Managerial Accounting for Cost and Control: A Comprehensive Report

VerifiedAdded on 2020/02/24

|9

|1873

|39

Report

AI Summary

This report delves into various aspects of managerial accounting, beginning with the purpose of management accounting reports, emphasizing their role in communication, future referencing, budgeting, and inventory process efficiency. It then examines the control function of management, highlighting its significance in ensuring business alignment with expectations and facilitating effective decision-making. The report further explores product costing, detailing its importance in financial accounting, cost management, and reporting to the organization. It covers labor costing, including recording liabilities, distributing costs, and overtime premium treatment. Additionally, the report includes journal entries and an in-depth analysis of Activity Based Costing (ABC), discussing its arguments for and against implementation, ultimately recommending its use for effective inventory control and strategic decision-making. The report concludes with a comprehensive set of references.

RUNNING HEAD: Managerial accounting for cost and control

Managerial accounting for cost and

control

Managerial accounting for cost and

control

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Managerial accounting for cost and control

Table of Contents

Question 1.............................................................................................................................................3

Purpose of management accounting reports....................................................................................3

Question 2.............................................................................................................................................3

Control function of management......................................................................................................3

Question 3.............................................................................................................................................4

Purpose of product costing................................................................................................................4

Question 4.............................................................................................................................................5

A. Two aspects of labour costing...................................................................................................5

B. Overtime premium treatment...................................................................................................5

Question 5.............................................................................................................................................6

Journal entries...................................................................................................................................6

Question 6.............................................................................................................................................6

Introduction.......................................................................................................................................6

Arguments for ABC analysis...............................................................................................................7

Arguments against ABC analysis........................................................................................................7

Conclusion.........................................................................................................................................8

Recommendations.............................................................................................................................8

References.............................................................................................................................................9

Table of Contents

Question 1.............................................................................................................................................3

Purpose of management accounting reports....................................................................................3

Question 2.............................................................................................................................................3

Control function of management......................................................................................................3

Question 3.............................................................................................................................................4

Purpose of product costing................................................................................................................4

Question 4.............................................................................................................................................5

A. Two aspects of labour costing...................................................................................................5

B. Overtime premium treatment...................................................................................................5

Question 5.............................................................................................................................................6

Journal entries...................................................................................................................................6

Question 6.............................................................................................................................................6

Introduction.......................................................................................................................................6

Arguments for ABC analysis...............................................................................................................7

Arguments against ABC analysis........................................................................................................7

Conclusion.........................................................................................................................................8

Recommendations.............................................................................................................................8

References.............................................................................................................................................9

Managerial accounting for cost and control

Question 1

Purpose of management accounting reports:

Means of communication: Management reports are used for upward communication. It is

made for use by internal users. Examples are management, government agencies, creditors

and many more uses the report to know about inside condition of organization (Garrison, et

al., 2010).

Record for future: The reports provide valuable and significant information that can be used

as reference in future. Due to this data is collected with maximum care to become source of

information in future.

Prepare budget: Managers analyse department’s performance in order to control cost. The

managers prepare budget in order to estimate expenses and income over a future period of

time. A manager also uses these reports to provide incentive and increment to its employees.

From budget reports analysis for future goals and budgets is prepared.

Inventory process efficiency: Companies having physical inventory system uses managerial

accounting reports to keep their manufacturing process effective. The reports prepared shows

the labour hour wasted, overhead cost and many more which helps company to analyse

profitable department and areas needing improvement.

Question 2

Control function of management:

Controlling as function of management is of significant value in business

organization. It assures of the actual state of business condition is parallel to expectation. It

also gives the exact data needed for effective decision making process and maintaining

Question 1

Purpose of management accounting reports:

Means of communication: Management reports are used for upward communication. It is

made for use by internal users. Examples are management, government agencies, creditors

and many more uses the report to know about inside condition of organization (Garrison, et

al., 2010).

Record for future: The reports provide valuable and significant information that can be used

as reference in future. Due to this data is collected with maximum care to become source of

information in future.

Prepare budget: Managers analyse department’s performance in order to control cost. The

managers prepare budget in order to estimate expenses and income over a future period of

time. A manager also uses these reports to provide incentive and increment to its employees.

From budget reports analysis for future goals and budgets is prepared.

