HI5017 Trimester 3 2018 Individual Assignment 2: Budgeting Analysis

VerifiedAdded on 2023/04/21

|16

|3682

|451

Report

AI Summary

This report analyzes the elements of a master budget, which is a crucial financial planning tool for businesses. It explores the differences between top-down and bottom-up budgeting approaches, evaluating their suitability for Accent Group, a retailing company. The analysis includes a detailed comparison of these two approaches, highlighting their advantages and disadvantages. Furthermore, the report develops a budgeted income statement for Accent Group for the year 2019, utilizing financial data from 2018, and compares it with the actual income statement from 2018. The report also includes a discussion on the preparation of the budgeted income statement, considering factors such as changes in sales, costs, and inflation. The conclusion summarizes the findings and emphasizes the importance of the master budget in guiding the strategic direction of a company.

1

HI5017 Managerial Accounting

Trimester 3 2018

Individual Assignment

HI5017 Managerial Accounting

Trimester 3 2018

Individual Assignment

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2

Executive Summary

Management accounting is important business process and it involves preparing the

budgets for estimating the future performance and position of the company. Budgets are drafted

for shorter period as well as for longer period of time. There are many types of budgets that are

required to be developed depending upon the requirement of the company. Master budget is the

combination of all the budgets as it takes in values from all the budgets such as sales budget,

purchase budget etc.

In this financial report, elements of master budget is explained together with top down &

bottom up approach to the budget process is discussed in detail to analyse which is more suitable

for the selected company. The company selected for this purpose is Accent Group. In addition to

budgeted income statement is developed of Accent Group for year 2019 through using the

financial data of year 2018.

Executive Summary

Management accounting is important business process and it involves preparing the

budgets for estimating the future performance and position of the company. Budgets are drafted

for shorter period as well as for longer period of time. There are many types of budgets that are

required to be developed depending upon the requirement of the company. Master budget is the

combination of all the budgets as it takes in values from all the budgets such as sales budget,

purchase budget etc.

In this financial report, elements of master budget is explained together with top down &

bottom up approach to the budget process is discussed in detail to analyse which is more suitable

for the selected company. The company selected for this purpose is Accent Group. In addition to

budgeted income statement is developed of Accent Group for year 2019 through using the

financial data of year 2018.

3

Contents

Executive Summary.........................................................................................................................2

Introduction......................................................................................................................................4

Part A: Elements of Master Budget.................................................................................................4

Part B: Comparison of the Top-Down and Bottom-Up Approach to the Budget Process and their

Suitability for the Selected Company..............................................................................................5

Part C: Preparation of Budgeted income statement for year 2019 based on financial data of year

2018.................................................................................................................................................7

Part D: Comparison of actual income statement of year 2018 and budgeted income statement for

year 2019.......................................................................................................................................10

Conclusion.....................................................................................................................................12

References......................................................................................................................................13

Contents

Executive Summary.........................................................................................................................2

Introduction......................................................................................................................................4

Part A: Elements of Master Budget.................................................................................................4

Part B: Comparison of the Top-Down and Bottom-Up Approach to the Budget Process and their

Suitability for the Selected Company..............................................................................................5

Part C: Preparation of Budgeted income statement for year 2019 based on financial data of year

2018.................................................................................................................................................7

Part D: Comparison of actual income statement of year 2018 and budgeted income statement for

year 2019.......................................................................................................................................10

Conclusion.....................................................................................................................................12

References......................................................................................................................................13

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4

Introduction

The present report is developed for analyzing the budgeted income statement of an ASX

listed entity. This is carried out by providing an explanation of the elements of master budget and

discussing the comparison between the top-down and bottom-up approach for the budgeted

process. This is done for analysis of the budgeted process that is more suitable for the selected

company. It is followed by developing the budgeted income statements for the selected company

for the following year on the basis of the past year annual report. This is done for providing a

comparison of the budgeted income statement prepared for the year 2019 with the actual income

statement developed for the year 2018. The company selected for analysis purpose is Accent

Group Limited, a retailing company involved in distribution of various types of footwear and

apparel products.

Part A: Elements of Master Budget

Master budget can be described as the financial plan that is developed for managing the

manufacturing and sales activity of a company for meeting the profitability goals. It is mainly

developed for estimating the future income and expenses of a company. The master budget

developed cam ne used by small-business owners for development of different specific budgets

for the business. The development of master budget requires coordination of different smaller

budgets for covering the different activities involved in an organization (Jones, 2015). As such,

the budget helps in creation of various small budgets and so the different elements of a master

budget can be described as below:

Materials Budget

The budget provides information related to acquisition of raw materials that is required

for carrying out the production process of a company. The budget helps in providing an

estimation of the material process over a period of time and thus estimates the material

requirement (Warren, Reeve and Duchac, 2011).

Labor Budget

Introduction

The present report is developed for analyzing the budgeted income statement of an ASX

listed entity. This is carried out by providing an explanation of the elements of master budget and

discussing the comparison between the top-down and bottom-up approach for the budgeted

process. This is done for analysis of the budgeted process that is more suitable for the selected

company. It is followed by developing the budgeted income statements for the selected company

for the following year on the basis of the past year annual report. This is done for providing a

comparison of the budgeted income statement prepared for the year 2019 with the actual income

statement developed for the year 2018. The company selected for analysis purpose is Accent

Group Limited, a retailing company involved in distribution of various types of footwear and

apparel products.

