Capital Budgeting & Investment Analysis: Managerial Finance Case

VerifiedAdded on 2023/06/10

|11

|1213

|305

Case Study

AI Summary

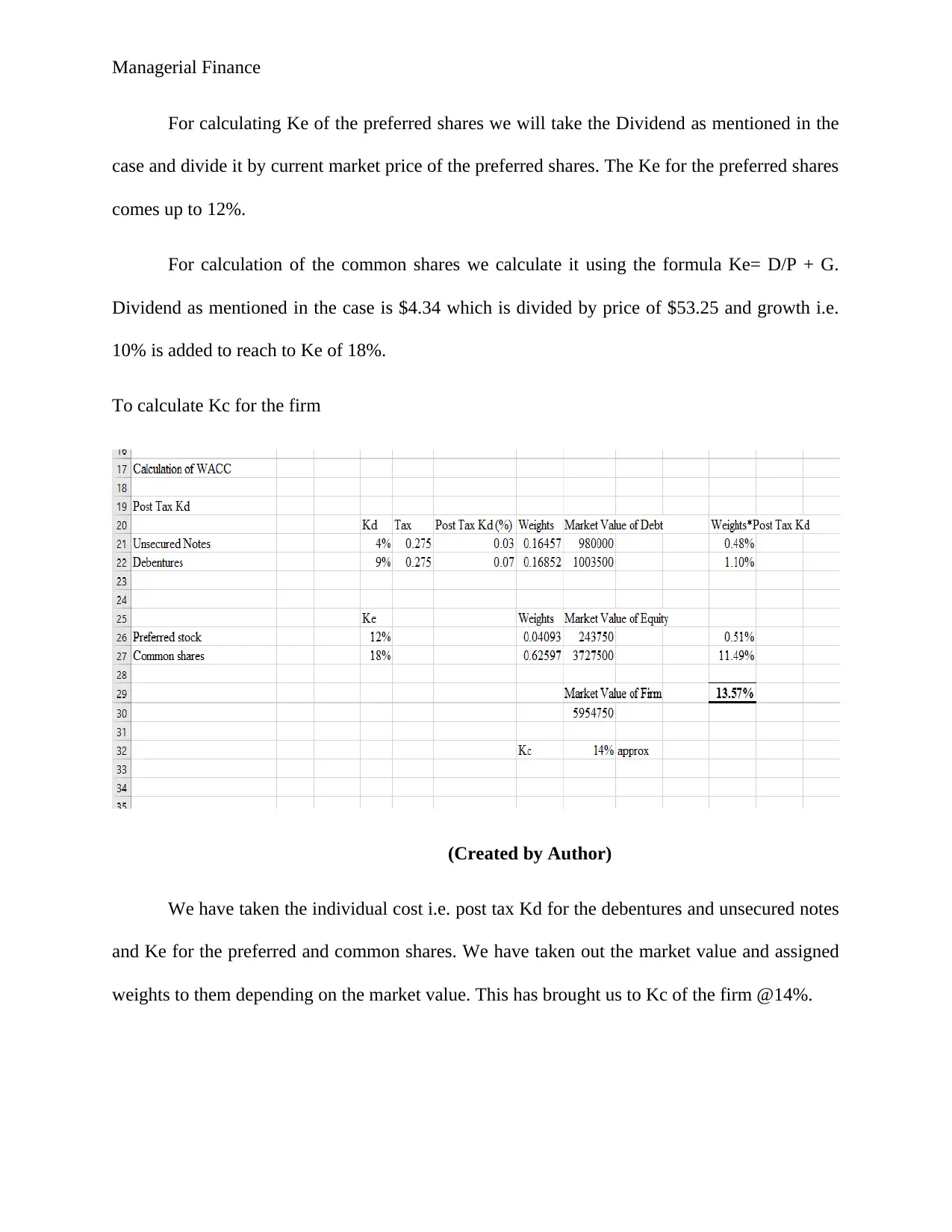

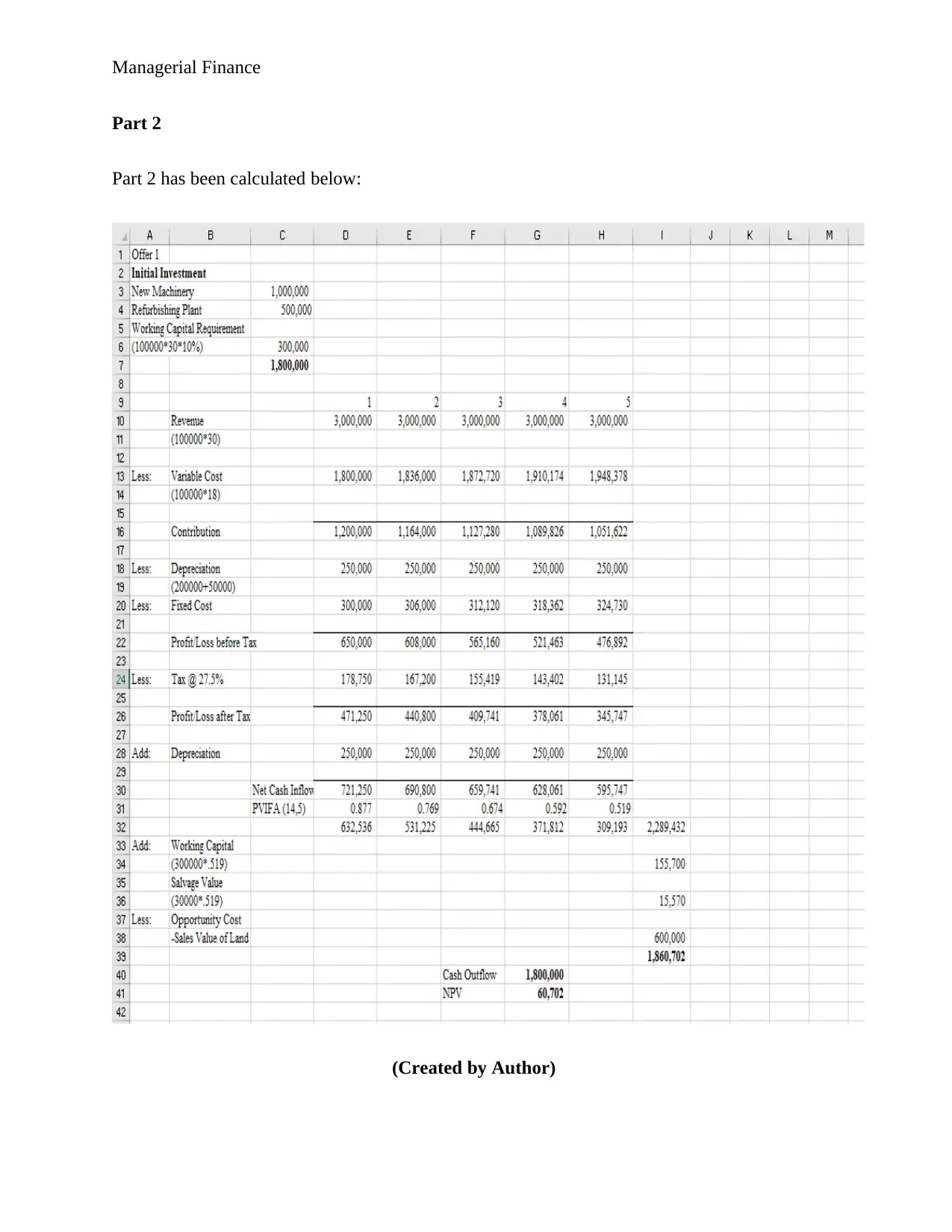

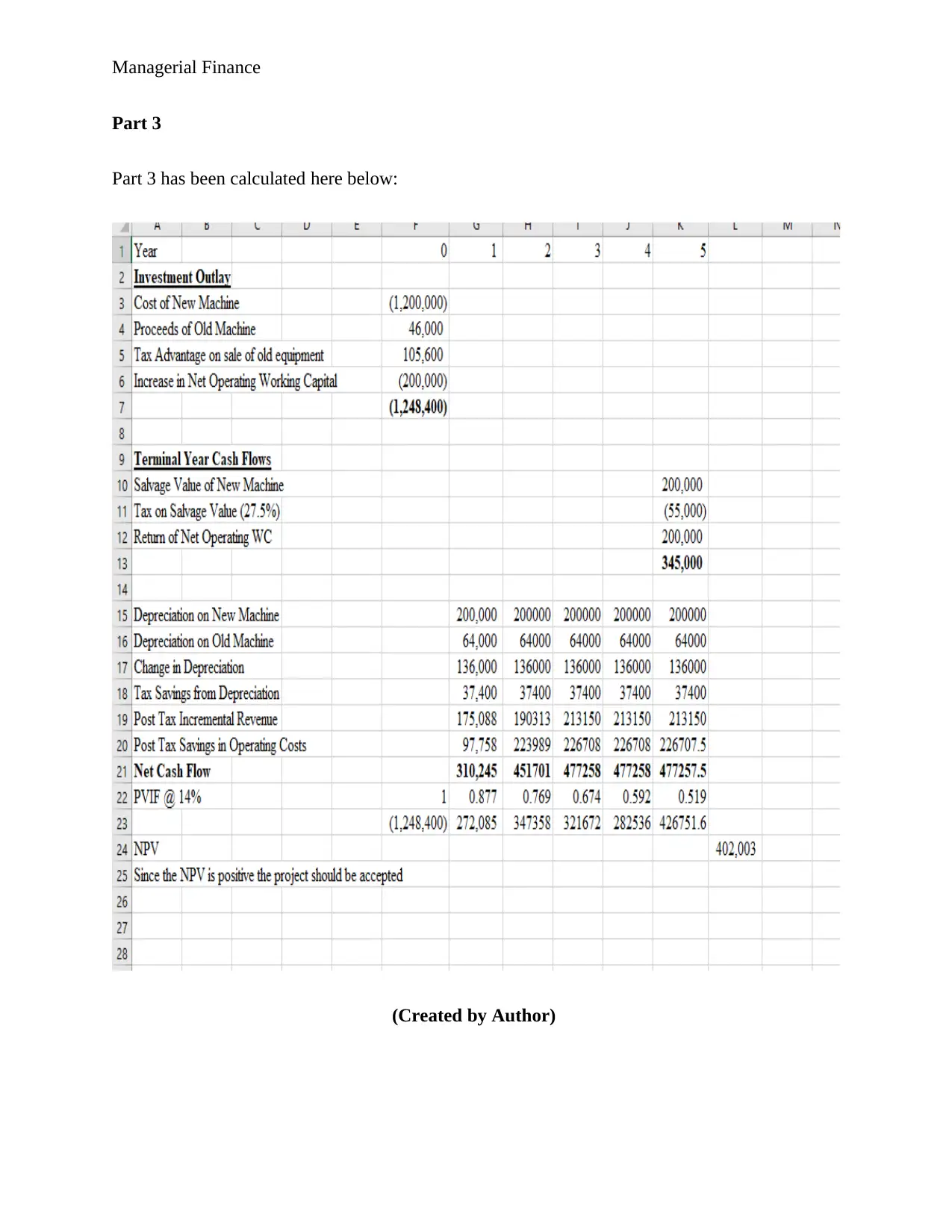

This case study solution for a Managerial Finance assignment involves analyzing investment decisions for an Australian defense firm. It includes calculating the weighted average cost of capital (WACC) considering various debt and equity components. The analysis evaluates two investment offers: one involving investment in new machinery and working capital for duffel bag production, and another involving selling land after development. The solution recommends pursuing the duffel bag production due to its positive NPV. Furthermore, the case addresses a replacement decision between an existing and a new machine, advocating for the replacement based on a positive NPV, indicating increased profitability. Desklib offers a wealth of similar solved assignments and study materials to aid students in their academic pursuits.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.