Managerial Finance Report: Capital Budgeting Analysis - RWE Enterprise

VerifiedAdded on 2021/06/17

|12

|2679

|71

Report

AI Summary

This report provides a detailed analysis of capital budgeting techniques applied to investment decisions for RWE Enterprise Pty Ltd. The report begins by evaluating a new plant investment, calculating Net Present Value (NPV), Internal Rate of Return (IRR), and payback period to determine its financial viability. It includes a visual representation of cash flows and a discussion of the project's profitability. The second part of the report compares two potential projects, employing the same capital budgeting methods (NPV, IRR, and payback period) to assess their suitability for investment, considering both independent and mutually exclusive scenarios. The analysis includes ranking the projects based on their financial metrics, providing recommendations for the management's decision-making process. The report emphasizes the importance of these techniques in evaluating and selecting profitable investments.

Running head: MANAGERIAL FINANCE

Managerial Finance

Name of the Student:

Name of the University:

Author’s Note

Managerial Finance

Name of the Student:

Name of the University:

Author’s Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

MANAGERIAL FINANCE

Table of Contents

Answer to Question 1......................................................................................................................2

Answer to Question 2......................................................................................................................6

Calculation of NPV, IRR and Payback Period for Project A and Project B...............................6

Analysis of the Results................................................................................................................7

Ranking of Projects......................................................................................................................8

Reference.......................................................................................................................................10

MANAGERIAL FINANCE

Table of Contents

Answer to Question 1......................................................................................................................2

Answer to Question 2......................................................................................................................6

Calculation of NPV, IRR and Payback Period for Project A and Project B...............................6

Analysis of the Results................................................................................................................7

Ranking of Projects......................................................................................................................8

Reference.......................................................................................................................................10

2

MANAGERIAL FINANCE

Answer to Question 1

As per the case study which is provided in the question, RWE Enterprise Pty ltd is

engaged in manufacturing business which is located in Brisbane. The company is planning to set

up a new plant which has an upfront cost of $ 3 million. The management of RWE Enterprise

wants to decide whether the business should invest in the project or not. For the purpose of

taking an appropriate decision, the management has decided to conduct capital budgeting

analysis which would be including analysis of how much cash inflows would the project be able

to generate in the coming year (Rossi 2015). The necessary computation of the capital budgeting

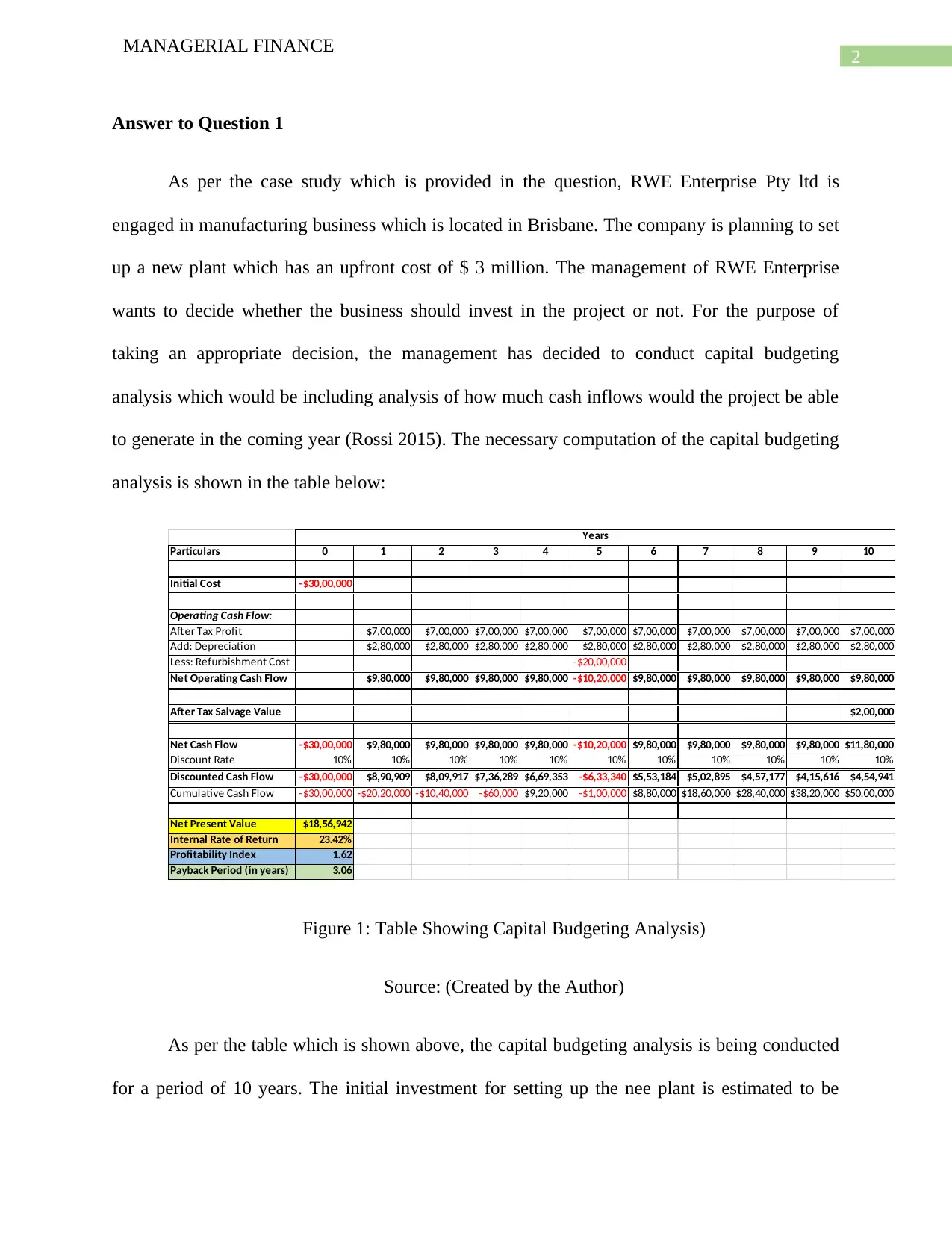

analysis is shown in the table below:

Particulars 0 1 2 3 4 5 6 7 8 9 10

Initial Cost -$30,00,000

Operating Cash Flow:

After Tax Profit $7,00,000 $7,00,000 $7,00,000 $7,00,000 $7,00,000 $7,00,000 $7,00,000 $7,00,000 $7,00,000 $7,00,000

Add: Depreciation $2,80,000 $2,80,000 $2,80,000 $2,80,000 $2,80,000 $2,80,000 $2,80,000 $2,80,000 $2,80,000 $2,80,000

Less: Refurbishment Cost -$20,00,000

Net Operating Cash Flow $9,80,000 $9,80,000 $9,80,000 $9,80,000 -$10,20,000 $9,80,000 $9,80,000 $9,80,000 $9,80,000 $9,80,000

After Tax Salvage Value $2,00,000

Net Cash Flow -$30,00,000 $9,80,000 $9,80,000 $9,80,000 $9,80,000 -$10,20,000 $9,80,000 $9,80,000 $9,80,000 $9,80,000 $11,80,000

