Financial Analysis Report: Tesco and Sainsbury's, Investment Appraisal

VerifiedAdded on 2023/01/06

|20

|4047

|57

Report

AI Summary

This report, created for a Managerial Finance assessment, analyzes the financial performance of Tesco plc and Sainsbury's plc through ratio analysis and investment appraisal techniques. Portfolio 1 focuses on ratio analysis, examining current ratio, quick ratio, net profit margin, gross profit margin, gearing ratio, P/E ratio, earnings per share, return on capital employed, inventory turnover, and dividend payout ratio for both companies over two years. The report evaluates their liquidity, profitability, and efficiency, highlighting strengths and weaknesses. Portfolio 2 discusses investment appraisal techniques, which are crucial for making sound investment decisions. The report concludes with recommendations for improvement and limitations of ratio analysis.

Finance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTRODUCTION.......................................................................................................................................3

PORTFOLIO 1............................................................................................................................................3

Ratio analysis..........................................................................................................................................3

PORTFOLIO 2..........................................................................................................................................14

Investment appraisal techniques............................................................................................................14

CONCLUSION.........................................................................................................................................18

PORTFOLIO 1............................................................................................................................................3

Ratio analysis..........................................................................................................................................3

PORTFOLIO 2..........................................................................................................................................14

Investment appraisal techniques............................................................................................................14

CONCLUSION.........................................................................................................................................18

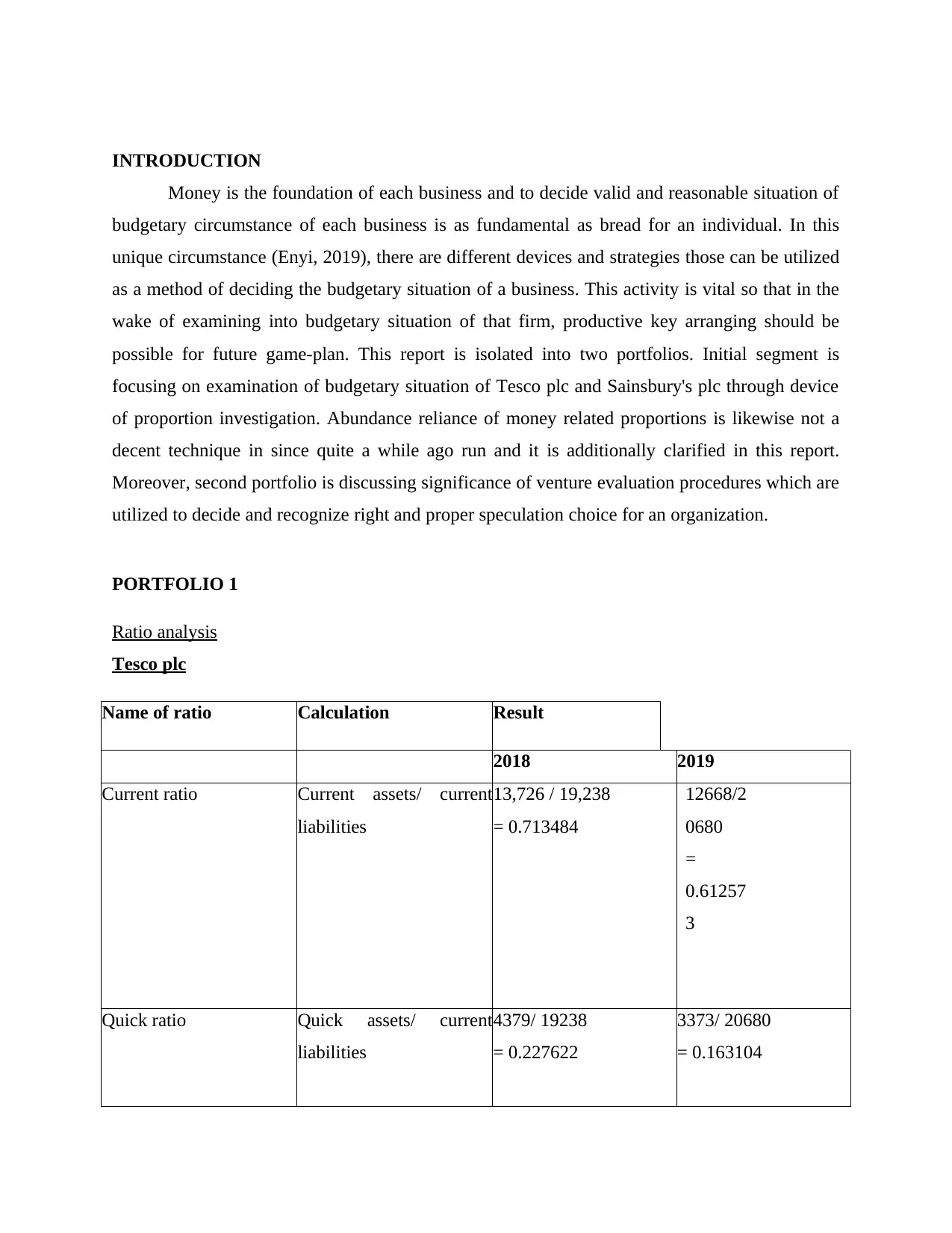

INTRODUCTION

Money is the foundation of each business and to decide valid and reasonable situation of

budgetary circumstance of each business is as fundamental as bread for an individual. In this

unique circumstance (Enyi, 2019), there are different devices and strategies those can be utilized

as a method of deciding the budgetary situation of a business. This activity is vital so that in the

wake of examining into budgetary situation of that firm, productive key arranging should be

possible for future game-plan. This report is isolated into two portfolios. Initial segment is

focusing on examination of budgetary situation of Tesco plc and Sainsbury's plc through device

of proportion investigation. Abundance reliance of money related proportions is likewise not a

decent technique in since quite a while ago run and it is additionally clarified in this report.

Moreover, second portfolio is discussing significance of venture evaluation procedures which are

utilized to decide and recognize right and proper speculation choice for an organization.

PORTFOLIO 1

Ratio analysis

Tesco plc

Name of ratio Calculation Result

2018 2019

Current ratio Current assets/ current

liabilities

13,726 / 19,238

= 0.713484

12668/2

0680

=

0.61257

3

Quick ratio Quick assets/ current

liabilities

4379/ 19238

= 0.227622

3373/ 20680

= 0.163104

Money is the foundation of each business and to decide valid and reasonable situation of

budgetary circumstance of each business is as fundamental as bread for an individual. In this

unique circumstance (Enyi, 2019), there are different devices and strategies those can be utilized

as a method of deciding the budgetary situation of a business. This activity is vital so that in the

wake of examining into budgetary situation of that firm, productive key arranging should be

possible for future game-plan. This report is isolated into two portfolios. Initial segment is

focusing on examination of budgetary situation of Tesco plc and Sainsbury's plc through device

of proportion investigation. Abundance reliance of money related proportions is likewise not a

decent technique in since quite a while ago run and it is additionally clarified in this report.

Moreover, second portfolio is discussing significance of venture evaluation procedures which are

utilized to decide and recognize right and proper speculation choice for an organization.

