Managerial Finance Report: Ratio Analysis and Budgeting Techniques

VerifiedAdded on 2020/10/23

|12

|3663

|55

Report

AI Summary

This managerial finance report delves into key aspects of financial management. It begins with an introduction to managerial finance, emphasizing its role in decision-making and strategic planning. The report then proceeds to calculate and interpret various financial ratios, such as gross profit margin, net profit margin, current ratio, quick ratio, gearing ratio, return on capital employed, inventory turnover, and asset turnover, using data from H&M. Furthermore, the report explores the impact of non-financial information on managerial decisions, highlighting the importance of social and sustainability information. The report also examines budgeting techniques, differentiating between fixed and flexible budgeting, and outlining their respective uses. Finally, it contrasts management accounting with financial accounting, explaining their distinct purposes and audiences. The report concludes with a discussion on sources of finance.

``

Managerial Finance

Managerial Finance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

``

Contents

INTRODUCTION...........................................................................................................................3

QUESTION 1...................................................................................................................................3

a). CALUALTION OF RATIOS................................................................................................3

b). INTERPREATAION OF RATIOS.......................................................................................5

c). IMPACT OF NON FINACIAL INFORMATION................................................................5

QUESTION 2...................................................................................................................................6

A. Uses of budget........................................................................................................................6

B. Difference between fix and flexible budgeting......................................................................7

C. Difference between management and financial accounting...................................................8

QUESTION 4...................................................................................................................................9

a). CALCLUATION OF PAYBACK PERIOD..........................................................................9

b). CALCULATION OF ACCOUNITNG RATE OF RETURN...............................................9

c). RECOMMENDATION OF PROJECT.................................................................................9

d). SOURCES OF FINANCE AVAILABLE...........................................................................10

CONCLUSION..............................................................................................................................10

REFRENCES.................................................................................................................................11

Contents

INTRODUCTION...........................................................................................................................3

QUESTION 1...................................................................................................................................3

a). CALUALTION OF RATIOS................................................................................................3

b). INTERPREATAION OF RATIOS.......................................................................................5

c). IMPACT OF NON FINACIAL INFORMATION................................................................5

QUESTION 2...................................................................................................................................6

A. Uses of budget........................................................................................................................6

B. Difference between fix and flexible budgeting......................................................................7

C. Difference between management and financial accounting...................................................8

QUESTION 4...................................................................................................................................9

a). CALCLUATION OF PAYBACK PERIOD..........................................................................9

b). CALCULATION OF ACCOUNITNG RATE OF RETURN...............................................9

c). RECOMMENDATION OF PROJECT.................................................................................9

d). SOURCES OF FINANCE AVAILABLE...........................................................................10

CONCLUSION..............................................................................................................................10

REFRENCES.................................................................................................................................11

``

INTRODUCTION

Managerial finance is a field of finance which concern itself with the significance of finance

technique in managerial aspects (Gitman, Juchau and Flanagan, 2015). It is an approach which

is interdisciplinary which borrows from both corporate finance and managerial accounting. It

helps the managers to take necessary decisions for the company to take competitive advantage

over its competitors and improve its financial positions. It provides an aid to monitoring and

implementation of business strategies which help mangers to achieve its business objectives. The

following report contains the financial ratios which help mangers to take decisions. This report

also consists of the various budgeting techniques used by mangers to prepare the budgets. It also

explains the difference between financial accounting and management accounting. This reports

also contains the details of the various financing methods and different sources of finance

available with the companies.

QUESTION 1

a). CALUALTION OF RATIOS

Financial ratio: Financial ratio are the key indicators of the various financial

performance of the company which are usually derived from the company’s three statements

which includes balance sheets, income statements and cash flow statements (Coles, Lemmon and

Meschke, 2012). These ratios are used by the top level management to analyse company’s

liquidity, profitability and its financial stability. Following are some financial ratios which help

companies to check their stability:

Gross profit margin: It is a metric which is used by the company to assess its business

model and financial health by showing the total amount of money which is earned by the

company sales after deducting the cost which a company incurred in manufacturing that

product.

Net profit margin: Net profit margin is the profit which is generated by company’s

operations. It shows the percentage of revenue generated by its operations after adjusting

its both direct and indirect expenses. It is also called considered as a company’s bottom

line. It is usually determined in the percentage form or decimal.

3

INTRODUCTION

Managerial finance is a field of finance which concern itself with the significance of finance

technique in managerial aspects (Gitman, Juchau and Flanagan, 2015). It is an approach which

is interdisciplinary which borrows from both corporate finance and managerial accounting. It

helps the managers to take necessary decisions for the company to take competitive advantage

over its competitors and improve its financial positions. It provides an aid to monitoring and

implementation of business strategies which help mangers to achieve its business objectives. The

following report contains the financial ratios which help mangers to take decisions. This report

also consists of the various budgeting techniques used by mangers to prepare the budgets. It also

explains the difference between financial accounting and management accounting. This reports

also contains the details of the various financing methods and different sources of finance

available with the companies.

QUESTION 1

a). CALUALTION OF RATIOS

Financial ratio: Financial ratio are the key indicators of the various financial

performance of the company which are usually derived from the company’s three statements

which includes balance sheets, income statements and cash flow statements (Coles, Lemmon and

Meschke, 2012). These ratios are used by the top level management to analyse company’s

liquidity, profitability and its financial stability. Following are some financial ratios which help

companies to check their stability:

Gross profit margin: It is a metric which is used by the company to assess its business

model and financial health by showing the total amount of money which is earned by the

company sales after deducting the cost which a company incurred in manufacturing that

product.

Net profit margin: Net profit margin is the profit which is generated by company’s

operations. It shows the percentage of revenue generated by its operations after adjusting

its both direct and indirect expenses. It is also called considered as a company’s bottom

line. It is usually determined in the percentage form or decimal.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

``

Current ratio: The current ratio is a liquidity ratio which helps mangers to find out the

company’s ability to pay off its short term liabilities which are due within the one year. It

also tells the investors and analyses that how a company can maximize its current assets

to satisfy their current liabilities.

Quick ratio: It is an indicator used by the companies to find out the company’s short

term liquidity position (Park and Jang, 2014). It helps managers to measure the

company’s ability to meet their short term obligations which they can meet with its most

of its liquid assets. It indicates the company’s ability to quickly convert its assets into

cash.