Discount Rate 10% 10% 10% 10% 10% 10% 10% 10% 10% 10% 10%

Discounted Cash Flow -$30,00,000 $8,90,909 $8,09,917 $7,36,289 $6,69,353 -$6,33,340 $5,53,184 $5,02,895 $4,57,177 $4,15,616 $4,54,941

Cumulative Cash Flow -$30,00,000 -$20,20,000 -$10,40,000 -$60,000 $9,20,000 -$1,00,000 $8,80,000 $18,60,000 $28,40,000 $38,20,000 $50,00,000

Net Present Value $18,56,942

Internal Rate of Return 23.42%

Profitability Index 1.62

Payback Period (in years) 3.06

Years

Figure 1: Table Showing Capital Budgeting Analysis)

Source: (Created by the Author)

As per the table which is shown above, the capital budgeting analysis is being conducted

for a period of 10 years. The initial investment for setting up the nee plant is estimated to be

MANAGERIAL FINANCE

Answer to Question 1

As per the case study which is provided in the question, RWE Enterprise Pty ltd is

engaged in manufacturing business which is located in Brisbane. The company is planning to set

up a new plant which has an upfront cost of $ 3 million. The management of RWE Enterprise

wants to decide whether the business should invest in the project or not. For the purpose of

taking an appropriate decision, the management has decided to conduct capital budgeting

analysis which would be including analysis of how much cash inflows would the project be able

to generate in the coming year (Rossi 2015). The necessary computation of the capital budgeting

analysis is shown in the table below:

Particulars 0 1 2 3 4 5 6 7 8 9 10

Initial Cost -$30,00,000

Operating Cash Flow:

After Tax Profit $7,00,000 $7,00,000 $7,00,000 $7,00,000 $7,00,000 $7,00,000 $7,00,000 $7,00,000 $7,00,000 $7,00,000

Add: Depreciation $2,80,000 $2,80,000 $2,80,000 $2,80,000 $2,80,000 $2,80,000 $2,80,000 $2,80,000 $2,80,000 $2,80,000

Less: Refurbishment Cost -$20,00,000

Net Operating Cash Flow $9,80,000 $9,80,000 $9,80,000 $9,80,000 -$10,20,000 $9,80,000 $9,80,000 $9,80,000 $9,80,000 $9,80,000

After Tax Salvage Value $2,00,000

Net Cash Flow -$30,00,000 $9,80,000 $9,80,000 $9,80,000 $9,80,000 -$10,20,000 $9,80,000 $9,80,000 $9,80,000 $9,80,000 $11,80,000

Discount Rate 10% 10% 10% 10% 10% 10% 10% 10% 10% 10% 10%

Discounted Cash Flow -$30,00,000 $8,90,909 $8,09,917 $7,36,289 $6,69,353 -$6,33,340 $5,53,184 $5,02,895 $4,57,177 $4,15,616 $4,54,941

Cumulative Cash Flow -$30,00,000 -$20,20,000 -$10,40,000 -$60,000 $9,20,000 -$1,00,000 $8,80,000 $18,60,000 $28,40,000 $38,20,000 $50,00,000

Net Present Value $18,56,942

Internal Rate of Return 23.42%

Profitability Index 1.62

Payback Period (in years) 3.06

Years

Figure 1: Table Showing Capital Budgeting Analysis)

Source: (Created by the Author)

As per the table which is shown above, the capital budgeting analysis is being conducted

for a period of 10 years. The initial investment for setting up the nee plant is estimated to be

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

MANAGERIAL FINANCE

around $ 30,00,000. As shown in the above table, the new plant will be adding $ 7,00,000 to the

operating profit before tax in the business. The above table also shows that at the end of five

years, the business needs to incur a refurbishment costs for the plant which costs the business

around $ 20,00,000. At the end of 10 years, it is anticipated that the plant will have a salvage

value of $ 2,00,000 which will be revenues for the business. The cash flows which is estimated

to be generated with the help of new plant is shown to be $ 9,80,000 for the first four years

constantly. Then there is a significant fall in the cash flows which is shown as negative in the

fifth year as $ 10,20,000. This is mainly due to the refurbishment cost which was undertaken by

the business during the fifth years as per the estimates of the management. Thereafter at the end

of the 10th year, the plant is estimated to generate a cash flow of $ 11,80,000 which is a bit higher

due to the realization of the salvage value of the plant which the business will selling at the end

