Managerial Accounting Assignment: Cost Analysis, Budgeting, and ROI

VerifiedAdded on 2022/11/24

|11

|1878

|198

Homework Assignment

AI Summary

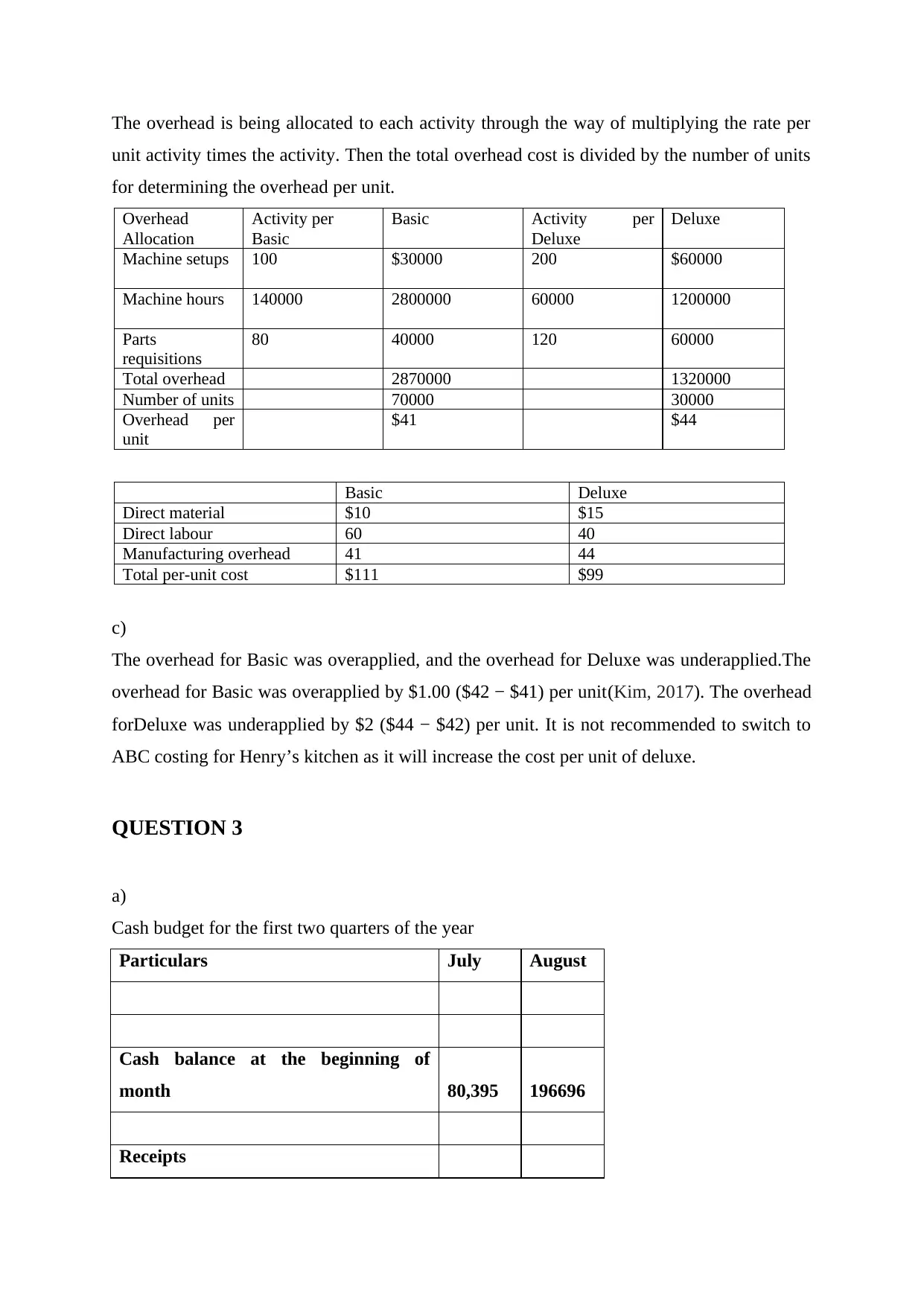

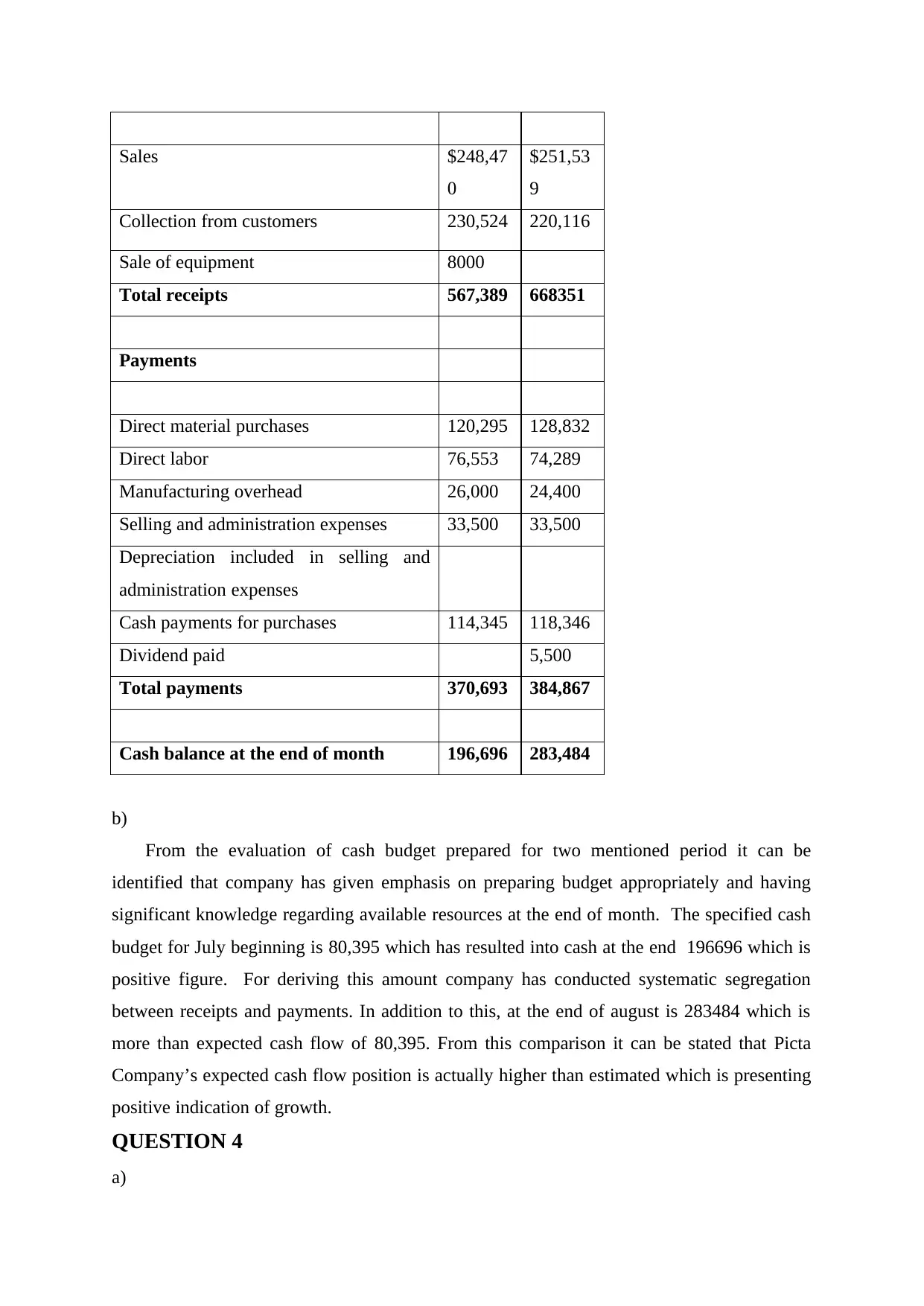

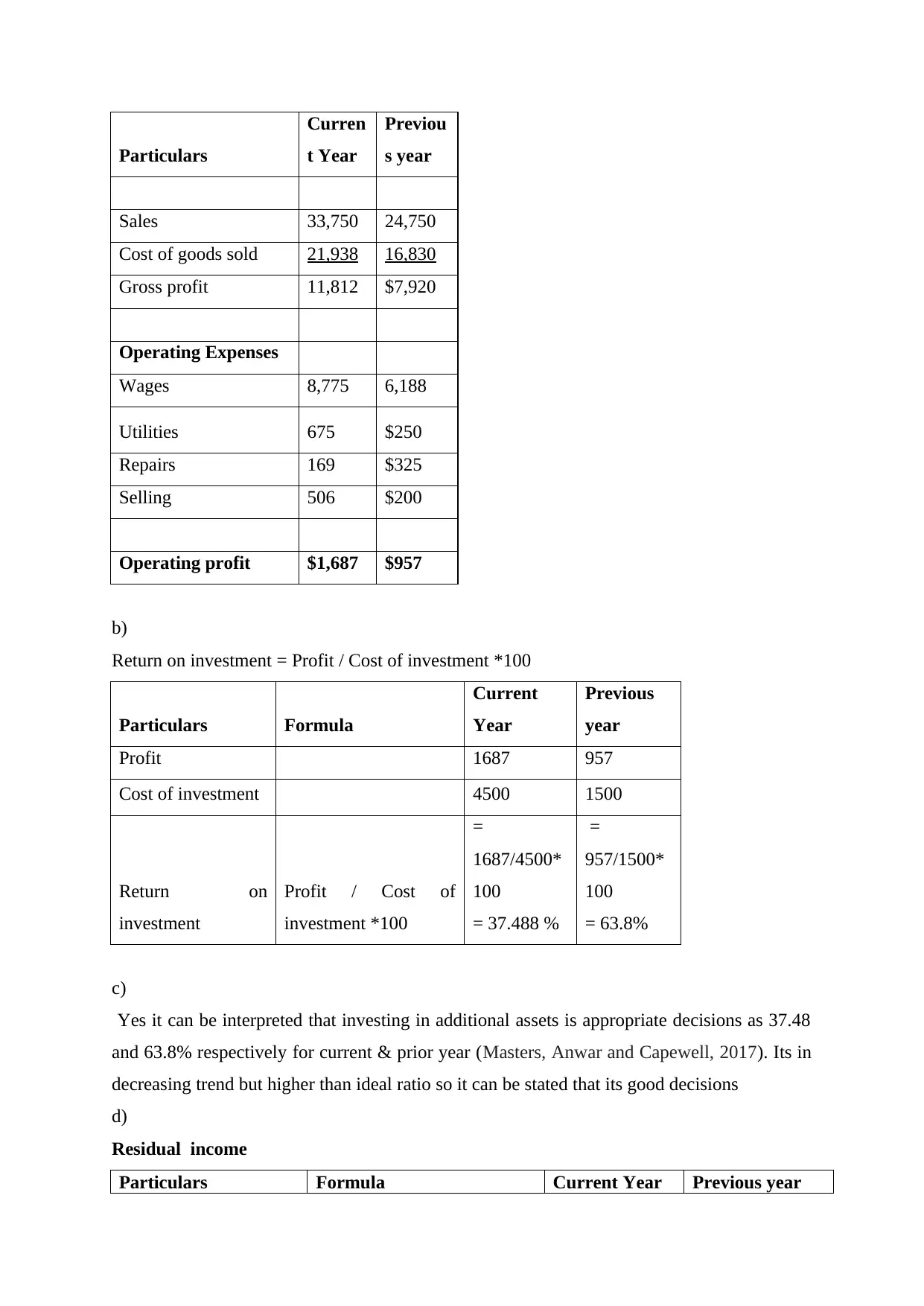

