Managerial Finance: Portfolio Analysis, Investment Appraisal Report

VerifiedAdded on 2022/12/30

|18

|3711

|70

Report

AI Summary

This report delves into managerial finance, commencing with an introduction to financial decision-making and its significance. It presents a detailed portfolio analysis, calculating and interpreting various financial ratios such as current, quick, net profit margin, gross profit margin, gearing ratio, P/E ratio, earnings per share, return on capital employed, and dividend payout ratio for Tesco and Sainsbury companies. The analysis highlights the financial positions of both companies, followed by recommendations for the underperforming entity. The report also addresses the limitations of financial ratios. Furthermore, it explores capital investment appraisal, discussing the evaluation of potential projects (A and B) for Ross Hill Limited, including their initial investments. The report concludes by acknowledging the limitations of investment appraisal techniques in long-term decision-making.

Managerial Finance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

Portfolio 1........................................................................................................................................3

Calculation of financial ratios......................................................................................................3

Analysis financial position of companies....................................................................................7

Recommendations for poorly performing company....................................................................9

Limitation of financial ratios.....................................................................................................10

A.Capital Investment Appraisal.................................................................................................11

B. Limitations of using investment appraisal techniques in long term decision-making..........14

CONCLUSION..............................................................................................................................15

REFERENCES................................................................................................................................1

INTRODUCTION...........................................................................................................................3

Portfolio 1........................................................................................................................................3

Calculation of financial ratios......................................................................................................3

Analysis financial position of companies....................................................................................7

Recommendations for poorly performing company....................................................................9

Limitation of financial ratios.....................................................................................................10

A.Capital Investment Appraisal.................................................................................................11

B. Limitations of using investment appraisal techniques in long term decision-making..........14

CONCLUSION..............................................................................................................................15

REFERENCES................................................................................................................................1

INTRODUCTION

Financial decision-making is about to make the decisions in relation to company's

business operations on the basis of the financial position reflected in company's books of

accounts (Pazarskis and et.al., 2018). This report will indicate about the ratios in respect to

different business organisation. Interpretation will also done over the financial ratios calculated

in the first half of report to identify the financial position of the organisation. Necessary

recommendations will also provide to improve or boost the overall financial performance of

organisation. Furthermore, this project will also talk about the investment decision-making with

the use of different methods in respect to the organisation.

Portfolio 1

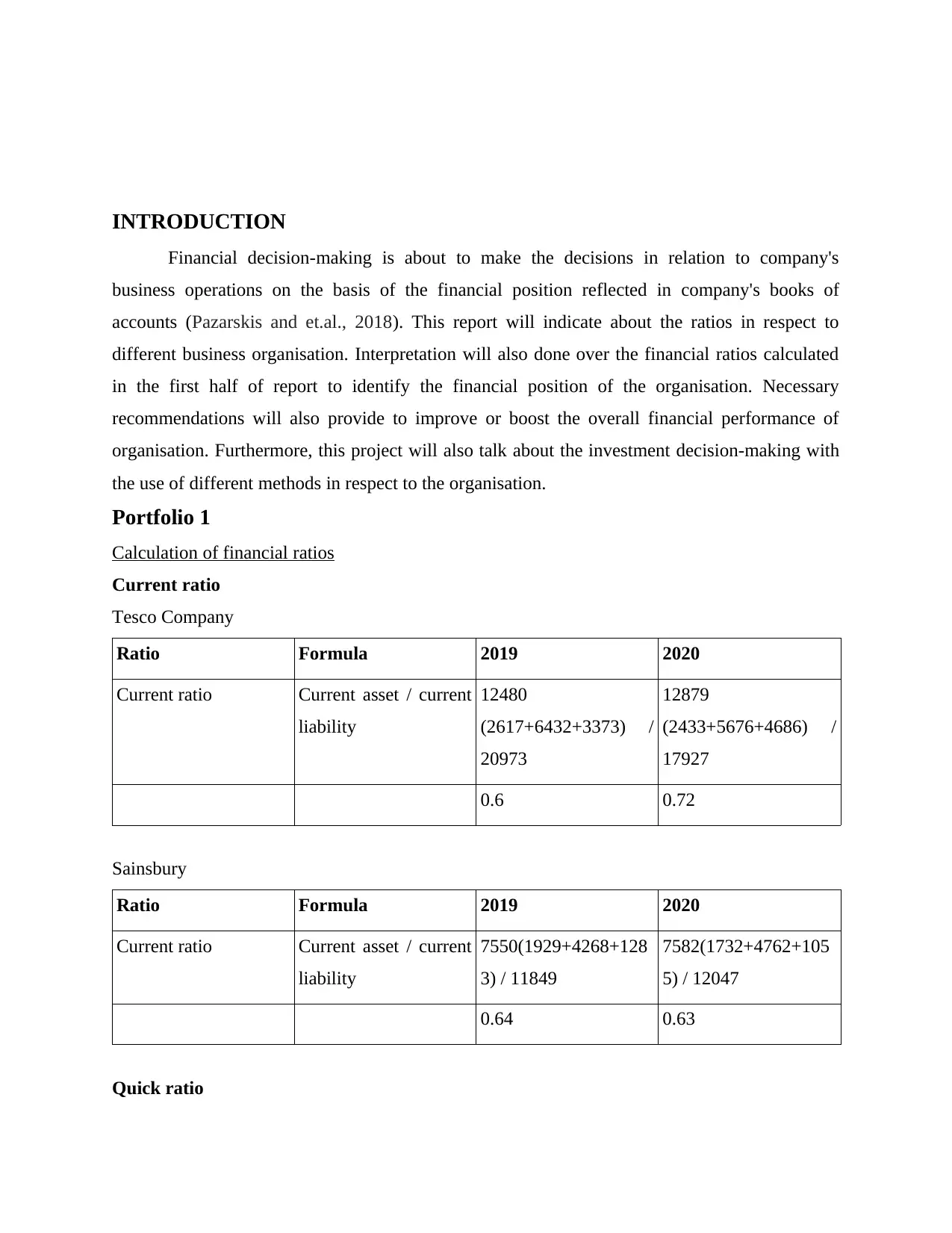

Calculation of financial ratios

Current ratio

Tesco Company

Ratio Formula 2019 2020

Current ratio Current asset / current

liability

12480

(2617+6432+3373) /

20973

12879

(2433+5676+4686) /

17927

0.6 0.72

Sainsbury

Ratio Formula 2019 2020

Current ratio Current asset / current

liability

7550(1929+4268+128

3) / 11849

7582(1732+4762+105

5) / 12047

0.64 0.63

Quick ratio

Financial decision-making is about to make the decisions in relation to company's

business operations on the basis of the financial position reflected in company's books of

accounts (Pazarskis and et.al., 2018). This report will indicate about the ratios in respect to

different business organisation. Interpretation will also done over the financial ratios calculated

in the first half of report to identify the financial position of the organisation. Necessary

recommendations will also provide to improve or boost the overall financial performance of

organisation. Furthermore, this project will also talk about the investment decision-making with

the use of different methods in respect to the organisation.