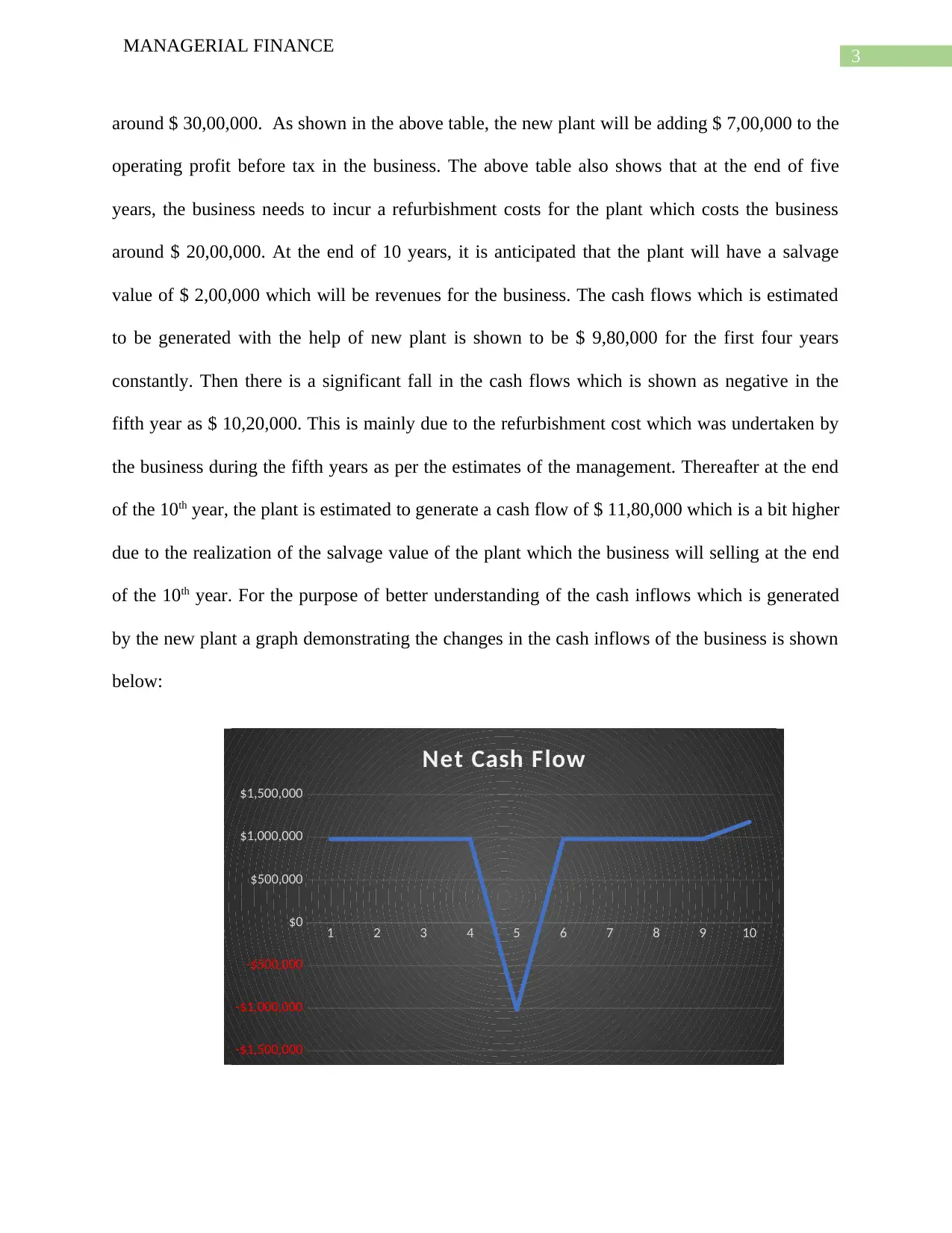

of the 10th year. For the purpose of better understanding of the cash inflows which is generated

by the new plant a graph demonstrating the changes in the cash inflows of the business is shown

below:

1 2 3 4 5 6 7 8 9 10

-$1,500,000

-$1,000,000

-$500,000

$0

$500,000

$1,000,000

$1,500,000

Net Cash Flow

MANAGERIAL FINANCE

around $ 30,00,000. As shown in the above table, the new plant will be adding $ 7,00,000 to the

operating profit before tax in the business. The above table also shows that at the end of five

years, the business needs to incur a refurbishment costs for the plant which costs the business

around $ 20,00,000. At the end of 10 years, it is anticipated that the plant will have a salvage

value of $ 2,00,000 which will be revenues for the business. The cash flows which is estimated

to be generated with the help of new plant is shown to be $ 9,80,000 for the first four years

constantly. Then there is a significant fall in the cash flows which is shown as negative in the

fifth year as $ 10,20,000. This is mainly due to the refurbishment cost which was undertaken by

the business during the fifth years as per the estimates of the management. Thereafter at the end

of the 10th year, the plant is estimated to generate a cash flow of $ 11,80,000 which is a bit higher

due to the realization of the salvage value of the plant which the business will selling at the end

of the 10th year. For the purpose of better understanding of the cash inflows which is generated

by the new plant a graph demonstrating the changes in the cash inflows of the business is shown

below:

1 2 3 4 5 6 7 8 9 10

-$1,500,000

-$1,000,000

-$500,000

$0

$500,000

$1,000,000

$1,500,000

Net Cash Flow

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

MANAGERIAL FINANCE

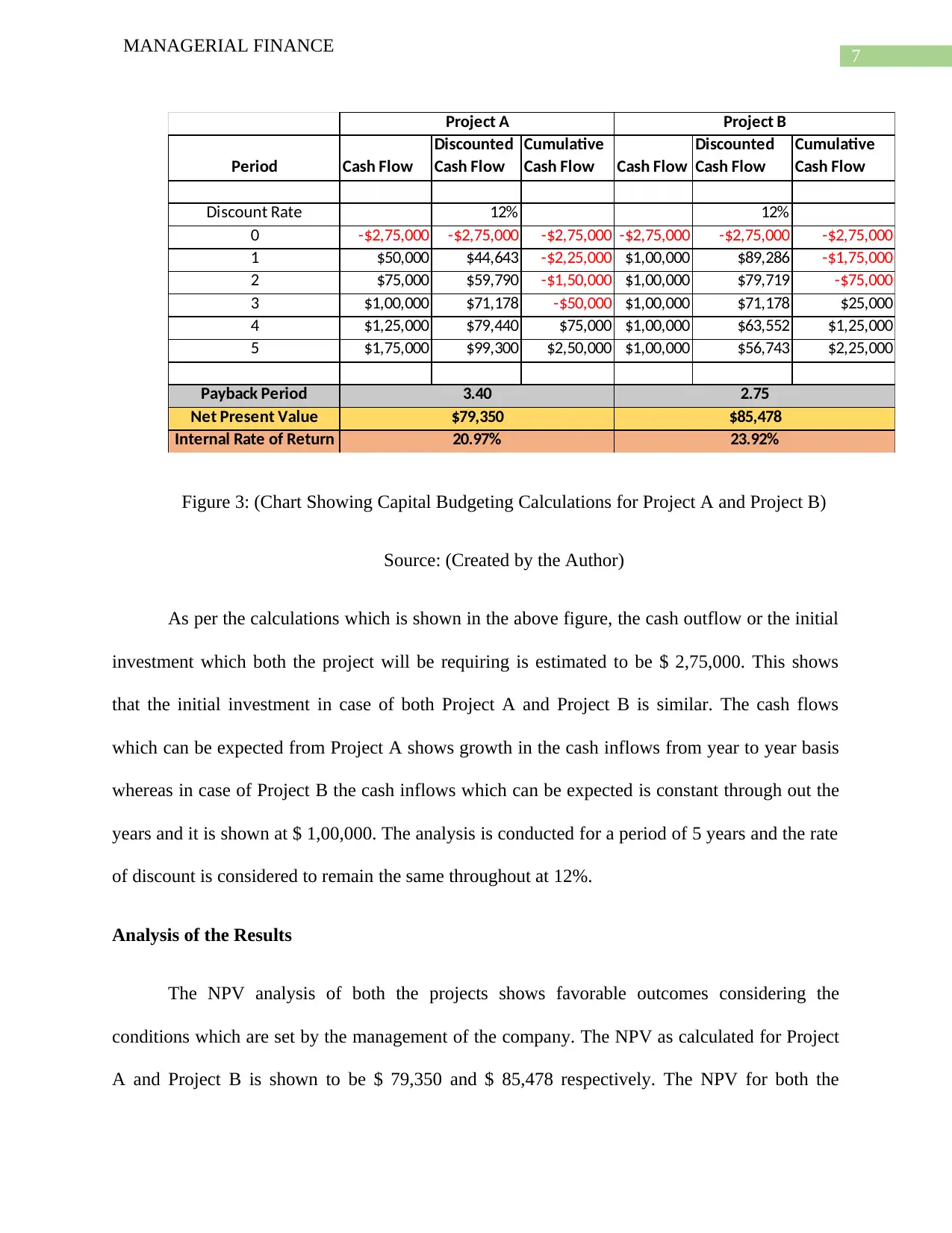

Figure 2: (Line diagram showing changes in the Net Cash flow)

Source: (Created by the Author)

As per the line diagram which is shown above, the net cash flows from the new plan t is

constant for the first four years and then there is a significantly fall in the cash inflows in the fifth

year due to extra investment for refurbishing cost which the management has to incur during the

fifth year. After the fifth year the cash flows generated is back to normal and are constant

through the useful life of the plant (Farshadfar and Monem 2013). There is no growth in the cash

flows and the cash inflows of the business remains constant as shown in the above graph except

for the estimates of the fifth year.

