ACC4029: Managerial Operations and Finance Case Study Analysis

VerifiedAdded on 2023/01/11

|15

|3571

|55

Case Study

AI Summary

This case study analysis examines the managerial operations and finance of Cucumber Ltd, a smartphone producer. The assignment addresses the role of management accounting in the management process, contrasting it with financial accounting, and explores costing models used in operational management, including specific order and operational costing, with marginal costing as an example. Capital investment appraisal techniques are applied to evaluate project proposals. The role of business plans and budgets in operational management is discussed, identifying areas for improvement, particularly in communication, forecasting, and budgeting flexibility. The case study also touches upon the usefulness of the Balanced Scorecard approach and its application to Cucumber Limited. The analysis covers financial targets, operational strategies, and the importance of aligning departmental goals with overall company objectives.

Running Head: MANAGERIAL OPERATIONS AND FINANCE

MANAGERIAL OPERATIONS AND FINANCE

Name of the Student

Name of the University

Author Note

MANAGERIAL OPERATIONS AND FINANCE

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1MANAGERIAL OPERATIONS AND FINANCE

Table of Contents

Answer to Question 1.................................................................................................................2

Management accounting role in Management Process..........................................................2

Major Differences between Management Accounting and Financial Accounting................2

Techniques of different Models of Costing used in Investment decisions............................4

Answer to Question 2.................................................................................................................5

Techniques of Capital Investment Appraisal in making Investment Decisions....................5

Answer to Question 3.................................................................................................................6

Role of Business Plan and Budget in Operational Management...........................................6

Areas of Improvement............................................................................................................8

Answer to Question 4.................................................................................................................9

Usefulness of Balanced Scorecard Approach........................................................................9

Balance Scorecard for Cucumber Limited.............................................................................9

Reference..................................................................................................................................11

Table of Contents

Answer to Question 1.................................................................................................................2

Management accounting role in Management Process..........................................................2

Major Differences between Management Accounting and Financial Accounting................2

Techniques of different Models of Costing used in Investment decisions............................4

Answer to Question 2.................................................................................................................5

Techniques of Capital Investment Appraisal in making Investment Decisions....................5

Answer to Question 3.................................................................................................................6

Role of Business Plan and Budget in Operational Management...........................................6

Areas of Improvement............................................................................................................8

Answer to Question 4.................................................................................................................9

Usefulness of Balanced Scorecard Approach........................................................................9

Balance Scorecard for Cucumber Limited.............................................................................9

Reference..................................................................................................................................11

2MANAGERIAL OPERATIONS AND FINANCE

Answer to Question 1

Management accounting role in Management Process

The management accountant has the role of performing the series of the task for

ensuring the financial security of the company, handing of all the essential matters of the

finance and therefore helping in driving the overall management of the business and their

strategy (Fullerton, Kennedy and Widener 2014). Management accounting helps the

managers in making goods decisions. The information that is provided by the managerial

accounting is about the overall costs of the goods and services. The actual performance is

compared with the planned performances that facilitate the important decisions, which are

critical for the success of the organizations (Otley 2016).

For the determinations of the success and status of the company, management

accountant are the key figures. Depending upon the level of the experiences, type of the

industry and time of the year, management accountant are engaged in delivering following

tasks for the enhancement of the managerial performance and processes:

Budgeting

Aiding in the strategic planning

Handling taxes

Managing the assets for helping to determine the compensation as well as packages of

benefits.

Major Differences between Management Accounting and Financial Accounting

In comparison with the financial accounting that provides the financial accounting

that is primarily required for the external use, managerial accounting provides the

information, which is for external use. Financial accounting provides the information’s by

reporting on the organization’s financial activities, needed by the creditors and investors

Answer to Question 1

Management accounting role in Management Process

The management accountant has the role of performing the series of the task for

ensuring the financial security of the company, handing of all the essential matters of the

finance and therefore helping in driving the overall management of the business and their

strategy (Fullerton, Kennedy and Widener 2014). Management accounting helps the

managers in making goods decisions. The information that is provided by the managerial

accounting is about the overall costs of the goods and services. The actual performance is

compared with the planned performances that facilitate the important decisions, which are

critical for the success of the organizations (Otley 2016).

For the determinations of the success and status of the company, management

accountant are the key figures. Depending upon the level of the experiences, type of the

industry and time of the year, management accountant are engaged in delivering following

tasks for the enhancement of the managerial performance and processes:

Budgeting

Aiding in the strategic planning

Handling taxes

Managing the assets for helping to determine the compensation as well as packages of

benefits.

Major Differences between Management Accounting and Financial Accounting

In comparison with the financial accounting that provides the financial accounting

that is primarily required for the external use, managerial accounting provides the

information, which is for external use. Financial accounting provides the information’s by

reporting on the organization’s financial activities, needed by the creditors and investors

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3MANAGERIAL OPERATIONS AND FINANCE

