Managerial Accounting Assignment: Cost and Performance Analysis

VerifiedAdded on 2021/05/31

|30

|3829

|187

Homework Assignment

AI Summary

This managerial accounting assignment solution provides a detailed analysis of various cost and performance-related topics. It covers variance analysis, including variable and fixed overhead variances, direct material and labor variances, and their economic significance. The solution also delves into sales compensation strategies, evaluating different approaches from both employee and employer perspectives. Furthermore, the assignment explores return on investment (ROI) and economic value added (EVA) calculations to assess the performance of different business divisions, offering recommendations based on the financial results. The document includes figures and calculations to support the analysis, providing a comprehensive understanding of the managerial accounting concepts discussed.

Running head: MANAGERIAL ACCOUNTING

MANAGERIAL ACCOUNTING

Name of the Student:

Name of the University:

Author’s Note:

MANAGERIAL ACCOUNTING

Name of the Student:

Name of the University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

MANAGERIAL ACCOUNTING

Table of Contents

Answer to Question 1......................................................................................................................3

Requirement (a)...........................................................................................................................3

Requirement (b)...........................................................................................................................5

Requirement (c)...........................................................................................................................7

Requirement (d)...........................................................................................................................8

Requirement (e).........................................................................................................................10

Answer to Question 2....................................................................................................................12

Answer to Question 3....................................................................................................................14

Requirement A...........................................................................................................................14

Requirement B...........................................................................................................................15

Requirement C...........................................................................................................................16

Answer to Question 4....................................................................................................................17

Requirement (a).........................................................................................................................17

Requirement (b).........................................................................................................................18

Requirement (c).........................................................................................................................18

Answer to Question 5....................................................................................................................19

Requirement (a).........................................................................................................................19

Requirement (b).........................................................................................................................20

Requirement (c).........................................................................................................................20

MANAGERIAL ACCOUNTING

Table of Contents

Answer to Question 1......................................................................................................................3

Requirement (a)...........................................................................................................................3

Requirement (b)...........................................................................................................................5

Requirement (c)...........................................................................................................................7

Requirement (d)...........................................................................................................................8

Requirement (e).........................................................................................................................10

Answer to Question 2....................................................................................................................12

Answer to Question 3....................................................................................................................14

Requirement A...........................................................................................................................14

Requirement B...........................................................................................................................15

Requirement C...........................................................................................................................16

Answer to Question 4....................................................................................................................17

Requirement (a).........................................................................................................................17

Requirement (b).........................................................................................................................18

Requirement (c).........................................................................................................................18

Answer to Question 5....................................................................................................................19

Requirement (a).........................................................................................................................19

Requirement (b).........................................................................................................................20

Requirement (c).........................................................................................................................20

2

MANAGERIAL ACCOUNTING

Requirement (d).........................................................................................................................21

Answer to Question 6....................................................................................................................21

Requirement 1............................................................................................................................21

Requirement 2............................................................................................................................26

Requirement 3............................................................................................................................26

Reference.......................................................................................................................................27

MANAGERIAL ACCOUNTING

Requirement (d).........................................................................................................................21

Answer to Question 6....................................................................................................................21

Requirement 1............................................................................................................................21

Requirement 2............................................................................................................................26

Requirement 3............................................................................................................................26

Reference.......................................................................................................................................27