For the purpose of estimating the worthiness of the new product line which RWE

Enterprise Pty ltd is intending to invest in, the company has decided to conduct NPV analysis.

NPV analysis is used by business to estimate the net cash inflows from a project and also judge

whether the product is worth investing in or not (Matos et al. 2015). NPV analysis is considered

to be one of the most popular methods of determining whether the investment decision as

intended by the management is appropriate or not (Peña, Azevedo and Ferreira 2014). For the

purpose of calculating the NPV of the product line, the discounted rate is assumed to be same for

every year and the same is shown in the above table as 10%. The NPV as calculated for the

project is shown to be $ 18,56,942 which suggest that the product will be generating appropriate

cash inflows for the business. In addition to this, judging by the NPV analysis which is shown in

the table above, RWE Enterprise should invest in the project. The NPV analysis also shows that

it can be clearly estimated that the cash inflows of the business is much more than the cash

MANAGERIAL FINANCE

Figure 2: (Line diagram showing changes in the Net Cash flow)

Source: (Created by the Author)

As per the line diagram which is shown above, the net cash flows from the new plan t is

constant for the first four years and then there is a significantly fall in the cash inflows in the fifth

year due to extra investment for refurbishing cost which the management has to incur during the

fifth year. After the fifth year the cash flows generated is back to normal and are constant

through the useful life of the plant (Farshadfar and Monem 2013). There is no growth in the cash

flows and the cash inflows of the business remains constant as shown in the above graph except

for the estimates of the fifth year.

For the purpose of estimating the worthiness of the new product line which RWE

Enterprise Pty ltd is intending to invest in, the company has decided to conduct NPV analysis.

NPV analysis is used by business to estimate the net cash inflows from a project and also judge

whether the product is worth investing in or not (Matos et al. 2015). NPV analysis is considered

to be one of the most popular methods of determining whether the investment decision as

intended by the management is appropriate or not (Peña, Azevedo and Ferreira 2014). For the

purpose of calculating the NPV of the product line, the discounted rate is assumed to be same for

every year and the same is shown in the above table as 10%. The NPV as calculated for the

project is shown to be $ 18,56,942 which suggest that the product will be generating appropriate

cash inflows for the business. In addition to this, judging by the NPV analysis which is shown in

the table above, RWE Enterprise should invest in the project. The NPV analysis also shows that

it can be clearly estimated that the cash inflows of the business is much more than the cash

5

MANAGERIAL FINANCE

outflows of the business and therefore the profitability of the project is also secured (Ognjenovic

et al. 2016).

The internal rate of return is the rate at which the cash inflows which can be generated

from the project and the cash outflows which is incurred on the project becomes zero. In other

words, IRR is the rate at which the NPV of the project becomes zero (Magni 2013). The IRR of

the project as computed in the above table is shown at 23.42% which signifies that NPV of the

project will become zero when the discount rate is 23.42% and beyond this rate the project will

be earning negative returns (Burns and Walker 2015). Profitability Index of a business shows the

profits which can be generated by the profit which considers the cash inflows and cash outflows

of the business for such a purpose. The profitability index for the project is shown to 1.62 in the

above table which signifies that the business will be able to generate profits with the

implementation of the project. The profitability index is greater than 1 which signifies that the

cash inflows which is generated by the project is much more than the cash outflows which is

related to the project (Visser and Fiksen 2013). Thus, considering IRR and Profitability index as

the base for decision making, the company should invest in the project as both the results are

shown favorable.

The payback period is also one of the techniques which is used in capital budgeting

analysis. The technique reveals the minimum time which a business takes for the purpose of

recovering the initial investment which the company had made in the project (San Ong and

Thum 2013). The payback period of the project as shown in the table is 3.06 years which means

in a little more than 3 years the business will be able to recover the initial investments of the

business. This is a favorable result and on the basis of such a result the company should invest in

the project.

MANAGERIAL FINANCE

outflows of the business and therefore the profitability of the project is also secured (Ognjenovic

et al. 2016).

The internal rate of return is the rate at which the cash inflows which can be generated

from the project and the cash outflows which is incurred on the project becomes zero. In other

words, IRR is the rate at which the NPV of the project becomes zero (Magni 2013). The IRR of

the project as computed in the above table is shown at 23.42% which signifies that NPV of the

project will become zero when the discount rate is 23.42% and beyond this rate the project will

be earning negative returns (Burns and Walker 2015). Profitability Index of a business shows the

profits which can be generated by the profit which considers the cash inflows and cash outflows

of the business for such a purpose. The profitability index for the project is shown to 1.62 in the

above table which signifies that the business will be able to generate profits with the

implementation of the project. The profitability index is greater than 1 which signifies that the

cash inflows which is generated by the project is much more than the cash outflows which is

related to the project (Visser and Fiksen 2013). Thus, considering IRR and Profitability index as

the base for decision making, the company should invest in the project as both the results are

shown favorable.

The payback period is also one of the techniques which is used in capital budgeting

analysis. The technique reveals the minimum time which a business takes for the purpose of

recovering the initial investment which the company had made in the project (San Ong and

Thum 2013). The payback period of the project as shown in the table is 3.06 years which means

in a little more than 3 years the business will be able to recover the initial investments of the

business. This is a favorable result and on the basis of such a result the company should invest in