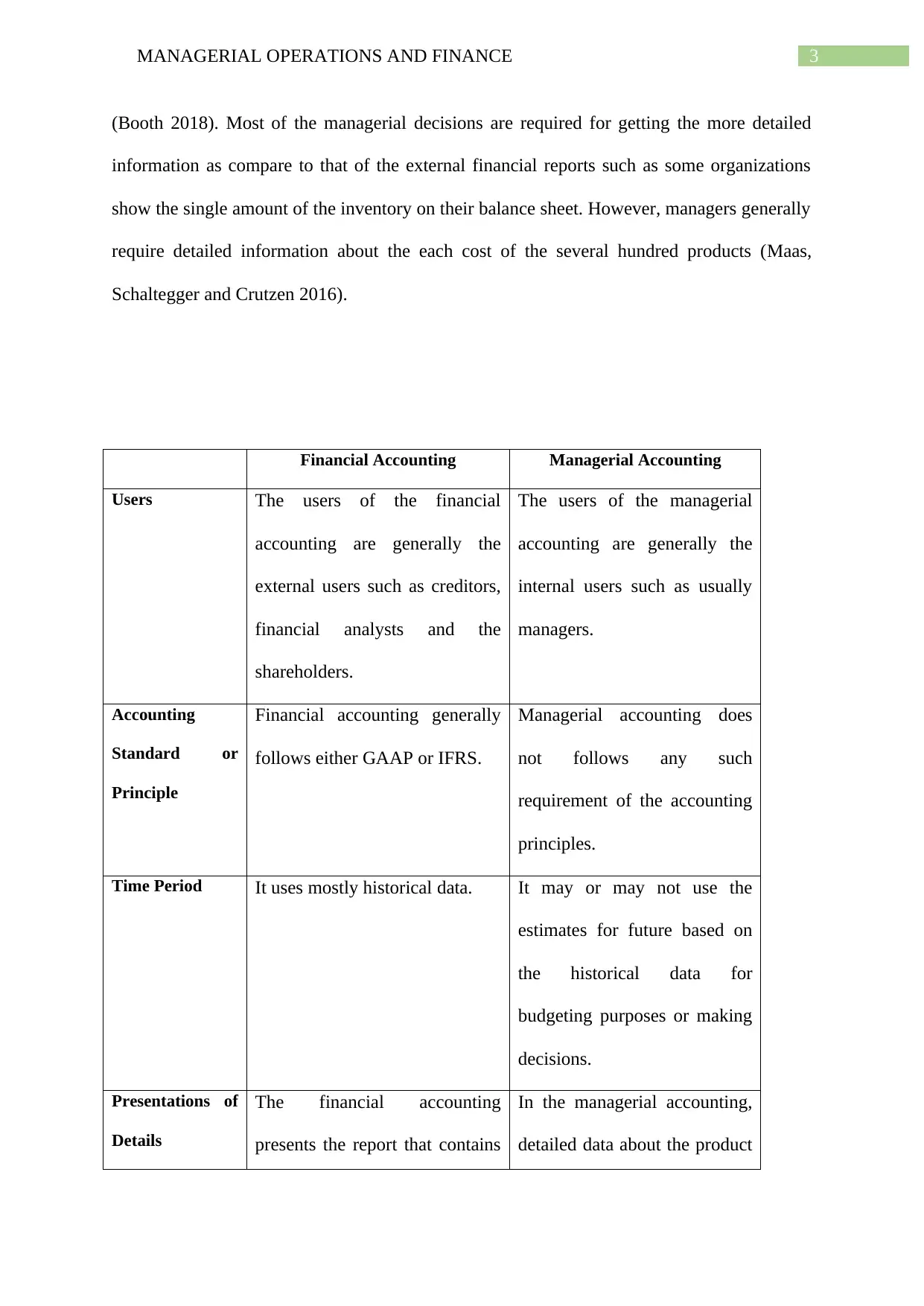

(Booth 2018). Most of the managerial decisions are required for getting the more detailed

information as compare to that of the external financial reports such as some organizations

show the single amount of the inventory on their balance sheet. However, managers generally

require detailed information about the each cost of the several hundred products (Maas,

Schaltegger and Crutzen 2016).

Financial Accounting Managerial Accounting

Users The users of the financial

accounting are generally the

external users such as creditors,

financial analysts and the

shareholders.

The users of the managerial

accounting are generally the

internal users such as usually

managers.

Accounting

Standard or

Principle

Financial accounting generally

follows either GAAP or IFRS.

Managerial accounting does

not follows any such

requirement of the accounting

principles.

Time Period It uses mostly historical data. It may or may not use the

estimates for future based on

the historical data for

budgeting purposes or making

decisions.

Presentations of

Details

The financial accounting

presents the report that contains

In the managerial accounting,

detailed data about the product

(Booth 2018). Most of the managerial decisions are required for getting the more detailed

information as compare to that of the external financial reports such as some organizations

show the single amount of the inventory on their balance sheet. However, managers generally

require detailed information about the each cost of the several hundred products (Maas,

Schaltegger and Crutzen 2016).

Financial Accounting Managerial Accounting

Users The users of the financial

accounting are generally the

external users such as creditors,

financial analysts and the

shareholders.

The users of the managerial

accounting are generally the

internal users such as usually

managers.

Accounting

Standard or

Principle

Financial accounting generally

follows either GAAP or IFRS.

Managerial accounting does

not follows any such

requirement of the accounting

principles.

Time Period It uses mostly historical data. It may or may not use the

estimates for future based on

the historical data for

budgeting purposes or making

decisions.

Presentations of

Details

The financial accounting

presents the report that contains

In the managerial accounting,

detailed data about the product

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4MANAGERIAL OPERATIONS AND FINANCE

the summary of the data,

revenues, costs and profits.

is presented in the reports.

Therefore, it is important to for understanding the differences as well as

distinguishing between the three concepts such as cost accounting, managerial accounting as

well as financial accounting. The good manager is required for knowing the usefulness of

each of these particular concepts (Nobes and Stadler 2015). The managerial accounting is

considered as the complex processes that is used by the mangers for the decision making in

order to achieve the objectives of the organizations by learning how these process affects

each of the functions of management such as planning, organizing, communicating,

motivating and controlling (Nielsen and Roslender 2015).

Techniques of different Models of Costing used in Investment decisions

Cost is the money or the resources associated with the purchases or the business

transactions. For ascertaining the costs of the product, different industries adopt different

methods and the models, which depend upon the nature and type of the production and

output. The analysis of the models of cost helps in calculating the cost of the products, with

the analysis of value that helps in allowing for reducing the waste, secondary functions and

elements (Zowall, Brewer and Deutsch 2015). There are two methods of costing that is used

in operational management:

Specific Order Costing: This is the basic method that is applicable for the work that

consists of batches or contracts, separate jobs, which are authorized by the specific

contract or order. The costing models included in this are batch-costing, job costing as

well as contract costing.

the summary of the data,

revenues, costs and profits.

is presented in the reports.

Therefore, it is important to for understanding the differences as well as

distinguishing between the three concepts such as cost accounting, managerial accounting as

well as financial accounting. The good manager is required for knowing the usefulness of

each of these particular concepts (Nobes and Stadler 2015). The managerial accounting is

considered as the complex processes that is used by the mangers for the decision making in

order to achieve the objectives of the organizations by learning how these process affects

each of the functions of management such as planning, organizing, communicating,

motivating and controlling (Nielsen and Roslender 2015).

