Managerial Economics: OPEC, Demand, Supply and Market Analysis

VerifiedAdded on 2023/06/13

|12

|2802

|195

Report

AI Summary

This report provides a detailed analysis of several key concepts in managerial economics. It begins by examining the decisions made at a recent OPEC meeting and their subsequent impact on global oil supply and demand, considering factors such as production restrictions, public transport closures due to COVID-19, advancements in electric battery technology, and the discovery of new oil fields. The report then explores how changes in the number of entrepreneurs and consumers affect demand curves, followed by an explanation of the impact of price ceilings on heating gas prices in Europe. Furthermore, it calculates and analyzes equilibrium prices and quantities in a restaurant setting, including scenarios with cost reductions. The report also includes cost analysis, calculating total cost, average variable cost, average total cost, and marginal cost. Finally, the report critically evaluates the characteristics and equilibrium points of perfect competition, discussing shutdown points and equilibrium situations, highlighting the theoretical aspects and real-world limitations of this market structure. Students can find similar solved assignments and resources on Desklib.

Managerial Economics

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Contents...........................................................................................................................................2

INTRODUCTION...........................................................................................................................3

Main Body.......................................................................................................................................3

1. Discussion on the OPEC meeting and its impact on demand and supply...............................3

2. Explain the changes in the demand curve because of the changes in the number of

entrepreneurs and customers........................................................................................................4

3. Explaining the impact of price ceiling on the price of heating gas in Europe.........................5

4. Explain the equilibrium price and new equilibrium price and Quantity after deducting $15

million at every Cost....................................................................................................................6

5. Find out the Total Cost, Average Variable Cost, Average Total Cost, and Marginal Cost.. . .7

6. Characteristics of perfect competition.....................................................................................8

7. Critical evaluation of equilibrium point in perfect competition..............................................9

a.) Description of shutting down point when marginal revenue is less than the Average Cost.. 9

b.) Explaining the situation of Equilibrium in the perfect competition market...........................9

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

Contents...........................................................................................................................................2

INTRODUCTION...........................................................................................................................3

Main Body.......................................................................................................................................3

1. Discussion on the OPEC meeting and its impact on demand and supply...............................3

2. Explain the changes in the demand curve because of the changes in the number of

entrepreneurs and customers........................................................................................................4

3. Explaining the impact of price ceiling on the price of heating gas in Europe.........................5

4. Explain the equilibrium price and new equilibrium price and Quantity after deducting $15

million at every Cost....................................................................................................................6

5. Find out the Total Cost, Average Variable Cost, Average Total Cost, and Marginal Cost.. . .7

6. Characteristics of perfect competition.....................................................................................8

7. Critical evaluation of equilibrium point in perfect competition..............................................9

a.) Description of shutting down point when marginal revenue is less than the Average Cost.. 9

b.) Explaining the situation of Equilibrium in the perfect competition market...........................9

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION

Managerial economics is the study and application of economic concepts and theories. This

report contains the decisions of the OPEC meeting which was conducted recently. It also

includes studying the equilibrium price and Quantity of the restaurants. Price celling is a

concept introduced by the government to safeguard the suppliers. It is a measure to control

the costs. The idea of the same is also discussed in the report. There are several forms of

market structure, but precisely perfect competition and its Equilibrium are elaborated in the

report.

Main Body

1. Discussion on the OPEC meeting and its impact on demand and supply

OPEC stands for the organization for petroleum exporting countries; recently, the

organization has taken some decisions regarding the global pandemic. The OPEC meeting

discusses the following points and there is an effect on demand and supply which can be

understood from the following points.

a.) Decision related to restriction of production

In OPEC meeting, there are several issues were discussed. One of the major issue was the

activities of productions declined at the time of Covid-19. There was decline in the demand

of oil and petroleum because movement of people from one place to another also

minimised. Therefore, price of the petroleum also falls.

b.) Discussion on the public transport closure.

At the time of covid-19, supply of the public transport reduced by the manufacturers

because there was no sense of public transport, the lock down has stopped the movement

of the public. Therefore, the supply curve shifts leftwards.

c.) Electric batteries technology has recently undergone significant improvements in terms

of durability (longer autonomy).

