Managerial Finance Report: Analysis of Coach Inc. Financial Statements

VerifiedAdded on 2020/11/12

|10

|3094

|263

Report

AI Summary

This report provides a comprehensive financial analysis of Coach Inc., covering the months of September and October. It begins with an introduction to managerial finance and its significance in making financial judgments. The main body of the report includes a detailed profit and loss account, a balance sheet, and a cash budget, along with their interpretations. The cash budget projects cash inflows and outflows, determining the end-of-month cash balance. The report also includes a cash flow statement and a report for the managing director analyzing customer terms, specifically comparing 30-day and 60-day credit periods. Recommendations are made to reduce the debtors' policy from 60 days to 30 days. Overall, the report aims to evaluate Coach Inc.'s financial position and provide insights for improved financial management.

MANAGERIAL

FINANCE

FINANCE

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

Profit And Loss Account.............................................................................................................1

Balance Sheet..............................................................................................................................2

Cash Budget................................................................................................................................3

Cash Flow....................................................................................................................................5

Report for managing director .....................................................................................................6

CONCLUSION ...............................................................................................................................7

REFERENCES................................................................................................................................8

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

Profit And Loss Account.............................................................................................................1

Balance Sheet..............................................................................................................................2

Cash Budget................................................................................................................................3

Cash Flow....................................................................................................................................5

Report for managing director .....................................................................................................6

CONCLUSION ...............................................................................................................................7

REFERENCES................................................................................................................................8

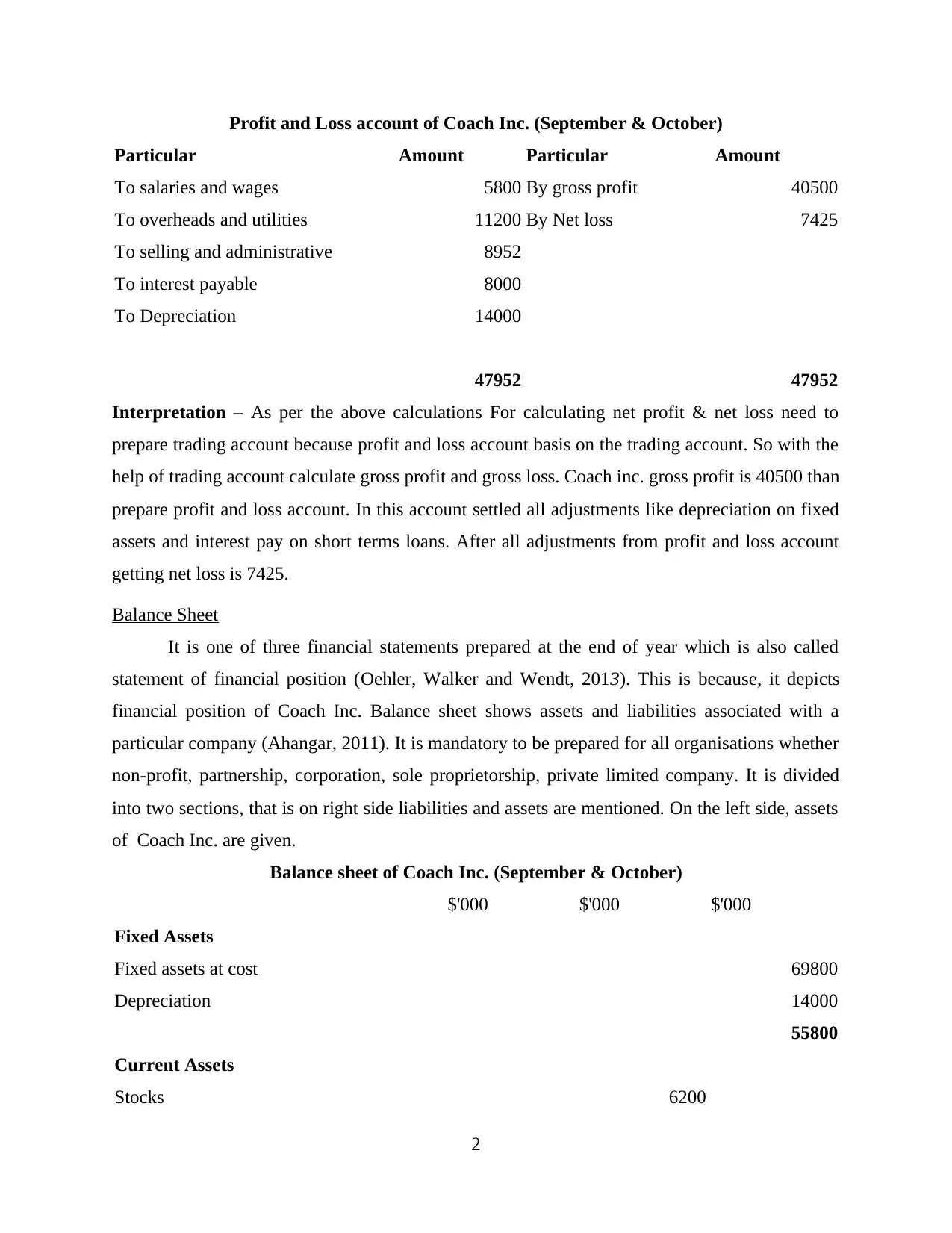

INTRODUCTION

The term Managerial Finance as is apparent from its meaning is used for taking financial

judgement which have managerial implication. A manager will rather be curious what the

financial calculations or figures mean. It is the branch of finance that concerns itself with the

managerial significance of finance techniques (Alhassan, 2015). It is focused on assessment

rather than technique. This report covers that preparing Financial statements of coach Inc. of two

months of September and October such as forecast profit and loss account, forecast balance

sheet, Prepare cash budget for cash balance in the end of the month for determining the phasing

of the cash budget for result, also prepare month end cash flow for cash balance September to

February 2019. Draft a report for managing director to analysis customer terms 30 days or 60

days.