Techniques of different Models of Costing used in Investment decisions

Cost is the money or the resources associated with the purchases or the business

transactions. For ascertaining the costs of the product, different industries adopt different

methods and the models, which depend upon the nature and type of the production and

output. The analysis of the models of cost helps in calculating the cost of the products, with

the analysis of value that helps in allowing for reducing the waste, secondary functions and

elements (Zowall, Brewer and Deutsch 2015). There are two methods of costing that is used

in operational management:

Specific Order Costing: This is the basic method that is applicable for the work that

consists of batches or contracts, separate jobs, which are authorized by the specific

contract or order. The costing models included in this are batch-costing, job costing as

well as contract costing.

5MANAGERIAL OPERATIONS AND FINANCE

Operational Costing: This method is applicable in case where the standardized

services and goods results from the repetitive sequences as well as more or less

process or operations that is continuous for which the costs are charged before

averaging over the produced units during the period (Kaspina, Khapugina and Zakirov

2014).

The techniques that can be applied by for analyzing and explaining the model of costing

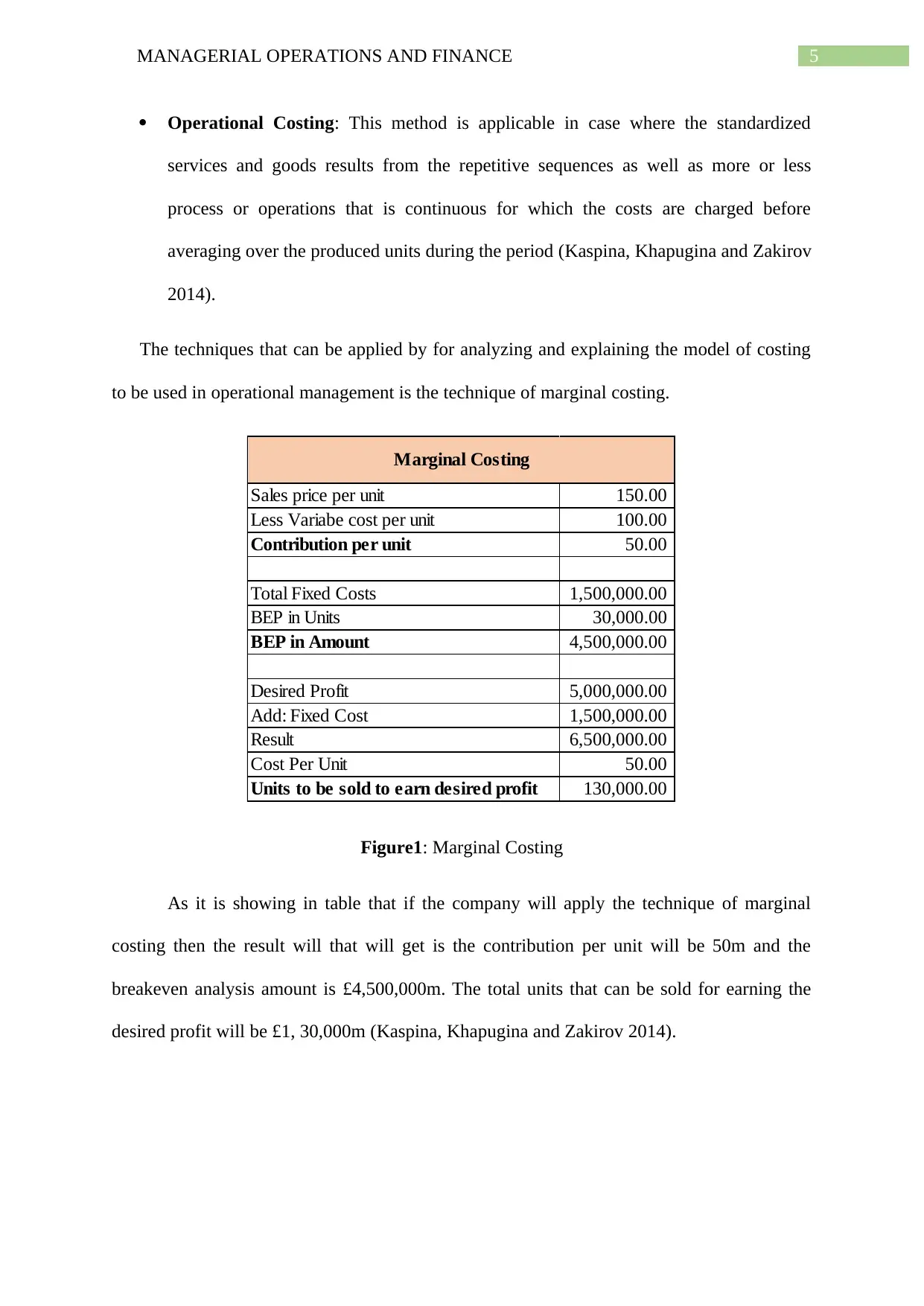

to be used in operational management is the technique of marginal costing.

