Capital Budgeting and Project Analysis: EFN406 Assignment - Semester 2

VerifiedAdded on 2022/11/14

|10

|1497

|202

Homework Assignment

AI Summary

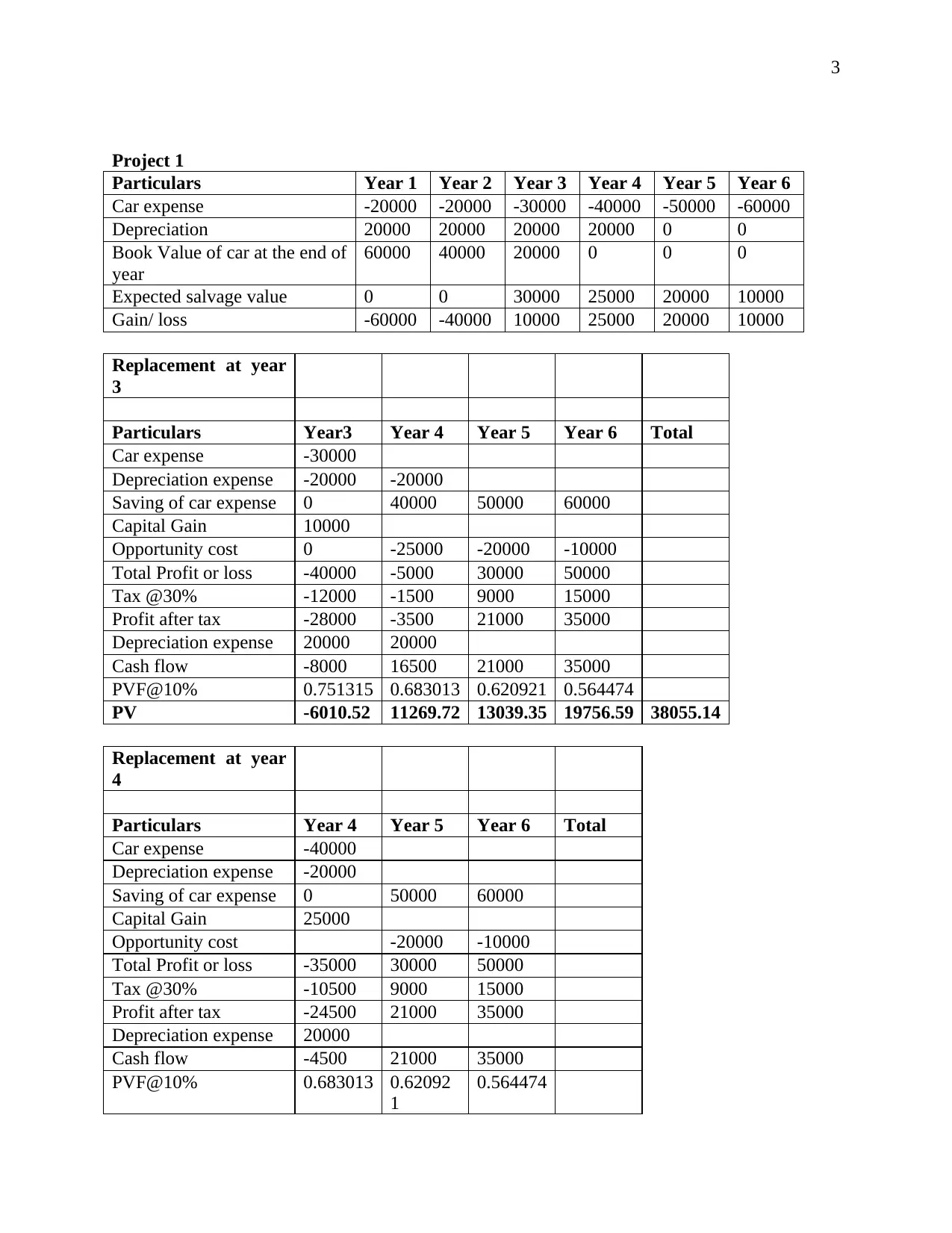

