Managerial Accounting: Performance Evaluation and Financial Planning

VerifiedAdded on 2023/06/09

|8

|699

|91

Homework Assignment

AI Summary

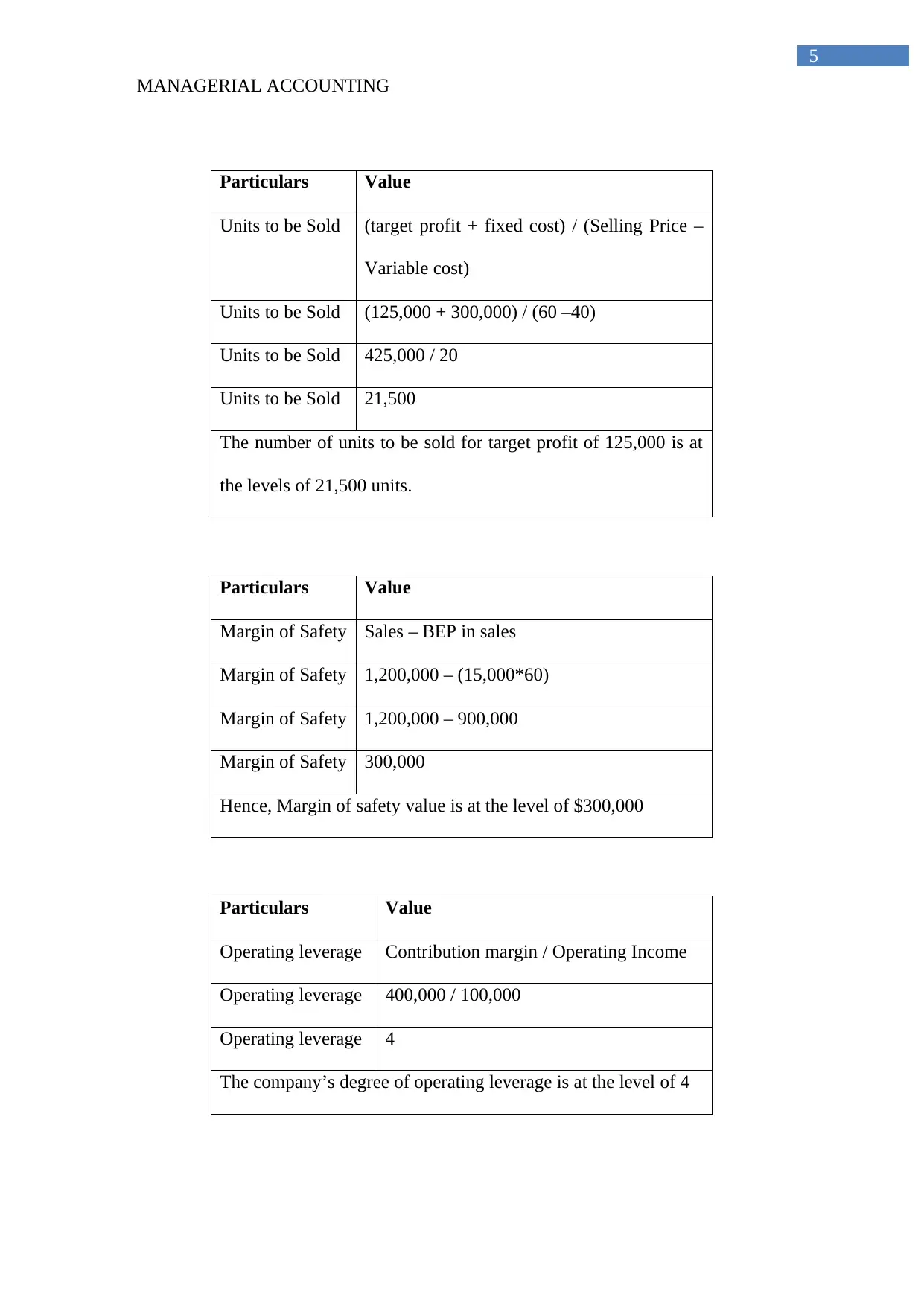

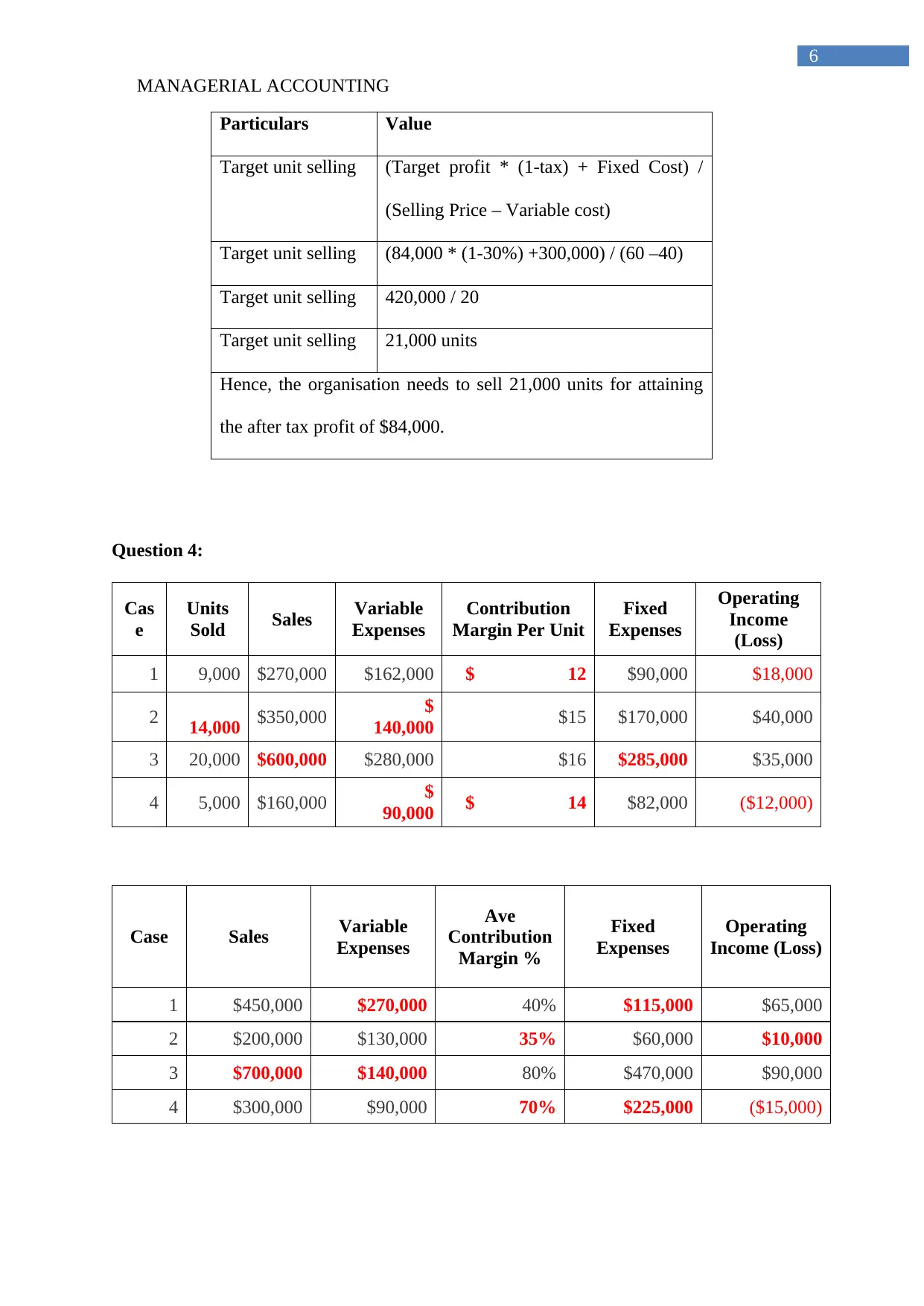

This assignment provides solutions to managerial accounting problems. It includes the preparation of an income statement using the contribution approach, cost behavior analysis using the high-low method to determine variable and fixed costs, and cost-volume-profit (CVP) analysis covering contribution margin ratio, break-even point, impact of unit increment on operating income, units to be sold for a target profit, margin of safety, operating leverage, and target unit sales for after-tax profit. The assignment also includes case studies, analyzing units sold, sales, variable expenses, contribution margin, fixed expenses, and operating income (loss) to compute average contribution margin percentage and assess profitability.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.