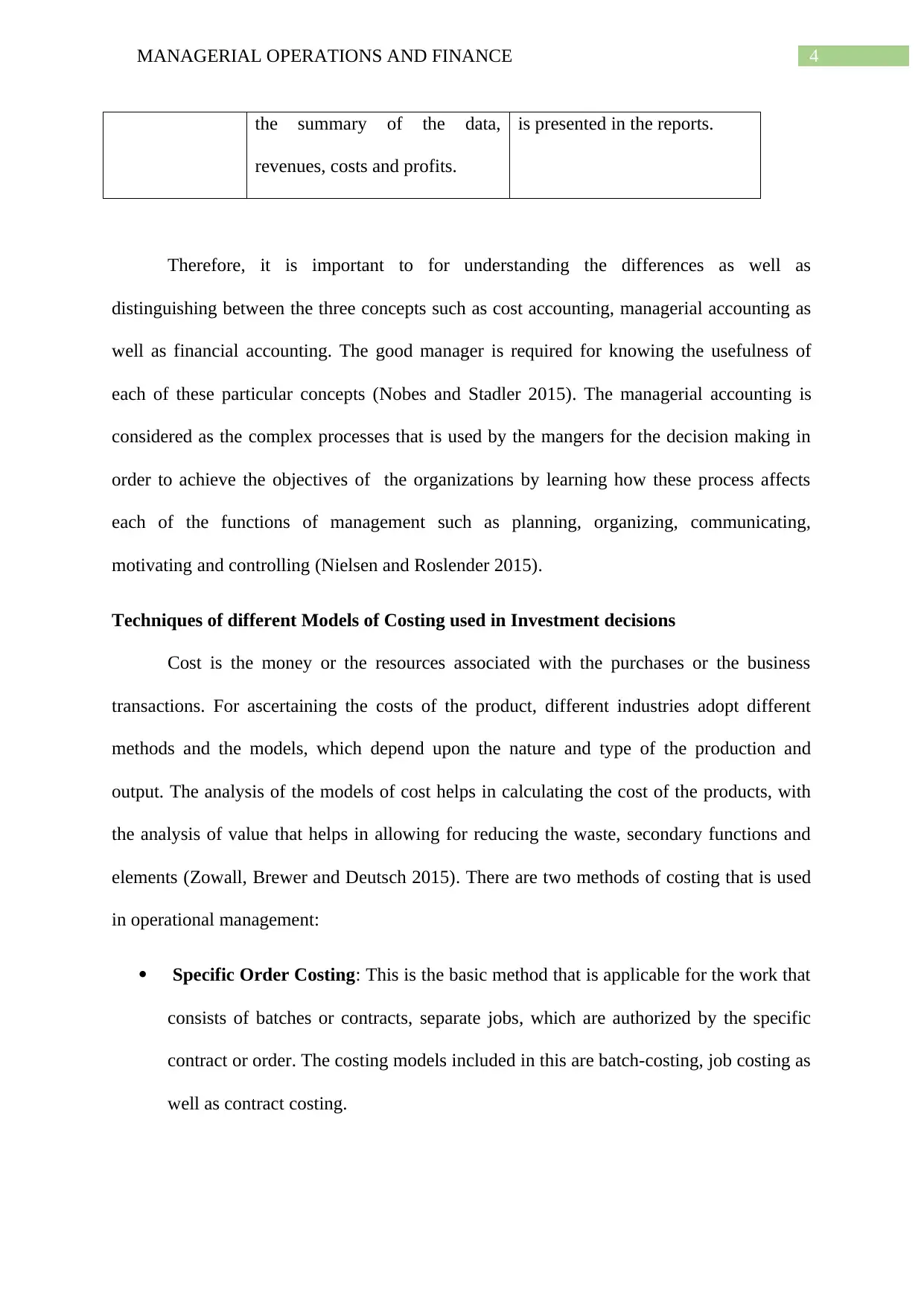

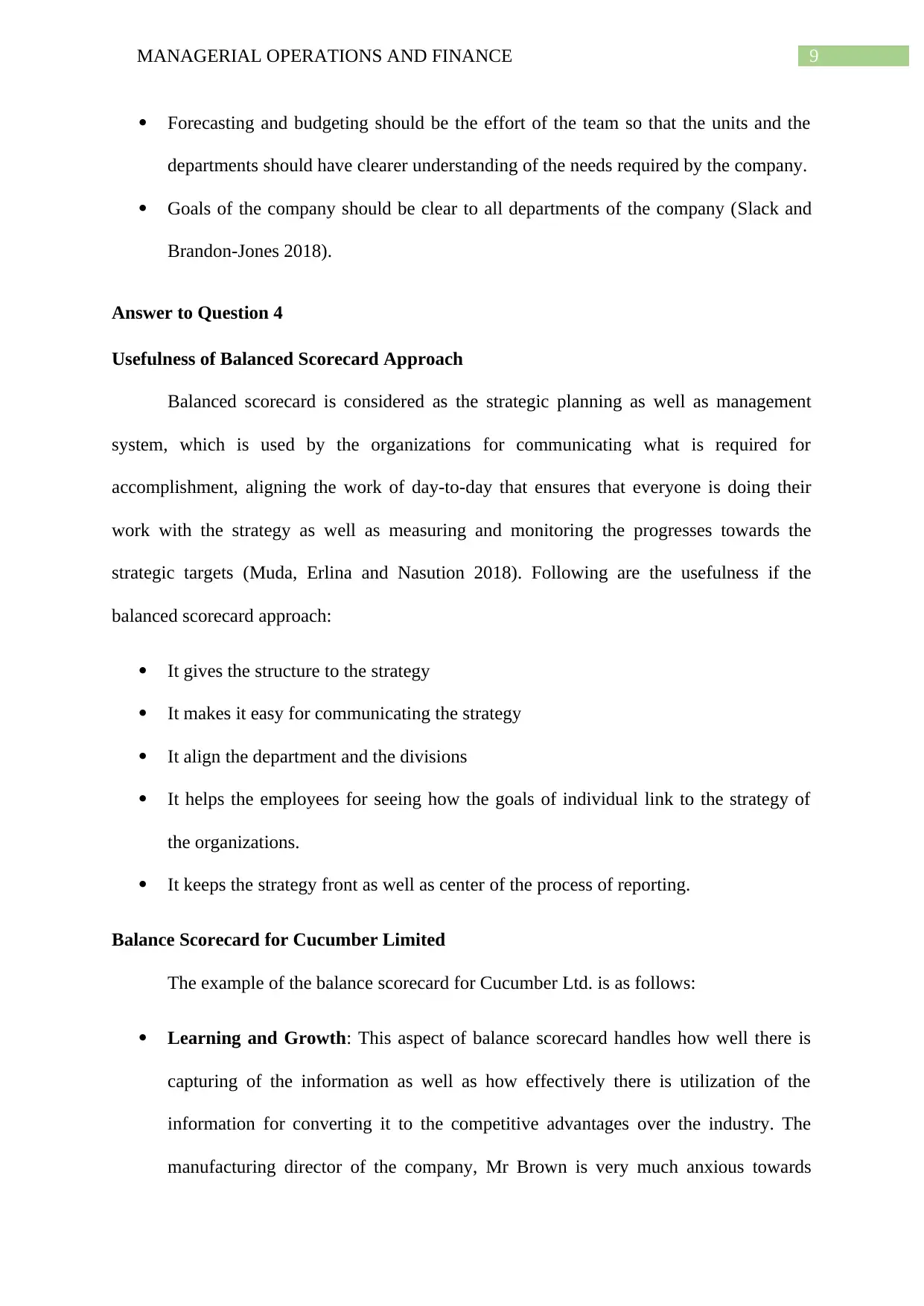

Sales price per unit 150.00

Less Variabe cost per unit 100.00

Contribution per unit 50.00

Total Fixed Costs 1,500,000.00

BEP in Units 30,000.00

BEP in Amount 4,500,000.00

Desired Profit 5,000,000.00

Add: Fixed Cost 1,500,000.00

Result 6,500,000.00

Cost Per Unit 50.00

Units to be sold to earn desired profit 130,000.00

Marginal Costing

Figure1: Marginal Costing

As it is showing in table that if the company will apply the technique of marginal

costing then the result will that will get is the contribution per unit will be 50m and the

breakeven analysis amount is £4,500,000m. The total units that can be sold for earning the

desired profit will be £1, 30,000m (Kaspina, Khapugina and Zakirov 2014).

