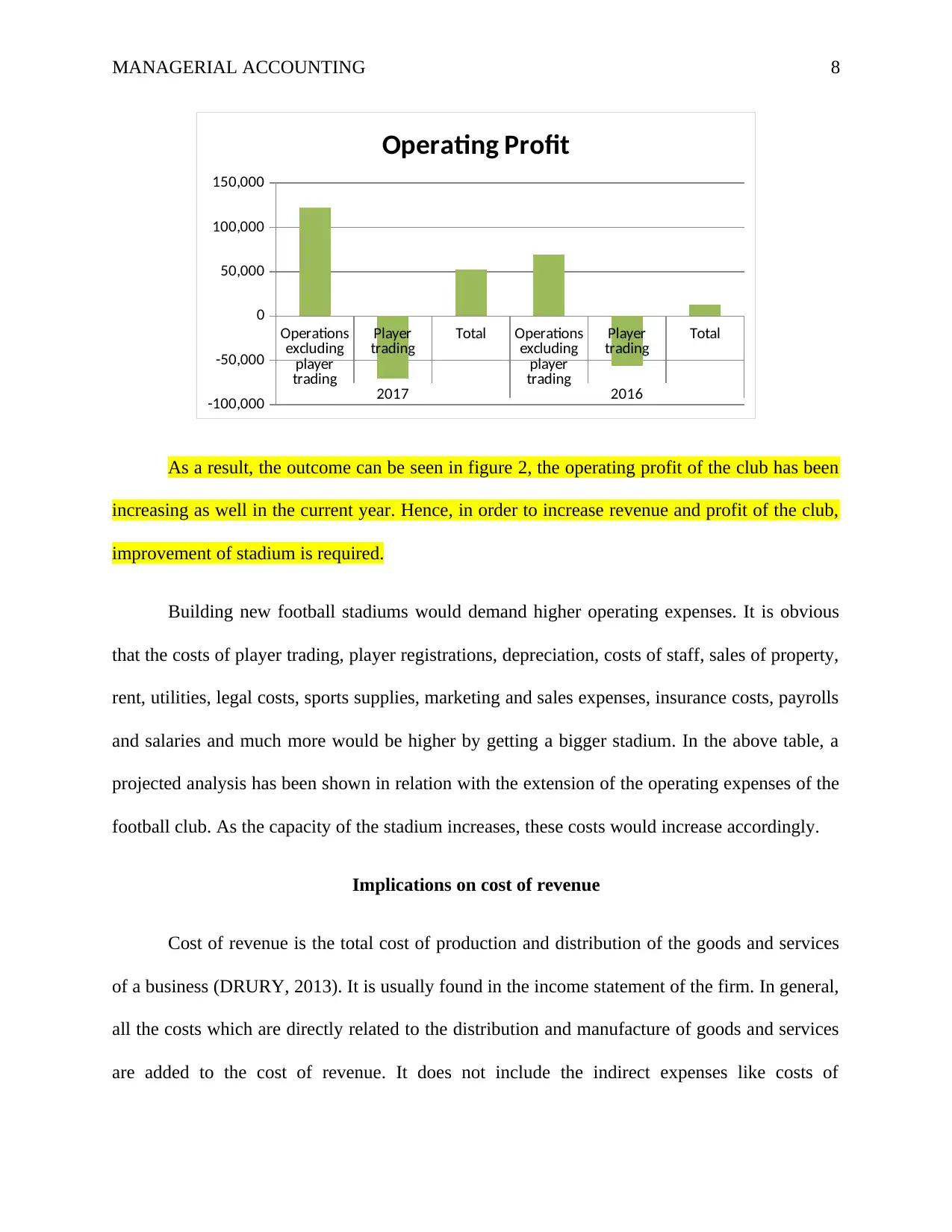

As a result, the outcome can be seen in figure 2, the operating profit of the club has been

increasing as well in the current year. Hence, in order to increase revenue and profit of the club,

improvement of stadium is required.

Building new football stadiums would demand higher operating expenses. It is obvious

that the costs of player trading, player registrations, depreciation, costs of staff, sales of property,

rent, utilities, legal costs, sports supplies, marketing and sales expenses, insurance costs, payrolls

and salaries and much more would be higher by getting a bigger stadium. In the above table, a

projected analysis has been shown in relation with the extension of the operating expenses of the

football club. As the capacity of the stadium increases, these costs would increase accordingly.