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

MANAGERIAL ACCOUNTING

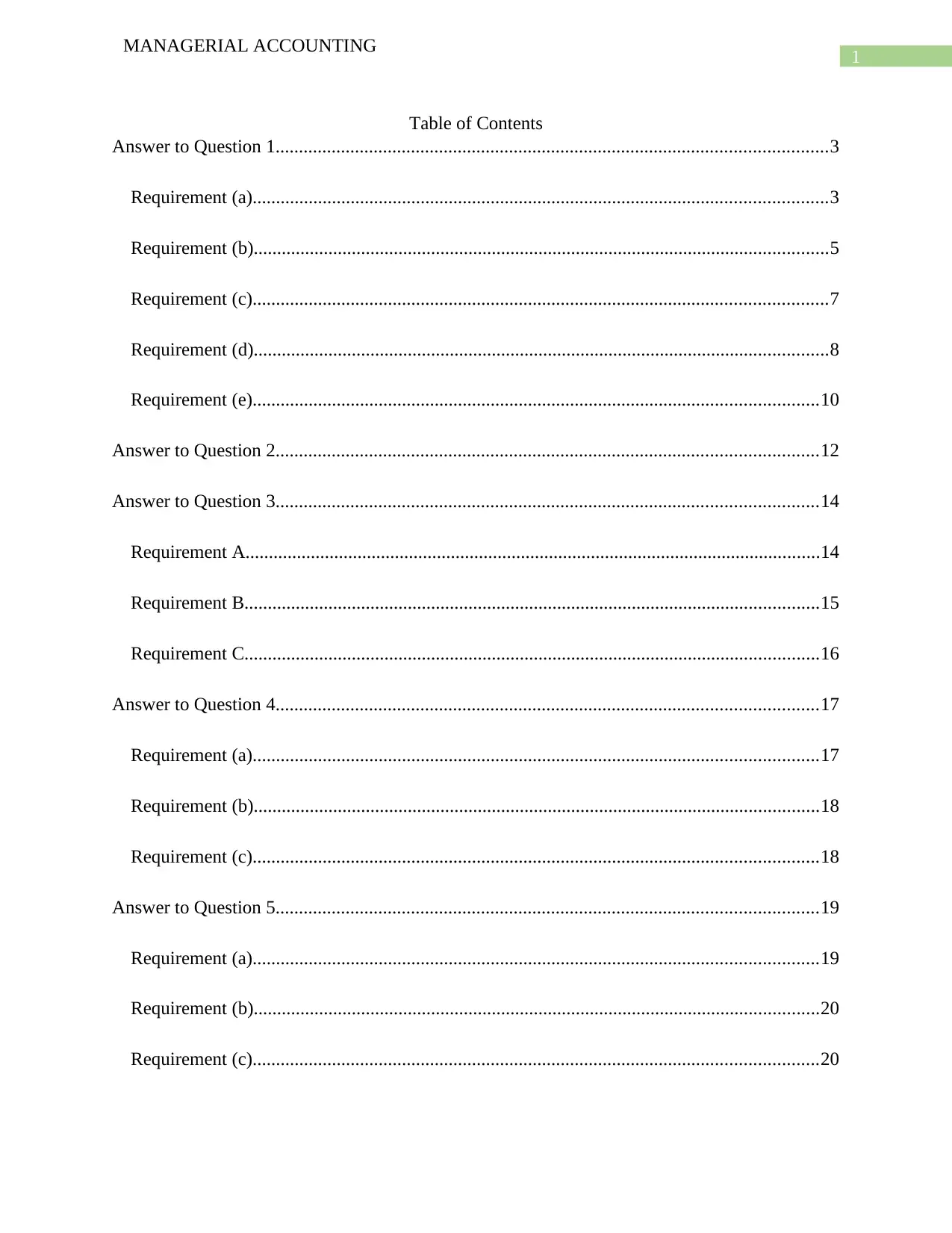

Answer to Question 1

Requirement (a)

Particulars Amount

Budgeted Variable Overhead Costs $36,000

Total Estimated Overhead Cost $36,000

Budgeted Output 9000

Machine Hours required per unit 2

Budgeted Machine Hours 18000

Predetermined Overhead Rate $2.00

Predetermined Overhead Rate:

Figure 1: (Image showing Predetermined Overhead rate)

Source: (Created by Author)

Particulars Amount

Actual Variable Overhead Costs $38,000

Actual Machine Hours 15000

Predetermined Overhead Rate $2

Standard Overhead for Actual Hours $30,000

Variable Overhead Spending Variances $8,000

Adverse

Figure 2: (Image showing Variable Overhead Variances)

Source: (Created by Author)

MANAGERIAL ACCOUNTING

Answer to Question 1

Requirement (a)

Particulars Amount

Budgeted Variable Overhead Costs $36,000

Total Estimated Overhead Cost $36,000

Budgeted Output 9000

Machine Hours required per unit 2

Budgeted Machine Hours 18000

Predetermined Overhead Rate $2.00

Predetermined Overhead Rate:

Figure 1: (Image showing Predetermined Overhead rate)

Source: (Created by Author)

Particulars Amount

Actual Variable Overhead Costs $38,000

Actual Machine Hours 15000

Predetermined Overhead Rate $2

Standard Overhead for Actual Hours $30,000

Variable Overhead Spending Variances $8,000

Adverse

Figure 2: (Image showing Variable Overhead Variances)