Operational Costing: This method is applicable in case where the standardized

services and goods results from the repetitive sequences as well as more or less

process or operations that is continuous for which the costs are charged before

averaging over the produced units during the period (Kaspina, Khapugina and Zakirov

2014).

The techniques that can be applied by for analyzing and explaining the model of costing

to be used in operational management is the technique of marginal costing.

Sales price per unit 150.00

Less Variabe cost per unit 100.00

Contribution per unit 50.00

Total Fixed Costs 1,500,000.00

BEP in Units 30,000.00

BEP in Amount 4,500,000.00

Desired Profit 5,000,000.00

Add: Fixed Cost 1,500,000.00

Result 6,500,000.00

Cost Per Unit 50.00

Units to be sold to earn desired profit 130,000.00

Marginal Costing

Figure1: Marginal Costing

As it is showing in table that if the company will apply the technique of marginal

costing then the result will that will get is the contribution per unit will be 50m and the

breakeven analysis amount is £4,500,000m. The total units that can be sold for earning the

desired profit will be £1, 30,000m (Kaspina, Khapugina and Zakirov 2014).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6MANAGERIAL OPERATIONS AND FINANCE

Answer to Question 2

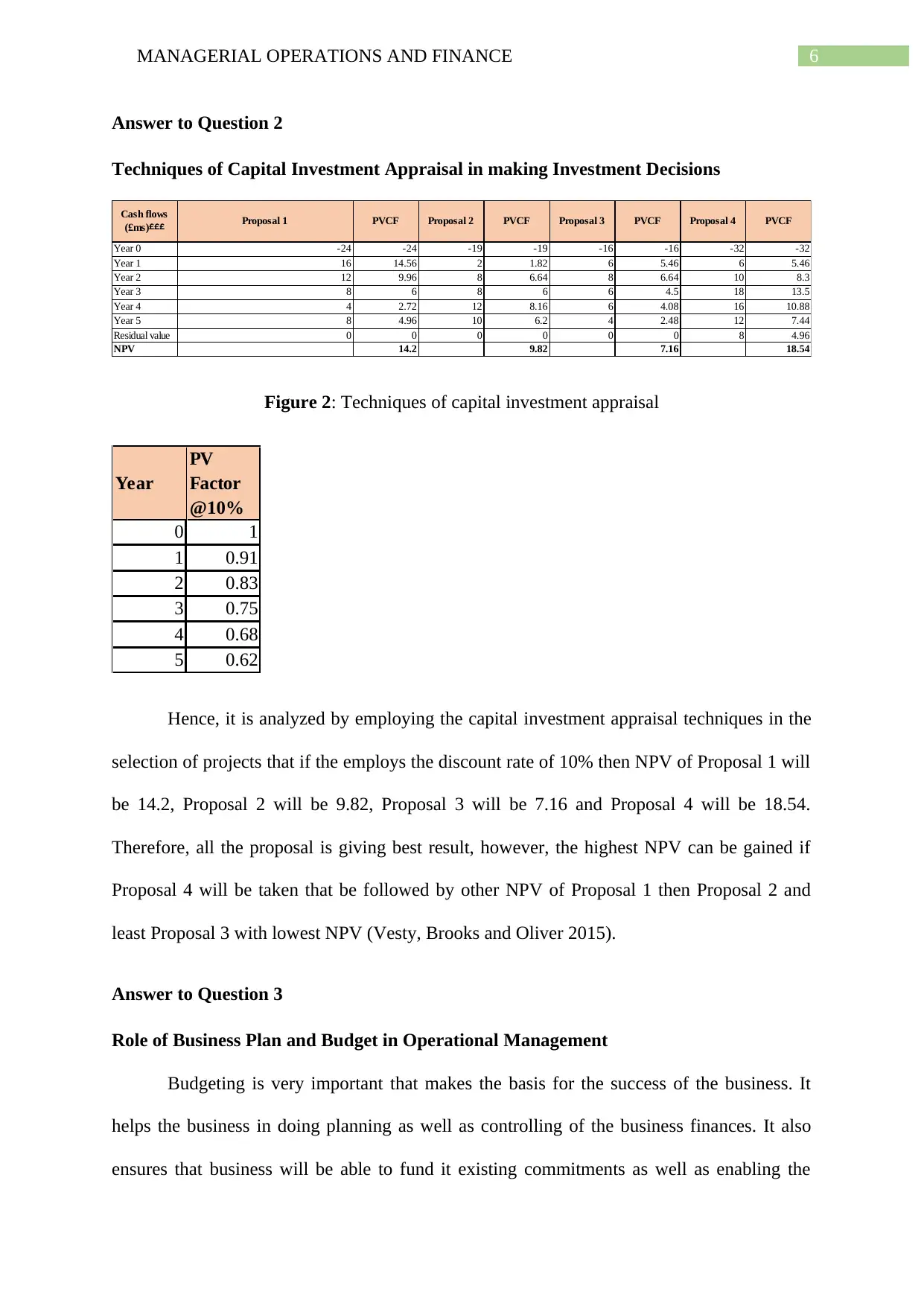

Techniques of Capital Investment Appraisal in making Investment Decisions

Cash flows

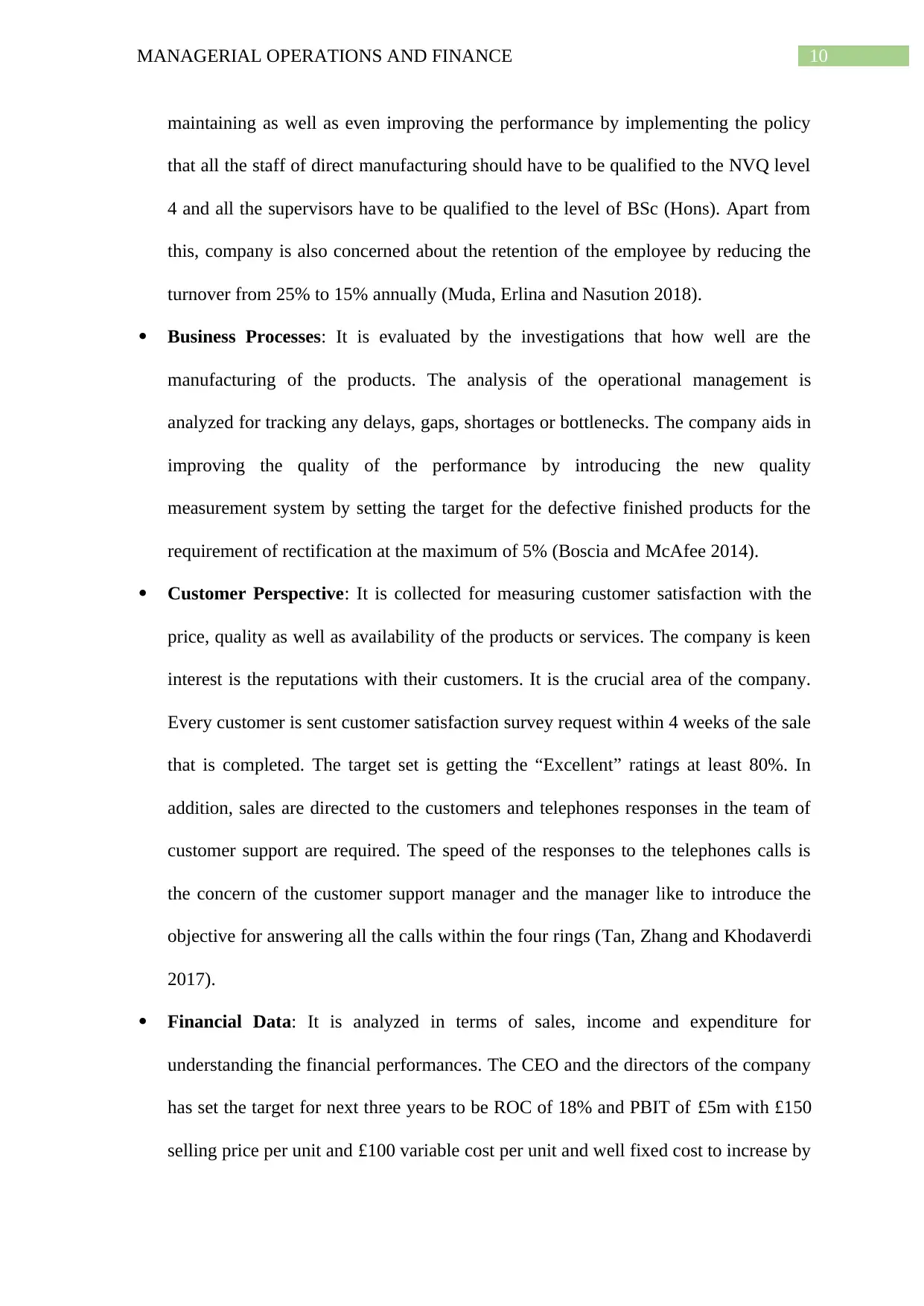

(£ms)£££ Proposal 1 PVCF Proposal 2 PVCF Proposal 3 PVCF Proposal 4 PVCF

Year 0 -24 -24 -19 -19 -16 -16 -32 -32

Year 1 16 14.56 2 1.82 6 5.46 6 5.46

Year 2 12 9.96 8 6.64 8 6.64 10 8.3

Year 3 8 6 8 6 6 4.5 18 13.5

Year 4 4 2.72 12 8.16 6 4.08 16 10.88

Year 5 8 4.96 10 6.2 4 2.48 12 7.44

Residual value 0 0 0 0 0 0 8 4.96

NPV 14.2 9.82 7.16 18.54

