Managerial Finance Report: Analysis of Coach Inc.'s Finances

VerifiedAdded on 2020/11/12

|10

|2975

|111

Report

AI Summary

This report, focusing on managerial finance, analyzes the financial performance of Coach Inc. for the period of September 2018 to February 2019. It includes a detailed examination of the profit & loss account, balance sheet, and cash budget, alongside cash flow projections. The report highlights key financial metrics such as gross profit, net loss, and cash balances. It interprets the financial data, including the impact of debtors' policy on cash flow and provides recommendations for improving financial management, such as reducing the debtor's policy period. The report also includes working notes to support the calculations and interpretations of the financial data.

MANAGERIAL

FINANCE

FINANCE

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

Profit & Loss Account ...........................................................................................................1

Balance Sheet.........................................................................................................................2

Cash Budget............................................................................................................................3

Cash flows..............................................................................................................................5

Report for the managing director...........................................................................................6

CONCLUSION................................................................................................................................7

REFERENCES................................................................................................................................8

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

Profit & Loss Account ...........................................................................................................1

Balance Sheet.........................................................................................................................2

Cash Budget............................................................................................................................3

Cash flows..............................................................................................................................5

Report for the managing director...........................................................................................6

CONCLUSION................................................................................................................................7

REFERENCES................................................................................................................................8

INTRODUCTION

Managerial finance is the branch of finance that asset of financial techniques to determine

how they affect the business externally and internally (Alhassan, 2015). Managerial finance takes

into mentation how to modify financial techniques to better the company and where changes can

be made to preclude loss. This approach is a assortment between managerial and corporate

financing. This reports covers prepare forecast profit and loss account for the two months of

September and October, a forecast balance sheet at the end 31 October. Prepare a cash budget for

the managing directors, a forecast cash flow and month end cash balances form September to

February 2019. Preparation of draft report to the managing director to analyse customers terms

of 30 to 60 days including financial and non financial factors.

MAIN BODY

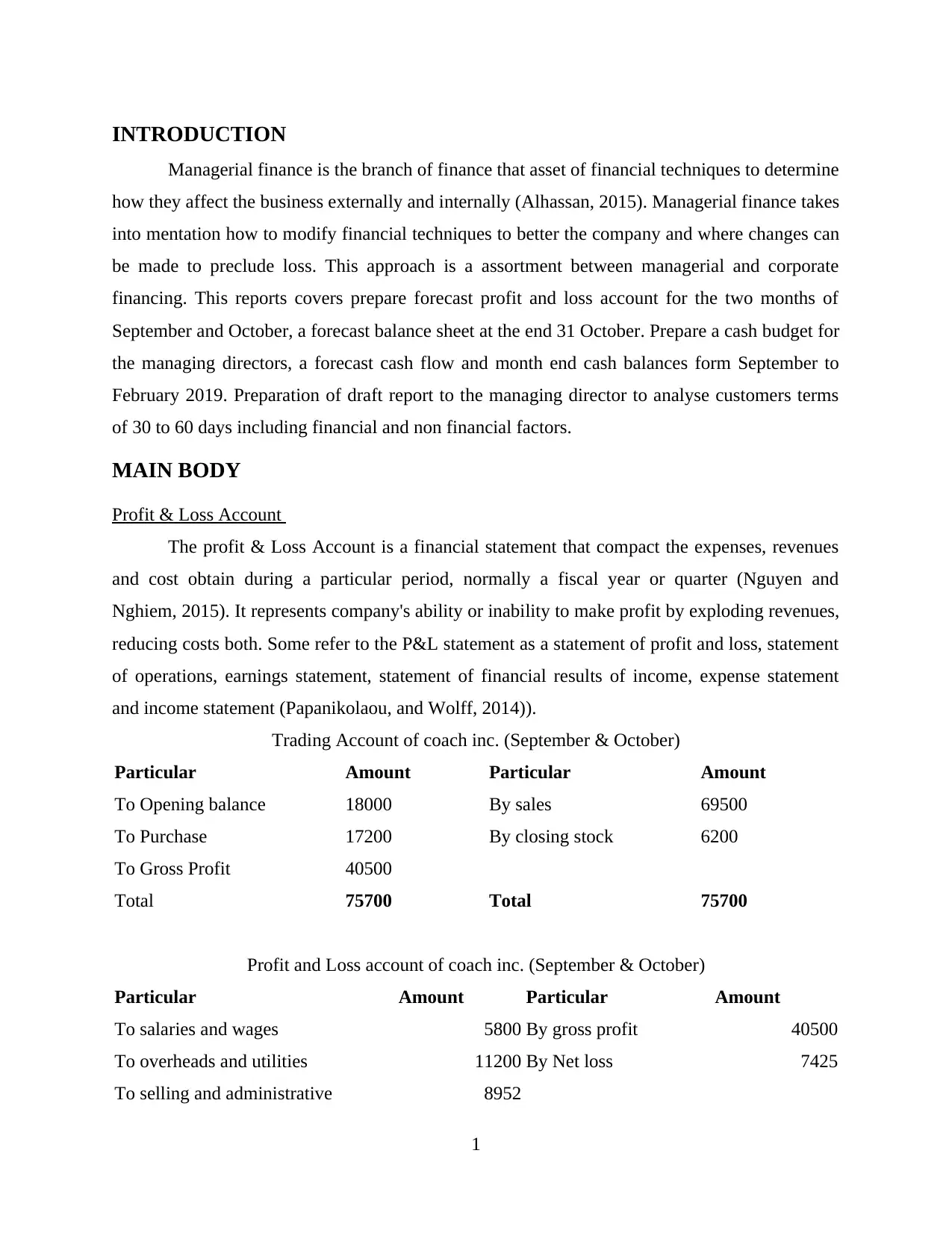

Profit & Loss Account

The profit & Loss Account is a financial statement that compact the expenses, revenues

and cost obtain during a particular period, normally a fiscal year or quarter (Nguyen and

Nghiem, 2015). It represents company's ability or inability to make profit by exploding revenues,

reducing costs both. Some refer to the P&L statement as a statement of profit and loss, statement

of operations, earnings statement, statement of financial results of income, expense statement

and income statement (Papanikolaou, and Wolff, 2014)).