Inventory process efficiency: Companies having physical inventory system uses managerial

accounting reports to keep their manufacturing process effective. The reports prepared shows

the labour hour wasted, overhead cost and many more which helps company to analyse

profitable department and areas needing improvement.

Question 2

Control function of management:

Controlling as function of management is of significant value in business

organization. It assures of the actual state of business condition is parallel to expectation. It

also gives the exact data needed for effective decision making process and maintaining

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Managerial accounting for cost and control

healthy state of business (Granlund, 2011). Controlling function is used to offer timely

encourage and key to manage people in business. Control is not restricted to decide if the

plans are being inclined to, yet it also prompts recognizing the reasons of deviations and to

take remedial practices accordingly. It is the process by which actions are directed to produce

better results and ways are improved to promote outcomes. Controlling also eliminates the

obstacles resent and upcoming in path of business. It has great uses on areas which require

immediate action. Controlling is also targeted at effectiveness, efficiency and better

outcomes. Controlling can lead an organization to survive in difficult time, attain sustainable

development and many more.

Question 3:

Purpose of product costing:

Reporting to organization: It refers to business effectiveness in monitoring expenses through

product cost and inventory control. The accuracy in product costing helps increasing

correctness in variable costing (Fisher & Krumwiede, 2012). This also helps in administering

the matching principle, combining cost to value, and creating value of business.

Financial accounting: Product costing helps in decision making in financial statement. It

mainly involves return on investment and profit earning capacity for an organization. For

example variable costing is used to know the expenses that vary with changing level of

output and profitability of contract can be determined. Hence product costing acts as a

decision making tool for these decisions.

Cost management: It refers to development of new products. When an organization is

planning to enter into new product line or innovate some of existing products then product

costing act as a valuable resource. This allows business to add some specific cost not only in

healthy state of business (Granlund, 2011). Controlling function is used to offer timely

encourage and key to manage people in business. Control is not restricted to decide if the

plans are being inclined to, yet it also prompts recognizing the reasons of deviations and to

take remedial practices accordingly. It is the process by which actions are directed to produce

better results and ways are improved to promote outcomes. Controlling also eliminates the

obstacles resent and upcoming in path of business. It has great uses on areas which require

immediate action. Controlling is also targeted at effectiveness, efficiency and better

outcomes. Controlling can lead an organization to survive in difficult time, attain sustainable

development and many more.

Question 3:

Purpose of product costing:

Reporting to organization: It refers to business effectiveness in monitoring expenses through

product cost and inventory control. The accuracy in product costing helps increasing

correctness in variable costing (Fisher & Krumwiede, 2012). This also helps in administering

the matching principle, combining cost to value, and creating value of business.

Financial accounting: Product costing helps in decision making in financial statement. It

mainly involves return on investment and profit earning capacity for an organization. For

example variable costing is used to know the expenses that vary with changing level of

output and profitability of contract can be determined. Hence product costing acts as a

decision making tool for these decisions.

Cost management: It refers to development of new products. When an organization is

planning to enter into new product line or innovate some of existing products then product

costing act as a valuable resource. This allows business to add some specific cost not only in

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Managerial accounting for cost and control

product but also to material, labour and many more to enable accurate calculation of product

cost.

Managerial accounting: Product costs are those which are necessary to produce a product.

Product cost composes of direct material, production overhead and direct labour cost (Wyatt

& Frick 2010). It also helps in determining actual expenses incurred during a period for

manufacturing a product. After knowing a product cost, sale prices and future profit can

easily be estimated.

Question 4:

A. Two aspects of labour costing:

1. Recording liability and distributing labour costs: In this labour cost will recorded as

business liability. It allows flexibility to manage the allocation of payroll expenses

among different departments. It also can be assigned to special project and determine

profit. It gives the idea where the department is lacking due to labour control

measures and decide which department is giving result.

2. Payment of labour: During payment of labour direct labour A/c is debited and cash

A/c is credited.

B. Overtime premium treatment:

Overtime premiums is considered as direct labor costs, if it is at the specific request of

a client because they want a job to be finished in lesser time the process usually takes

(Hart & Ma, 2010). Because where overtime is worked on some specific requirement

to meet urgent target for which customer paid extra money as well. Then complete

labor cost is charged as direct labor cost.

product but also to material, labour and many more to enable accurate calculation of product

cost.

Managerial accounting: Product costs are those which are necessary to produce a product.