Part A: Elements of Master Budget

Master budget can be described as the financial plan that is developed for managing the

manufacturing and sales activity of a company for meeting the profitability goals. It is mainly

developed for estimating the future income and expenses of a company. The master budget

developed cam ne used by small-business owners for development of different specific budgets

for the business. The development of master budget requires coordination of different smaller

budgets for covering the different activities involved in an organization (Jones, 2015). As such,

the budget helps in creation of various small budgets and so the different elements of a master

budget can be described as below:

Materials Budget

The budget provides information related to acquisition of raw materials that is required

for carrying out the production process of a company. The budget helps in providing an

estimation of the material process over a period of time and thus estimates the material

requirement (Warren, Reeve and Duchac, 2011).

Labor Budget

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5

The budget is prepared for depicting the total direct labor and number of labor hours that

are required for production. The budget helps in planning of the labor workforce that is required

by a company for carrying out its different operational processes.

Sales and Administrative Expenses

The budget is used for estimating the overall expenditure that is involved in all the non-

manufacturing operations of an organization. It includes the activities such as marketing,

accounting, engineering o other such non-manufacturing operations. The budget is usually

presented in a monthly or quarterly format (Needles, Powers and Crosson, 2010).

Revenue and Expense Budget

The budget depicts the anticipated sales of the products of a company by taking into

consideration all the operational expenditures and other such factors. It forecast the revenue and

expenses of a company which depicts the capital-related expenses. The budget helps in

developing an estimate whether a company possesses adequate financial resources for carrying

out its different operational activities and making a profit.

Capital Expenditure Budgets

The budget is developed for preparing the long-term investments of a company which

include the expenses incurred on plants, machinery, renovations, installations and maintenance.

The budget depicts the cash required by a company to carry out different projects and

maintenance of its long-term assets (Crosson and Needles, 2010).

Sales Budget

The budget is required for carrying out forecast of the sales by taking into account the

past and present trend in sales and the impact of any seasonal or other operational factors that

can impact the sales trend. In addition to this, the forecast of sales also need to consider the

factors such as economic environment, inflation rate and price trends of products.

Production Budget

The budget is prepared for depicting the total direct labor and number of labor hours that

are required for production. The budget helps in planning of the labor workforce that is required

by a company for carrying out its different operational processes.

Sales and Administrative Expenses

The budget is used for estimating the overall expenditure that is involved in all the non-

manufacturing operations of an organization. It includes the activities such as marketing,

accounting, engineering o other such non-manufacturing operations. The budget is usually

presented in a monthly or quarterly format (Needles, Powers and Crosson, 2010).

Revenue and Expense Budget

The budget depicts the anticipated sales of the products of a company by taking into

consideration all the operational expenditures and other such factors. It forecast the revenue and

expenses of a company which depicts the capital-related expenses. The budget helps in

developing an estimate whether a company possesses adequate financial resources for carrying

out its different operational activities and making a profit.

Capital Expenditure Budgets

The budget is developed for preparing the long-term investments of a company which

include the expenses incurred on plants, machinery, renovations, installations and maintenance.

The budget depicts the cash required by a company to carry out different projects and

maintenance of its long-term assets (Crosson and Needles, 2010).

Sales Budget

The budget is required for carrying out forecast of the sales by taking into account the

past and present trend in sales and the impact of any seasonal or other operational factors that

can impact the sales trend. In addition to this, the forecast of sales also need to consider the

factors such as economic environment, inflation rate and price trends of products.

Production Budget

6

The budget indicates the plan for carrying out the future manufacturing operations of a

firm and is based on the sales forecasts. The breaking down of the master budget into different

production and overhead costs helps in obtaining adequate price of a product or service. The

costs are identified on the basis of different operational activities such as machinery, materials or

labor (Cunningham, Bazley and Simmons, 2018).

Annual Performance Projection

The most important component of the master budget is providing projection of the annual

performance. The calculation of the average monthly income or expenses helps in providing a

projection of the annual performance of a company.

Thus, it can be said that master budget can be stated to be major planning tool that is used

mainly for the development of all lower-level budgets. The budgets helps in directing the various

activities of a corporation and thus helpful in taking the strategic direction of a company.

Part B: Comparison of the Top-Down and Bottom-Up Approach to the Budget Process and

their Suitability for the Selected Company

Top-Down Budget Process

This type of budgeting process involves development of high-level budget for detailing

the overall activities of an organization. The creation of a budget involves the allocation of

different amounts to each of the departments. The different departments then develop the

respective budgets for estimation of the future opportunities and risks. This type of budget is

mainly developed by the senior-level management people that determine the high-level targets

for the company. The targets are determined for achieving the desired level of sales, expenses or

profitability. The overall objective determined by the senior management is taken by the

individual departments of an organization that are taken to the respective department. The

department manager needs to develop a detailed budget on the basis of target determined by the

senior level management people. For example, the finance departments receive the overall

revenue and cost figures for developing a detailed budget to depict the procedures of achieving

the assigned revenue or cost figures. The is done by providing an explanation regarding the

estimated quantity of product to be sold, estimation of workforce required and expenditure that

The budget indicates the plan for carrying out the future manufacturing operations of a

firm and is based on the sales forecasts. The breaking down of the master budget into different

production and overhead costs helps in obtaining adequate price of a product or service. The

costs are identified on the basis of different operational activities such as machinery, materials or

labor (Cunningham, Bazley and Simmons, 2018).

Annual Performance Projection

The most important component of the master budget is providing projection of the annual

performance. The calculation of the average monthly income or expenses helps in providing a

projection of the annual performance of a company.

Thus, it can be said that master budget can be stated to be major planning tool that is used

mainly for the development of all lower-level budgets. The budgets helps in directing the various

activities of a corporation and thus helpful in taking the strategic direction of a company.

