Managerial Accounting Report: Trion Corporation Analysis

VerifiedAdded on 2023/04/23

|18

|4742

|54

Report

AI Summary

This managerial accounting report analyzes the financial performance of the Trion Corporation, a manufacturing company with six operating divisions. The analysis focuses on divisional profitability, market share, and the application of ratio analysis to assess financial leverage, liquidity, and return on assets and equity. The report evaluates the performance of the bathroom accessories and pipes divisions, highlighting their profitability and financial viability. It considers factors affecting capital budgeting decisions, such as initial investment and cash flows, and discusses the decentralization of head office staff for operational efficiency. The study assesses the company's financial position through ratio analysis, including operating profit margin, return on total assets, and return on equity. Strategic decisions, such as improving operational efficiency and market share, are recommended, especially for underperforming divisions. The report concludes with recommendations for improved financial performance and sustainable profitability, considering the impact of competition and operational costs.

Running head: MANAGERIAL ACCOUNTING

Managerial Accounting

Name of the Student:

Name of the University:

Author’s Note:

Managerial Accounting

Name of the Student:

Name of the University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1MANAGERIAL ACCOUNTING

Executive Summary

The assignment aims at analysing the Trion Corporation and the various

operational divisions of the company. The analysis of the company for the

various operational division was done by taking the revenue generated

and the profitability from each of the division for assessing the financial

viability of the divisions. The application of ratio analysis was done for the

analysis of the company where the financial leverage or the leverage of

the company were assessed. The importance and the relevance of the

ratio analysis for evaluating the financial performance of the company

was taken into consideration for the company. Both the bathroom

accessories divisions and the pipes division will be analysed based on the

profitability and financial viability of the divisions. There are various

factors that affects the capital budgeting decisions of the company like

the initial cost or investment into the project and the cash expected cash

flows from the project. Decentralisation of the head office staff for bring

operational efficiency in the daily workings of the company was also taken

into consideration. The importance and the exposure of the financial

leverage of the company was taken into account for the purpose of

discussion of the financial performance of the company.

Executive Summary

The assignment aims at analysing the Trion Corporation and the various

operational divisions of the company. The analysis of the company for the

various operational division was done by taking the revenue generated

and the profitability from each of the division for assessing the financial

viability of the divisions. The application of ratio analysis was done for the

analysis of the company where the financial leverage or the leverage of

the company were assessed. The importance and the relevance of the

ratio analysis for evaluating the financial performance of the company

was taken into consideration for the company. Both the bathroom

accessories divisions and the pipes division will be analysed based on the

profitability and financial viability of the divisions. There are various

factors that affects the capital budgeting decisions of the company like

the initial cost or investment into the project and the cash expected cash

flows from the project. Decentralisation of the head office staff for bring

operational efficiency in the daily workings of the company was also taken

into consideration. The importance and the exposure of the financial

leverage of the company was taken into account for the purpose of

discussion of the financial performance of the company.

2MANAGERIAL ACCOUNTING

Table of Contents

Introduction.................................................................................................3

Discussion...................................................................................................3

a) Evaluation of Various Divisions............................................................3

b) Strategic Decisions..............................................................................6

c) Financial Gearing.................................................................................7

d) Decentralize Program..........................................................................9

Conclusion.................................................................................................10

References................................................................................................12

Appendix...................................................................................................14

Table of Contents

Introduction.................................................................................................3

Discussion...................................................................................................3

a) Evaluation of Various Divisions............................................................3

b) Strategic Decisions..............................................................................6

c) Financial Gearing.................................................................................7

d) Decentralize Program..........................................................................9

Conclusion.................................................................................................10

References................................................................................................12

Appendix...................................................................................................14

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3MANAGERIAL ACCOUNTING

Introduction

The financial analysis of the Triton Company primarily engaged in

the manufacturing activities was taken into consideration for the analysis

of the various divisions of the company. With the growth of the level of

the competition under which the operations of the company is based

needs to be analysed depending upon the performance of the various

divisions of the company. The analysis of the various divisions of the

company was done based on the return generated by each of the

divisions (Williams and Dobelman 2017). There are in total of six divisions

for the company that will be analysed based on the sales generated in

each of them in correspondence to the level of expenses and profitability

share of each of the divisions. Business risk and financial risk are some of

the key risk associated with the company the same has been taken into

consideration for the purpose of the analysis (Vogel 2014). High level of

debt increases the financial risk associated with the company and it is

optimal for the company to have an optimal level of debt in the company.