Portfolio 1

Calculation of financial ratios

Current ratio

Tesco Company

Ratio Formula 2019 2020

Current ratio Current asset / current

liability

12480

(2617+6432+3373) /

20973

12879

(2433+5676+4686) /

17927

0.6 0.72

Sainsbury

Ratio Formula 2019 2020

Current ratio Current asset / current

liability

7550(1929+4268+128

3) / 11849

7582(1732+4762+105

5) / 12047

0.64 0.63

Quick ratio

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Tesco Company

Ratio Formula 2019 2020

Quick ratio Current asset -

Inventory/ current

liability

9863 (12480-2617) /

20973

10446 (12879-2433) /

17927

0.47 0.58

Sainsbury

Ratio Formula 2019 2020

Quick ratio Current asset -

Inventory/ current

liability

5621(7550-1929) /

11849

5850(7582-1732) /

12047

0.47 0.49

Net profit margin

Tesco Company

Ratio Formula 2019 2020

Net profit margin Net profit / sales *100 1270/63911*100 935/64760*100

1.99% 1.44%

Sainsbury

Ratio Formula 2019 2020

Net profit margin Net profit / sales *100 186/29007*100 152/28993*100

0.64% 0.52%

Gross profit margin

Tesco Company

Ratio Formula 2019 2020

Ratio Formula 2019 2020

Quick ratio Current asset -

Inventory/ current

liability

9863 (12480-2617) /

20973

10446 (12879-2433) /

17927

0.47 0.58

Sainsbury

Ratio Formula 2019 2020

Quick ratio Current asset -

Inventory/ current

liability

5621(7550-1929) /

11849

5850(7582-1732) /

12047

0.47 0.49

Net profit margin

Tesco Company

Ratio Formula 2019 2020

Net profit margin Net profit / sales *100 1270/63911*100 935/64760*100

1.99% 1.44%

Sainsbury

Ratio Formula 2019 2020

Net profit margin Net profit / sales *100 186/29007*100 152/28993*100

0.64% 0.52%

Gross profit margin

Tesco Company

Ratio Formula 2019 2020

