Managerial Finance Assignment: Forecasting and Financial Analysis

VerifiedAdded on 2020/05/08

|8

|1364

|38

Homework Assignment

AI Summary

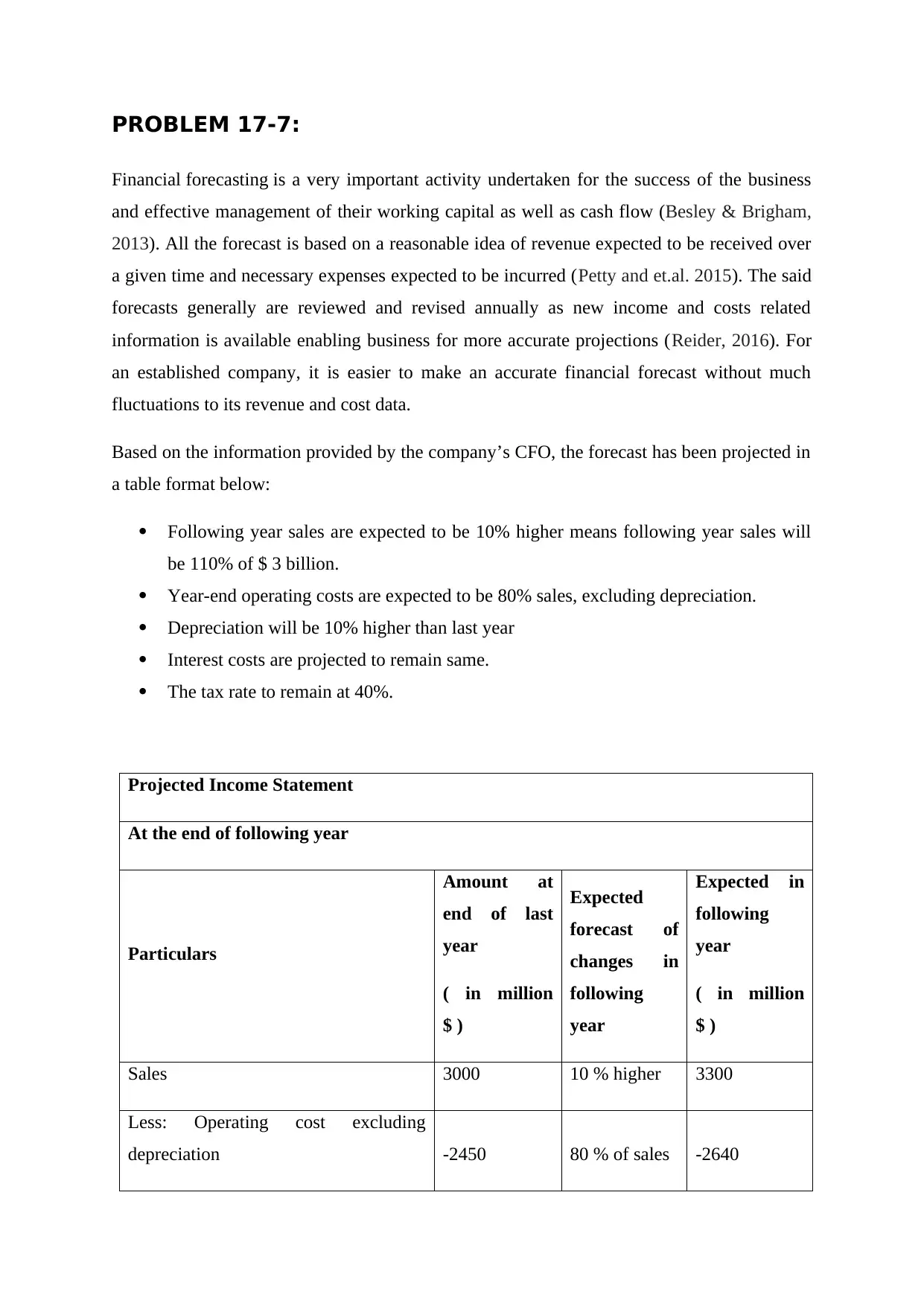

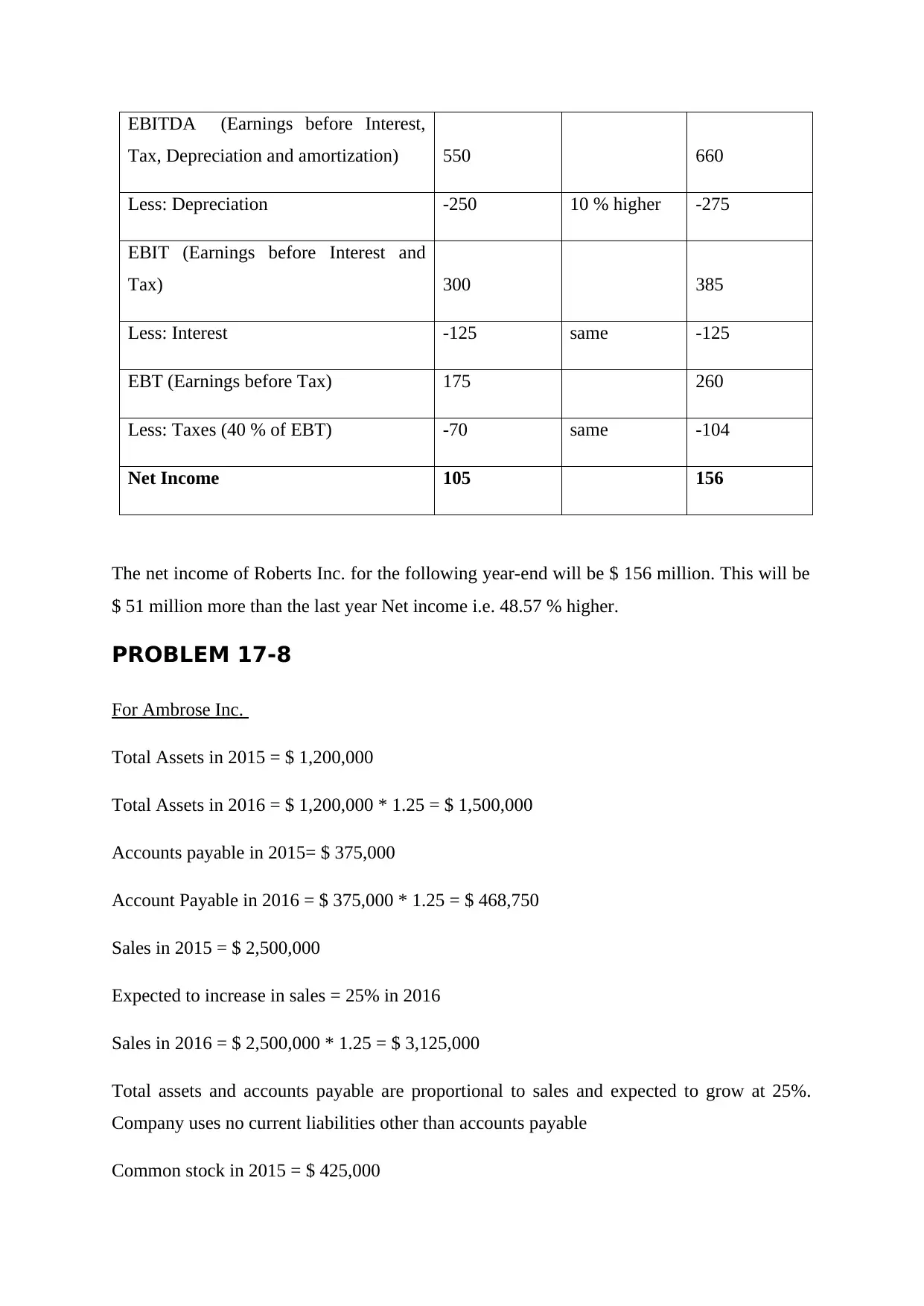

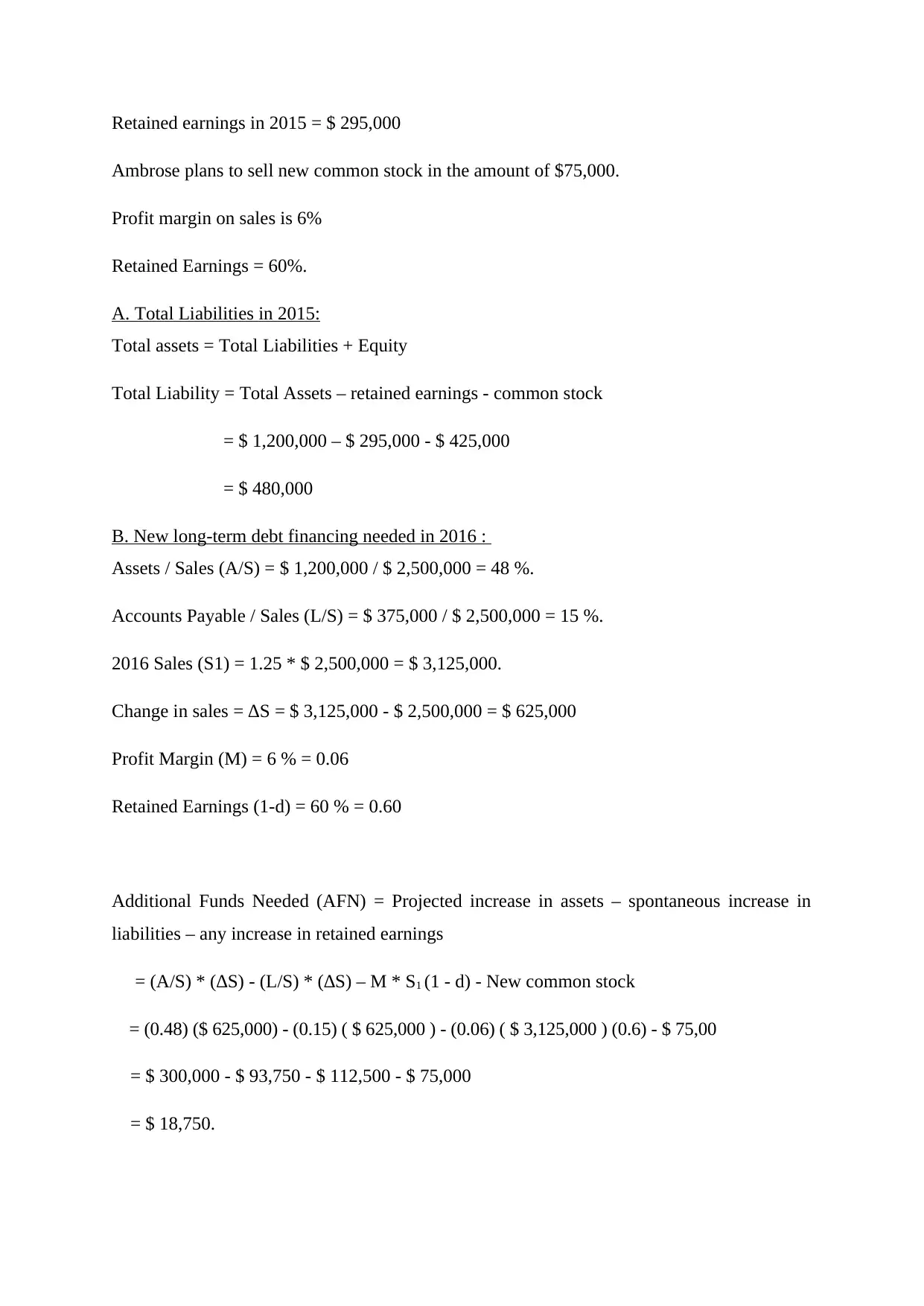