There are various factors that affects the capital budgeting decisions of

the company like the initial cost/ investment into the project and the cash

expected cash flows from the project (Burns and Walker 2015). The

importance and the relevance of the ratio analysis for evaluating the

financial performance of the company was taken into consideration for the

company. Decentralisation of the head office staff for bring operational

efficiency in the daily workings of the company was also taken into

consideration. As a going concern it is very important to review the

performance of the company and the various aspects of the operations of

the company (Blum and Dacorogna 2014). For the long-term viability of

the project it is important for the company to make a strategic decision in

the context of the operational performance of the company. The

importance and the exposure of the financial leverage of the company

was taken into account for the purpose of discussion of the financial

performance of the company (Post and Byron 2015). Various quantitative

Introduction

The financial analysis of the Triton Company primarily engaged in

the manufacturing activities was taken into consideration for the analysis

of the various divisions of the company. With the growth of the level of

the competition under which the operations of the company is based

needs to be analysed depending upon the performance of the various

divisions of the company. The analysis of the various divisions of the

company was done based on the return generated by each of the

divisions (Williams and Dobelman 2017). There are in total of six divisions

for the company that will be analysed based on the sales generated in

each of them in correspondence to the level of expenses and profitability

share of each of the divisions. Business risk and financial risk are some of

the key risk associated with the company the same has been taken into

consideration for the purpose of the analysis (Vogel 2014). High level of

debt increases the financial risk associated with the company and it is

optimal for the company to have an optimal level of debt in the company.

There are various factors that affects the capital budgeting decisions of

the company like the initial cost/ investment into the project and the cash

expected cash flows from the project (Burns and Walker 2015). The

importance and the relevance of the ratio analysis for evaluating the

financial performance of the company was taken into consideration for the

company. Decentralisation of the head office staff for bring operational

efficiency in the daily workings of the company was also taken into

consideration. As a going concern it is very important to review the

performance of the company and the various aspects of the operations of

the company (Blum and Dacorogna 2014). For the long-term viability of

the project it is important for the company to make a strategic decision in

the context of the operational performance of the company. The

importance and the exposure of the financial leverage of the company

was taken into account for the purpose of discussion of the financial

performance of the company (Post and Byron 2015). Various quantitative

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4MANAGERIAL ACCOUNTING

assessment tools like ratio analysis in the field of profitability, liquidity and

leverage was undertaken for the purpose of analysis of the company.

Discussion

a) Evaluation of Various Divisions

Triton Corporation has in total of six operating divisions for the

company wherein each of the operating divisions will be analysed base on

the return generated from them and the contribution provided in the

profitability of the company (Forsgren and Johanson 2014). The Electrical

Products Company is having the highest number of market share where

the revenue of the division has been the highest but the profitability of the

division has not been well in comparison to other divisions (Amrina and

Vilsi 2015).

1) Bathroom Accessories

Explain: Sales for the division has been around $7.0 MN, cost of

sales for the company has been around 6.5 MN and the net

profitability of division of the company has been around 0.5 MN.

The profitability generated from the Bathroom Accessories services

has been 7.14%, which is the operating profit margin of the division.

The division had a sound return while return on the total asset

generated from the division was just around 0.50%. The market

share of the division on the other hand was not significant with only

around 8% to be the total market share that was occupied by the

division (Deming 2018).

2) Industrial Services

Explain: The Industrial service of the company has reported a profit

of around 23.74% that stands the highest among the other divisions

of the company. The division did not have the highest revenue but

due to lower operational cost and various expenses related to the

division is relatively low which marks the high amount of profitability

from the division. The division contributed significantly in the overall

profitability of the company. The market share occupied by the

company was also significant at around 25% of the total market

assessment tools like ratio analysis in the field of profitability, liquidity and

leverage was undertaken for the purpose of analysis of the company.

