Managerial Finance Report: Financial Analysis and Investment Appraisal

VerifiedAdded on 2022/12/30

|19

|3832

|83

Report

AI Summary

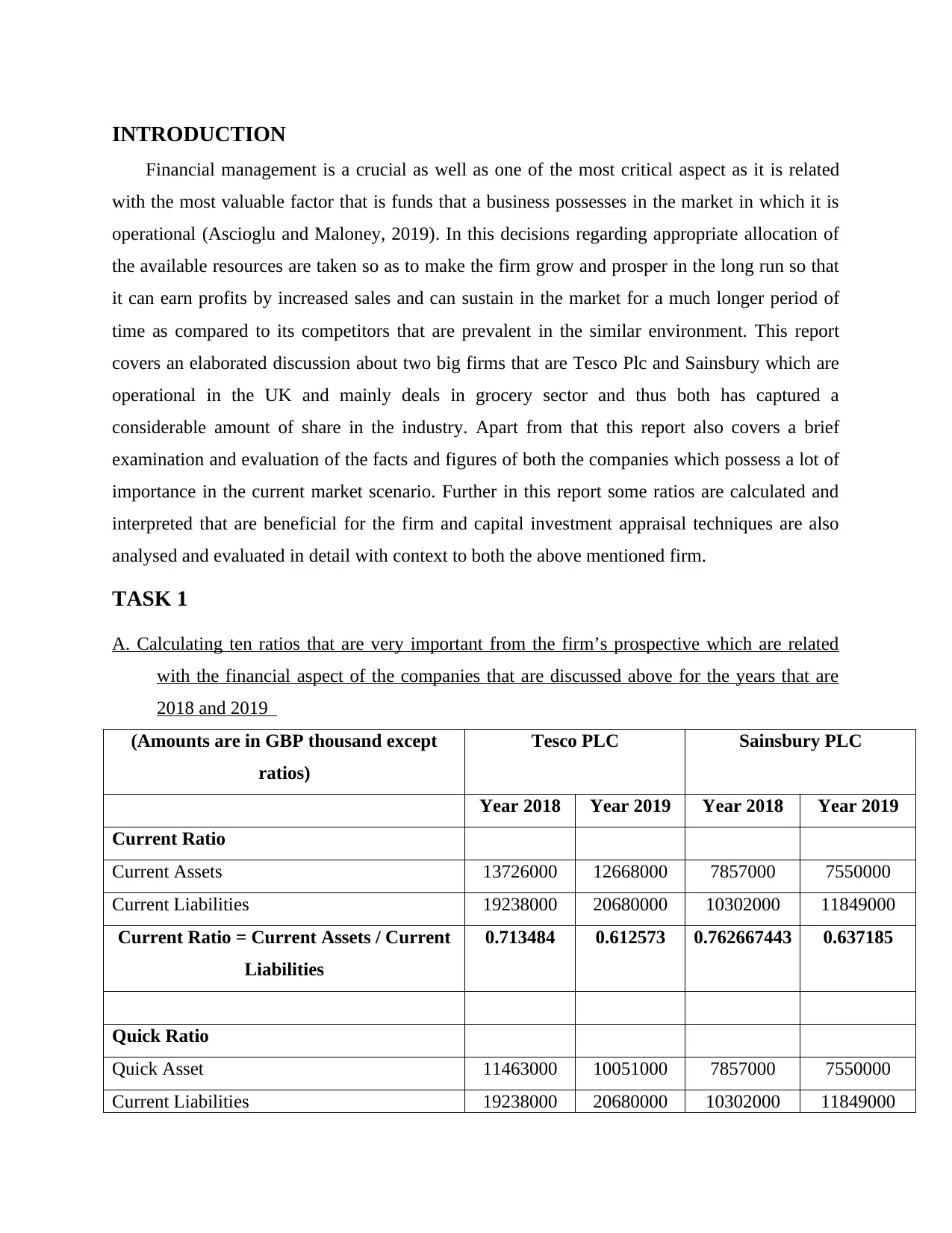

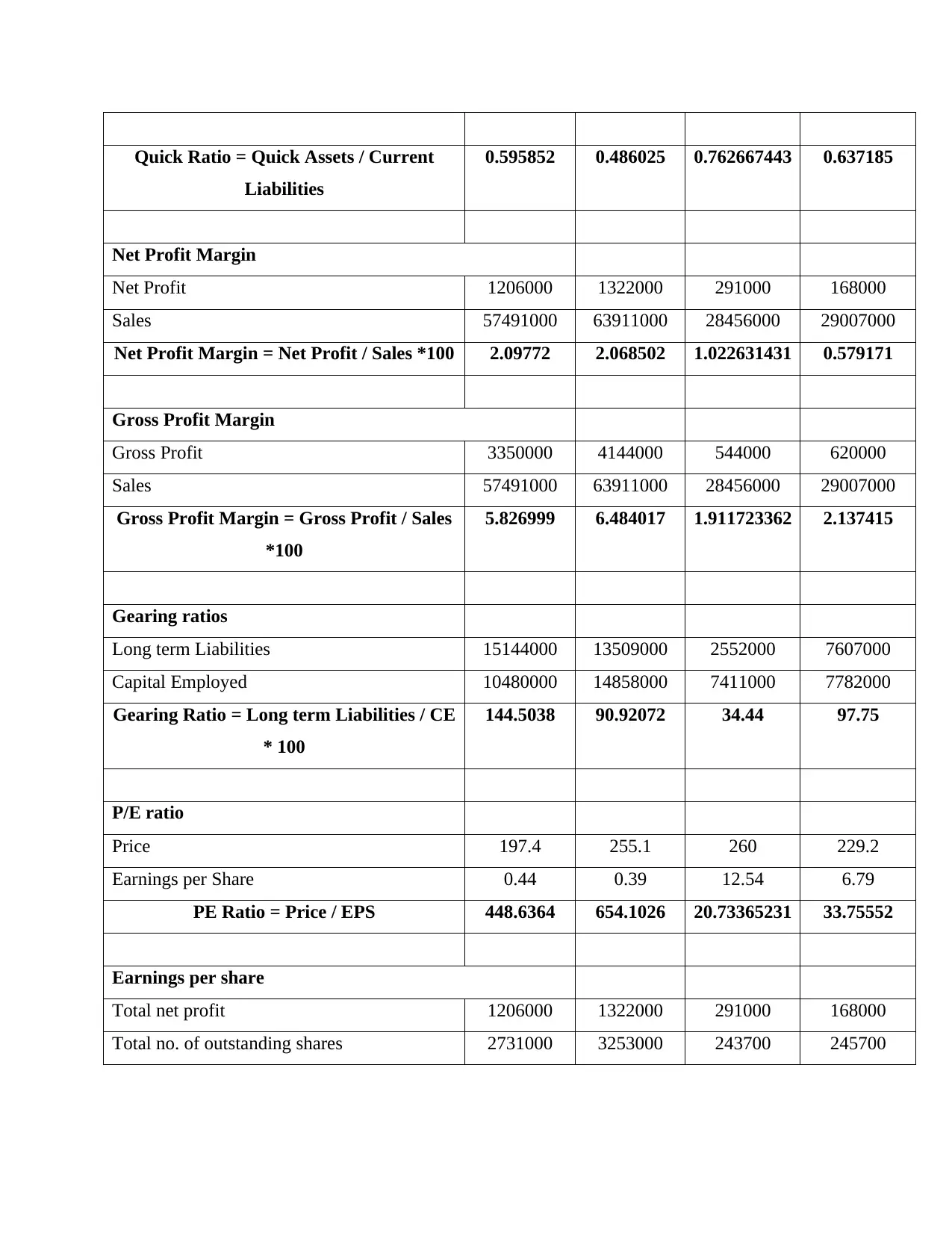

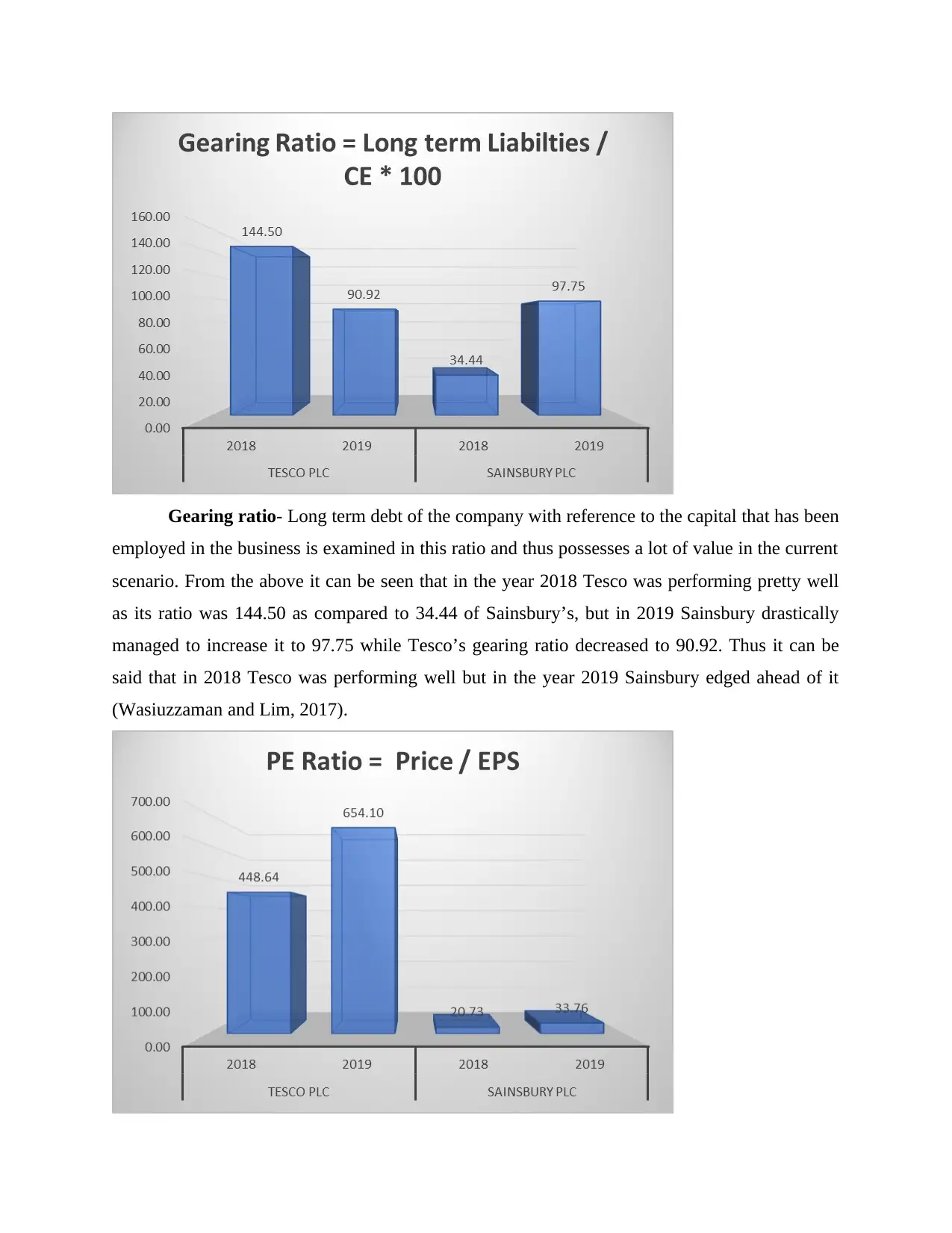

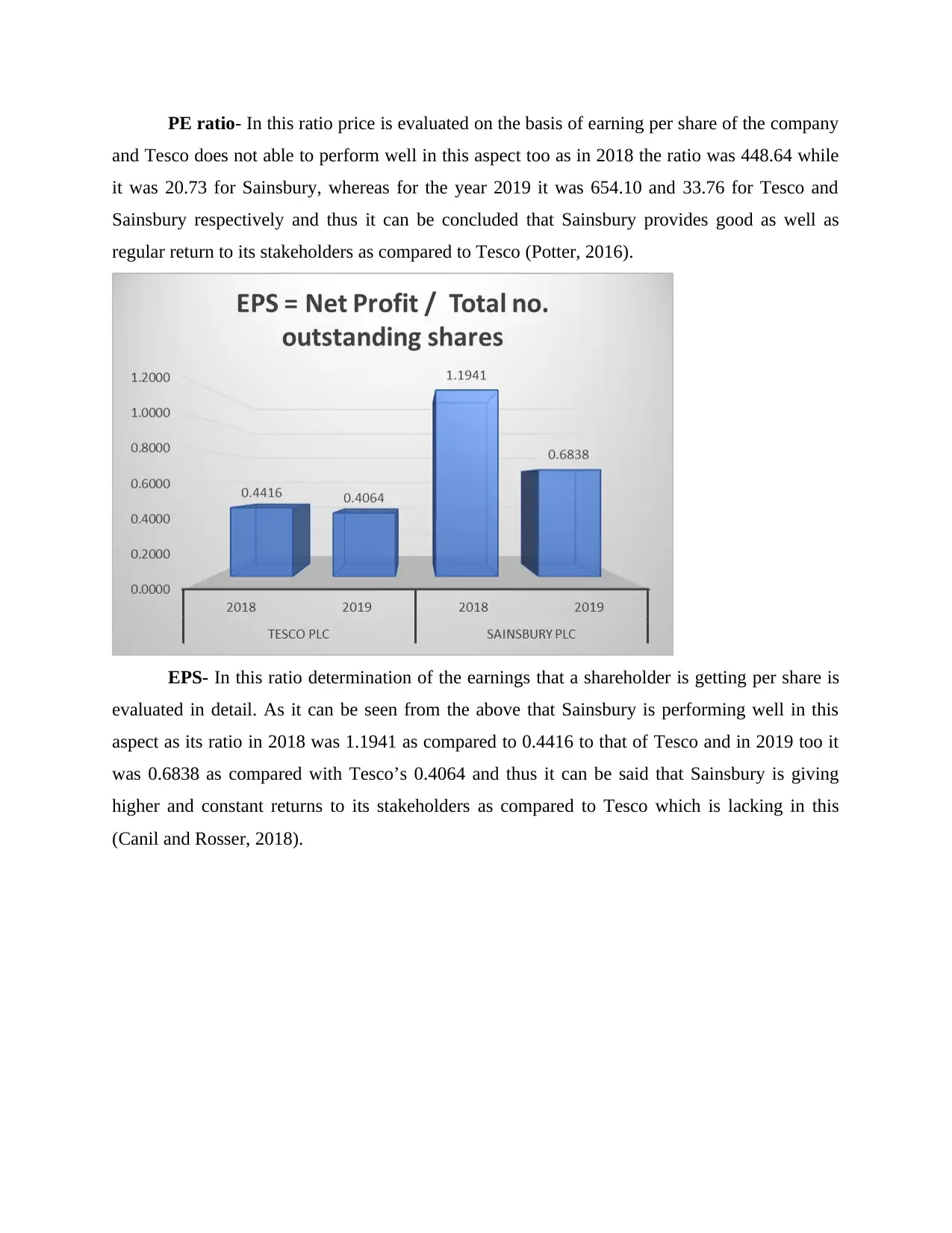