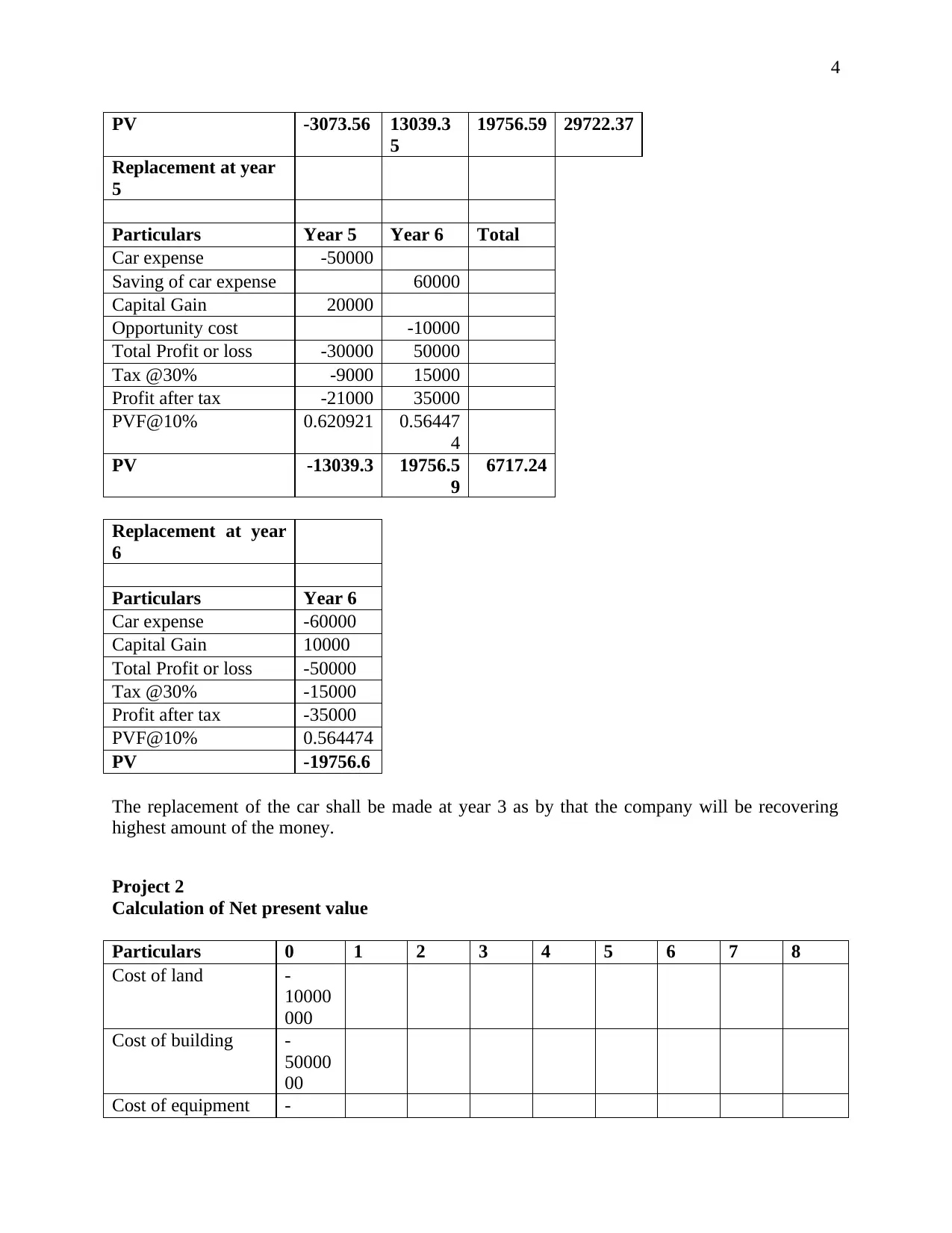

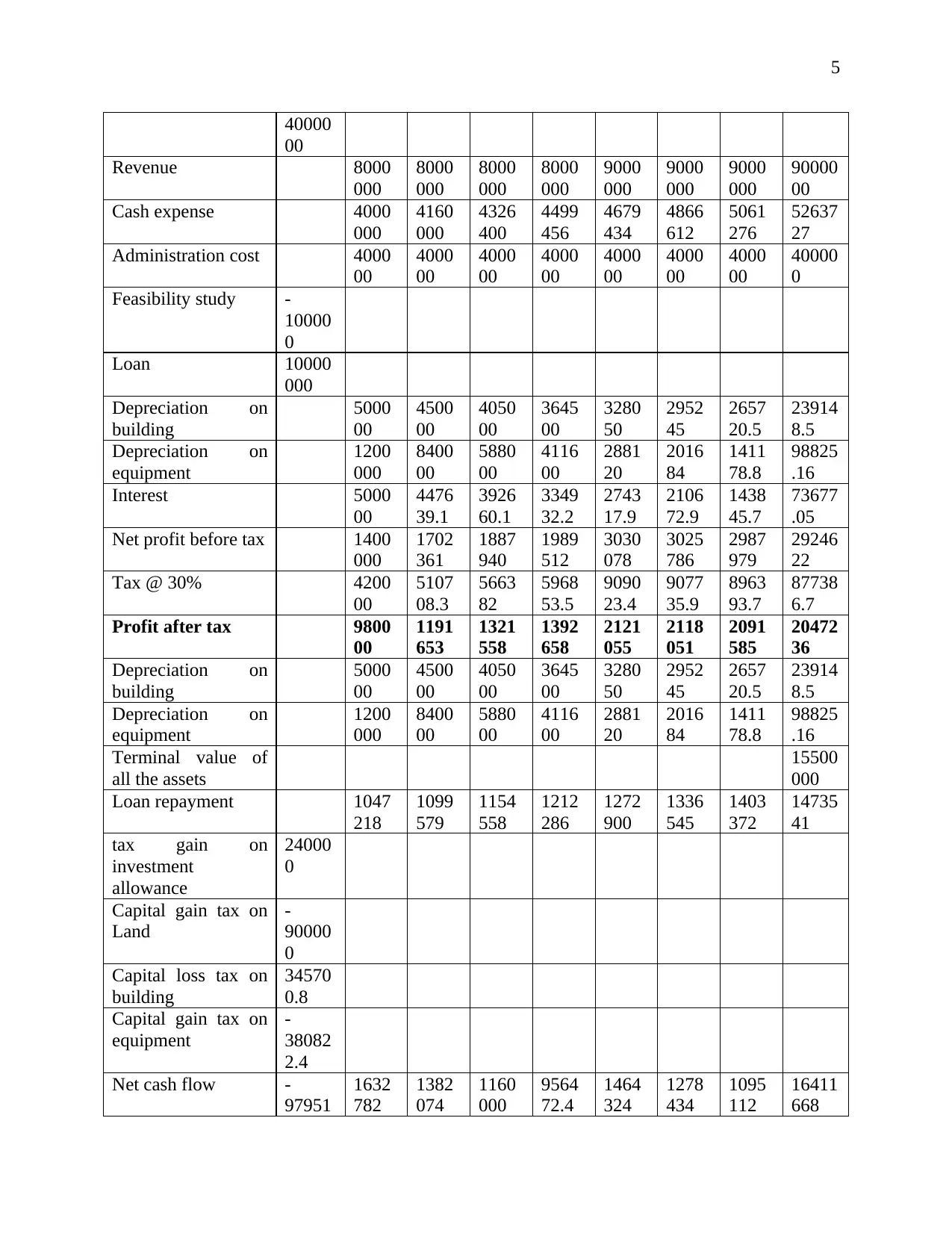

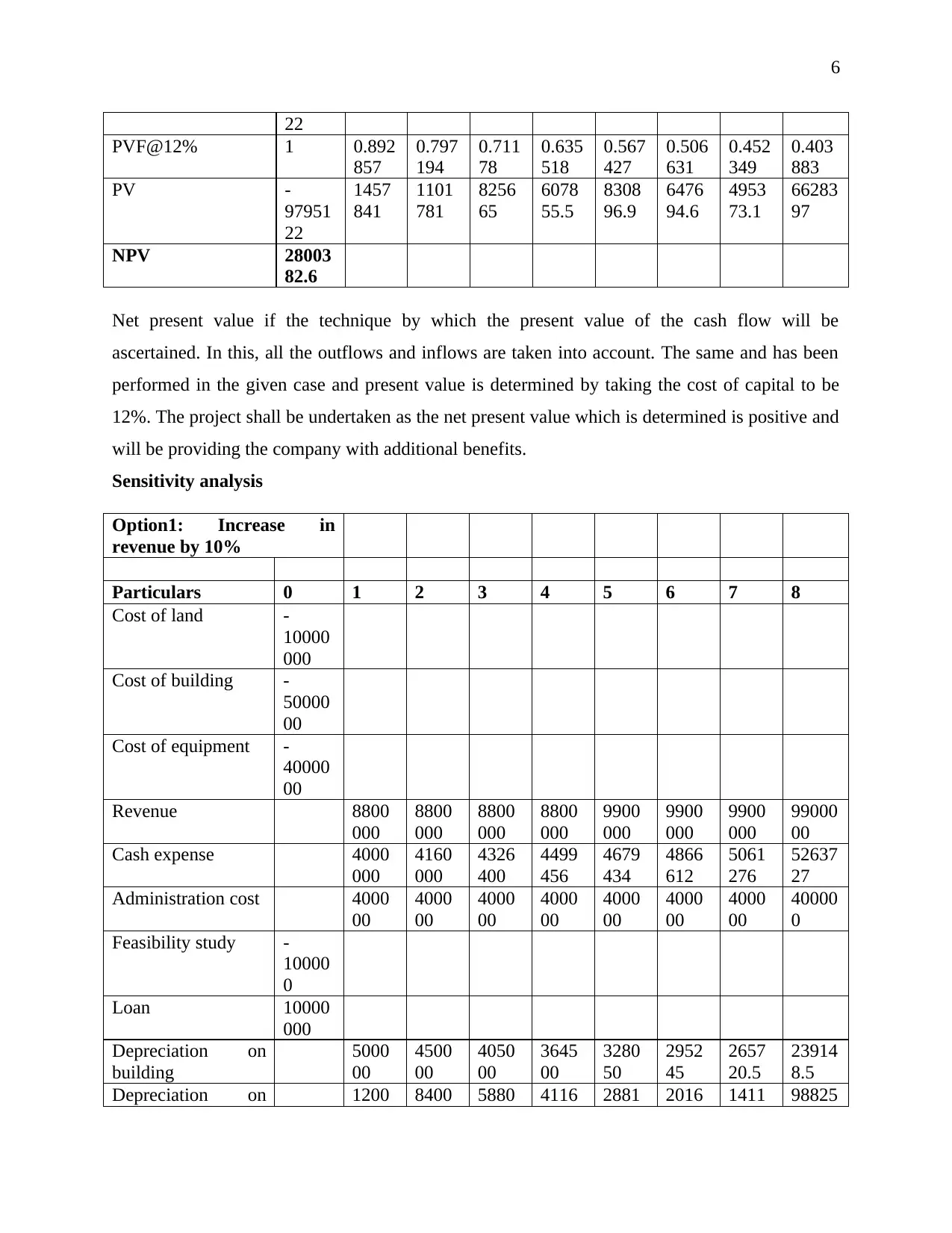

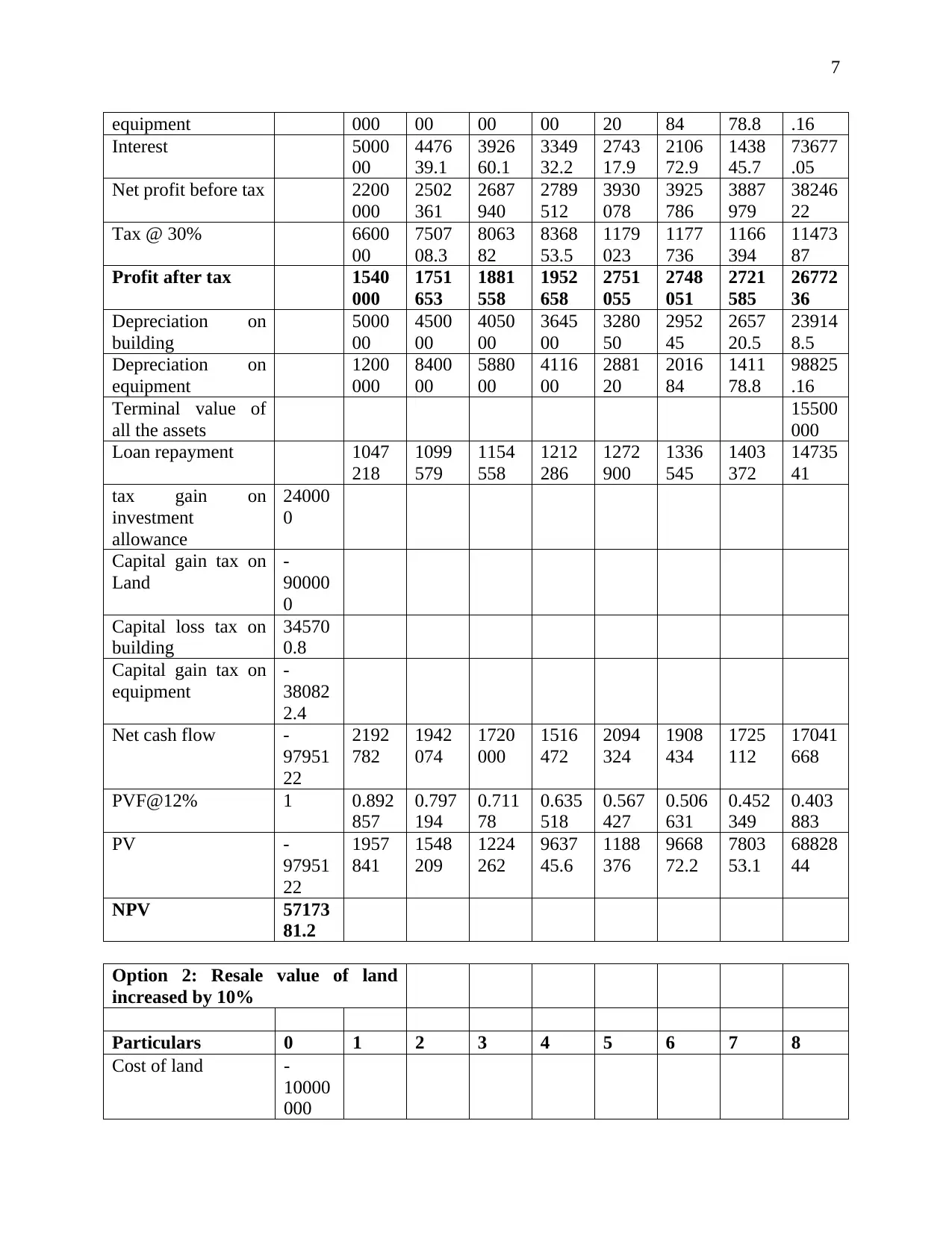

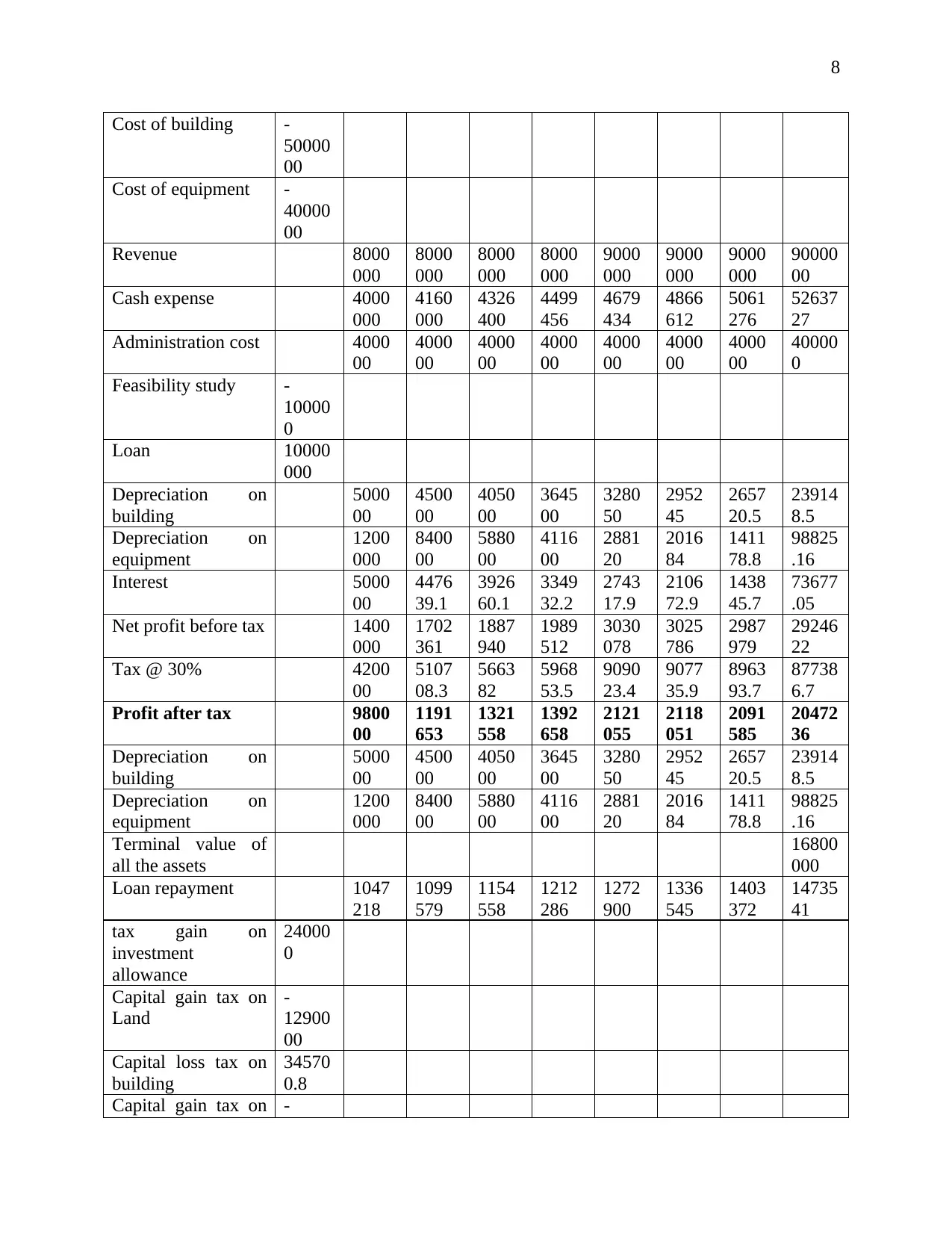