Discussion

a) Evaluation of Various Divisions

Triton Corporation has in total of six operating divisions for the

company wherein each of the operating divisions will be analysed base on

the return generated from them and the contribution provided in the

profitability of the company (Forsgren and Johanson 2014). The Electrical

Products Company is having the highest number of market share where

the revenue of the division has been the highest but the profitability of the

division has not been well in comparison to other divisions (Amrina and

Vilsi 2015).

1) Bathroom Accessories

Explain: Sales for the division has been around $7.0 MN, cost of

sales for the company has been around 6.5 MN and the net

profitability of division of the company has been around 0.5 MN.

The profitability generated from the Bathroom Accessories services

has been 7.14%, which is the operating profit margin of the division.

The division had a sound return while return on the total asset

generated from the division was just around 0.50%. The market

share of the division on the other hand was not significant with only

around 8% to be the total market share that was occupied by the

division (Deming 2018).

2) Industrial Services

Explain: The Industrial service of the company has reported a profit

of around 23.74% that stands the highest among the other divisions

of the company. The division did not have the highest revenue but

due to lower operational cost and various expenses related to the

division is relatively low which marks the high amount of profitability

from the division. The division contributed significantly in the overall

profitability of the company. The market share occupied by the

company was also significant at around 25% of the total market

5MANAGERIAL ACCOUNTING

share that was captured by the Industrial division of the company

(Tsay 2014).

3) Car Accessories

Explain: The division also has a sound profit with around $3 MN to

be the reported profitability of the company. The division has a

profitability of around 17.54% in the current year, which was the

second highest contributor of the overall profitability of the

company. The market share of this division of this company was

also sound with around 30% to be the overall market share that is

captured by the Car Accessories divisions (Afonso, Baxa and Slavík

2018).

4) Floor Boards

Explain: The division reported around 5.51% of the profitability in

the current year, which was not as high as other division the same

has been due to higher operating cost associated with this divisions.

The division in spite of 27% of the market share has not been able

to deliver better returns in the overall profitability of the company

(Cadle, Paul and Turner 2014).

5) Electrical Products

Explain: The electrical product division reported around 5.50% that

turned out to be poor performing division of the company. The

division had the highest amount of reported revenue in the current

fiscal year but the higher cost associated with the company in the

form of higher material cost has degraded the overall profitability of

the company. The company did also have a significant market share

of around 40% in the market but could not deliver higher return due

to operational inefficiencies and higher cost of operation associated

with the company division (Quinlan et al. 2019).

6) Pipes Division

Explain: The pipes division of the company reported around 0.1

million of profitability and an operating profit margin of around

1.67%, which has been the worst among other division. Significant

amount of operational cost associated with the division and lower

share that was captured by the Industrial division of the company

(Tsay 2014).

3) Car Accessories

Explain: The division also has a sound profit with around $3 MN to

be the reported profitability of the company. The division has a

profitability of around 17.54% in the current year, which was the

second highest contributor of the overall profitability of the

company. The market share of this division of this company was

also sound with around 30% to be the overall market share that is

captured by the Car Accessories divisions (Afonso, Baxa and Slavík

2018).

4) Floor Boards

Explain: The division reported around 5.51% of the profitability in

the current year, which was not as high as other division the same

has been due to higher operating cost associated with this divisions.

The division in spite of 27% of the market share has not been able

to deliver better returns in the overall profitability of the company

(Cadle, Paul and Turner 2014).

5) Electrical Products

Explain: The electrical product division reported around 5.50% that

turned out to be poor performing division of the company. The

division had the highest amount of reported revenue in the current

fiscal year but the higher cost associated with the company in the

form of higher material cost has degraded the overall profitability of

the company. The company did also have a significant market share

of around 40% in the market but could not deliver higher return due

to operational inefficiencies and higher cost of operation associated

with the company division (Quinlan et al. 2019).