In case of substitute goods, demand of electric vehicles increased because introduction of

new technology is required to increase the sales of the organisation and demand of petrol

Managerial economics is the study and application of economic concepts and theories. This

report contains the decisions of the OPEC meeting which was conducted recently. It also

includes studying the equilibrium price and Quantity of the restaurants. Price celling is a

concept introduced by the government to safeguard the suppliers. It is a measure to control

the costs. The idea of the same is also discussed in the report. There are several forms of

market structure, but precisely perfect competition and its Equilibrium are elaborated in the

report.

Main Body

1. Discussion on the OPEC meeting and its impact on demand and supply

OPEC stands for the organization for petroleum exporting countries; recently, the

organization has taken some decisions regarding the global pandemic. The OPEC meeting

discusses the following points and there is an effect on demand and supply which can be

understood from the following points.

a.) Decision related to restriction of production

In OPEC meeting, there are several issues were discussed. One of the major issue was the

activities of productions declined at the time of Covid-19. There was decline in the demand

of oil and petroleum because movement of people from one place to another also

minimised. Therefore, price of the petroleum also falls.

b.) Discussion on the public transport closure.

At the time of covid-19, supply of the public transport reduced by the manufacturers

because there was no sense of public transport, the lock down has stopped the movement

of the public. Therefore, the supply curve shifts leftwards.

c.) Electric batteries technology has recently undergone significant improvements in terms

of durability (longer autonomy).

In case of substitute goods, demand of electric vehicles increased because introduction of

new technology is required to increase the sales of the organisation and demand of petrol

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

declines due to the introduction of new electric batteries. These electric batteries reduce the

pollution from the environment. Therefore, the demand curve shifts leftwards.

d.) Introduction of new oil fields on the coast of Africa.

With the introduction of new oil fields at the coast of Africa, in the starting phase of the

trading they were not in a position to sell their petroleum products at a good price. In the

beginning year, they have to use price skimming approach in which manufacturer uses

very low prices in comparison to its competitors to achieve the level of desired sales.

2. Explain the changes in the demand curve because of the changes in the number of

entrepreneurs and customers.

Demand Curve shows changes in the Quantity Demanded with the difference in the price

of a commodity. An increase in the costs of a thing causes a decrease in the Quantity

Demanded, and if the price of an item decreases, then Quantity demanded of the product

increases. An increase in the number of entrepreneurs implies that the buyers will get more

options to choose from in the market (Baker, Kumar, and Pandey, 2020). This increases

the possibilities for the buyers so does for the sellers. More sellers in the market will lower

the price per unit. The seller will provide the product at a lower cost to sell more than the

other sellers. This will help the buyer in buying the product at a lower price. The

equilibrium price of the product will come down because of the increase in the competition

in the market (Pan, Liu, and Wang,2019.).

pollution from the environment. Therefore, the demand curve shifts leftwards.

d.) Introduction of new oil fields on the coast of Africa.

With the introduction of new oil fields at the coast of Africa, in the starting phase of the

trading they were not in a position to sell their petroleum products at a good price. In the

beginning year, they have to use price skimming approach in which manufacturer uses

very low prices in comparison to its competitors to achieve the level of desired sales.

2. Explain the changes in the demand curve because of the changes in the number of

entrepreneurs and customers.

Demand Curve shows changes in the Quantity Demanded with the difference in the price

of a commodity. An increase in the costs of a thing causes a decrease in the Quantity

Demanded, and if the price of an item decreases, then Quantity demanded of the product

increases. An increase in the number of entrepreneurs implies that the buyers will get more

options to choose from in the market (Baker, Kumar, and Pandey, 2020). This increases

the possibilities for the buyers so does for the sellers. More sellers in the market will lower

the price per unit. The seller will provide the product at a lower cost to sell more than the

other sellers. This will help the buyer in buying the product at a lower price. The

equilibrium price of the product will come down because of the increase in the competition

in the market (Pan, Liu, and Wang,2019.).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