Figure 2: Techniques of capital investment appraisal

Year

PV

Factor

@10%

0 1

1 0.91

2 0.83

3 0.75

4 0.68

5 0.62

Hence, it is analyzed by employing the capital investment appraisal techniques in the

selection of projects that if the employs the discount rate of 10% then NPV of Proposal 1 will

be 14.2, Proposal 2 will be 9.82, Proposal 3 will be 7.16 and Proposal 4 will be 18.54.

Therefore, all the proposal is giving best result, however, the highest NPV can be gained if

Proposal 4 will be taken that be followed by other NPV of Proposal 1 then Proposal 2 and

least Proposal 3 with lowest NPV (Vesty, Brooks and Oliver 2015).

Answer to Question 3

Role of Business Plan and Budget in Operational Management

Budgeting is very important that makes the basis for the success of the business. It

helps the business in doing planning as well as controlling of the business finances. It also

ensures that business will be able to fund it existing commitments as well as enabling the

Answer to Question 2

Techniques of Capital Investment Appraisal in making Investment Decisions

Cash flows

(£ms)£££ Proposal 1 PVCF Proposal 2 PVCF Proposal 3 PVCF Proposal 4 PVCF

Year 0 -24 -24 -19 -19 -16 -16 -32 -32

Year 1 16 14.56 2 1.82 6 5.46 6 5.46

Year 2 12 9.96 8 6.64 8 6.64 10 8.3

Year 3 8 6 8 6 6 4.5 18 13.5

Year 4 4 2.72 12 8.16 6 4.08 16 10.88

Year 5 8 4.96 10 6.2 4 2.48 12 7.44

Residual value 0 0 0 0 0 0 8 4.96

NPV 14.2 9.82 7.16 18.54

Figure 2: Techniques of capital investment appraisal

Year

PV

Factor

@10%

0 1

1 0.91

2 0.83

3 0.75

4 0.68

5 0.62

Hence, it is analyzed by employing the capital investment appraisal techniques in the

selection of projects that if the employs the discount rate of 10% then NPV of Proposal 1 will

be 14.2, Proposal 2 will be 9.82, Proposal 3 will be 7.16 and Proposal 4 will be 18.54.