the project.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

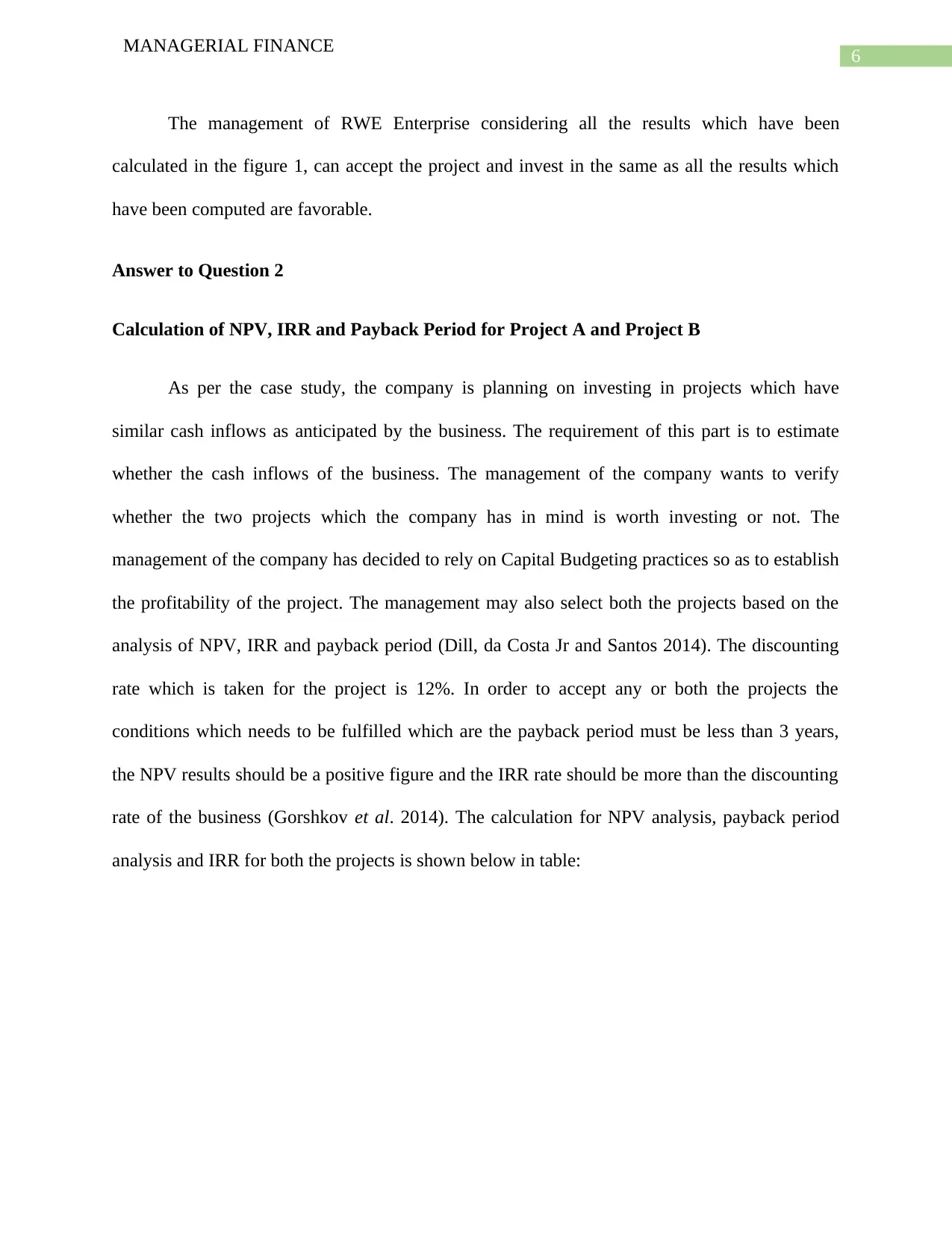

MANAGERIAL FINANCE

The management of RWE Enterprise considering all the results which have been

calculated in the figure 1, can accept the project and invest in the same as all the results which

have been computed are favorable.

Answer to Question 2

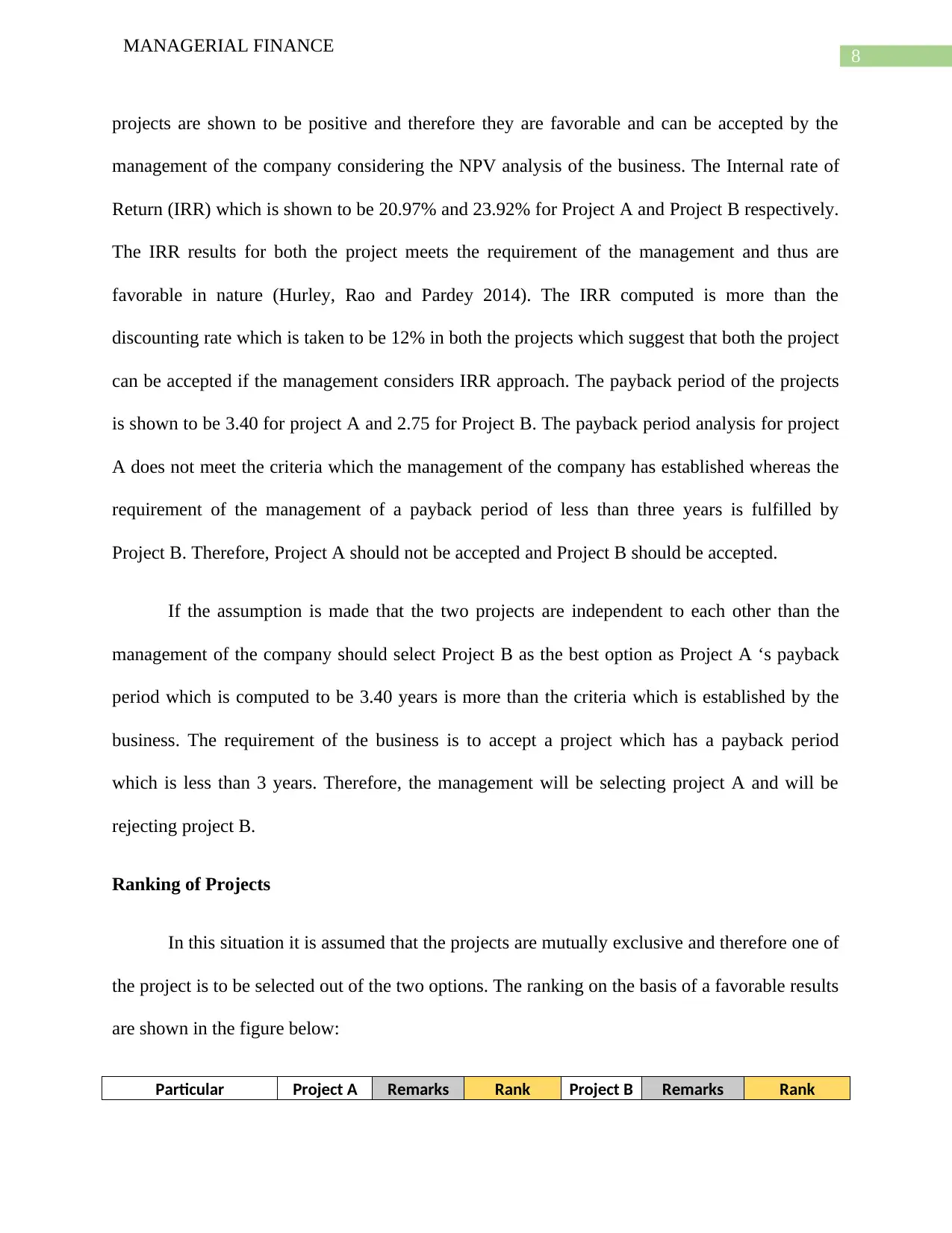

Calculation of NPV, IRR and Payback Period for Project A and Project B

As per the case study, the company is planning on investing in projects which have

similar cash inflows as anticipated by the business. The requirement of this part is to estimate

whether the cash inflows of the business. The management of the company wants to verify

whether the two projects which the company has in mind is worth investing or not. The

management of the company has decided to rely on Capital Budgeting practices so as to establish

the profitability of the project. The management may also select both the projects based on the

analysis of NPV, IRR and payback period (Dill, da Costa Jr and Santos 2014). The discounting

rate which is taken for the project is 12%. In order to accept any or both the projects the

conditions which needs to be fulfilled which are the payback period must be less than 3 years,

the NPV results should be a positive figure and the IRR rate should be more than the discounting

rate of the business (Gorshkov et al. 2014). The calculation for NPV analysis, payback period