MAIN BODY

Profit And Loss Account

Profit and loss statement or Income statement is a detailed statement showing revenues,

expenses, costs in summarized form prepared for a particular period of time. It is a part of

financial statements and prepared at the end of financial year (Kopparthi and Kagabo, 2013 ).

Net profit of Coach Inc. is calculated with the help of this record. It shows ability of profit

generation through improving revenue or cost reduction. Complexity of preparing P&L increases

with increase in size of organization. P&L is provided to comply with law (Nguyen and

Nghiem, 2015). Components of it are cost of sales, revenue, closing stock, opening stock. From

these, gross profit is determined in first section. Then, operating expenses are reduced from gross

profit to arrive at operating profit. After that, non-operating revenues as well as expenses are

taken into account to ascertain net revenue.

Trading Account of Coach Inc. (September & October)

Particular Amount Particular Amount

To Opening balance 18000 By sales 69500

To Purchase 17200 By closing stock 6200

To Gross Profit 40500

Total 75700 Total 75700

1

The term Managerial Finance as is apparent from its meaning is used for taking financial

judgement which have managerial implication. A manager will rather be curious what the

financial calculations or figures mean. It is the branch of finance that concerns itself with the

managerial significance of finance techniques (Alhassan, 2015). It is focused on assessment

rather than technique. This report covers that preparing Financial statements of coach Inc. of two

months of September and October such as forecast profit and loss account, forecast balance

sheet, Prepare cash budget for cash balance in the end of the month for determining the phasing

of the cash budget for result, also prepare month end cash flow for cash balance September to

February 2019. Draft a report for managing director to analysis customer terms 30 days or 60

days.

MAIN BODY

Profit And Loss Account

Profit and loss statement or Income statement is a detailed statement showing revenues,

expenses, costs in summarized form prepared for a particular period of time. It is a part of

financial statements and prepared at the end of financial year (Kopparthi and Kagabo, 2013 ).

Net profit of Coach Inc. is calculated with the help of this record. It shows ability of profit

generation through improving revenue or cost reduction. Complexity of preparing P&L increases

with increase in size of organization. P&L is provided to comply with law (Nguyen and

Nghiem, 2015). Components of it are cost of sales, revenue, closing stock, opening stock. From

these, gross profit is determined in first section. Then, operating expenses are reduced from gross

profit to arrive at operating profit. After that, non-operating revenues as well as expenses are

taken into account to ascertain net revenue.

Trading Account of Coach Inc. (September & October)

Particular Amount Particular Amount

To Opening balance 18000 By sales 69500

To Purchase 17200 By closing stock 6200

To Gross Profit 40500

Total 75700 Total 75700

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Profit and Loss account of Coach Inc. (September & October)

Particular Amount Particular Amount

To salaries and wages 5800 By gross profit 40500

To overheads and utilities 11200 By Net loss 7425

To selling and administrative 8952

To interest payable 8000

To Depreciation 14000

47952 47952

Interpretation – As per the above calculations For calculating net profit & net loss need to

prepare trading account because profit and loss account basis on the trading account. So with the

help of trading account calculate gross profit and gross loss. Coach inc. gross profit is 40500 than

prepare profit and loss account. In this account settled all adjustments like depreciation on fixed

assets and interest pay on short terms loans. After all adjustments from profit and loss account

getting net loss is 7425.

Balance Sheet

It is one of three financial statements prepared at the end of year which is also called

statement of financial position (Oehler, Walker and Wendt, 2013). This is because, it depicts

financial position of Coach Inc. Balance sheet shows assets and liabilities associated with a

particular company (Ahangar, 2011). It is mandatory to be prepared for all organisations whether

non-profit, partnership, corporation, sole proprietorship, private limited company. It is divided

into two sections, that is on right side liabilities and assets are mentioned. On the left side, assets

of Coach Inc. are given.

Balance sheet of Coach Inc. (September & October)

$'000 $'000 $'000

Fixed Assets

Fixed assets at cost 69800

Depreciation 14000

55800

Current Assets

Stocks 6200

2

Particular Amount Particular Amount

To salaries and wages 5800 By gross profit 40500

To overheads and utilities 11200 By Net loss 7425

To selling and administrative 8952

To interest payable 8000

To Depreciation 14000

47952 47952

Interpretation – As per the above calculations For calculating net profit & net loss need to

prepare trading account because profit and loss account basis on the trading account. So with the

help of trading account calculate gross profit and gross loss. Coach inc. gross profit is 40500 than

prepare profit and loss account. In this account settled all adjustments like depreciation on fixed

assets and interest pay on short terms loans. After all adjustments from profit and loss account

getting net loss is 7425.