Trading Account of coach inc. (September & October)

Particular Amount Particular Amount

To Opening balance 18000 By sales 69500

To Purchase 17200 By closing stock 6200

To Gross Profit 40500

Total 75700 Total 75700

Profit and Loss account of coach inc. (September & October)

Particular Amount Particular Amount

To salaries and wages 5800 By gross profit 40500

To overheads and utilities 11200 By Net loss 7425

To selling and administrative 8952

1

Managerial finance is the branch of finance that asset of financial techniques to determine

how they affect the business externally and internally (Alhassan, 2015). Managerial finance takes

into mentation how to modify financial techniques to better the company and where changes can

be made to preclude loss. This approach is a assortment between managerial and corporate

financing. This reports covers prepare forecast profit and loss account for the two months of

September and October, a forecast balance sheet at the end 31 October. Prepare a cash budget for

the managing directors, a forecast cash flow and month end cash balances form September to

February 2019. Preparation of draft report to the managing director to analyse customers terms

of 30 to 60 days including financial and non financial factors.

MAIN BODY

Profit & Loss Account

The profit & Loss Account is a financial statement that compact the expenses, revenues

and cost obtain during a particular period, normally a fiscal year or quarter (Nguyen and

Nghiem, 2015). It represents company's ability or inability to make profit by exploding revenues,

reducing costs both. Some refer to the P&L statement as a statement of profit and loss, statement

of operations, earnings statement, statement of financial results of income, expense statement

and income statement (Papanikolaou, and Wolff, 2014)).

Trading Account of coach inc. (September & October)

Particular Amount Particular Amount

To Opening balance 18000 By sales 69500

To Purchase 17200 By closing stock 6200

To Gross Profit 40500

Total 75700 Total 75700

Profit and Loss account of coach inc. (September & October)

Particular Amount Particular Amount

To salaries and wages 5800 By gross profit 40500

To overheads and utilities 11200 By Net loss 7425

To selling and administrative 8952

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

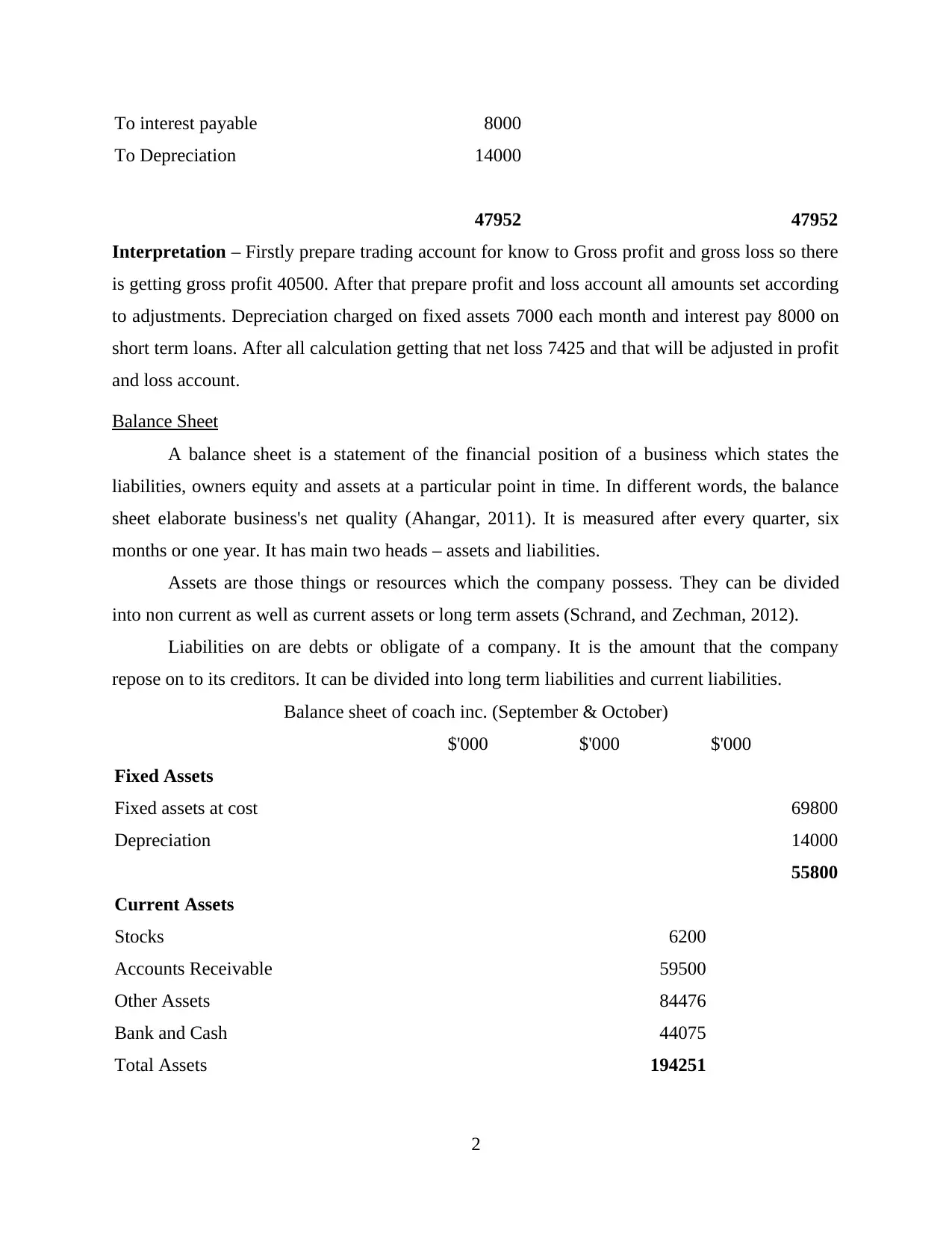

To interest payable 8000

To Depreciation 14000

47952 47952

Interpretation – Firstly prepare trading account for know to Gross profit and gross loss so there

is getting gross profit 40500. After that prepare profit and loss account all amounts set according

to adjustments. Depreciation charged on fixed assets 7000 each month and interest pay 8000 on

short term loans. After all calculation getting that net loss 7425 and that will be adjusted in profit

and loss account.