Gearing ratio (Debt/equity): Gearing Ratio is considered as a broad category of

financial ratios. Accountants, investors, lenders and company executive uses the gearing

ratios in order to measure the relation between the debts and the owner’s equity.

Return on capital employed: ROC is a financial ratio which measures the company’s

profitability and its efficiency to which company uses its capital. Return on Capital

Employed is a ratio which measures that how well a company can generate profit from its

capital which is employed by the business owners. It is considered as an important ratio

in determining the profitability and is also used by investors while screening for suitable

investments.

Inventory turnover: Inventory turnover is a ratio which shows the company that in a

given period of time how many times a company has replaced its inventory and sold its

goods. It also helps the company to find out the average time required by a company to

sell its inventory (Parkinson, 2012). It helps mangers to meaning full decisions on

manufacturing, purchasing, marketing and pricing its new inventory.

Asset turnover: This is a ratio which helps companies to find out the value of company’s

sales which is directly relative to the value of its assets. Assets turnover is used as a

efficiency indicators by company for the assets which is used to generate revenue.

Following are the calculation of all the ratios of a H & M

2016 2017

4

Current ratio: The current ratio is a liquidity ratio which helps mangers to find out the

company’s ability to pay off its short term liabilities which are due within the one year. It

also tells the investors and analyses that how a company can maximize its current assets

to satisfy their current liabilities.

Quick ratio: It is an indicator used by the companies to find out the company’s short

term liquidity position (Park and Jang, 2014). It helps managers to measure the

company’s ability to meet their short term obligations which they can meet with its most

of its liquid assets. It indicates the company’s ability to quickly convert its assets into

cash.

Gearing ratio (Debt/equity): Gearing Ratio is considered as a broad category of

financial ratios. Accountants, investors, lenders and company executive uses the gearing

ratios in order to measure the relation between the debts and the owner’s equity.

Return on capital employed: ROC is a financial ratio which measures the company’s

profitability and its efficiency to which company uses its capital. Return on Capital

Employed is a ratio which measures that how well a company can generate profit from its

capital which is employed by the business owners. It is considered as an important ratio

in determining the profitability and is also used by investors while screening for suitable

investments.

Inventory turnover: Inventory turnover is a ratio which shows the company that in a

given period of time how many times a company has replaced its inventory and sold its

goods. It also helps the company to find out the average time required by a company to

sell its inventory (Parkinson, 2012). It helps mangers to meaning full decisions on

manufacturing, purchasing, marketing and pricing its new inventory.

Asset turnover: This is a ratio which helps companies to find out the value of company’s

sales which is directly relative to the value of its assets. Assets turnover is used as a

efficiency indicators by company for the assets which is used to generate revenue.