6) Pipes Division

Explain: The pipes division of the company reported around 0.1

million of profitability and an operating profit margin of around

1.67%, which has been the worst among other division. Significant

amount of operational cost associated with the division and lower

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

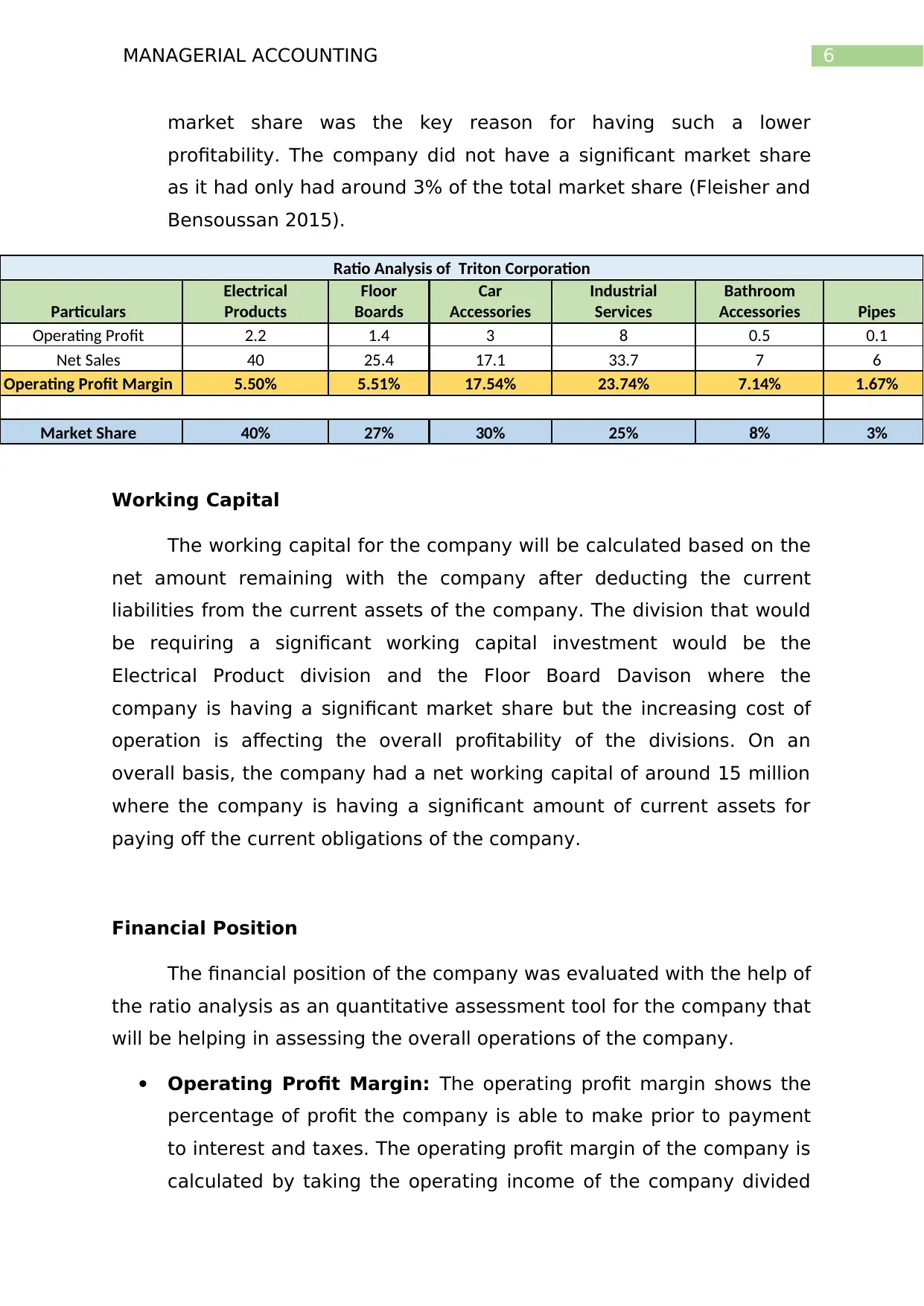

6MANAGERIAL ACCOUNTING

market share was the key reason for having such a lower

profitability. The company did not have a significant market share

as it had only had around 3% of the total market share (Fleisher and

Bensoussan 2015).

Ratio Analysis of Triton Corporation

Particulars

Electrical

Products

Floor

Boards

Car

Accessories

Industrial

Services

Bathroom

Accessories Pipes

Operating Profit 2.2 1.4 3 8 0.5 0.1

Net Sales 40 25.4 17.1 33.7 7 6

Operating Profit Margin 5.50% 5.51% 17.54% 23.74% 7.14% 1.67%

Market Share 40% 27% 30% 25% 8% 3%

Working Capital

The working capital for the company will be calculated based on the

net amount remaining with the company after deducting the current

liabilities from the current assets of the company. The division that would

be requiring a significant working capital investment would be the

Electrical Product division and the Floor Board Davison where the

company is having a significant market share but the increasing cost of

operation is affecting the overall profitability of the divisions. On an

overall basis, the company had a net working capital of around 15 million

where the company is having a significant amount of current assets for

paying off the current obligations of the company.

