Managerial Finance Report: Financial Performance of Sainsbury & Tesco

VerifiedAdded on 2020/01/07

|20

|4362

|182

Report

AI Summary

This report presents a comprehensive analysis of the financial performance of two major retail companies, Sainsbury and Tesco, using various financial ratios. The analysis includes the calculation and interpretation of key ratios such as current ratio, quick ratio, net profit ratio, gross profit ratio, debt-equity ratio, price-earnings ratio, ROCE, inventory turnover ratio, dividend payout ratio, and gearing ratio. The report compares the performance of the two companies across these metrics, highlighting their strengths and weaknesses. Furthermore, it explores potential strategies for improving the performance of poorly performing businesses. The second part of the report delves into project evaluation methods, including payback period, average rate of return (ARR), net present value (NPV), and internal rate of return (IRR), along with a discussion of the limitations of using investment appraisal techniques for long-term decision-making.

MANAGERIAL FINANCE

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION.....................................................................................................................................3

Portfolio1...................................................................................................................................................3

(a) Calculation of ratios..........................................................................................................................3

(b) Way in which performance of poorly performing business can be improved.................................13

© Limitation of relying on ratios to measure firm performance...........................................................14

Portfolio 2................................................................................................................................................15

(a)Project evaluation method...............................................................................................................15

(b) Limitations of using investment appraisal techniques for long term decision making....................17

CONCLUSION........................................................................................................................................18

REFERENCES........................................................................................................................................19

Figure 1Current ratio of Tesco and Sainsbury...........................................................................................3

Figure 2 Quick ratio of Sainsbury and Tesco.............................................................................................4

Figure 3 Net profit ratio of Sainsbury and Tesco.......................................................................................5

Figure 4 Gross profit ratio of Sainsbury and Tesco....................................................................................6

Figure 6 PE ratio of Sainsbury and Tesco..................................................................................................7

Figure 7 ROCE of Sainsbury and Tesco....................................................................................................8

Figure 8 Inventory turnover ratio of Sainsbury and Tesco.........................................................................9

Figure 9 Dividend payout ratio of Tesco and Sainsbury............................................................................9

Figure 10 Gearing ratio of Sainsbury and Tesco......................................................................................10

Table 1 Ratio analysis of Sainsbury...........................................................................................................4

Table 2 Ratio analysis of Tesco.................................................................................................................5

Table 3 Calculation of payback period.....................................................................................................16

Table 4 Calculation of ARR....................................................................................................................16

Table 5 Calculation of NPV.....................................................................................................................17

Table 6 Calculation of IRR......................................................................................................................18

INTRODUCTION.....................................................................................................................................3

Portfolio1...................................................................................................................................................3

(a) Calculation of ratios..........................................................................................................................3

(b) Way in which performance of poorly performing business can be improved.................................13

© Limitation of relying on ratios to measure firm performance...........................................................14

Portfolio 2................................................................................................................................................15

(a)Project evaluation method...............................................................................................................15

(b) Limitations of using investment appraisal techniques for long term decision making....................17

CONCLUSION........................................................................................................................................18

REFERENCES........................................................................................................................................19

Figure 1Current ratio of Tesco and Sainsbury...........................................................................................3

Figure 2 Quick ratio of Sainsbury and Tesco.............................................................................................4

Figure 3 Net profit ratio of Sainsbury and Tesco.......................................................................................5

Figure 4 Gross profit ratio of Sainsbury and Tesco....................................................................................6

Figure 6 PE ratio of Sainsbury and Tesco..................................................................................................7

Figure 7 ROCE of Sainsbury and Tesco....................................................................................................8

Figure 8 Inventory turnover ratio of Sainsbury and Tesco.........................................................................9

Figure 9 Dividend payout ratio of Tesco and Sainsbury............................................................................9

Figure 10 Gearing ratio of Sainsbury and Tesco......................................................................................10

Table 1 Ratio analysis of Sainsbury...........................................................................................................4

Table 2 Ratio analysis of Tesco.................................................................................................................5

Table 3 Calculation of payback period.....................................................................................................16

Table 4 Calculation of ARR....................................................................................................................16

Table 5 Calculation of NPV.....................................................................................................................17

Table 6 Calculation of IRR......................................................................................................................18

INTRODUCTION

Making an investment in the business firm is a very tough task and lots of decisions

need to be made in respect to making an investment in the shares. In the current report ratio

analysis is done and comments are made on the firm ratios. In this respect two firms are taken

which are Sainsbury and Tesco. Comparison of both firms’ ratios is done and recommendations

are given in respect to improvements that can be done in specific area. In second part of the

report project evaluation is done and on that basis specific project is selected. Limitation of

project evaluation methods are also explained briefly at end of the report.

Portfolio1

(a) Calculation of ratios

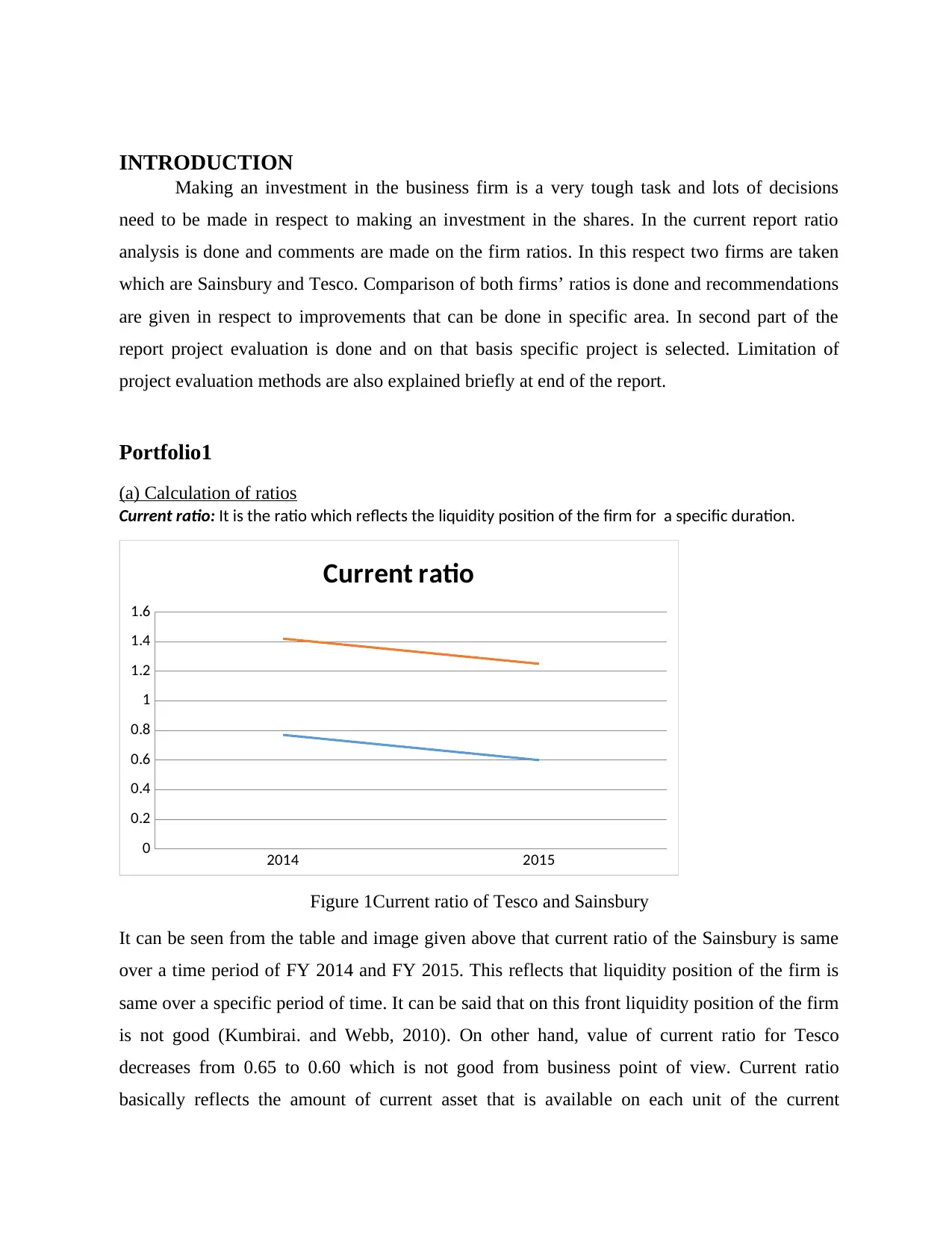

Current ratio: It is the ratio which reflects the liquidity position of the firm for a specific duration.