Balance Sheet

It is one of three financial statements prepared at the end of year which is also called

statement of financial position (Oehler, Walker and Wendt, 2013). This is because, it depicts

financial position of Coach Inc. Balance sheet shows assets and liabilities associated with a

particular company (Ahangar, 2011). It is mandatory to be prepared for all organisations whether

non-profit, partnership, corporation, sole proprietorship, private limited company. It is divided

into two sections, that is on right side liabilities and assets are mentioned. On the left side, assets

of Coach Inc. are given.

Balance sheet of Coach Inc. (September & October)

$'000 $'000 $'000

Fixed Assets

Fixed assets at cost 69800

Depreciation 14000

55800

Current Assets

Stocks 6200

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

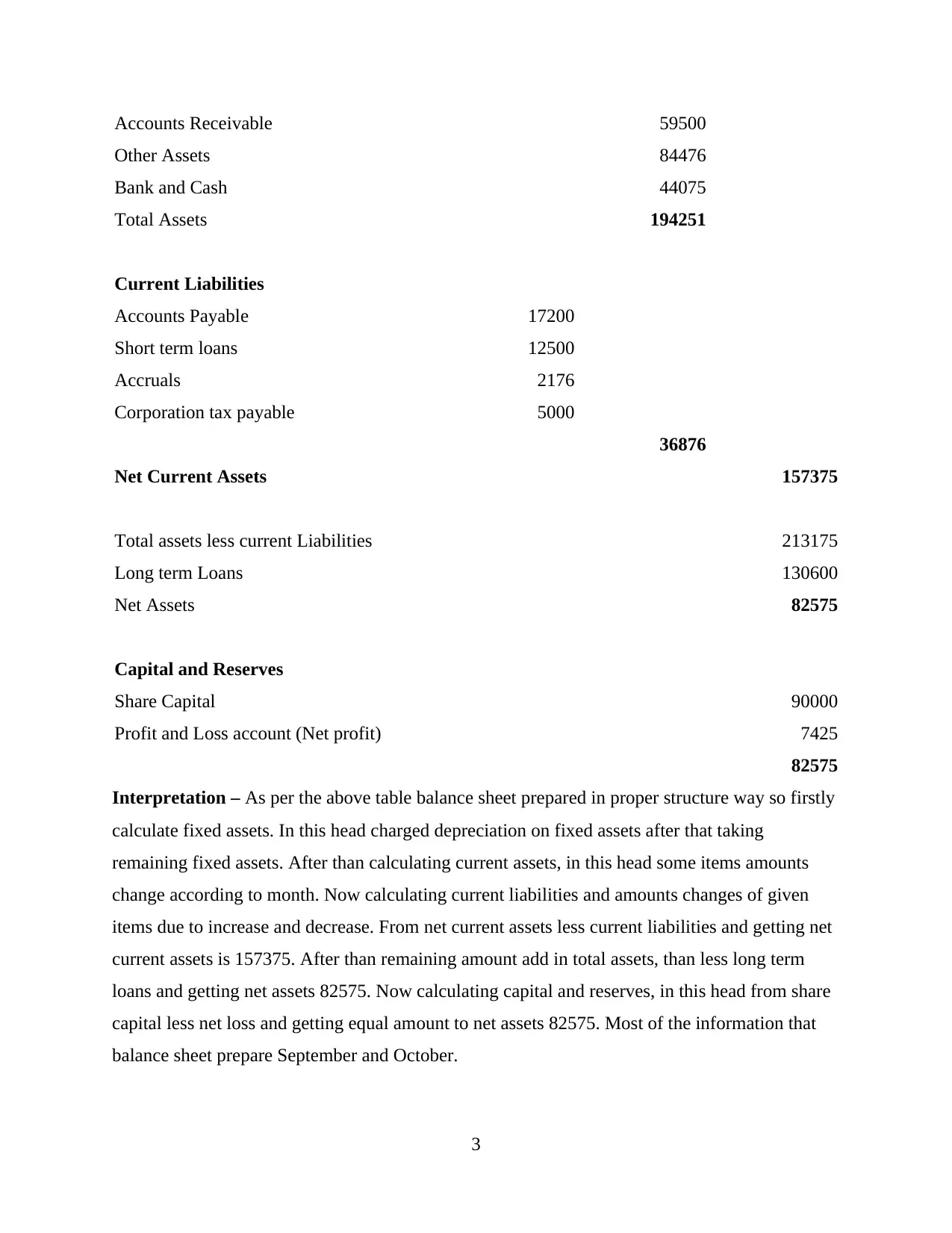

Accounts Receivable 59500

Other Assets 84476

Bank and Cash 44075

Total Assets 194251

Current Liabilities

Accounts Payable 17200

Short term loans 12500

Accruals 2176

Corporation tax payable 5000

36876

Net Current Assets 157375

Total assets less current Liabilities 213175

Long term Loans 130600

Net Assets 82575

Capital and Reserves

Share Capital 90000

Profit and Loss account (Net profit) 7425

82575

Interpretation – As per the above table balance sheet prepared in proper structure way so firstly

calculate fixed assets. In this head charged depreciation on fixed assets after that taking

remaining fixed assets. After than calculating current assets, in this head some items amounts

change according to month. Now calculating current liabilities and amounts changes of given

items due to increase and decrease. From net current assets less current liabilities and getting net

current assets is 157375. After than remaining amount add in total assets, than less long term

loans and getting net assets 82575. Now calculating capital and reserves, in this head from share

capital less net loss and getting equal amount to net assets 82575. Most of the information that

balance sheet prepare September and October.