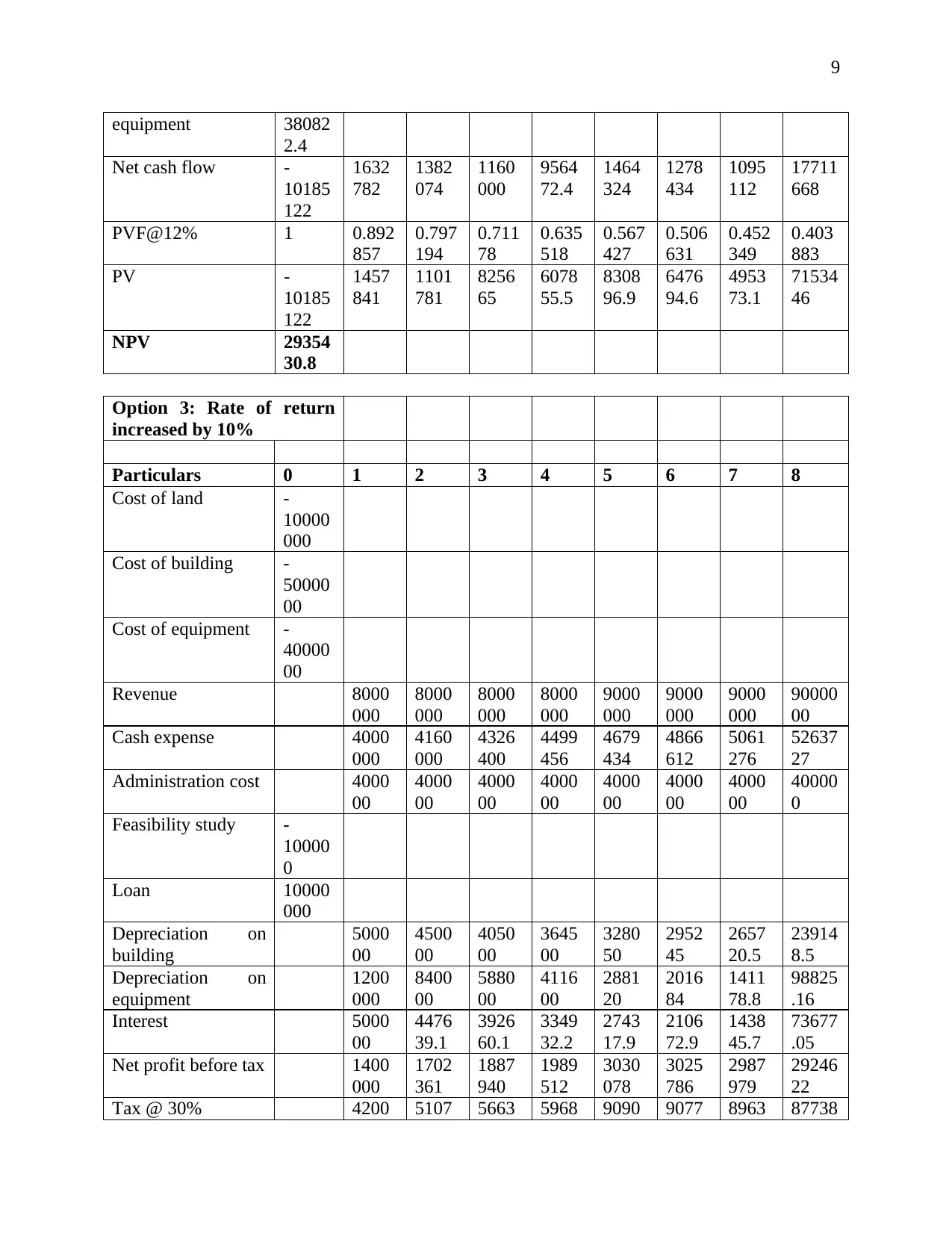

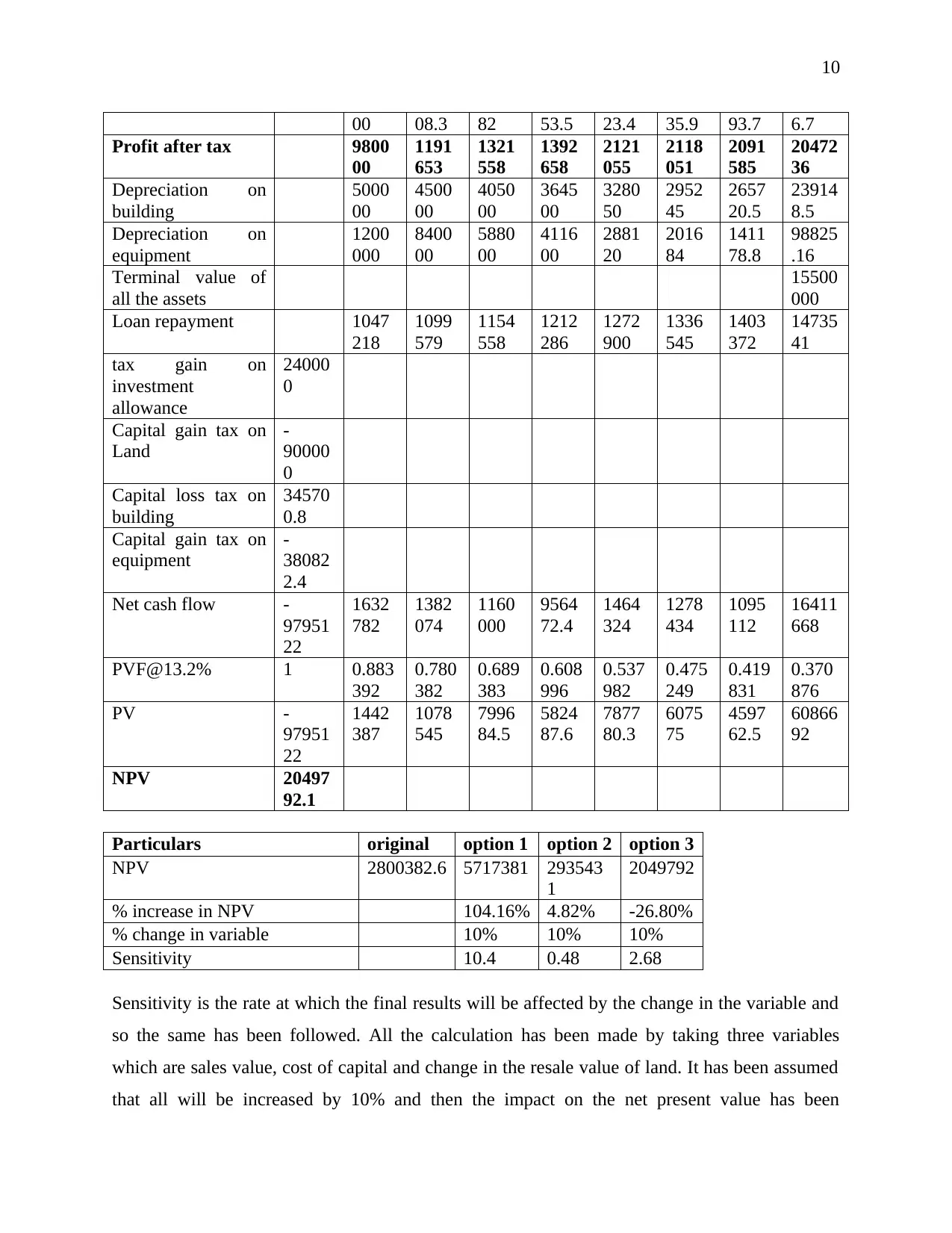

This document presents a comprehensive solution to a capital budgeting assignment, evaluating two distinct projects using financial analysis techniques. Project 1 assesses the optimal timing for car replacement, considering car expenses, depreciation, salvage value, and opportunity costs across multiple years. The analysis includes calculating cash flows, applying a 30% tax rate, and determining the present value of cash flows at a 10% discount rate to identify the most financially advantageous replacement year. Project 2 involves a detailed net present value (NPV) calculation for a new project, incorporating costs, revenues, cash expenses, administration costs, and depreciation. It accounts for loan repayments, interest, and tax implications, and also includes a sensitivity analysis to assess the impact of changes in revenue, resale value of land, and the rate of return on the project's NPV. The findings are presented in Excel format, illustrating the financial viability and sensitivity of the projects.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.