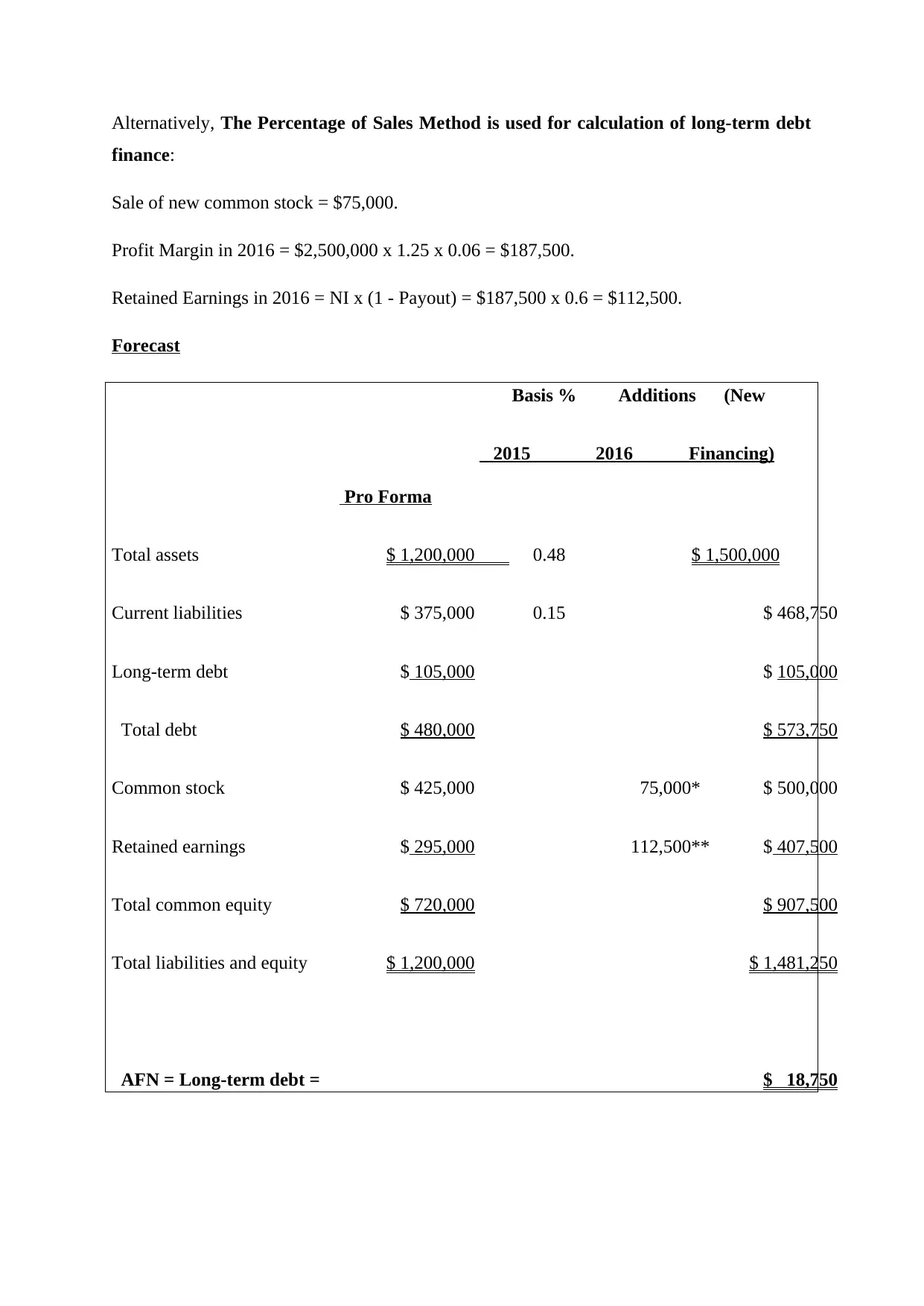

This managerial finance assignment presents solutions to two problems. Problem 17-7 focuses on financial forecasting for Roberts Inc., calculating net income based on projected sales and expenses. Problem 17-8 addresses Ambrose Inc., calculating total liabilities in 2015 and the new long-term debt financing needed in 2016. It utilizes the percentage of sales method and explores strategies to reduce debt financing, such as increasing sales, improving profitability, issuing right shares, and better inventory management. The solution includes detailed calculations, financial statement projections, and references to relevant finance literature.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.