2014 2015

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

Current ratio

Figure 1Current ratio of Tesco and Sainsbury

It can be seen from the table and image given above that current ratio of the Sainsbury is same

over a time period of FY 2014 and FY 2015. This reflects that liquidity position of the firm is

same over a specific period of time. It can be said that on this front liquidity position of the firm

is not good (Kumbirai. and Webb, 2010). On other hand, value of current ratio for Tesco

decreases from 0.65 to 0.60 which is not good from business point of view. Current ratio

basically reflects the amount of current asset that is available on each unit of the current

Making an investment in the business firm is a very tough task and lots of decisions

need to be made in respect to making an investment in the shares. In the current report ratio

analysis is done and comments are made on the firm ratios. In this respect two firms are taken

which are Sainsbury and Tesco. Comparison of both firms’ ratios is done and recommendations

are given in respect to improvements that can be done in specific area. In second part of the

report project evaluation is done and on that basis specific project is selected. Limitation of

project evaluation methods are also explained briefly at end of the report.

Portfolio1

(a) Calculation of ratios

Current ratio: It is the ratio which reflects the liquidity position of the firm for a specific duration.

2014 2015

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

Current ratio

Figure 1Current ratio of Tesco and Sainsbury

It can be seen from the table and image given above that current ratio of the Sainsbury is same

over a time period of FY 2014 and FY 2015. This reflects that liquidity position of the firm is

same over a specific period of time. It can be said that on this front liquidity position of the firm

is not good (Kumbirai. and Webb, 2010). On other hand, value of current ratio for Tesco

decreases from 0.65 to 0.60 which is not good from business point of view. Current ratio

basically reflects the amount of current asset that is available on each unit of the current

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

liability. It can be said that for every one pound of current liability Sainsbury have 0.33 current

asset. This reflects that firm does not have sufficient amount of money to pay its current liability

on time by using current asset.This happened because it failed to make and implement good

cash management strategy for the business. The availability of current asset in Tesco business

also decline. In case of both firms insufficient cash is available which is matter of concern for

them in terms of timely payment of current liability. However, on comparison it can be said that

Tesco liquidity position is better than Sainsbury. Due to decline in current ratio firm may face

shortage of cash in its business and may find it difficult to pay current liability on time.

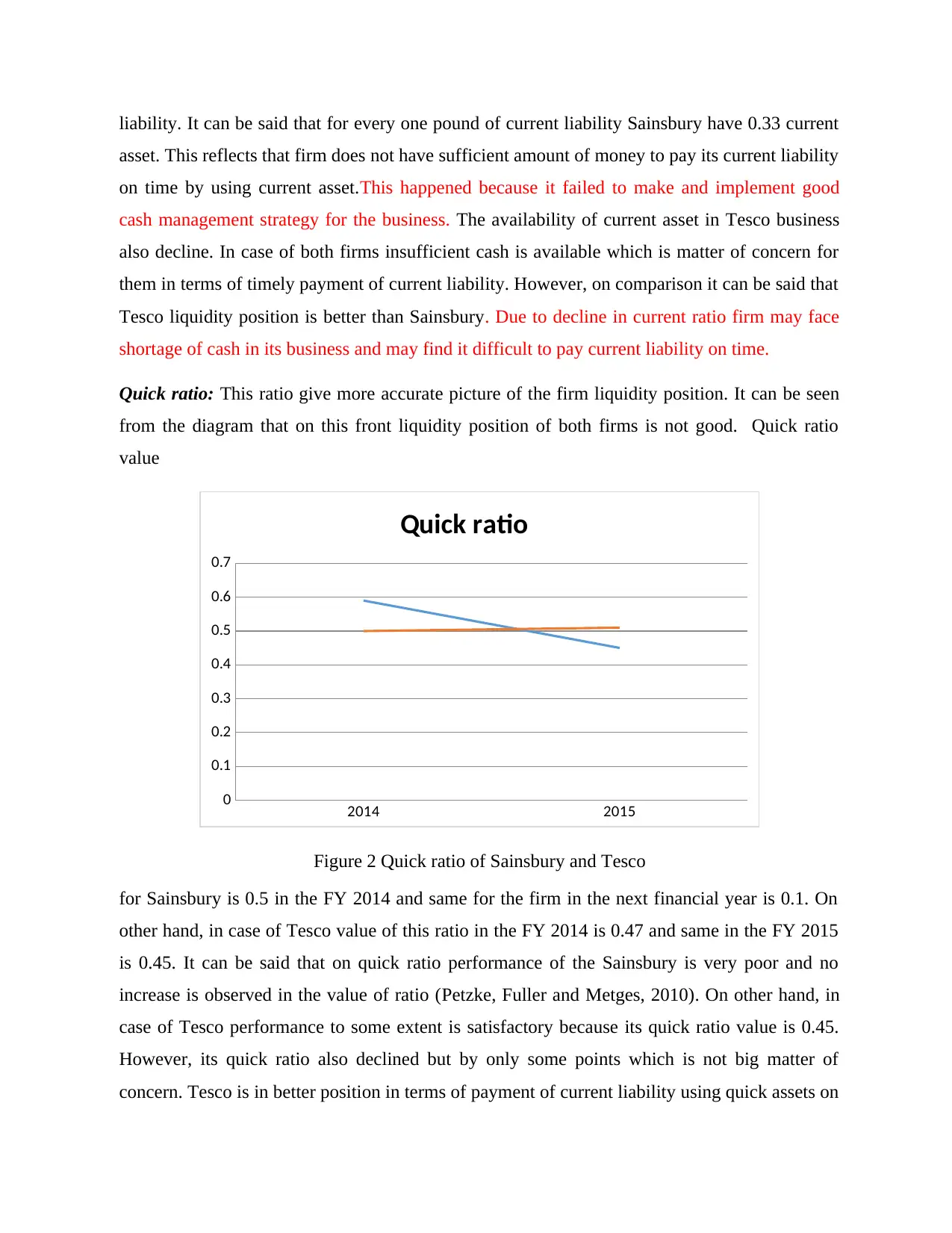

Quick ratio: This ratio give more accurate picture of the firm liquidity position. It can be seen

from the diagram that on this front liquidity position of both firms is not good. Quick ratio

value

2014 2015

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

Quick ratio

Figure 2 Quick ratio of Sainsbury and Tesco

for Sainsbury is 0.5 in the FY 2014 and same for the firm in the next financial year is 0.1. On

other hand, in case of Tesco value of this ratio in the FY 2014 is 0.47 and same in the FY 2015

is 0.45. It can be said that on quick ratio performance of the Sainsbury is very poor and no

increase is observed in the value of ratio (Petzke, Fuller and Metges, 2010). On other hand, in

case of Tesco performance to some extent is satisfactory because its quick ratio value is 0.45.

However, its quick ratio also declined but by only some points which is not big matter of

concern. Tesco is in better position in terms of payment of current liability using quick assets on

asset. This reflects that firm does not have sufficient amount of money to pay its current liability

on time by using current asset.This happened because it failed to make and implement good

cash management strategy for the business. The availability of current asset in Tesco business

also decline. In case of both firms insufficient cash is available which is matter of concern for

them in terms of timely payment of current liability. However, on comparison it can be said that

Tesco liquidity position is better than Sainsbury. Due to decline in current ratio firm may face

shortage of cash in its business and may find it difficult to pay current liability on time.

Quick ratio: This ratio give more accurate picture of the firm liquidity position. It can be seen

from the diagram that on this front liquidity position of both firms is not good. Quick ratio

value

2014 2015

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

Quick ratio

Figure 2 Quick ratio of Sainsbury and Tesco

for Sainsbury is 0.5 in the FY 2014 and same for the firm in the next financial year is 0.1. On

other hand, in case of Tesco value of this ratio in the FY 2014 is 0.47 and same in the FY 2015

is 0.45. It can be said that on quick ratio performance of the Sainsbury is very poor and no

increase is observed in the value of ratio (Petzke, Fuller and Metges, 2010). On other hand, in

case of Tesco performance to some extent is satisfactory because its quick ratio value is 0.45.