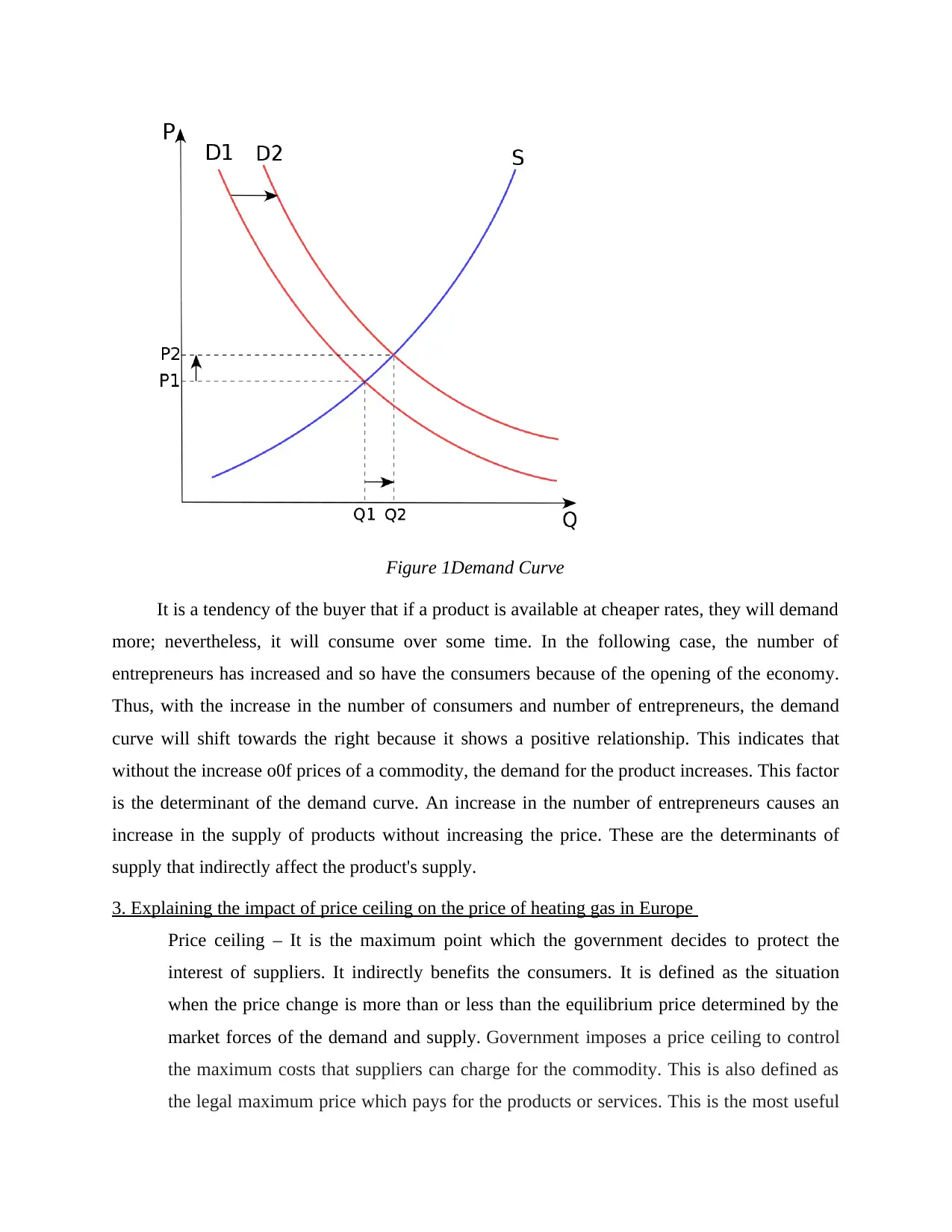

Figure 1Demand Curve

It is a tendency of the buyer that if a product is available at cheaper rates, they will demand

more; nevertheless, it will consume over some time. In the following case, the number of

entrepreneurs has increased and so have the consumers because of the opening of the economy.

Thus, with the increase in the number of consumers and number of entrepreneurs, the demand

curve will shift towards the right because it shows a positive relationship. This indicates that

without the increase o0f prices of a commodity, the demand for the product increases. This factor

is the determinant of the demand curve. An increase in the number of entrepreneurs causes an

increase in the supply of products without increasing the price. These are the determinants of

supply that indirectly affect the product's supply.