Financial Position

The financial position of the company was evaluated with the help of

the ratio analysis as an quantitative assessment tool for the company that

will be helping in assessing the overall operations of the company.

Operating Profit Margin: The operating profit margin shows the

percentage of profit the company is able to make prior to payment

to interest and taxes. The operating profit margin of the company is

calculated by taking the operating income of the company divided

market share was the key reason for having such a lower

profitability. The company did not have a significant market share

as it had only had around 3% of the total market share (Fleisher and

Bensoussan 2015).

Ratio Analysis of Triton Corporation

Particulars

Electrical

Products

Floor

Boards

Car

Accessories

Industrial

Services

Bathroom

Accessories Pipes

Operating Profit 2.2 1.4 3 8 0.5 0.1

Net Sales 40 25.4 17.1 33.7 7 6

Operating Profit Margin 5.50% 5.51% 17.54% 23.74% 7.14% 1.67%

Market Share 40% 27% 30% 25% 8% 3%

Working Capital

The working capital for the company will be calculated based on the

net amount remaining with the company after deducting the current

liabilities from the current assets of the company. The division that would

be requiring a significant working capital investment would be the

Electrical Product division and the Floor Board Davison where the

company is having a significant market share but the increasing cost of

operation is affecting the overall profitability of the divisions. On an

overall basis, the company had a net working capital of around 15 million

where the company is having a significant amount of current assets for

paying off the current obligations of the company.

Financial Position

The financial position of the company was evaluated with the help of

the ratio analysis as an quantitative assessment tool for the company that

will be helping in assessing the overall operations of the company.

Operating Profit Margin: The operating profit margin shows the

percentage of profit the company is able to make prior to payment

to interest and taxes. The operating profit margin of the company is

calculated by taking the operating income of the company divided

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7MANAGERIAL ACCOUNTING

by the net sales of the company. The operating profit margin of the

company was around 12.3%, which is sound for the company.

Return on Total Assets: The return shows the level of profitability

earned on total assets for the company. The return on total assets

for the company was calculated by taking the Net Income/ Total

Assets. The return on total assets of the company was around

15.1% for the company showing that the assets of the company are

well utilized by the management of the company (Pilbeam 2018).

Return on Equity: The return on equity for the company was

calculated by taking the net income divided by the total

shareholders’ equity of the company. The ratio shows the level of

profitability or the return generate y the company on the total

shareholders’ equity of the company. The ratio stands as one of the

most important financial performance assessor for identifying the

financial performance of the company. The return on equity for the

company was around 47.2% for the company.

b) Strategic Decisions

In order to stay profitable and have a sustainable profitability

condition it is necessary for the company to identify various factors that

contribute the overall profitability which affect the profitability of the

divisions. Both the bathroom accessories divisions and the pipes division

will be analysed based on the profitability and financial viability of the

divisions. The bathroom division of the company had a sound operating

profitability with around 7.14% to be the total profitability with a market

share of around 8% and a chance to improve the overall profitability by

bringing operational efficiency in the company. On the other hand, side

the pipe division of the company had almost the same revenue as the

bathroom accessories division but the reported profitability was poor

when compared to the other divisions. The reported profitability of the

division was around 1.67% and the same has been due to higher

operating costs associated with the divisions and a lower market share

(Wheelen et al. 2017).

by the net sales of the company. The operating profit margin of the

company was around 12.3%, which is sound for the company.

Return on Total Assets: The return shows the level of profitability

earned on total assets for the company. The return on total assets

for the company was calculated by taking the Net Income/ Total

Assets. The return on total assets of the company was around

15.1% for the company showing that the assets of the company are

well utilized by the management of the company (Pilbeam 2018).