Implications on cost of revenue

Cost of revenue is the total cost of production and distribution of the goods and services

of a business (DRURY, 2013). It is usually found in the income statement of the firm. In general,

all the costs which are directly related to the distribution and manufacture of goods and services

are added to the cost of revenue. It does not include the indirect expenses like costs of

Operations

excluding

player

trading

Player

trading Total Operations

excluding

player

trading

Player

trading Total

2017 2016

-100,000

-50,000

0

50,000

100,000

150,000

Operating Profit

As a result, the outcome can be seen in figure 2, the operating profit of the club has been

increasing as well in the current year. Hence, in order to increase revenue and profit of the club,

improvement of stadium is required.

Building new football stadiums would demand higher operating expenses. It is obvious

that the costs of player trading, player registrations, depreciation, costs of staff, sales of property,

rent, utilities, legal costs, sports supplies, marketing and sales expenses, insurance costs, payrolls

and salaries and much more would be higher by getting a bigger stadium. In the above table, a

projected analysis has been shown in relation with the extension of the operating expenses of the

football club. As the capacity of the stadium increases, these costs would increase accordingly.

Implications on cost of revenue

Cost of revenue is the total cost of production and distribution of the goods and services

of a business (DRURY, 2013). It is usually found in the income statement of the firm. In general,

all the costs which are directly related to the distribution and manufacture of goods and services

are added to the cost of revenue. It does not include the indirect expenses like costs of

MANAGERIAL ACCOUNTING 9

distribution and sales force. If the operating expenses of the football club are extended for

building a bigger stadium, the cost of revenue of club would increase as well. Building a new

stadium would directly impact and increase the cost of revenue; however, the operating expenses

of the club might not change necessarily since they are not directly related to the goods and

services’ production of a firm. However, in this case, since the club is already planning to extend

its operating expenses, both the cost of revenue as well the operating expenditure would increase.

A better stadium with enhanced capacity and facilities would provide the club with a

platform and opportunity for becoming a commercial and modern entity. Operating expenses

represent the indirect costs of the football club, which are not directly related to its production of

goods and services. The cost of revenue of the club represents the costs which are directly related

to its production of goods and services. In this case, both these costs would be increasing for

building a new stadium.

distribution and sales force. If the operating expenses of the football club are extended for

building a bigger stadium, the cost of revenue of club would increase as well. Building a new

stadium would directly impact and increase the cost of revenue; however, the operating expenses

of the club might not change necessarily since they are not directly related to the goods and

services’ production of a firm. However, in this case, since the club is already planning to extend

its operating expenses, both the cost of revenue as well the operating expenditure would increase.

A better stadium with enhanced capacity and facilities would provide the club with a

platform and opportunity for becoming a commercial and modern entity. Operating expenses

represent the indirect costs of the football club, which are not directly related to its production of

goods and services. The cost of revenue of the club represents the costs which are directly related

to its production of goods and services. In this case, both these costs would be increasing for

building a new stadium.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

MANAGERIAL ACCOUNTING 10

References

Arsenal, (2018a). History. Retrieved from: https://www.arsenal.com/history

Arsenal, (2018b). The Club. Financial Results. Retrieved from: https://www.arsenal.com/the-

club/corporate-info/arsenal-holdings-financial-results

DRURY, C. M. (2013). Management and cost accounting. New York, USA: Springer.

Hilton, R. W. & Platt D. E. (2014). Managerial accounting: creating value in a dynamic business

environment. Tenth edition. New York, USA: McGraw-Hill.

Manson, D. (2012). Quotations from the Public Comments of Arsene Wenger: Manager, Arsenal

Football Club.

Walters, G. (2011). The implementation of a stakeholder management strategy during stadium

development: a case study of Arsenal Football Club and the Emirates Stadium. Managing

Leisure, 16(1), 49-64.

References

Arsenal, (2018a). History. Retrieved from: https://www.arsenal.com/history

Arsenal, (2018b). The Club. Financial Results. Retrieved from: https://www.arsenal.com/the-

club/corporate-info/arsenal-holdings-financial-results

DRURY, C. M. (2013). Management and cost accounting. New York, USA: Springer.

Hilton, R. W. & Platt D. E. (2014). Managerial accounting: creating value in a dynamic business

environment. Tenth edition. New York, USA: McGraw-Hill.

Manson, D. (2012). Quotations from the Public Comments of Arsene Wenger: Manager, Arsenal

Football Club.

Walters, G. (2011). The implementation of a stakeholder management strategy during stadium

development: a case study of Arsenal Football Club and the Emirates Stadium. Managing

Leisure, 16(1), 49-64.

1 out of 10

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.