3

Other Assets 84476

Bank and Cash 44075

Total Assets 194251

Current Liabilities

Accounts Payable 17200

Short term loans 12500

Accruals 2176

Corporation tax payable 5000

36876

Net Current Assets 157375

Total assets less current Liabilities 213175

Long term Loans 130600

Net Assets 82575

Capital and Reserves

Share Capital 90000

Profit and Loss account (Net profit) 7425

82575

Interpretation – As per the above table balance sheet prepared in proper structure way so firstly

calculate fixed assets. In this head charged depreciation on fixed assets after that taking

remaining fixed assets. After than calculating current assets, in this head some items amounts

change according to month. Now calculating current liabilities and amounts changes of given

items due to increase and decrease. From net current assets less current liabilities and getting net

current assets is 157375. After than remaining amount add in total assets, than less long term

loans and getting net assets 82575. Now calculating capital and reserves, in this head from share

capital less net loss and getting equal amount to net assets 82575. Most of the information that

balance sheet prepare September and October.

3

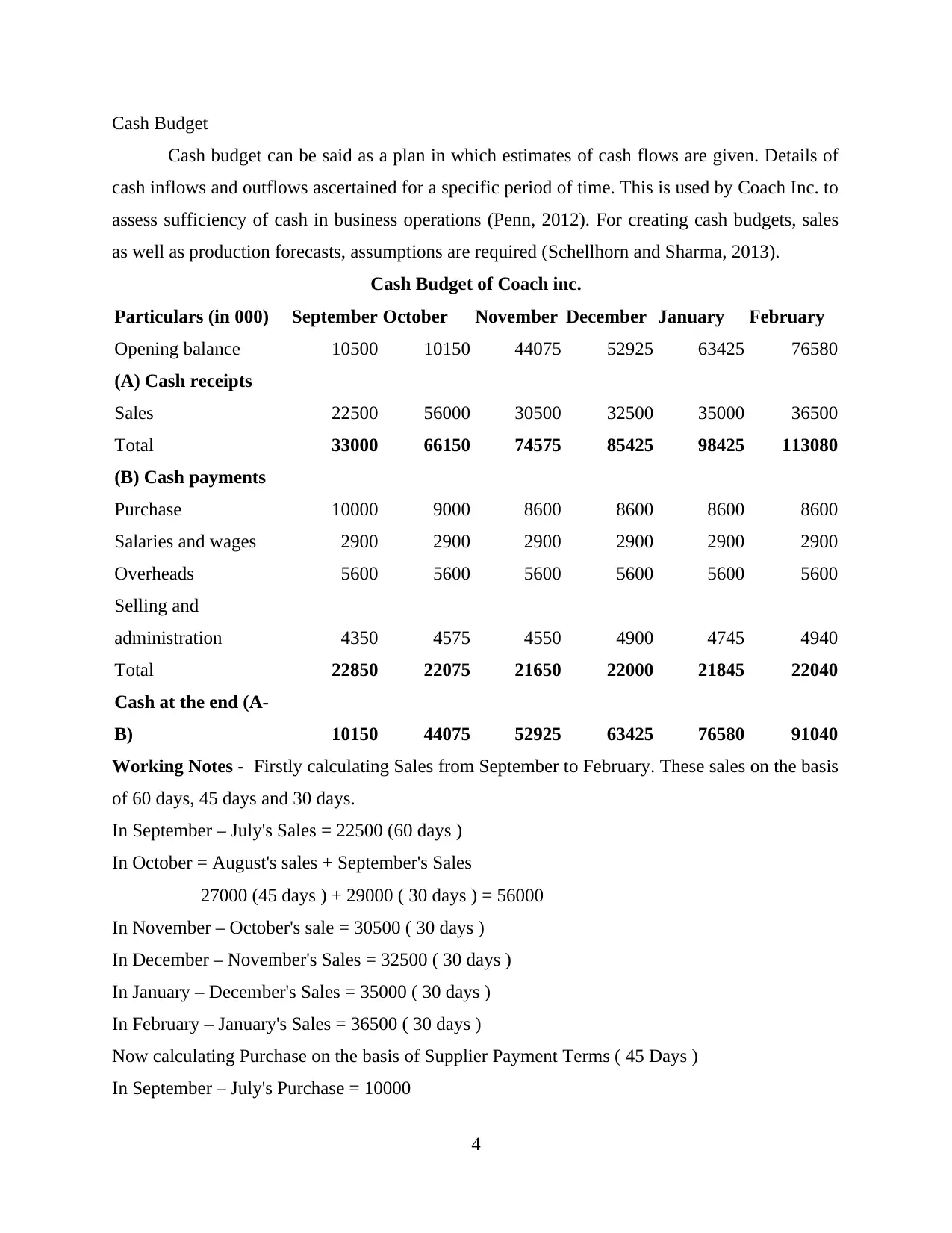

Cash Budget

Cash budget can be said as a plan in which estimates of cash flows are given. Details of

cash inflows and outflows ascertained for a specific period of time. This is used by Coach Inc. to

assess sufficiency of cash in business operations (Penn, 2012). For creating cash budgets, sales

as well as production forecasts, assumptions are required (Schellhorn and Sharma, 2013).

Cash Budget of Coach inc.