Source: (Created by Author)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

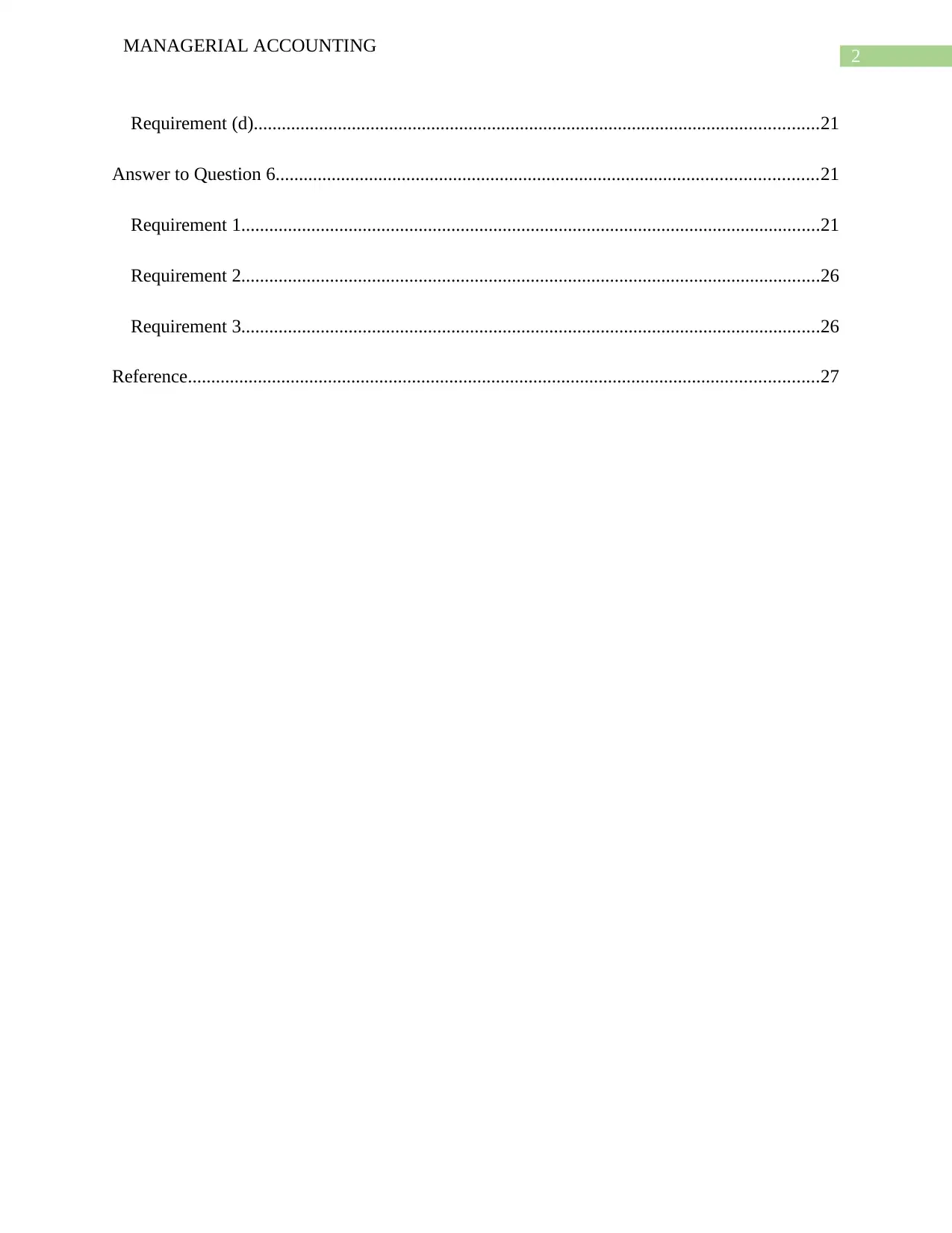

MANAGERIAL ACCOUNTING

Particulars Amount

Actual Output 8000

Machine Hours required per unit 2

Standard Hours for Actual Output 16000

Predetermined Overhead Rate $2.00

Standard Overhead for Standard Hours $32,000.00

Actual Hours 15000

Standard Overhead for Actual Hours $30,000.00

Variable Overhead Efficiency Variances $2,000

Favorable

Figure 3: (Image showing Variable Overhead Efficiency Variances)

Source: (Created by Author)