Balance Sheet

A balance sheet is a statement of the financial position of a business which states the

liabilities, owners equity and assets at a particular point in time. In different words, the balance

sheet elaborate business's net quality (Ahangar, 2011). It is measured after every quarter, six

months or one year. It has main two heads – assets and liabilities.

Assets are those things or resources which the company possess. They can be divided

into non current as well as current assets or long term assets (Schrand, and Zechman, 2012).

Liabilities on are debts or obligate of a company. It is the amount that the company

repose on to its creditors. It can be divided into long term liabilities and current liabilities.

Balance sheet of coach inc. (September & October)

$'000 $'000 $'000

Fixed Assets

Fixed assets at cost 69800

Depreciation 14000

55800

Current Assets

Stocks 6200

Accounts Receivable 59500

Other Assets 84476

Bank and Cash 44075

Total Assets 194251

2

To Depreciation 14000

47952 47952

Interpretation – Firstly prepare trading account for know to Gross profit and gross loss so there

is getting gross profit 40500. After that prepare profit and loss account all amounts set according

to adjustments. Depreciation charged on fixed assets 7000 each month and interest pay 8000 on

short term loans. After all calculation getting that net loss 7425 and that will be adjusted in profit

and loss account.

Balance Sheet

A balance sheet is a statement of the financial position of a business which states the

liabilities, owners equity and assets at a particular point in time. In different words, the balance

sheet elaborate business's net quality (Ahangar, 2011). It is measured after every quarter, six

months or one year. It has main two heads – assets and liabilities.

Assets are those things or resources which the company possess. They can be divided

into non current as well as current assets or long term assets (Schrand, and Zechman, 2012).

Liabilities on are debts or obligate of a company. It is the amount that the company

repose on to its creditors. It can be divided into long term liabilities and current liabilities.

Balance sheet of coach inc. (September & October)

$'000 $'000 $'000

Fixed Assets

Fixed assets at cost 69800

Depreciation 14000

55800

Current Assets

Stocks 6200

Accounts Receivable 59500

Other Assets 84476

Bank and Cash 44075

Total Assets 194251

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

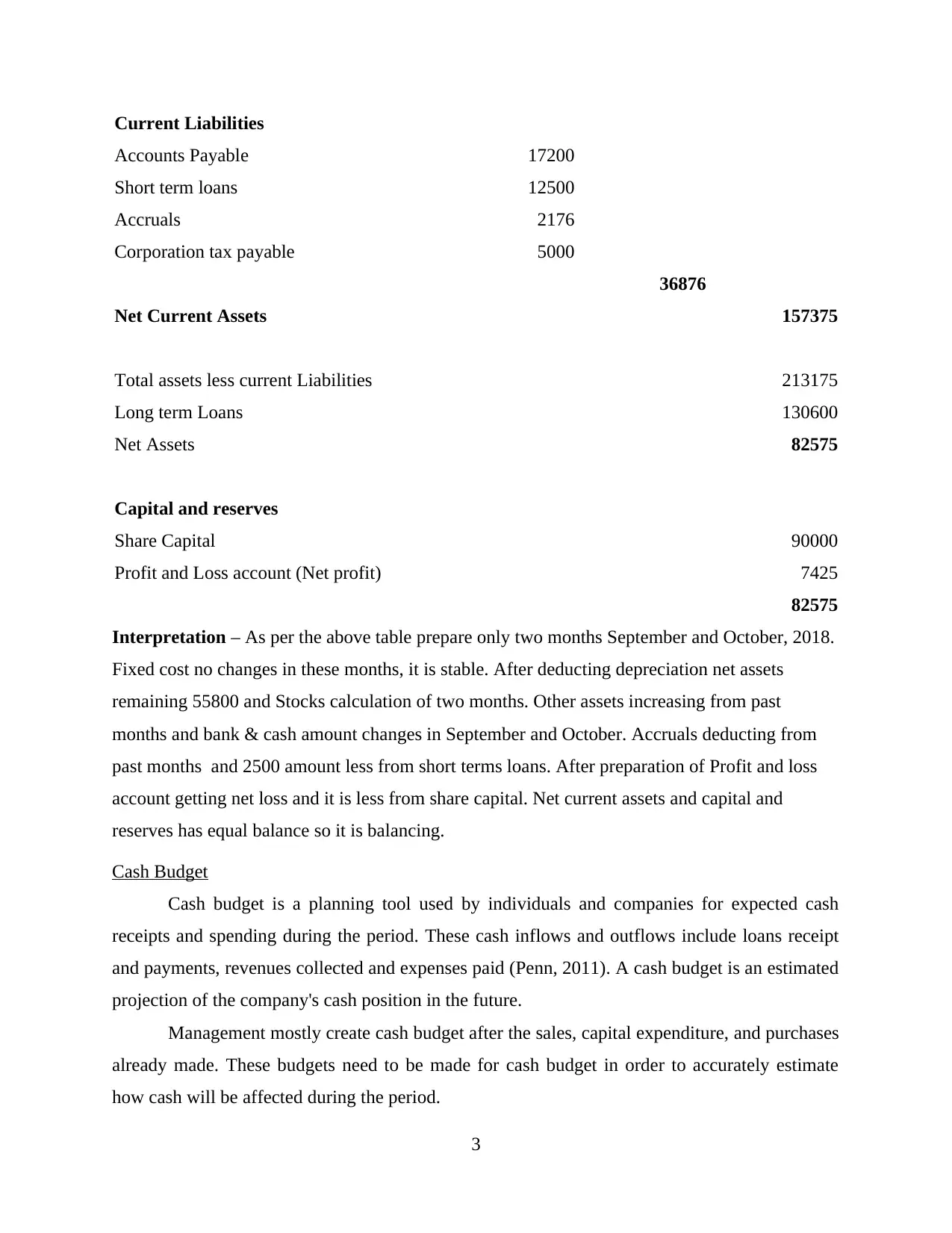

Current Liabilities

Accounts Payable 17200

Short term loans 12500

Accruals 2176

Corporation tax payable 5000

36876

Net Current Assets 157375

Total assets less current Liabilities 213175

Long term Loans 130600

Net Assets 82575

Capital and reserves

Share Capital 90000

Profit and Loss account (Net profit) 7425

82575

Interpretation – As per the above table prepare only two months September and October, 2018.