Product cost composes of direct material, production overhead and direct labour cost (Wyatt

& Frick 2010). It also helps in determining actual expenses incurred during a period for

manufacturing a product. After knowing a product cost, sale prices and future profit can

easily be estimated.

Question 4:

A. Two aspects of labour costing:

1. Recording liability and distributing labour costs: In this labour cost will recorded as

business liability. It allows flexibility to manage the allocation of payroll expenses

among different departments. It also can be assigned to special project and determine

profit. It gives the idea where the department is lacking due to labour control

measures and decide which department is giving result.

2. Payment of labour: During payment of labour direct labour A/c is debited and cash

A/c is credited.

B. Overtime premium treatment:

Overtime premiums is considered as direct labor costs, if it is at the specific request of

a client because they want a job to be finished in lesser time the process usually takes

(Hart & Ma, 2010). Because where overtime is worked on some specific requirement

to meet urgent target for which customer paid extra money as well. Then complete

labor cost is charged as direct labor cost.

Managerial accounting for cost and control

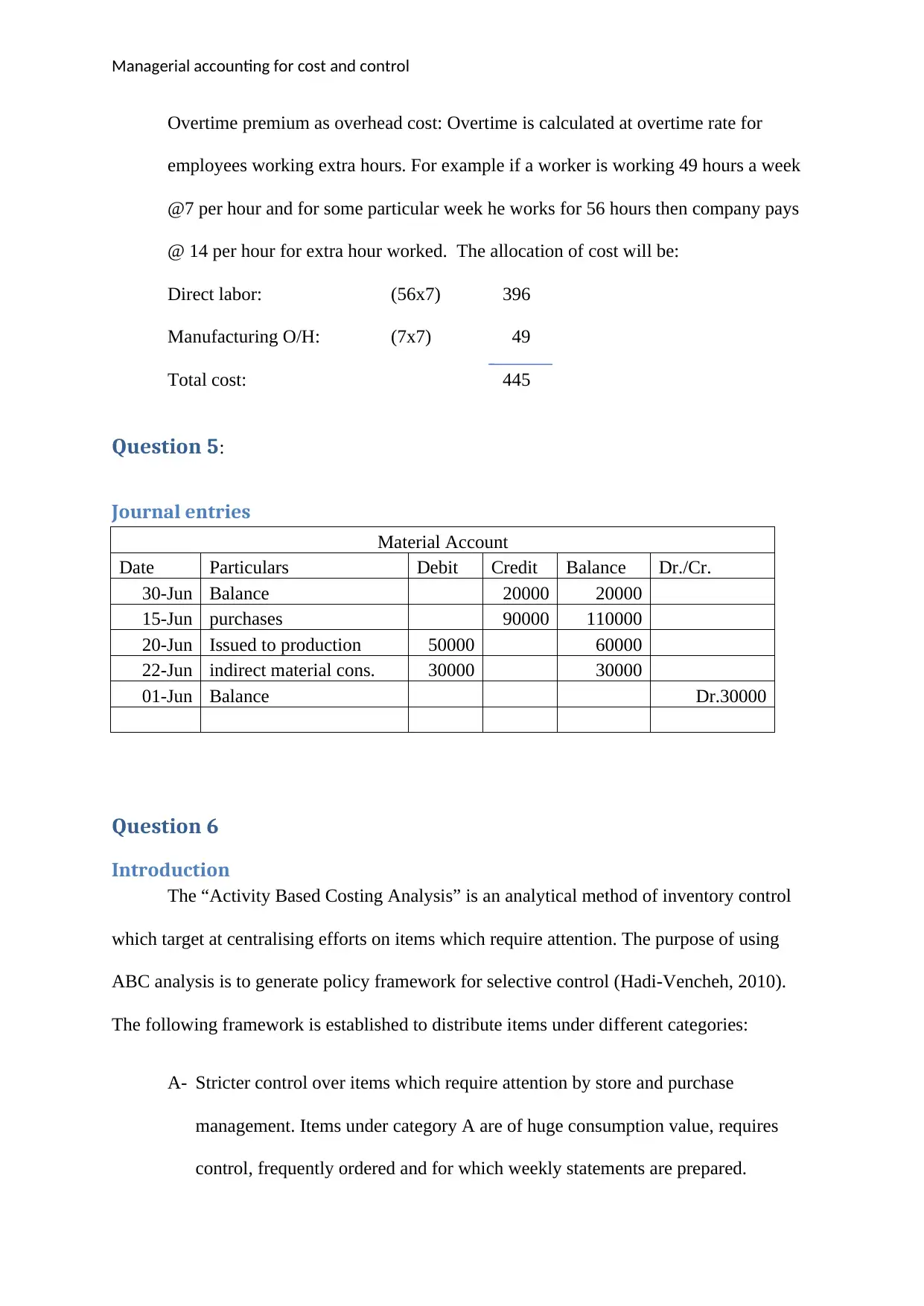

Overtime premium as overhead cost: Overtime is calculated at overtime rate for

employees working extra hours. For example if a worker is working 49 hours a week

@7 per hour and for some particular week he works for 56 hours then company pays

@ 14 per hour for extra hour worked. The allocation of cost will be:

Direct labor: (56x7) 396

Manufacturing O/H: (7x7) 49

Total cost: 445

Question 5:

Journal entries

Material Account

Date Particulars Debit Credit Balance Dr./Cr.

