Managerial Finance Report: Ratio Analysis and Capital Budgeting

VerifiedAdded on 2022/12/30

|25

|3875

|83

Report

AI Summary

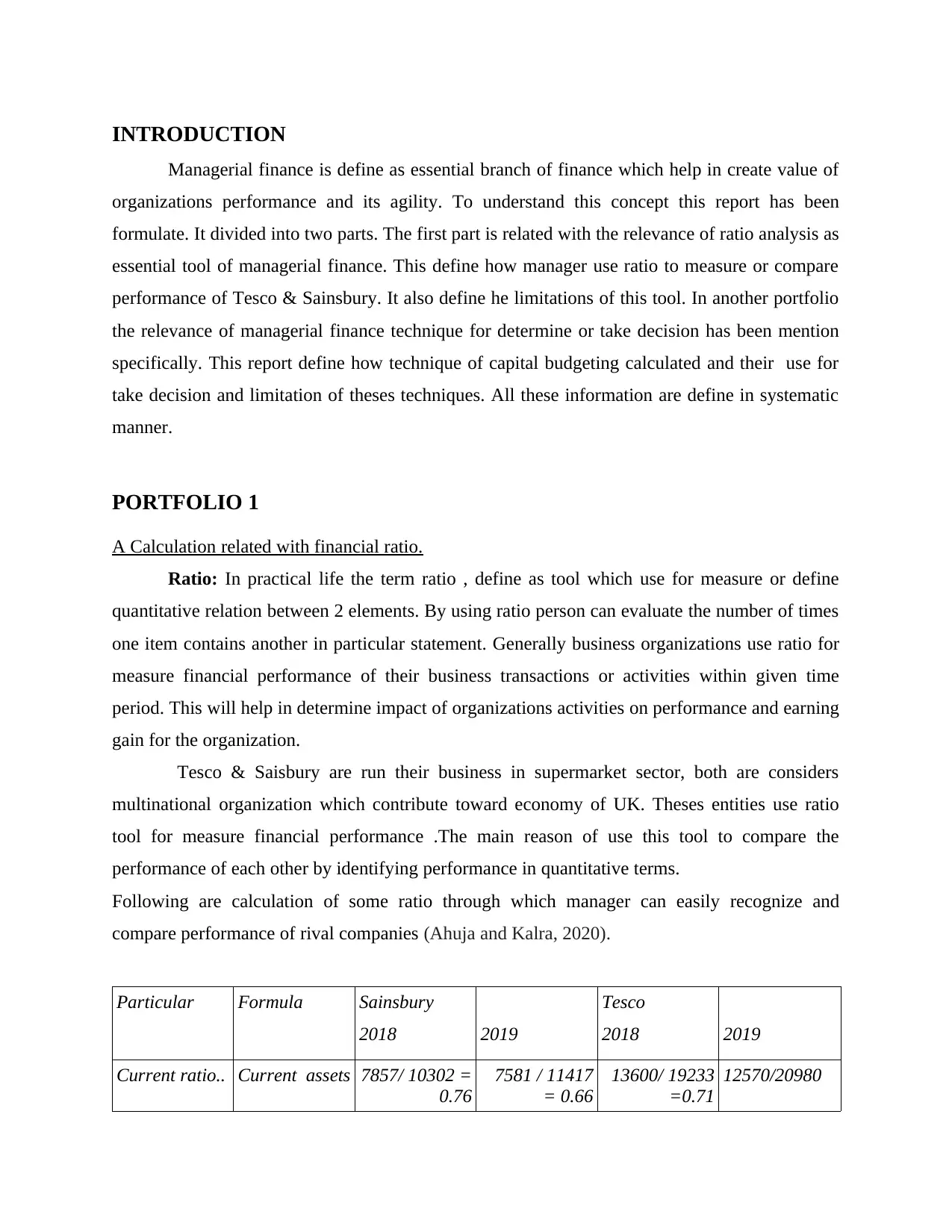

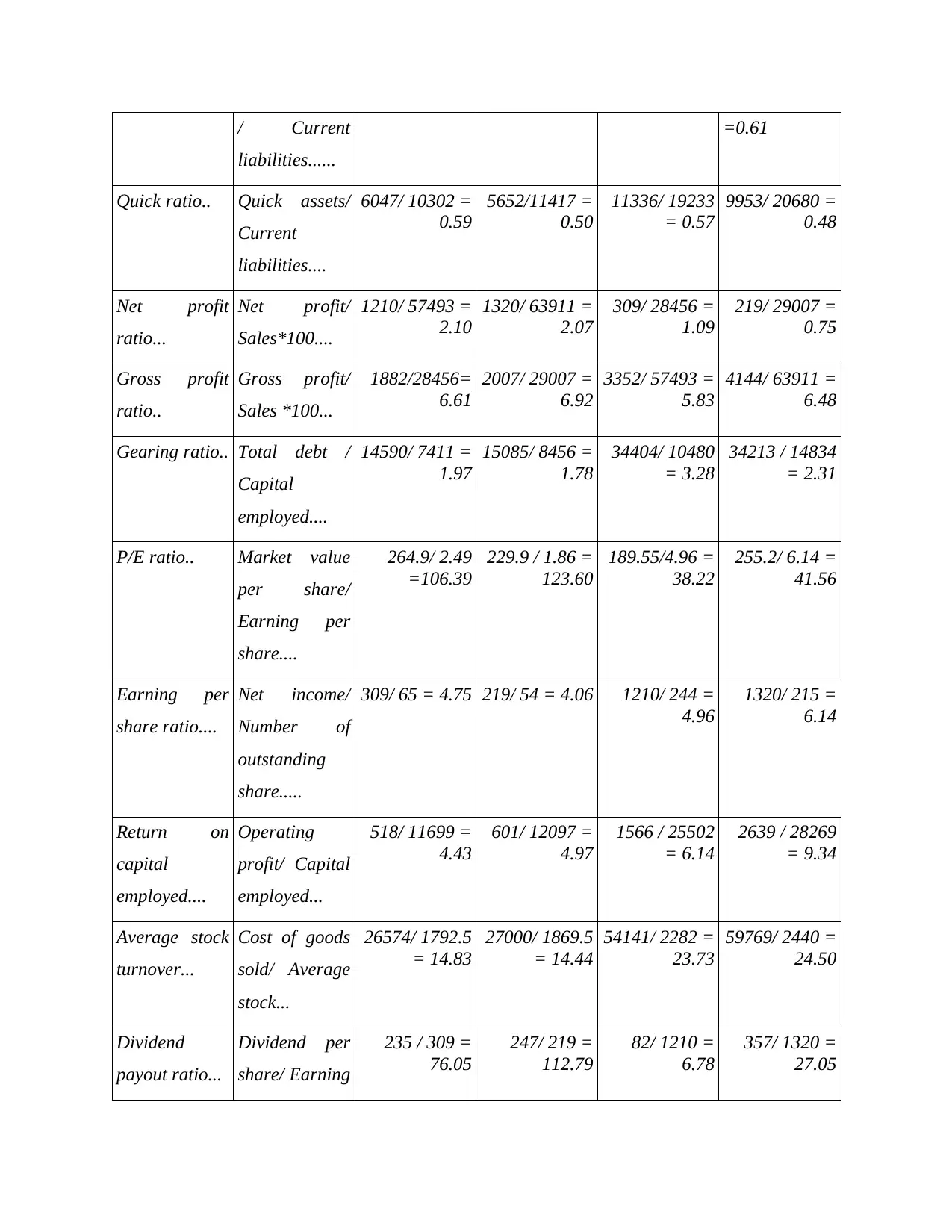