Part B: Comparison of the Top-Down and Bottom-Up Approach to the Budget Process and

their Suitability for the Selected Company

Top-Down Budget Process

This type of budgeting process involves development of high-level budget for detailing

the overall activities of an organization. The creation of a budget involves the allocation of

different amounts to each of the departments. The different departments then develop the

respective budgets for estimation of the future opportunities and risks. This type of budget is

mainly developed by the senior-level management people that determine the high-level targets

for the company. The targets are determined for achieving the desired level of sales, expenses or

profitability. The overall objective determined by the senior management is taken by the

individual departments of an organization that are taken to the respective department. The

department manager needs to develop a detailed budget on the basis of target determined by the

senior level management people. For example, the finance departments receive the overall

revenue and cost figures for developing a detailed budget to depict the procedures of achieving

the assigned revenue or cost figures. The is done by providing an explanation regarding the

estimated quantity of product to be sold, estimation of workforce required and expenditure that

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7

will be incurred such as office supplies, equipment or payroll. The development of final budget

is followed by creation of monthly reports that provides a comparison of the actual activity with

that of the detailed budget. This helps in assessing the progress of each month towards the

revenue goals with the allowed expenses (Cunningham, Nikolai, Bazley and Slaughter, 2014).

The major advantage of the budgeted process is that helps in providing an increased

understanding of the long-term goals and objectives of the organization within each of its

department. However, the major drawback of the method is that it can sometime result in

creation of bottom-up budgets that is not compatible with the goals and objectives of the

corporation. Also, the results obtained may deviate with the budgeted target if the department

manager focuses only on improving the departmental performance rather than placing focus on

the organizational concerns (Krantz, 2016).

Bottom-Up Budgeting Process

The bottom-up budgeting process involves the participation of the all the departments for

development of final budget. It can be said to a type of budgeting that attempts to determine the

costs of each individual department or segment of an organization. This type of budget is also

known as participative budgeting as it involves co-ordination among all the department levels. It

primarily involves planning the activities of each department and then is followed by assigning

the costs to each of the project activities. Lastly, it totals up the cost of each department for

achieving an overall budgeted cost (OECD, 2014). Thus, it involves co-coordinating among

different departments to assign a total budget amount and then developing the final budget. The

methodology of the preparing the budget through the bottom-up budgeting process involves the

following steps. The first step is to identify the individual component of business such as salaries

of staff or other expenses for purchasing new equipment. The planning of projects is then done

by each department level and this is followed by developing the overall total from all the

department projects to arrive an estimated overall budget for that department. The cost involved

in each of the department is then added for developing the overall annual budget. The budget

after the completion is submitted to the executive management for gaining final approval.

The major advantage of the bottom-up budgeting process is that it leads to the

development of very accurate budget that leads to determination of actual costs. This helps in

will be incurred such as office supplies, equipment or payroll. The development of final budget

is followed by creation of monthly reports that provides a comparison of the actual activity with

that of the detailed budget. This helps in assessing the progress of each month towards the

revenue goals with the allowed expenses (Cunningham, Nikolai, Bazley and Slaughter, 2014).

The major advantage of the budgeted process is that helps in providing an increased

understanding of the long-term goals and objectives of the organization within each of its

department. However, the major drawback of the method is that it can sometime result in

creation of bottom-up budgets that is not compatible with the goals and objectives of the

corporation. Also, the results obtained may deviate with the budgeted target if the department

manager focuses only on improving the departmental performance rather than placing focus on

the organizational concerns (Krantz, 2016).

Bottom-Up Budgeting Process

The bottom-up budgeting process involves the participation of the all the departments for

development of final budget. It can be said to a type of budgeting that attempts to determine the

costs of each individual department or segment of an organization. This type of budget is also

known as participative budgeting as it involves co-ordination among all the department levels. It

primarily involves planning the activities of each department and then is followed by assigning

the costs to each of the project activities. Lastly, it totals up the cost of each department for

achieving an overall budgeted cost (OECD, 2014). Thus, it involves co-coordinating among

different departments to assign a total budget amount and then developing the final budget. The

methodology of the preparing the budget through the bottom-up budgeting process involves the

following steps. The first step is to identify the individual component of business such as salaries

of staff or other expenses for purchasing new equipment. The planning of projects is then done

by each department level and this is followed by developing the overall total from all the

department projects to arrive an estimated overall budget for that department. The cost involved

in each of the department is then added for developing the overall annual budget. The budget

after the completion is submitted to the executive management for gaining final approval.

The major advantage of the bottom-up budgeting process is that it leads to the

development of very accurate budget that leads to determination of actual costs. This helps in

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

developing the new goals and objectives promoting the long-term growth and development of an

organization. However, the major drawback of the method is that can lead to the development of

over-estimation of costs which can subsequently hamper the organizational growth and

development. In addition to this, it is also time-consuming as it large amount of time is involved

in meeting, discussing and preparing the budgets (Butz, 2011).

Budgeting process Suitable for Accent Group

On the basis of the discussion of both the approaches, bottom-up budgeting process can

be regarded as the most suitable for the company selected that is Accent Group Retailing. The

bottom-up budgeting process involves developing the long-term goals of the organization and

bottom up approach proves to be successful in achieving the desired in easy manner. This type

budgeting approach is very accurate as every department is involved in this process and head of

each department uses its specialized knowledge to draft the budget of their department. For

example, sales department have the complete knowledge of the sales figures and they are right

person for developing the sales budget. The large size firms have long term goals and they

require long term budgets so that they can overview their budgeting performance over the period

of time. For this purpose it is essential that budgets must be accurate and must be developed

through the corporation of all departments as they are ones that decides the future of the

company. The bottom up budgeting process will improve the morale of employees of Accent

Group employees and they get motivated to achieve the formulate goals frame by them (Brigham

& Michael, 2013).