30-Jun Balance 20000 20000

15-Jun purchases 90000 110000

20-Jun Issued to production 50000 60000

22-Jun indirect material cons. 30000 30000

01-Jun Balance Dr.30000

Question 6

Introduction

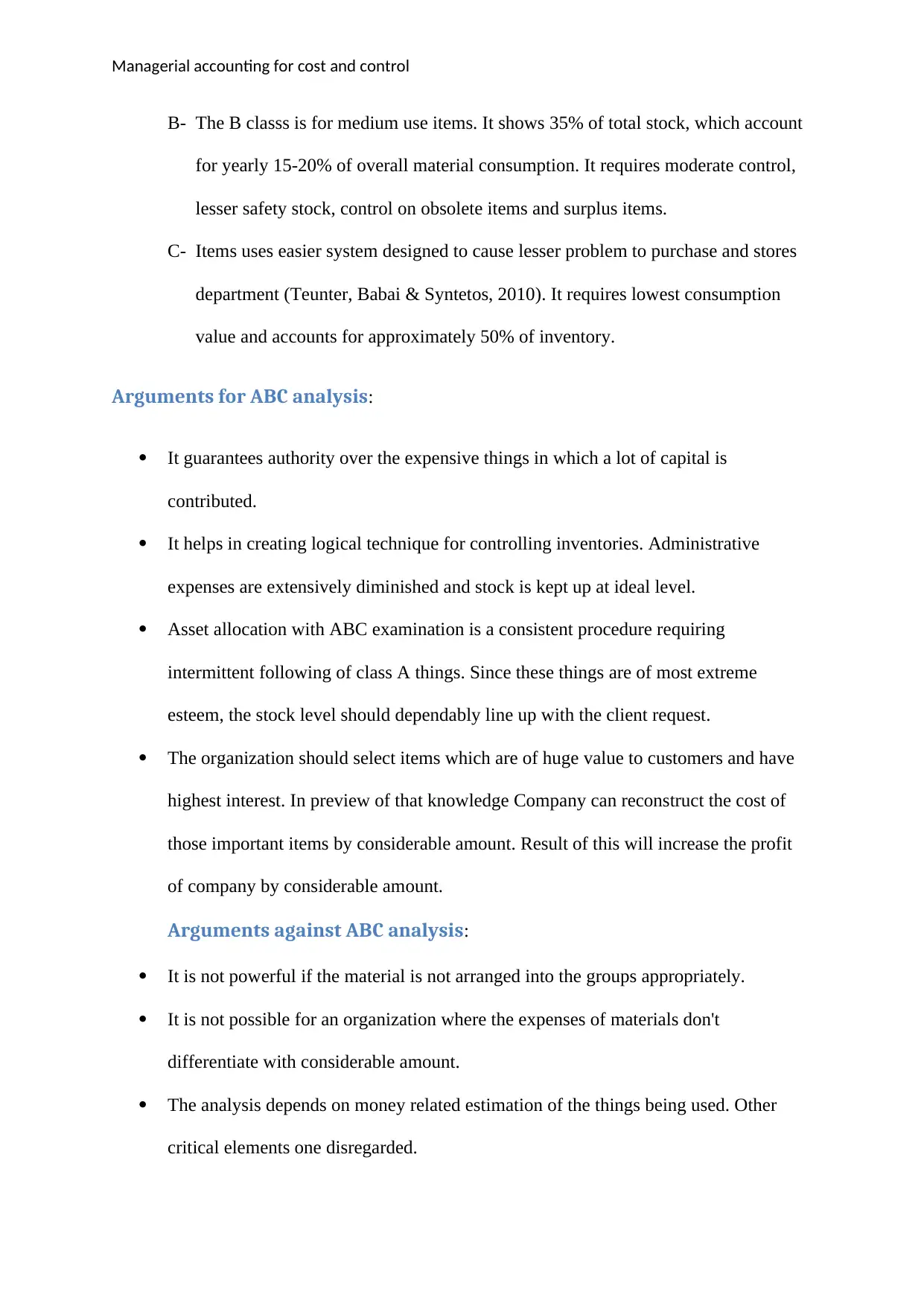

The “Activity Based Costing Analysis” is an analytical method of inventory control

which target at centralising efforts on items which require attention. The purpose of using

ABC analysis is to generate policy framework for selective control (Hadi-Vencheh, 2010).

The following framework is established to distribute items under different categories:

A- Stricter control over items which require attention by store and purchase

management. Items under category A are of huge consumption value, requires

control, frequently ordered and for which weekly statements are prepared.

Overtime premium as overhead cost: Overtime is calculated at overtime rate for

employees working extra hours. For example if a worker is working 49 hours a week

@7 per hour and for some particular week he works for 56 hours then company pays

@ 14 per hour for extra hour worked. The allocation of cost will be:

Direct labor: (56x7) 396

Manufacturing O/H: (7x7) 49

Total cost: 445

Question 5:

Journal entries

Material Account

Date Particulars Debit Credit Balance Dr./Cr.

30-Jun Balance 20000 20000

15-Jun purchases 90000 110000

20-Jun Issued to production 50000 60000

22-Jun indirect material cons. 30000 30000

01-Jun Balance Dr.30000

Question 6

Introduction

The “Activity Based Costing Analysis” is an analytical method of inventory control

which target at centralising efforts on items which require attention. The purpose of using

ABC analysis is to generate policy framework for selective control (Hadi-Vencheh, 2010).

The following framework is established to distribute items under different categories:

A- Stricter control over items which require attention by store and purchase

management. Items under category A are of huge consumption value, requires

control, frequently ordered and for which weekly statements are prepared.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Managerial accounting for cost and control

B- The B classs is for medium use items. It shows 35% of total stock, which account

for yearly 15-20% of overall material consumption. It requires moderate control,