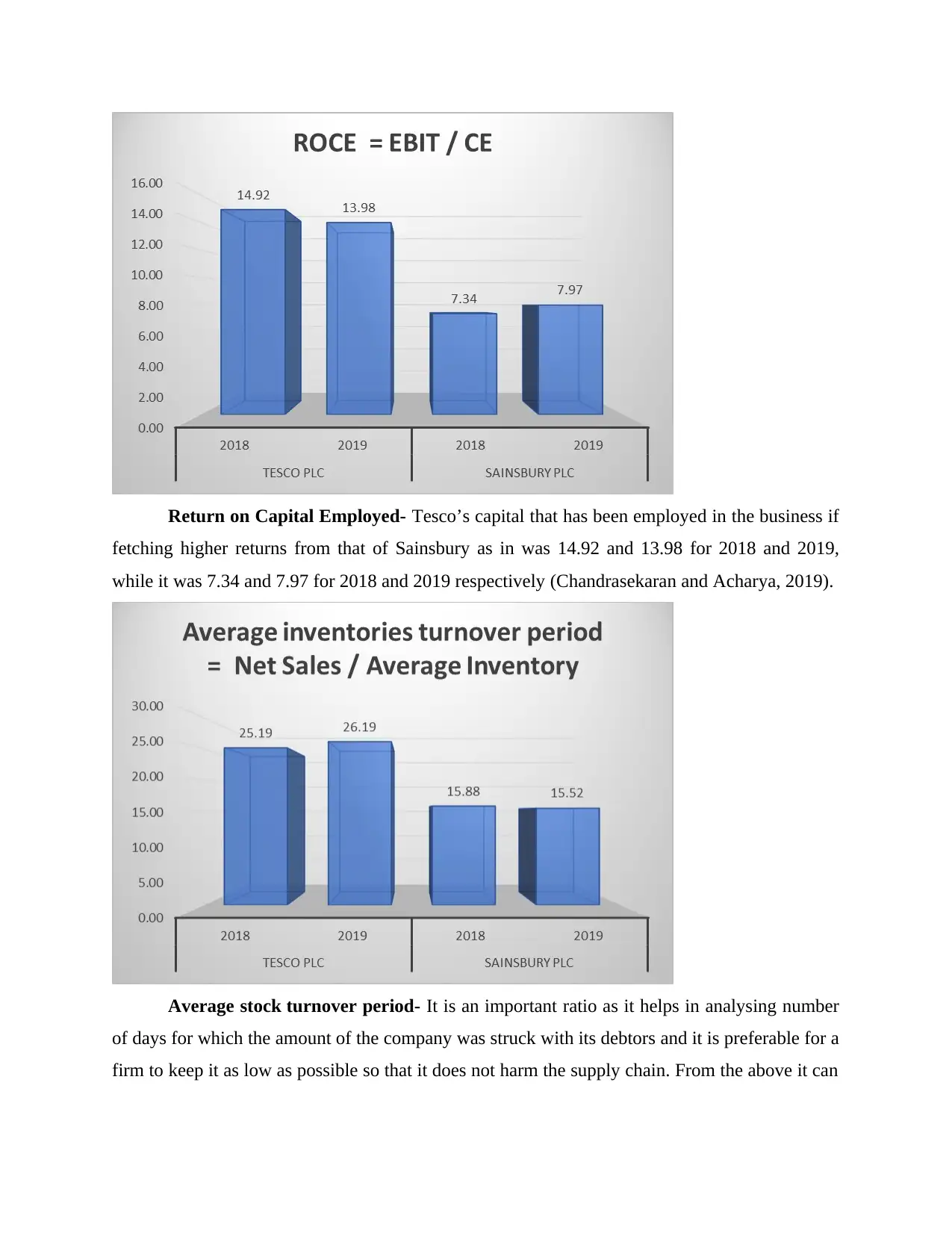

This report provides a comprehensive financial analysis of Tesco PLC and Sainsbury PLC, two major players in the UK grocery sector. It begins with an introduction to financial management and its importance in business decision-making. The core of the report involves calculating and interpreting ten key financial ratios for both companies for the years 2018 and 2019, including current ratio, quick ratio, net profit margin, gross profit margin, gearing ratio, P/E ratio, EPS, ROCE, average inventory turnover period, and dividend payout ratio. The analysis compares the financial performance of the two companies across these ratios, highlighting their strengths and weaknesses. Furthermore, the report delves into investment appraisal techniques, examining their calculation and limitations, particularly in long-term decision-making. Recommendations are provided for both Tesco and Sainsbury based on the financial analysis, along with a discussion of the limitations of relying solely on financial ratios. The report concludes with a summary of the key findings and insights.

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.