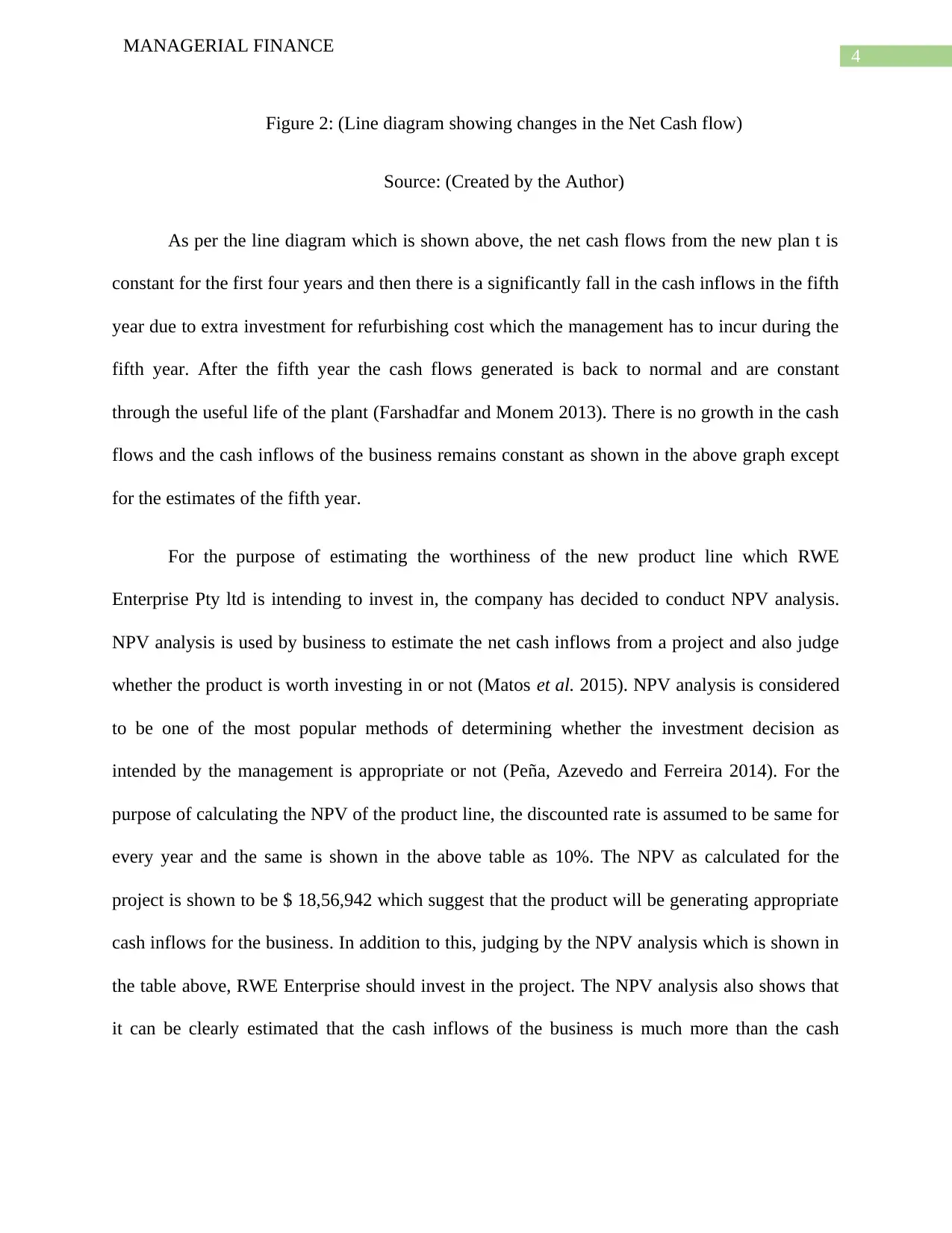

analysis and IRR for both the projects is shown below in table:

MANAGERIAL FINANCE

The management of RWE Enterprise considering all the results which have been

calculated in the figure 1, can accept the project and invest in the same as all the results which

have been computed are favorable.

Answer to Question 2

Calculation of NPV, IRR and Payback Period for Project A and Project B

As per the case study, the company is planning on investing in projects which have

similar cash inflows as anticipated by the business. The requirement of this part is to estimate

whether the cash inflows of the business. The management of the company wants to verify

whether the two projects which the company has in mind is worth investing or not. The

management of the company has decided to rely on Capital Budgeting practices so as to establish

the profitability of the project. The management may also select both the projects based on the

analysis of NPV, IRR and payback period (Dill, da Costa Jr and Santos 2014). The discounting

rate which is taken for the project is 12%. In order to accept any or both the projects the

conditions which needs to be fulfilled which are the payback period must be less than 3 years,

the NPV results should be a positive figure and the IRR rate should be more than the discounting

rate of the business (Gorshkov et al. 2014). The calculation for NPV analysis, payback period

analysis and IRR for both the projects is shown below in table:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

MANAGERIAL FINANCE

Period Cash Flow

Discounted

Cash Flow

Cumulative

Cash Flow Cash Flow

Discounted

Cash Flow

Cumulative

Cash Flow

Discount Rate 12% 12%

0 -$2,75,000 -$2,75,000 -$2,75,000 -$2,75,000 -$2,75,000 -$2,75,000

1 $50,000 $44,643 -$2,25,000 $1,00,000 $89,286 -$1,75,000

2 $75,000 $59,790 -$1,50,000 $1,00,000 $79,719 -$75,000

3 $1,00,000 $71,178 -$50,000 $1,00,000 $71,178 $25,000

4 $1,25,000 $79,440 $75,000 $1,00,000 $63,552 $1,25,000

5 $1,75,000 $99,300 $2,50,000 $1,00,000 $56,743 $2,25,000

Payback Period

Net Present Value

Internal Rate of Return 20.97% 23.92%

Project A Project B

3.40 2.75

$85,478$79,350

Figure 3: (Chart Showing Capital Budgeting Calculations for Project A and Project B)

Source: (Created by the Author)

As per the calculations which is shown in the above figure, the cash outflow or the initial

investment which both the project will be requiring is estimated to be $ 2,75,000. This shows

that the initial investment in case of both Project A and Project B is similar. The cash flows

which can be expected from Project A shows growth in the cash inflows from year to year basis

whereas in case of Project B the cash inflows which can be expected is constant through out the

years and it is shown at $ 1,00,000. The analysis is conducted for a period of 5 years and the rate

of discount is considered to remain the same throughout at 12%.