PORTFOLIO 1

Ratio analysis

Tesco plc

Name of ratio Calculation Result

2018 2019

Current ratio Current assets/ current

liabilities

13,726 / 19,238

= 0.713484

12668/2

0680

=

0.61257

3

Quick ratio Quick assets/ current

liabilities

4379/ 19238

= 0.227622

3373/ 20680

= 0.163104

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

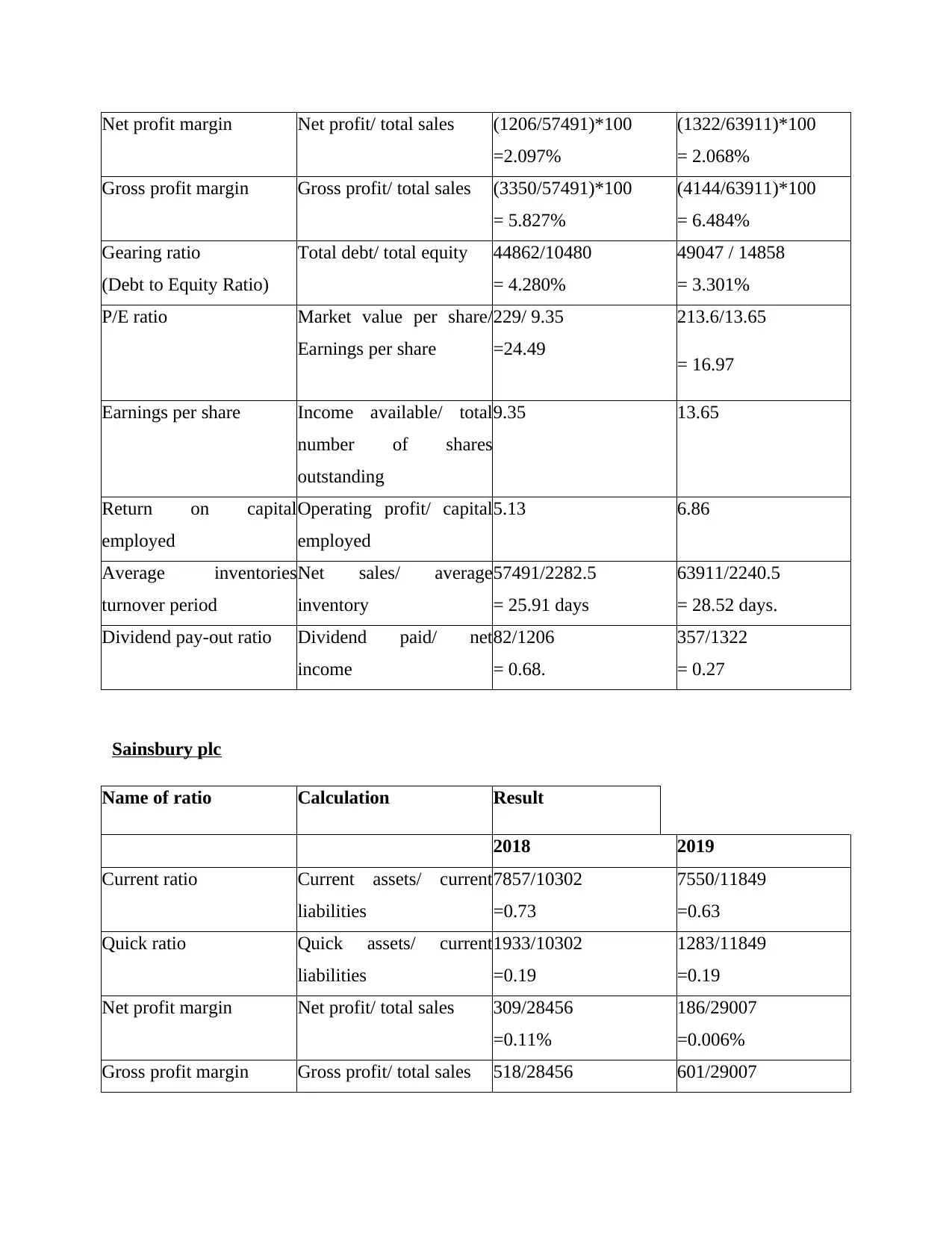

Net profit margin Net profit/ total sales (1206/57491)*100

=2.097%

(1322/63911)*100

= 2.068%

Gross profit margin Gross profit/ total sales (3350/57491)*100

= 5.827%

(4144/63911)*100

= 6.484%

Gearing ratio

(Debt to Equity Ratio)

Total debt/ total equity 44862/10480

= 4.280%

49047 / 14858

= 3.301%

P/E ratio Market value per share/

Earnings per share

229/ 9.35

=24.49

213.6/13.65

= 16.97

Earnings per share Income available/ total

number of shares

outstanding

9.35 13.65

Return on capital

employed

Operating profit/ capital

employed

5.13 6.86

Average inventories

turnover period

Net sales/ average

inventory

57491/2282.5

= 25.91 days

63911/2240.5

= 28.52 days.

Dividend pay-out ratio Dividend paid/ net

income

82/1206

= 0.68.

357/1322

= 0.27

Sainsbury plc

Name of ratio Calculation Result

2018 2019

Current ratio Current assets/ current

liabilities

7857/10302

=0.73

7550/11849

=0.63

Quick ratio Quick assets/ current

liabilities

1933/10302

=0.19

1283/11849

=0.19

Net profit margin Net profit/ total sales 309/28456

=0.11%

186/29007

=0.006%

Gross profit margin Gross profit/ total sales 518/28456 601/29007

=2.097%

(1322/63911)*100

= 2.068%

Gross profit margin Gross profit/ total sales (3350/57491)*100

= 5.827%

(4144/63911)*100

= 6.484%

Gearing ratio

(Debt to Equity Ratio)

Total debt/ total equity 44862/10480

= 4.280%

49047 / 14858

= 3.301%

P/E ratio Market value per share/

Earnings per share

229/ 9.35

=24.49

213.6/13.65

= 16.97

Earnings per share Income available/ total

number of shares

outstanding

9.35 13.65

Return on capital

employed

Operating profit/ capital

employed

5.13 6.86

Average inventories

turnover period

Net sales/ average

inventory

57491/2282.5

= 25.91 days

63911/2240.5

= 28.52 days.

Dividend pay-out ratio Dividend paid/ net

income

82/1206

= 0.68.

357/1322

= 0.27

Sainsbury plc

Name of ratio Calculation Result

2018 2019

Current ratio Current assets/ current

liabilities

7857/10302

=0.73

7550/11849

=0.63

Quick ratio Quick assets/ current

liabilities

1933/10302

=0.19

1283/11849

=0.19

Net profit margin Net profit/ total sales 309/28456

=0.11%

186/29007

=0.006%

Gross profit margin Gross profit/ total sales 518/28456 601/29007

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

=0.018% =0.02%

Gearing ratio

(Debt to Equity Ratio)

Total debt/ total equity 34.44 97.75

P/E ratio Market value per share/

Earnings per share

238.80/0.22

=10.85

213.40/46

=4.64

Earnings per share Income available/ total

number of shares

outstanding

22 46

Return on capital

employed

Operating profit/ capital

employed

4.65 3.84

Average inventories

turnover period

Net sales/ average

inventory

28456/1792.5

=15.87 days.