lesser safety stock, control on obsolete items and surplus items.

C- Items uses easier system designed to cause lesser problem to purchase and stores

department (Teunter, Babai & Syntetos, 2010). It requires lowest consumption

value and accounts for approximately 50% of inventory.

Arguments for ABC analysis:

It guarantees authority over the expensive things in which a lot of capital is

contributed.

It helps in creating logical technique for controlling inventories. Administrative

expenses are extensively diminished and stock is kept up at ideal level.

Asset allocation with ABC examination is a consistent procedure requiring

intermittent following of class A things. Since these things are of most extreme

esteem, the stock level should dependably line up with the client request.

The organization should select items which are of huge value to customers and have

highest interest. In preview of that knowledge Company can reconstruct the cost of

those important items by considerable amount. Result of this will increase the profit

of company by considerable amount.

Arguments against ABC analysis:

It is not powerful if the material is not arranged into the groups appropriately.

It is not possible for an organization where the expenses of materials don't

differentiate with considerable amount.

The analysis depends on money related estimation of the things being used. Other

critical elements one disregarded.

B- The B classs is for medium use items. It shows 35% of total stock, which account

for yearly 15-20% of overall material consumption. It requires moderate control,

lesser safety stock, control on obsolete items and surplus items.

C- Items uses easier system designed to cause lesser problem to purchase and stores

department (Teunter, Babai & Syntetos, 2010). It requires lowest consumption

value and accounts for approximately 50% of inventory.

Arguments for ABC analysis:

It guarantees authority over the expensive things in which a lot of capital is

contributed.

It helps in creating logical technique for controlling inventories. Administrative

expenses are extensively diminished and stock is kept up at ideal level.

Asset allocation with ABC examination is a consistent procedure requiring

intermittent following of class A things. Since these things are of most extreme

esteem, the stock level should dependably line up with the client request.