However, its quick ratio also declined but by only some points which is not big matter of

concern. Tesco is in better position in terms of payment of current liability using quick assets on

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

time. However, it can only pay 50% of its liability by using current assets. It can be said that

Tesco perform better then Sainsbury.

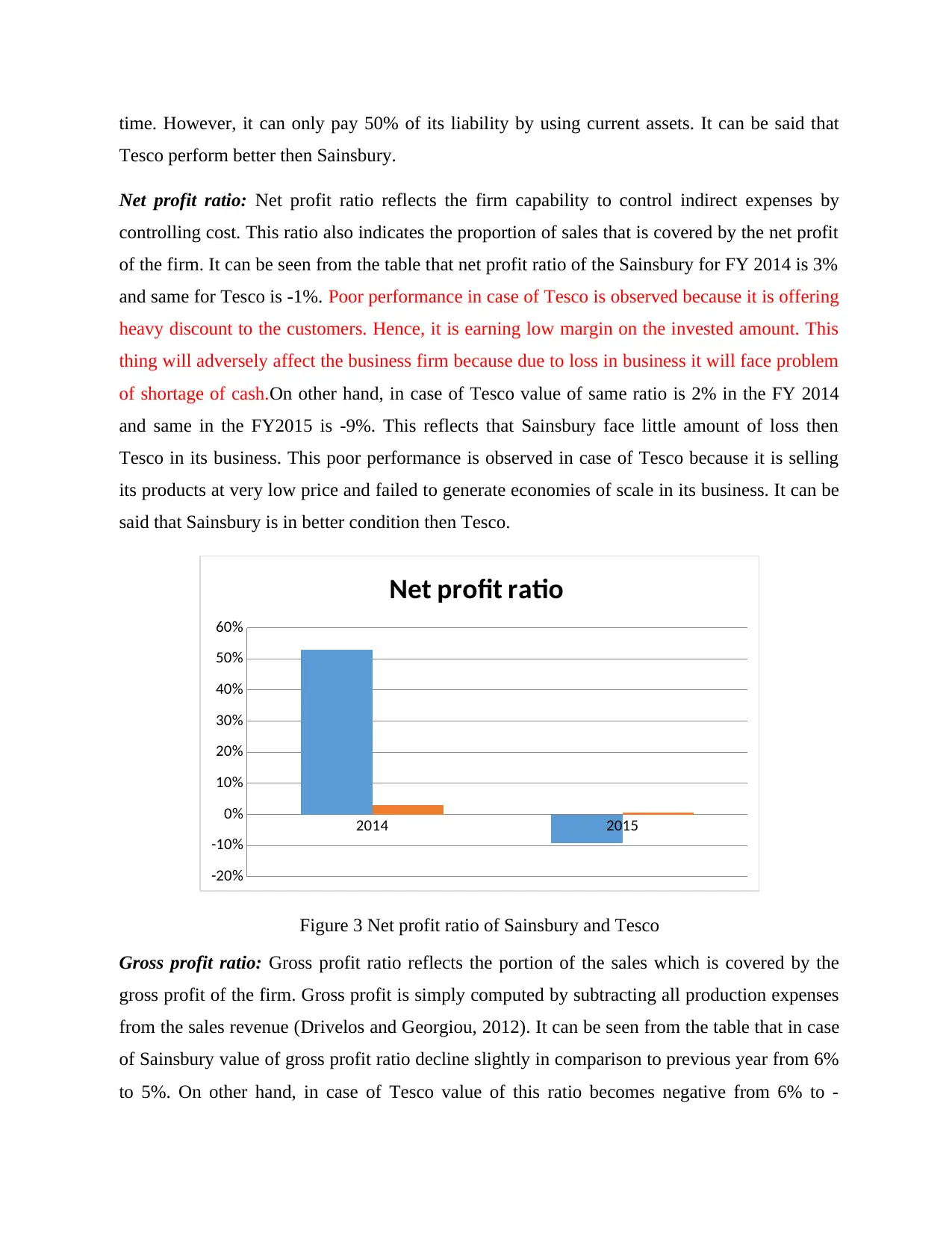

Net profit ratio: Net profit ratio reflects the firm capability to control indirect expenses by

controlling cost. This ratio also indicates the proportion of sales that is covered by the net profit

of the firm. It can be seen from the table that net profit ratio of the Sainsbury for FY 2014 is 3%

and same for Tesco is -1%. Poor performance in case of Tesco is observed because it is offering

heavy discount to the customers. Hence, it is earning low margin on the invested amount. This

thing will adversely affect the business firm because due to loss in business it will face problem

of shortage of cash.On other hand, in case of Tesco value of same ratio is 2% in the FY 2014

and same in the FY2015 is -9%. This reflects that Sainsbury face little amount of loss then

Tesco in its business. This poor performance is observed in case of Tesco because it is selling

its products at very low price and failed to generate economies of scale in its business. It can be

said that Sainsbury is in better condition then Tesco.

2014 2015

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

Net profit ratio

Figure 3 Net profit ratio of Sainsbury and Tesco

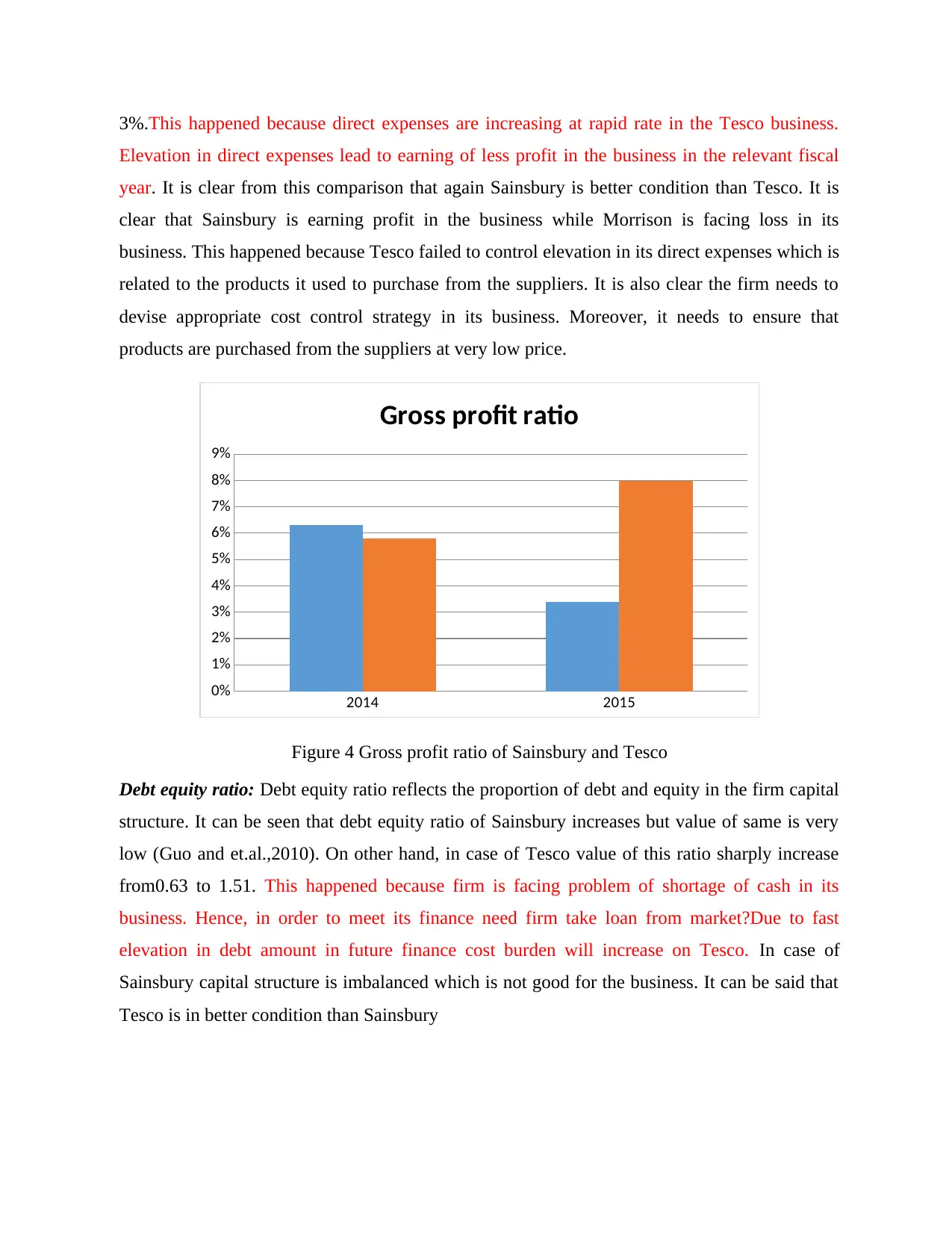

Gross profit ratio: Gross profit ratio reflects the portion of the sales which is covered by the

gross profit of the firm. Gross profit is simply computed by subtracting all production expenses

from the sales revenue (Drivelos and Georgiou, 2012). It can be seen from the table that in case

of Sainsbury value of gross profit ratio decline slightly in comparison to previous year from 6%

to 5%. On other hand, in case of Tesco value of this ratio becomes negative from 6% to -