29007/1869.5

=15.51 days.

Dividend pay-out ratio Dividend paid/ net

income

235/309

=0.76

247/186

=1.33

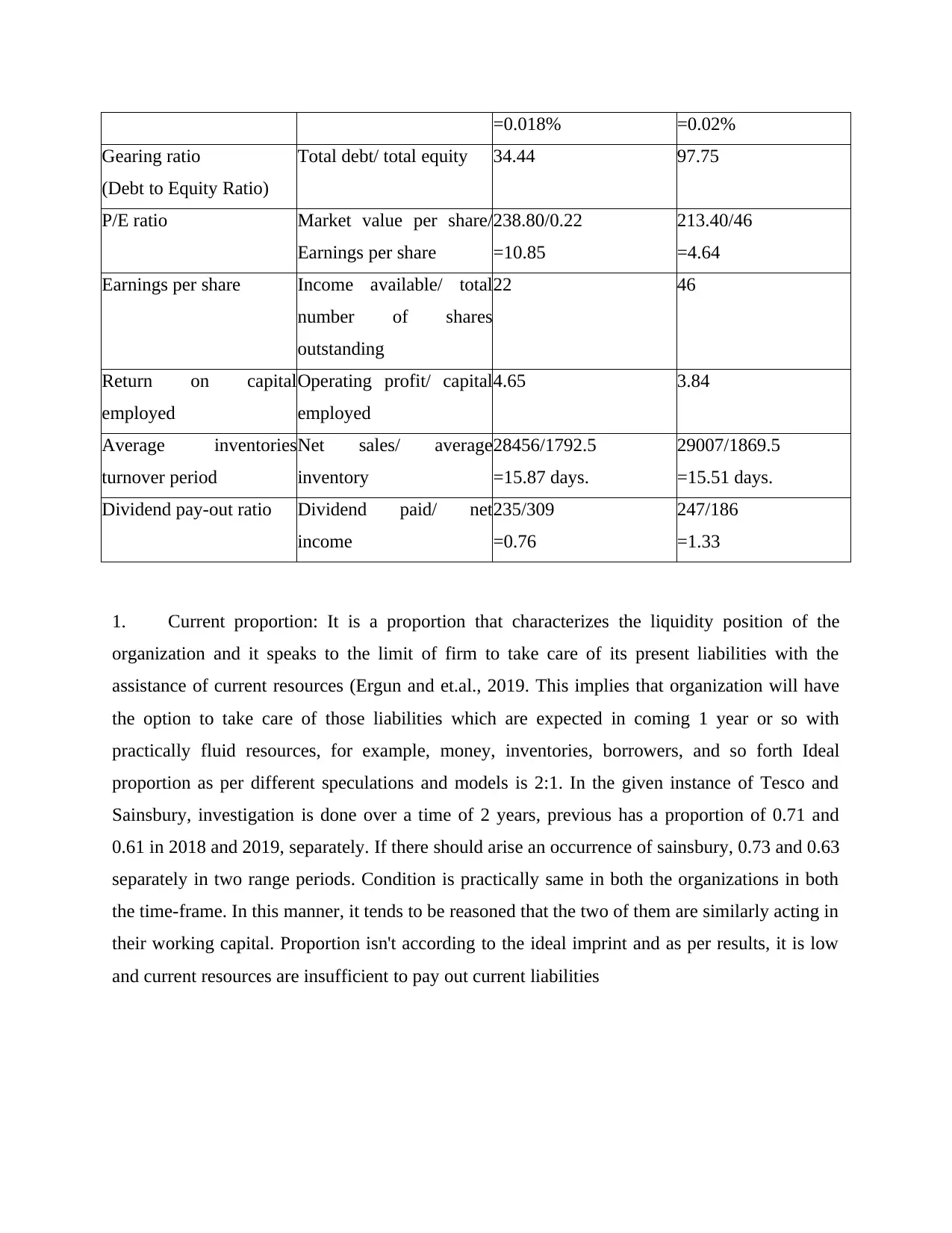

1. Current proportion: It is a proportion that characterizes the liquidity position of the

organization and it speaks to the limit of firm to take care of its present liabilities with the

assistance of current resources (Ergun and et.al., 2019. This implies that organization will have

the option to take care of those liabilities which are expected in coming 1 year or so with

practically fluid resources, for example, money, inventories, borrowers, and so forth Ideal

proportion as per different speculations and models is 2:1. In the given instance of Tesco and

Sainsbury, investigation is done over a time of 2 years, previous has a proportion of 0.71 and

0.61 in 2018 and 2019, separately. If there should arise an occurrence of sainsbury, 0.73 and 0.63

separately in two range periods. Condition is practically same in both the organizations in both

the time-frame. In this manner, it tends to be reasoned that the two of them are similarly acting in

their working capital. Proportion isn't according to the ideal imprint and as per results, it is low

and current resources are insufficient to pay out current liabilities

Gearing ratio

(Debt to Equity Ratio)

Total debt/ total equity 34.44 97.75

P/E ratio Market value per share/

Earnings per share

238.80/0.22

=10.85

213.40/46

=4.64

Earnings per share Income available/ total

number of shares

outstanding

22 46

Return on capital

employed

Operating profit/ capital

employed

4.65 3.84

Average inventories

turnover period

Net sales/ average

inventory

28456/1792.5

=15.87 days.

29007/1869.5

=15.51 days.

Dividend pay-out ratio Dividend paid/ net

income

235/309

=0.76

247/186

=1.33

1. Current proportion: It is a proportion that characterizes the liquidity position of the

organization and it speaks to the limit of firm to take care of its present liabilities with the

assistance of current resources (Ergun and et.al., 2019. This implies that organization will have

the option to take care of those liabilities which are expected in coming 1 year or so with

practically fluid resources, for example, money, inventories, borrowers, and so forth Ideal

proportion as per different speculations and models is 2:1. In the given instance of Tesco and

Sainsbury, investigation is done over a time of 2 years, previous has a proportion of 0.71 and