Part C: Preparation of Budgeted income statement for year 2019 based on financial data of

year 2018

In this section of financial report budgeted income statement has been developed through

using the financial data provided in income statement of year 2018. While preparing the

budgeted income statement through using the financial data of previous year there is need to

make some changes due to change in sales value, increase in cost expenses, inflation, rise in

prices of goods, etc. While preparing the budgeted income statement various data has to be taken

from other budgets such sales budget, cost of goods sold budget, purchase budget, expense

developing the new goals and objectives promoting the long-term growth and development of an

organization. However, the major drawback of the method is that can lead to the development of

over-estimation of costs which can subsequently hamper the organizational growth and

development. In addition to this, it is also time-consuming as it large amount of time is involved

in meeting, discussing and preparing the budgets (Butz, 2011).

Budgeting process Suitable for Accent Group

On the basis of the discussion of both the approaches, bottom-up budgeting process can

be regarded as the most suitable for the company selected that is Accent Group Retailing. The

bottom-up budgeting process involves developing the long-term goals of the organization and

bottom up approach proves to be successful in achieving the desired in easy manner. This type

budgeting approach is very accurate as every department is involved in this process and head of

each department uses its specialized knowledge to draft the budget of their department. For

example, sales department have the complete knowledge of the sales figures and they are right

person for developing the sales budget. The large size firms have long term goals and they

require long term budgets so that they can overview their budgeting performance over the period

of time. For this purpose it is essential that budgets must be accurate and must be developed

through the corporation of all departments as they are ones that decides the future of the

company. The bottom up budgeting process will improve the morale of employees of Accent

Group employees and they get motivated to achieve the formulate goals frame by them (Brigham

& Michael, 2013).

Part C: Preparation of Budgeted income statement for year 2019 based on financial data of

year 2018

In this section of financial report budgeted income statement has been developed through

using the financial data provided in income statement of year 2018. While preparing the

budgeted income statement through using the financial data of previous year there is need to

make some changes due to change in sales value, increase in cost expenses, inflation, rise in

prices of goods, etc. While preparing the budgeted income statement various data has to be taken

from other budgets such sales budget, cost of goods sold budget, purchase budget, expense

9

budget etc. Through using data drafted in these budgets, budgeted income statement can be

drafted (Damodaran, 2011).

An income statement of a company reflects the income earned and expenses occurred

during the selected period of time, generally it is for 1 month, a quarter or a year. Budgeted

income statement is typical income statement drafted for the purpose of predicting the future

financial values of income statement. It is also known as pro forma income statement. Budgeted

income statement is the important part of financial planning process as it helps to determine

whether financial plans are feasible or not. The purpose is to find out how much earnings the

business will earn in future and total value of expenses need to pay for earning those incomes.

After the facts of budgeted year have been gathered, the budgeted and actual values of income

statement are compared to analyse the performance of the company for that particular year. This

comparison helps to improve the budgeted income statement of next year (Davies and Crawford,

2011).

In order to prepare the budgeted income statement of Accent Group for year 2019,

following are changes that need to be performed while calculating the value of income statement.

Following are the proposed changes:

It has been decided to increase the value of sales/revenue by 10%

The value of cost of goods sold has been projected to grow up by 8%

All other expenses has been projected to be grow by 2%

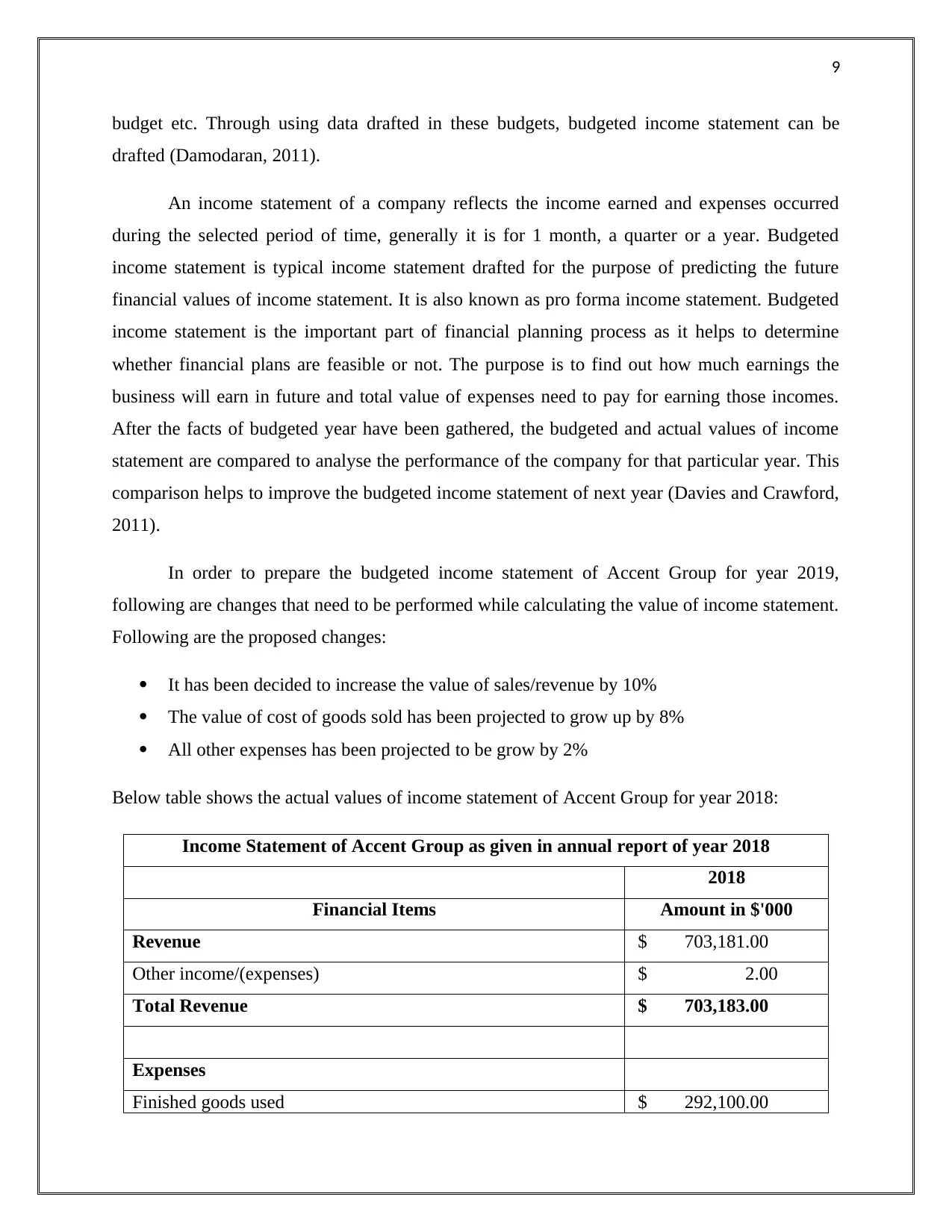

Below table shows the actual values of income statement of Accent Group for year 2018:

Income Statement of Accent Group as given in annual report of year 2018

2018

Financial Items Amount in $'000

Revenue $ 703,181.00

Other income/(expenses) $ 2.00

Total Revenue $ 703,183.00

Expenses

Finished goods used $ 292,100.00

budget etc. Through using data drafted in these budgets, budgeted income statement can be

drafted (Damodaran, 2011).

An income statement of a company reflects the income earned and expenses occurred

during the selected period of time, generally it is for 1 month, a quarter or a year. Budgeted

income statement is typical income statement drafted for the purpose of predicting the future

financial values of income statement. It is also known as pro forma income statement. Budgeted

income statement is the important part of financial planning process as it helps to determine

whether financial plans are feasible or not. The purpose is to find out how much earnings the

business will earn in future and total value of expenses need to pay for earning those incomes.

After the facts of budgeted year have been gathered, the budgeted and actual values of income

statement are compared to analyse the performance of the company for that particular year. This

comparison helps to improve the budgeted income statement of next year (Davies and Crawford,

2011).

In order to prepare the budgeted income statement of Accent Group for year 2019,

following are changes that need to be performed while calculating the value of income statement.

Following are the proposed changes:

It has been decided to increase the value of sales/revenue by 10%

The value of cost of goods sold has been projected to grow up by 8%

All other expenses has been projected to be grow by 2%

Below table shows the actual values of income statement of Accent Group for year 2018:

