B9MG009 Managerial Financial Analysis Assignment - Summer 2020

VerifiedAdded on 2022/08/02

|6

|645

|74

Homework Assignment

AI Summary

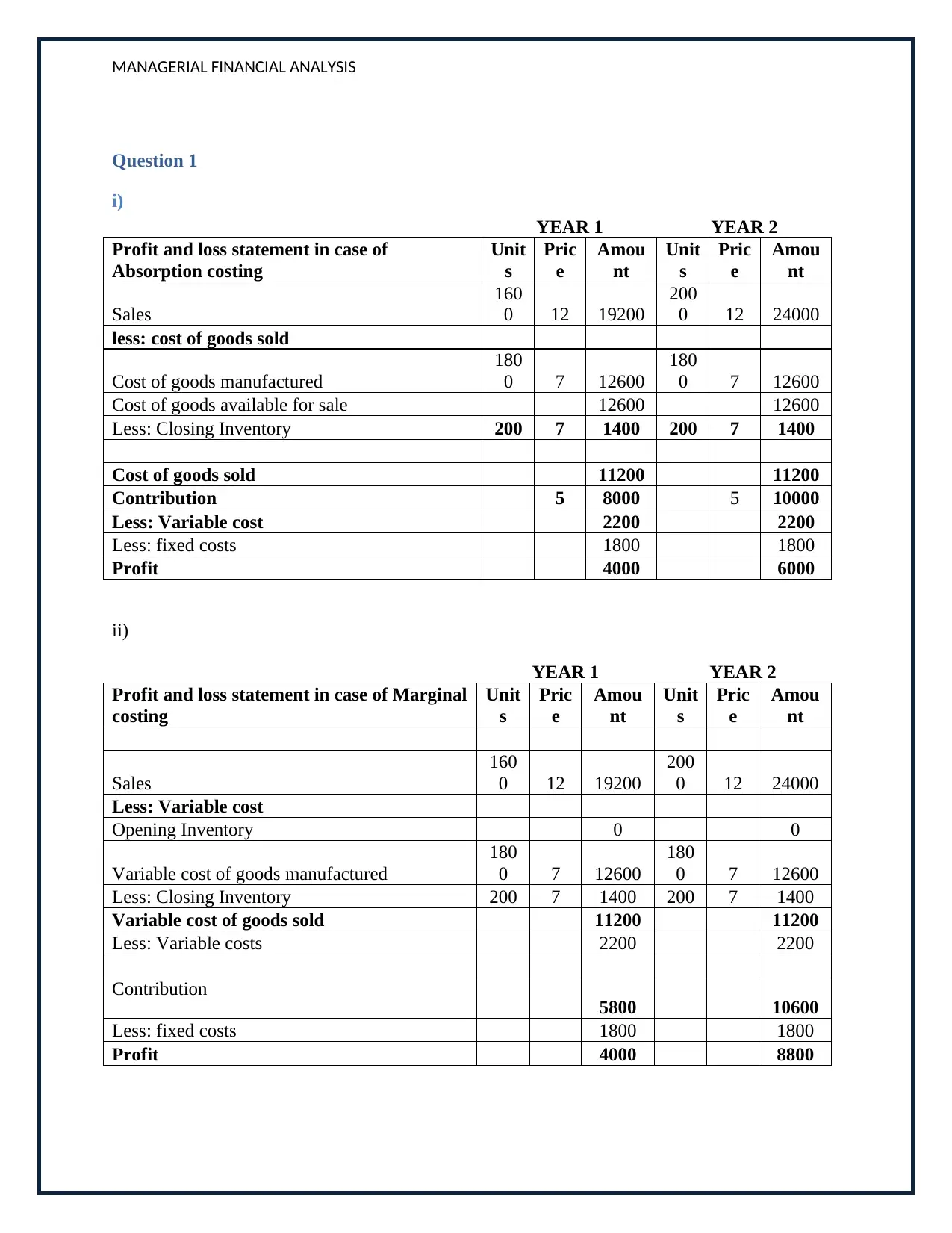

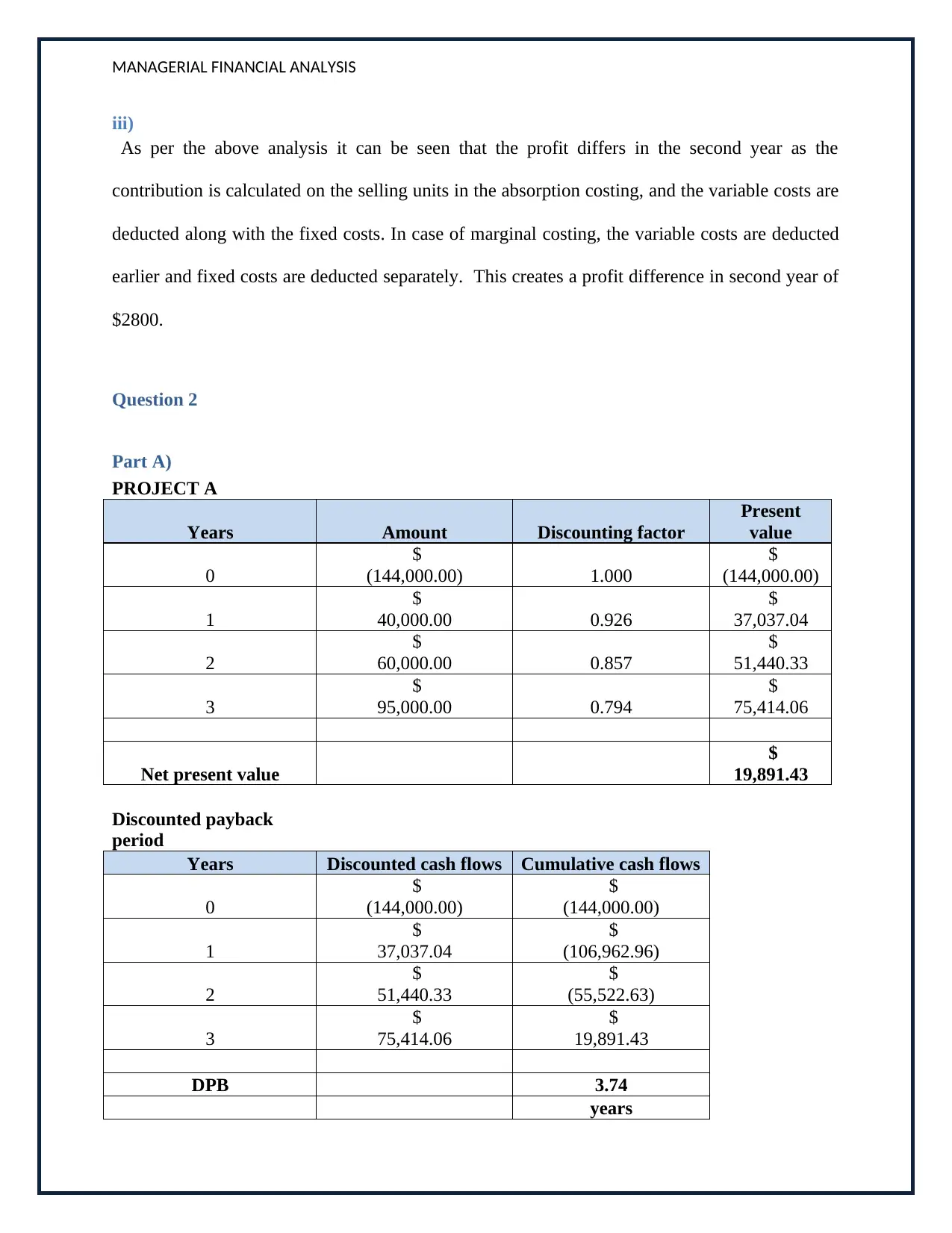

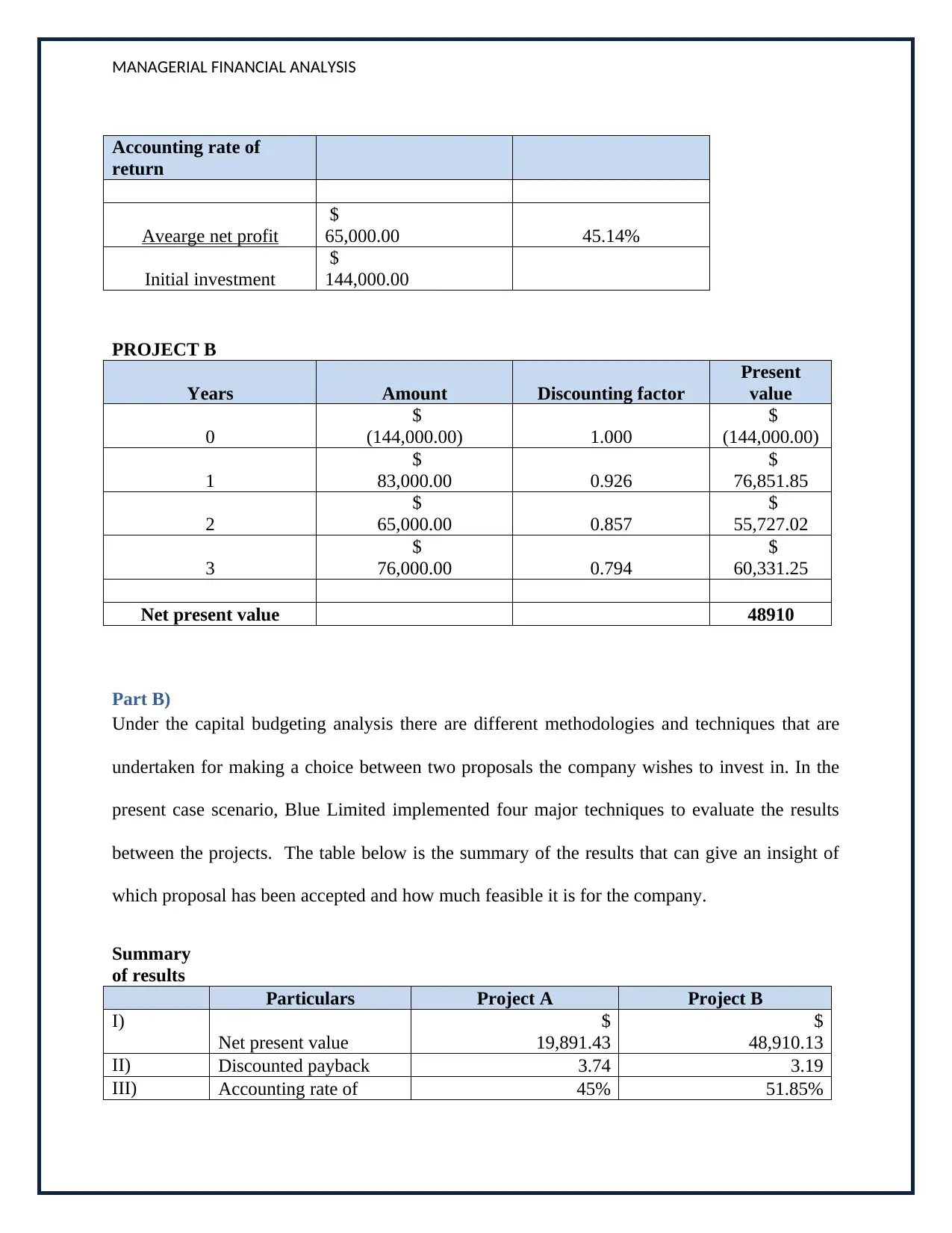

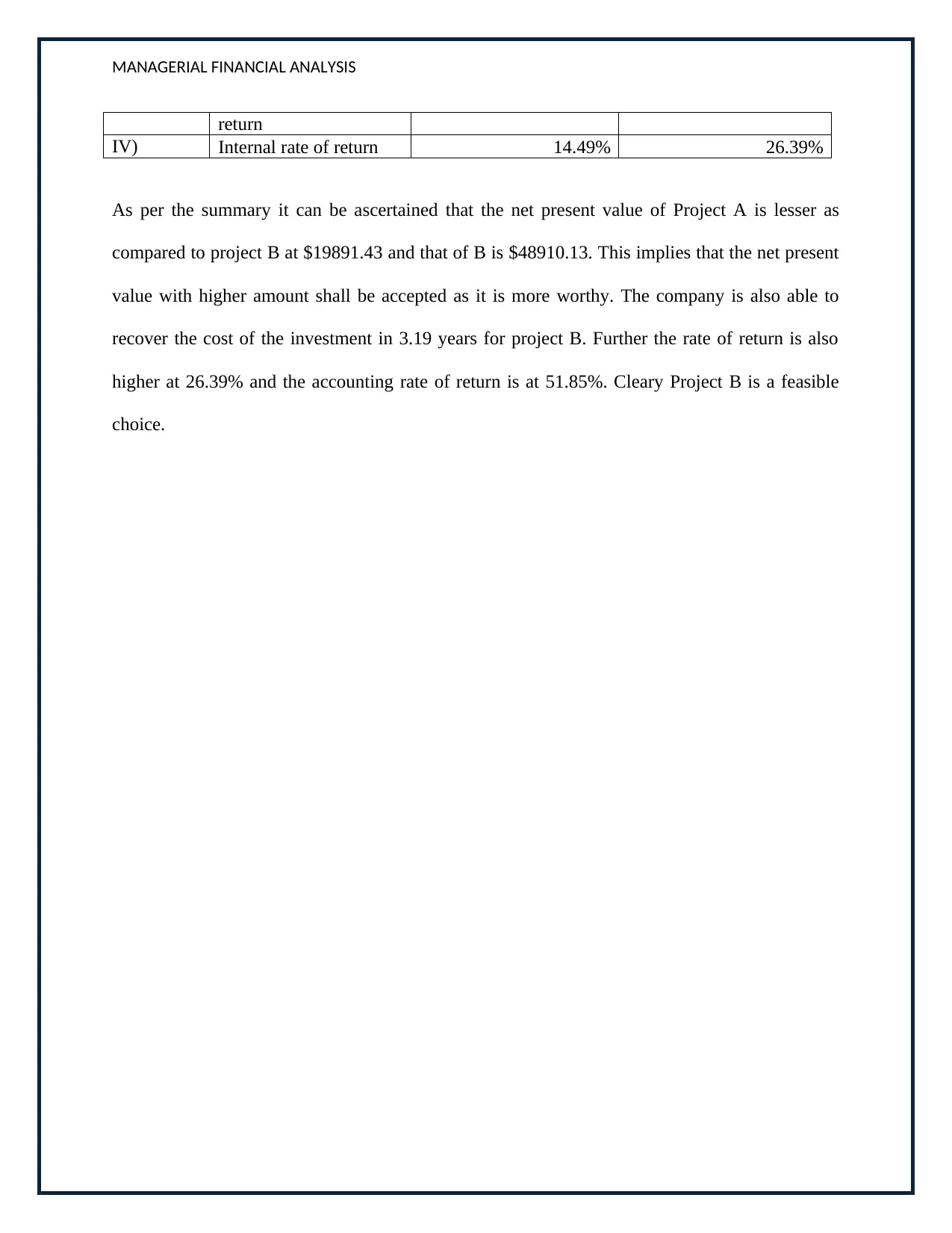

This assignment solution addresses key concepts in managerial financial analysis, providing a detailed breakdown of two main questions. Question 1 explores the preparation of income statements using both absorption costing and marginal costing methods, comparing profit calculations over two years. It analyzes the differences in profit arising from these costing approaches, considering the treatment of fixed and variable costs. Question 2 delves into capital budgeting techniques, evaluating two projects (A and B) using Net Present Value (NPV), Discounted Payback Period, Accounting Rate of Return, and Internal Rate of Return (IRR). The solution presents the calculations for each project and concludes with a comparative analysis, recommending the more financially viable project based on the results. The assignment demonstrates a solid understanding of financial statement preparation and investment appraisal techniques.

1 out of 6

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.