Return on Equity: The return on equity for the company was

calculated by taking the net income divided by the total

shareholders’ equity of the company. The ratio shows the level of

profitability or the return generate y the company on the total

shareholders’ equity of the company. The ratio stands as one of the

most important financial performance assessor for identifying the

financial performance of the company. The return on equity for the

company was around 47.2% for the company.

b) Strategic Decisions

In order to stay profitable and have a sustainable profitability

condition it is necessary for the company to identify various factors that

contribute the overall profitability which affect the profitability of the

divisions. Both the bathroom accessories divisions and the pipes division

will be analysed based on the profitability and financial viability of the

divisions. The bathroom division of the company had a sound operating

profitability with around 7.14% to be the total profitability with a market

share of around 8% and a chance to improve the overall profitability by

bringing operational efficiency in the company. On the other hand, side

the pipe division of the company had almost the same revenue as the

bathroom accessories division but the reported profitability was poor

when compared to the other divisions. The reported profitability of the

division was around 1.67% and the same has been due to higher

operating costs associated with the divisions and a lower market share

(Wheelen et al. 2017).

8MANAGERIAL ACCOUNTING

Both the division of the company is having a lower market share but

it is important to bring operational efficiency in the business by reducing

the operation cost and various expense related to the business. The

market share of both the divisions and the share of revenue of each of the

division needs to be improved for both the division. Capital expenditure on

the division would be significantly based on the capacity and the ability of

the divisions of the company. The Pipe Division needs to be significantly

improve the operations of the company as the profitability is poor and the

market share held by the division is low. The operations of the company is

significantly based on the increasing competition and higher operational

cost for the company, which makes difficult for the company to bring

operational efficiency in the form of higher return to the company (Bansal

and DesJardine 2014).

It is recommended that the company should sell the Pipe Division

due to the unconditional factors that are affecting the overall viability and

sustainability of the company. The Bathroom Accessories on the other

hand should be taken as Capital Expenditure Programme that would be

helping the division further in bring operational efficiency by increasing

the level of sales in the company and the amount of market share

captured by the divisions. Material cost was the main component of the

total expenses in the Bathroom accessories divisions, which can be well

settled off with the higher amount or growth of the business in the form of

rising revenue for the company. On the other hand side the Pipe division

had a higher wages cost and salaries cost, which constituted the majority

of the total expenses that was spend by the division in the overall

operations of the company. It is advisable for the company to spend

resources and efforts of the management in the development and

planning of the other key divisions of the company (Hagiu 2014). The

other divisions of the company are having a sound profitability and

sufficient market share in the industry that will be allowing the company

in reporting higher profitability and wealth creation of the shareholders of

the company (Enekwe, Agu and Eziedo 2014).

Both the division of the company is having a lower market share but

it is important to bring operational efficiency in the business by reducing

the operation cost and various expense related to the business. The

market share of both the divisions and the share of revenue of each of the

division needs to be improved for both the division. Capital expenditure on

the division would be significantly based on the capacity and the ability of

the divisions of the company. The Pipe Division needs to be significantly

improve the operations of the company as the profitability is poor and the

market share held by the division is low. The operations of the company is

significantly based on the increasing competition and higher operational

cost for the company, which makes difficult for the company to bring

operational efficiency in the form of higher return to the company (Bansal

and DesJardine 2014).

It is recommended that the company should sell the Pipe Division

due to the unconditional factors that are affecting the overall viability and

sustainability of the company. The Bathroom Accessories on the other

hand should be taken as Capital Expenditure Programme that would be

helping the division further in bring operational efficiency by increasing

the level of sales in the company and the amount of market share

captured by the divisions. Material cost was the main component of the

total expenses in the Bathroom accessories divisions, which can be well

settled off with the higher amount or growth of the business in the form of

rising revenue for the company. On the other hand side the Pipe division

had a higher wages cost and salaries cost, which constituted the majority

of the total expenses that was spend by the division in the overall

operations of the company. It is advisable for the company to spend

resources and efforts of the management in the development and

planning of the other key divisions of the company (Hagiu 2014). The

other divisions of the company are having a sound profitability and

sufficient market share in the industry that will be allowing the company

in reporting higher profitability and wealth creation of the shareholders of

the company (Enekwe, Agu and Eziedo 2014).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9MANAGERIAL ACCOUNTING

c) Financial Gearing

The financial gearing of the company shows the level and exposure

of the level of debt in a company. The debt to equity ratio for the

company was calculated by taking the long-term debt of the company and

the total shareholder’s equity. For the potential investment into the new

project or development, it is necessary for the company to review the

financial performance of the company and the financial position of the

company (Amba 2014).