Following are the calculation of all the ratios of a H & M

2016 2017

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

``

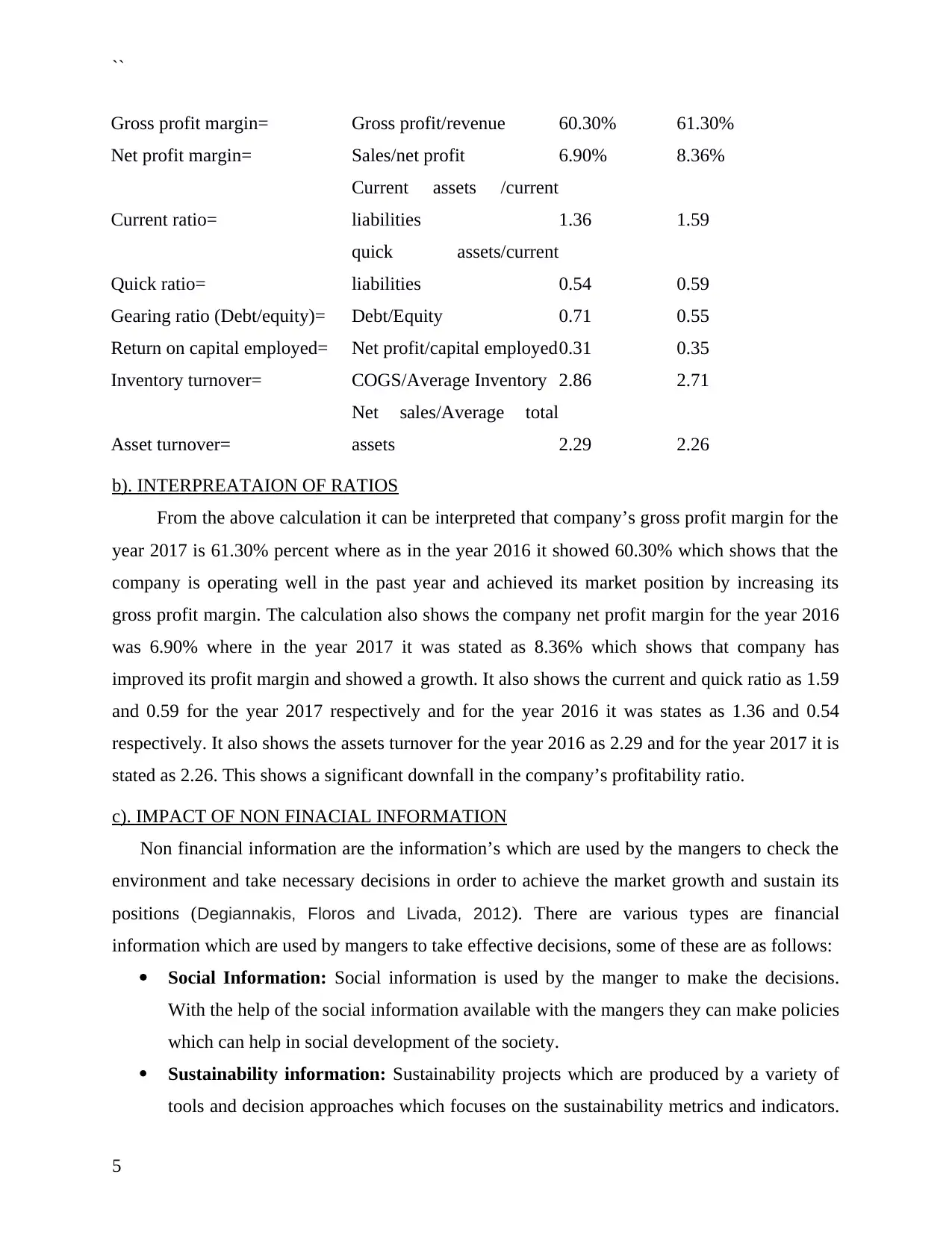

Gross profit margin= Gross profit/revenue 60.30% 61.30%

Net profit margin= Sales/net profit 6.90% 8.36%

Current ratio=

Current assets /current

liabilities 1.36 1.59

Quick ratio=

quick assets/current

liabilities 0.54 0.59

Gearing ratio (Debt/equity)= Debt/Equity 0.71 0.55

Return on capital employed= Net profit/capital employed0.31 0.35

Inventory turnover= COGS/Average Inventory 2.86 2.71

Asset turnover=

Net sales/Average total

assets 2.29 2.26

b). INTERPREATAION OF RATIOS

From the above calculation it can be interpreted that company’s gross profit margin for the

year 2017 is 61.30% percent where as in the year 2016 it showed 60.30% which shows that the

company is operating well in the past year and achieved its market position by increasing its

gross profit margin. The calculation also shows the company net profit margin for the year 2016

was 6.90% where in the year 2017 it was stated as 8.36% which shows that company has

improved its profit margin and showed a growth. It also shows the current and quick ratio as 1.59

and 0.59 for the year 2017 respectively and for the year 2016 it was states as 1.36 and 0.54

respectively. It also shows the assets turnover for the year 2016 as 2.29 and for the year 2017 it is

stated as 2.26. This shows a significant downfall in the company’s profitability ratio.

c). IMPACT OF NON FINACIAL INFORMATION

Non financial information are the information’s which are used by the mangers to check the

environment and take necessary decisions in order to achieve the market growth and sustain its

positions (Degiannakis, Floros and Livada, 2012). There are various types are financial

information which are used by mangers to take effective decisions, some of these are as follows:

Social Information: Social information is used by the manger to make the decisions.

With the help of the social information available with the mangers they can make policies

which can help in social development of the society.

Sustainability information: Sustainability projects which are produced by a variety of

tools and decision approaches which focuses on the sustainability metrics and indicators.

5

Gross profit margin= Gross profit/revenue 60.30% 61.30%

Net profit margin= Sales/net profit 6.90% 8.36%

Current ratio=

Current assets /current

liabilities 1.36 1.59

Quick ratio=

quick assets/current

liabilities 0.54 0.59

Gearing ratio (Debt/equity)= Debt/Equity 0.71 0.55

Return on capital employed= Net profit/capital employed0.31 0.35

Inventory turnover= COGS/Average Inventory 2.86 2.71

Asset turnover=

Net sales/Average total

assets 2.29 2.26

b). INTERPREATAION OF RATIOS

From the above calculation it can be interpreted that company’s gross profit margin for the

year 2017 is 61.30% percent where as in the year 2016 it showed 60.30% which shows that the

company is operating well in the past year and achieved its market position by increasing its

gross profit margin. The calculation also shows the company net profit margin for the year 2016

was 6.90% where in the year 2017 it was stated as 8.36% which shows that company has

improved its profit margin and showed a growth. It also shows the current and quick ratio as 1.59

and 0.59 for the year 2017 respectively and for the year 2016 it was states as 1.36 and 0.54

respectively. It also shows the assets turnover for the year 2016 as 2.29 and for the year 2017 it is

stated as 2.26. This shows a significant downfall in the company’s profitability ratio.

c). IMPACT OF NON FINACIAL INFORMATION

Non financial information are the information’s which are used by the mangers to check the

environment and take necessary decisions in order to achieve the market growth and sustain its

positions (Degiannakis, Floros and Livada, 2012). There are various types are financial

information which are used by mangers to take effective decisions, some of these are as follows:

Social Information: Social information is used by the manger to make the decisions.

With the help of the social information available with the mangers they can make policies

which can help in social development of the society.

Sustainability information: Sustainability projects which are produced by a variety of

tools and decision approaches which focuses on the sustainability metrics and indicators.

5

``

This information is required by the mangers to take decisions in order to improve the

company’s sustainability in the market and improve its financial position.

QUESTION 2

A. Uses of budget

Budget: It is an estimation of incomes and expenditures for a future period in order to

reduce possibility of losses and issues such as lack of financial resources (Chen, Yang and Lin,

2012). It is detailed financial plan which is based upon past years data and carry information for

future. Managers distribute budget to all the functional departments of the company so that they

can operate all the business activities in appropriate manner. Main purpose of formulating

budgets to allocate monetary resources properly, form plans, facilitate coordination, control

activities of employees and motivation them. It is tool which is used by top executives in process

of decision making, monitor actual and budget performance and estimate future incomes and

expenditures that may take place in upcoming period. With the help of effective and efficient

budgeting limited resources can be managed in an appropriate manner. In other words, it can also

be defined as a plan to spend the monetary resources. The process of formulating this plan is

known as budgeting. In order to form it managers analyse various aspects such as studying

previous year’s data, determine future expenses and then formulate a budget. Afterwards it is

presented in front of top executives for their approval. When they approve it then it is

implemented within the company in order to manage all the money related activities. It is used

by organisation for different purposes. All its uses are as follows:

Main use of budget is to track expenses of the company in which managers can figure out

that where the organisation has spent extra money. It helps to formulate effective

decisions for the purpose of controlling overspending of monetary resources. Keeping

detailed record can help to track expenditures in detail.

Another use of budget is to limit spending of business entity. It helps to determine that

what amount of money is being spent by company on monthly basis and then formulate

plans to stop them.

Budgets are formulated for the purpose of attain financial goals of organisation by

reducing unnecessary expenses and enhances funds for business activities (Caglayan and

Demir, 2014).

6

This information is required by the mangers to take decisions in order to improve the

company’s sustainability in the market and improve its financial position.