0.61 in 2018 and 2019, separately. If there should arise an occurrence of sainsbury, 0.73 and 0.63

separately in two range periods. Condition is practically same in both the organizations in both

the time-frame. In this manner, it tends to be reasoned that the two of them are similarly acting in

their working capital. Proportion isn't according to the ideal imprint and as per results, it is low

and current resources are insufficient to pay out current liabilities

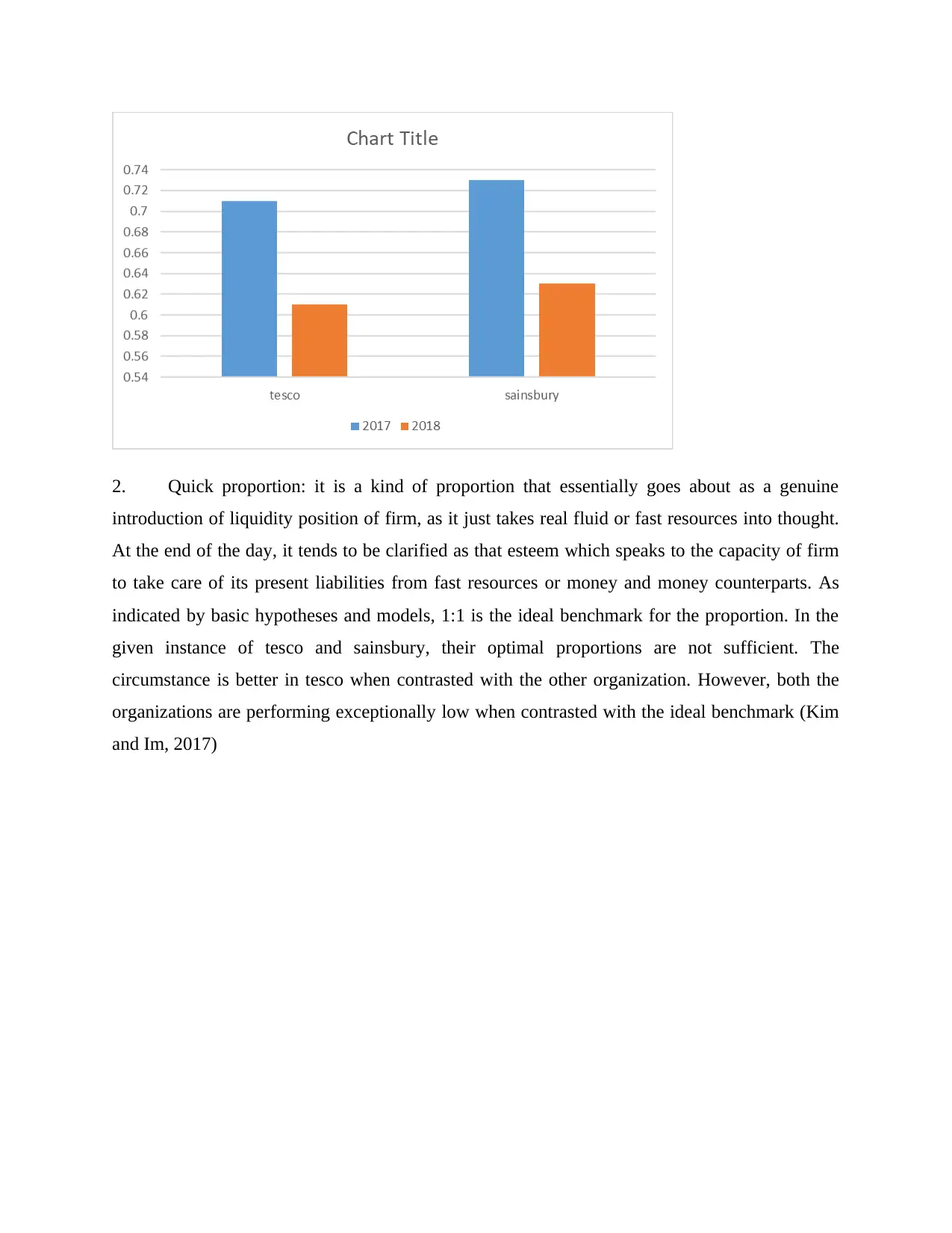

2. Quick proportion: it is a kind of proportion that essentially goes about as a genuine

introduction of liquidity position of firm, as it just takes real fluid or fast resources into thought.

At the end of the day, it tends to be clarified as that esteem which speaks to the capacity of firm

to take care of its present liabilities from fast resources or money and money counterparts. As

indicated by basic hypotheses and models, 1:1 is the ideal benchmark for the proportion. In the

given instance of tesco and sainsbury, their optimal proportions are not sufficient. The

circumstance is better in tesco when contrasted with the other organization. However, both the

organizations are performing exceptionally low when contrasted with the ideal benchmark (Kim

and Im, 2017)

introduction of liquidity position of firm, as it just takes real fluid or fast resources into thought.

At the end of the day, it tends to be clarified as that esteem which speaks to the capacity of firm

to take care of its present liabilities from fast resources or money and money counterparts. As

indicated by basic hypotheses and models, 1:1 is the ideal benchmark for the proportion. In the

given instance of tesco and sainsbury, their optimal proportions are not sufficient. The

circumstance is better in tesco when contrasted with the other organization. However, both the

organizations are performing exceptionally low when contrasted with the ideal benchmark (Kim

and Im, 2017)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

.