Fixed cost no changes in these months, it is stable. After deducting depreciation net assets

remaining 55800 and Stocks calculation of two months. Other assets increasing from past

months and bank & cash amount changes in September and October. Accruals deducting from

past months and 2500 amount less from short terms loans. After preparation of Profit and loss

account getting net loss and it is less from share capital. Net current assets and capital and

reserves has equal balance so it is balancing.

Cash Budget

Cash budget is a planning tool used by individuals and companies for expected cash

receipts and spending during the period. These cash inflows and outflows include loans receipt

and payments, revenues collected and expenses paid (Penn, 2011). A cash budget is an estimated

projection of the company's cash position in the future.

Management mostly create cash budget after the sales, capital expenditure, and purchases

already made. These budgets need to be made for cash budget in order to accurately estimate

how cash will be affected during the period.

3

Accounts Payable 17200

Short term loans 12500

Accruals 2176

Corporation tax payable 5000

36876

Net Current Assets 157375

Total assets less current Liabilities 213175

Long term Loans 130600

Net Assets 82575

Capital and reserves

Share Capital 90000

Profit and Loss account (Net profit) 7425

82575

Interpretation – As per the above table prepare only two months September and October, 2018.

Fixed cost no changes in these months, it is stable. After deducting depreciation net assets

remaining 55800 and Stocks calculation of two months. Other assets increasing from past

months and bank & cash amount changes in September and October. Accruals deducting from

past months and 2500 amount less from short terms loans. After preparation of Profit and loss

account getting net loss and it is less from share capital. Net current assets and capital and

reserves has equal balance so it is balancing.

Cash Budget

Cash budget is a planning tool used by individuals and companies for expected cash

receipts and spending during the period. These cash inflows and outflows include loans receipt

and payments, revenues collected and expenses paid (Penn, 2011). A cash budget is an estimated

projection of the company's cash position in the future.

Management mostly create cash budget after the sales, capital expenditure, and purchases

already made. These budgets need to be made for cash budget in order to accurately estimate

how cash will be affected during the period.

3

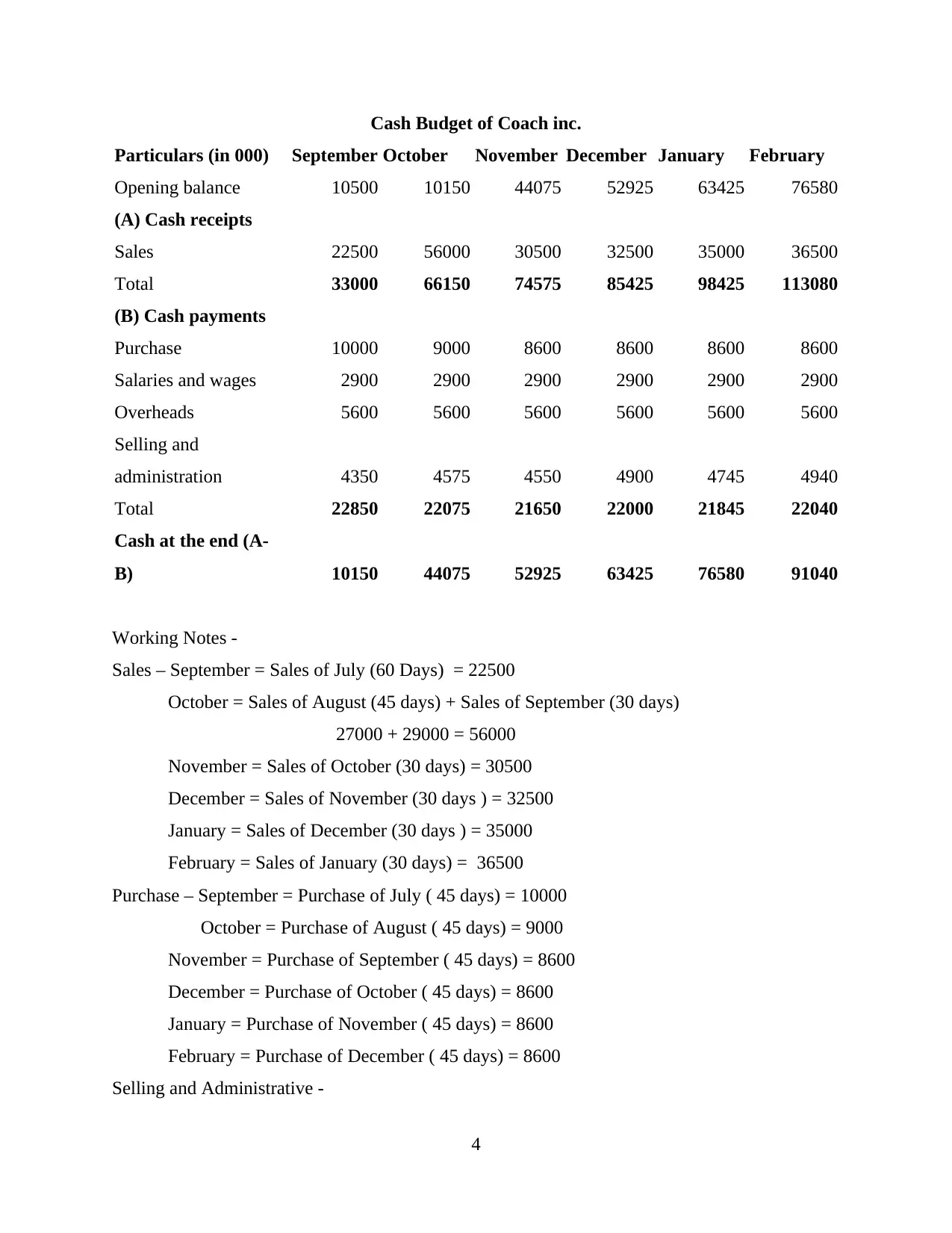

Cash Budget of Coach inc.