Tesco perform better then Sainsbury.

Net profit ratio: Net profit ratio reflects the firm capability to control indirect expenses by

controlling cost. This ratio also indicates the proportion of sales that is covered by the net profit

of the firm. It can be seen from the table that net profit ratio of the Sainsbury for FY 2014 is 3%

and same for Tesco is -1%. Poor performance in case of Tesco is observed because it is offering

heavy discount to the customers. Hence, it is earning low margin on the invested amount. This

thing will adversely affect the business firm because due to loss in business it will face problem

of shortage of cash.On other hand, in case of Tesco value of same ratio is 2% in the FY 2014

and same in the FY2015 is -9%. This reflects that Sainsbury face little amount of loss then

Tesco in its business. This poor performance is observed in case of Tesco because it is selling

its products at very low price and failed to generate economies of scale in its business. It can be

said that Sainsbury is in better condition then Tesco.

2014 2015

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

Net profit ratio

Figure 3 Net profit ratio of Sainsbury and Tesco

Gross profit ratio: Gross profit ratio reflects the portion of the sales which is covered by the

gross profit of the firm. Gross profit is simply computed by subtracting all production expenses

from the sales revenue (Drivelos and Georgiou, 2012). It can be seen from the table that in case

of Sainsbury value of gross profit ratio decline slightly in comparison to previous year from 6%

to 5%. On other hand, in case of Tesco value of this ratio becomes negative from 6% to -

3%.This happened because direct expenses are increasing at rapid rate in the Tesco business.

Elevation in direct expenses lead to earning of less profit in the business in the relevant fiscal

year. It is clear from this comparison that again Sainsbury is better condition than Tesco. It is

clear that Sainsbury is earning profit in the business while Morrison is facing loss in its

business. This happened because Tesco failed to control elevation in its direct expenses which is

related to the products it used to purchase from the suppliers. It is also clear the firm needs to

devise appropriate cost control strategy in its business. Moreover, it needs to ensure that

products are purchased from the suppliers at very low price.

2014 2015

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

Gross profit ratio

Figure 4 Gross profit ratio of Sainsbury and Tesco

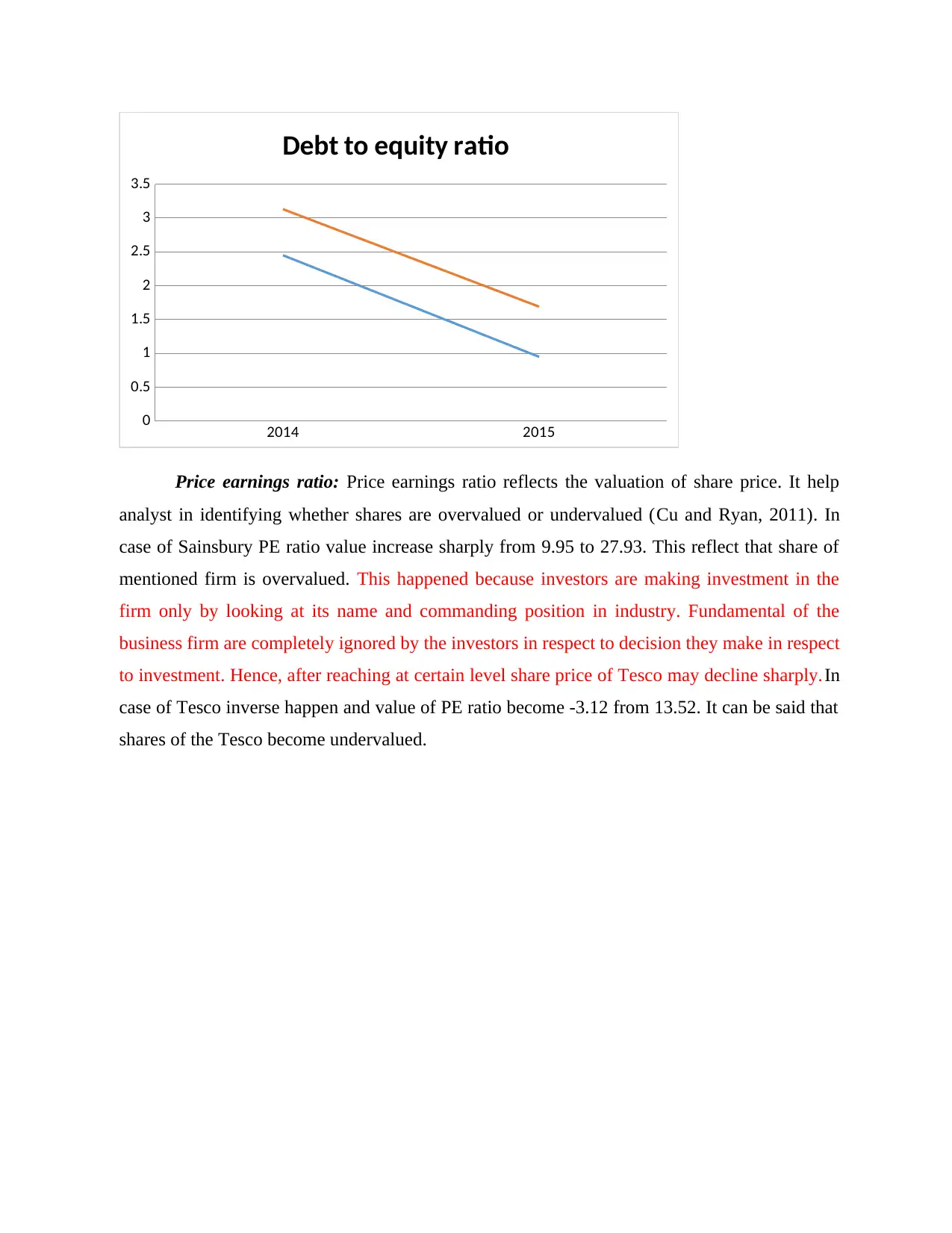

Debt equity ratio: Debt equity ratio reflects the proportion of debt and equity in the firm capital

structure. It can be seen that debt equity ratio of Sainsbury increases but value of same is very

low (Guo and et.al.,2010). On other hand, in case of Tesco value of this ratio sharply increase

from0.63 to 1.51. This happened because firm is facing problem of shortage of cash in its

business. Hence, in order to meet its finance need firm take loan from market?Due to fast

elevation in debt amount in future finance cost burden will increase on Tesco. In case of

Sainsbury capital structure is imbalanced which is not good for the business. It can be said that

Tesco is in better condition than Sainsbury

Elevation in direct expenses lead to earning of less profit in the business in the relevant fiscal

year. It is clear from this comparison that again Sainsbury is better condition than Tesco. It is

clear that Sainsbury is earning profit in the business while Morrison is facing loss in its

business. This happened because Tesco failed to control elevation in its direct expenses which is

related to the products it used to purchase from the suppliers. It is also clear the firm needs to

devise appropriate cost control strategy in its business. Moreover, it needs to ensure that

products are purchased from the suppliers at very low price.