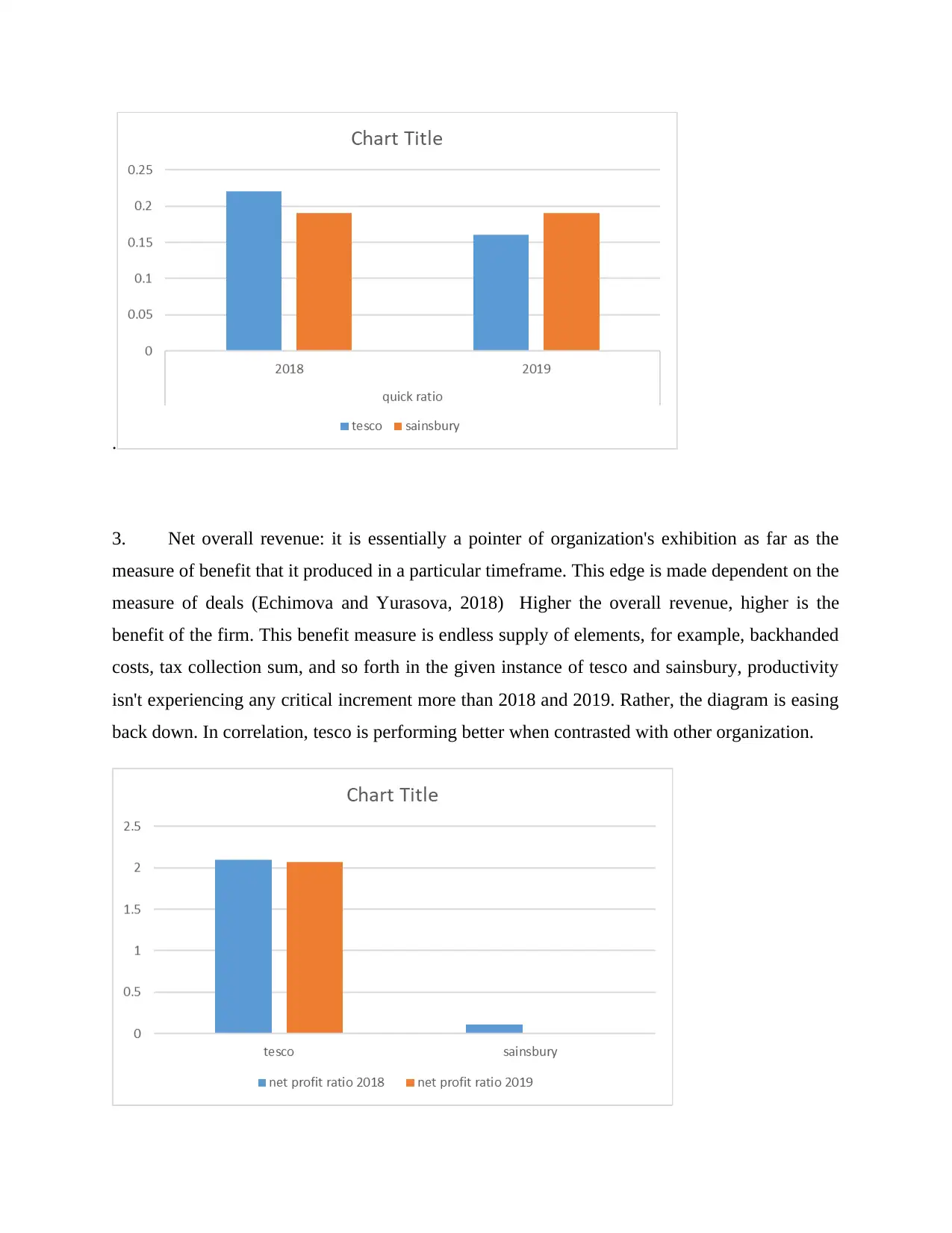

3. Net overall revenue: it is essentially a pointer of organization's exhibition as far as the

measure of benefit that it produced in a particular timeframe. This edge is made dependent on the

measure of deals (Echimova and Yurasova, 2018) Higher the overall revenue, higher is the

benefit of the firm. This benefit measure is endless supply of elements, for example, backhanded

costs, tax collection sum, and so forth in the given instance of tesco and sainsbury, productivity

isn't experiencing any critical increment more than 2018 and 2019. Rather, the diagram is easing

back down. In correlation, tesco is performing better when contrasted with other organization.

3. Net overall revenue: it is essentially a pointer of organization's exhibition as far as the

measure of benefit that it produced in a particular timeframe. This edge is made dependent on the

measure of deals (Echimova and Yurasova, 2018) Higher the overall revenue, higher is the

benefit of the firm. This benefit measure is endless supply of elements, for example, backhanded

costs, tax collection sum, and so forth in the given instance of tesco and sainsbury, productivity

isn't experiencing any critical increment more than 2018 and 2019. Rather, the diagram is easing

back down. In correlation, tesco is performing better when contrasted with other organization.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

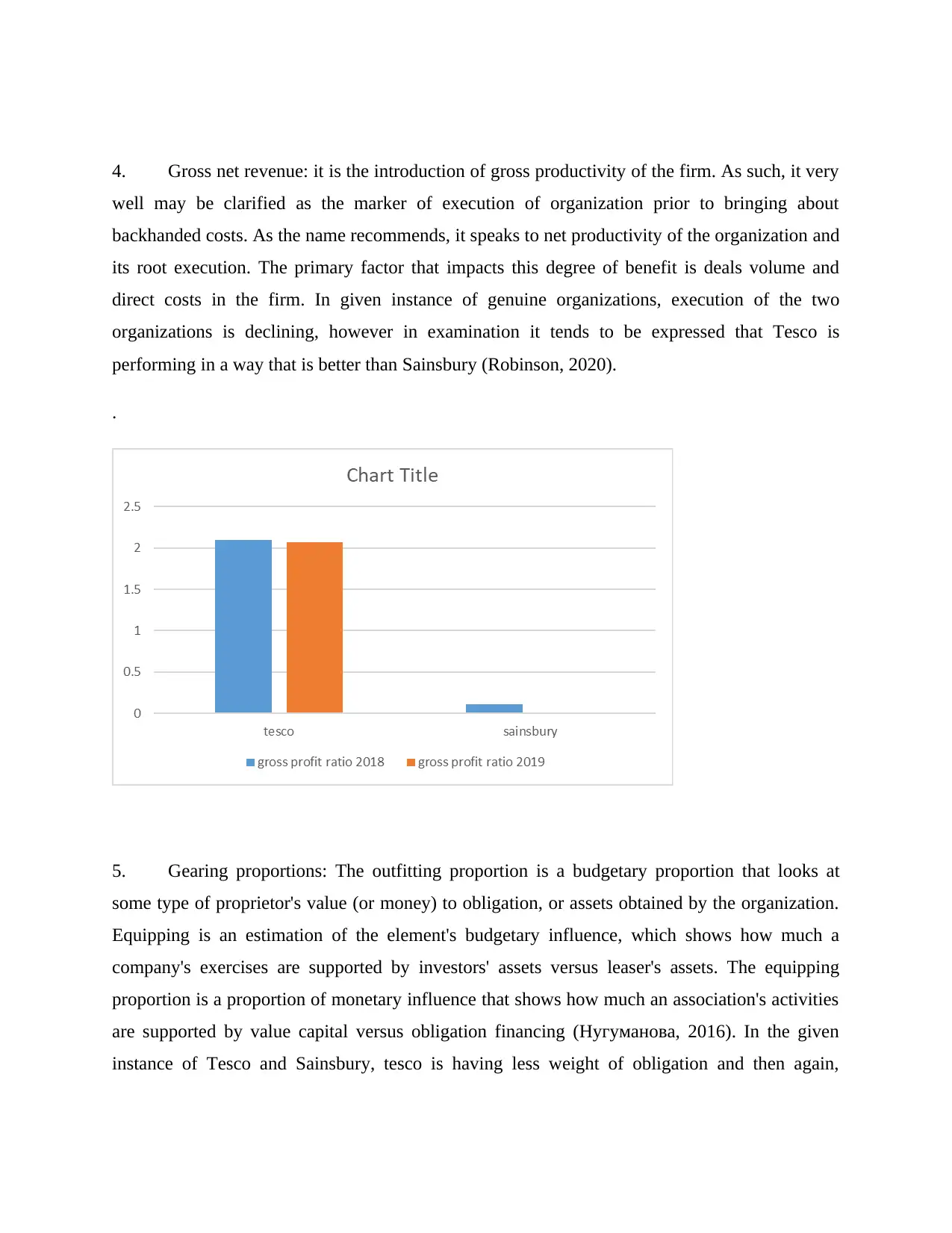

4. Gross net revenue: it is the introduction of gross productivity of the firm. As such, it very

well may be clarified as the marker of execution of organization prior to bringing about

backhanded costs. As the name recommends, it speaks to net productivity of the organization and

its root execution. The primary factor that impacts this degree of benefit is deals volume and

direct costs in the firm. In given instance of genuine organizations, execution of the two

organizations is declining, however in examination it tends to be expressed that Tesco is

performing in a way that is better than Sainsbury (Robinson, 2020).

.