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

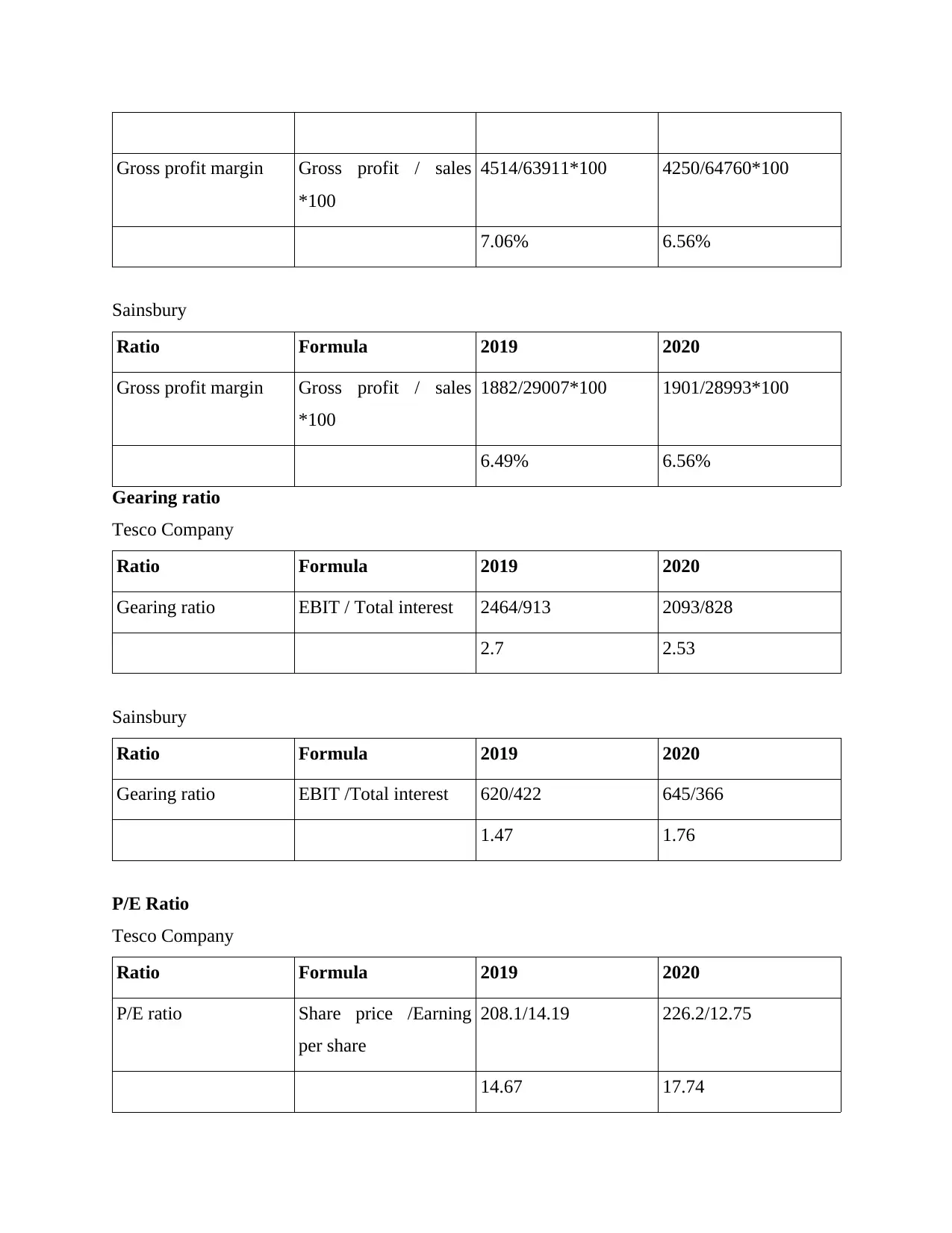

Gross profit margin Gross profit / sales

*100

4514/63911*100 4250/64760*100

7.06% 6.56%

Sainsbury

Ratio Formula 2019 2020

Gross profit margin Gross profit / sales

*100

1882/29007*100 1901/28993*100

6.49% 6.56%

Gearing ratio

Tesco Company

Ratio Formula 2019 2020

Gearing ratio EBIT / Total interest 2464/913 2093/828

2.7 2.53

Sainsbury

Ratio Formula 2019 2020

Gearing ratio EBIT /Total interest 620/422 645/366

1.47 1.76

P/E Ratio

Tesco Company

Ratio Formula 2019 2020

P/E ratio Share price /Earning

per share

208.1/14.19 226.2/12.75

14.67 17.74

*100

4514/63911*100 4250/64760*100

7.06% 6.56%

Sainsbury

Ratio Formula 2019 2020

Gross profit margin Gross profit / sales

*100

1882/29007*100 1901/28993*100

6.49% 6.56%

Gearing ratio

Tesco Company

Ratio Formula 2019 2020

Gearing ratio EBIT / Total interest 2464/913 2093/828

2.7 2.53

Sainsbury

Ratio Formula 2019 2020

Gearing ratio EBIT /Total interest 620/422 645/366

1.47 1.76

P/E Ratio

Tesco Company

Ratio Formula 2019 2020

P/E ratio Share price /Earning

per share

208.1/14.19 226.2/12.75

14.67 17.74

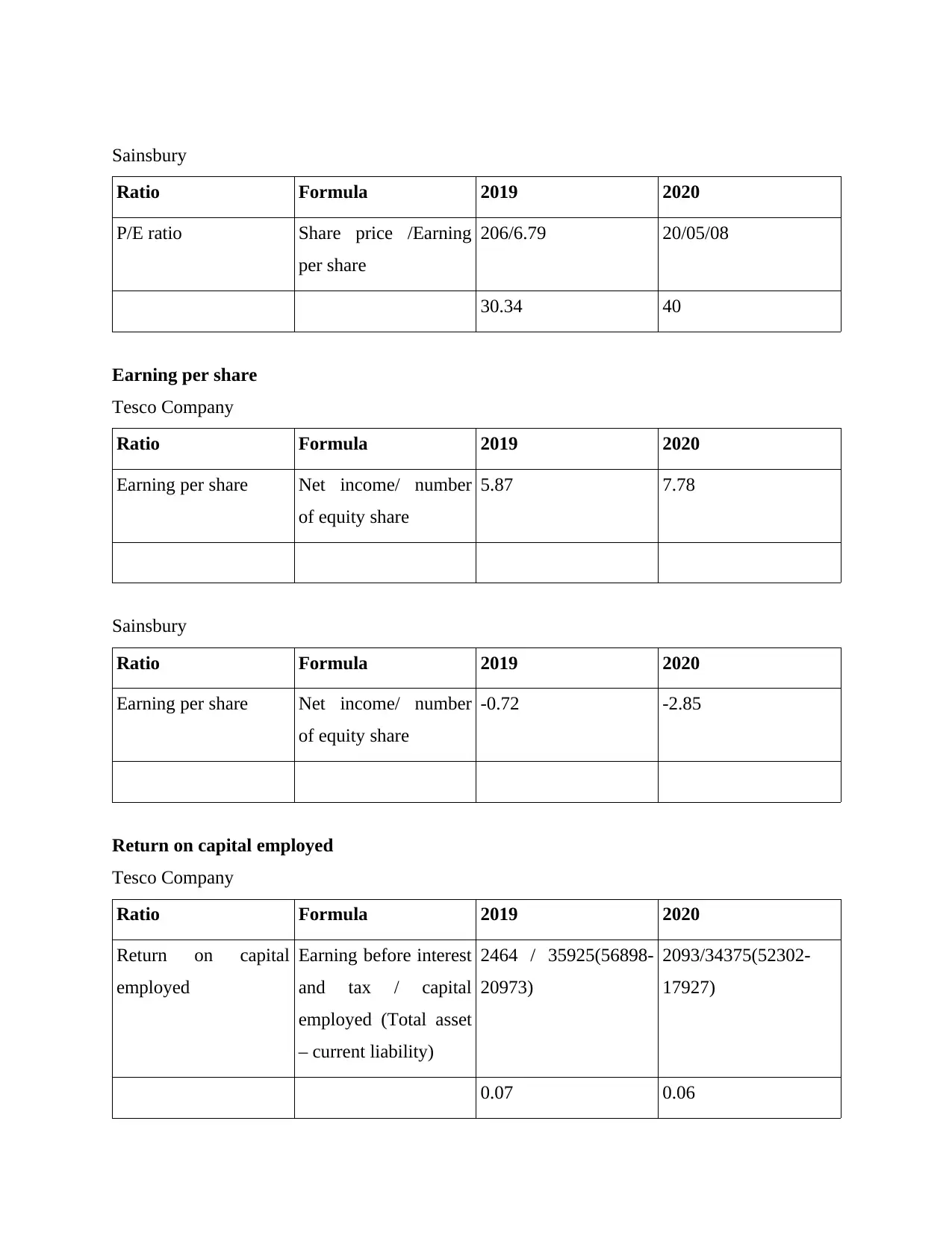

Sainsbury

Ratio Formula 2019 2020

P/E ratio Share price /Earning

per share

206/6.79 20/05/08

30.34 40

Earning per share

Tesco Company

Ratio Formula 2019 2020

Earning per share Net income/ number

of equity share

5.87 7.78

Sainsbury

Ratio Formula 2019 2020

Earning per share Net income/ number

of equity share

-0.72 -2.85

Return on capital employed

Tesco Company

Ratio Formula 2019 2020

Return on capital

employed

Earning before interest

and tax / capital

employed (Total asset

– current liability)