Particulars (in 000) September October November December January February

Opening balance 10500 10150 44075 52925 63425 76580

(A) Cash receipts

Sales 22500 56000 30500 32500 35000 36500

Total 33000 66150 74575 85425 98425 113080

(B) Cash payments

Purchase 10000 9000 8600 8600 8600 8600

Salaries and wages 2900 2900 2900 2900 2900 2900

Overheads 5600 5600 5600 5600 5600 5600

Selling and

administration 4350 4575 4550 4900 4745 4940

Total 22850 22075 21650 22000 21845 22040

Cash at the end (A-

B) 10150 44075 52925 63425 76580 91040

Working Notes -

Sales – September = Sales of July (60 Days) = 22500

October = Sales of August (45 days) + Sales of September (30 days)

27000 + 29000 = 56000

November = Sales of October (30 days) = 30500

December = Sales of November (30 days ) = 32500

January = Sales of December (30 days ) = 35000

February = Sales of January (30 days) = 36500

Purchase – September = Purchase of July ( 45 days) = 10000

October = Purchase of August ( 45 days) = 9000

November = Purchase of September ( 45 days) = 8600

December = Purchase of October ( 45 days) = 8600

January = Purchase of November ( 45 days) = 8600

February = Purchase of December ( 45 days) = 8600

Selling and Administrative -

4

Particulars (in 000) September October November December January February

Opening balance 10500 10150 44075 52925 63425 76580

(A) Cash receipts

Sales 22500 56000 30500 32500 35000 36500

Total 33000 66150 74575 85425 98425 113080

(B) Cash payments

Purchase 10000 9000 8600 8600 8600 8600

Salaries and wages 2900 2900 2900 2900 2900 2900

Overheads 5600 5600 5600 5600 5600 5600

Selling and

administration 4350 4575 4550 4900 4745 4940

Total 22850 22075 21650 22000 21845 22040

Cash at the end (A-

B) 10150 44075 52925 63425 76580 91040

Working Notes -

Sales – September = Sales of July (60 Days) = 22500

October = Sales of August (45 days) + Sales of September (30 days)

27000 + 29000 = 56000

November = Sales of October (30 days) = 30500

December = Sales of November (30 days ) = 32500

January = Sales of December (30 days ) = 35000

February = Sales of January (30 days) = 36500

Purchase – September = Purchase of July ( 45 days) = 10000

October = Purchase of August ( 45 days) = 9000

November = Purchase of September ( 45 days) = 8600

December = Purchase of October ( 45 days) = 8600

January = Purchase of November ( 45 days) = 8600

February = Purchase of December ( 45 days) = 8600

Selling and Administrative -

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

September = 15% of Sales = 29000*15% = 4350

October = 15% of Sales = 30500*15% = 4575

November = 14% of Sales = 32500*14% = 4550

December = 14% of Sales = 35000*14% = 4900

January = 13% of Sales = 36500*13% = 4745

February = 13% of Sales = 38000*13% = 4940

Interpretation - As per the above table prepare six months cash budgets from September to

February 2019 and taking opening balance (September) as closing cash balance of August. The

bend balances of cash for September was calculated 10150, for October 44075, for November

52925, for December 63425, For January 76580, for February 91040. It's divided in two heads

first cash receipts in this section taking those item that helping in cash receipts like sales that are

taking 60 days credit controller, after that it reduce from august (45 days), in September, 31 it

will 30 days.

In cash payment head including all Purchase taking on the basis of 45 days credit term

period so in September taking July's purchase amount. Selling and administrative calculated on

the basis of sales percentage. In September and October taking 15% of sales, in November and

December taking 14% of sales and in January and February taking 13% of sales. Overhead,

salaries and wages related to incurred month. After total of cash receipts and cash payments, less

amount (A-B). Now getting closing balance of cash at the end of the month, it is opening balance

of next month.

Cash flows

A cash flow statement is the net amount of cash that an entity receives and pay out during

a period of time. A positive level of cash flow must be retained for an entity to continue in

business (Cash flow 2018). The time period over which cash flow is tracked is usually a standard

reporting period, such as a quarter, month, or year. Cash inflows come from the following

sources:

Operations – This is cash paid by customers for services or goods provided by the entity.

Financing activities – An illustration is debt obtain by the entity.

Investment Activities – An illustration is the profit on invested fund.