3. Explaining the impact of price ceiling on the price of heating gas in Europe

Price ceiling – It is the maximum point which the government decides to protect the

interest of suppliers. It indirectly benefits the consumers. It is defined as the situation

when the price change is more than or less than the equilibrium price determined by the

market forces of the demand and supply. Government imposes a price ceiling to control

the maximum costs that suppliers can charge for the commodity. This is also defined as

the legal maximum price which pays for the products or services. This is the most useful

It is a tendency of the buyer that if a product is available at cheaper rates, they will demand

more; nevertheless, it will consume over some time. In the following case, the number of

entrepreneurs has increased and so have the consumers because of the opening of the economy.

Thus, with the increase in the number of consumers and number of entrepreneurs, the demand

curve will shift towards the right because it shows a positive relationship. This indicates that

without the increase o0f prices of a commodity, the demand for the product increases. This factor

is the determinant of the demand curve. An increase in the number of entrepreneurs causes an

increase in the supply of products without increasing the price. These are the determinants of

supply that indirectly affect the product's supply.

3. Explaining the impact of price ceiling on the price of heating gas in Europe

Price ceiling – It is the maximum point which the government decides to protect the

interest of suppliers. It indirectly benefits the consumers. It is defined as the situation

when the price change is more than or less than the equilibrium price determined by the

market forces of the demand and supply. Government imposes a price ceiling to control

the maximum costs that suppliers can charge for the commodity. This is also defined as

the legal maximum price which pays for the products or services. This is the most useful

and great in the house rent market. This is imposed by the government in order to control

the maximum prices which can be charged by the suppliers for the commodity.

Equilibrium price – It is a situation where quantity demand and supplied are matched at the same

point (Gack,, 2018.). In simple words, if 10 units are supplied and the same is demanded by the

consumers is known as equilibrium point.

4. Explain the equilibrium price and new equilibrium price and Quantity after deducting $15

million at every Cost.

Price Per Gallon Quantity Supplied Quantity demanded

$50 130 170

$60 135 150

$70 140 140

$80 145 135

$90 150 125

$100 155 110

Equilibrium is the point where the Quantity demanded and Quantity supplied of a commodity

equals, which means that it is a price where Quantity required by the consumer equals the

Quantity provided by the supplier of an item. This is the position where the buyer at the suppler

the maximum prices which can be charged by the suppliers for the commodity.

Equilibrium price – It is a situation where quantity demand and supplied are matched at the same

point (Gack,, 2018.). In simple words, if 10 units are supplied and the same is demanded by the

consumers is known as equilibrium point.

4. Explain the equilibrium price and new equilibrium price and Quantity after deducting $15

million at every Cost.

Price Per Gallon Quantity Supplied Quantity demanded

$50 130 170

$60 135 150

$70 140 140

$80 145 135

$90 150 125

$100 155 110

Equilibrium is the point where the Quantity demanded and Quantity supplied of a commodity

equals, which means that it is a price where Quantity required by the consumer equals the

Quantity provided by the supplier of an item. This is the position where the buyer at the suppler

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

of the product gets the maximum benefit from the consumption of the product as well as suppler

gets a point the supplier can supply their there product the most. The following equilibrium point

is for $70, where the Quantity demanded by the consumers of the commodity equals the Quantity

required by the supplier of the petrol ( Li, Monroe, and Coulton,2018).

Change in the demand curve because of reduction in the price of petrol.

Price Per Gallon Quantity Supplied Quantity demanded

$50 130 155

$60 135 135

$70 140 125

$80 145 120

$90 150 110

$100 155 95

The changes can see the impact of change in price of petrol in the Quantity demanded by the

consumer as the price of the commodity decreases the demand of the commodity increases and if

the costs of a commodity decreases then the Quantity demanded of the product decreases. With

the decline in the Quantity demanded of petrol, the Equilibrium of the given set of data has also

shifted to $60, which means the buyer will tends to purchase more at this price level (Khaki and

et.al., 2021). The Equilibrium is the price where any individual is ready to buy the product as so

as the seller maximise the return.

5. Find out the Total Cost, Average Variable Cost, Average Total Cost, and Marginal Cost.

Quantity Variable

Cost (VC)

Fixed Cost

(FC)

Total Cost

(TC)

Average

variable

Cost

(AVC)

Average

Total Cost

(ATC)

Marginal

Cost (MC)

0 100 100 0 -

100 100 100 200 1 2 100

200 300 100 400 1.5 2 200

300 500 100 600 1.67 2 200

gets a point the supplier can supply their there product the most. The following equilibrium point

is for $70, where the Quantity demanded by the consumers of the commodity equals the Quantity

required by the supplier of the petrol ( Li, Monroe, and Coulton,2018).