Particulars (in 000) September October November December January February

Opening balance 10500 10150 44075 52925 63425 76580

(A) Cash receipts

Sales 22500 56000 30500 32500 35000 36500

Total 33000 66150 74575 85425 98425 113080

(B) Cash payments

Purchase 10000 9000 8600 8600 8600 8600

Salaries and wages 2900 2900 2900 2900 2900 2900

Overheads 5600 5600 5600 5600 5600 5600

Selling and

administration 4350 4575 4550 4900 4745 4940

Total 22850 22075 21650 22000 21845 22040

Cash at the end (A-

B) 10150 44075 52925 63425 76580 91040

Working Notes - Firstly calculating Sales from September to February. These sales on the basis

of 60 days, 45 days and 30 days.

In September – July's Sales = 22500 (60 days )

In October = August's sales + September's Sales

27000 (45 days ) + 29000 ( 30 days ) = 56000

In November – October's sale = 30500 ( 30 days )

In December – November's Sales = 32500 ( 30 days )

In January – December's Sales = 35000 ( 30 days )

In February – January's Sales = 36500 ( 30 days )

Now calculating Purchase on the basis of Supplier Payment Terms ( 45 Days )

In September – July's Purchase = 10000

4

Cash budget can be said as a plan in which estimates of cash flows are given. Details of

cash inflows and outflows ascertained for a specific period of time. This is used by Coach Inc. to

assess sufficiency of cash in business operations (Penn, 2012). For creating cash budgets, sales

as well as production forecasts, assumptions are required (Schellhorn and Sharma, 2013).

Cash Budget of Coach inc.

Particulars (in 000) September October November December January February

Opening balance 10500 10150 44075 52925 63425 76580

(A) Cash receipts

Sales 22500 56000 30500 32500 35000 36500

Total 33000 66150 74575 85425 98425 113080

(B) Cash payments

Purchase 10000 9000 8600 8600 8600 8600

Salaries and wages 2900 2900 2900 2900 2900 2900

Overheads 5600 5600 5600 5600 5600 5600

Selling and

administration 4350 4575 4550 4900 4745 4940

Total 22850 22075 21650 22000 21845 22040

Cash at the end (A-

B) 10150 44075 52925 63425 76580 91040

Working Notes - Firstly calculating Sales from September to February. These sales on the basis

of 60 days, 45 days and 30 days.

In September – July's Sales = 22500 (60 days )

In October = August's sales + September's Sales

27000 (45 days ) + 29000 ( 30 days ) = 56000

In November – October's sale = 30500 ( 30 days )

In December – November's Sales = 32500 ( 30 days )

In January – December's Sales = 35000 ( 30 days )

In February – January's Sales = 36500 ( 30 days )

Now calculating Purchase on the basis of Supplier Payment Terms ( 45 Days )