Particulars Amount

Actual Fixed Overhead $70,000

Budgeted Fixed Overhead $72,000

Fixed Overhead Spending Variance -$2,000

Favorable

Figure 4: (Image showing Fixed Overhead Spending Variance)

Source: (Created by Author)

Particulars Amount

Budgeted Fixed Overhead $72,000

Budgeted Output 9000

Standard Fixed Overhead Absorption Rate $8

Actual Output 8000

Standard Overhead for Actual Output $64,000

Fixed Overhead Volume Variance -$8,000

Adverse

Figure 5: (Image showing Fixed Overhead Volume Variance)

MANAGERIAL ACCOUNTING

Particulars Amount

Actual Output 8000

Machine Hours required per unit 2

Standard Hours for Actual Output 16000

Predetermined Overhead Rate $2.00

Standard Overhead for Standard Hours $32,000.00

Actual Hours 15000

Standard Overhead for Actual Hours $30,000.00

Variable Overhead Efficiency Variances $2,000

Favorable

Figure 3: (Image showing Variable Overhead Efficiency Variances)

Source: (Created by Author)

Particulars Amount

Actual Fixed Overhead $70,000

Budgeted Fixed Overhead $72,000

Fixed Overhead Spending Variance -$2,000

Favorable

Figure 4: (Image showing Fixed Overhead Spending Variance)

Source: (Created by Author)

Particulars Amount

Budgeted Fixed Overhead $72,000

Budgeted Output 9000

Standard Fixed Overhead Absorption Rate $8

Actual Output 8000

Standard Overhead for Actual Output $64,000

Fixed Overhead Volume Variance -$8,000

Adverse

Figure 5: (Image showing Fixed Overhead Volume Variance)

5

MANAGERIAL ACCOUNTING

Source: (Created by Author)