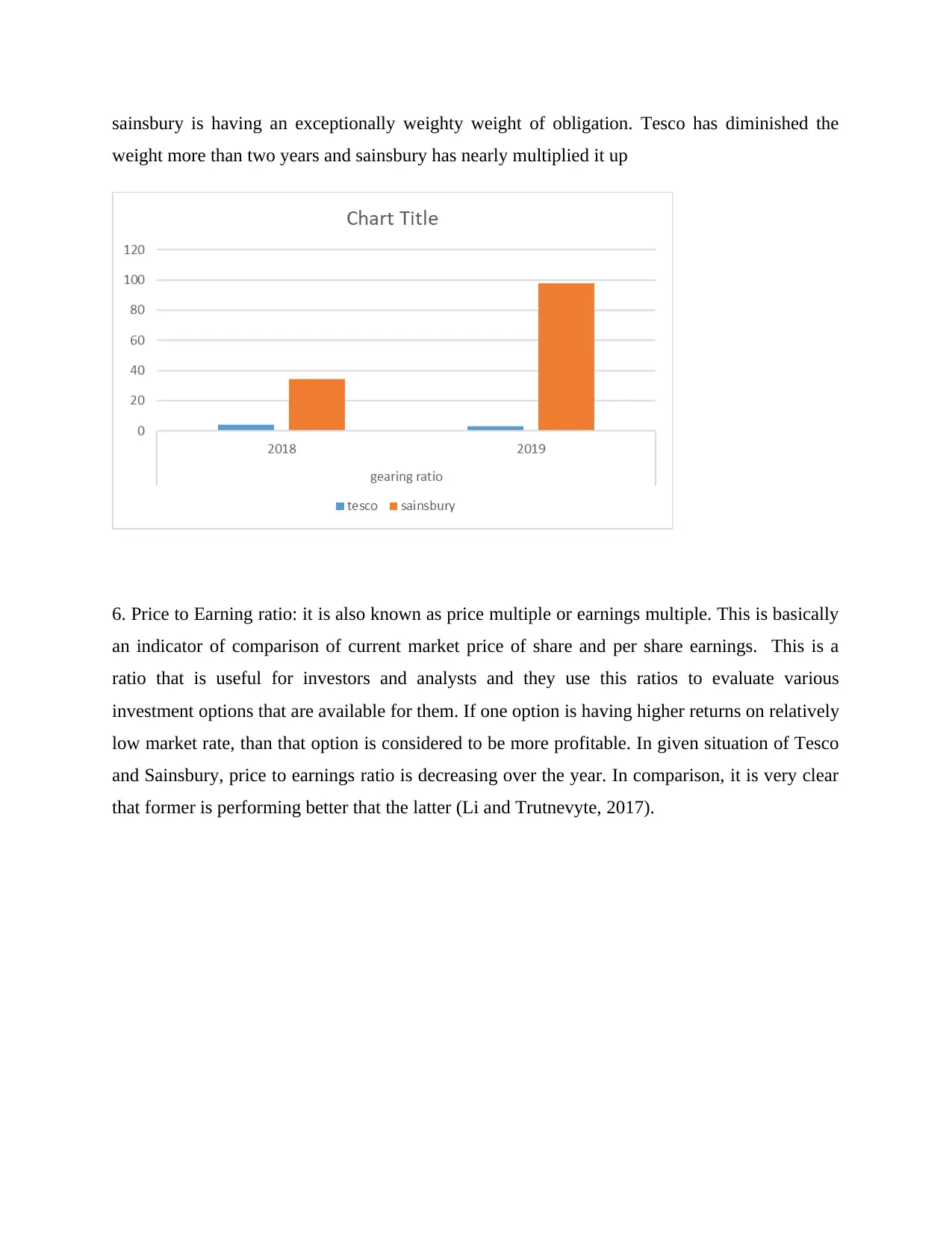

5. Gearing proportions: The outfitting proportion is a budgetary proportion that looks at

some type of proprietor's value (or money) to obligation, or assets obtained by the organization.

Equipping is an estimation of the element's budgetary influence, which shows how much a

company's exercises are supported by investors' assets versus leaser's assets. The equipping

proportion is a proportion of monetary influence that shows how much an association's activities

are supported by value capital versus obligation financing (Нугуманова, 2016). In the given

instance of Tesco and Sainsbury, tesco is having less weight of obligation and then again,

well may be clarified as the marker of execution of organization prior to bringing about

backhanded costs. As the name recommends, it speaks to net productivity of the organization and

its root execution. The primary factor that impacts this degree of benefit is deals volume and

direct costs in the firm. In given instance of genuine organizations, execution of the two

organizations is declining, however in examination it tends to be expressed that Tesco is

performing in a way that is better than Sainsbury (Robinson, 2020).

.

5. Gearing proportions: The outfitting proportion is a budgetary proportion that looks at

some type of proprietor's value (or money) to obligation, or assets obtained by the organization.

Equipping is an estimation of the element's budgetary influence, which shows how much a

company's exercises are supported by investors' assets versus leaser's assets. The equipping

proportion is a proportion of monetary influence that shows how much an association's activities

are supported by value capital versus obligation financing (Нугуманова, 2016). In the given

instance of Tesco and Sainsbury, tesco is having less weight of obligation and then again,

sainsbury is having an exceptionally weighty weight of obligation. Tesco has diminished the