In September – July's Purchase = 10000

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

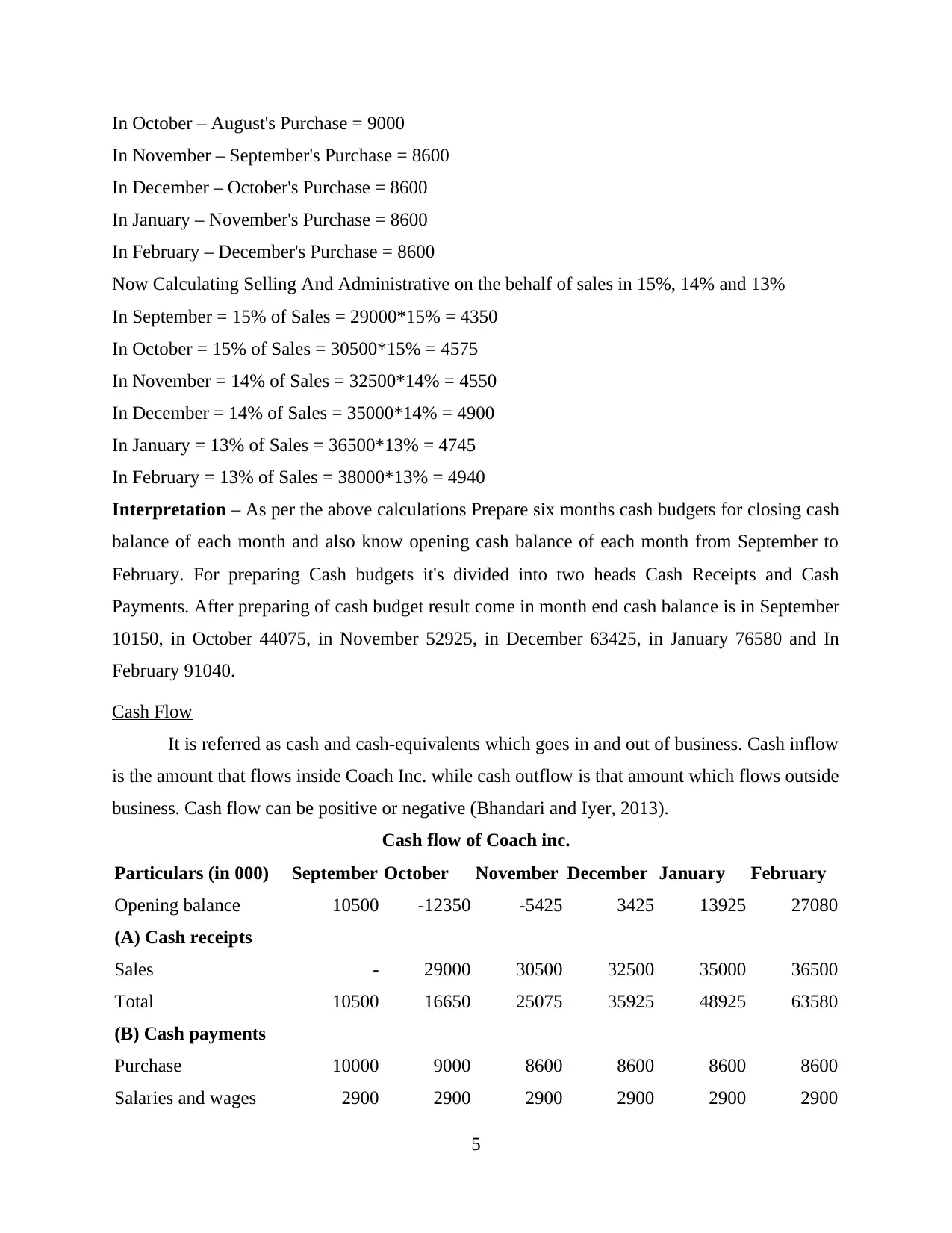

In October – August's Purchase = 9000

In November – September's Purchase = 8600

In December – October's Purchase = 8600

In January – November's Purchase = 8600

In February – December's Purchase = 8600

Now Calculating Selling And Administrative on the behalf of sales in 15%, 14% and 13%

In September = 15% of Sales = 29000*15% = 4350

In October = 15% of Sales = 30500*15% = 4575

In November = 14% of Sales = 32500*14% = 4550

In December = 14% of Sales = 35000*14% = 4900

In January = 13% of Sales = 36500*13% = 4745

In February = 13% of Sales = 38000*13% = 4940

Interpretation – As per the above calculations Prepare six months cash budgets for closing cash

balance of each month and also know opening cash balance of each month from September to

February. For preparing Cash budgets it's divided into two heads Cash Receipts and Cash

Payments. After preparing of cash budget result come in month end cash balance is in September

10150, in October 44075, in November 52925, in December 63425, in January 76580 and In

February 91040.

Cash Flow

It is referred as cash and cash-equivalents which goes in and out of business. Cash inflow

is the amount that flows inside Coach Inc. while cash outflow is that amount which flows outside

business. Cash flow can be positive or negative (Bhandari and Iyer, 2013).

Cash flow of Coach inc.

Particulars (in 000) September October November December January February

Opening balance 10500 -12350 -5425 3425 13925 27080

(A) Cash receipts

Sales - 29000 30500 32500 35000 36500

Total 10500 16650 25075 35925 48925 63580

(B) Cash payments

Purchase 10000 9000 8600 8600 8600 8600

Salaries and wages 2900 2900 2900 2900 2900 2900

5

In November – September's Purchase = 8600

In December – October's Purchase = 8600

In January – November's Purchase = 8600

In February – December's Purchase = 8600

Now Calculating Selling And Administrative on the behalf of sales in 15%, 14% and 13%

In September = 15% of Sales = 29000*15% = 4350

In October = 15% of Sales = 30500*15% = 4575

In November = 14% of Sales = 32500*14% = 4550

In December = 14% of Sales = 35000*14% = 4900

In January = 13% of Sales = 36500*13% = 4745

In February = 13% of Sales = 38000*13% = 4940

Interpretation – As per the above calculations Prepare six months cash budgets for closing cash

balance of each month and also know opening cash balance of each month from September to

February. For preparing Cash budgets it's divided into two heads Cash Receipts and Cash

Payments. After preparing of cash budget result come in month end cash balance is in September

10150, in October 44075, in November 52925, in December 63425, in January 76580 and In

February 91040.

Cash Flow

It is referred as cash and cash-equivalents which goes in and out of business. Cash inflow

is the amount that flows inside Coach Inc. while cash outflow is that amount which flows outside

business. Cash flow can be positive or negative (Bhandari and Iyer, 2013).

Cash flow of Coach inc.