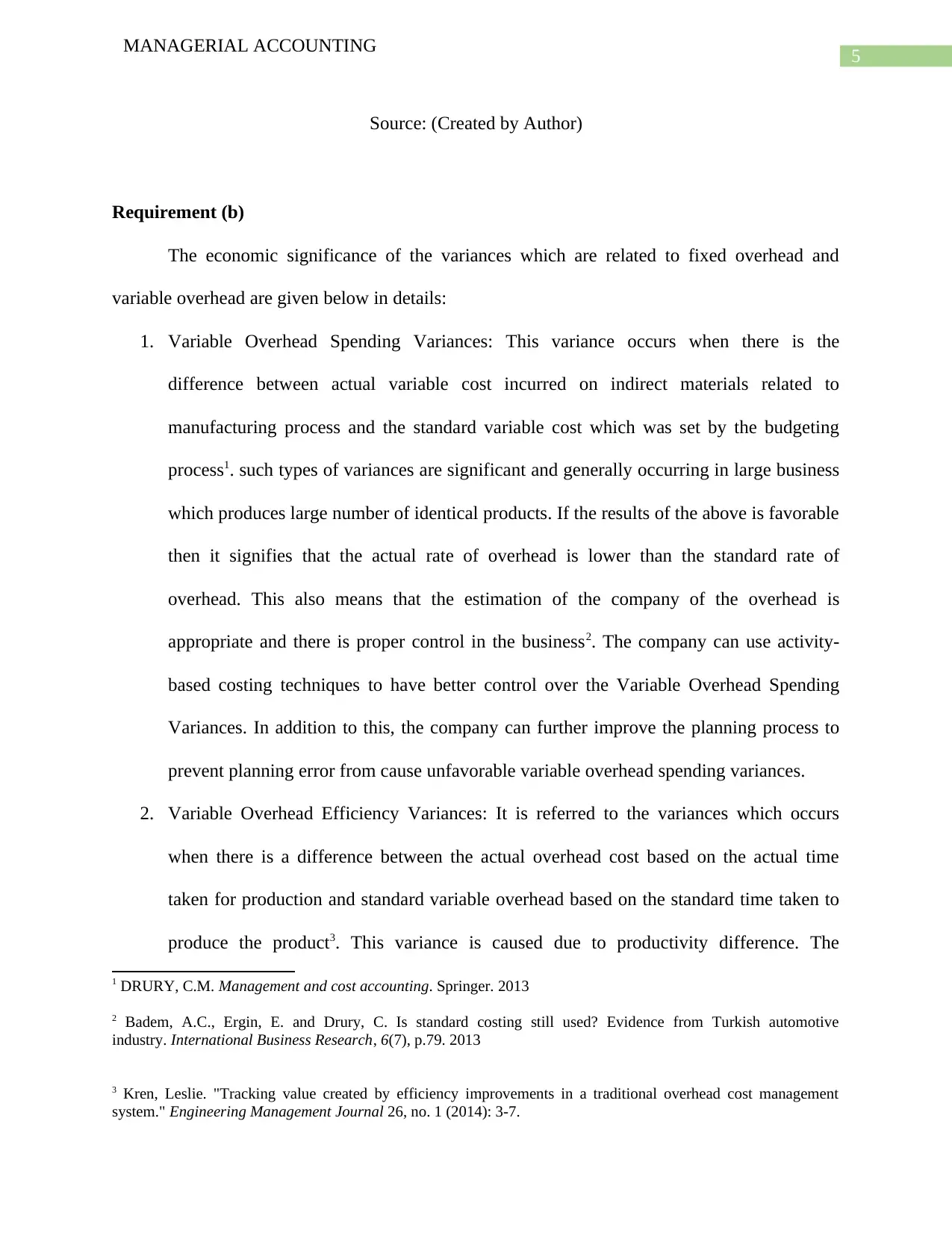

Requirement (b)

The economic significance of the variances which are related to fixed overhead and

variable overhead are given below in details:

1. Variable Overhead Spending Variances: This variance occurs when there is the

difference between actual variable cost incurred on indirect materials related to

manufacturing process and the standard variable cost which was set by the budgeting

process1. such types of variances are significant and generally occurring in large business

which produces large number of identical products. If the results of the above is favorable

then it signifies that the actual rate of overhead is lower than the standard rate of

overhead. This also means that the estimation of the company of the overhead is

appropriate and there is proper control in the business2. The company can use activity-

based costing techniques to have better control over the Variable Overhead Spending

Variances. In addition to this, the company can further improve the planning process to

prevent planning error from cause unfavorable variable overhead spending variances.

2. Variable Overhead Efficiency Variances: It is referred to the variances which occurs

when there is a difference between the actual overhead cost based on the actual time

taken for production and standard variable overhead based on the standard time taken to

produce the product3. This variance is caused due to productivity difference. The

1 DRURY, C.M. Management and cost accounting. Springer. 2013

2 Badem, A.C., Ergin, E. and Drury, C. Is standard costing still used? Evidence from Turkish automotive

industry. International Business Research, 6(7), p.79. 2013

3 Kren, Leslie. "Tracking value created by efficiency improvements in a traditional overhead cost management

system." Engineering Management Journal 26, no. 1 (2014): 3-7.

MANAGERIAL ACCOUNTING

Source: (Created by Author)

Requirement (b)

The economic significance of the variances which are related to fixed overhead and

variable overhead are given below in details:

1. Variable Overhead Spending Variances: This variance occurs when there is the

difference between actual variable cost incurred on indirect materials related to

manufacturing process and the standard variable cost which was set by the budgeting

process1. such types of variances are significant and generally occurring in large business

which produces large number of identical products. If the results of the above is favorable

then it signifies that the actual rate of overhead is lower than the standard rate of

overhead. This also means that the estimation of the company of the overhead is

appropriate and there is proper control in the business2. The company can use activity-

based costing techniques to have better control over the Variable Overhead Spending

Variances. In addition to this, the company can further improve the planning process to

prevent planning error from cause unfavorable variable overhead spending variances.

2. Variable Overhead Efficiency Variances: It is referred to the variances which occurs

when there is a difference between the actual overhead cost based on the actual time

taken for production and standard variable overhead based on the standard time taken to

produce the product3. This variance is caused due to productivity difference. The

1 DRURY, C.M. Management and cost accounting. Springer. 2013

2 Badem, A.C., Ergin, E. and Drury, C. Is standard costing still used? Evidence from Turkish automotive

industry. International Business Research, 6(7), p.79. 2013

3 Kren, Leslie. "Tracking value created by efficiency improvements in a traditional overhead cost management

system." Engineering Management Journal 26, no. 1 (2014): 3-7.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