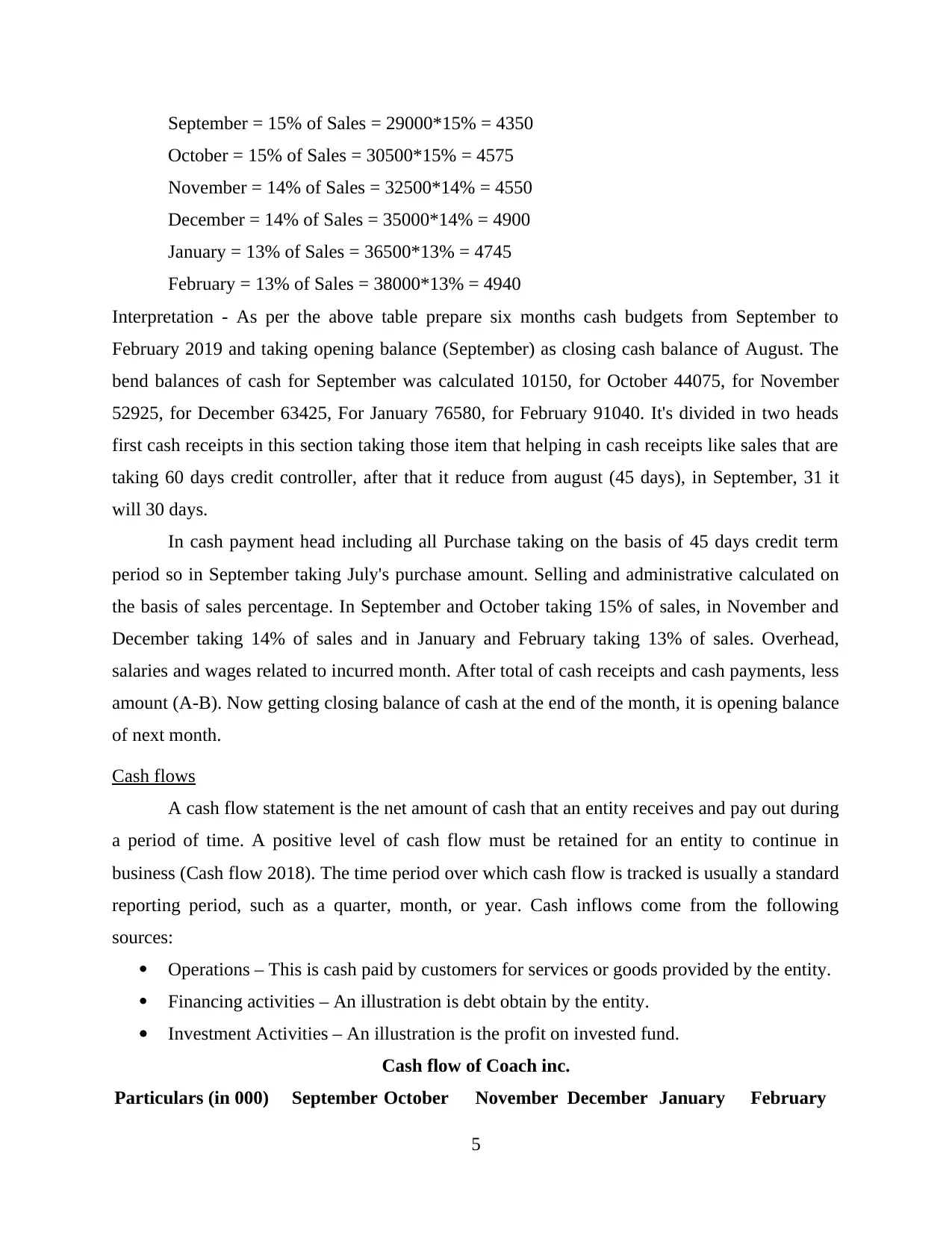

Cash flow of Coach inc.

Particulars (in 000) September October November December January February

5

October = 15% of Sales = 30500*15% = 4575

November = 14% of Sales = 32500*14% = 4550

December = 14% of Sales = 35000*14% = 4900

January = 13% of Sales = 36500*13% = 4745

February = 13% of Sales = 38000*13% = 4940

Interpretation - As per the above table prepare six months cash budgets from September to

February 2019 and taking opening balance (September) as closing cash balance of August. The

bend balances of cash for September was calculated 10150, for October 44075, for November

52925, for December 63425, For January 76580, for February 91040. It's divided in two heads

first cash receipts in this section taking those item that helping in cash receipts like sales that are

taking 60 days credit controller, after that it reduce from august (45 days), in September, 31 it

will 30 days.

In cash payment head including all Purchase taking on the basis of 45 days credit term

period so in September taking July's purchase amount. Selling and administrative calculated on

the basis of sales percentage. In September and October taking 15% of sales, in November and

December taking 14% of sales and in January and February taking 13% of sales. Overhead,

salaries and wages related to incurred month. After total of cash receipts and cash payments, less

amount (A-B). Now getting closing balance of cash at the end of the month, it is opening balance

of next month.

Cash flows

A cash flow statement is the net amount of cash that an entity receives and pay out during

a period of time. A positive level of cash flow must be retained for an entity to continue in

business (Cash flow 2018). The time period over which cash flow is tracked is usually a standard

reporting period, such as a quarter, month, or year. Cash inflows come from the following

sources:

Operations – This is cash paid by customers for services or goods provided by the entity.

Financing activities – An illustration is debt obtain by the entity.

Investment Activities – An illustration is the profit on invested fund.

Cash flow of Coach inc.

