Managerial Finance Report: Analysis of JD and SD Financial Performance

VerifiedAdded on 2020/06/06

|30

|4984

|25

Report

AI Summary

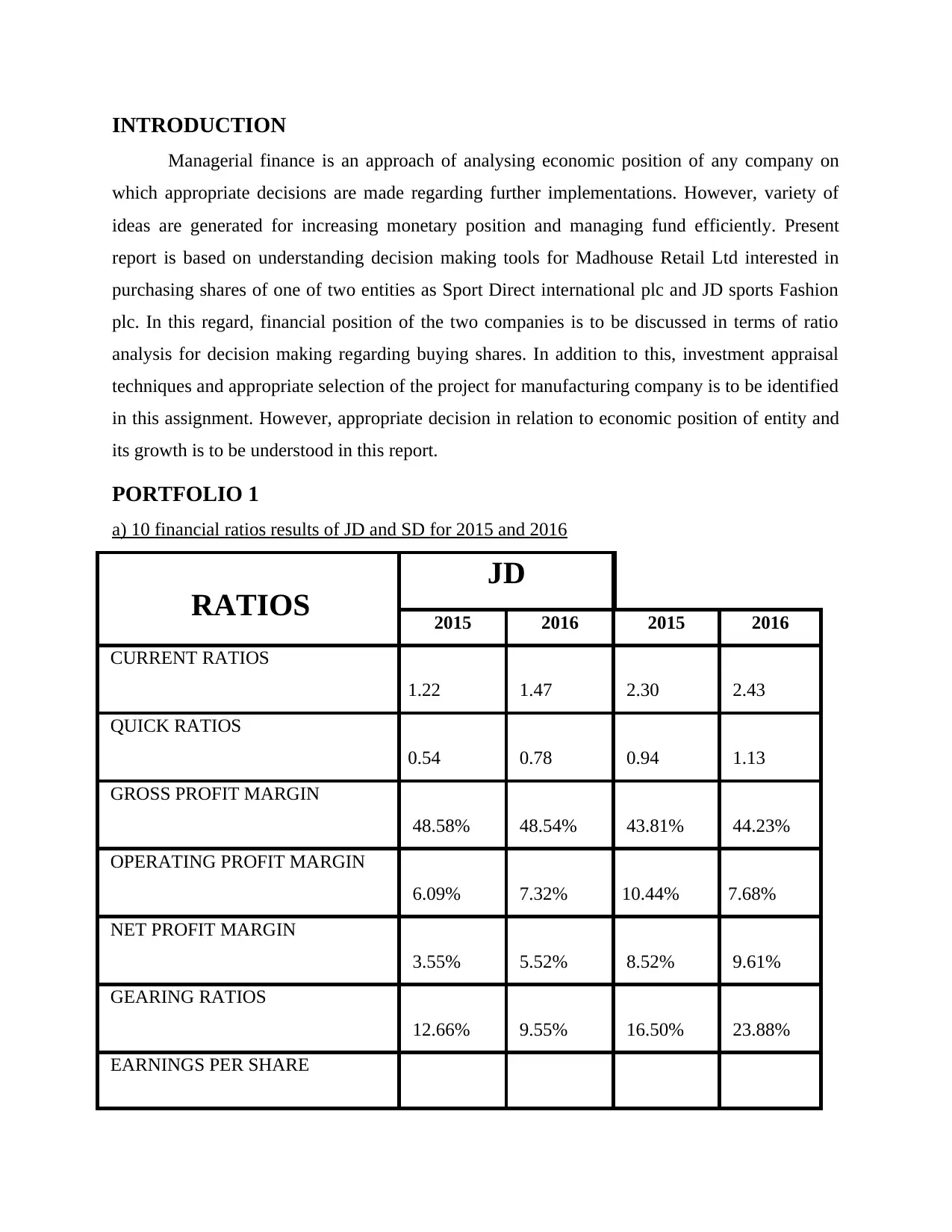

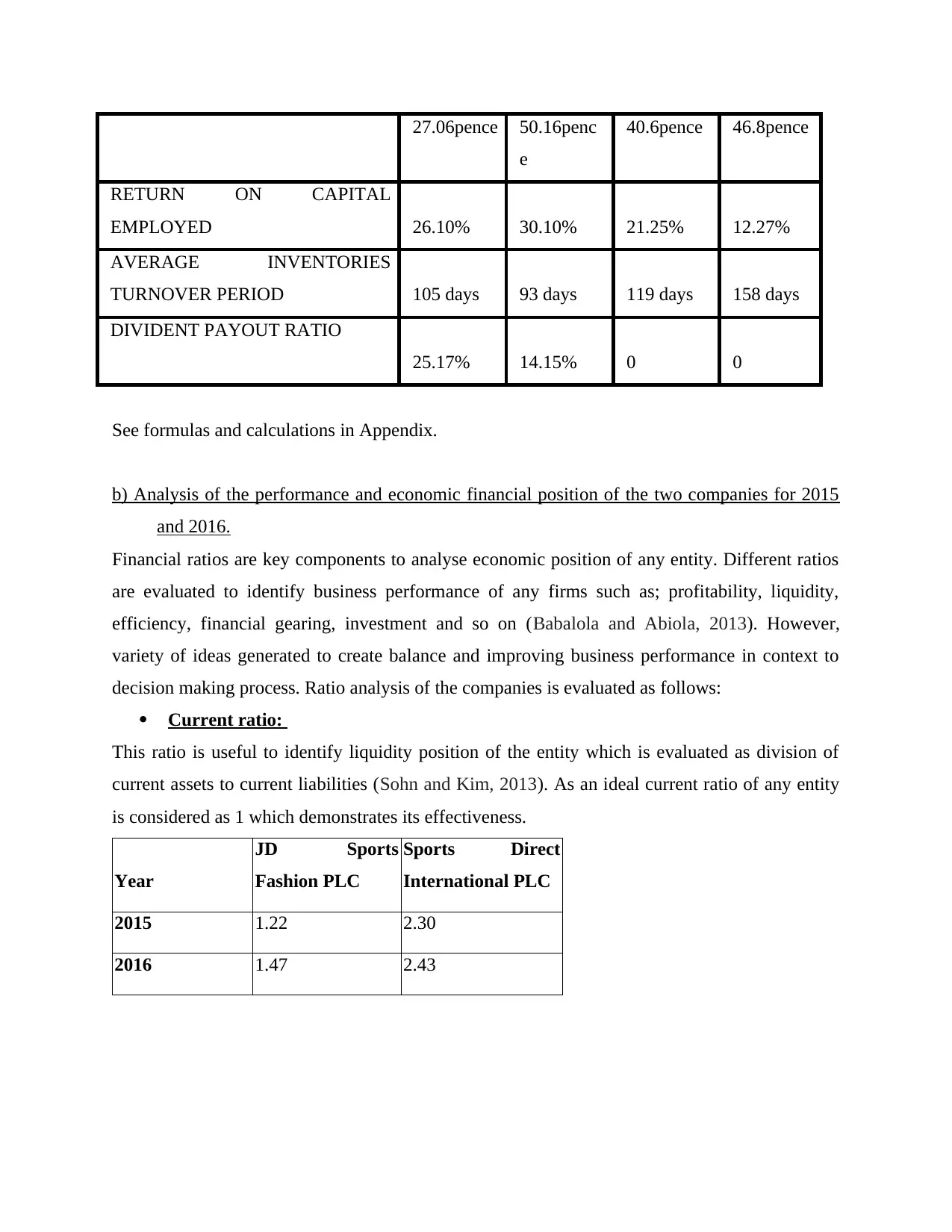

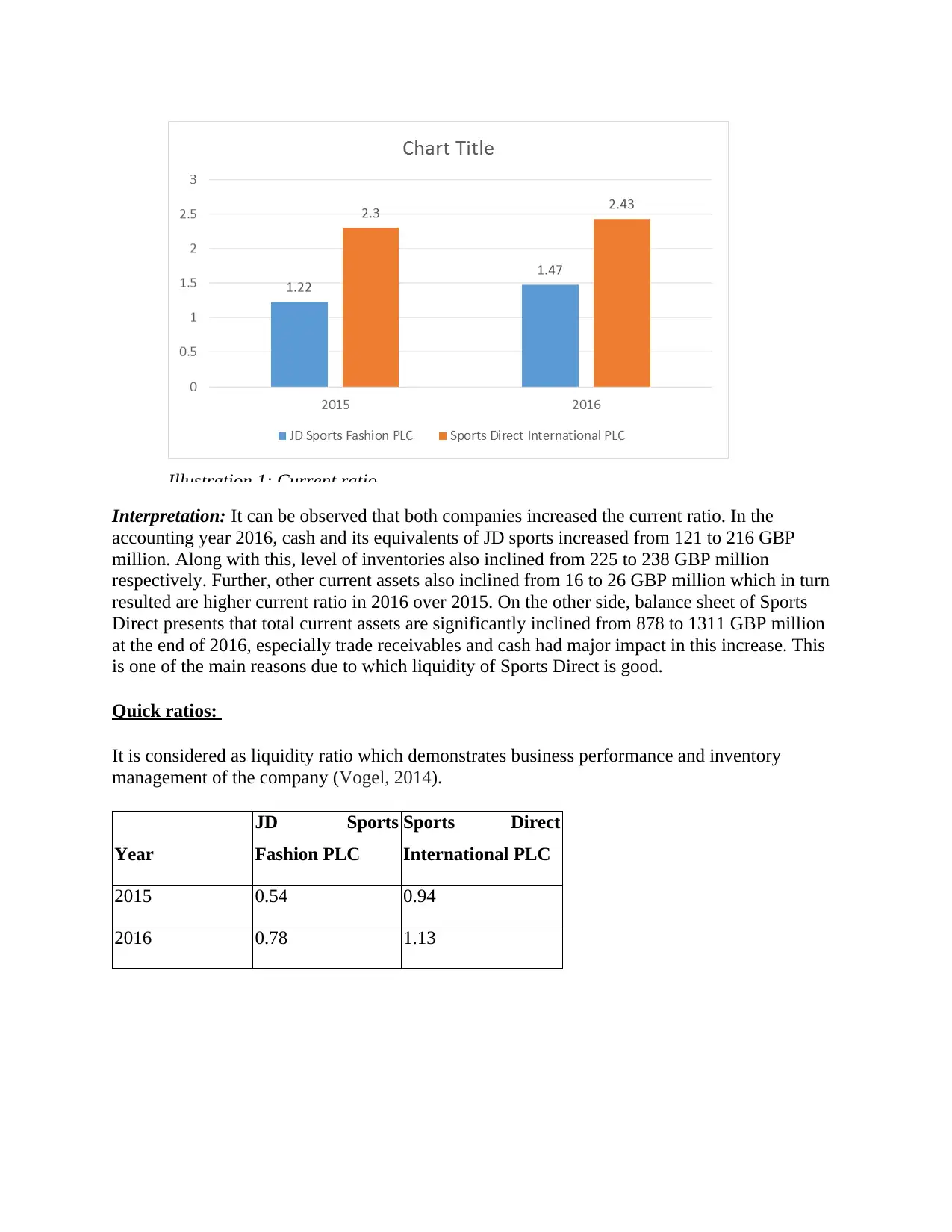