MANAGERIAL ACCOUNTING

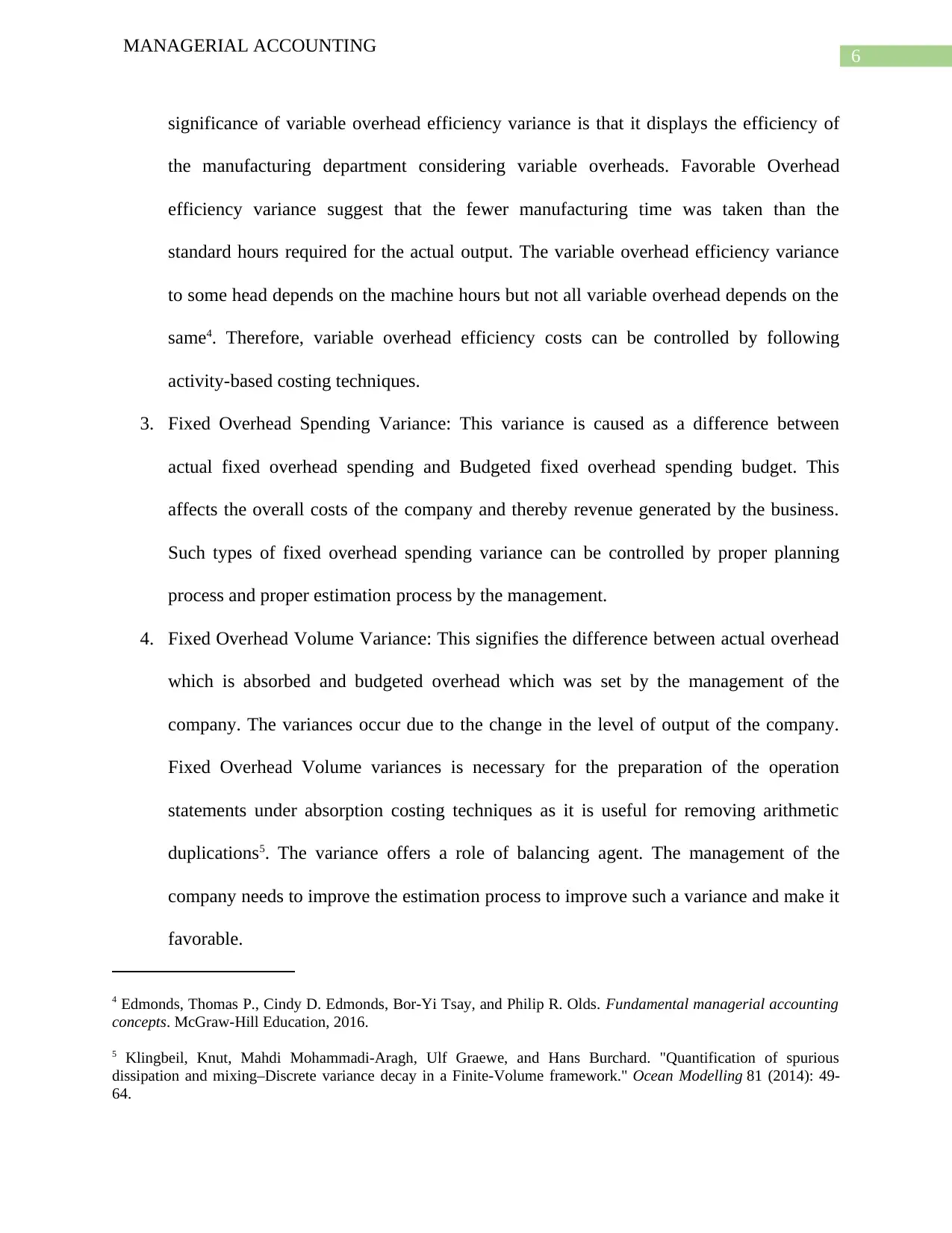

significance of variable overhead efficiency variance is that it displays the efficiency of

the manufacturing department considering variable overheads. Favorable Overhead

efficiency variance suggest that the fewer manufacturing time was taken than the

standard hours required for the actual output. The variable overhead efficiency variance

to some head depends on the machine hours but not all variable overhead depends on the

same4. Therefore, variable overhead efficiency costs can be controlled by following

activity-based costing techniques.

3. Fixed Overhead Spending Variance: This variance is caused as a difference between

actual fixed overhead spending and Budgeted fixed overhead spending budget. This

affects the overall costs of the company and thereby revenue generated by the business.

Such types of fixed overhead spending variance can be controlled by proper planning

process and proper estimation process by the management.

