Managerial Economics Assignment: Supply, Demand, Elasticity, and Costs

VerifiedAdded on 2020/04/21

|10

|1048

|444

Homework Assignment

AI Summary

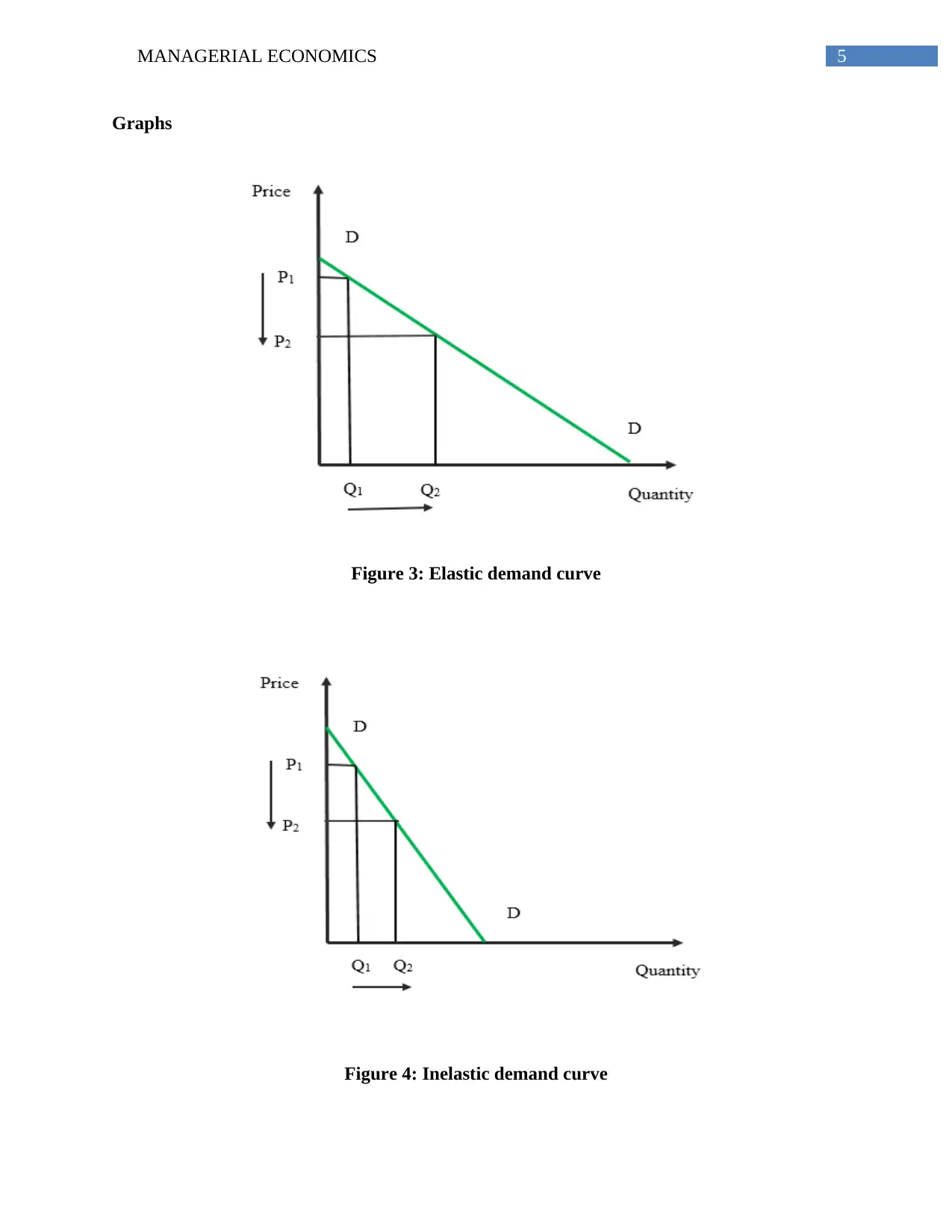

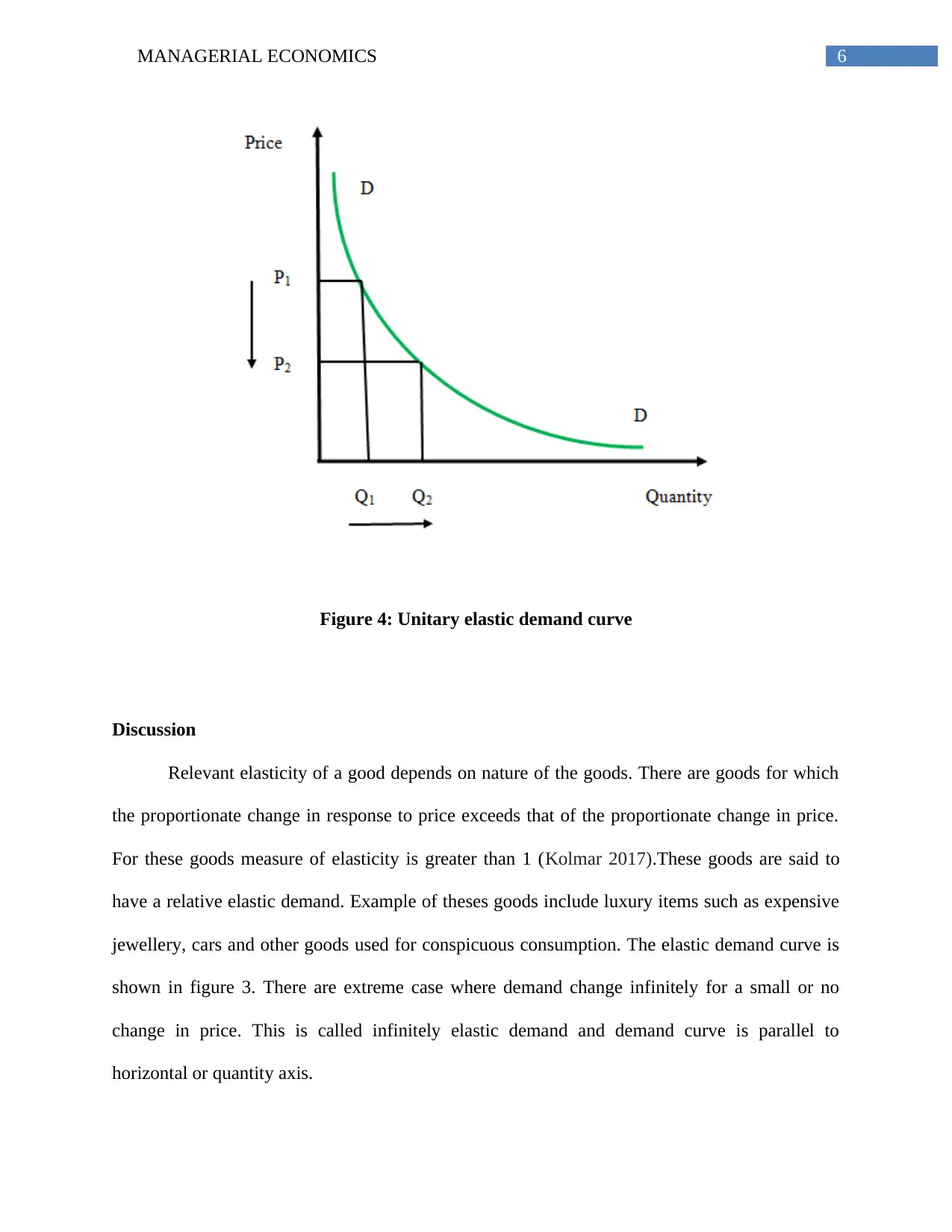

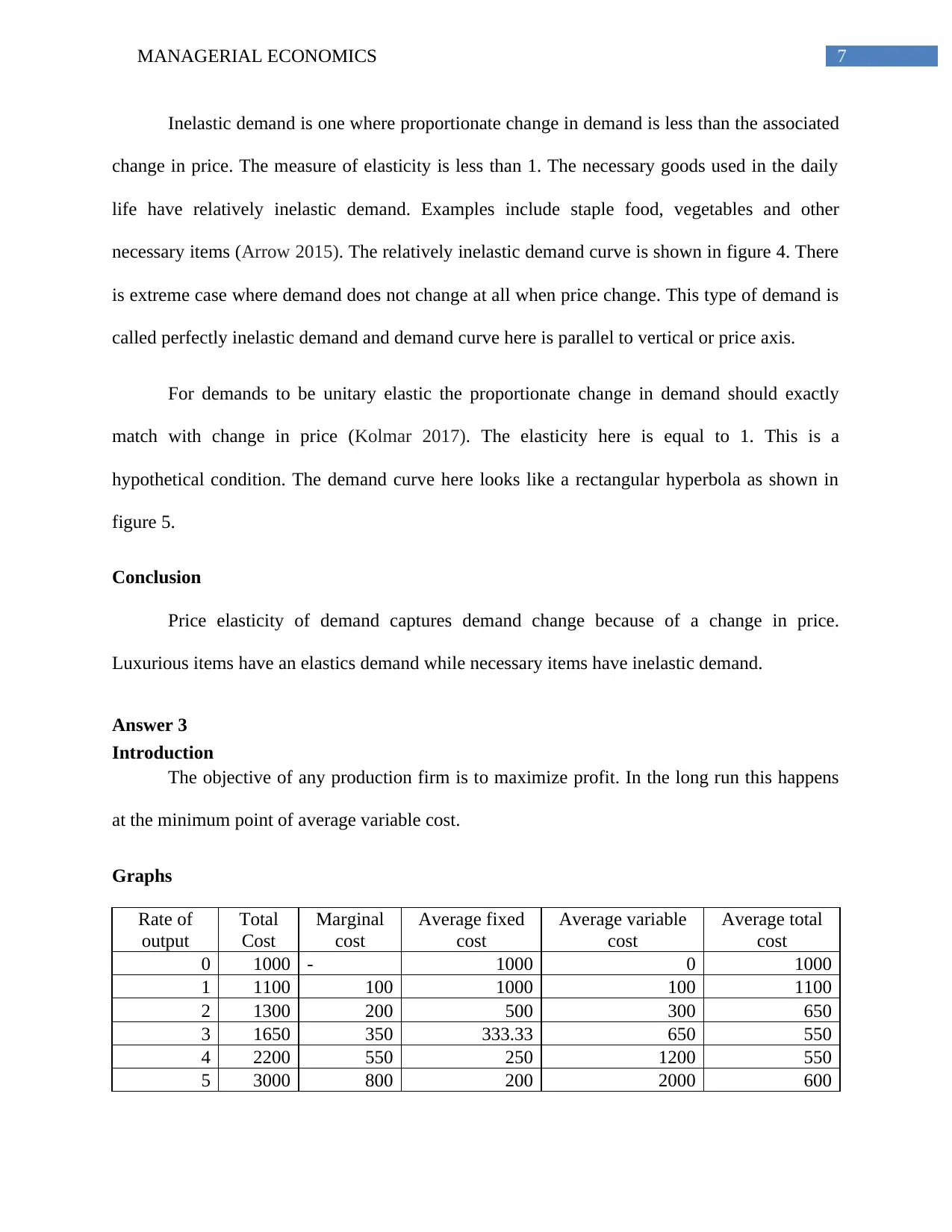

This managerial economics assignment analyzes key economic concepts. It begins with an introduction to market equilibrium, explaining how demand and supply interact to determine prices and quantities, and illustrates these concepts with graphs. The assignment then delves into price elasticity of demand, differentiating between elastic, inelastic, and unitary elastic demands, with graphical representations of each. Finally, the assignment concludes with an examination of cost functions and production, aiming to maximize profit, and presents a cost schedule to determine the minimum average total cost and the optimal output level. This assignment offers a comprehensive overview of core microeconomic principles relevant to managerial decision-making.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.