Therefore, all the proposal is giving best result, however, the highest NPV can be gained if

Proposal 4 will be taken that be followed by other NPV of Proposal 1 then Proposal 2 and

least Proposal 3 with lowest NPV (Vesty, Brooks and Oliver 2015).

Answer to Question 3

Role of Business Plan and Budget in Operational Management

Budgeting is very important that makes the basis for the success of the business. It

helps the business in doing planning as well as controlling of the business finances. It also

ensures that business will be able to fund it existing commitments as well as enabling the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7MANAGERIAL OPERATIONS AND FINANCE

business for meeting its objectives and making confident financial decisions. Budget is

necessary for highlighting the financial implications of the plans for defining the required

resources for achieving these plans and for providing the means for measurement, viewing as

well as controlling the results obtained that is comparison with that of the plans. Budgets are

considered as excellent tools for communication that points out the financial and operational

objectives of the particular period. It communicates the expectations of the top management

to the upper level as well as middle level management. In addition, budgets set out the prices

for the internal services and it is considered as the basis for the evaluation of the business.

In case of the company Cucumber Limited, the CEO of the company has make the

strategic plan with the fellow directors, for the financial targets for each and every next three

years that there should be Return on the capital employed of 18% and profit before tax of £5

million. The company has also working flat out of selling price per unit of £150 and variable

cost per unit of £100 and the company is planning for spending more on the development of

the products for making significantly improvement to the products. The accounting

department head noted for increasing the fixed cost by £1,500,000 as the result of the

expansion (Chong and Mahama 2014). Moreover, for assisting with the quality

improvements, the manufacturing head sets out the target for the defective finished products

that requires rectification for maximum 5%. However, Mr. McDonald who is the manager of

Screen making department has raised the concerns regarding the reports the budget control

that was issued by the earlier finance director. These budget control reports are issued on

each month on the last Friday, with the previous month’s data (Chenhall and Moers 2015).

However, the screen-making department that, despite of the fact that their team was working

hard for achieving the level of the output, the report indicated that the manager was not doing

his job in the better way as there was reporting of adverse variances has analyzed it.

Therefore, it has been accessed that there was not proper communication between the top

business for meeting its objectives and making confident financial decisions. Budget is

necessary for highlighting the financial implications of the plans for defining the required

resources for achieving these plans and for providing the means for measurement, viewing as

well as controlling the results obtained that is comparison with that of the plans. Budgets are

considered as excellent tools for communication that points out the financial and operational

objectives of the particular period. It communicates the expectations of the top management

to the upper level as well as middle level management. In addition, budgets set out the prices

for the internal services and it is considered as the basis for the evaluation of the business.

In case of the company Cucumber Limited, the CEO of the company has make the

strategic plan with the fellow directors, for the financial targets for each and every next three

years that there should be Return on the capital employed of 18% and profit before tax of £5

million. The company has also working flat out of selling price per unit of £150 and variable

cost per unit of £100 and the company is planning for spending more on the development of

the products for making significantly improvement to the products. The accounting

department head noted for increasing the fixed cost by £1,500,000 as the result of the

expansion (Chong and Mahama 2014). Moreover, for assisting with the quality

improvements, the manufacturing head sets out the target for the defective finished products

that requires rectification for maximum 5%. However, Mr. McDonald who is the manager of

Screen making department has raised the concerns regarding the reports the budget control

that was issued by the earlier finance director. These budget control reports are issued on

each month on the last Friday, with the previous month’s data (Chenhall and Moers 2015).

However, the screen-making department that, despite of the fact that their team was working

hard for achieving the level of the output, the report indicated that the manager was not doing

his job in the better way as there was reporting of adverse variances has analyzed it.

Therefore, it has been accessed that there was not proper communication between the top

8MANAGERIAL OPERATIONS AND FINANCE

management and the departmental head regarding the planned actions as well as expected

results that resulted into the adverse variances in the budgetary control report (Berman, L.,

2015). Apart from this, it has been accessed that the company is staffed with the team of the

committed staff but the operating teams did not know overall strategy of the Directors of the

company clearly. The teams of the company was unsure regarding the fact that what was their

part or role in the achievement of the objectives of the company as well as they were having

no projects or plans for the improvement if required by the teams (Barr and McClellan 2018).

Areas of Improvement

Budgeting and forecasting allows the business for planning accurately for the fiscal

year or the respective period of reporting it. The areas that should be improved will be

making business plan and budget that is achievable. The business plan has to be clearly stated

to all the employees and respective teams. It is not sufficient just to set the target rather it

requires proper planning, coordination and communication among all in the organization

(Bhatt, Manadhata and Zomlot 2014). Following are the recommendations that can be

provided for the improvements:

Forecast and budget that are rigid are not useful. In this organization, if there will be

building of the flexibility into the forecasting and budgeting then it will be more

accurate for the better result of the teams and overall business.

There should be implementation of rolling forecast and the budget. The budgets

should not be based on the forecast that have been made several months ago rather it

should be updated again and again, as it allows for better aligning with the states plans

with improving the projections accuracy (Heldman 2018).

Communications should be open with all the departments that are throughout of the

overall process for helping to minimize the issues as well as ensuring the alignments

between the operations of the company and strategies of the organizations.

management and the departmental head regarding the planned actions as well as expected

results that resulted into the adverse variances in the budgetary control report (Berman, L.,

2015). Apart from this, it has been accessed that the company is staffed with the team of the

committed staff but the operating teams did not know overall strategy of the Directors of the

company clearly. The teams of the company was unsure regarding the fact that what was their

part or role in the achievement of the objectives of the company as well as they were having

no projects or plans for the improvement if required by the teams (Barr and McClellan 2018).

Areas of Improvement

Budgeting and forecasting allows the business for planning accurately for the fiscal

year or the respective period of reporting it. The areas that should be improved will be

making business plan and budget that is achievable. The business plan has to be clearly stated

to all the employees and respective teams. It is not sufficient just to set the target rather it

requires proper planning, coordination and communication among all in the organization

(Bhatt, Manadhata and Zomlot 2014). Following are the recommendations that can be

provided for the improvements:

Forecast and budget that are rigid are not useful. In this organization, if there will be

building of the flexibility into the forecasting and budgeting then it will be more

accurate for the better result of the teams and overall business.