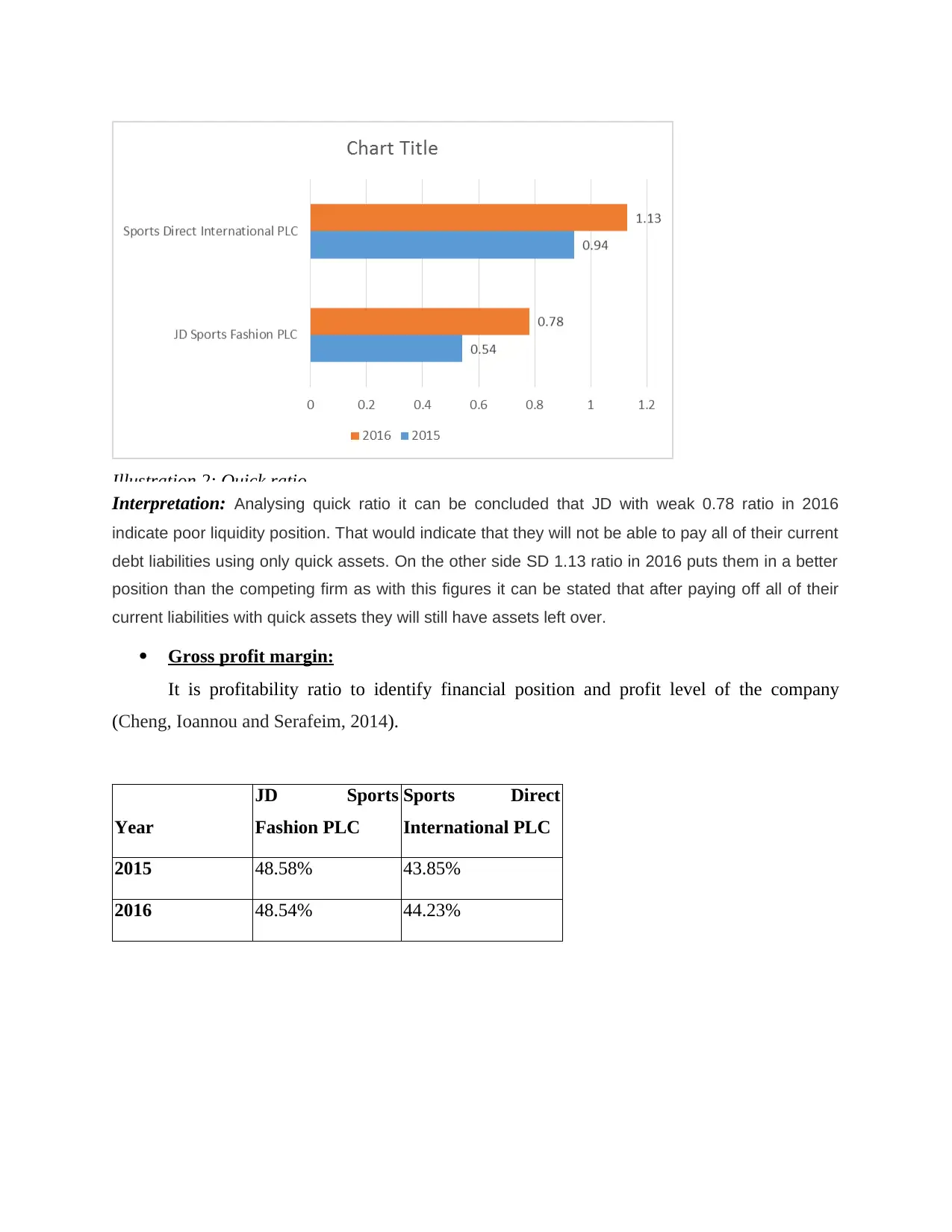

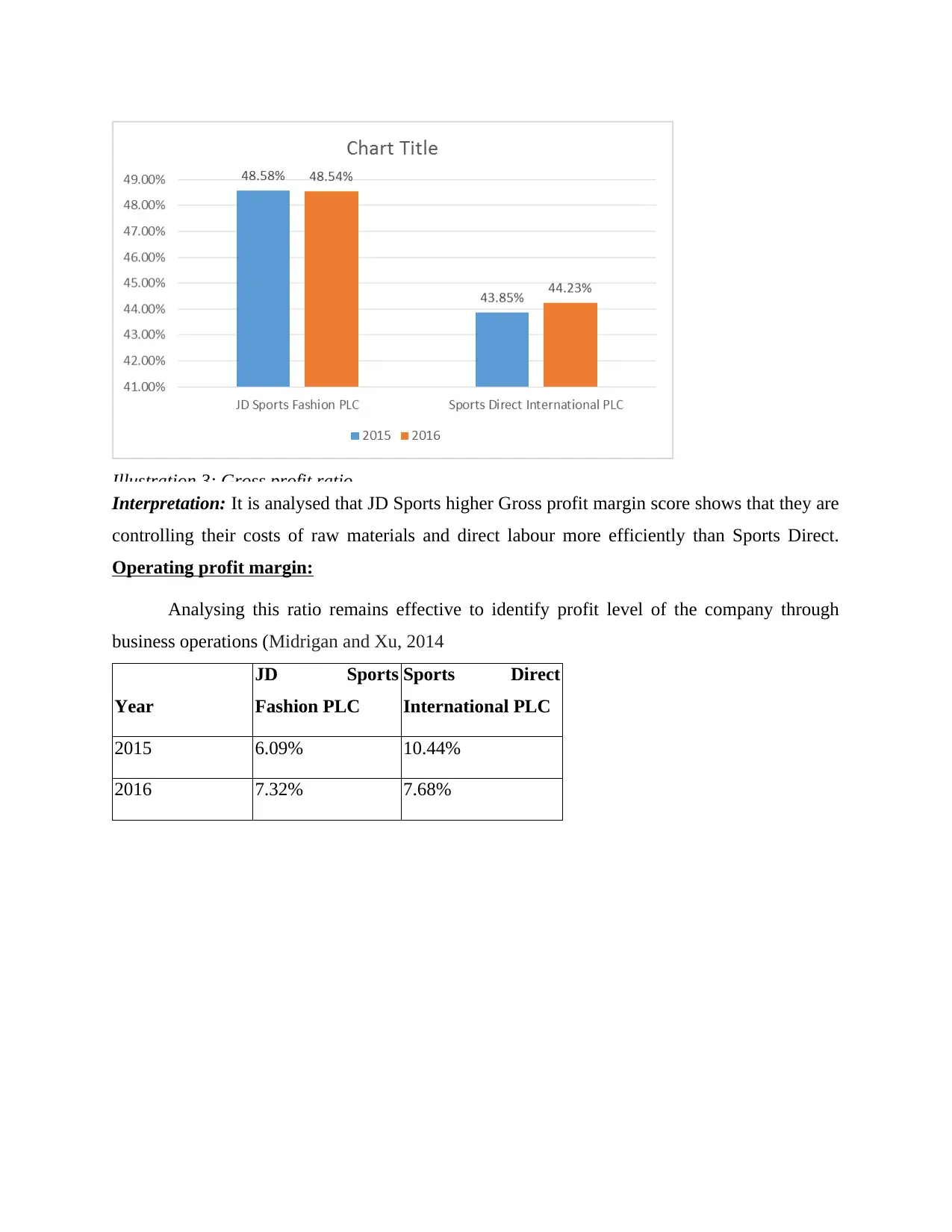

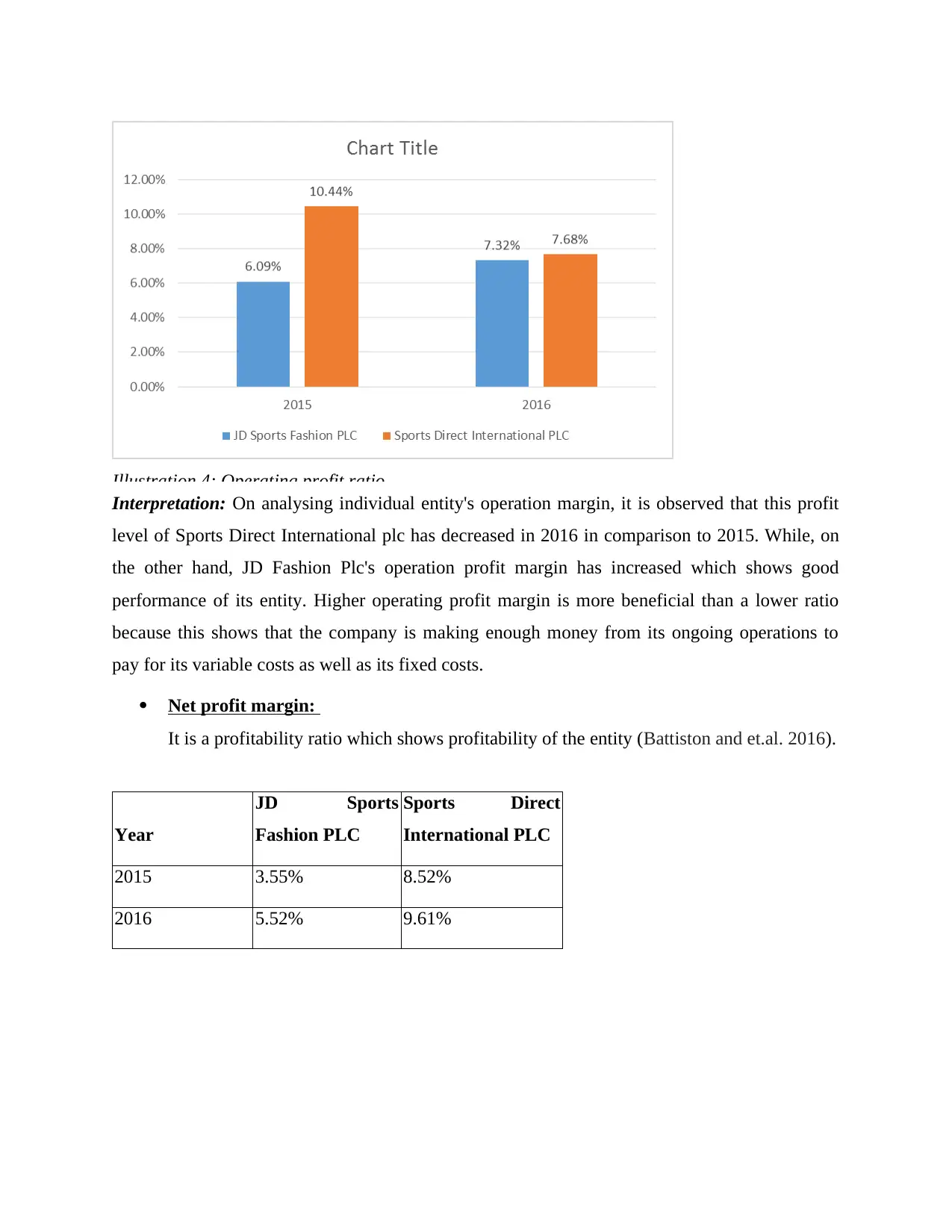

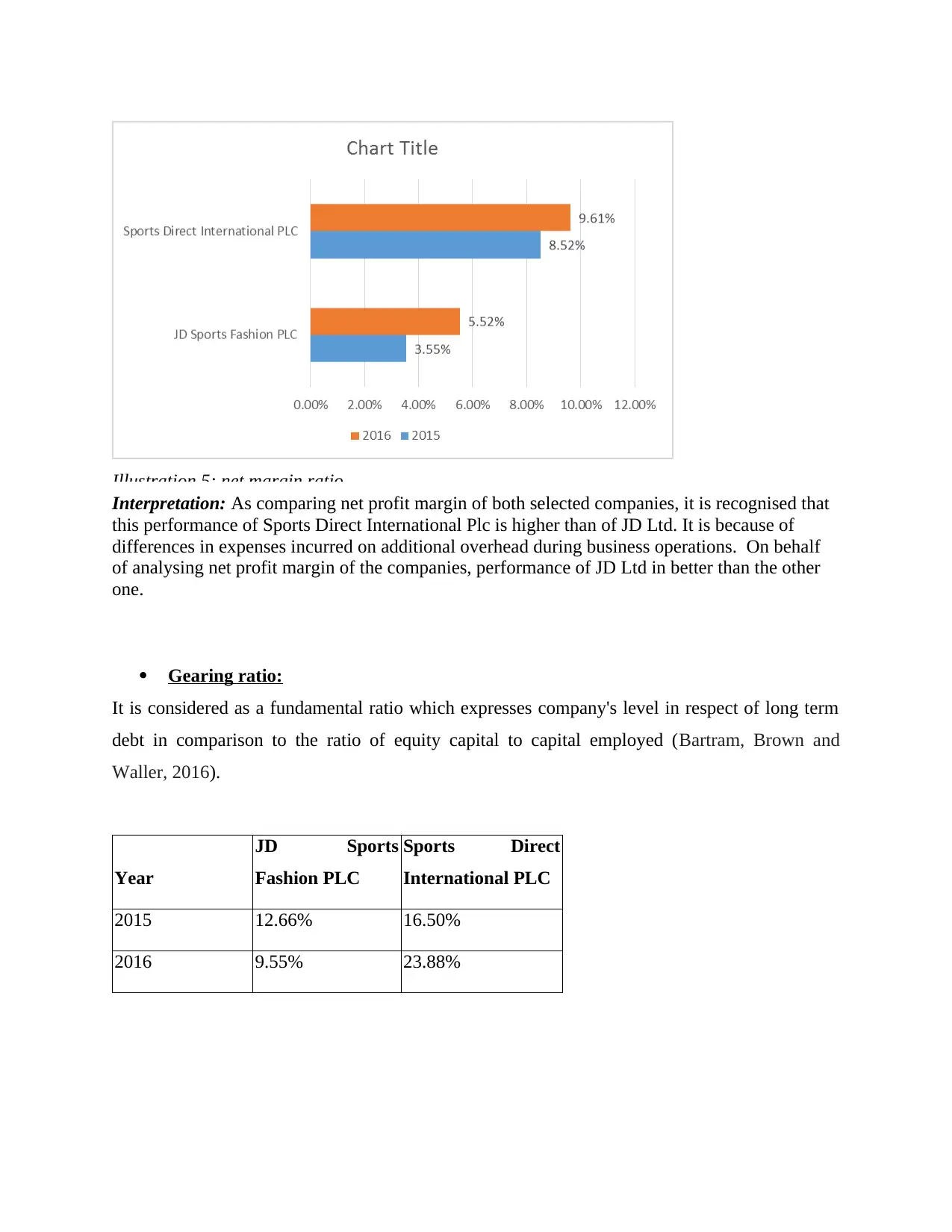

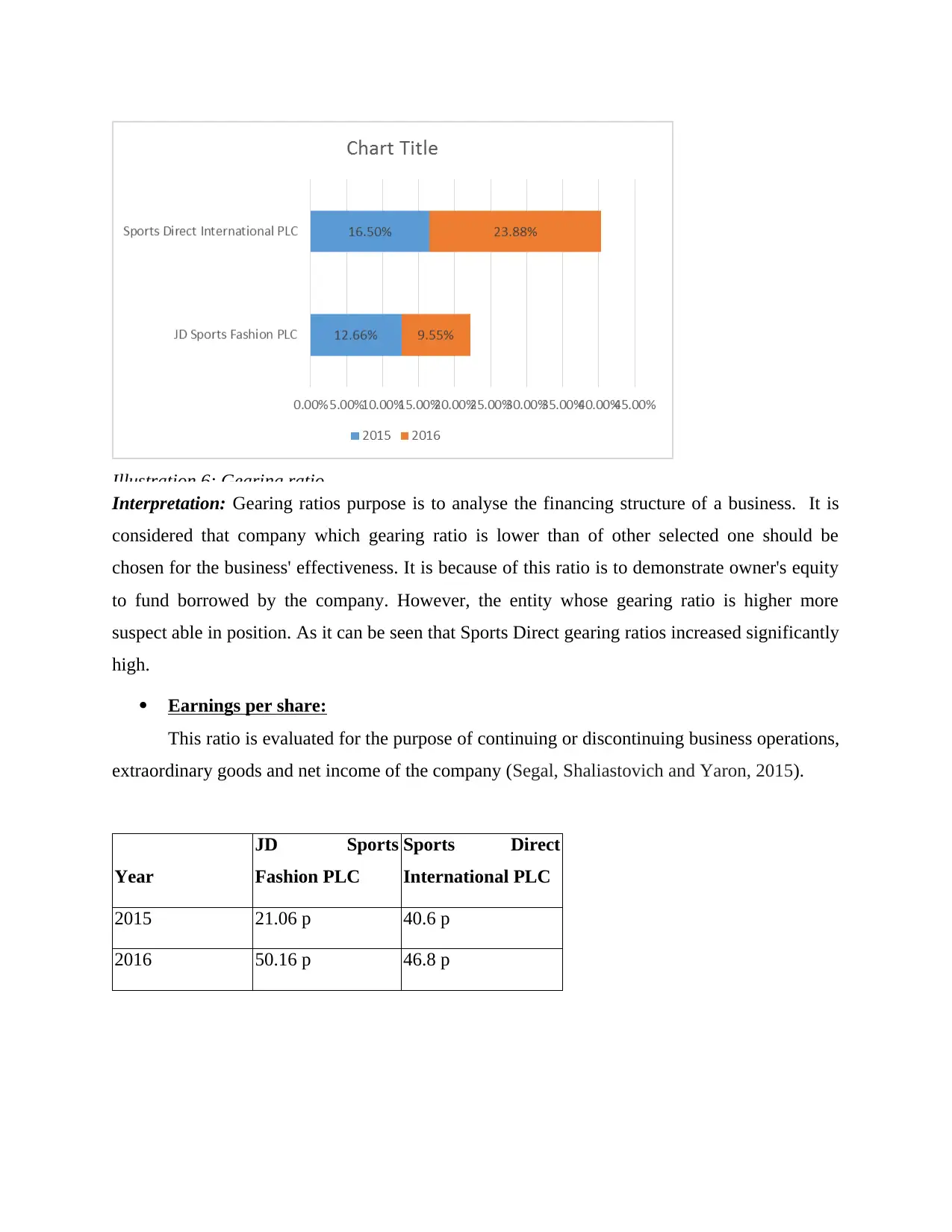