2464 / 35925(56898-

20973)

2093/34375(52302-

17927)

0.07 0.06

Ratio Formula 2019 2020

P/E ratio Share price /Earning

per share

206/6.79 20/05/08

30.34 40

Earning per share

Tesco Company

Ratio Formula 2019 2020

Earning per share Net income/ number

of equity share

5.87 7.78

Sainsbury

Ratio Formula 2019 2020

Earning per share Net income/ number

of equity share

-0.72 -2.85

Return on capital employed

Tesco Company

Ratio Formula 2019 2020

Return on capital

employed

Earning before interest

and tax / capital

employed (Total asset

– current liability)

2464 / 35925(56898-

20973)

2093/34375(52302-

17927)

0.07 0.06

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

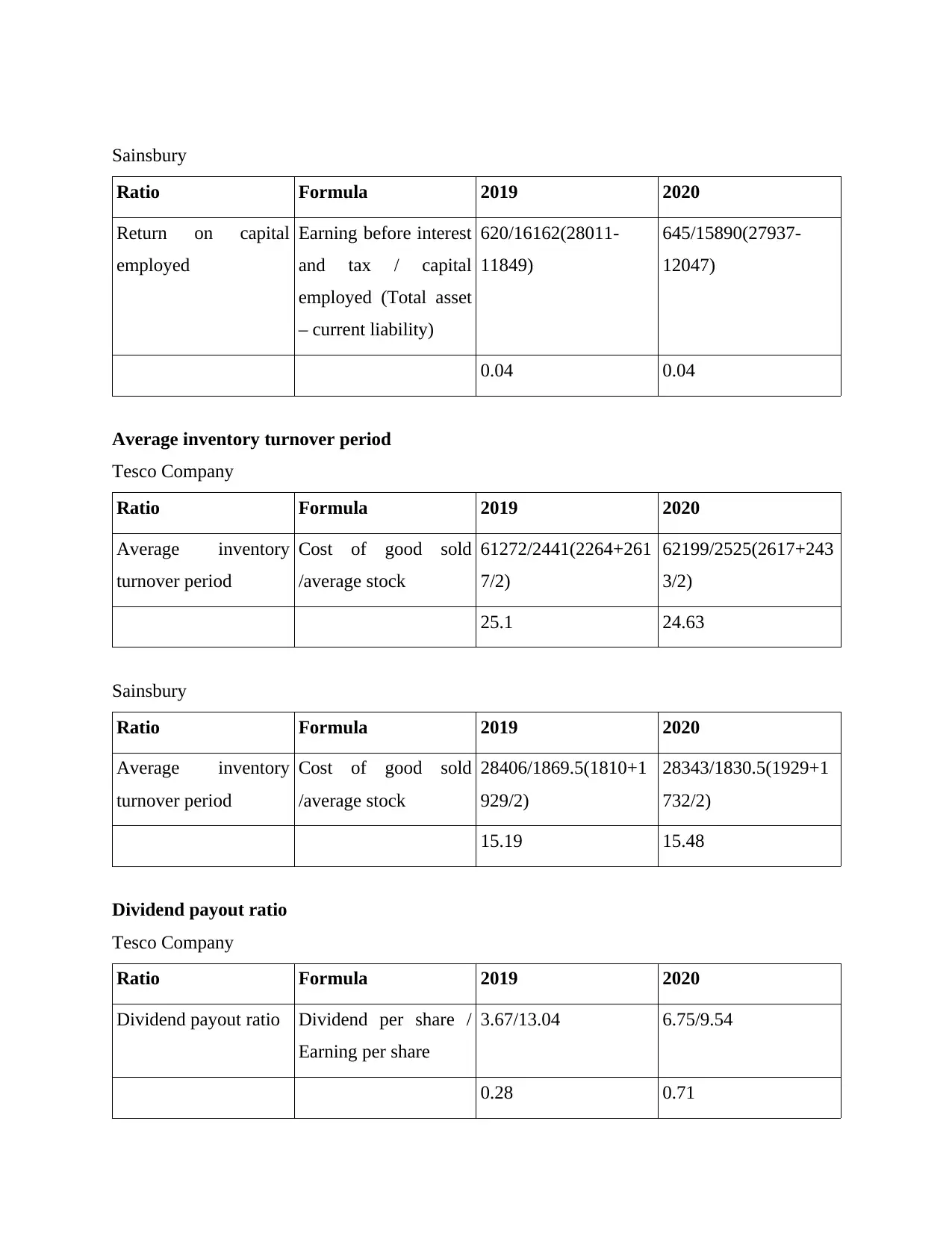

Sainsbury

Ratio Formula 2019 2020

Return on capital

employed

Earning before interest

and tax / capital

employed (Total asset

– current liability)

620/16162(28011-

11849)

645/15890(27937-

12047)

0.04 0.04

Average inventory turnover period

Tesco Company

Ratio Formula 2019 2020

Average inventory

turnover period

Cost of good sold

/average stock

61272/2441(2264+261

7/2)

62199/2525(2617+243

3/2)

25.1 24.63

Sainsbury

Ratio Formula 2019 2020

Average inventory

turnover period

Cost of good sold

/average stock

28406/1869.5(1810+1

929/2)

28343/1830.5(1929+1

732/2)

15.19 15.48

Dividend payout ratio

Tesco Company

Ratio Formula 2019 2020

Dividend payout ratio Dividend per share /

Earning per share

3.67/13.04 6.75/9.54

0.28 0.71

Ratio Formula 2019 2020

Return on capital

employed

Earning before interest

and tax / capital

employed (Total asset

– current liability)

620/16162(28011-

11849)

645/15890(27937-

12047)

0.04 0.04

Average inventory turnover period

Tesco Company

Ratio Formula 2019 2020

Average inventory

turnover period

Cost of good sold

/average stock

61272/2441(2264+261

7/2)

62199/2525(2617+243

3/2)

25.1 24.63

Sainsbury

Ratio Formula 2019 2020

Average inventory

turnover period

Cost of good sold

/average stock

28406/1869.5(1810+1

929/2)

