Managerial Accounting: Cost, Trends, and Financial Statements

VerifiedAdded on 2021/08/03

|43

|2540

|237

Presentation

AI Summary

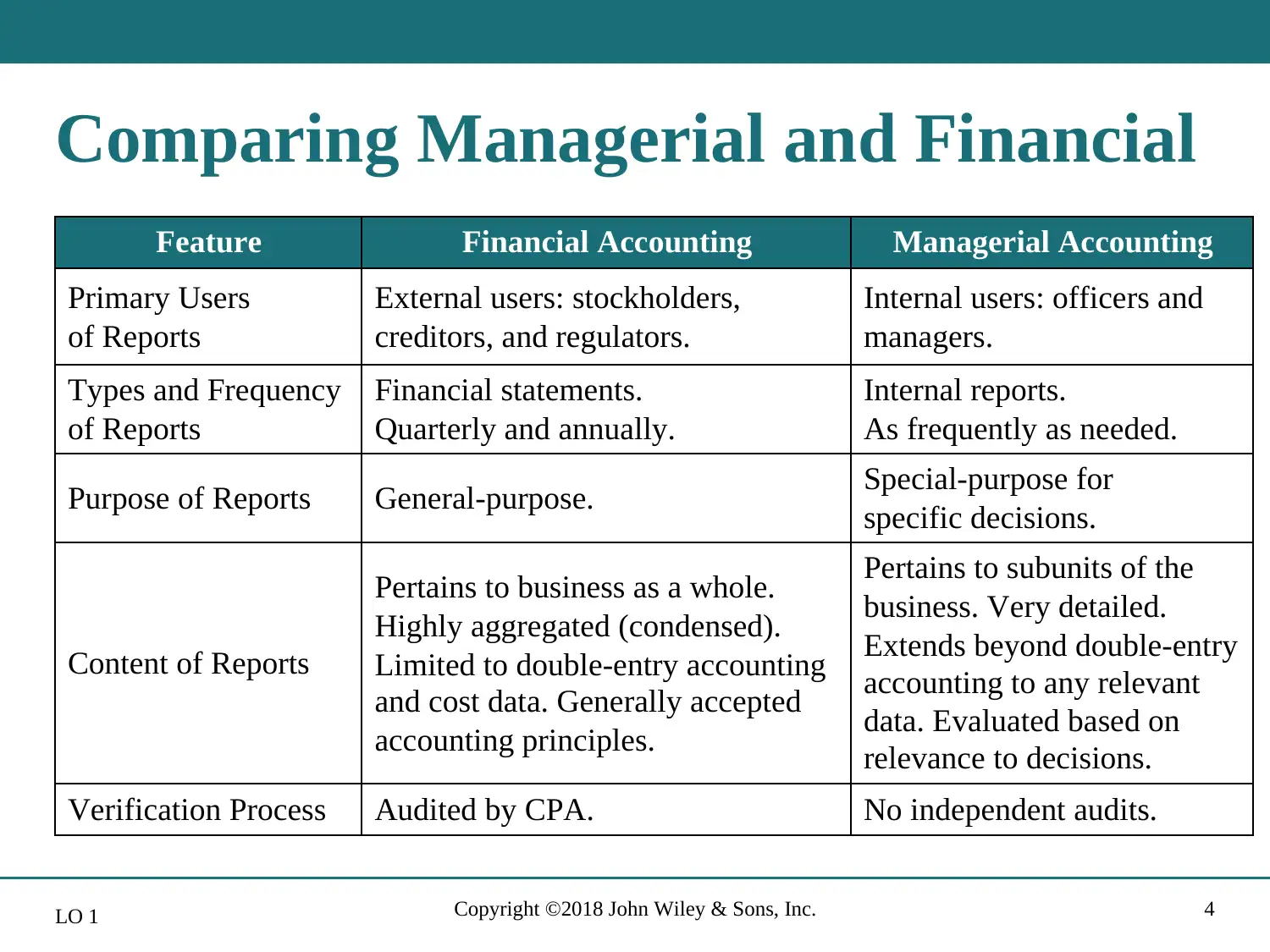

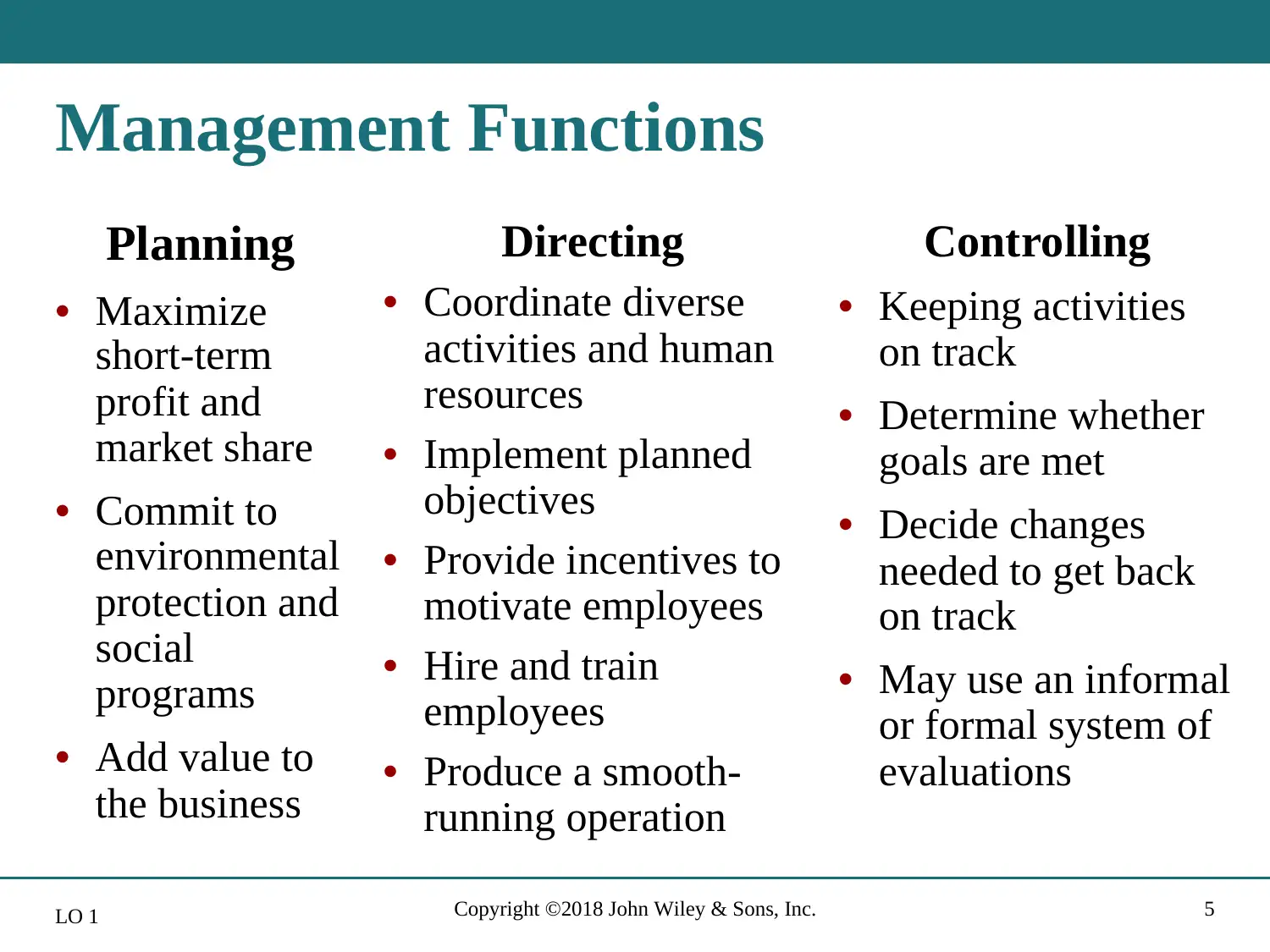

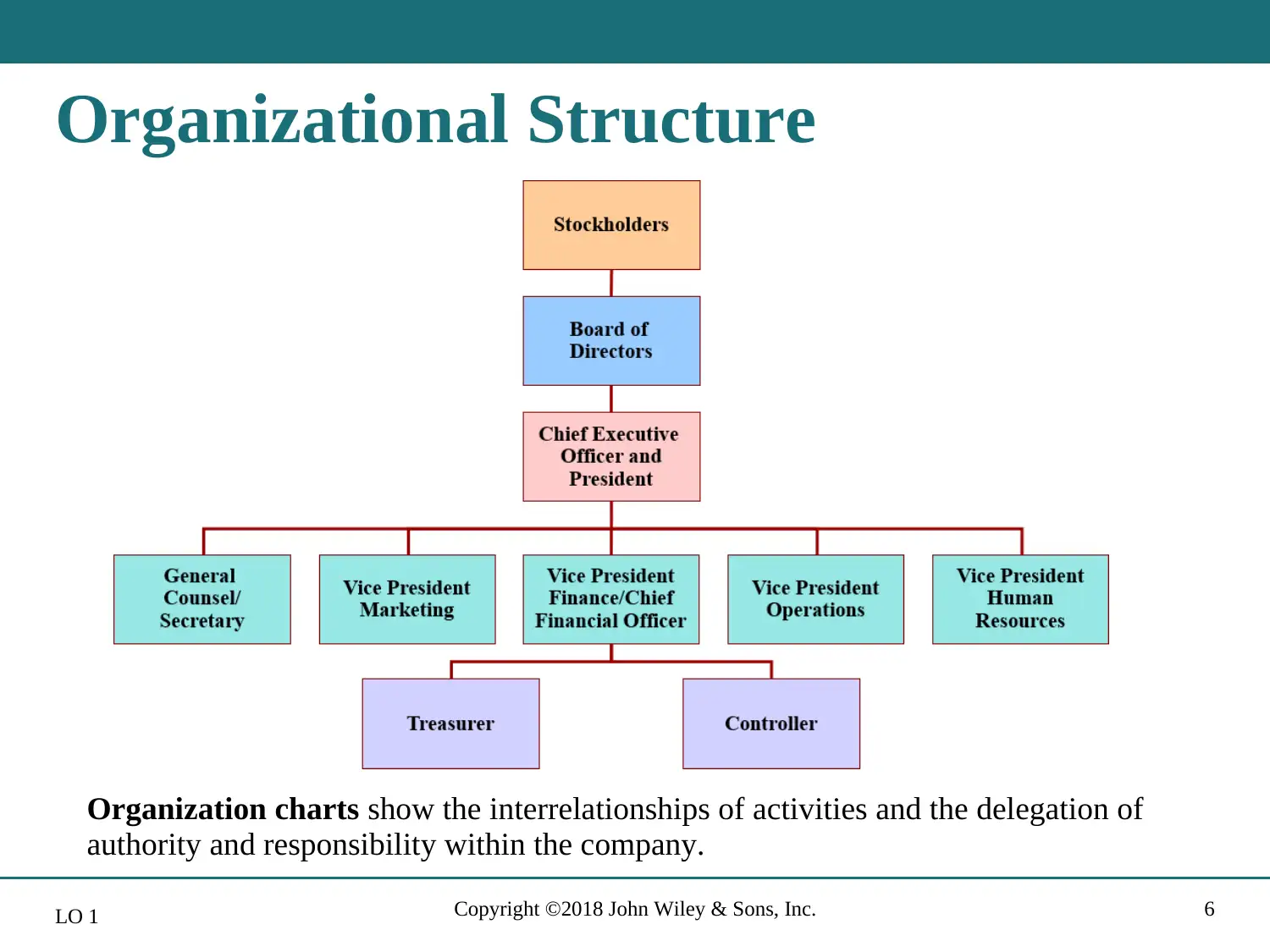

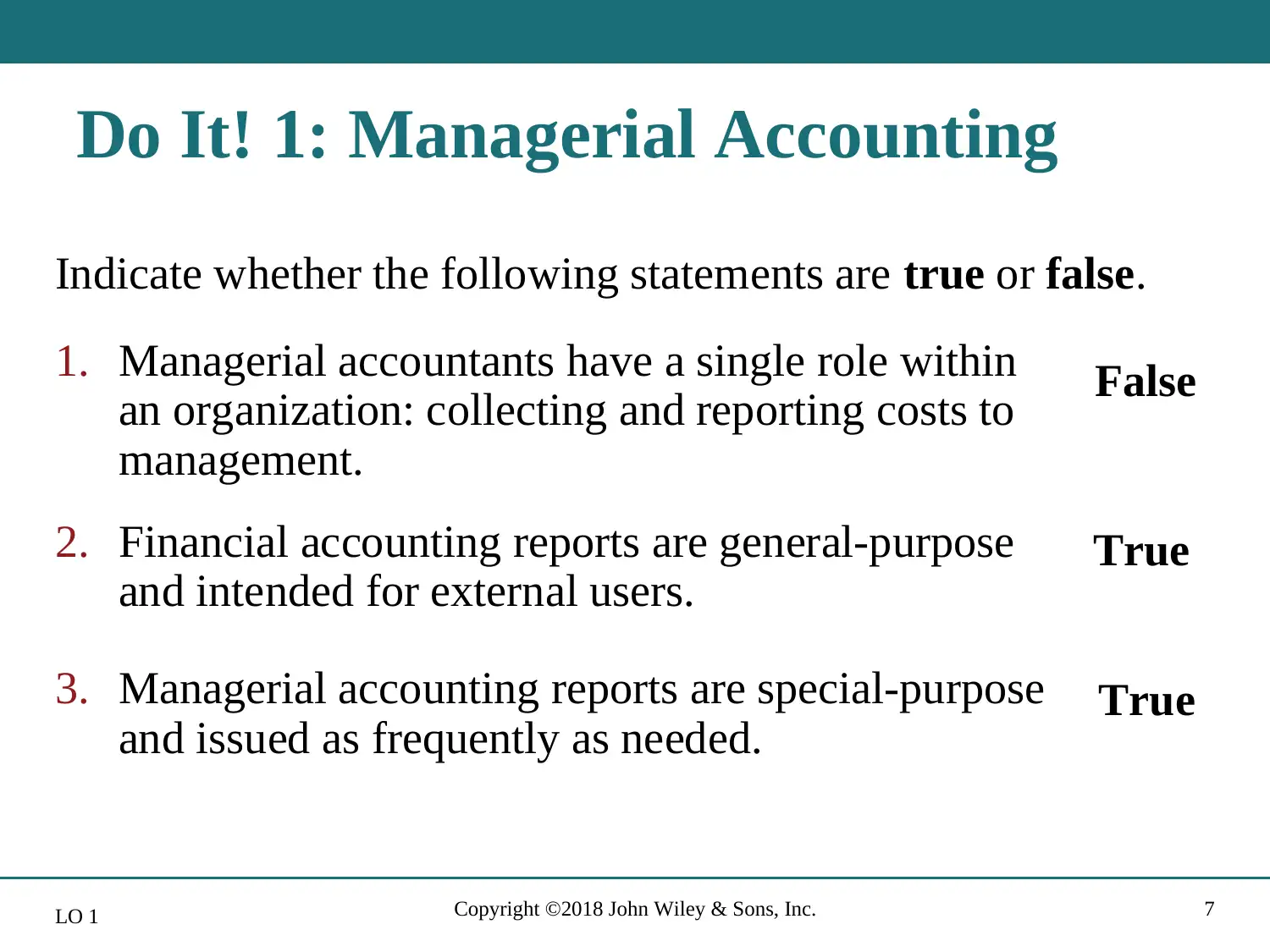