Particulars (in 000) September October November December January February

Opening balance 10500 -12350 -5425 3425 13925 27080

(A) Cash receipts

Sales - 29000 30500 32500 35000 36500

Total 10500 16650 25075 35925 48925 63580

(B) Cash payments

Purchase 10000 9000 8600 8600 8600 8600

Salaries and wages 2900 2900 2900 2900 2900 2900

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

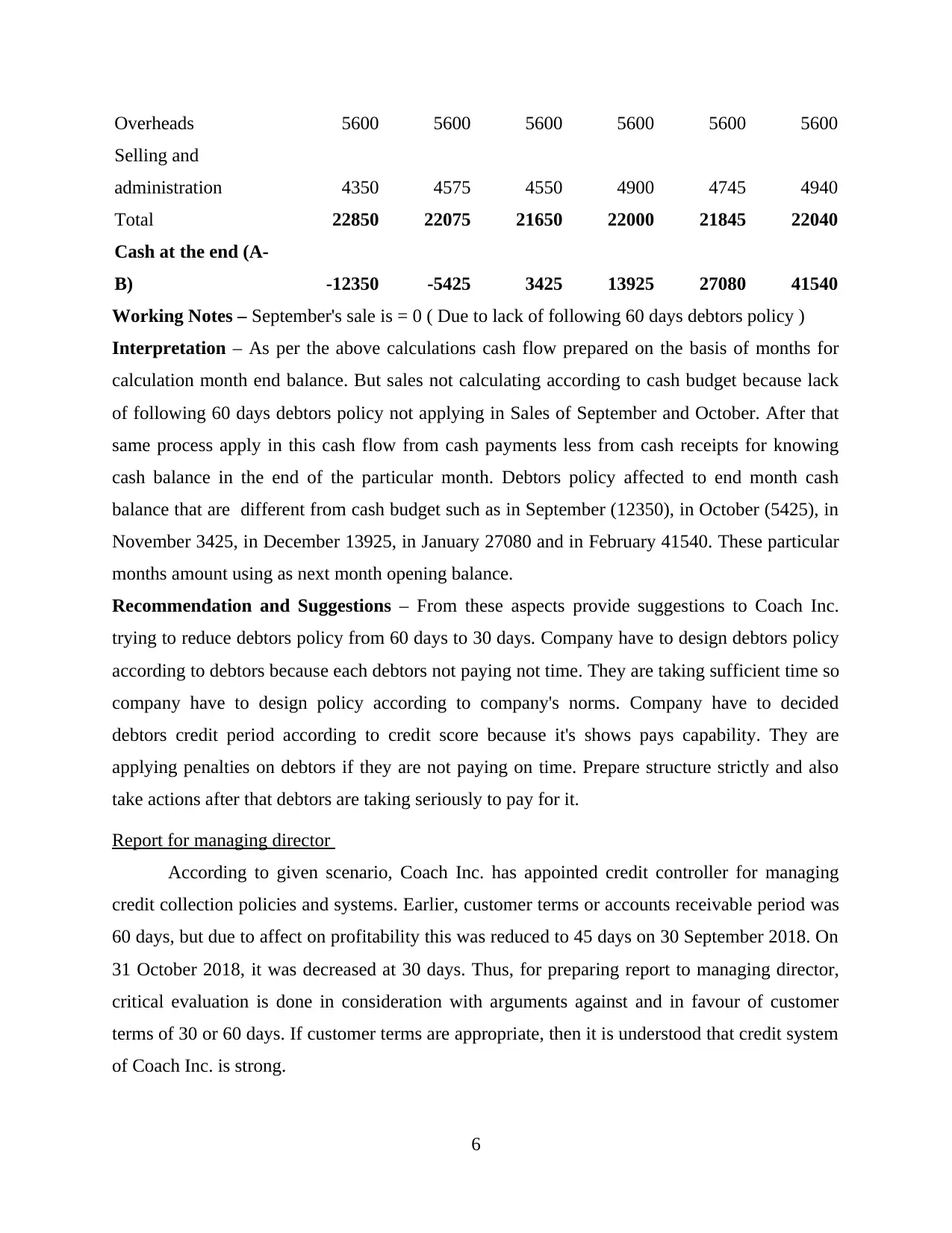

Overheads 5600 5600 5600 5600 5600 5600

Selling and

administration 4350 4575 4550 4900 4745 4940

Total 22850 22075 21650 22000 21845 22040

Cash at the end (A-

B) -12350 -5425 3425 13925 27080 41540

Working Notes – September's sale is = 0 ( Due to lack of following 60 days debtors policy )

Interpretation – As per the above calculations cash flow prepared on the basis of months for

calculation month end balance. But sales not calculating according to cash budget because lack

of following 60 days debtors policy not applying in Sales of September and October. After that

same process apply in this cash flow from cash payments less from cash receipts for knowing

cash balance in the end of the particular month. Debtors policy affected to end month cash

balance that are different from cash budget such as in September (12350), in October (5425), in

November 3425, in December 13925, in January 27080 and in February 41540. These particular

months amount using as next month opening balance.

Recommendation and Suggestions – From these aspects provide suggestions to Coach Inc.

trying to reduce debtors policy from 60 days to 30 days. Company have to design debtors policy

according to debtors because each debtors not paying not time. They are taking sufficient time so

company have to design policy according to company's norms. Company have to decided

debtors credit period according to credit score because it's shows pays capability. They are

applying penalties on debtors if they are not paying on time. Prepare structure strictly and also

take actions after that debtors are taking seriously to pay for it.

Report for managing director

According to given scenario, Coach Inc. has appointed credit controller for managing

credit collection policies and systems. Earlier, customer terms or accounts receivable period was

60 days, but due to affect on profitability this was reduced to 45 days on 30 September 2018. On

31 October 2018, it was decreased at 30 days. Thus, for preparing report to managing director,

critical evaluation is done in consideration with arguments against and in favour of customer

terms of 30 or 60 days. If customer terms are appropriate, then it is understood that credit system

of Coach Inc. is strong.

6

Selling and

administration 4350 4575 4550 4900 4745 4940

Total 22850 22075 21650 22000 21845 22040

Cash at the end (A-

B) -12350 -5425 3425 13925 27080 41540

Working Notes – September's sale is = 0 ( Due to lack of following 60 days debtors policy )

Interpretation – As per the above calculations cash flow prepared on the basis of months for

calculation month end balance. But sales not calculating according to cash budget because lack

of following 60 days debtors policy not applying in Sales of September and October. After that

same process apply in this cash flow from cash payments less from cash receipts for knowing

cash balance in the end of the particular month. Debtors policy affected to end month cash

balance that are different from cash budget such as in September (12350), in October (5425), in

November 3425, in December 13925, in January 27080 and in February 41540. These particular

months amount using as next month opening balance.