4. Fixed Overhead Volume Variance: This signifies the difference between actual overhead

which is absorbed and budgeted overhead which was set by the management of the

company. The variances occur due to the change in the level of output of the company.

Fixed Overhead Volume variances is necessary for the preparation of the operation

statements under absorption costing techniques as it is useful for removing arithmetic

duplications5. The variance offers a role of balancing agent. The management of the

company needs to improve the estimation process to improve such a variance and make it

favorable.

4 Edmonds, Thomas P., Cindy D. Edmonds, Bor-Yi Tsay, and Philip R. Olds. Fundamental managerial accounting

concepts. McGraw-Hill Education, 2016.

5 Klingbeil, Knut, Mahdi Mohammadi-Aragh, Ulf Graewe, and Hans Burchard. "Quantification of spurious

dissipation and mixing–Discrete variance decay in a Finite-Volume framework." Ocean Modelling 81 (2014): 49-

64.

MANAGERIAL ACCOUNTING

significance of variable overhead efficiency variance is that it displays the efficiency of

the manufacturing department considering variable overheads. Favorable Overhead

efficiency variance suggest that the fewer manufacturing time was taken than the

standard hours required for the actual output. The variable overhead efficiency variance

to some head depends on the machine hours but not all variable overhead depends on the

same4. Therefore, variable overhead efficiency costs can be controlled by following

activity-based costing techniques.

3. Fixed Overhead Spending Variance: This variance is caused as a difference between

actual fixed overhead spending and Budgeted fixed overhead spending budget. This

affects the overall costs of the company and thereby revenue generated by the business.

Such types of fixed overhead spending variance can be controlled by proper planning

process and proper estimation process by the management.

4. Fixed Overhead Volume Variance: This signifies the difference between actual overhead

which is absorbed and budgeted overhead which was set by the management of the

company. The variances occur due to the change in the level of output of the company.

Fixed Overhead Volume variances is necessary for the preparation of the operation

statements under absorption costing techniques as it is useful for removing arithmetic

duplications5. The variance offers a role of balancing agent. The management of the

company needs to improve the estimation process to improve such a variance and make it

favorable.

4 Edmonds, Thomas P., Cindy D. Edmonds, Bor-Yi Tsay, and Philip R. Olds. Fundamental managerial accounting

concepts. McGraw-Hill Education, 2016.

5 Klingbeil, Knut, Mahdi Mohammadi-Aragh, Ulf Graewe, and Hans Burchard. "Quantification of spurious

dissipation and mixing–Discrete variance decay in a Finite-Volume framework." Ocean Modelling 81 (2014): 49-