QUESTION 2

A. Uses of budget

Budget: It is an estimation of incomes and expenditures for a future period in order to

reduce possibility of losses and issues such as lack of financial resources (Chen, Yang and Lin,

2012). It is detailed financial plan which is based upon past years data and carry information for

future. Managers distribute budget to all the functional departments of the company so that they

can operate all the business activities in appropriate manner. Main purpose of formulating

budgets to allocate monetary resources properly, form plans, facilitate coordination, control

activities of employees and motivation them. It is tool which is used by top executives in process

of decision making, monitor actual and budget performance and estimate future incomes and

expenditures that may take place in upcoming period. With the help of effective and efficient

budgeting limited resources can be managed in an appropriate manner. In other words, it can also

be defined as a plan to spend the monetary resources. The process of formulating this plan is

known as budgeting. In order to form it managers analyse various aspects such as studying

previous year’s data, determine future expenses and then formulate a budget. Afterwards it is

presented in front of top executives for their approval. When they approve it then it is

implemented within the company in order to manage all the money related activities. It is used

by organisation for different purposes. All its uses are as follows:

Main use of budget is to track expenses of the company in which managers can figure out

that where the organisation has spent extra money. It helps to formulate effective

decisions for the purpose of controlling overspending of monetary resources. Keeping

detailed record can help to track expenditures in detail.

Another use of budget is to limit spending of business entity. It helps to determine that

what amount of money is being spent by company on monthly basis and then formulate

plans to stop them.

Budgets are formulated for the purpose of attain financial goals of organisation by

reducing unnecessary expenses and enhances funds for business activities (Caglayan and

Demir, 2014).

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

``

In order to build business wealth business entities, formulate budgets which helps to

spend money appropriately and control them properly and appropriately.

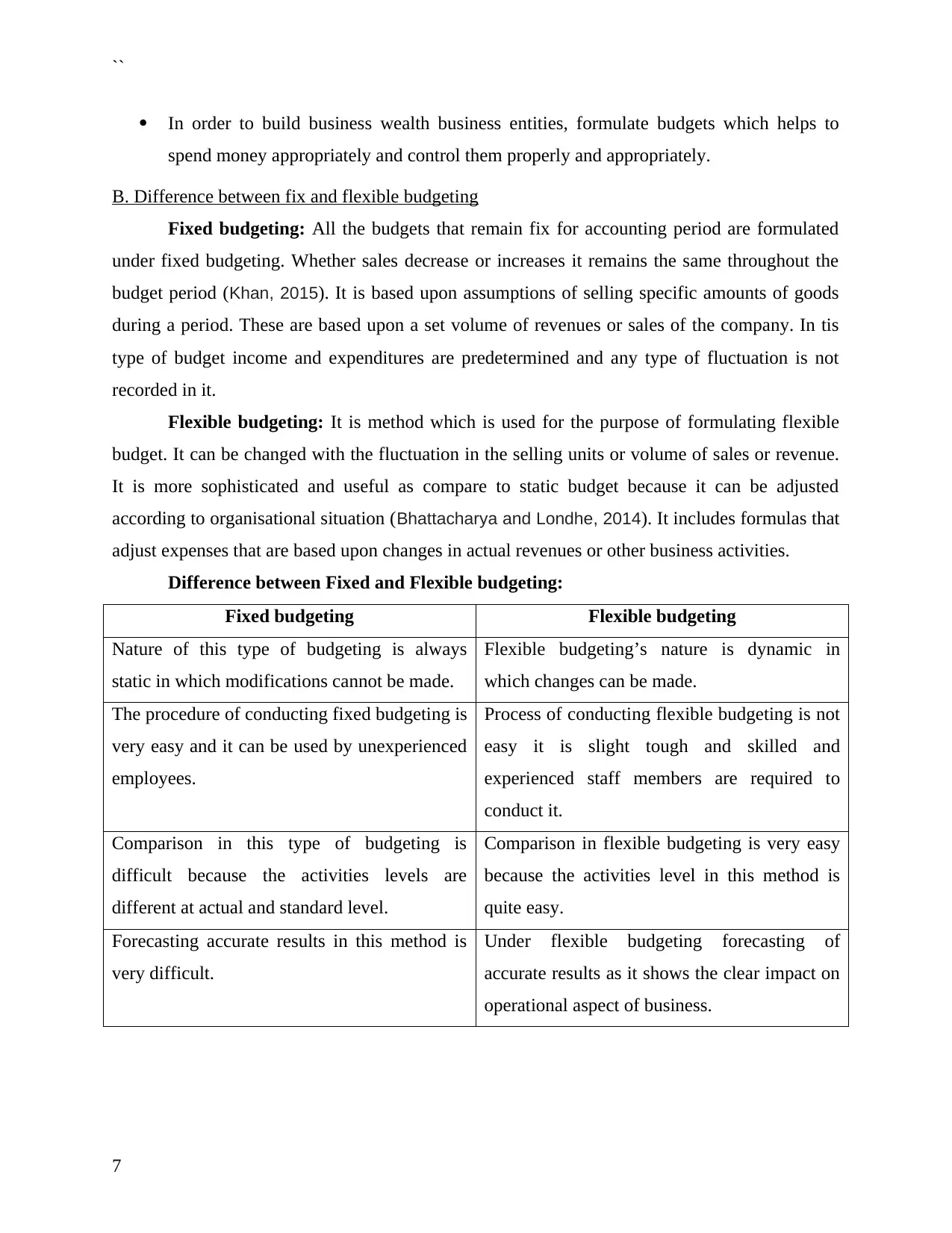

B. Difference between fix and flexible budgeting

Fixed budgeting: All the budgets that remain fix for accounting period are formulated

under fixed budgeting. Whether sales decrease or increases it remains the same throughout the

budget period (Khan, 2015). It is based upon assumptions of selling specific amounts of goods

during a period. These are based upon a set volume of revenues or sales of the company. In tis

type of budget income and expenditures are predetermined and any type of fluctuation is not

recorded in it.

Flexible budgeting: It is method which is used for the purpose of formulating flexible

budget. It can be changed with the fluctuation in the selling units or volume of sales or revenue.

It is more sophisticated and useful as compare to static budget because it can be adjusted

according to organisational situation (Bhattacharya and Londhe, 2014). It includes formulas that

adjust expenses that are based upon changes in actual revenues or other business activities.

Difference between Fixed and Flexible budgeting:

Fixed budgeting Flexible budgeting

Nature of this type of budgeting is always

static in which modifications cannot be made.