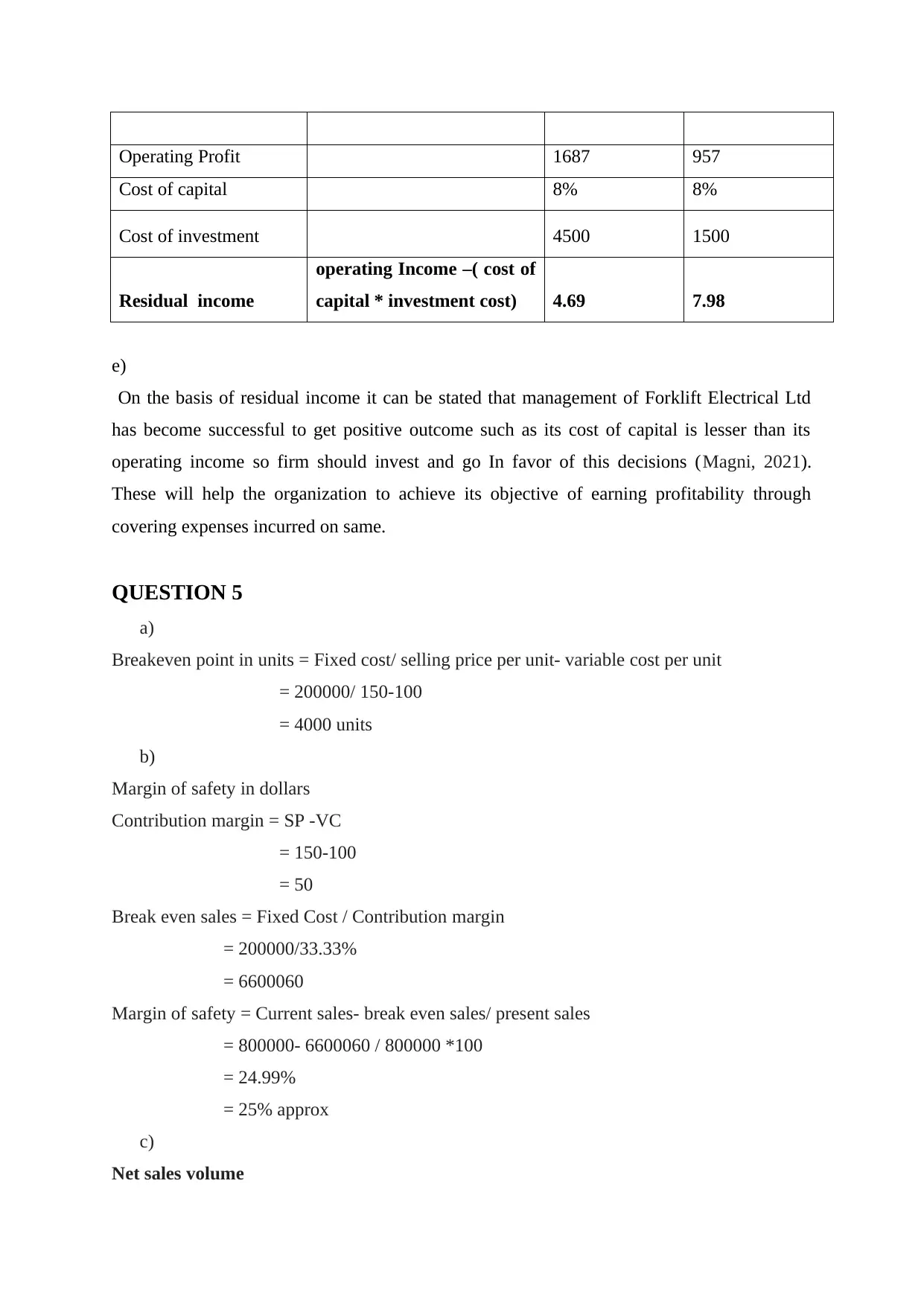

This managerial accounting assignment solution addresses several key concepts, including variable and fixed costs, cost analysis using the high-low method, activity-based costing (ABC), cash budgeting, return on investment (ROI), and residual income calculations. The solution provides detailed calculations and explanations for each question, covering topics such as break-even analysis, margin of safety, and contribution margin income statements. Furthermore, the assignment explores special order decisions and the relevant costs to consider. The document offers a comprehensive analysis of various managerial accounting principles and their application in different scenarios, providing a valuable resource for students studying finance.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.