Income Statement of Accent Group as given in annual report of year 2018

2018

Financial Items Amount in $'000

Revenue $ 703,181.00

Other income/(expenses) $ 2.00

Total Revenue $ 703,183.00

Expenses

Finished goods used $ 292,100.00

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10

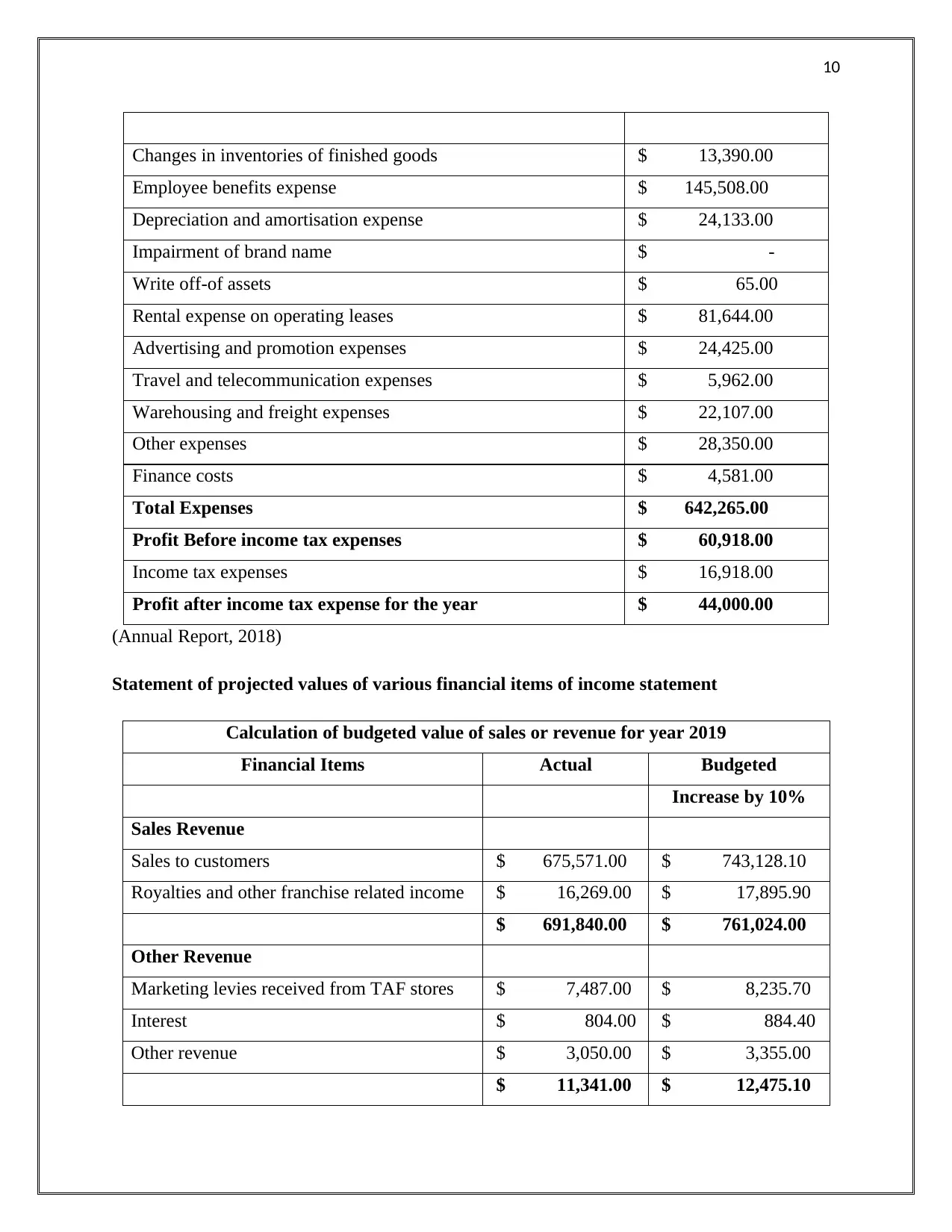

Changes in inventories of finished goods $ 13,390.00

Employee benefits expense $ 145,508.00

Depreciation and amortisation expense $ 24,133.00

Impairment of brand name $ -

Write off-of assets $ 65.00

Rental expense on operating leases $ 81,644.00

Advertising and promotion expenses $ 24,425.00

Travel and telecommunication expenses $ 5,962.00

Warehousing and freight expenses $ 22,107.00

Other expenses $ 28,350.00

Finance costs $ 4,581.00

Total Expenses $ 642,265.00

Profit Before income tax expenses $ 60,918.00

Income tax expenses $ 16,918.00

Profit after income tax expense for the year $ 44,000.00

(Annual Report, 2018)

Statement of projected values of various financial items of income statement

Calculation of budgeted value of sales or revenue for year 2019

Financial Items Actual Budgeted

Increase by 10%

Sales Revenue

Sales to customers $ 675,571.00 $ 743,128.10

Royalties and other franchise related income $ 16,269.00 $ 17,895.90

$ 691,840.00 $ 761,024.00

Other Revenue

Marketing levies received from TAF stores $ 7,487.00 $ 8,235.70

Interest $ 804.00 $ 884.40

Other revenue $ 3,050.00 $ 3,355.00

$ 11,341.00 $ 12,475.10

Changes in inventories of finished goods $ 13,390.00

Employee benefits expense $ 145,508.00

Depreciation and amortisation expense $ 24,133.00

Impairment of brand name $ -

Write off-of assets $ 65.00

Rental expense on operating leases $ 81,644.00

Advertising and promotion expenses $ 24,425.00

Travel and telecommunication expenses $ 5,962.00

Warehousing and freight expenses $ 22,107.00

Other expenses $ 28,350.00

Finance costs $ 4,581.00

Total Expenses $ 642,265.00

Profit Before income tax expenses $ 60,918.00

Income tax expenses $ 16,918.00

Profit after income tax expense for the year $ 44,000.00

(Annual Report, 2018)