Flexible budgeting’s nature is dynamic in

which changes can be made.

The procedure of conducting fixed budgeting is

very easy and it can be used by unexperienced

employees.

Process of conducting flexible budgeting is not

easy it is slight tough and skilled and

experienced staff members are required to

conduct it.

Comparison in this type of budgeting is

difficult because the activities levels are

different at actual and standard level.

Comparison in flexible budgeting is very easy

because the activities level in this method is

quite easy.

Forecasting accurate results in this method is

very difficult.

Under flexible budgeting forecasting of

accurate results as it shows the clear impact on

operational aspect of business.

7

In order to build business wealth business entities, formulate budgets which helps to

spend money appropriately and control them properly and appropriately.

B. Difference between fix and flexible budgeting

Fixed budgeting: All the budgets that remain fix for accounting period are formulated

under fixed budgeting. Whether sales decrease or increases it remains the same throughout the

budget period (Khan, 2015). It is based upon assumptions of selling specific amounts of goods

during a period. These are based upon a set volume of revenues or sales of the company. In tis

type of budget income and expenditures are predetermined and any type of fluctuation is not

recorded in it.

Flexible budgeting: It is method which is used for the purpose of formulating flexible

budget. It can be changed with the fluctuation in the selling units or volume of sales or revenue.

It is more sophisticated and useful as compare to static budget because it can be adjusted

according to organisational situation (Bhattacharya and Londhe, 2014). It includes formulas that

adjust expenses that are based upon changes in actual revenues or other business activities.

Difference between Fixed and Flexible budgeting:

Fixed budgeting Flexible budgeting

Nature of this type of budgeting is always

static in which modifications cannot be made.

Flexible budgeting’s nature is dynamic in

which changes can be made.

The procedure of conducting fixed budgeting is

very easy and it can be used by unexperienced

employees.

Process of conducting flexible budgeting is not

easy it is slight tough and skilled and

experienced staff members are required to

conduct it.

Comparison in this type of budgeting is

difficult because the activities levels are

different at actual and standard level.

Comparison in flexible budgeting is very easy

because the activities level in this method is

quite easy.

Forecasting accurate results in this method is

very difficult.

Under flexible budgeting forecasting of

accurate results as it shows the clear impact on

operational aspect of business.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

``

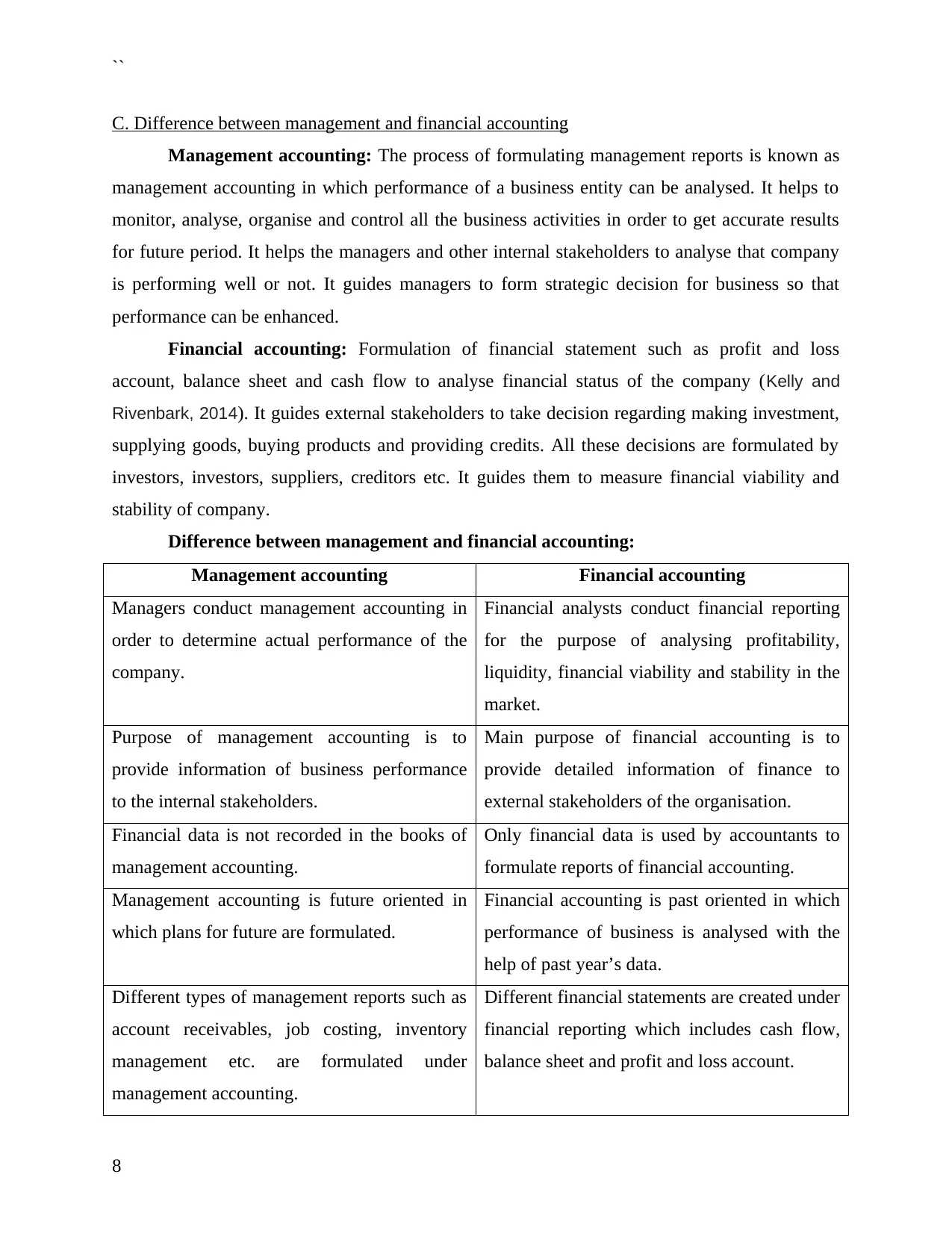

C. Difference between management and financial accounting

Management accounting: The process of formulating management reports is known as

management accounting in which performance of a business entity can be analysed. It helps to

monitor, analyse, organise and control all the business activities in order to get accurate results

for future period. It helps the managers and other internal stakeholders to analyse that company

is performing well or not. It guides managers to form strategic decision for business so that

performance can be enhanced.