The gearing ratio for the company was around 34%, which is

considered as an optimal debt coverage ratio for the company, which is

considered as optimal for the company. The gearing ratio for the company

is optimal as the companies needs to consider the same by analysing the

various factors and conditions under which the operations of the company

is based. High level of debt in the company may increase the financial risk

associated with the company thus, it is necessary for the company to

have an optimal level of debt and equity in the company (O'Hare 2016).

The liquidity ratio for the company was calculated by taking the current

ratio of the company. The liquidity ratio for the company was calculated

by dividing the current assets divided by the current liabilities of the

company. The current ratio for the company was around 1.75 times which

is sound for the company implying the company is having an sufficient

amount of current assets for covering the current liabilities of the

company.

i) Payback period

The Payback Period is calculated as = Cost of project or investment /

Annual cash inflow

The factors that influence the payback period of the development

activities undertaken and the equipment replacement programs

undertaken by the company can be the initial cost of investment, the

timing of the cash inflows from the project. The payback period simply

calculates the average time taken by the investment project top return

c) Financial Gearing

The financial gearing of the company shows the level and exposure

of the level of debt in a company. The debt to equity ratio for the

company was calculated by taking the long-term debt of the company and

the total shareholder’s equity. For the potential investment into the new

project or development, it is necessary for the company to review the

financial performance of the company and the financial position of the

company (Amba 2014).

The gearing ratio for the company was around 34%, which is

considered as an optimal debt coverage ratio for the company, which is

considered as optimal for the company. The gearing ratio for the company

is optimal as the companies needs to consider the same by analysing the

various factors and conditions under which the operations of the company

is based. High level of debt in the company may increase the financial risk

associated with the company thus, it is necessary for the company to

have an optimal level of debt and equity in the company (O'Hare 2016).

The liquidity ratio for the company was calculated by taking the current

ratio of the company. The liquidity ratio for the company was calculated

by dividing the current assets divided by the current liabilities of the

company. The current ratio for the company was around 1.75 times which

is sound for the company implying the company is having an sufficient

amount of current assets for covering the current liabilities of the

company.

i) Payback period

The Payback Period is calculated as = Cost of project or investment /

Annual cash inflow

The factors that influence the payback period of the development

activities undertaken and the equipment replacement programs

undertaken by the company can be the initial cost of investment, the

timing of the cash inflows from the project. The payback period simply

calculates the average time taken by the investment project top return

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10MANAGERIAL ACCOUNTING

back the initial invested amount by considering the annual cash inflows

from the company. Delay in cash inflows of the project and increase in the

initial invested amount are some of the crucial factors that can affect the

overall operations of the company and the payback period of the

company. Thus, it is important for the company to materialize various

factors and points that may significantly affect the operations and the

payback period of the company.

ii) Reducing Gearing

Reducing gearing ratio for the company implies the reducing

exposure of debt for the company. Gearing ratio for the company implies

the extent of debt. The company can reduce the gearing ratio in the

company in various ways. It is important to note that primarily there are

two keys risks that are associated with the company, which is the

business risk, and financial risk. Reducing gearing ratio for the company in

the form of repayment of borrowed funds, retaining the profits of the

company rather than distributing the same to the shareholders of the

company. Issuing more equity shares and converting the loans into equity

shares are some of the common forms of reducing the overall equity level

of the company.

The strategic aim for reducing the gearing ratio of the company is to

reduce the overall risk of the company in the form of financial risk that

would be associated in a company in the form of higher debt of the

company. The aim of the company to invest in the modernization program

is due to the operational efficiency and the expansion of the company that

would be seen by the company in the form of increasing business of the

company. Better and efficient technology and better utilization of the

asset through better and modern equipment’s of the company will be

helping the company in creating better returns for the company.