Particulars (in 000) September October November December January February

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

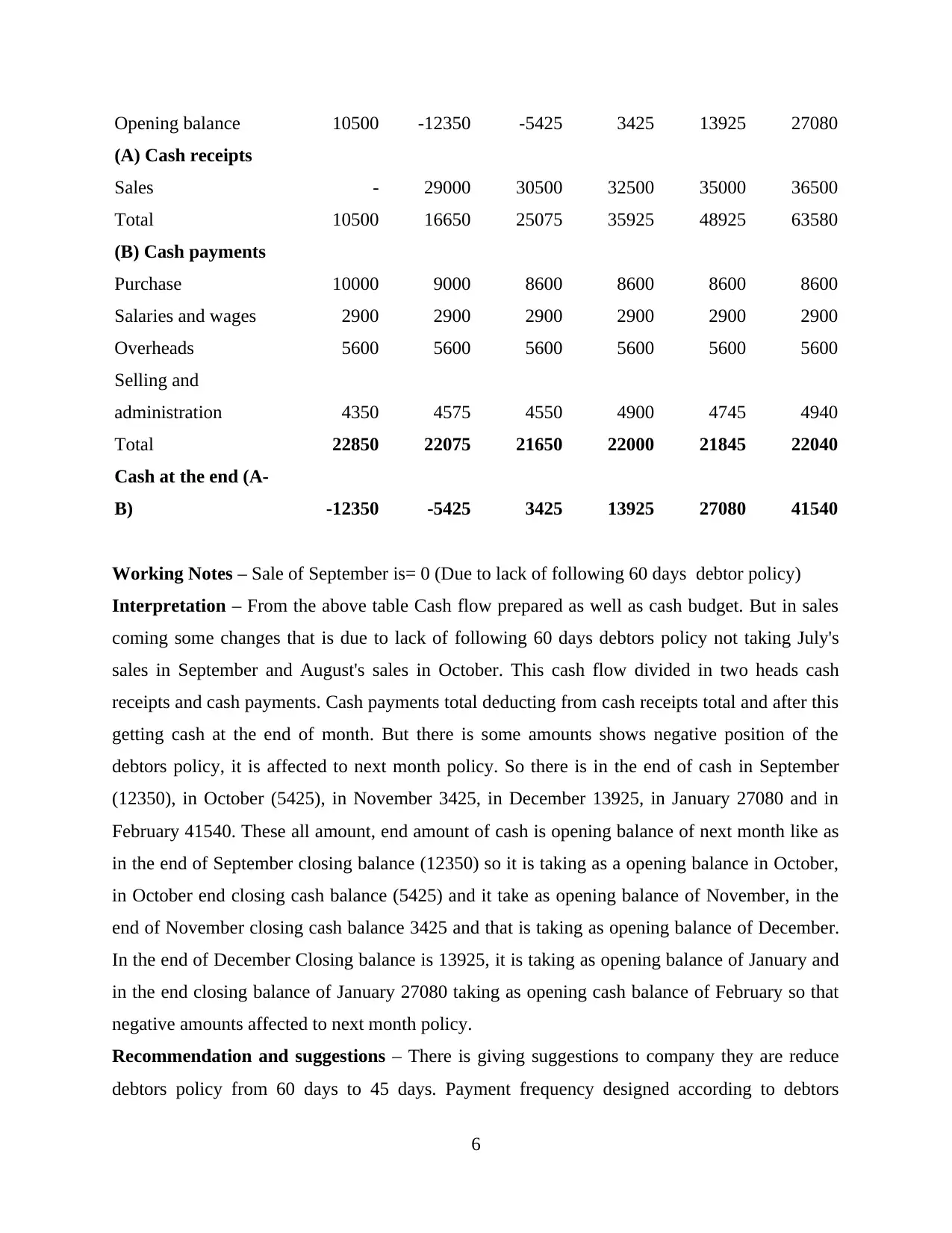

Opening balance 10500 -12350 -5425 3425 13925 27080

(A) Cash receipts

Sales - 29000 30500 32500 35000 36500

Total 10500 16650 25075 35925 48925 63580

(B) Cash payments

Purchase 10000 9000 8600 8600 8600 8600

Salaries and wages 2900 2900 2900 2900 2900 2900

Overheads 5600 5600 5600 5600 5600 5600

Selling and

administration 4350 4575 4550 4900 4745 4940

Total 22850 22075 21650 22000 21845 22040

Cash at the end (A-

B) -12350 -5425 3425 13925 27080 41540

Working Notes – Sale of September is= 0 (Due to lack of following 60 days debtor policy)

Interpretation – From the above table Cash flow prepared as well as cash budget. But in sales

coming some changes that is due to lack of following 60 days debtors policy not taking July's

sales in September and August's sales in October. This cash flow divided in two heads cash

receipts and cash payments. Cash payments total deducting from cash receipts total and after this

getting cash at the end of month. But there is some amounts shows negative position of the

debtors policy, it is affected to next month policy. So there is in the end of cash in September

(12350), in October (5425), in November 3425, in December 13925, in January 27080 and in

February 41540. These all amount, end amount of cash is opening balance of next month like as

in the end of September closing balance (12350) so it is taking as a opening balance in October,

in October end closing cash balance (5425) and it take as opening balance of November, in the

end of November closing cash balance 3425 and that is taking as opening balance of December.

In the end of December Closing balance is 13925, it is taking as opening balance of January and

in the end closing balance of January 27080 taking as opening cash balance of February so that

negative amounts affected to next month policy.

Recommendation and suggestions – There is giving suggestions to company they are reduce

debtors policy from 60 days to 45 days. Payment frequency designed according to debtors

6

(A) Cash receipts

Sales - 29000 30500 32500 35000 36500

Total 10500 16650 25075 35925 48925 63580

(B) Cash payments

Purchase 10000 9000 8600 8600 8600 8600

Salaries and wages 2900 2900 2900 2900 2900 2900

Overheads 5600 5600 5600 5600 5600 5600

Selling and

administration 4350 4575 4550 4900 4745 4940

Total 22850 22075 21650 22000 21845 22040

Cash at the end (A-

B) -12350 -5425 3425 13925 27080 41540

Working Notes – Sale of September is= 0 (Due to lack of following 60 days debtor policy)

Interpretation – From the above table Cash flow prepared as well as cash budget. But in sales

coming some changes that is due to lack of following 60 days debtors policy not taking July's

sales in September and August's sales in October. This cash flow divided in two heads cash

receipts and cash payments. Cash payments total deducting from cash receipts total and after this

getting cash at the end of month. But there is some amounts shows negative position of the

debtors policy, it is affected to next month policy. So there is in the end of cash in September

(12350), in October (5425), in November 3425, in December 13925, in January 27080 and in

February 41540. These all amount, end amount of cash is opening balance of next month like as

in the end of September closing balance (12350) so it is taking as a opening balance in October,

in October end closing cash balance (5425) and it take as opening balance of November, in the

end of November closing cash balance 3425 and that is taking as opening balance of December.

In the end of December Closing balance is 13925, it is taking as opening balance of January and

in the end closing balance of January 27080 taking as opening cash balance of February so that

negative amounts affected to next month policy.

Recommendation and suggestions – There is giving suggestions to company they are reduce

debtors policy from 60 days to 45 days. Payment frequency designed according to debtors

6

because each debtor have rules and regulations for payment and they are applied on payment

system. Accuracy is major fact for the debtor because if in company not applying accuracy so it

is affected to debtors collection (Bhandari and Iyer, 2013). Credibility, Debtors credit policy

decided according to credit score, if credit score is good so giving loan easily but it's not good so

not giving easily loan to debtors, duration also set according to credit score because it's totally

depended on credit score, collection period should also reduce of debtors otherwise it is always

affected to debtors policy (Cunha, 2014).

Report for the managing director

After analysis results come out that company have to reduce debtors collection policy. In

Starting they applying 60 days collection period but they were not getting on time and not paying

suppliers on time. So in September they reduce collection period from 60 to 45 days but it also

not effected to collection period. So it reduce 30 days and stay that time period for debtors

because debtors not paying on time (Larkin, 2013). If giving more days to debtors so they taking

more time for paying and cash balance fluctuated time to time and that's not good for company.

So for stable cash balance collect amounts on time, and paying to creditors on time.

It also affected to cash flow factors like monetary or non monetary because in cash flow

calculated operating, investing and financial activities. So these activities effected by this policy

because mostly in investing activities calculated on the basis of collection period and payable

period. Non monetary factors effected due to relations between debtors and customers and

services provided by company (Attanasio, and Lechene, 2014).