There should be implementation of rolling forecast and the budget. The budgets

should not be based on the forecast that have been made several months ago rather it

should be updated again and again, as it allows for better aligning with the states plans

with improving the projections accuracy (Heldman 2018).

Communications should be open with all the departments that are throughout of the

overall process for helping to minimize the issues as well as ensuring the alignments

between the operations of the company and strategies of the organizations.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9MANAGERIAL OPERATIONS AND FINANCE

Forecasting and budgeting should be the effort of the team so that the units and the

departments should have clearer understanding of the needs required by the company.

Goals of the company should be clear to all departments of the company (Slack and

Brandon-Jones 2018).

Answer to Question 4

Usefulness of Balanced Scorecard Approach

Balanced scorecard is considered as the strategic planning as well as management

system, which is used by the organizations for communicating what is required for

accomplishment, aligning the work of day-to-day that ensures that everyone is doing their

work with the strategy as well as measuring and monitoring the progresses towards the

strategic targets (Muda, Erlina and Nasution 2018). Following are the usefulness if the

balanced scorecard approach:

It gives the structure to the strategy

It makes it easy for communicating the strategy

It align the department and the divisions

It helps the employees for seeing how the goals of individual link to the strategy of

the organizations.

It keeps the strategy front as well as center of the process of reporting.

Balance Scorecard for Cucumber Limited

The example of the balance scorecard for Cucumber Ltd. is as follows:

Learning and Growth: This aspect of balance scorecard handles how well there is

capturing of the information as well as how effectively there is utilization of the

information for converting it to the competitive advantages over the industry. The

manufacturing director of the company, Mr Brown is very much anxious towards

Forecasting and budgeting should be the effort of the team so that the units and the

departments should have clearer understanding of the needs required by the company.

Goals of the company should be clear to all departments of the company (Slack and

Brandon-Jones 2018).

Answer to Question 4

Usefulness of Balanced Scorecard Approach

Balanced scorecard is considered as the strategic planning as well as management

system, which is used by the organizations for communicating what is required for

accomplishment, aligning the work of day-to-day that ensures that everyone is doing their

work with the strategy as well as measuring and monitoring the progresses towards the

strategic targets (Muda, Erlina and Nasution 2018). Following are the usefulness if the

balanced scorecard approach:

It gives the structure to the strategy

It makes it easy for communicating the strategy

It align the department and the divisions

It helps the employees for seeing how the goals of individual link to the strategy of

the organizations.

It keeps the strategy front as well as center of the process of reporting.

Balance Scorecard for Cucumber Limited

The example of the balance scorecard for Cucumber Ltd. is as follows:

Learning and Growth: This aspect of balance scorecard handles how well there is

capturing of the information as well as how effectively there is utilization of the

information for converting it to the competitive advantages over the industry. The

manufacturing director of the company, Mr Brown is very much anxious towards

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10MANAGERIAL OPERATIONS AND FINANCE

maintaining as well as even improving the performance by implementing the policy

that all the staff of direct manufacturing should have to be qualified to the NVQ level

4 and all the supervisors have to be qualified to the level of BSc (Hons). Apart from

this, company is also concerned about the retention of the employee by reducing the

turnover from 25% to 15% annually (Muda, Erlina and Nasution 2018).

Business Processes: It is evaluated by the investigations that how well are the

manufacturing of the products. The analysis of the operational management is

analyzed for tracking any delays, gaps, shortages or bottlenecks. The company aids in

improving the quality of the performance by introducing the new quality

measurement system by setting the target for the defective finished products for the

requirement of rectification at the maximum of 5% (Boscia and McAfee 2014).

Customer Perspective: It is collected for measuring customer satisfaction with the

price, quality as well as availability of the products or services. The company is keen

interest is the reputations with their customers. It is the crucial area of the company.

Every customer is sent customer satisfaction survey request within 4 weeks of the sale

that is completed. The target set is getting the “Excellent” ratings at least 80%. In

addition, sales are directed to the customers and telephones responses in the team of

customer support are required. The speed of the responses to the telephones calls is

the concern of the customer support manager and the manager like to introduce the

objective for answering all the calls within the four rings (Tan, Zhang and Khodaverdi

2017).

Financial Data: It is analyzed in terms of sales, income and expenditure for

understanding the financial performances. The CEO and the directors of the company

has set the target for next three years to be ROC of 18% and PBIT of £5m with £150

selling price per unit and £100 variable cost per unit and well fixed cost to increase by

maintaining as well as even improving the performance by implementing the policy

that all the staff of direct manufacturing should have to be qualified to the NVQ level

4 and all the supervisors have to be qualified to the level of BSc (Hons). Apart from

this, company is also concerned about the retention of the employee by reducing the

turnover from 25% to 15% annually (Muda, Erlina and Nasution 2018).

Business Processes: It is evaluated by the investigations that how well are the

manufacturing of the products. The analysis of the operational management is

analyzed for tracking any delays, gaps, shortages or bottlenecks. The company aids in

improving the quality of the performance by introducing the new quality

measurement system by setting the target for the defective finished products for the

requirement of rectification at the maximum of 5% (Boscia and McAfee 2014).

Customer Perspective: It is collected for measuring customer satisfaction with the

price, quality as well as availability of the products or services. The company is keen

interest is the reputations with their customers. It is the crucial area of the company.

Every customer is sent customer satisfaction survey request within 4 weeks of the sale

that is completed. The target set is getting the “Excellent” ratings at least 80%. In

addition, sales are directed to the customers and telephones responses in the team of

customer support are required. The speed of the responses to the telephones calls is

the concern of the customer support manager and the manager like to introduce the

objective for answering all the calls within the four rings (Tan, Zhang and Khodaverdi

2017).

Financial Data: It is analyzed in terms of sales, income and expenditure for

understanding the financial performances. The CEO and the directors of the company

has set the target for next three years to be ROC of 18% and PBIT of £5m with £150

selling price per unit and £100 variable cost per unit and well fixed cost to increase by

11MANAGERIAL OPERATIONS AND FINANCE

£1,500,000, if production facilities is expanded. However, the actual performance of

screen making department has resulted into report of adverse variances (Fooladvand,

Yarmohammadian and Shahtalebi 2015).

£1,500,000, if production facilities is expanded. However, the actual performance of

screen making department has resulted into report of adverse variances (Fooladvand,

Yarmohammadian and Shahtalebi 2015).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.