weight more than two years and sainsbury has nearly multiplied it up

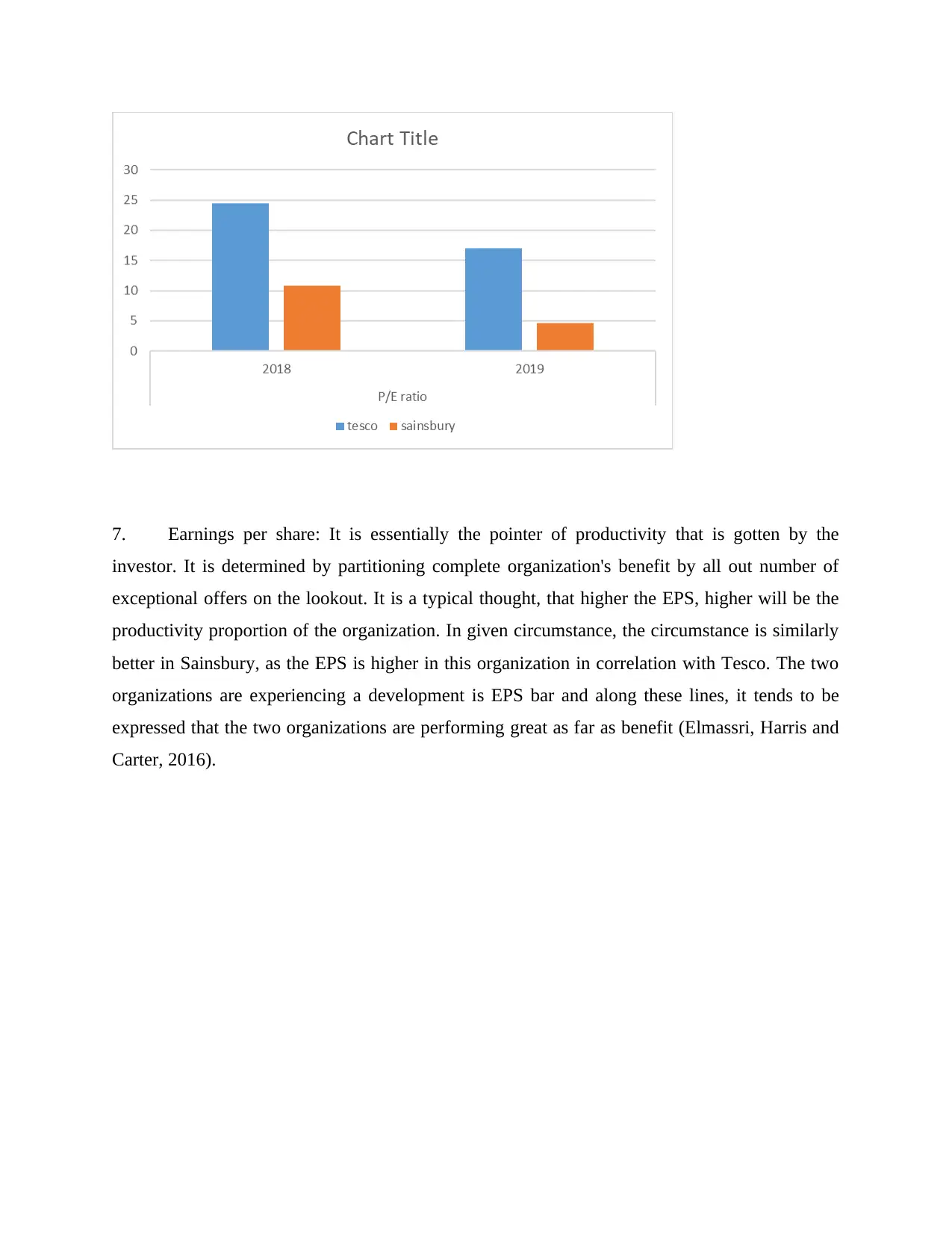

6. Price to Earning ratio: it is also known as price multiple or earnings multiple. This is basically

an indicator of comparison of current market price of share and per share earnings. This is a

ratio that is useful for investors and analysts and they use this ratios to evaluate various

investment options that are available for them. If one option is having higher returns on relatively

low market rate, than that option is considered to be more profitable. In given situation of Tesco

and Sainsbury, price to earnings ratio is decreasing over the year. In comparison, it is very clear

that former is performing better that the latter (Li and Trutnevyte, 2017).

weight more than two years and sainsbury has nearly multiplied it up

6. Price to Earning ratio: it is also known as price multiple or earnings multiple. This is basically

an indicator of comparison of current market price of share and per share earnings. This is a

ratio that is useful for investors and analysts and they use this ratios to evaluate various

investment options that are available for them. If one option is having higher returns on relatively

low market rate, than that option is considered to be more profitable. In given situation of Tesco

and Sainsbury, price to earnings ratio is decreasing over the year. In comparison, it is very clear

that former is performing better that the latter (Li and Trutnevyte, 2017).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

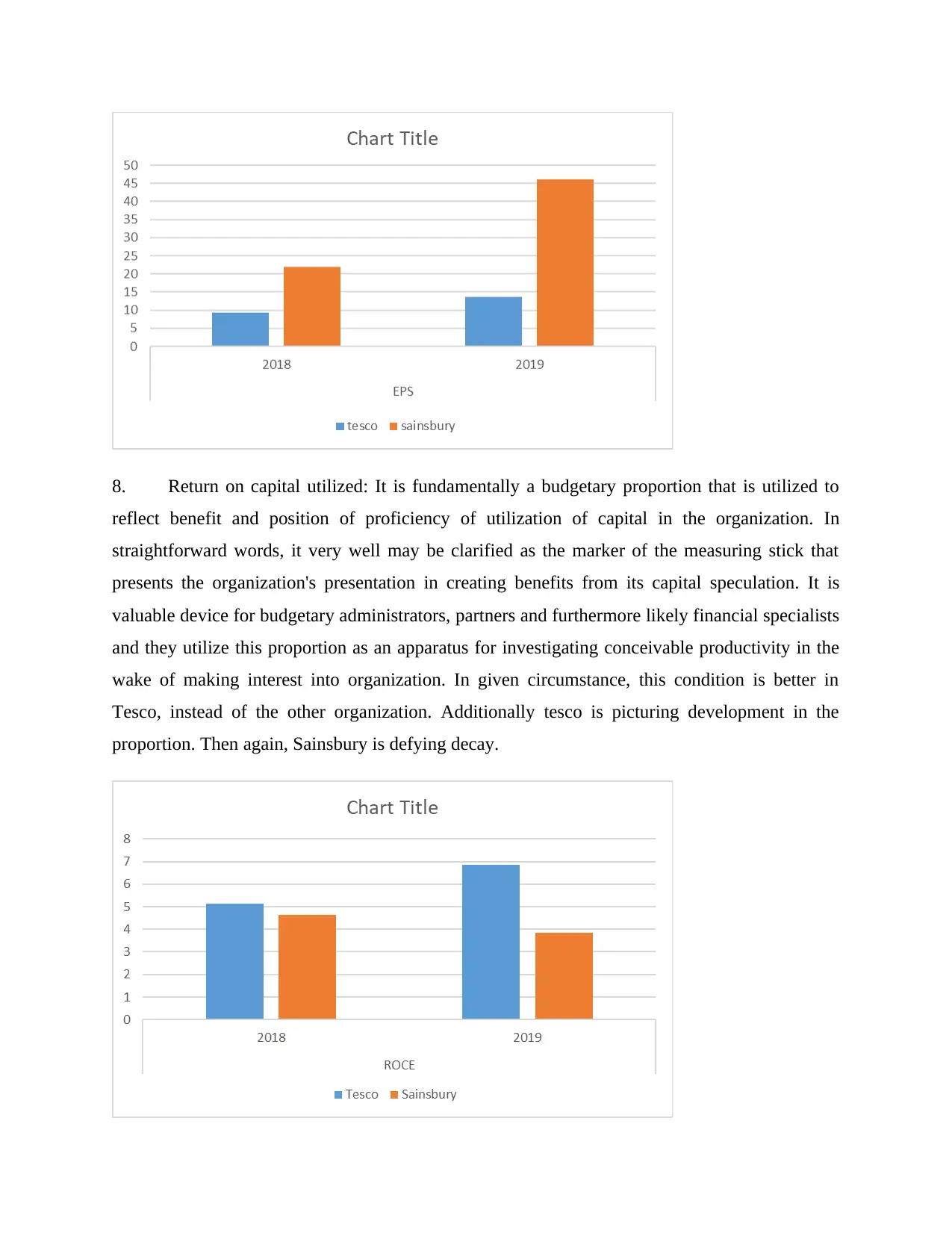

7. Earnings per share: It is essentially the pointer of productivity that is gotten by the

investor. It is determined by partitioning complete organization's benefit by all out number of

exceptional offers on the lookout. It is a typical thought, that higher the EPS, higher will be the

productivity proportion of the organization. In given circumstance, the circumstance is similarly

better in Sainsbury, as the EPS is higher in this organization in correlation with Tesco. The two

organizations are experiencing a development is EPS bar and along these lines, it tends to be

expressed that the two organizations are performing great as far as benefit (Elmassri, Harris and