The organization should select items which are of huge value to customers and have

highest interest. In preview of that knowledge Company can reconstruct the cost of

those important items by considerable amount. Result of this will increase the profit

of company by considerable amount.

Arguments against ABC analysis:

It is not powerful if the material is not arranged into the groups appropriately.

It is not possible for an organization where the expenses of materials don't

differentiate with considerable amount.

The analysis depends on money related estimation of the things being used. Other

critical elements one disregarded.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Managerial accounting for cost and control

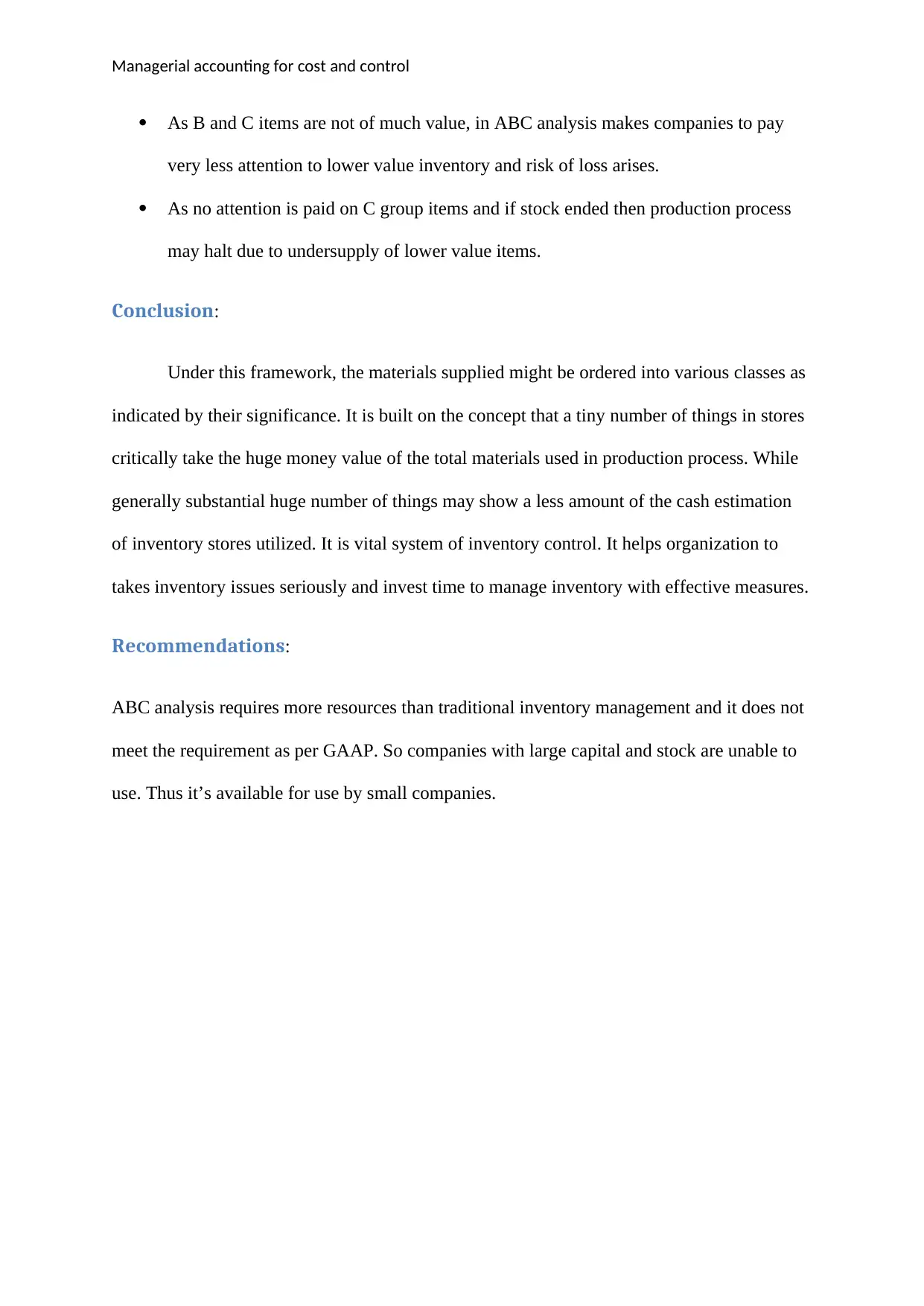

As B and C items are not of much value, in ABC analysis makes companies to pay

very less attention to lower value inventory and risk of loss arises.