CONCLUSION

It is concluded that managerial finance important for business because it's using for

financial statement. It is using for apply techniques on financial statements. In financial

statement including profit and loss account, balance sheet, also including cash budget, cash

flows. Cash budgets shows cash information in month starting and month ending, and cash flows

shows effect collection period policy. Coach inc. prepare financial statements for two months of

September and October like balance sheet for actual position of company. Cash budget for

ending and starting cash balance, cash flow for show effect collection period policy and profit &

loss account for calculation net profit and loss. So these accounts prepare by managerial finance

techniques.

7

system. Accuracy is major fact for the debtor because if in company not applying accuracy so it

is affected to debtors collection (Bhandari and Iyer, 2013). Credibility, Debtors credit policy

decided according to credit score, if credit score is good so giving loan easily but it's not good so

not giving easily loan to debtors, duration also set according to credit score because it's totally

depended on credit score, collection period should also reduce of debtors otherwise it is always

affected to debtors policy (Cunha, 2014).

Report for the managing director

After analysis results come out that company have to reduce debtors collection policy. In

Starting they applying 60 days collection period but they were not getting on time and not paying

suppliers on time. So in September they reduce collection period from 60 to 45 days but it also

not effected to collection period. So it reduce 30 days and stay that time period for debtors

because debtors not paying on time (Larkin, 2013). If giving more days to debtors so they taking

more time for paying and cash balance fluctuated time to time and that's not good for company.

So for stable cash balance collect amounts on time, and paying to creditors on time.

It also affected to cash flow factors like monetary or non monetary because in cash flow

calculated operating, investing and financial activities. So these activities effected by this policy

because mostly in investing activities calculated on the basis of collection period and payable

period. Non monetary factors effected due to relations between debtors and customers and

services provided by company (Attanasio, and Lechene, 2014).

CONCLUSION

It is concluded that managerial finance important for business because it's using for

financial statement. It is using for apply techniques on financial statements. In financial

statement including profit and loss account, balance sheet, also including cash budget, cash

flows. Cash budgets shows cash information in month starting and month ending, and cash flows

shows effect collection period policy. Coach inc. prepare financial statements for two months of

September and October like balance sheet for actual position of company. Cash budget for

ending and starting cash balance, cash flow for show effect collection period policy and profit &

loss account for calculation net profit and loss. So these accounts prepare by managerial finance

techniques.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

Books and journal

Alhassan, A.L., 2015. Income diversification and bank efficiency in an emerging market.

Managerial Finance. 41(12). pp.1318-1335.

Nguyen, T.P.T. and Nghiem, S.H., 2015. The interrelationships among default risk, capital ratio

and efficiency: evidence from Indian banks. Managerial Finance. 41(5). pp.507-525.

Ahangar, R.G., 2011. The relationship between intellectual capital and financial performance: An

empirical investigation in an Iranian company. African journal of business

management. 5(1). pp.88-95.

Penn, H., 2011. Gambling on the market: The role of for-profit provision in early childhood

education and care. Journal of Early Childhood Research. 9(2). pp.150-161.

Bhandari, S.B. and Iyer, R., 2013. Predicting business failure using cash flow statement based

measures. Managerial Finance. 39(7). pp.667-676.

Larkin, Y., 2013. Brand perception, cash flow stability, and financial policy. Journal of Financial

Economics. 110(1), pp.232-253.

Attanasio, O.P. and Lechene, V., 2014. Efficient responses to targeted cash transfers. Journal of

Political Economy. 122(1). pp.178-222.

Cunha, J.M., 2014. Testing paternalism: Cash versus in-kind transfers. American Economic

Journal: Applied Economics. 6(2). pp.195-230.

Schrand, C.M. and Zechman, S.L., 2012. Executive overconfidence and the slippery slope to

financial misreporting. Journal of Accounting and Economics. 53(1-2), pp.311-329.

Papanikolaou, N.I. and Wolff, C.C., 2014. The role of on-and off-balance-sheet leverage of

banks in the late 2000s crisis. Journal of Financial Stability. 14. pp.3-22.

Online

Cash flow 2018. [Online] Avilable through;

<https://corporatefinanceinstitute.com/resources/knowledge/finance/cash-flow/>

8

Books and journal

Alhassan, A.L., 2015. Income diversification and bank efficiency in an emerging market.

Managerial Finance. 41(12). pp.1318-1335.

Nguyen, T.P.T. and Nghiem, S.H., 2015. The interrelationships among default risk, capital ratio

and efficiency: evidence from Indian banks. Managerial Finance. 41(5). pp.507-525.

Ahangar, R.G., 2011. The relationship between intellectual capital and financial performance: An

empirical investigation in an Iranian company. African journal of business

management. 5(1). pp.88-95.

Penn, H., 2011. Gambling on the market: The role of for-profit provision in early childhood

education and care. Journal of Early Childhood Research. 9(2). pp.150-161.

Bhandari, S.B. and Iyer, R., 2013. Predicting business failure using cash flow statement based

measures. Managerial Finance. 39(7). pp.667-676.

Larkin, Y., 2013. Brand perception, cash flow stability, and financial policy. Journal of Financial

Economics. 110(1), pp.232-253.

Attanasio, O.P. and Lechene, V., 2014. Efficient responses to targeted cash transfers. Journal of

Political Economy. 122(1). pp.178-222.

Cunha, J.M., 2014. Testing paternalism: Cash versus in-kind transfers. American Economic

Journal: Applied Economics. 6(2). pp.195-230.

Schrand, C.M. and Zechman, S.L., 2012. Executive overconfidence and the slippery slope to

financial misreporting. Journal of Accounting and Economics. 53(1-2), pp.311-329.

Papanikolaou, N.I. and Wolff, C.C., 2014. The role of on-and off-balance-sheet leverage of

banks in the late 2000s crisis. Journal of Financial Stability. 14. pp.3-22.

Online

Cash flow 2018. [Online] Avilable through;

<https://corporatefinanceinstitute.com/resources/knowledge/finance/cash-flow/>

8

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.