Financial accounting: Formulation of financial statement such as profit and loss

account, balance sheet and cash flow to analyse financial status of the company (Kelly and

Rivenbark, 2014). It guides external stakeholders to take decision regarding making investment,

supplying goods, buying products and providing credits. All these decisions are formulated by

investors, investors, suppliers, creditors etc. It guides them to measure financial viability and

stability of company.

Difference between management and financial accounting:

Management accounting Financial accounting

Managers conduct management accounting in

order to determine actual performance of the

company.

Financial analysts conduct financial reporting

for the purpose of analysing profitability,

liquidity, financial viability and stability in the

market.

Purpose of management accounting is to

provide information of business performance

to the internal stakeholders.

Main purpose of financial accounting is to

provide detailed information of finance to

external stakeholders of the organisation.

Financial data is not recorded in the books of

management accounting.

Only financial data is used by accountants to

formulate reports of financial accounting.

Management accounting is future oriented in

which plans for future are formulated.

Financial accounting is past oriented in which

performance of business is analysed with the

help of past year’s data.

Different types of management reports such as

account receivables, job costing, inventory

management etc. are formulated under

management accounting.

Different financial statements are created under

financial reporting which includes cash flow,

balance sheet and profit and loss account.

8

C. Difference between management and financial accounting

Management accounting: The process of formulating management reports is known as

management accounting in which performance of a business entity can be analysed. It helps to

monitor, analyse, organise and control all the business activities in order to get accurate results

for future period. It helps the managers and other internal stakeholders to analyse that company

is performing well or not. It guides managers to form strategic decision for business so that

performance can be enhanced.

Financial accounting: Formulation of financial statement such as profit and loss

account, balance sheet and cash flow to analyse financial status of the company (Kelly and

Rivenbark, 2014). It guides external stakeholders to take decision regarding making investment,

supplying goods, buying products and providing credits. All these decisions are formulated by

investors, investors, suppliers, creditors etc. It guides them to measure financial viability and

stability of company.

Difference between management and financial accounting:

Management accounting Financial accounting

Managers conduct management accounting in

order to determine actual performance of the

company.

Financial analysts conduct financial reporting

for the purpose of analysing profitability,

liquidity, financial viability and stability in the

market.

Purpose of management accounting is to

provide information of business performance

to the internal stakeholders.

Main purpose of financial accounting is to

provide detailed information of finance to

external stakeholders of the organisation.

Financial data is not recorded in the books of

management accounting.

Only financial data is used by accountants to

formulate reports of financial accounting.

Management accounting is future oriented in

which plans for future are formulated.

Financial accounting is past oriented in which

performance of business is analysed with the

help of past year’s data.

Different types of management reports such as

account receivables, job costing, inventory

management etc. are formulated under

management accounting.

Different financial statements are created under

financial reporting which includes cash flow,

balance sheet and profit and loss account.