Carter, 2016).

investor. It is determined by partitioning complete organization's benefit by all out number of

exceptional offers on the lookout. It is a typical thought, that higher the EPS, higher will be the

productivity proportion of the organization. In given circumstance, the circumstance is similarly

better in Sainsbury, as the EPS is higher in this organization in correlation with Tesco. The two

organizations are experiencing a development is EPS bar and along these lines, it tends to be

expressed that the two organizations are performing great as far as benefit (Elmassri, Harris and

Carter, 2016).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8. Return on capital utilized: It is fundamentally a budgetary proportion that is utilized to

reflect benefit and position of proficiency of utilization of capital in the organization. In

straightforward words, it very well may be clarified as the marker of the measuring stick that

presents the organization's presentation in creating benefits from its capital speculation. It is

valuable device for budgetary administrators, partners and furthermore likely financial specialists

and they utilize this proportion as an apparatus for investigating conceivable productivity in the

wake of making interest into organization. In given circumstance, this condition is better in

Tesco, instead of the other organization. Additionally tesco is picturing development in the

proportion. Then again, Sainsbury is defying decay.

reflect benefit and position of proficiency of utilization of capital in the organization. In

straightforward words, it very well may be clarified as the marker of the measuring stick that

presents the organization's presentation in creating benefits from its capital speculation. It is

valuable device for budgetary administrators, partners and furthermore likely financial specialists

and they utilize this proportion as an apparatus for investigating conceivable productivity in the

wake of making interest into organization. In given circumstance, this condition is better in

Tesco, instead of the other organization. Additionally tesco is picturing development in the

proportion. Then again, Sainsbury is defying decay.

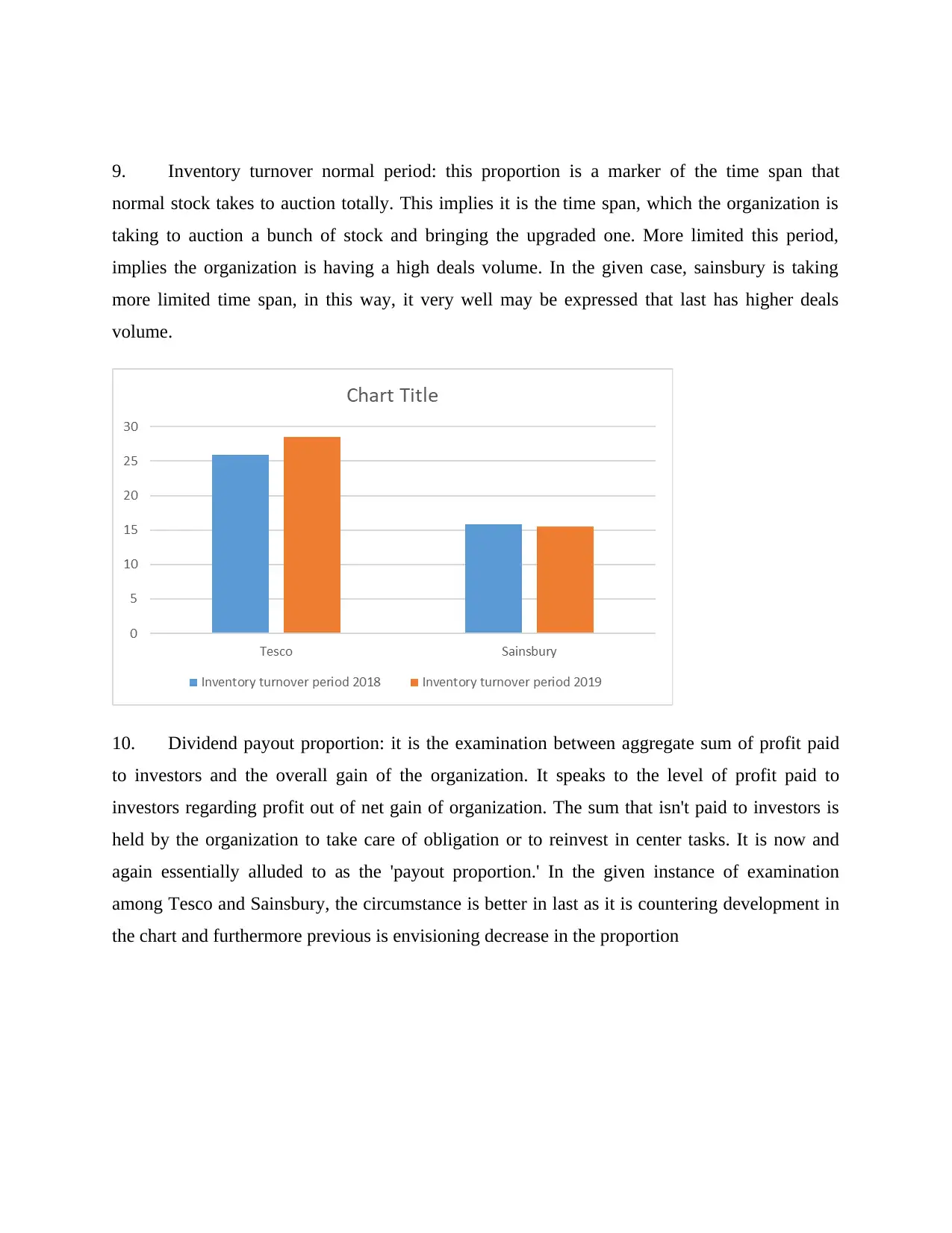

9. Inventory turnover normal period: this proportion is a marker of the time span that

normal stock takes to auction totally. This implies it is the time span, which the organization is

taking to auction a bunch of stock and bringing the upgraded one. More limited this period,

implies the organization is having a high deals volume. In the given case, sainsbury is taking

more limited time span, in this way, it very well may be expressed that last has higher deals

volume.

10. Dividend payout proportion: it is the examination between aggregate sum of profit paid

to investors and the overall gain of the organization. It speaks to the level of profit paid to

investors regarding profit out of net gain of organization. The sum that isn't paid to investors is

held by the organization to take care of obligation or to reinvest in center tasks. It is now and

again essentially alluded to as the 'payout proportion.' In the given instance of examination

among Tesco and Sainsbury, the circumstance is better in last as it is countering development in

the chart and furthermore previous is envisioning decrease in the proportion

normal stock takes to auction totally. This implies it is the time span, which the organization is

taking to auction a bunch of stock and bringing the upgraded one. More limited this period,

implies the organization is having a high deals volume. In the given case, sainsbury is taking

more limited time span, in this way, it very well may be expressed that last has higher deals

volume.

10. Dividend payout proportion: it is the examination between aggregate sum of profit paid

to investors and the overall gain of the organization. It speaks to the level of profit paid to

investors regarding profit out of net gain of organization. The sum that isn't paid to investors is

held by the organization to take care of obligation or to reinvest in center tasks. It is now and

again essentially alluded to as the 'payout proportion.' In the given instance of examination

among Tesco and Sainsbury, the circumstance is better in last as it is countering development in

the chart and furthermore previous is envisioning decrease in the proportion

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.