Change in the demand curve because of reduction in the price of petrol.

Price Per Gallon Quantity Supplied Quantity demanded

$50 130 155

$60 135 135

$70 140 125

$80 145 120

$90 150 110

$100 155 95

The changes can see the impact of change in price of petrol in the Quantity demanded by the

consumer as the price of the commodity decreases the demand of the commodity increases and if

the costs of a commodity decreases then the Quantity demanded of the product decreases. With

the decline in the Quantity demanded of petrol, the Equilibrium of the given set of data has also

shifted to $60, which means the buyer will tends to purchase more at this price level (Khaki and

et.al., 2021). The Equilibrium is the price where any individual is ready to buy the product as so

as the seller maximise the return.

5. Find out the Total Cost, Average Variable Cost, Average Total Cost, and Marginal Cost.

Quantity Variable

Cost (VC)

Fixed Cost

(FC)

Total Cost

(TC)

Average

variable

Cost

(AVC)

Average

Total Cost

(ATC)

Marginal

Cost (MC)

0 100 100 0 -

100 100 100 200 1 2 100

200 300 100 400 1.5 2 200

300 500 100 600 1.67 2 200

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

400 700 100 800 1.75 2 200

500 800 100 900 1.6 1.8 100

600 120 100 220 0.2 0.37 -680

The following table shows that different types of Cost which includes Variable Cost, Fixed Cost,

Total Cost, Average Variable Cost, Average Total Cost and Marginal Cost. Fixed Cost remains

always fix irrespective of the level of production. Even at 0 output the Fixed remains the same.

Variable Cost varies with the level of production, increase in the Quantity produced also causes

increases the variable Cost (Youssef, and Teng, 2021). Total Cost is the combination of Fixed

Cost and Variable Cost. Marginal Cost is difference between the two level of production. It

explains that if the organization moves to the next alternative the Cost incurred on such process

is termed as Marginal Cost. Average Variable Cost is a average cost incurred on a single unit and

Average Total Cost is a price that is allocated to a single product means per unit cost of a

product.

6. Characteristics of perfect competition

Perfect competition is a form of market in which there are many buyers and sellers, and

firms are the price takers, which is decided by the industry. The features of perfect

competition are given as below -

1. a Large number of buyers and sellers - In this form of market, it has a significant number of

buyers and sellers, but they are not able to influence the price and output of the whole industry

(Zhao, 2021).

2. Price taker - The sellers of perfect competition are price takers because the industry is

responsible for setting price and output.

3. Homogeneous products - The sellers used to sell similar goods, eliminating the differentiation

among the products.

4. Free entry and exit - In perfect competition, the firms are liberal in entering and exiting the

market at any point in time.

5. Perfect knowledge of the market - In this form, buyers and sellers are fully aware of the price

at which goods are being sold (Gao and Han,2018).

500 800 100 900 1.6 1.8 100

600 120 100 220 0.2 0.37 -680

The following table shows that different types of Cost which includes Variable Cost, Fixed Cost,

Total Cost, Average Variable Cost, Average Total Cost and Marginal Cost. Fixed Cost remains

always fix irrespective of the level of production. Even at 0 output the Fixed remains the same.

Variable Cost varies with the level of production, increase in the Quantity produced also causes

increases the variable Cost (Youssef, and Teng, 2021). Total Cost is the combination of Fixed

Cost and Variable Cost. Marginal Cost is difference between the two level of production. It

explains that if the organization moves to the next alternative the Cost incurred on such process

is termed as Marginal Cost. Average Variable Cost is a average cost incurred on a single unit and

Average Total Cost is a price that is allocated to a single product means per unit cost of a

product.

6. Characteristics of perfect competition

Perfect competition is a form of market in which there are many buyers and sellers, and

firms are the price takers, which is decided by the industry. The features of perfect

competition are given as below -

1. a Large number of buyers and sellers - In this form of market, it has a significant number of

buyers and sellers, but they are not able to influence the price and output of the whole industry

(Zhao, 2021).

2. Price taker - The sellers of perfect competition are price takers because the industry is

responsible for setting price and output.