8

``

QUESTION 3

a). Calculation of the budgeted production cost per unit

Income statement under ABC costing

Particulars X Y Z

Product units 23000 19500 18000

Direct material 644000 487500 396000

Direct labour 713000 663000 486000

Direct expenses 0 0 0

Prime cost 1380000 1170000 900000

Add: overhead cost driver rate

Machine Set up cost

95454.545

4545455

65454.545

4545455

139090.90

9090909

Material ordering costs 69750 42750 103500

Machine running costs

126237.62

3762376

84158.415

8415841

129603.96

039604

General facility costs

212413.36

6336634

141608.91

0891089

218077.72

2772277

Total costs

1883855.5

3555356

1503971.8

7218722

1490272.5

9225923

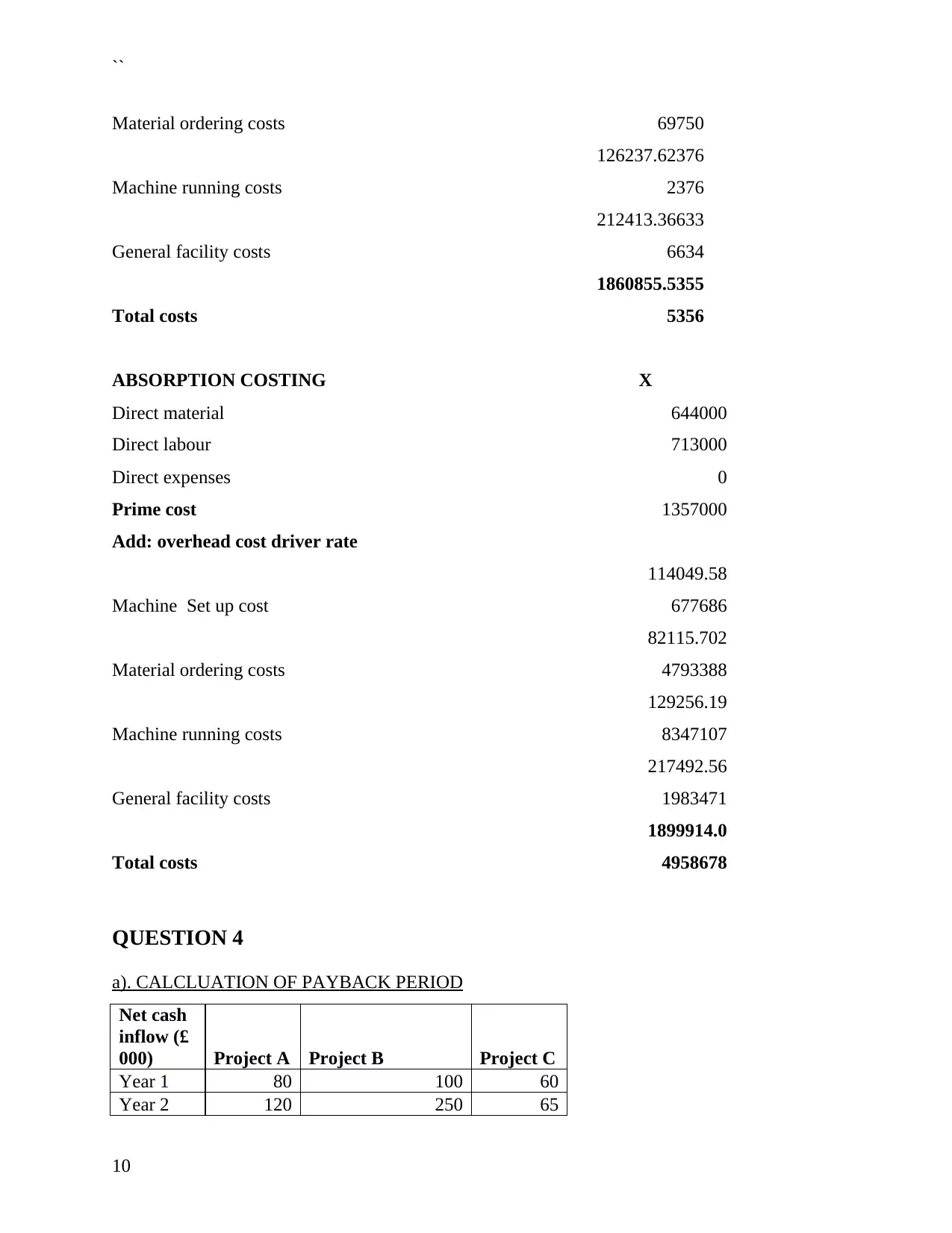

b). Comparative calculations using absorption costing method and ABC method

ABC COSTING X

Direct material 644000

Direct labour 713000

Direct expenses 0

Prime cost 1357000

Add: overhead cost driver rate

Machine Set up cost

95454.545454

5455

9

QUESTION 3

a). Calculation of the budgeted production cost per unit

Income statement under ABC costing

Particulars X Y Z

Product units 23000 19500 18000

Direct material 644000 487500 396000

Direct labour 713000 663000 486000

Direct expenses 0 0 0

Prime cost 1380000 1170000 900000

Add: overhead cost driver rate

Machine Set up cost

95454.545

4545455

65454.545

4545455

139090.90

9090909

Material ordering costs 69750 42750 103500

Machine running costs

126237.62

3762376

84158.415

8415841

129603.96

039604

General facility costs

212413.36

6336634

141608.91

0891089

218077.72

2772277

Total costs

1883855.5

3555356

1503971.8

7218722

1490272.5

9225923

b). Comparative calculations using absorption costing method and ABC method

ABC COSTING X

Direct material 644000

Direct labour 713000

Direct expenses 0

Prime cost 1357000

Add: overhead cost driver rate

Machine Set up cost

95454.545454

5455

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

``

Material ordering costs 69750

Machine running costs

126237.62376

2376

General facility costs

212413.36633

6634

Total costs

1860855.5355

5356

ABSORPTION COSTING X

Direct material 644000

Direct labour 713000

Direct expenses 0

Prime cost 1357000

Add: overhead cost driver rate

Machine Set up cost

114049.58

677686

Material ordering costs

82115.702

4793388

Machine running costs

129256.19

8347107

General facility costs

217492.56

1983471

Total costs

1899914.0

4958678

QUESTION 4

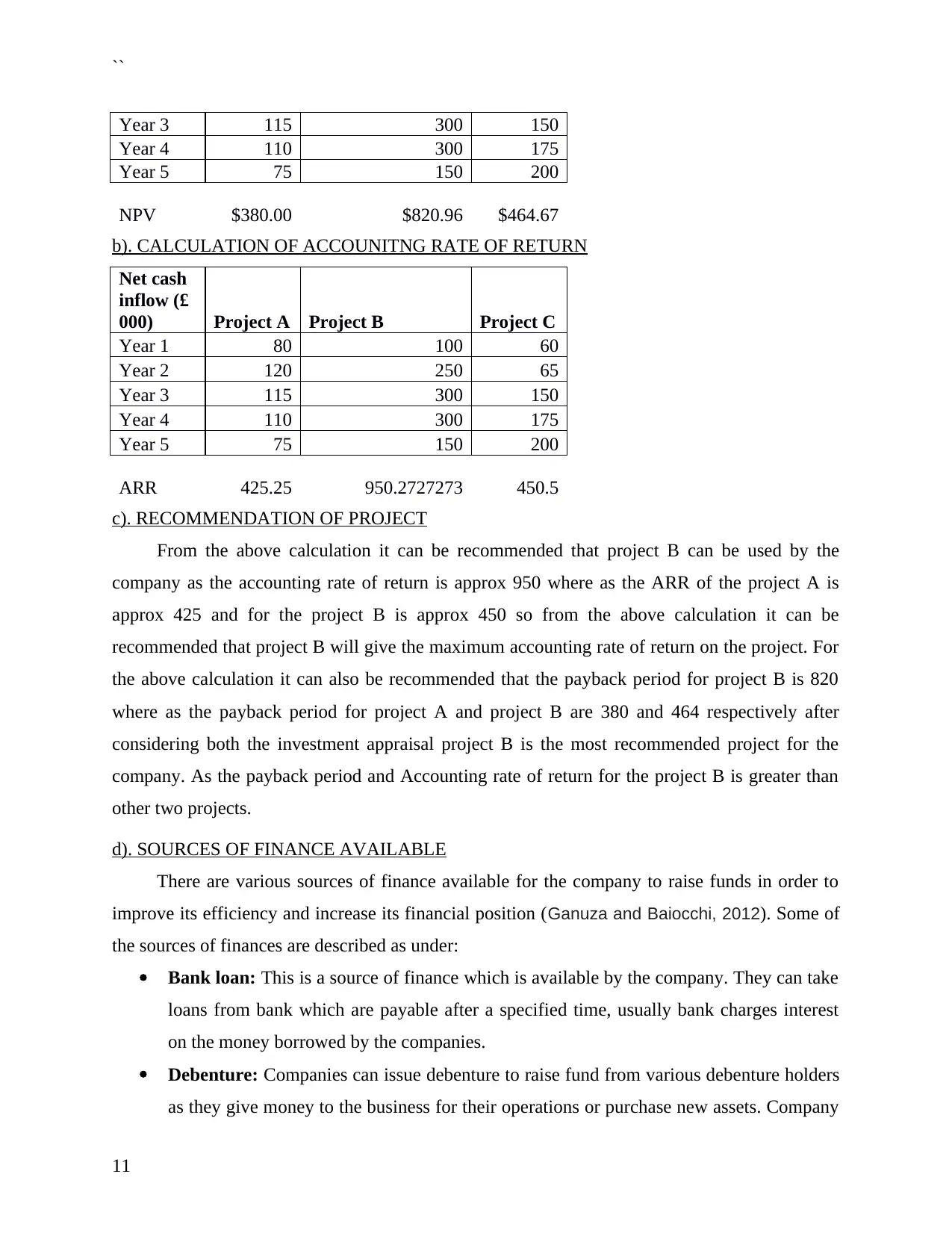

a). CALCLUATION OF PAYBACK PERIOD

Net cash

inflow (£

000) Project A Project B Project C

Year 1 80 100 60

Year 2 120 250 65

10

Material ordering costs 69750

Machine running costs

126237.62376

2376

General facility costs

212413.36633

6634

Total costs

1860855.5355

5356

ABSORPTION COSTING X

Direct material 644000

Direct labour 713000

Direct expenses 0

Prime cost 1357000

Add: overhead cost driver rate

Machine Set up cost

114049.58

677686

Material ordering costs

82115.702

4793388

Machine running costs

129256.19

8347107

General facility costs

217492.56

1983471

Total costs

1899914.0

4958678

QUESTION 4

a). CALCLUATION OF PAYBACK PERIOD

Net cash

inflow (£

000) Project A Project B Project C

Year 1 80 100 60

Year 2 120 250 65

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

``

Year 3 115 300 150

Year 4 110 300 175

Year 5 75 150 200

NPV $380.00 $820.96 $464.67

b). CALCULATION OF ACCOUNITNG RATE OF RETURN

Net cash

inflow (£

000) Project A Project B Project C

Year 1 80 100 60

Year 2 120 250 65

Year 3 115 300 150

Year 4 110 300 175

Year 5 75 150 200

ARR 425.25 950.2727273 450.5

c). RECOMMENDATION OF PROJECT

From the above calculation it can be recommended that project B can be used by the

company as the accounting rate of return is approx 950 where as the ARR of the project A is

approx 425 and for the project B is approx 450 so from the above calculation it can be

recommended that project B will give the maximum accounting rate of return on the project. For

the above calculation it can also be recommended that the payback period for project B is 820

where as the payback period for project A and project B are 380 and 464 respectively after

considering both the investment appraisal project B is the most recommended project for the

company. As the payback period and Accounting rate of return for the project B is greater than

other two projects.

d). SOURCES OF FINANCE AVAILABLE

There are various sources of finance available for the company to raise funds in order to

improve its efficiency and increase its financial position (Ganuza and Baiocchi, 2012). Some of