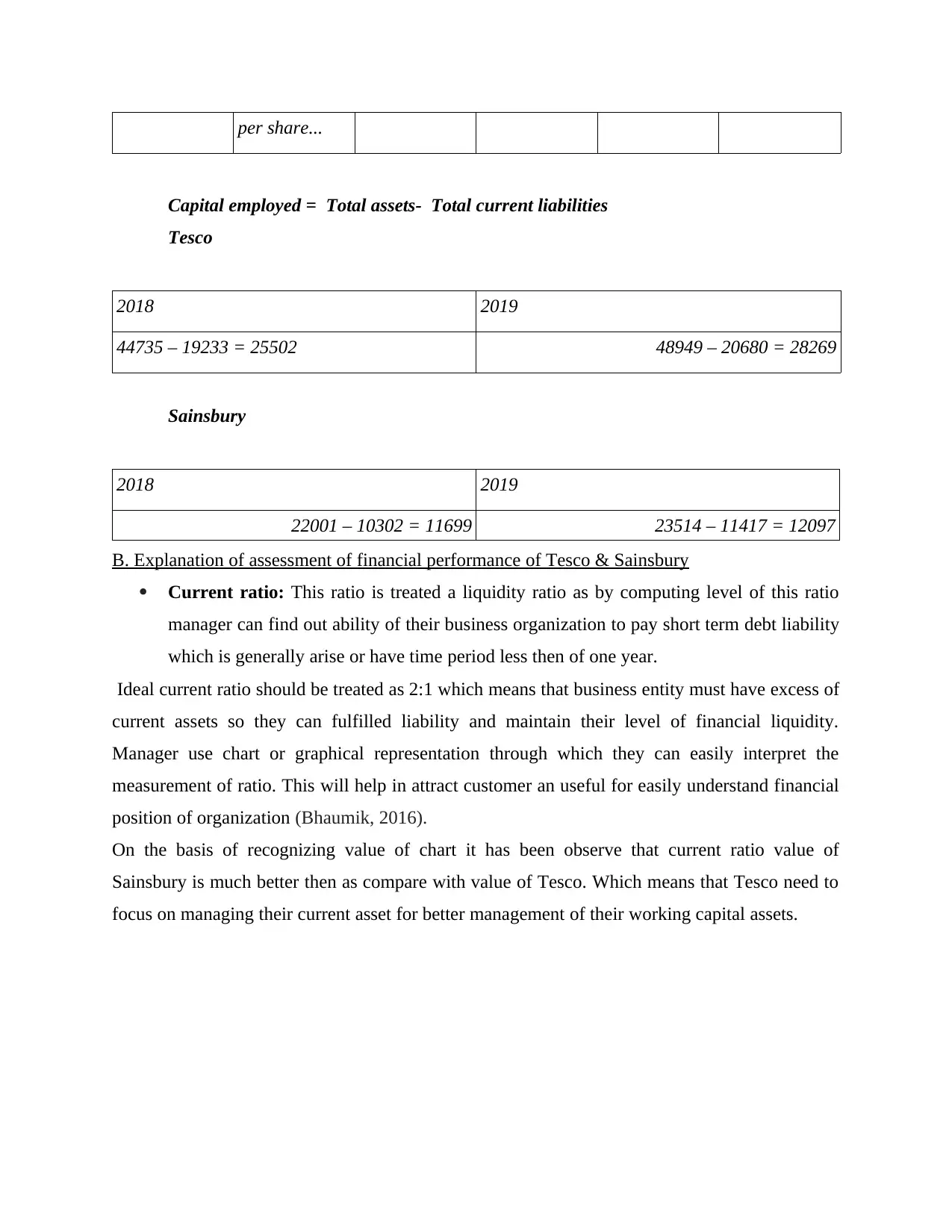

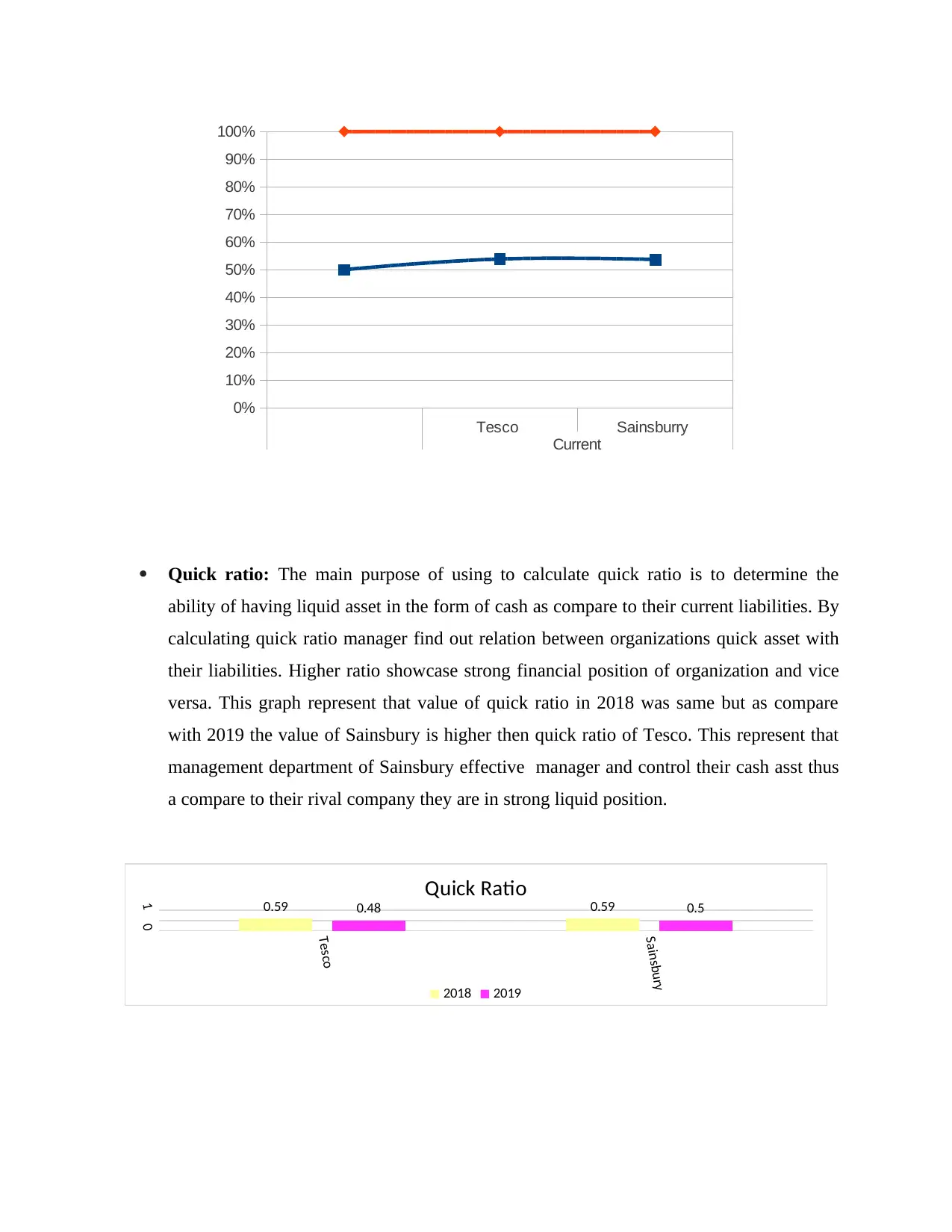

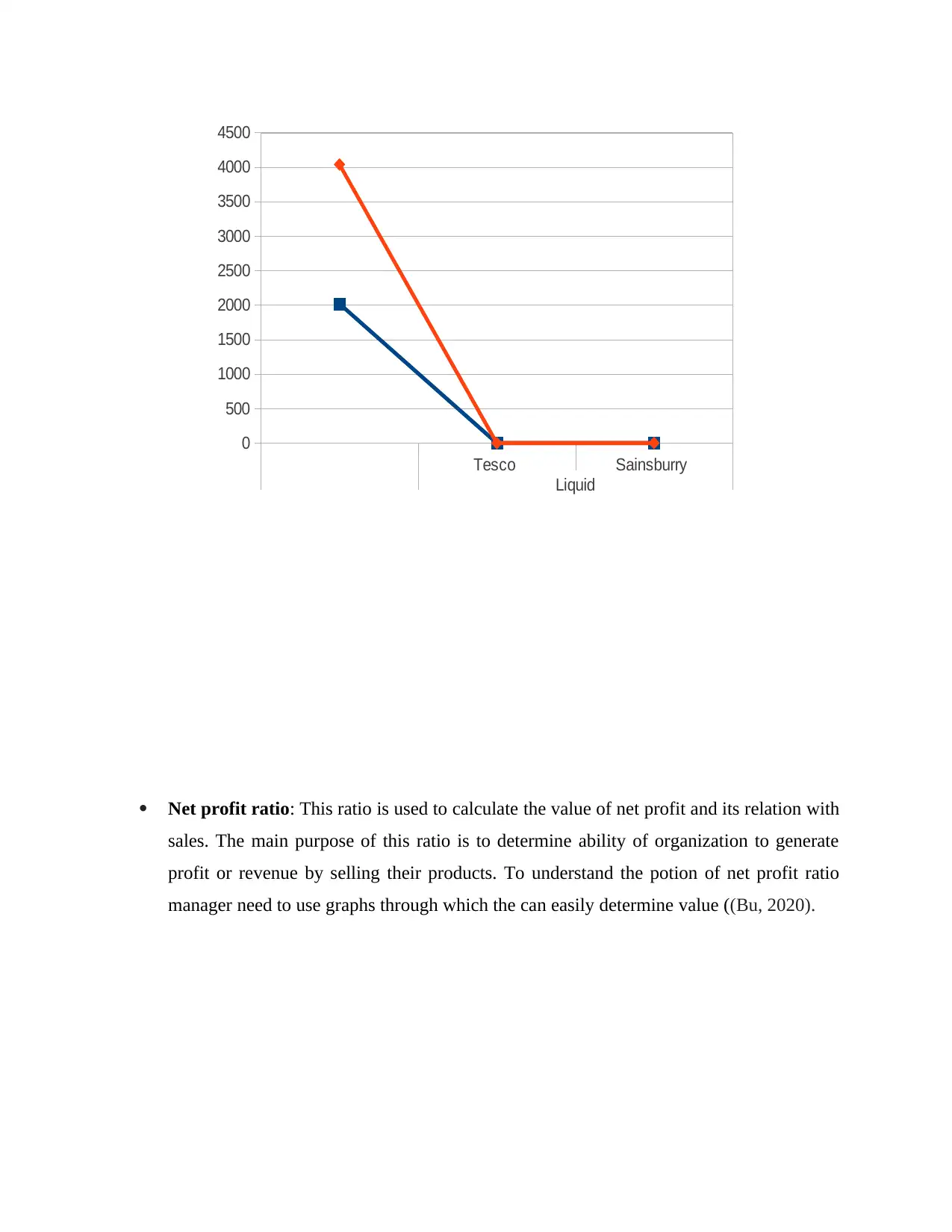

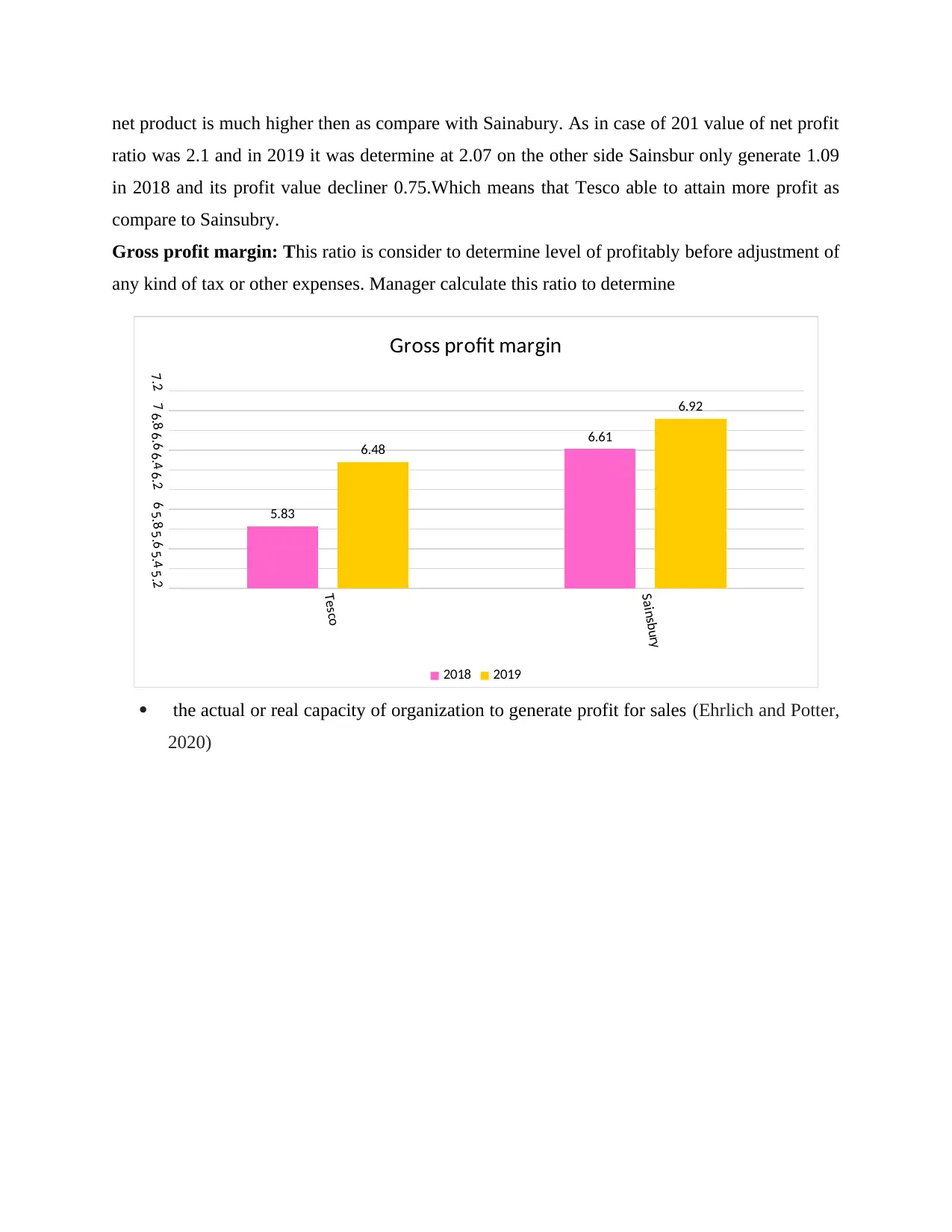