Statement of projected values of various financial items of income statement

Calculation of budgeted value of sales or revenue for year 2019

Financial Items Actual Budgeted

Increase by 10%

Sales Revenue

Sales to customers $ 675,571.00 $ 743,128.10

Royalties and other franchise related income $ 16,269.00 $ 17,895.90

$ 691,840.00 $ 761,024.00

Other Revenue

Marketing levies received from TAF stores $ 7,487.00 $ 8,235.70

Interest $ 804.00 $ 884.40

Other revenue $ 3,050.00 $ 3,355.00

$ 11,341.00 $ 12,475.10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11

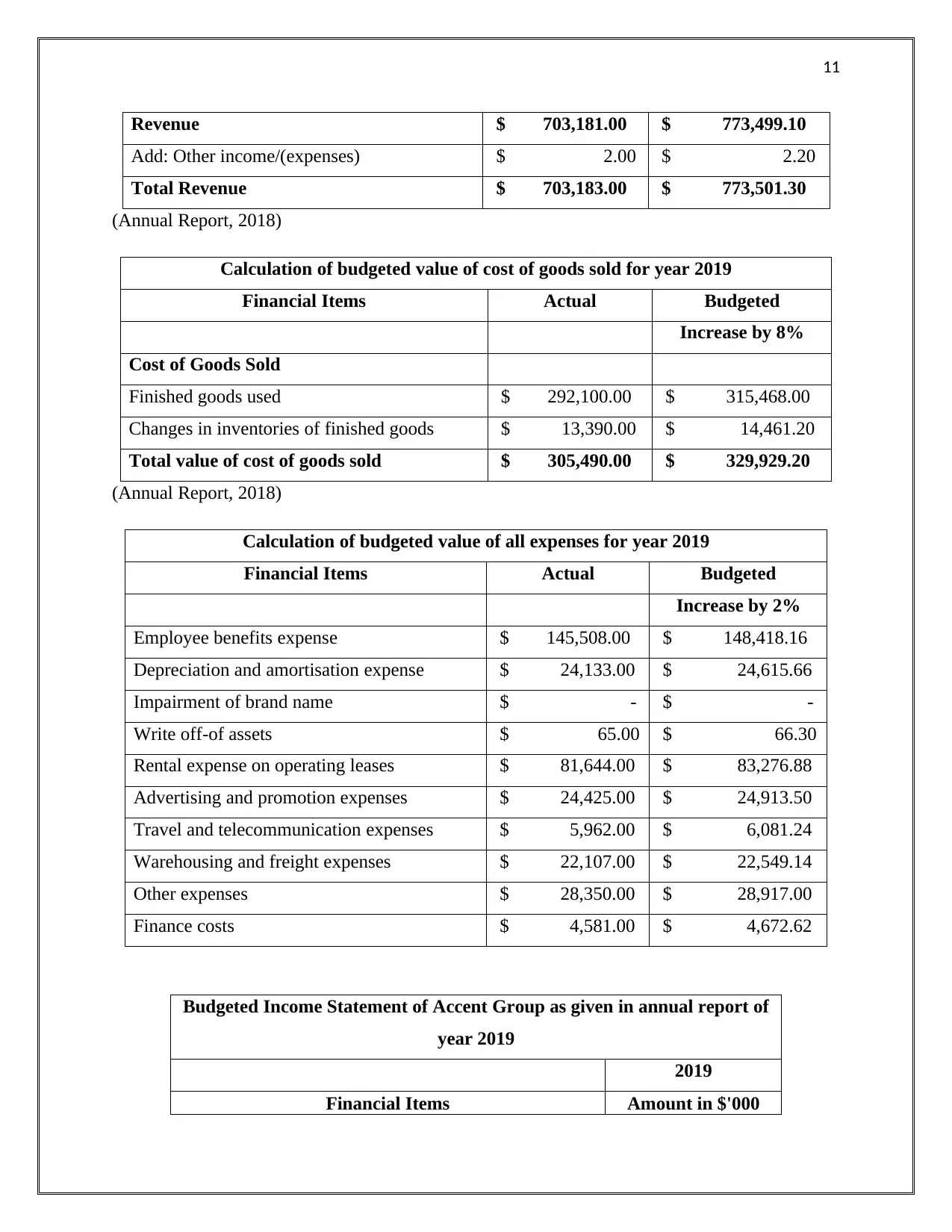

Revenue $ 703,181.00 $ 773,499.10

Add: Other income/(expenses) $ 2.00 $ 2.20

Total Revenue $ 703,183.00 $ 773,501.30

(Annual Report, 2018)

Calculation of budgeted value of cost of goods sold for year 2019

Financial Items Actual Budgeted

Increase by 8%

Cost of Goods Sold

Finished goods used $ 292,100.00 $ 315,468.00

Changes in inventories of finished goods $ 13,390.00 $ 14,461.20

Total value of cost of goods sold $ 305,490.00 $ 329,929.20

(Annual Report, 2018)

Calculation of budgeted value of all expenses for year 2019

Financial Items Actual Budgeted

Increase by 2%

Employee benefits expense $ 145,508.00 $ 148,418.16

Depreciation and amortisation expense $ 24,133.00 $ 24,615.66

Impairment of brand name $ - $ -

Write off-of assets $ 65.00 $ 66.30

Rental expense on operating leases $ 81,644.00 $ 83,276.88

Advertising and promotion expenses $ 24,425.00 $ 24,913.50

Travel and telecommunication expenses $ 5,962.00 $ 6,081.24

Warehousing and freight expenses $ 22,107.00 $ 22,549.14

Other expenses $ 28,350.00 $ 28,917.00

Finance costs $ 4,581.00 $ 4,672.62

Budgeted Income Statement of Accent Group as given in annual report of

year 2019

2019

Financial Items Amount in $'000

Revenue $ 703,181.00 $ 773,499.10

Add: Other income/(expenses) $ 2.00 $ 2.20

Total Revenue $ 703,183.00 $ 773,501.30

(Annual Report, 2018)

Calculation of budgeted value of cost of goods sold for year 2019

Financial Items Actual Budgeted

Increase by 8%

Cost of Goods Sold

Finished goods used $ 292,100.00 $ 315,468.00

Changes in inventories of finished goods $ 13,390.00 $ 14,461.20

Total value of cost of goods sold $ 305,490.00 $ 329,929.20

(Annual Report, 2018)