Recommendation and Suggestions – From these aspects provide suggestions to Coach Inc.

trying to reduce debtors policy from 60 days to 30 days. Company have to design debtors policy

according to debtors because each debtors not paying not time. They are taking sufficient time so

company have to design policy according to company's norms. Company have to decided

debtors credit period according to credit score because it's shows pays capability. They are

applying penalties on debtors if they are not paying on time. Prepare structure strictly and also

take actions after that debtors are taking seriously to pay for it.

Report for managing director

According to given scenario, Coach Inc. has appointed credit controller for managing

credit collection policies and systems. Earlier, customer terms or accounts receivable period was

60 days, but due to affect on profitability this was reduced to 45 days on 30 September 2018. On

31 October 2018, it was decreased at 30 days. Thus, for preparing report to managing director,

critical evaluation is done in consideration with arguments against and in favour of customer

terms of 30 or 60 days. If customer terms are appropriate, then it is understood that credit system

of Coach Inc. is strong.

6

Customer terms have great impact on amount of cash in hand of organization. As delay in

collections affects liquidity position (Gottardo and Maria Moisello, 2014). If a customer is not

paying its dues on time, but Coach Inc. has to make payment to its suppliers for goods

purchased. Thus, it needs to pay them out of reserves of company. As all suppliers needs

payment on time and also interest will be charged if delayed. Reserves of Coach Inc. would be

vanished if customers frequently delayed the payment.

Collection period of 30 days is said to be more beneficial as it strengthens credit policies.

Customers will become more attentive and punctual towards timely payment. This is because,

customers does not so much cares about time and interest charged on them. Decrease in

collection period will assist in risk minimization and enhancement in expectations of payment.

Coach Inc. can reduce its customer credit term by offering discounts on advance payment and

charge fees on late payment. For this, proper training should be provided to employees in making

calls and send letters to customers who often delays. Also a software of purchase account

receivable should be developed by which due dates of payment could be tracked.

Customer terms of 60 days will not prove beneficial for Coach Inc. This is because, high

collection period can create few problems. When collection period will be high then Coach Inc.

needs to waste time on communication with customers in respect to their debts as well as

expected date of payment. Also, organization needs to take crucial bill collection decisions (Gay,

2016). Term of 60 days implies that customers are not willing or intended to make payment.

Risk of bad debts also increases.

In both scenarios of 30 days and 60 days, some of financial and non-financial factors

impacts cash flow. Cash flow is affected by collection period in such a way that if Coach Inc. is

available with enough cash then problem of uneven cash flow will not arise. Financial factors

includes increase in possibility of bad debts, opportunity costs in receivables, cost of doing credit

analysis, bearing collection costs, discount cost which is offered for early payments (Profit and

loss statement, 2018). Non-financial factors are relation with customers, management of

inventory.

CONCLUSION

From above discussion, it is concluded that management of financing is important from

point of view of assessment of financing techniques. Concepts of it are derived from managerial

accounting as well as corporate finance that assists in sound financial management. In this report,

7

collections affects liquidity position (Gottardo and Maria Moisello, 2014). If a customer is not

paying its dues on time, but Coach Inc. has to make payment to its suppliers for goods

purchased. Thus, it needs to pay them out of reserves of company. As all suppliers needs

payment on time and also interest will be charged if delayed. Reserves of Coach Inc. would be

vanished if customers frequently delayed the payment.

Collection period of 30 days is said to be more beneficial as it strengthens credit policies.

Customers will become more attentive and punctual towards timely payment. This is because,

customers does not so much cares about time and interest charged on them. Decrease in

collection period will assist in risk minimization and enhancement in expectations of payment.

Coach Inc. can reduce its customer credit term by offering discounts on advance payment and

charge fees on late payment. For this, proper training should be provided to employees in making

calls and send letters to customers who often delays. Also a software of purchase account

receivable should be developed by which due dates of payment could be tracked.

Customer terms of 60 days will not prove beneficial for Coach Inc. This is because, high

collection period can create few problems. When collection period will be high then Coach Inc.

needs to waste time on communication with customers in respect to their debts as well as

expected date of payment. Also, organization needs to take crucial bill collection decisions (Gay,

2016). Term of 60 days implies that customers are not willing or intended to make payment.

Risk of bad debts also increases.

In both scenarios of 30 days and 60 days, some of financial and non-financial factors

impacts cash flow. Cash flow is affected by collection period in such a way that if Coach Inc. is

available with enough cash then problem of uneven cash flow will not arise. Financial factors

includes increase in possibility of bad debts, opportunity costs in receivables, cost of doing credit

analysis, bearing collection costs, discount cost which is offered for early payments (Profit and

loss statement, 2018). Non-financial factors are relation with customers, management of

inventory.

CONCLUSION

From above discussion, it is concluded that management of financing is important from

point of view of assessment of financing techniques. Concepts of it are derived from managerial

accounting as well as corporate finance that assists in sound financial management. In this report,

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

profit and loss account, cash budget, and forecasted cash flows have been prepared. These

statements help in calculating net income, maintaining cash balances, keeping track on expenses

as well as revenues. Also, credit policies of company should be as much strict as these lead to

timely payment by customers. All these in complete manner, contributes to overall assessment of

financial success and growth.

8

statements help in calculating net income, maintaining cash balances, keeping track on expenses

as well as revenues. Also, credit policies of company should be as much strict as these lead to

timely payment by customers. All these in complete manner, contributes to overall assessment of

financial success and growth.

8

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.