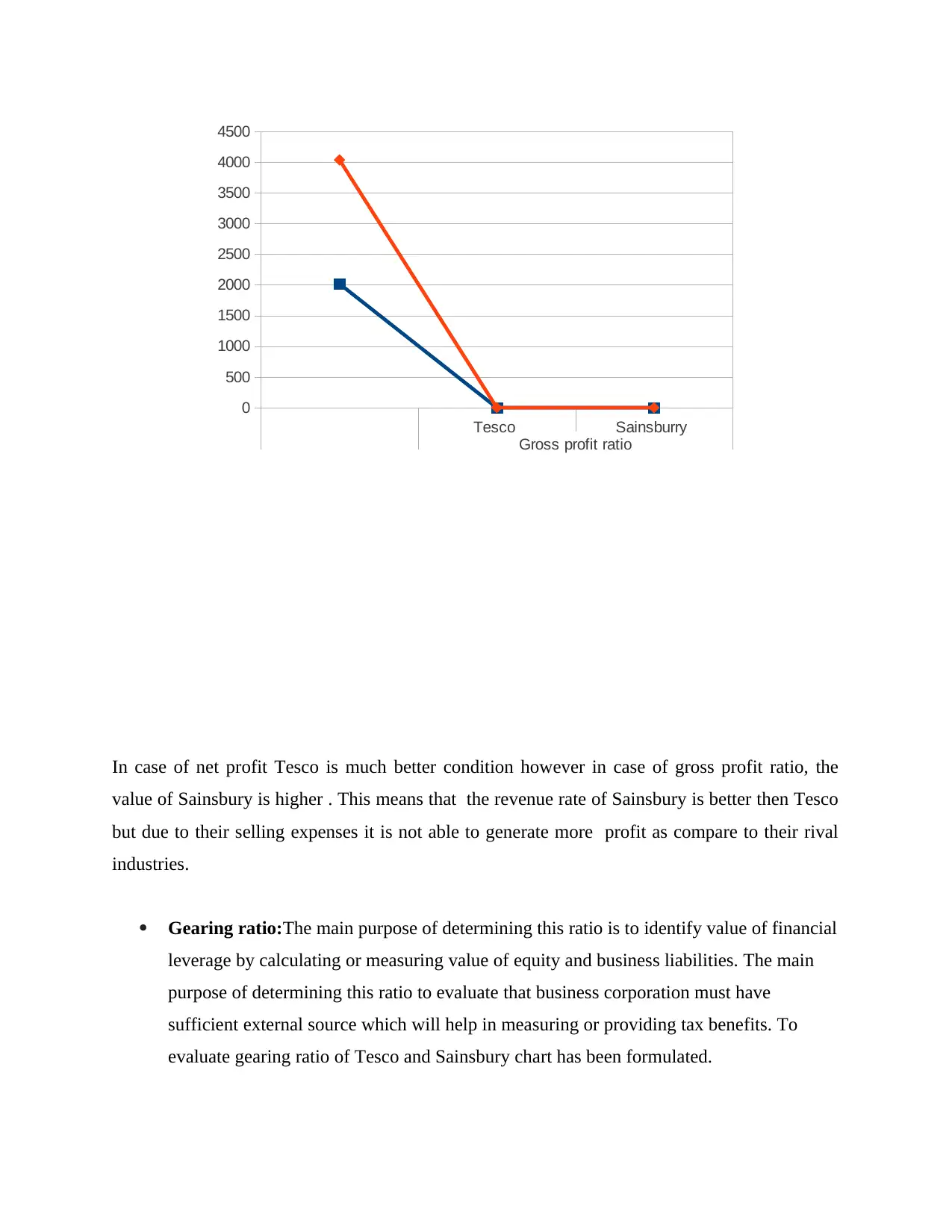

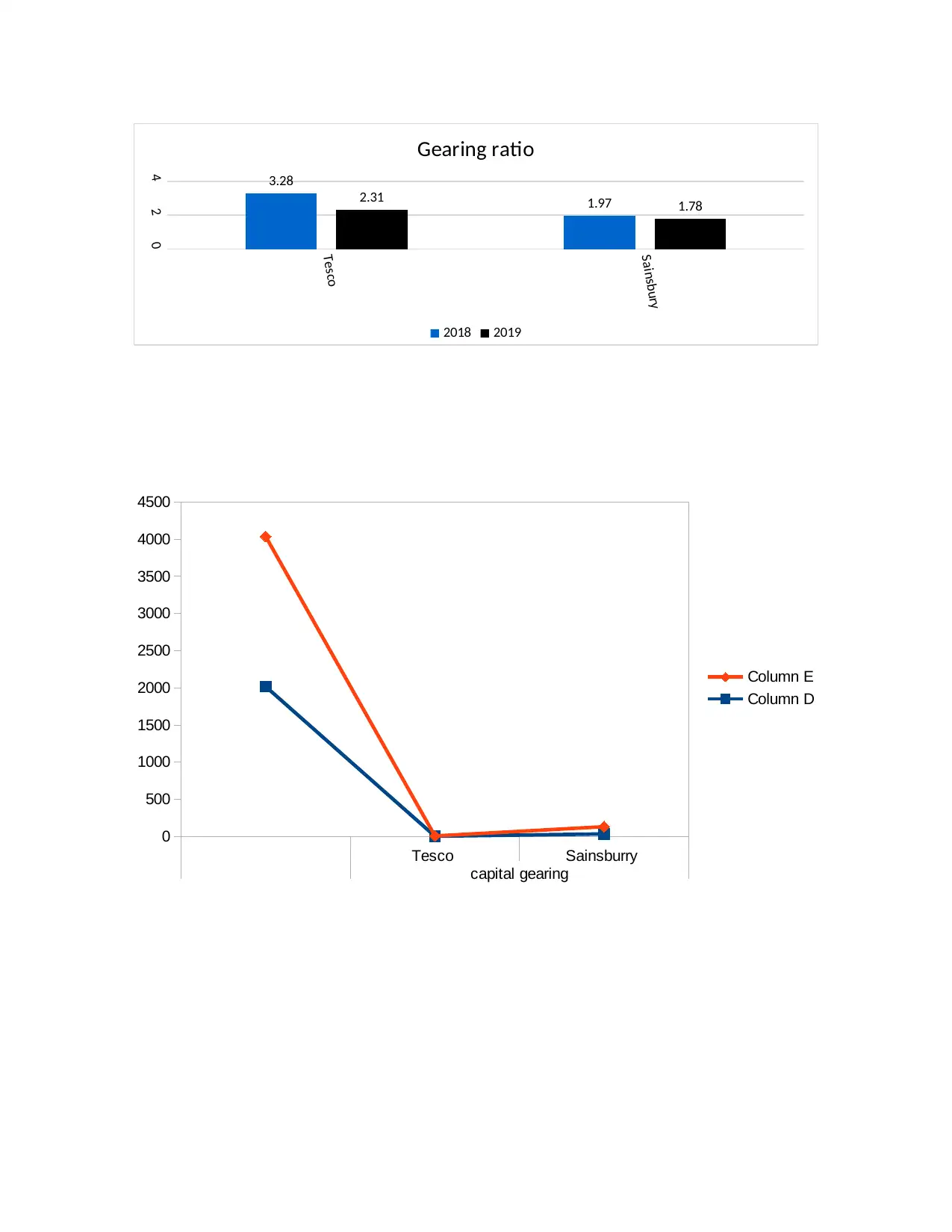

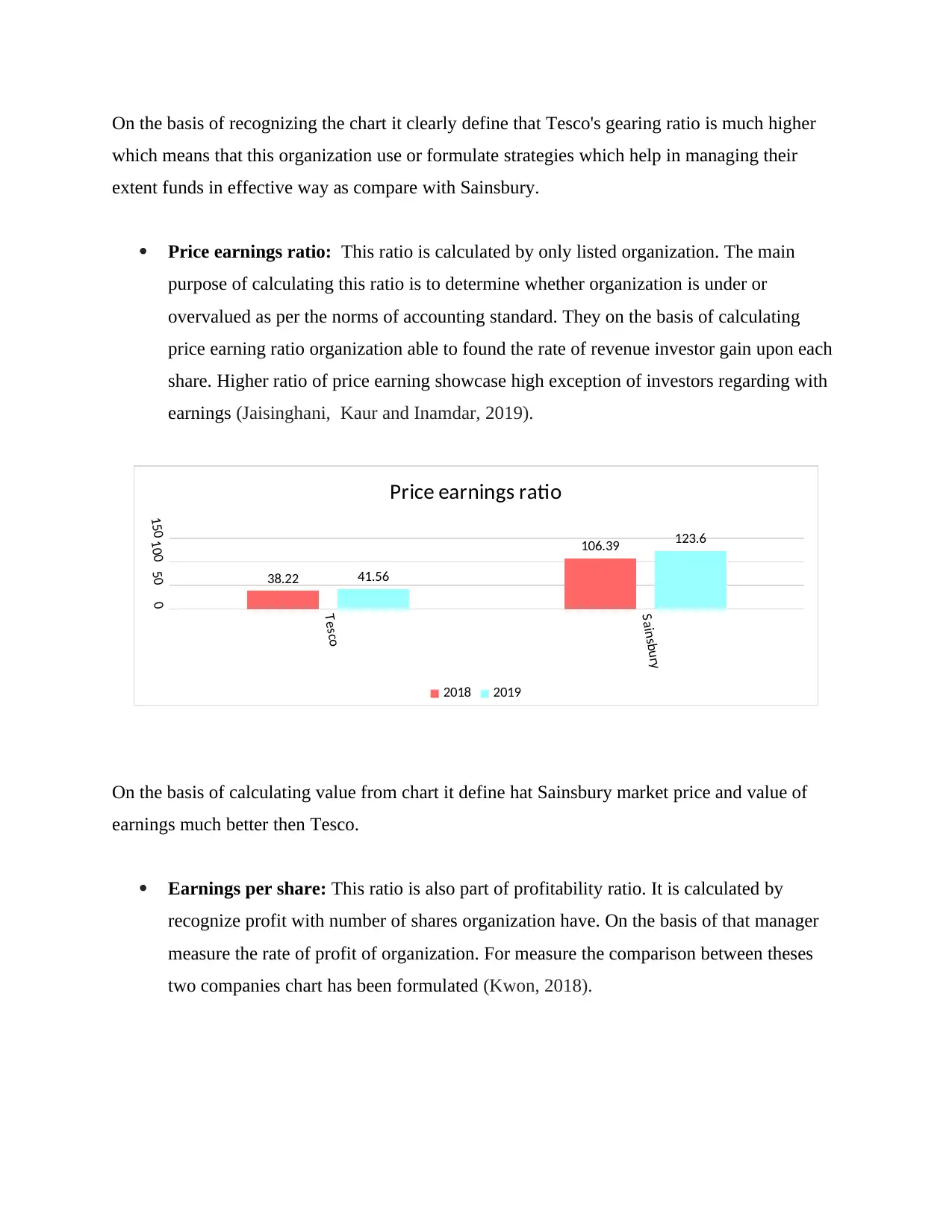

This report delves into the core concepts of managerial finance, presenting a comprehensive analysis of financial ratios and investment appraisal techniques. The report is divided into two portfolios, the first of which focuses on the application of ratio analysis to assess the financial performance of Tesco and Sainsbury, including calculations of current ratio, quick ratio, and profitability ratios. The second portfolio explores the use of various investment appraisal techniques for making investment decisions, including capital budgeting. The report also discusses the limitations of these techniques. The analysis includes detailed calculations, graphical representations, and interpretations of the financial data to provide a clear understanding of the financial positions of the companies and the effectiveness of the financial tools used. The report concludes with a synthesis of the key findings and implications for managerial decision-making, providing valuable insights for students of finance.

1 out of 25

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.