Analysis of the Results

The NPV analysis of both the projects shows favorable outcomes considering the

conditions which are set by the management of the company. The NPV as calculated for Project

A and Project B is shown to be $ 79,350 and $ 85,478 respectively. The NPV for both the

MANAGERIAL FINANCE

Period Cash Flow

Discounted

Cash Flow

Cumulative

Cash Flow Cash Flow

Discounted

Cash Flow

Cumulative

Cash Flow

Discount Rate 12% 12%

0 -$2,75,000 -$2,75,000 -$2,75,000 -$2,75,000 -$2,75,000 -$2,75,000

1 $50,000 $44,643 -$2,25,000 $1,00,000 $89,286 -$1,75,000

2 $75,000 $59,790 -$1,50,000 $1,00,000 $79,719 -$75,000

3 $1,00,000 $71,178 -$50,000 $1,00,000 $71,178 $25,000

4 $1,25,000 $79,440 $75,000 $1,00,000 $63,552 $1,25,000

5 $1,75,000 $99,300 $2,50,000 $1,00,000 $56,743 $2,25,000

Payback Period

Net Present Value

Internal Rate of Return 20.97% 23.92%

Project A Project B

3.40 2.75

$85,478$79,350

Figure 3: (Chart Showing Capital Budgeting Calculations for Project A and Project B)

Source: (Created by the Author)

As per the calculations which is shown in the above figure, the cash outflow or the initial

investment which both the project will be requiring is estimated to be $ 2,75,000. This shows

that the initial investment in case of both Project A and Project B is similar. The cash flows

which can be expected from Project A shows growth in the cash inflows from year to year basis

whereas in case of Project B the cash inflows which can be expected is constant through out the

years and it is shown at $ 1,00,000. The analysis is conducted for a period of 5 years and the rate

of discount is considered to remain the same throughout at 12%.

Analysis of the Results

The NPV analysis of both the projects shows favorable outcomes considering the

conditions which are set by the management of the company. The NPV as calculated for Project

A and Project B is shown to be $ 79,350 and $ 85,478 respectively. The NPV for both the

8

MANAGERIAL FINANCE

projects are shown to be positive and therefore they are favorable and can be accepted by the

management of the company considering the NPV analysis of the business. The Internal rate of

Return (IRR) which is shown to be 20.97% and 23.92% for Project A and Project B respectively.

The IRR results for both the project meets the requirement of the management and thus are

favorable in nature (Hurley, Rao and Pardey 2014). The IRR computed is more than the

discounting rate which is taken to be 12% in both the projects which suggest that both the project

can be accepted if the management considers IRR approach. The payback period of the projects

is shown to be 3.40 for project A and 2.75 for Project B. The payback period analysis for project

A does not meet the criteria which the management of the company has established whereas the

requirement of the management of a payback period of less than three years is fulfilled by

Project B. Therefore, Project A should not be accepted and Project B should be accepted.

If the assumption is made that the two projects are independent to each other than the

management of the company should select Project B as the best option as Project A ‘s payback

period which is computed to be 3.40 years is more than the criteria which is established by the

business. The requirement of the business is to accept a project which has a payback period

which is less than 3 years. Therefore, the management will be selecting project A and will be

rejecting project B.

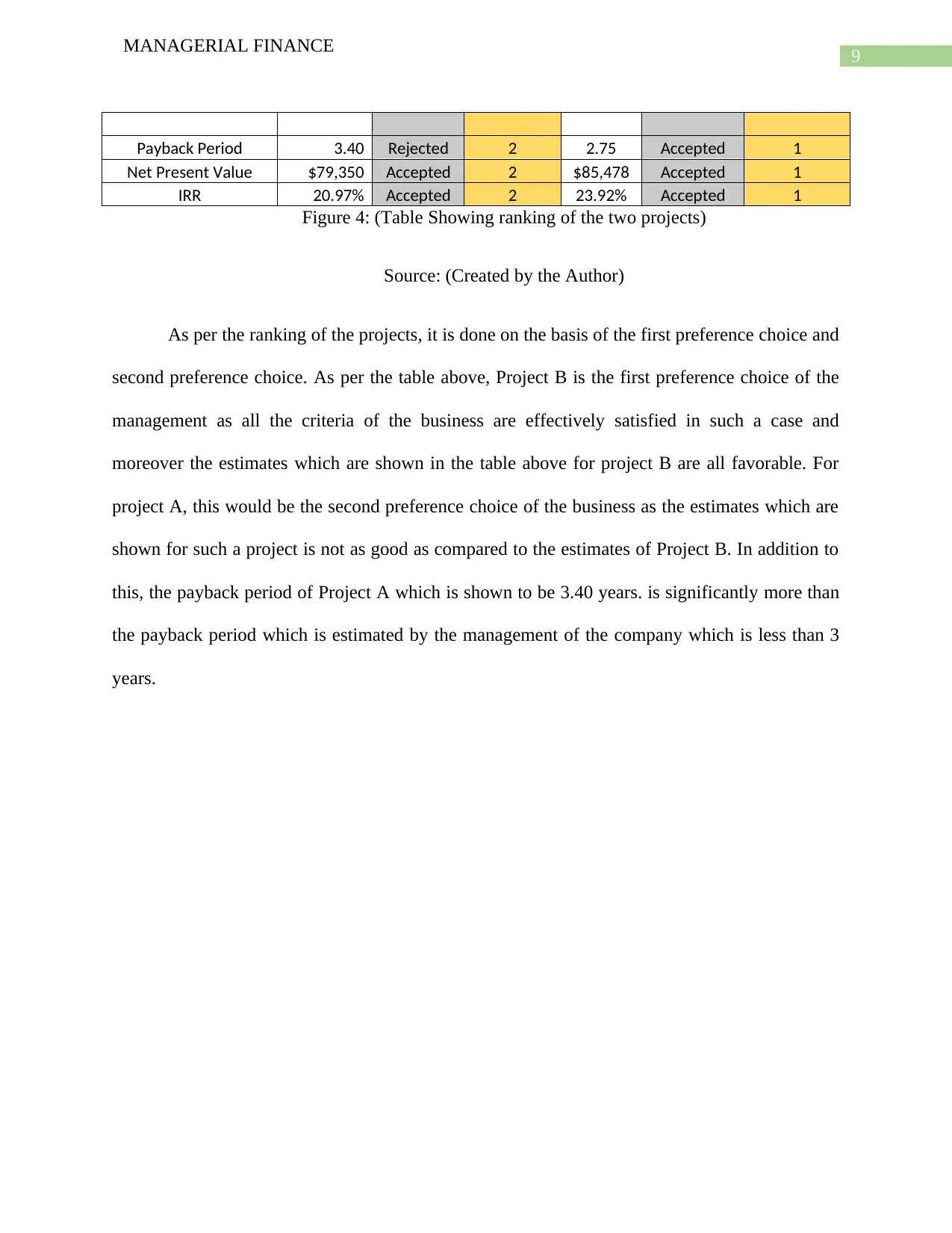

Ranking of Projects

In this situation it is assumed that the projects are mutually exclusive and therefore one of

the project is to be selected out of the two options. The ranking on the basis of a favorable results

are shown in the figure below:

Particular Project A Remarks Rank Project B Remarks Rank

MANAGERIAL FINANCE

projects are shown to be positive and therefore they are favorable and can be accepted by the

management of the company considering the NPV analysis of the business. The Internal rate of

Return (IRR) which is shown to be 20.97% and 23.92% for Project A and Project B respectively.

The IRR results for both the project meets the requirement of the management and thus are

favorable in nature (Hurley, Rao and Pardey 2014). The IRR computed is more than the

discounting rate which is taken to be 12% in both the projects which suggest that both the project

can be accepted if the management considers IRR approach. The payback period of the projects

is shown to be 3.40 for project A and 2.75 for Project B. The payback period analysis for project

A does not meet the criteria which the management of the company has established whereas the

requirement of the management of a payback period of less than three years is fulfilled by

Project B. Therefore, Project A should not be accepted and Project B should be accepted.