28343/1830.5(1929+1

732/2)

15.19 15.48

Dividend payout ratio

Tesco Company

Ratio Formula 2019 2020

Dividend payout ratio Dividend per share /

Earning per share

3.67/13.04 6.75/9.54

0.28 0.71

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Sainsbury

Ratio Formula 2019 2020

Dividend payout ratio Dividend per share /

Earning per share

10.2/7.5 11.2/5.8

1.36 1.93

Analysis financial position of companies

Current ratio of Tesco Company indicate that company has entertained a current ratio

of .6 in the year 2019 and .72 in the year 2020 which indicate that company's current ratio

management has been improved and become more effective as compare to the previous financial

year. In case of Sainsbury Company is projected that company's current ratio of the receptive

organisation is calculated as .64 for the year 2019 and .63 for financial year 2020. In both the

financial year company's current ratio management has been almost similar. It can be stated that

Tesco Company could manage in more professional way its current assets and current liabilities

(Mirhaj and Izadinia, 2017). Both these companies can provide better control in its current assets

and current liabilities position which will allow these companies to improve the overall potential

outcomes in the respective organisations. Quick ratio calculated denote that Tesco Company

hold the quick ratio for the year 2019 as .47 and in the year 2020 the ratio is .58 whereas for the

Sainsbury Company the ratio is .47 and .49. The quick ratio indicate about the liquidity position

and situation of organisation. ON the basis of the quick ratio it has indicated that Tesco

Company hold better liquidity position in comparison to the Sainsbury Company. Both the

companies can look for more fruitful choices in respect to management of the liquidity situation

of organisation. The ideal quick ratio is defined as 1:1 that indicate that there is a huge potential

of improvement and development in the liquidity situation of company.

Net profitability indicate that the net benefits or financial outcomes derived out of the

operations of organisation. This is the sole advantage and benefits that a company is derived out

of the business operations entertained by the company. In case of Tesco Company net profit is

reported as 1.99% for the year 2019 and 1.44% for the financial year 2020 whereas on the other

side for the Sainsbury Company the net profitability is defined as .64% and .52% that reflect that

Ratio Formula 2019 2020

Dividend payout ratio Dividend per share /

Earning per share

10.2/7.5 11.2/5.8

1.36 1.93

Analysis financial position of companies

Current ratio of Tesco Company indicate that company has entertained a current ratio

of .6 in the year 2019 and .72 in the year 2020 which indicate that company's current ratio

management has been improved and become more effective as compare to the previous financial

year. In case of Sainsbury Company is projected that company's current ratio of the receptive

organisation is calculated as .64 for the year 2019 and .63 for financial year 2020. In both the

financial year company's current ratio management has been almost similar. It can be stated that

Tesco Company could manage in more professional way its current assets and current liabilities

(Mirhaj and Izadinia, 2017). Both these companies can provide better control in its current assets

and current liabilities position which will allow these companies to improve the overall potential

outcomes in the respective organisations. Quick ratio calculated denote that Tesco Company

hold the quick ratio for the year 2019 as .47 and in the year 2020 the ratio is .58 whereas for the

Sainsbury Company the ratio is .47 and .49. The quick ratio indicate about the liquidity position

and situation of organisation. ON the basis of the quick ratio it has indicated that Tesco

Company hold better liquidity position in comparison to the Sainsbury Company. Both the

companies can look for more fruitful choices in respect to management of the liquidity situation

of organisation. The ideal quick ratio is defined as 1:1 that indicate that there is a huge potential

of improvement and development in the liquidity situation of company.

Net profitability indicate that the net benefits or financial outcomes derived out of the

operations of organisation. This is the sole advantage and benefits that a company is derived out

of the business operations entertained by the company. In case of Tesco Company net profit is

reported as 1.99% for the year 2019 and 1.44% for the financial year 2020 whereas on the other

side for the Sainsbury Company the net profitability is defined as .64% and .52% that reflect that

Tesco Company hold stronger position or financial stability in comparison with the Sainsbury

Company. Net profit is the sole projection of company's operations. Gross profit ratio calculated

by the company indicate that the Tesco Company gross profit is identified as 7.06% for the year

2019 and 6.56% for the year 2020 in context to the Tresco Company. The other hand of the

Sainsbury Company it I calculated as 6.49% and 6.56% which further reflect that Tesco

Company hold better and more impressive trading profits as compare to other organisation (Ji,

Lee and Lee, 2017). The another aspect related to the gross profitability indicate that Sainsbury

Company irrespective of having the lower profit margin it could somehow increase or boost its

amount of of gross profitability in the year 2020 as compare to the year 2019 whereas on the

other side Tesco Company irrespective of having better profit ratio the organisation could

entertain decline in its gross profit margins.

Gearing ratio further indicate that Tesco Company could sustain better management of its

EBIT in context to the interest burden as compare to the Sainsbury Company. P/E ratio

calculated identified that company could address the ratio as 14.67 and 17.74 and the Sainsbury

Company could reflect the ratios as 30.34 and 40 which indicate more favourable ratios as

compare to the Tesco Company. In this context it can be projected that Sainsbury Company's

performance is more favourable as compare to other company. Earning per share is the clinical

ratio that project the financial performance of company bin ore professional manner. This ratio

indicates the amount of advantage and benefits company is providing to its shareholders against

the investment they have created in the organisation. Tesco Company has offered an earning per

share of 5.87 in 2019 and 7.78 in the year 2020 on the other side Sainsbury Company has given

an earning per share of -.72 and -2.85 for the previous two financial years to its shareholders that

reflect that Tesco Company could deliver better and more fruitful outcomes against the

investment shareholders could make in the organisation. Return on capital employed in the ratio

that further reflect tha ratios as .07 and .06 in context to the Tesco Company whereas for the

Sainsbury Company it has derived its returns as .04 for both the previous financial years. The

figures are more effective in respect to the Tesco Company. Average inventory period for the

Tesco Company is 25.1 days and 24.63 days on the other side the days are 15.19 and 15.48 for

the Sainsbury Company. This ratio further indicate that Tesco Company is holding its stock for

more number of days in comparison with the Stantonbury Company (Korol, 2018). Dividend

payout ratio identify as .28 and .71in respect to the Tesco Company and in case of the Sainsbury

Company. Net profit is the sole projection of company's operations. Gross profit ratio calculated

by the company indicate that the Tesco Company gross profit is identified as 7.06% for the year

2019 and 6.56% for the year 2020 in context to the Tresco Company. The other hand of the

Sainsbury Company it I calculated as 6.49% and 6.56% which further reflect that Tesco

Company hold better and more impressive trading profits as compare to other organisation (Ji,

Lee and Lee, 2017). The another aspect related to the gross profitability indicate that Sainsbury

Company irrespective of having the lower profit margin it could somehow increase or boost its

amount of of gross profitability in the year 2020 as compare to the year 2019 whereas on the

other side Tesco Company irrespective of having better profit ratio the organisation could

entertain decline in its gross profit margins.