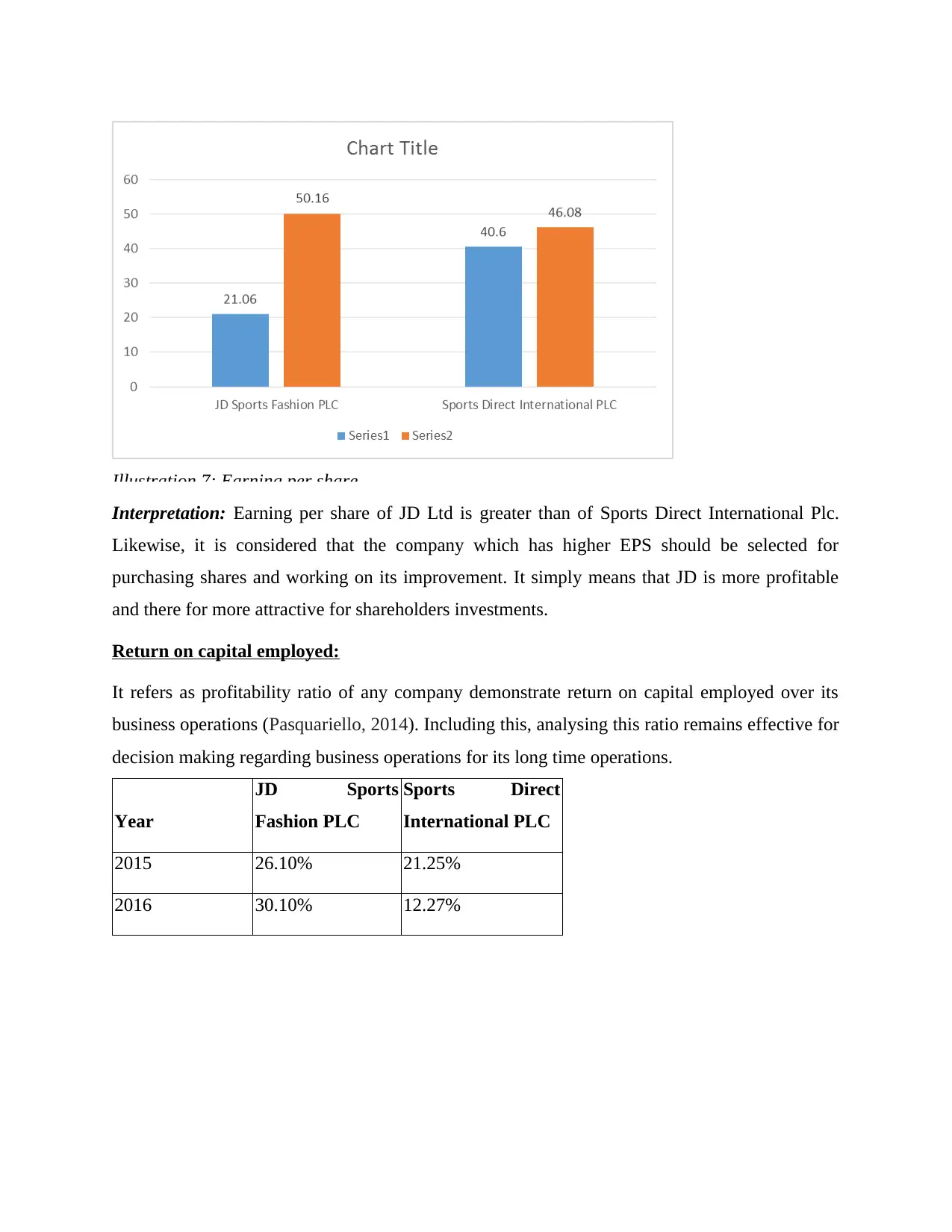

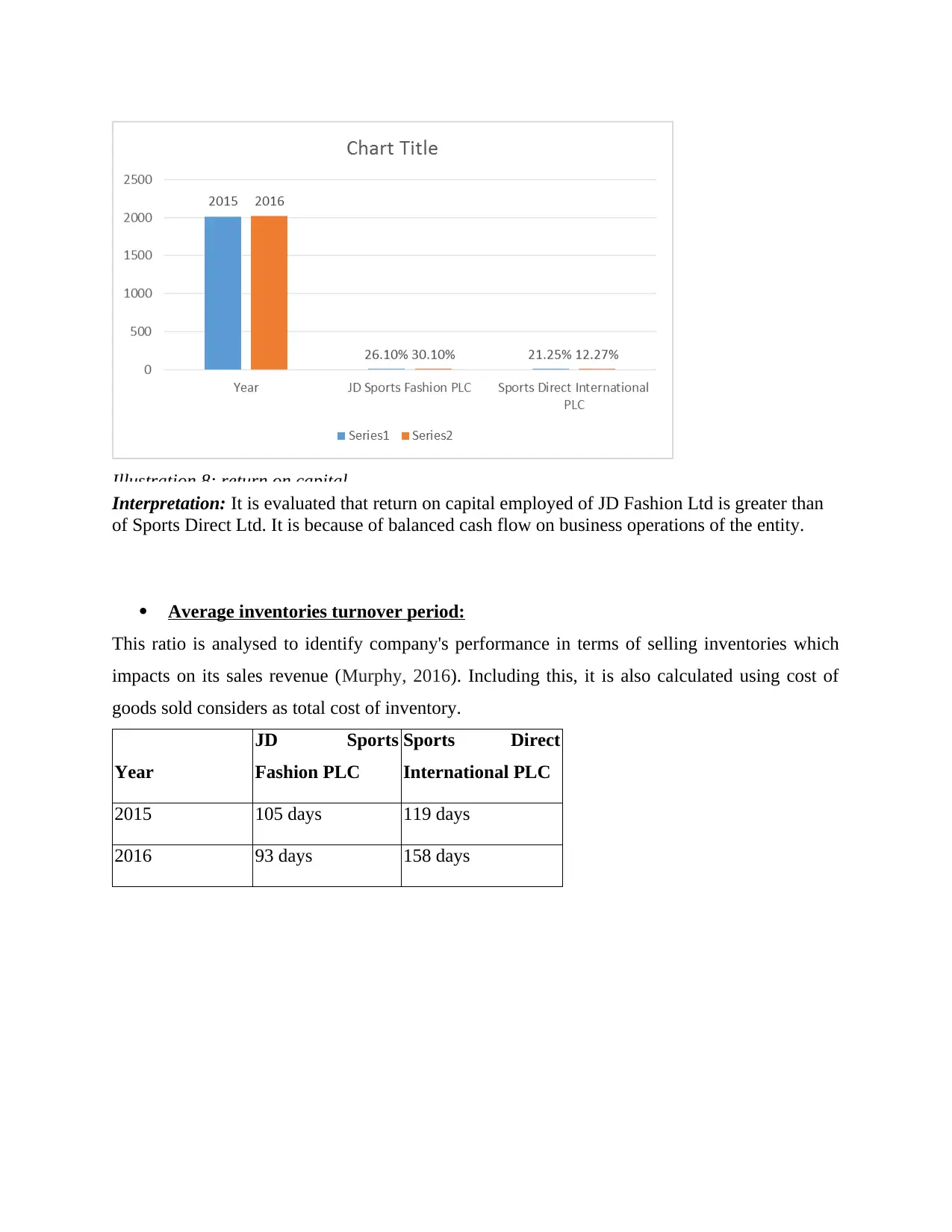

This report provides a comprehensive analysis of managerial finance, focusing on the financial performance of JD Sports Fashion PLC and Sports Direct International PLC. The report begins with an introduction to managerial finance and its application in decision-making, particularly in the context of share purchases. The core of the report is Portfolio 1, which includes a detailed analysis of ten key financial ratios for both companies over the years 2015 and 2016. These ratios include current ratio, quick ratio, gross profit margin, operating profit margin, net profit margin, gearing ratio, earnings per share, return on capital employed, average inventories turnover, and dividend payout ratio. The analysis compares the performance of the two companies, highlighting their strengths and weaknesses based on these ratios. Portfolio 2 then discusses the limitations of investment appraisal techniques in long-term decision-making. The report concludes with recommendations for improving financial performance, such as inventory turnover optimization and budgetary control. Formulas, calculations, and interpretations are provided to support the analysis, making it a valuable resource for understanding financial performance and investment potential. The report is concluded with references and an appendix with the calculations.

1 out of 30

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.