Calculation of budgeted value of all expenses for year 2019

Financial Items Actual Budgeted

Increase by 2%

Employee benefits expense $ 145,508.00 $ 148,418.16

Depreciation and amortisation expense $ 24,133.00 $ 24,615.66

Impairment of brand name $ - $ -

Write off-of assets $ 65.00 $ 66.30

Rental expense on operating leases $ 81,644.00 $ 83,276.88

Advertising and promotion expenses $ 24,425.00 $ 24,913.50

Travel and telecommunication expenses $ 5,962.00 $ 6,081.24

Warehousing and freight expenses $ 22,107.00 $ 22,549.14

Other expenses $ 28,350.00 $ 28,917.00

Finance costs $ 4,581.00 $ 4,672.62

Budgeted Income Statement of Accent Group as given in annual report of

year 2019

2019

Financial Items Amount in $'000

12

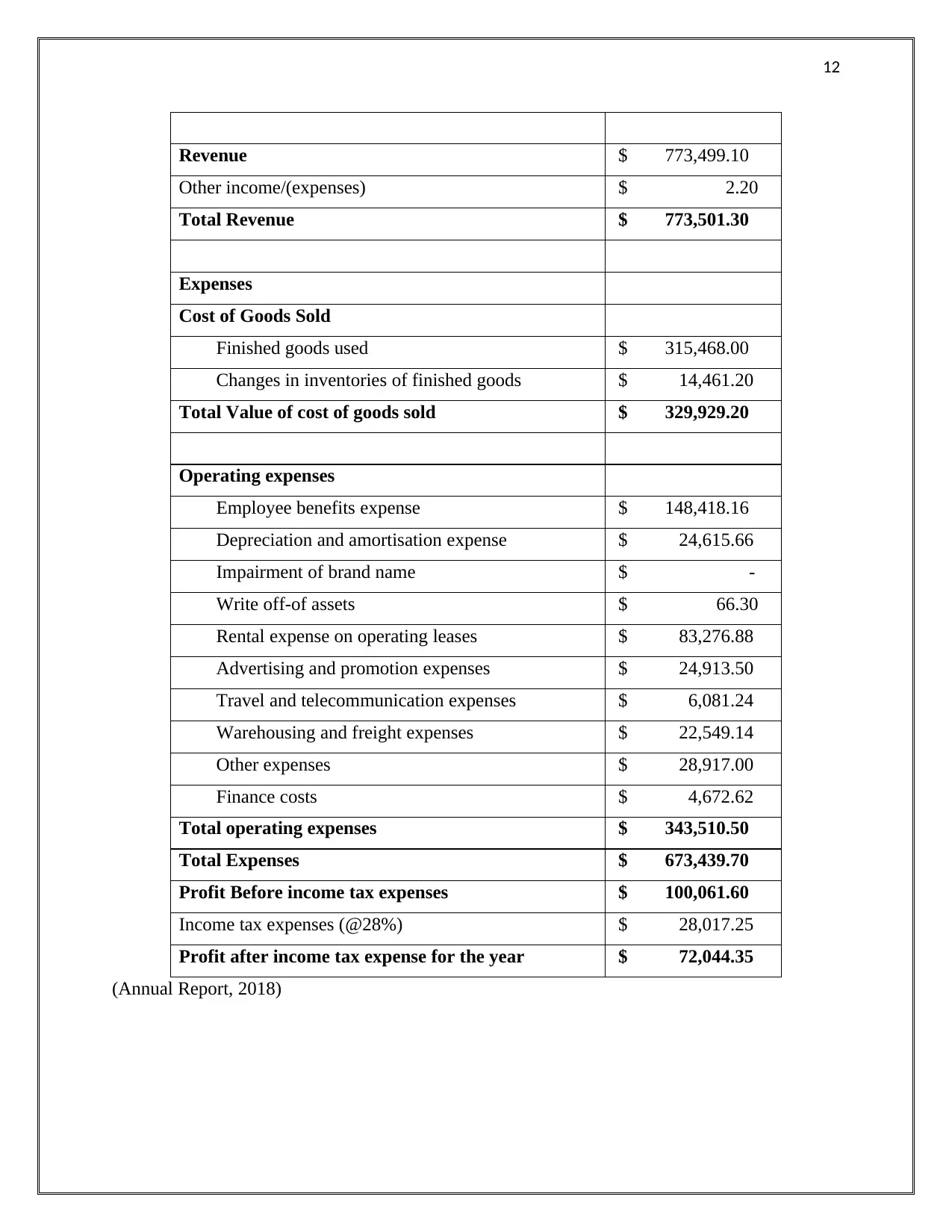

Revenue $ 773,499.10

Other income/(expenses) $ 2.20

Total Revenue $ 773,501.30

Expenses

Cost of Goods Sold

Finished goods used $ 315,468.00

Changes in inventories of finished goods $ 14,461.20

Total Value of cost of goods sold $ 329,929.20

Operating expenses

Employee benefits expense $ 148,418.16

Depreciation and amortisation expense $ 24,615.66

Impairment of brand name $ -

Write off-of assets $ 66.30

Rental expense on operating leases $ 83,276.88

Advertising and promotion expenses $ 24,913.50

Travel and telecommunication expenses $ 6,081.24

Warehousing and freight expenses $ 22,549.14

Other expenses $ 28,917.00

Finance costs $ 4,672.62

Total operating expenses $ 343,510.50

Total Expenses $ 673,439.70

Profit Before income tax expenses $ 100,061.60

Income tax expenses (@28%) $ 28,017.25

Profit after income tax expense for the year $ 72,044.35

(Annual Report, 2018)

Revenue $ 773,499.10

Other income/(expenses) $ 2.20

Total Revenue $ 773,501.30

Expenses

Cost of Goods Sold

Finished goods used $ 315,468.00

Changes in inventories of finished goods $ 14,461.20

Total Value of cost of goods sold $ 329,929.20

Operating expenses

Employee benefits expense $ 148,418.16

Depreciation and amortisation expense $ 24,615.66

Impairment of brand name $ -

Write off-of assets $ 66.30

Rental expense on operating leases $ 83,276.88

Advertising and promotion expenses $ 24,913.50

Travel and telecommunication expenses $ 6,081.24

Warehousing and freight expenses $ 22,549.14

Other expenses $ 28,917.00

Finance costs $ 4,672.62

Total operating expenses $ 343,510.50

Total Expenses $ 673,439.70

Profit Before income tax expenses $ 100,061.60

Income tax expenses (@28%) $ 28,017.25

Profit after income tax expense for the year $ 72,044.35

(Annual Report, 2018)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.