Gearing ratio further indicate that Tesco Company could sustain better management of its

EBIT in context to the interest burden as compare to the Sainsbury Company. P/E ratio

calculated identified that company could address the ratio as 14.67 and 17.74 and the Sainsbury

Company could reflect the ratios as 30.34 and 40 which indicate more favourable ratios as

compare to the Tesco Company. In this context it can be projected that Sainsbury Company's

performance is more favourable as compare to other company. Earning per share is the clinical

ratio that project the financial performance of company bin ore professional manner. This ratio

indicates the amount of advantage and benefits company is providing to its shareholders against

the investment they have created in the organisation. Tesco Company has offered an earning per

share of 5.87 in 2019 and 7.78 in the year 2020 on the other side Sainsbury Company has given

an earning per share of -.72 and -2.85 for the previous two financial years to its shareholders that

reflect that Tesco Company could deliver better and more fruitful outcomes against the

investment shareholders could make in the organisation. Return on capital employed in the ratio

that further reflect tha ratios as .07 and .06 in context to the Tesco Company whereas for the

Sainsbury Company it has derived its returns as .04 for both the previous financial years. The

figures are more effective in respect to the Tesco Company. Average inventory period for the

Tesco Company is 25.1 days and 24.63 days on the other side the days are 15.19 and 15.48 for

the Sainsbury Company. This ratio further indicate that Tesco Company is holding its stock for

more number of days in comparison with the Stantonbury Company (Korol, 2018). Dividend

payout ratio identify as .28 and .71in respect to the Tesco Company and in case of the Sainsbury

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Company the same ratios calculated as 1.36 and 1.93 that indicate that Sainsbury Company hold

better management in respect to the dividend payout process. It can be analysis on the basis of all

the ratios calculated that Tesco Company could dominate in majority of ratio calculation whereas

Sainsbury Company hold better position ion case of some specific ratios. Both the companies

needed to make strong decision-making so that better and more effective results can considered

out of the business operations entertained by the company.

Recommendations for poorly performing company

On the basis of the financial ratios calculated and interpretation conducted in the previous

part of the report it can be stated that Sainsbury Company is more poorly performing

organisation in comparison to the Tesco Company. Sainsbury Company can focus over

improving the liquidity situation of company. It can improve its current ratio and quick ratio in

such a way that company can entertain the best level of liquidity in the market (Shaverd and

et.al., 2016). Both ratios must be registered at 1:1 ratio. Company should control its current

liability to improve the liquidity situation of the organisation. Company's net profitability is also

going into the negative mark that also needed to improve by the organisation. It should control

its indirect nature of expenditures that would further increase or boost the overall profitability of

the organisation. Company must further improve its gross nature profitability tat can enhance and

boost the further amount of profitability of the organisation. Net profit can only be improved by

controlling the indirect category expenditure of the company. In comparison to other key

competitors like Tesco Company the gross and net profit of the company is low that needed to

boost by the organisation. Company should also focuses over improving the use of its fixed

nature assets. This is the basic need and requirement that company needed to overlook as it is

required to improve the utilisation of its fixed nature assets so that better profitability of

company can entertain.

Limitation of financial ratios

Financial ratios are of different types and denote about different areas of the organisation

performance. They are the true reflector of company's financial position in the respective

financial year that support company to make crucial decisions in favour of the organisation.

Financial ratios indicate about the financial position and stability of the organisation that further

over shadowed different and various factors which also influence overall performance of the

organisation. It involve different external; business environment factors like political,

better management in respect to the dividend payout process. It can be analysis on the basis of all

the ratios calculated that Tesco Company could dominate in majority of ratio calculation whereas

Sainsbury Company hold better position ion case of some specific ratios. Both the companies

needed to make strong decision-making so that better and more effective results can considered

out of the business operations entertained by the company.

Recommendations for poorly performing company

On the basis of the financial ratios calculated and interpretation conducted in the previous

part of the report it can be stated that Sainsbury Company is more poorly performing

organisation in comparison to the Tesco Company. Sainsbury Company can focus over

improving the liquidity situation of company. It can improve its current ratio and quick ratio in

such a way that company can entertain the best level of liquidity in the market (Shaverd and

et.al., 2016). Both ratios must be registered at 1:1 ratio. Company should control its current

liability to improve the liquidity situation of the organisation. Company's net profitability is also

going into the negative mark that also needed to improve by the organisation. It should control

its indirect nature of expenditures that would further increase or boost the overall profitability of

the organisation. Company must further improve its gross nature profitability tat can enhance and

boost the further amount of profitability of the organisation. Net profit can only be improved by

controlling the indirect category expenditure of the company. In comparison to other key

competitors like Tesco Company the gross and net profit of the company is low that needed to

boost by the organisation. Company should also focuses over improving the use of its fixed

nature assets. This is the basic need and requirement that company needed to overlook as it is

required to improve the utilisation of its fixed nature assets so that better profitability of

company can entertain.

Limitation of financial ratios

Financial ratios are of different types and denote about different areas of the organisation

performance. They are the true reflector of company's financial position in the respective

financial year that support company to make crucial decisions in favour of the organisation.