2014 2015

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

Gross profit ratio

Figure 4 Gross profit ratio of Sainsbury and Tesco

Debt equity ratio: Debt equity ratio reflects the proportion of debt and equity in the firm capital

structure. It can be seen that debt equity ratio of Sainsbury increases but value of same is very

low (Guo and et.al.,2010). On other hand, in case of Tesco value of this ratio sharply increase

from0.63 to 1.51. This happened because firm is facing problem of shortage of cash in its

business. Hence, in order to meet its finance need firm take loan from market?Due to fast

elevation in debt amount in future finance cost burden will increase on Tesco. In case of

Sainsbury capital structure is imbalanced which is not good for the business. It can be said that

Tesco is in better condition than Sainsbury

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2014 2015

0

0.5

1

1.5

2

2.5

3

3.5

Debt to equity ratio

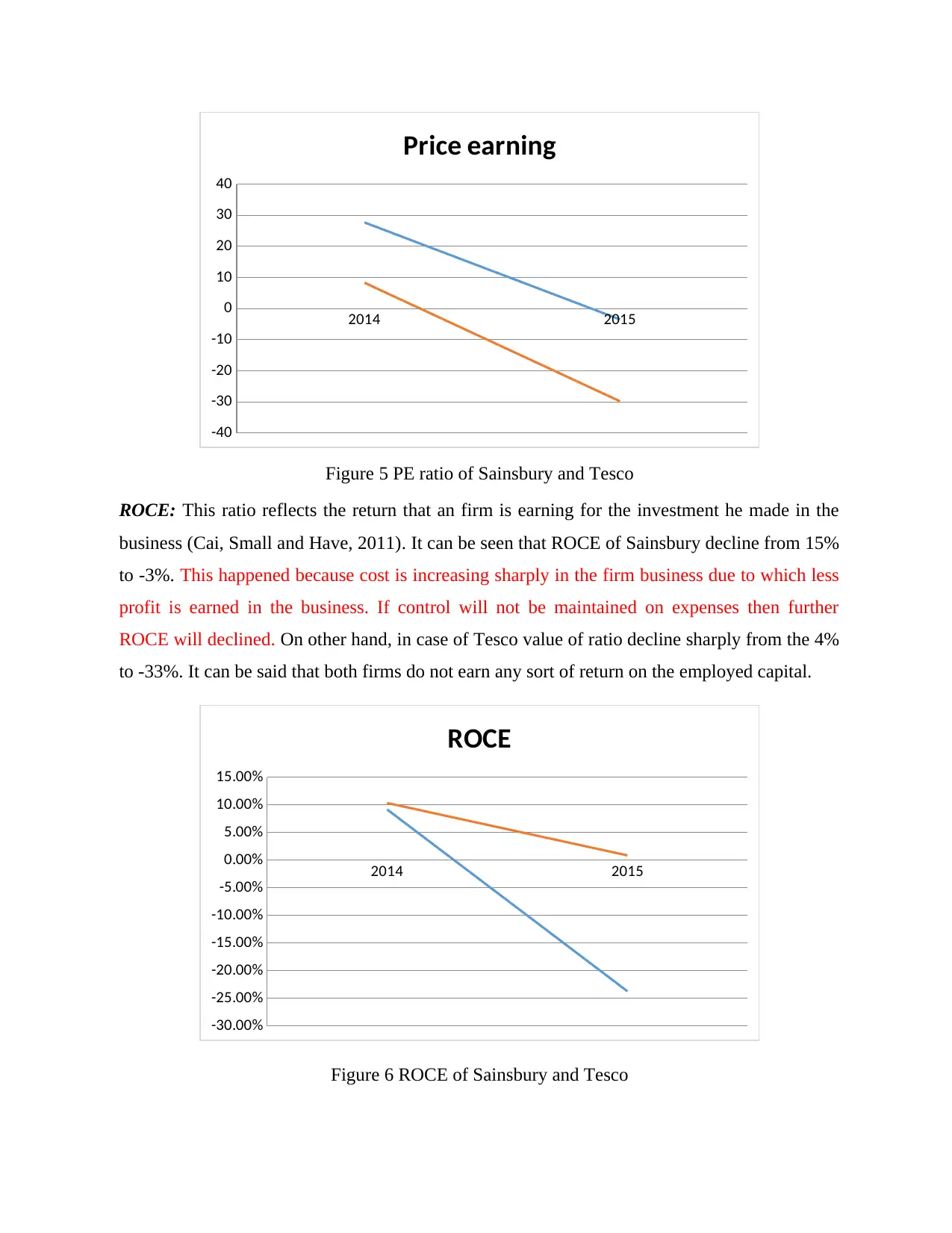

Price earnings ratio: Price earnings ratio reflects the valuation of share price. It help

analyst in identifying whether shares are overvalued or undervalued (Cu and Ryan, 2011). In

case of Sainsbury PE ratio value increase sharply from 9.95 to 27.93. This reflect that share of

mentioned firm is overvalued. This happened because investors are making investment in the

firm only by looking at its name and commanding position in industry. Fundamental of the

business firm are completely ignored by the investors in respect to decision they make in respect

to investment. Hence, after reaching at certain level share price of Tesco may decline sharply.In

case of Tesco inverse happen and value of PE ratio become -3.12 from 13.52. It can be said that

shares of the Tesco become undervalued.

0

0.5

1

1.5

2

2.5

3

3.5

Debt to equity ratio

Price earnings ratio: Price earnings ratio reflects the valuation of share price. It help

analyst in identifying whether shares are overvalued or undervalued (Cu and Ryan, 2011). In

case of Sainsbury PE ratio value increase sharply from 9.95 to 27.93. This reflect that share of

mentioned firm is overvalued. This happened because investors are making investment in the

firm only by looking at its name and commanding position in industry. Fundamental of the

business firm are completely ignored by the investors in respect to decision they make in respect

to investment. Hence, after reaching at certain level share price of Tesco may decline sharply.In

case of Tesco inverse happen and value of PE ratio become -3.12 from 13.52. It can be said that

shares of the Tesco become undervalued.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2014 2015

-40

-30

-20

-10

0

10

20

30

40

Price earning

Figure 5 PE ratio of Sainsbury and Tesco

ROCE: This ratio reflects the return that an firm is earning for the investment he made in the

business (Cai, Small and Have, 2011). It can be seen that ROCE of Sainsbury decline from 15%

to -3%. This happened because cost is increasing sharply in the firm business due to which less

profit is earned in the business. If control will not be maintained on expenses then further

ROCE will declined. On other hand, in case of Tesco value of ratio decline sharply from the 4%

to -33%. It can be said that both firms do not earn any sort of return on the employed capital.

2014 2015

-30.00%

-25.00%

-20.00%

-15.00%

-10.00%

-5.00%

0.00%

5.00%

10.00%

15.00%

ROCE

Figure 6 ROCE of Sainsbury and Tesco

-40

-30

-20

-10

0

10

20

30

40

Price earning

Figure 5 PE ratio of Sainsbury and Tesco

ROCE: This ratio reflects the return that an firm is earning for the investment he made in the

business (Cai, Small and Have, 2011). It can be seen that ROCE of Sainsbury decline from 15%

to -3%. This happened because cost is increasing sharply in the firm business due to which less

profit is earned in the business. If control will not be maintained on expenses then further

ROCE will declined. On other hand, in case of Tesco value of ratio decline sharply from the 4%

to -33%. It can be said that both firms do not earn any sort of return on the employed capital.