If the assumption is made that the two projects are independent to each other than the

management of the company should select Project B as the best option as Project A ‘s payback

period which is computed to be 3.40 years is more than the criteria which is established by the

business. The requirement of the business is to accept a project which has a payback period

which is less than 3 years. Therefore, the management will be selecting project A and will be

rejecting project B.

Ranking of Projects

In this situation it is assumed that the projects are mutually exclusive and therefore one of

the project is to be selected out of the two options. The ranking on the basis of a favorable results

are shown in the figure below:

Particular Project A Remarks Rank Project B Remarks Rank

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

MANAGERIAL FINANCE

Payback Period 3.40 Rejected 2 2.75 Accepted 1

Net Present Value $79,350 Accepted 2 $85,478 Accepted 1

IRR 20.97% Accepted 2 23.92% Accepted 1

Figure 4: (Table Showing ranking of the two projects)

Source: (Created by the Author)

As per the ranking of the projects, it is done on the basis of the first preference choice and

second preference choice. As per the table above, Project B is the first preference choice of the

management as all the criteria of the business are effectively satisfied in such a case and

moreover the estimates which are shown in the table above for project B are all favorable. For

project A, this would be the second preference choice of the business as the estimates which are

shown for such a project is not as good as compared to the estimates of Project B. In addition to

this, the payback period of Project A which is shown to be 3.40 years. is significantly more than

the payback period which is estimated by the management of the company which is less than 3

years.

MANAGERIAL FINANCE

Payback Period 3.40 Rejected 2 2.75 Accepted 1

Net Present Value $79,350 Accepted 2 $85,478 Accepted 1

IRR 20.97% Accepted 2 23.92% Accepted 1

Figure 4: (Table Showing ranking of the two projects)

Source: (Created by the Author)

As per the ranking of the projects, it is done on the basis of the first preference choice and

second preference choice. As per the table above, Project B is the first preference choice of the

management as all the criteria of the business are effectively satisfied in such a case and

moreover the estimates which are shown in the table above for project B are all favorable. For

project A, this would be the second preference choice of the business as the estimates which are

shown for such a project is not as good as compared to the estimates of Project B. In addition to

this, the payback period of Project A which is shown to be 3.40 years. is significantly more than

the payback period which is estimated by the management of the company which is less than 3

years.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

MANAGERIAL FINANCE

Reference

Burns, R. and Walker, J., 2015. Capital budgeting surveys: the future is now.

Dill, R., da Costa Jr, N. and Santos, A.A., 2014. Corporate profitability analysis: a novel

application for paraconsistent logic. Applied Mathematical Sciences, 8(26), pp.1271-1288.

Farshadfar, S. and Monem, R., 2013. Further evidence on the usefulness of direct method cash

flow components for forecasting future cash flows. The international journal of accounting,

48(1), pp.111-133.

Gorshkov, A.S., Rymkevich, P.P., Nemova, D.V. and Vatin, N.I., 2014. Method of calculating

the payback period of investment for renovation of building facades. Stroitel'stvo Unikal'nyh

Zdanij i Sooruzenij, (2), p.82.

MANAGERIAL FINANCE

Reference

Burns, R. and Walker, J., 2015. Capital budgeting surveys: the future is now.

Dill, R., da Costa Jr, N. and Santos, A.A., 2014. Corporate profitability analysis: a novel

application for paraconsistent logic. Applied Mathematical Sciences, 8(26), pp.1271-1288.

Farshadfar, S. and Monem, R., 2013. Further evidence on the usefulness of direct method cash

flow components for forecasting future cash flows. The international journal of accounting,

48(1), pp.111-133.

Gorshkov, A.S., Rymkevich, P.P., Nemova, D.V. and Vatin, N.I., 2014. Method of calculating

the payback period of investment for renovation of building facades. Stroitel'stvo Unikal'nyh

Zdanij i Sooruzenij, (2), p.82.

11

MANAGERIAL FINANCE

Hurley, T.M., Rao, X. and Pardey, P.G., 2014. Re-examining the reported rates of return to food

and agricultural research and development. American Journal of Agricultural Economics, 96(5),

pp.1492-1504.

Magni, C.A., 2013. The internal rate of return approach and the AIRR paradigm: a refutation and

a corroboration. The Engineering Economist, 58(2), pp.73-111.

Matos, C., Bentes, I., Santos, C., Imteaz, M. and Pereira, S., 2015. Economic analysis of a

rainwater harvesting system in a commercial building. Water resources management, 29(11),

pp.3971-3986.

Ognjenovic, S., Ishkov, A., Cvetkovic, D., Peric, D. and Romanovich, M., 2016. Analyses of

Costs and Benefits in the Pavement Management Systems. Procedia Engineering, 165, pp.954-

959.

Peña, I., Azevedo, I.L. and Ferreira, L.A.F.M., 2014. Economic analysis of the profitability of

existing wind parks in Portugal. Energy Economics, 45, pp.353-363.

Rossi, M., 2015. The use of capital budgeting techniques: an outlook from Italy. International

Journal of Management Practice, 8(1), pp.43-56.

San Ong, T. and Thum, C.H., 2013. Net present value and payback period for building integrated

photovoltaic projects in Malaysia. International Journal of Academic Research in Business and

Social Sciences, 3(2), p.153.

Visser, A.W. and Fiksen, Ø., 2013. Optimal foraging in marine ecosystem models: selectivity,

profitability and switching. Marine Ecology Progress Series, 473, pp.91-101.

MANAGERIAL FINANCE

Hurley, T.M., Rao, X. and Pardey, P.G., 2014. Re-examining the reported rates of return to food

and agricultural research and development. American Journal of Agricultural Economics, 96(5),

pp.1492-1504.

Magni, C.A., 2013. The internal rate of return approach and the AIRR paradigm: a refutation and

a corroboration. The Engineering Economist, 58(2), pp.73-111.

Matos, C., Bentes, I., Santos, C., Imteaz, M. and Pereira, S., 2015. Economic analysis of a

rainwater harvesting system in a commercial building. Water resources management, 29(11),

pp.3971-3986.

Ognjenovic, S., Ishkov, A., Cvetkovic, D., Peric, D. and Romanovich, M., 2016. Analyses of

Costs and Benefits in the Pavement Management Systems. Procedia Engineering, 165, pp.954-

959.

Peña, I., Azevedo, I.L. and Ferreira, L.A.F.M., 2014. Economic analysis of the profitability of

existing wind parks in Portugal. Energy Economics, 45, pp.353-363.

Rossi, M., 2015. The use of capital budgeting techniques: an outlook from Italy. International

Journal of Management Practice, 8(1), pp.43-56.

San Ong, T. and Thum, C.H., 2013. Net present value and payback period for building integrated

photovoltaic projects in Malaysia. International Journal of Academic Research in Business and

Social Sciences, 3(2), p.153.

Visser, A.W. and Fiksen, Ø., 2013. Optimal foraging in marine ecosystem models: selectivity,

profitability and switching. Marine Ecology Progress Series, 473, pp.91-101.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.