Executive Remuneration Comparison: Managerial Accounting Report

VerifiedAdded on 2023/06/06

|10

|939

|288

Report

AI Summary

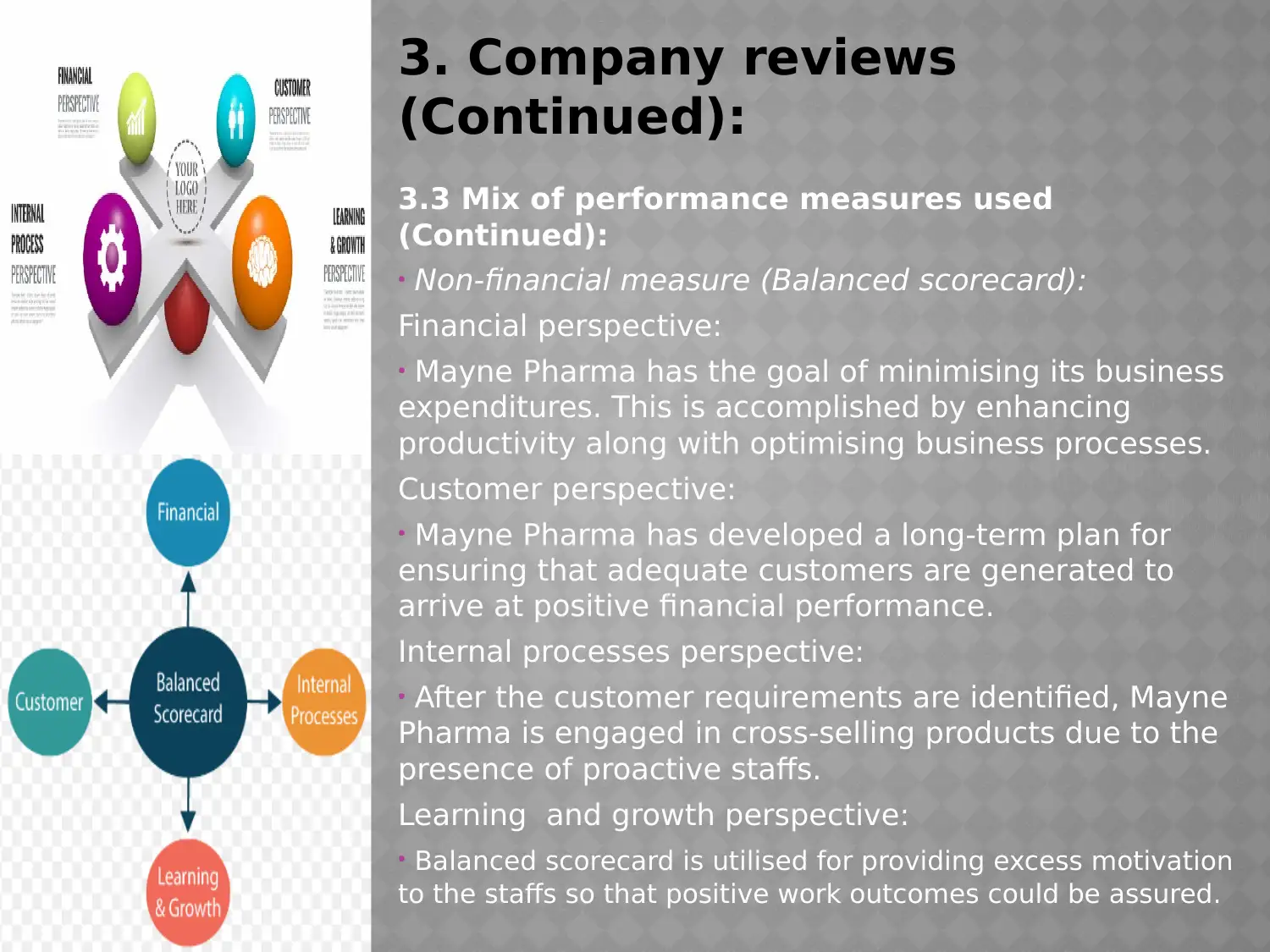

This report provides a comparative analysis of executive remuneration practices in Mayne Pharma and CSL Limited, focusing on the details of their remuneration committees, allocation of executive remuneration, and the mix of performance measures used. The report reviews the financial and non-financial performance measures, including earnings per share, return on investment, and return on capital invested, alongside a balanced scorecard approach to assess customer perspective, internal processes, and learning and growth. The study finds that both companies conduct timely meetings considering internal and external conditions, with Mayne Pharma focusing on minimizing business expenditures through enhanced productivity. The conclusion highlights that while both companies have remuneration committees, Mayne Pharma demonstrates a competitive advantage in the share market, correlating with increased executive remuneration. Desklib provides access to similar solved assignments and study materials for students.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.