2014 2015

-30.00%

-25.00%

-20.00%

-15.00%

-10.00%

-5.00%

0.00%

5.00%

10.00%

15.00%

ROCE

Figure 6 ROCE of Sainsbury and Tesco

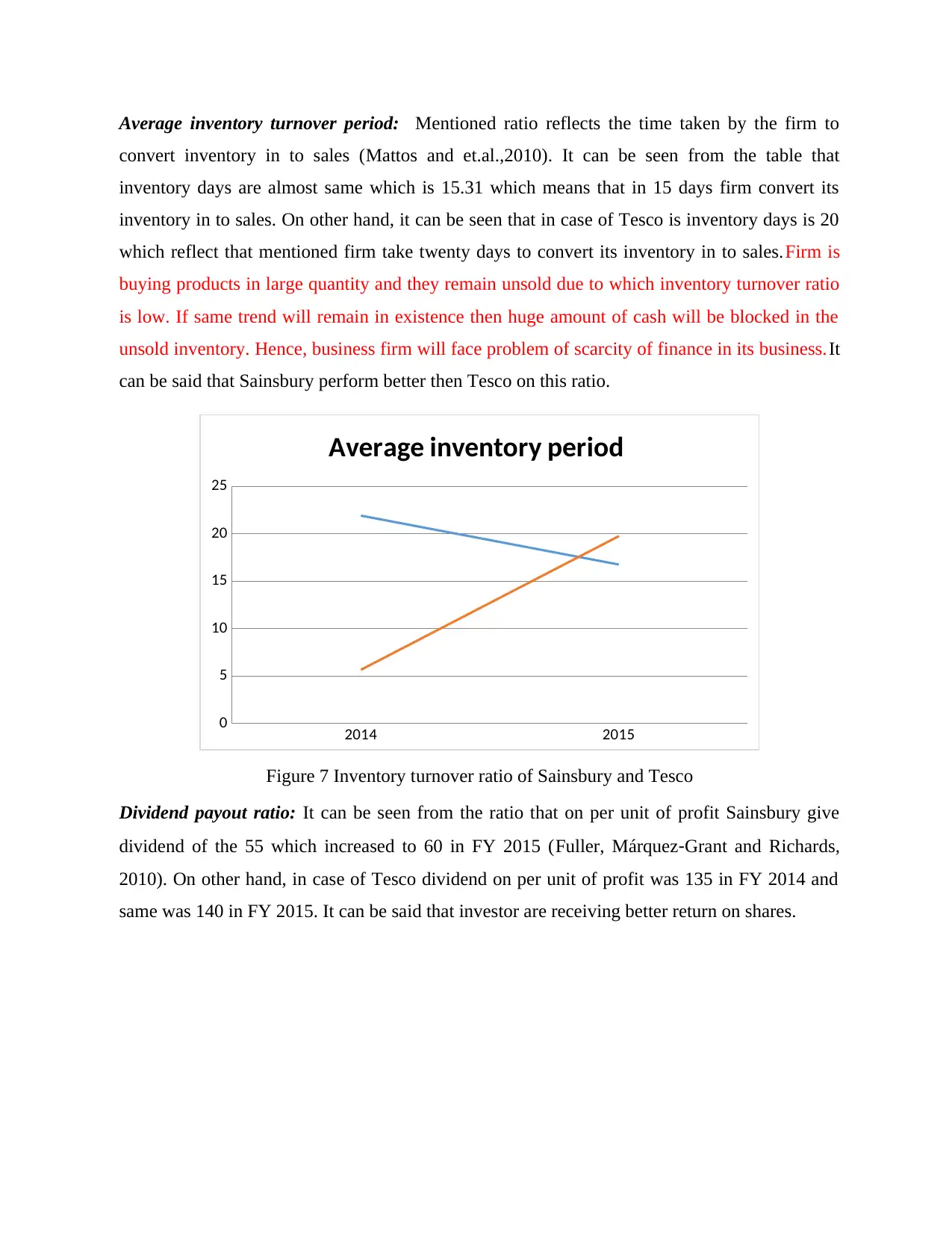

Average inventory turnover period: Mentioned ratio reflects the time taken by the firm to

convert inventory in to sales (Mattos and et.al.,2010). It can be seen from the table that

inventory days are almost same which is 15.31 which means that in 15 days firm convert its

inventory in to sales. On other hand, it can be seen that in case of Tesco is inventory days is 20

which reflect that mentioned firm take twenty days to convert its inventory in to sales.Firm is

buying products in large quantity and they remain unsold due to which inventory turnover ratio

is low. If same trend will remain in existence then huge amount of cash will be blocked in the

unsold inventory. Hence, business firm will face problem of scarcity of finance in its business.It

can be said that Sainsbury perform better then Tesco on this ratio.

2014 2015

0

5

10

15

20

25

Average inventory period

Figure 7 Inventory turnover ratio of Sainsbury and Tesco

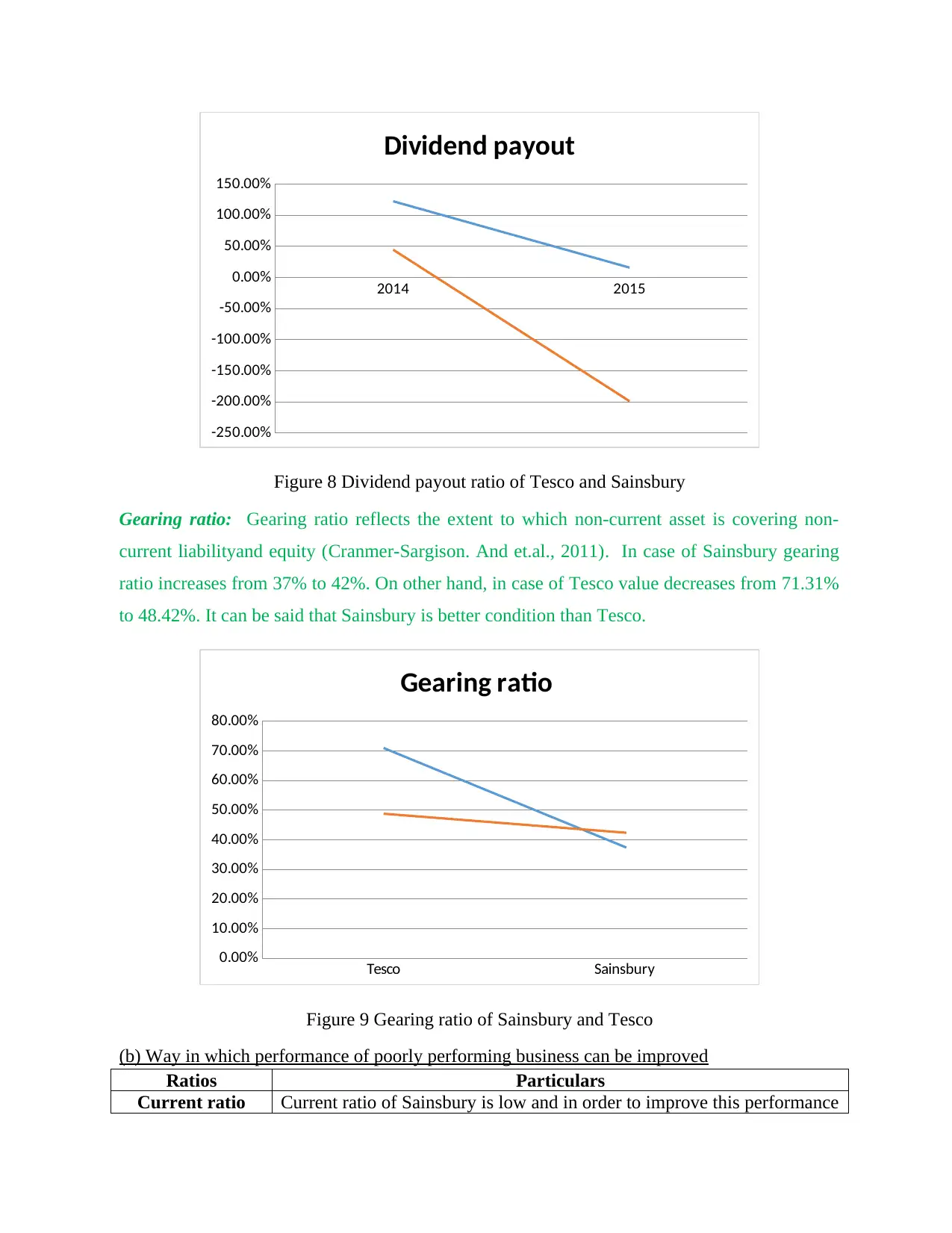

Dividend payout ratio: It can be seen from the ratio that on per unit of profit Sainsbury give

dividend of the 55 which increased to 60 in FY 2015 (Fuller, Márquez‐Grant and Richards,

2010). On other hand, in case of Tesco dividend on per unit of profit was 135 in FY 2014 and

same was 140 in FY 2015. It can be said that investor are receiving better return on shares.

convert inventory in to sales (Mattos and et.al.,2010). It can be seen from the table that

inventory days are almost same which is 15.31 which means that in 15 days firm convert its

inventory in to sales. On other hand, it can be seen that in case of Tesco is inventory days is 20

which reflect that mentioned firm take twenty days to convert its inventory in to sales.Firm is

buying products in large quantity and they remain unsold due to which inventory turnover ratio

is low. If same trend will remain in existence then huge amount of cash will be blocked in the

unsold inventory. Hence, business firm will face problem of scarcity of finance in its business.It

can be said that Sainsbury perform better then Tesco on this ratio.