As no attention is paid on C group items and if stock ended then production process

may halt due to undersupply of lower value items.

Conclusion:

Under this framework, the materials supplied might be ordered into various classes as

indicated by their significance. It is built on the concept that a tiny number of things in stores

critically take the huge money value of the total materials used in production process. While

generally substantial huge number of things may show a less amount of the cash estimation

of inventory stores utilized. It is vital system of inventory control. It helps organization to

takes inventory issues seriously and invest time to manage inventory with effective measures.

Recommendations:

ABC analysis requires more resources than traditional inventory management and it does not

meet the requirement as per GAAP. So companies with large capital and stock are unable to

use. Thus it’s available for use by small companies.

As B and C items are not of much value, in ABC analysis makes companies to pay

very less attention to lower value inventory and risk of loss arises.

As no attention is paid on C group items and if stock ended then production process

may halt due to undersupply of lower value items.

Conclusion:

Under this framework, the materials supplied might be ordered into various classes as

indicated by their significance. It is built on the concept that a tiny number of things in stores

critically take the huge money value of the total materials used in production process. While

generally substantial huge number of things may show a less amount of the cash estimation

of inventory stores utilized. It is vital system of inventory control. It helps organization to

takes inventory issues seriously and invest time to manage inventory with effective measures.

Recommendations:

ABC analysis requires more resources than traditional inventory management and it does not

meet the requirement as per GAAP. So companies with large capital and stock are unable to

use. Thus it’s available for use by small companies.

Managerial accounting for cost and control

References:

Fisher, J. G., & Krumwiede, K. (2012). Product costing systems: Finding the right

approach. Journal of Corporate Accounting & Finance, 23(3), 43-51.

Garrison, R. H., Noreen, E. W., Brewer, P. C., & McGowan, A. (2010). Managerial

accounting. Issues in Accounting Education, 25(4), 792-793.

Granlund, M. (2011). Extending AIS research to management accounting and control issues:

A research note. International Journal of Accounting Information Systems, 12(1), 3-

19.

Hadi-Vencheh, A. (2010). An improvement to multiple criteria ABC inventory

classification. European Journal of Operational Research, 201(3), 962-965.

Hart, R. A., & Ma, Y. (2010). Wage–hours contracts, overtime working and premium

pay. Labour Economics, 17(1), 170-179.

Teunter, R. H., Babai, M. Z., & Syntetos, A. A. (2010). ABC classification: service levels

and inventory costs. Production and Operations Management, 19(3), 343-352.

Wyatt, A., & Frick, H. (2010). Accounting for issnvestments in human capital: A

review. Australian Accounting Review, 20(3), 199-220.

Yu, M. C. (2011). Multi-criteria ABC analysis using artificial-intelligence-based

classification techniques. Expert Systems with Applications, 38(4), 3416-3421.

References:

Fisher, J. G., & Krumwiede, K. (2012). Product costing systems: Finding the right

approach. Journal of Corporate Accounting & Finance, 23(3), 43-51.

Garrison, R. H., Noreen, E. W., Brewer, P. C., & McGowan, A. (2010). Managerial

accounting. Issues in Accounting Education, 25(4), 792-793.

Granlund, M. (2011). Extending AIS research to management accounting and control issues:

A research note. International Journal of Accounting Information Systems, 12(1), 3-

19.

Hadi-Vencheh, A. (2010). An improvement to multiple criteria ABC inventory

classification. European Journal of Operational Research, 201(3), 962-965.

Hart, R. A., & Ma, Y. (2010). Wage–hours contracts, overtime working and premium

pay. Labour Economics, 17(1), 170-179.

Teunter, R. H., Babai, M. Z., & Syntetos, A. A. (2010). ABC classification: service levels

and inventory costs. Production and Operations Management, 19(3), 343-352.

Wyatt, A., & Frick, H. (2010). Accounting for issnvestments in human capital: A

review. Australian Accounting Review, 20(3), 199-220.

Yu, M. C. (2011). Multi-criteria ABC analysis using artificial-intelligence-based

classification techniques. Expert Systems with Applications, 38(4), 3416-3421.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.