Financial ratios indicate about the financial position and stability of the organisation that further

over shadowed different and various factors which also influence overall performance of the

organisation. It involve different external; business environment factors like political,

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

economical, social, technological, environment and legal fact0ors of external business

environment which also influence overall performance of the organisation in the respective

market. Different internal factors like organisation resources, leadership, employee issues, talent

management and many other internal aspects of company that do not reflect over the financial

book of accounts of company are also influence the overall performance of organisation (Cuong

and Ha, 2018). The financial statement and ratios only reflect the areas that are covered under the

evaluation of the financial position of organisation but it do not indicate the various indirect

factors or elements that also influence overall performance of organisation. Inflation is also a

critical factor that influence the overall performance of company do not reflect in the financial

statements of the organisation.

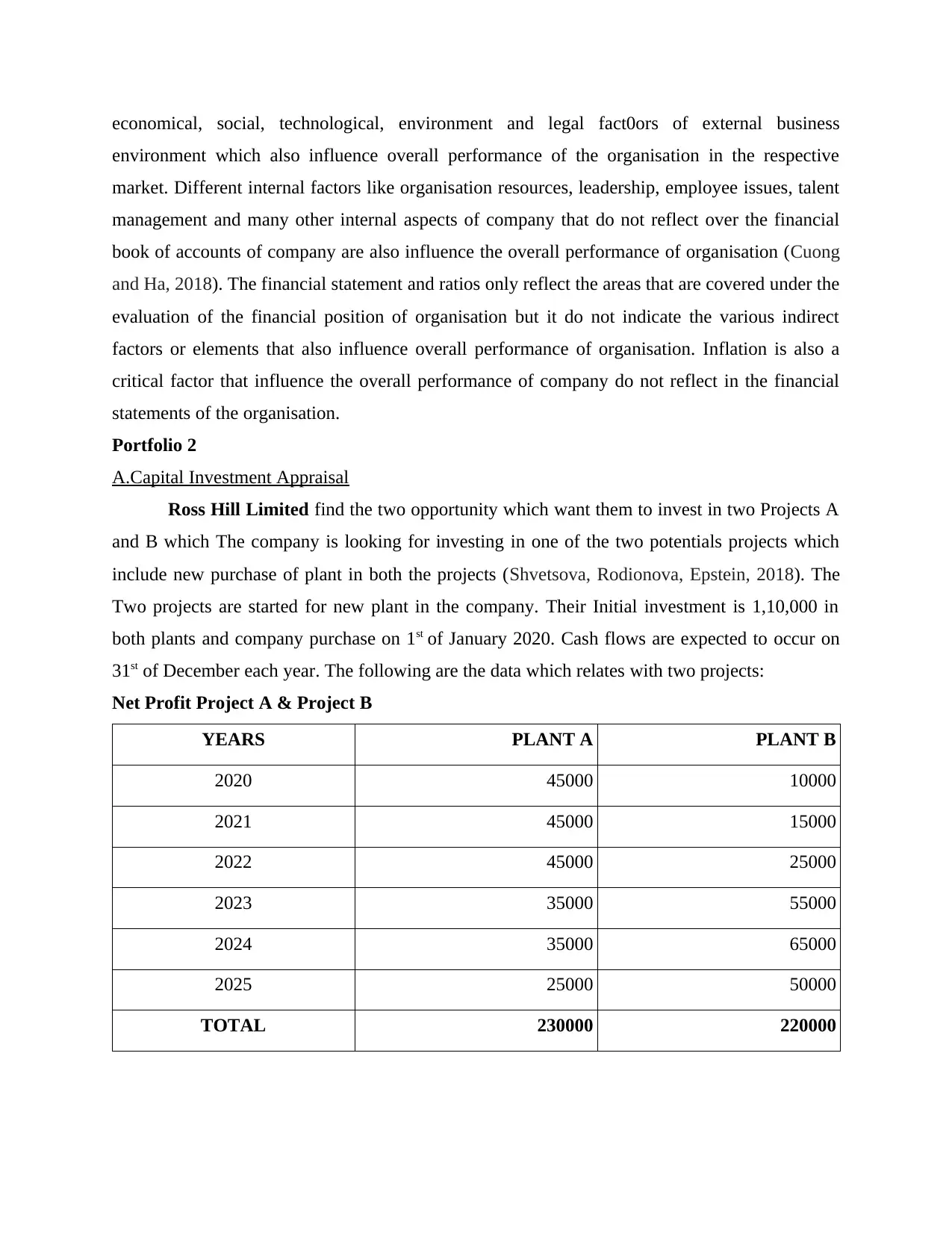

Portfolio 2

A.Capital Investment Appraisal

Ross Hill Limited find the two opportunity which want them to invest in two Projects A

and B which The company is looking for investing in one of the two potentials projects which

include new purchase of plant in both the projects (Shvetsova, Rodionova, Epstein, 2018). The

Two projects are started for new plant in the company. Their Initial investment is 1,10,000 in

both plants and company purchase on 1st of January 2020. Cash flows are expected to occur on

31st of December each year. The following are the data which relates with two projects:

Net Profit Project A & Project B

YEARS PLANT A PLANT B

2020 45000 10000

2021 45000 15000

2022 45000 25000

2023 35000 55000

2024 35000 65000

2025 25000 50000

TOTAL 230000 220000

environment which also influence overall performance of the organisation in the respective

market. Different internal factors like organisation resources, leadership, employee issues, talent

management and many other internal aspects of company that do not reflect over the financial

book of accounts of company are also influence the overall performance of organisation (Cuong

and Ha, 2018). The financial statement and ratios only reflect the areas that are covered under the

evaluation of the financial position of organisation but it do not indicate the various indirect

factors or elements that also influence overall performance of organisation. Inflation is also a

critical factor that influence the overall performance of company do not reflect in the financial

statements of the organisation.