2014 2015

0

5

10

15

20

25

Average inventory period

Figure 7 Inventory turnover ratio of Sainsbury and Tesco

Dividend payout ratio: It can be seen from the ratio that on per unit of profit Sainsbury give

dividend of the 55 which increased to 60 in FY 2015 (Fuller, Márquez‐Grant and Richards,

2010). On other hand, in case of Tesco dividend on per unit of profit was 135 in FY 2014 and

same was 140 in FY 2015. It can be said that investor are receiving better return on shares.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2014 2015

-250.00%

-200.00%

-150.00%

-100.00%

-50.00%

0.00%

50.00%

100.00%

150.00%

Dividend payout

Figure 8 Dividend payout ratio of Tesco and Sainsbury

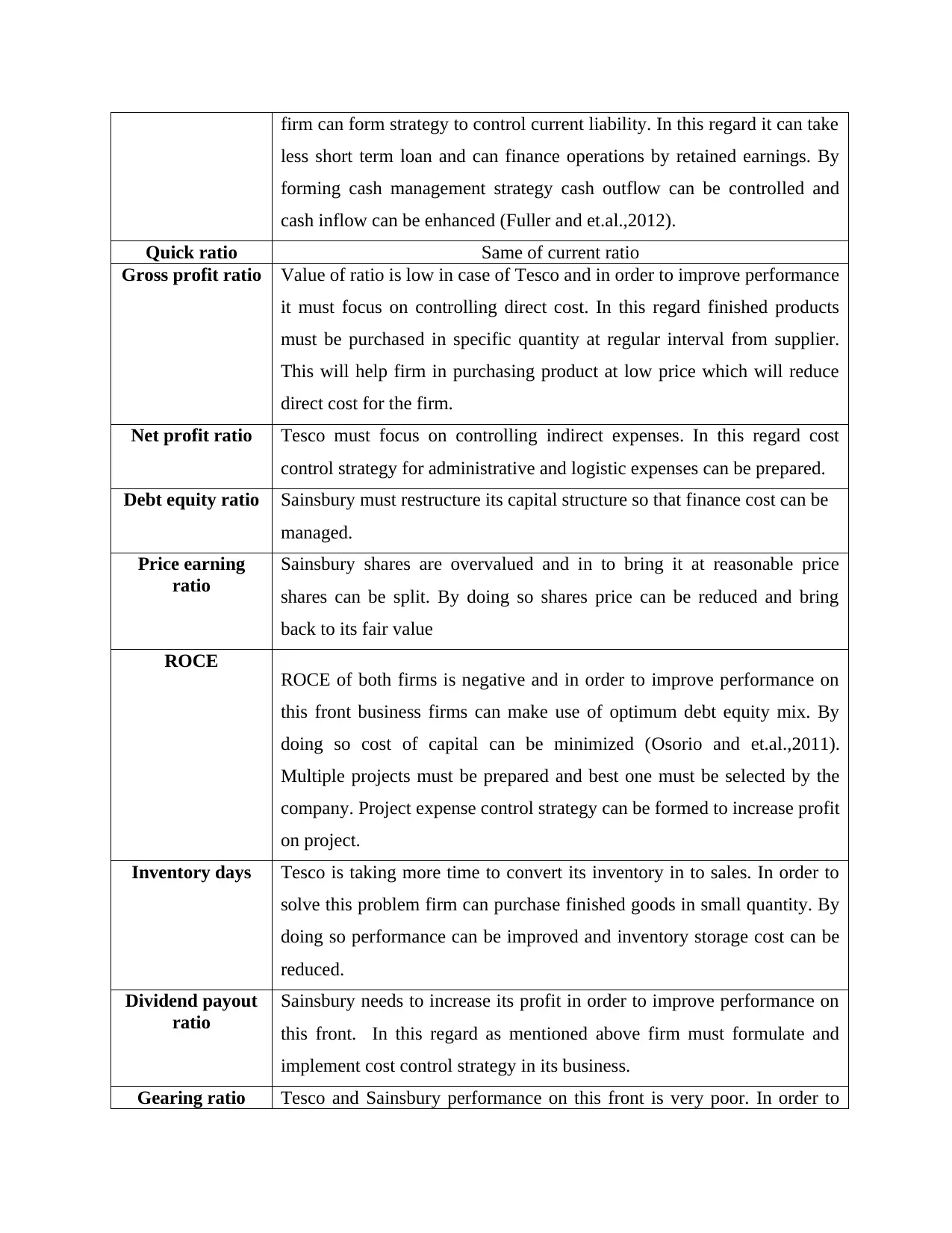

Gearing ratio: Gearing ratio reflects the extent to which non-current asset is covering non-

current liabilityand equity (Cranmer-Sargison. And et.al., 2011). In case of Sainsbury gearing

ratio increases from 37% to 42%. On other hand, in case of Tesco value decreases from 71.31%

to 48.42%. It can be said that Sainsbury is better condition than Tesco.

Tesco Sainsbury

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

70.00%

80.00%

Gearing ratio

Figure 9 Gearing ratio of Sainsbury and Tesco

(b) Way in which performance of poorly performing business can be improved

Ratios Particulars

Current ratio Current ratio of Sainsbury is low and in order to improve this performance

-250.00%

-200.00%

-150.00%

-100.00%

-50.00%

0.00%

50.00%

100.00%

150.00%

Dividend payout

Figure 8 Dividend payout ratio of Tesco and Sainsbury

Gearing ratio: Gearing ratio reflects the extent to which non-current asset is covering non-

current liabilityand equity (Cranmer-Sargison. And et.al., 2011). In case of Sainsbury gearing

ratio increases from 37% to 42%. On other hand, in case of Tesco value decreases from 71.31%

to 48.42%. It can be said that Sainsbury is better condition than Tesco.

Tesco Sainsbury

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

70.00%

80.00%

Gearing ratio

Figure 9 Gearing ratio of Sainsbury and Tesco

(b) Way in which performance of poorly performing business can be improved

Ratios Particulars

Current ratio Current ratio of Sainsbury is low and in order to improve this performance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

firm can form strategy to control current liability. In this regard it can take

less short term loan and can finance operations by retained earnings. By

forming cash management strategy cash outflow can be controlled and

cash inflow can be enhanced (Fuller and et.al.,2012).

Quick ratio Same of current ratio

Gross profit ratio Value of ratio is low in case of Tesco and in order to improve performance

it must focus on controlling direct cost. In this regard finished products

must be purchased in specific quantity at regular interval from supplier.

This will help firm in purchasing product at low price which will reduce

direct cost for the firm.

Net profit ratio Tesco must focus on controlling indirect expenses. In this regard cost

control strategy for administrative and logistic expenses can be prepared.

Debt equity ratio Sainsbury must restructure its capital structure so that finance cost can be

managed.

Price earning

ratio

Sainsbury shares are overvalued and in to bring it at reasonable price

shares can be split. By doing so shares price can be reduced and bring

back to its fair value

ROCE ROCE of both firms is negative and in order to improve performance on

this front business firms can make use of optimum debt equity mix. By

doing so cost of capital can be minimized (Osorio and et.al.,2011).

Multiple projects must be prepared and best one must be selected by the

company. Project expense control strategy can be formed to increase profit

on project.

Inventory days Tesco is taking more time to convert its inventory in to sales. In order to

solve this problem firm can purchase finished goods in small quantity. By

doing so performance can be improved and inventory storage cost can be

reduced.

Dividend payout

ratio

Sainsbury needs to increase its profit in order to improve performance on

this front. In this regard as mentioned above firm must formulate and

implement cost control strategy in its business.