3. Homogeneous products - The sellers used to sell similar goods, eliminating the differentiation

among the products.

4. Free entry and exit - In perfect competition, the firms are liberal in entering and exiting the

market at any point in time.

5. Perfect knowledge of the market - In this form, buyers and sellers are fully aware of the price

at which goods are being sold (Gao and Han,2018).

There are some limitations of the perfect competition which restrict the same to apply in the real

world.

Similar products - The main feature which is difficult to exist is the homogeneity of

products. There is some degree of differentiation that always exists between the products.

In reality, it is rarer to observe identical goods.

Government regulations - The policies for starting a new venture restrict firms from free

entry because several start-up costs are included in the commencement process.

Free entry and exit of the firms – In real world, there are several formalities which are

required to be fulfilled but as the features of perfect competition suggest that entry is not

restricted which is not possible in actual conditions.

7. Critical evaluation of equilibrium point in perfect competition.

a.) Description of shutting down point when marginal revenue is less than the Average Cost.

There is the situation of losses in perfect competition, which can be understood from the

following points.

In the short term, there are three situations such as-

Expected profit- In perfect competition, average and marginal revenue remains constant.

Supernormal profit is when average income is more significant than average Cost

(Ochinowski, 2021).

Losses- In this situation, there is a point when the average price exceeds the average

revenue. This is a situation of loss.

Shut down - It is a situation where a firm experiences no advantages for the continuing

operation of the business, and an enterprise is stuck in a situation where the enterprise is

not recovering short-term variable costs.

b.) Explaining the situation of Equilibrium in the perfect competition market.

In the perfect competition market, there are broadly two situations of Equilibrium, which

are as follows-

MC=MR.

MC Cuts MR from below

1.) MC=MR: It states that firms continue their production until marginal cost and marginal

revenue cut others at the same point (Wang, Huang, and Jiang, 2020).

world.

Similar products - The main feature which is difficult to exist is the homogeneity of

products. There is some degree of differentiation that always exists between the products.

In reality, it is rarer to observe identical goods.

Government regulations - The policies for starting a new venture restrict firms from free

entry because several start-up costs are included in the commencement process.

Free entry and exit of the firms – In real world, there are several formalities which are

required to be fulfilled but as the features of perfect competition suggest that entry is not

restricted which is not possible in actual conditions.

7. Critical evaluation of equilibrium point in perfect competition.

a.) Description of shutting down point when marginal revenue is less than the Average Cost.

There is the situation of losses in perfect competition, which can be understood from the

following points.

In the short term, there are three situations such as-

Expected profit- In perfect competition, average and marginal revenue remains constant.

Supernormal profit is when average income is more significant than average Cost

(Ochinowski, 2021).

Losses- In this situation, there is a point when the average price exceeds the average

revenue. This is a situation of loss.

Shut down - It is a situation where a firm experiences no advantages for the continuing

operation of the business, and an enterprise is stuck in a situation where the enterprise is

not recovering short-term variable costs.

b.) Explaining the situation of Equilibrium in the perfect competition market.

In the perfect competition market, there are broadly two situations of Equilibrium, which

are as follows-

MC=MR.

MC Cuts MR from below

1.) MC=MR: It states that firms continue their production until marginal cost and marginal

revenue cut others at the same point (Wang, Huang, and Jiang, 2020).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2.) In a curve where marginal Cost cuts Marginal revenue from below, a firm can attain its

equilibrium point ( Analoui, 2018).

CONCLUSION

From the above report, it can be concluded that worldwide events such as a global pandemic,

OPEC meeting, and introduction of new technologies increase or decreases the Quantity

demanded and supply. With the help of identifying different market structures, an organization

can take various decisions, such as placing the existing market in which it is operating and

pricing policies of the business environment.

equilibrium point ( Analoui, 2018).

CONCLUSION

From the above report, it can be concluded that worldwide events such as a global pandemic,

OPEC meeting, and introduction of new technologies increase or decreases the Quantity

demanded and supply. With the help of identifying different market structures, an organization

can take various decisions, such as placing the existing market in which it is operating and

pricing policies of the business environment.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals

Mardnly, Z., Badran, Z. and Mouselli, S., 2021. Earnings management and audit quality at

Damascus securities exchange: does managerial ownership matter?. Journal of Financial

Reporting and Accounting.