Portfolio 2

A.Capital Investment Appraisal

Ross Hill Limited find the two opportunity which want them to invest in two Projects A

and B which The company is looking for investing in one of the two potentials projects which

include new purchase of plant in both the projects (Shvetsova, Rodionova, Epstein, 2018). The

Two projects are started for new plant in the company. Their Initial investment is 1,10,000 in

both plants and company purchase on 1st of January 2020. Cash flows are expected to occur on

31st of December each year. The following are the data which relates with two projects:

Net Profit Project A & Project B

YEARS PLANT A PLANT B

2020 45000 10000

2021 45000 15000

2022 45000 25000

2023 35000 55000

2024 35000 65000

2025 25000 50000

TOTAL 230000 220000

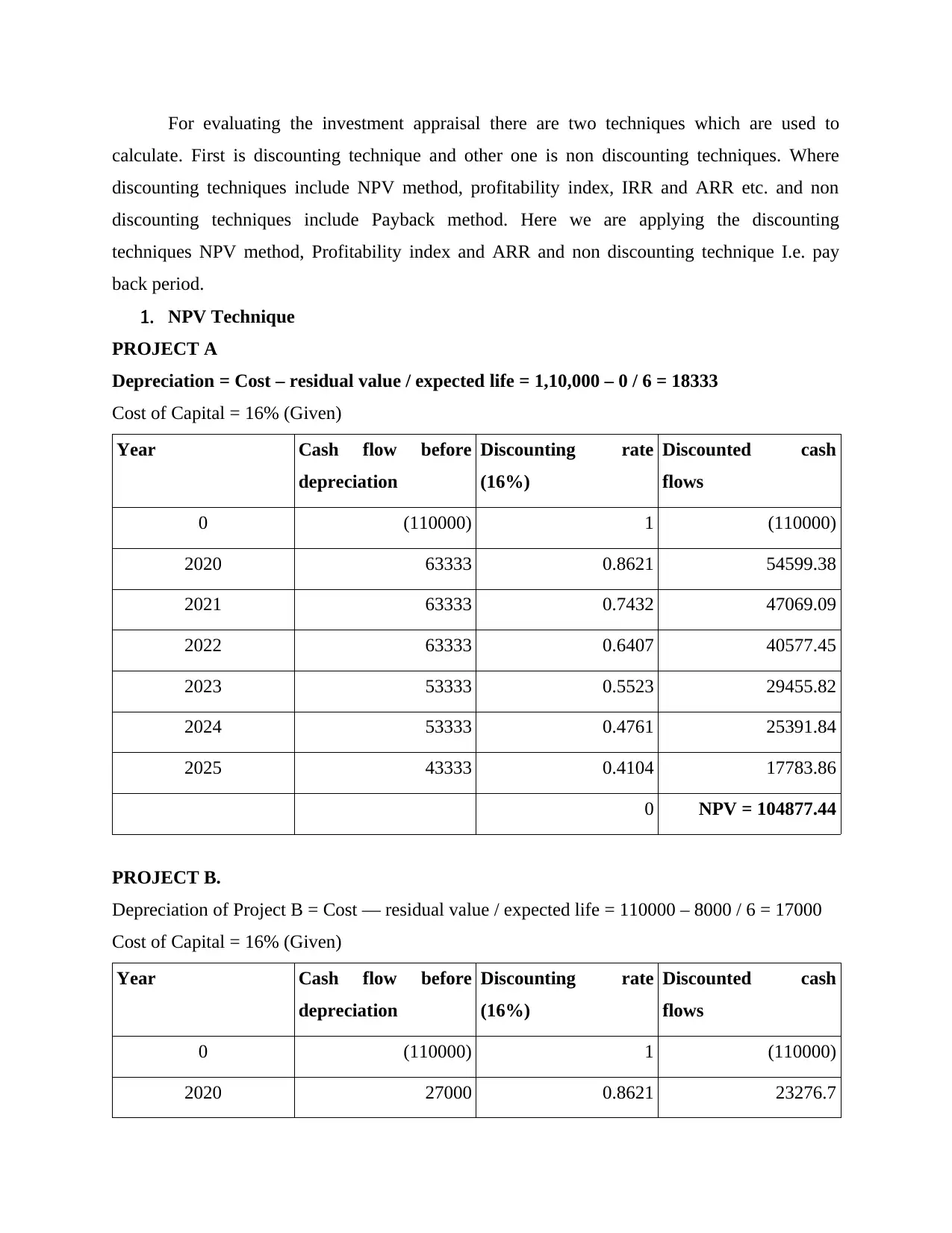

For evaluating the investment appraisal there are two techniques which are used to

calculate. First is discounting technique and other one is non discounting techniques. Where

discounting techniques include NPV method, profitability index, IRR and ARR etc. and non

discounting techniques include Payback method. Here we are applying the discounting

techniques NPV method, Profitability index and ARR and non discounting technique I.e. pay

back period.

1. NPV Technique

PROJECT A

Depreciation = Cost – residual value / expected life = 1,10,000 – 0 / 6 = 18333

Cost of Capital = 16% (Given)

Year Cash flow before

depreciation

Discounting rate

(16%)

Discounted cash

flows

0 (110000) 1 (110000)

2020 63333 0.8621 54599.38

2021 63333 0.7432 47069.09

2022 63333 0.6407 40577.45

2023 53333 0.5523 29455.82

2024 53333 0.4761 25391.84

2025 43333 0.4104 17783.86

0 NPV = 104877.44

PROJECT B.

Depreciation of Project B = Cost — residual value / expected life = 110000 – 8000 / 6 = 17000

Cost of Capital = 16% (Given)

Year Cash flow before

depreciation

Discounting rate

(16%)

Discounted cash

flows

0 (110000) 1 (110000)

2020 27000 0.8621 23276.7

calculate. First is discounting technique and other one is non discounting techniques. Where

discounting techniques include NPV method, profitability index, IRR and ARR etc. and non

discounting techniques include Payback method. Here we are applying the discounting

techniques NPV method, Profitability index and ARR and non discounting technique I.e. pay

back period.

1. NPV Technique

PROJECT A

Depreciation = Cost – residual value / expected life = 1,10,000 – 0 / 6 = 18333

Cost of Capital = 16% (Given)

Year Cash flow before

depreciation

Discounting rate

(16%)

Discounted cash

flows

0 (110000) 1 (110000)

2020 63333 0.8621 54599.38

2021 63333 0.7432 47069.09

2022 63333 0.6407 40577.45

2023 53333 0.5523 29455.82

2024 53333 0.4761 25391.84

2025 43333 0.4104 17783.86

0 NPV = 104877.44

PROJECT B.

Depreciation of Project B = Cost — residual value / expected life = 110000 – 8000 / 6 = 17000

Cost of Capital = 16% (Given)

Year Cash flow before

depreciation

Discounting rate

(16%)

Discounted cash

flows

0 (110000) 1 (110000)

2020 27000 0.8621 23276.7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.