Gearing ratio Tesco and Sainsbury performance on this front is very poor. In order to

less short term loan and can finance operations by retained earnings. By

forming cash management strategy cash outflow can be controlled and

cash inflow can be enhanced (Fuller and et.al.,2012).

Quick ratio Same of current ratio

Gross profit ratio Value of ratio is low in case of Tesco and in order to improve performance

it must focus on controlling direct cost. In this regard finished products

must be purchased in specific quantity at regular interval from supplier.

This will help firm in purchasing product at low price which will reduce

direct cost for the firm.

Net profit ratio Tesco must focus on controlling indirect expenses. In this regard cost

control strategy for administrative and logistic expenses can be prepared.

Debt equity ratio Sainsbury must restructure its capital structure so that finance cost can be

managed.

Price earning

ratio

Sainsbury shares are overvalued and in to bring it at reasonable price

shares can be split. By doing so shares price can be reduced and bring

back to its fair value

ROCE ROCE of both firms is negative and in order to improve performance on

this front business firms can make use of optimum debt equity mix. By

doing so cost of capital can be minimized (Osorio and et.al.,2011).

Multiple projects must be prepared and best one must be selected by the

company. Project expense control strategy can be formed to increase profit

on project.

Inventory days Tesco is taking more time to convert its inventory in to sales. In order to

solve this problem firm can purchase finished goods in small quantity. By

doing so performance can be improved and inventory storage cost can be

reduced.

Dividend payout

ratio

Sainsbury needs to increase its profit in order to improve performance on

this front. In this regard as mentioned above firm must formulate and

implement cost control strategy in its business.

Gearing ratio Tesco and Sainsbury performance on this front is very poor. In order to

improve performance on this front firm must try to reduce its finance cost.

Cost control strategy must be formulated in order to increase EBIT in the

business.

© Limitation of relying on ratios to measure firm performance

There is very big limitation of relying on ratios to measure firm financial performance.

For current ratio standard value is 2:1 which means that for every one unit of current liability

there must be two units of the current asset. When economy is in recession it is not possible to

maintain this standard (Mattos and et.al.,2010). This is because at that time cash outflow takes

place at rapid pace and cash inflow happen in the business at low rate. But whenever manager

will measure firm performance he will use standard value 2:1 in order to find out whether firm

liquidity position is good or bad. Same thing applied on other ratios. It can be said that one

cannot rely entirely on the ratios to measure firm performance.The other limitations of ratio

analysis method is that ratios are based on historical figures. It is not necessary that past will

repeat in future. Hence, results generated by ratios are not highly reliable. Ratio analysis

formula does not consider inflation. Hence, accurate performance of the firm cannot be

measured by using ratio analysis. Ratios results can be manipulated easily. Hence, due to this

reason results of ratios are not highly reliable.

Portfolio 2

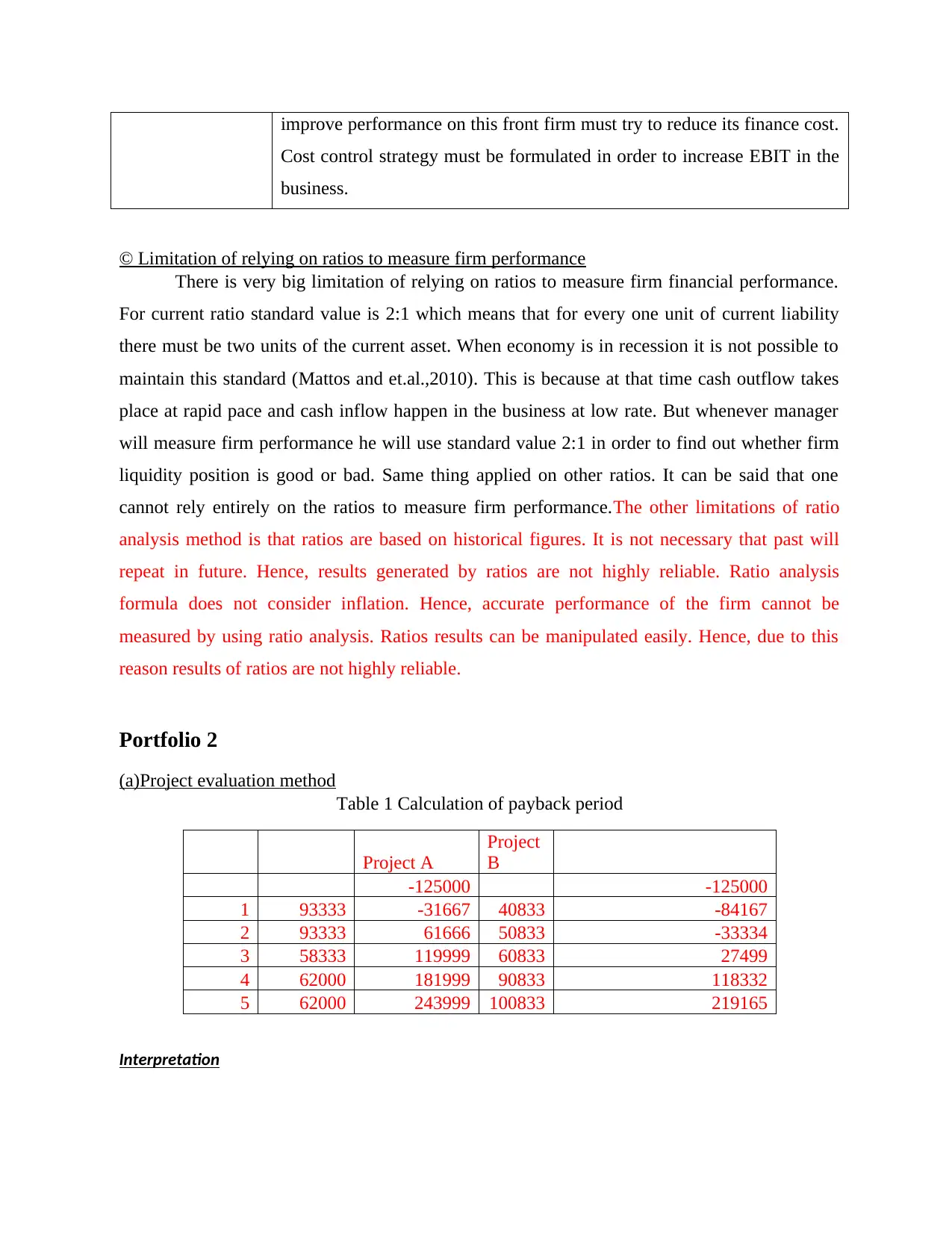

(a)Project evaluation method

Table 1 Calculation of payback period

Project A

Project

B

-125000 -125000

1 93333 -31667 40833 -84167

2 93333 61666 50833 -33334

3 58333 119999 60833 27499

4 62000 181999 90833 118332

5 62000 243999 100833 219165

Interpretation

Cost control strategy must be formulated in order to increase EBIT in the

business.

© Limitation of relying on ratios to measure firm performance

There is very big limitation of relying on ratios to measure firm financial performance.

For current ratio standard value is 2:1 which means that for every one unit of current liability

there must be two units of the current asset. When economy is in recession it is not possible to

maintain this standard (Mattos and et.al.,2010). This is because at that time cash outflow takes

place at rapid pace and cash inflow happen in the business at low rate. But whenever manager

will measure firm performance he will use standard value 2:1 in order to find out whether firm

liquidity position is good or bad. Same thing applied on other ratios. It can be said that one

cannot rely entirely on the ratios to measure firm performance.The other limitations of ratio

analysis method is that ratios are based on historical figures. It is not necessary that past will

repeat in future. Hence, results generated by ratios are not highly reliable. Ratio analysis

formula does not consider inflation. Hence, accurate performance of the firm cannot be

measured by using ratio analysis. Ratios results can be manipulated easily. Hence, due to this

reason results of ratios are not highly reliable.

Portfolio 2

(a)Project evaluation method

Table 1 Calculation of payback period

Project A

Project

B

-125000 -125000

1 93333 -31667 40833 -84167

2 93333 61666 50833 -33334

3 58333 119999 60833 27499

4 62000 181999 90833 118332

5 62000 243999 100833 219165

Interpretation

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.