the sources of finances are described as under:

Bank loan: This is a source of finance which is available by the company. They can take

loans from bank which are payable after a specified time, usually bank charges interest

on the money borrowed by the companies.

Debenture: Companies can issue debenture to raise fund from various debenture holders

as they give money to the business for their operations or purchase new assets. Company

11

Year 3 115 300 150

Year 4 110 300 175

Year 5 75 150 200

NPV $380.00 $820.96 $464.67

b). CALCULATION OF ACCOUNITNG RATE OF RETURN

Net cash

inflow (£

000) Project A Project B Project C

Year 1 80 100 60

Year 2 120 250 65

Year 3 115 300 150

Year 4 110 300 175

Year 5 75 150 200

ARR 425.25 950.2727273 450.5

c). RECOMMENDATION OF PROJECT

From the above calculation it can be recommended that project B can be used by the

company as the accounting rate of return is approx 950 where as the ARR of the project A is

approx 425 and for the project B is approx 450 so from the above calculation it can be

recommended that project B will give the maximum accounting rate of return on the project. For

the above calculation it can also be recommended that the payback period for project B is 820

where as the payback period for project A and project B are 380 and 464 respectively after

considering both the investment appraisal project B is the most recommended project for the

company. As the payback period and Accounting rate of return for the project B is greater than

other two projects.

d). SOURCES OF FINANCE AVAILABLE

There are various sources of finance available for the company to raise funds in order to

improve its efficiency and increase its financial position (Ganuza and Baiocchi, 2012). Some of

the sources of finances are described as under:

Bank loan: This is a source of finance which is available by the company. They can take

loans from bank which are payable after a specified time, usually bank charges interest

on the money borrowed by the companies.

Debenture: Companies can issue debenture to raise fund from various debenture holders

as they give money to the business for their operations or purchase new assets. Company

11

``

has the liability to pay interest to these debenture holders usually fixed before issuing

these debentures.

Equity share capital: companies can issue equity shares in the companies in order to

raise the funds to carry out its operations or acquire new assets. By issuing these share

companies give right to the share holders to take part in the decision making process in

the company. They are called as a owners of a company in return companies have to pay

dividends, it is not necessary for the companies to pay dividends every year.

CONCLUSION

From the above file it can be concluded that managerial finance plays an important in the

decision making process in order to survive in the market and sustain its market position. The

above report also establishes that the financial ratios are the important factor to determine the

financial positions of the company with the help of these ratios companies can find their liquidity

position and their ability to pay of its current liabilities with the help of current assets. It also

explains the various sources of the finance available for the company to raise its funds for

acquiring new assets and improving efficiency of its operations.

12

has the liability to pay interest to these debenture holders usually fixed before issuing

these debentures.

Equity share capital: companies can issue equity shares in the companies in order to

raise the funds to carry out its operations or acquire new assets. By issuing these share

companies give right to the share holders to take part in the decision making process in

the company. They are called as a owners of a company in return companies have to pay

dividends, it is not necessary for the companies to pay dividends every year.

CONCLUSION

From the above file it can be concluded that managerial finance plays an important in the

decision making process in order to survive in the market and sustain its market position. The

above report also establishes that the financial ratios are the important factor to determine the

financial positions of the company with the help of these ratios companies can find their liquidity

position and their ability to pay of its current liabilities with the help of current assets. It also

explains the various sources of the finance available for the company to raise its funds for

acquiring new assets and improving efficiency of its operations.

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.