Baker, H.K., Kumar, S. and Pandey, N., 2020. A bibliometric analysis of managerial finance: a

retrospective. Managerial Finance.

Pan, A., Liu, W. and Wang, X., 2019. Managerial overconfidence, debt capacity and merger &

acquisition premium. Nankai Business Review International.

Gack, S., 2018. Managerial implications for theory and management. In Service Innovation in

Agricultural Business (pp. 67-67). Springer Gabler, Wiesbaden.

Li, L., Monroe, G.S. and Coulton, J., 2018. Managerial litigation risk and corporate investment

efficiency: Evidence from derivative lawsuits. Available at SSRN 3147435.

Bu, Q., 2021. Mutual fund alpha: Is it managerial or emotional?. Journal of Behavioral Finance.

22(1). pp.46-55.

Khaki, M.R. and et.al., 2021. The Effect of Social Pressures Anomie on Aggressive Financial

Reporting: Analysis of the Theory of Managerial Critical Perception. Management

Accounting. 14(48). pp.23-44.

Youssef, M.H. and Teng, D., 2021. MANAGERIAL DISCRETION AND CORPORATE

GOVERNANCE: THE BONDED RELATIONSHIP.

Zhao, T., 2021. Managerial Overconfidence and Corporate Credit Ratings. Available at SSRN

3946723.

Gao, Y. and Han, K.S., 2018. The Influence of Managerial Overconfidence on Earnings

Management.33(3). pp.425-442.

Ochinowski, T., 2021. Character Strengths as a Tool of Resilience-Oriented Vocational Training

for Managerial Staff in a Life–Long Learning Perspective. Journal of International

Business Research and Marketing. 6(3). pp.7-10.

Wang, Z., Huang, J. and Jiang, Z., 2020. Change in sales, managerial overconfidence and

persistence of firm R&D investment: evidence from China. Economics of Innovation

and New Technology. pp.1-18.

Books and Journals

Mardnly, Z., Badran, Z. and Mouselli, S., 2021. Earnings management and audit quality at

Damascus securities exchange: does managerial ownership matter?. Journal of Financial

Reporting and Accounting.

Baker, H.K., Kumar, S. and Pandey, N., 2020. A bibliometric analysis of managerial finance: a

retrospective. Managerial Finance.

Pan, A., Liu, W. and Wang, X., 2019. Managerial overconfidence, debt capacity and merger &

acquisition premium. Nankai Business Review International.

Gack, S., 2018. Managerial implications for theory and management. In Service Innovation in

Agricultural Business (pp. 67-67). Springer Gabler, Wiesbaden.

Li, L., Monroe, G.S. and Coulton, J., 2018. Managerial litigation risk and corporate investment

efficiency: Evidence from derivative lawsuits. Available at SSRN 3147435.

Bu, Q., 2021. Mutual fund alpha: Is it managerial or emotional?. Journal of Behavioral Finance.

22(1). pp.46-55.

Khaki, M.R. and et.al., 2021. The Effect of Social Pressures Anomie on Aggressive Financial

Reporting: Analysis of the Theory of Managerial Critical Perception. Management

Accounting. 14(48). pp.23-44.

Youssef, M.H. and Teng, D., 2021. MANAGERIAL DISCRETION AND CORPORATE

GOVERNANCE: THE BONDED RELATIONSHIP.

Zhao, T., 2021. Managerial Overconfidence and Corporate Credit Ratings. Available at SSRN

3946723.

Gao, Y. and Han, K.S., 2018. The Influence of Managerial Overconfidence on Earnings

Management.33(3). pp.425-442.

Ochinowski, T., 2021. Character Strengths as a Tool of Resilience-Oriented Vocational Training

for Managerial Staff in a Life–Long Learning Perspective. Journal of International

Business Research and Marketing. 6(3). pp.7-10.

Wang, Z., Huang, J. and Jiang, Z., 2020. Change in sales, managerial overconfidence and

persistence of firm R&D investment: evidence from China. Economics of Innovation

and New Technology. pp.1-18.

Analoui, F., 2018. Managerial perspectives, assumptions and development of the human resource

management. In Human resource management issues in developing countries (pp. 1-20).

Routledge.

management. In Human resource management issues in developing countries (pp. 1-20).

Routledge.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.