Delivering better return and creating wealth for the shareholders of the

company is the prime objective of the company that would be helping the

company in achieving the overall sustainability of the company. The

capital structure of the company thus should be optimal allowing the

back the initial invested amount by considering the annual cash inflows

from the company. Delay in cash inflows of the project and increase in the

initial invested amount are some of the crucial factors that can affect the

overall operations of the company and the payback period of the

company. Thus, it is important for the company to materialize various

factors and points that may significantly affect the operations and the

payback period of the company.

ii) Reducing Gearing

Reducing gearing ratio for the company implies the reducing

exposure of debt for the company. Gearing ratio for the company implies

the extent of debt. The company can reduce the gearing ratio in the

company in various ways. It is important to note that primarily there are

two keys risks that are associated with the company, which is the

business risk, and financial risk. Reducing gearing ratio for the company in

the form of repayment of borrowed funds, retaining the profits of the

company rather than distributing the same to the shareholders of the

company. Issuing more equity shares and converting the loans into equity

shares are some of the common forms of reducing the overall equity level

of the company.

The strategic aim for reducing the gearing ratio of the company is to

reduce the overall risk of the company in the form of financial risk that

would be associated in a company in the form of higher debt of the

company. The aim of the company to invest in the modernization program

is due to the operational efficiency and the expansion of the company that

would be seen by the company in the form of increasing business of the

company. Better and efficient technology and better utilization of the

asset through better and modern equipment’s of the company will be

helping the company in creating better returns for the company.

Delivering better return and creating wealth for the shareholders of the

company is the prime objective of the company that would be helping the

company in achieving the overall sustainability of the company. The

capital structure of the company thus should be optimal allowing the

11MANAGERIAL ACCOUNTING

company to take the advantage of both equity and debt in the books of

accounts of the company and create a better capital structure for the

company. Low cost financing and tax deductible interest expenses makes

debt financing easy and attractable for the company. On the other hand,

low risk associated with equity financing is the key reason for financing

equity as a reliable capital source for the company. Thus, it is important

for the company to have an optimal mix of both debt and equity and

create a well and sustainable capital structure for the company. The same

should be analyzed based on the various business factors and macro-

economic factors under which the operations of the company is based.

d) Decentralize Program

i) Ratio Analysis is an important quantitative assessment tool that is used

for identifying the financial performance of the company.

The return on equity for the company was calculated by taking the

net income divided by the total shareholders’ equity of the company. The

ratio shows the level of profitability or the return generate by the

company on the total shareholders’ equity of the company. The ratio

stands as one of the most important financial performance assessor for

identifying the financial performance of the company. The return on

equity for the company was around 47.2% for the company.

Return on total assets of the company could be further calculated

with the help of the net income and the total assets of the company. The

management of the company can further assess the efficiency of the

company with the help of this ratio signifying the utilization of the assets

of the company.

Decentralisation of the office staff in the company will help the

management of the company in better management of the various office

head staffs that would be helping the company in making better informed

(Edwards, Yilmaz and Boex 2015). The company would be also saving

costs related to the office staff after the decentralisation of the office

staffs. Better-informed and quick decisions would be the quick

company to take the advantage of both equity and debt in the books of

accounts of the company and create a better capital structure for the

company. Low cost financing and tax deductible interest expenses makes

debt financing easy and attractable for the company. On the other hand,

low risk associated with equity financing is the key reason for financing

equity as a reliable capital source for the company. Thus, it is important

for the company to have an optimal mix of both debt and equity and

create a well and sustainable capital structure for the company. The same

should be analyzed based on the various business factors and macro-

economic factors under which the operations of the company is based.

d) Decentralize Program

i) Ratio Analysis is an important quantitative assessment tool that is used

for identifying the financial performance of the company.

The return on equity for the company was calculated by taking the

net income divided by the total shareholders’ equity of the company. The

ratio shows the level of profitability or the return generate by the

company on the total shareholders’ equity of the company. The ratio

stands as one of the most important financial performance assessor for

identifying the financial performance of the company. The return on

equity for the company was around 47.2% for the company.

Return on total assets of the company could be further calculated

with the help of the net income and the total assets of the company. The

management of the company can further assess the efficiency of the

company with the help of this ratio signifying the utilization of the assets

of the company.

Decentralisation of the office staff in the company will help the

management of the company in better management of the various office

head staffs that would be helping the company in making better informed

(Edwards, Yilmaz and Boex 2015). The company would be also saving

costs related to the office staff after the decentralisation of the office

staffs. Better-informed and quick decisions would be the quick

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.