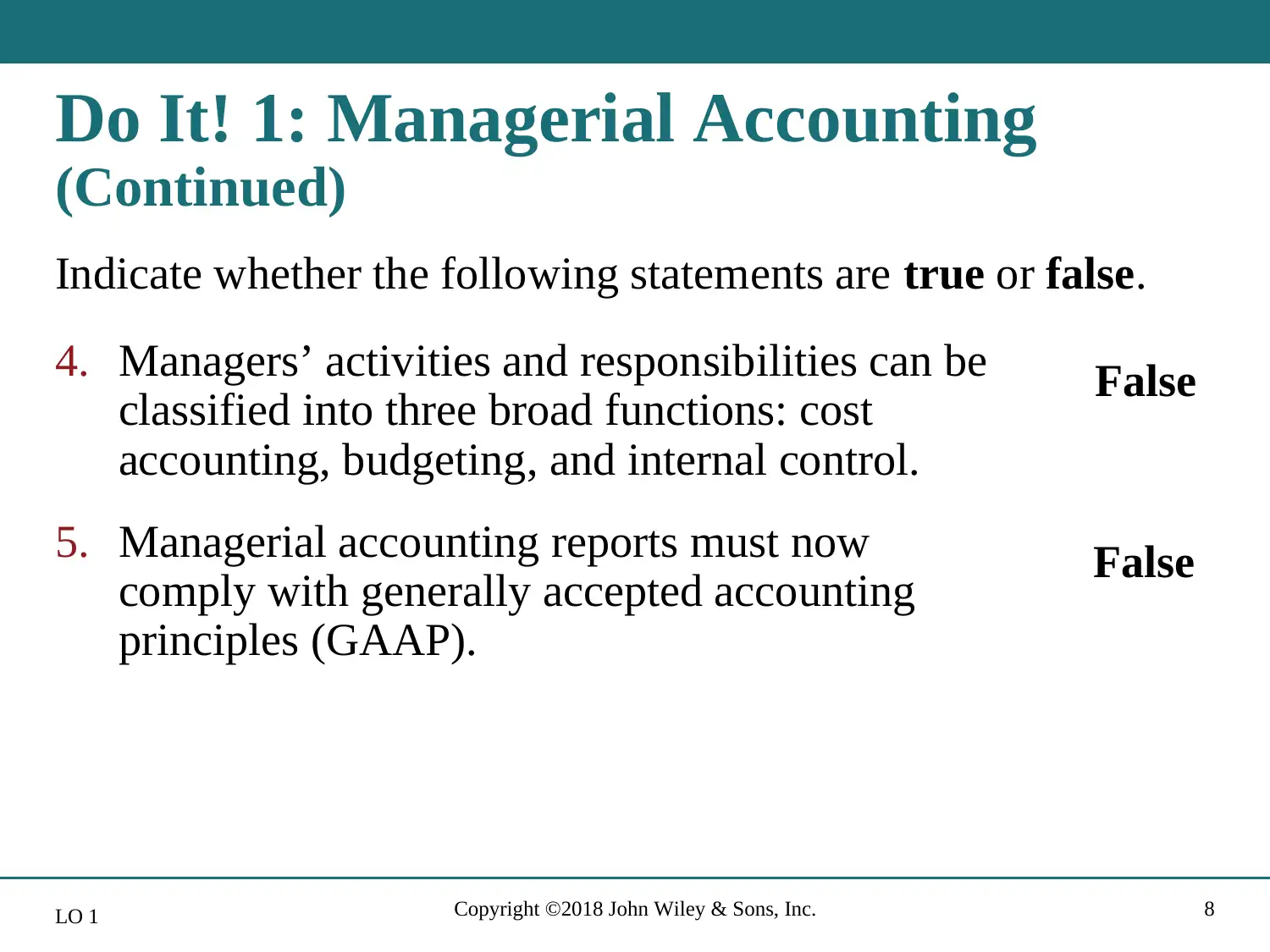

This presentation provides a comprehensive overview of managerial accounting, beginning with its fundamental features and contrasting it with financial accounting. It details the functions of management, including planning, directing, and controlling, and illustrates the organizational structure within a company. The presentation then delves into key cost concepts, such as direct materials, direct labor, and manufacturing overhead, distinguishing between product and period costs. It demonstrates how to compute the cost of goods manufactured and prepare essential financial statements for manufacturers, including the income statement, cost of goods sold section, and balance sheet. Furthermore, it explores current trends in managerial accounting, like the value chain, just-in-time inventory, total quality management, activity-based costing, and the balanced scorecard, along with discussions on business ethics and corporate social responsibility. This presentation offers valuable insights into managerial accounting principles and practices.

1 out of 43

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.