64.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

MANAGERIAL ACCOUNTING

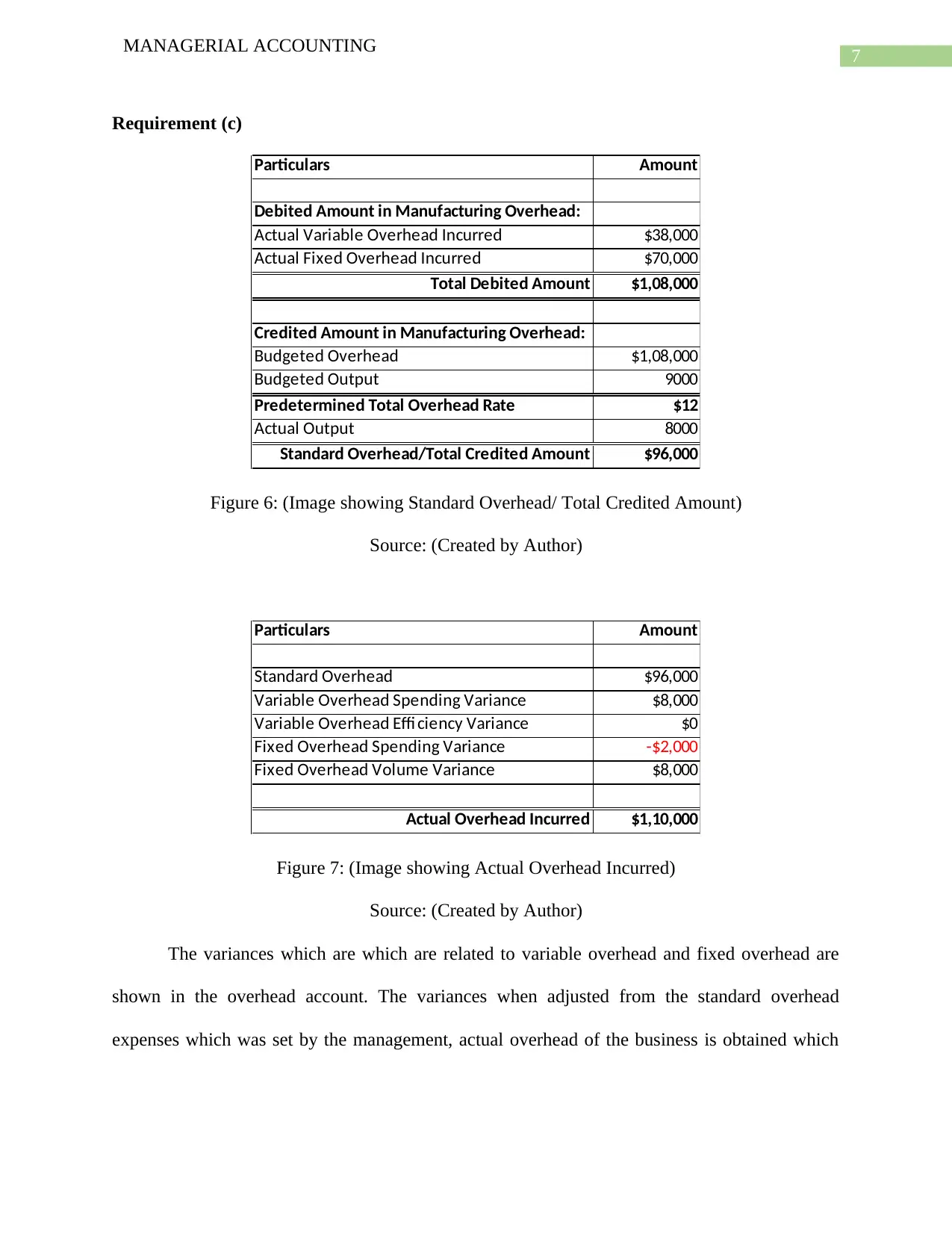

Requirement (c)

Particulars Amount

Debited Amount in Manufacturing Overhead:

Actual Variable Overhead Incurred $38,000

Actual Fixed Overhead Incurred $70,000

Total Debited Amount $1,08,000

Credited Amount in Manufacturing Overhead:

Budgeted Overhead $1,08,000

Budgeted Output 9000

Predetermined Total Overhead Rate $12

Actual Output 8000

Standard Overhead/Total Credited Amount $96,000

Figure 6: (Image showing Standard Overhead/ Total Credited Amount)

Source: (Created by Author)

Particulars Amount

Standard Overhead $96,000

Variable Overhead Spending Variance $8,000

Variable Overhead Effi ciency Variance $0

Fixed Overhead Spending Variance -$2,000

Fixed Overhead Volume Variance $8,000

Actual Overhead Incurred $1,10,000

Figure 7: (Image showing Actual Overhead Incurred)

Source: (Created by Author)

The variances which are which are related to variable overhead and fixed overhead are

shown in the overhead account. The variances when adjusted from the standard overhead

expenses which was set by the management, actual overhead of the business is obtained which

MANAGERIAL ACCOUNTING

Requirement (c)

Particulars Amount

Debited Amount in Manufacturing Overhead:

Actual Variable Overhead Incurred $38,000

Actual Fixed Overhead Incurred $70,000

Total Debited Amount $1,08,000

Credited Amount in Manufacturing Overhead:

Budgeted Overhead $1,08,000

Budgeted Output 9000

Predetermined Total Overhead Rate $12

Actual Output 8000

Standard Overhead/Total Credited Amount $96,000

Figure 6: (Image showing Standard Overhead/ Total Credited Amount)

Source: (Created by Author)

Particulars Amount

Standard Overhead $96,000

Variable Overhead Spending Variance $8,000

Variable Overhead Effi ciency Variance $0

Fixed Overhead Spending Variance -$2,000

Fixed Overhead Volume Variance $8,000

Actual Overhead Incurred $1,10,000

Figure 7: (Image showing Actual Overhead Incurred)

Source: (Created by Author)

The variances which are which are related to variable overhead and fixed overhead are

shown in the overhead account. The variances when adjusted from the standard overhead

expenses which was set by the management, actual overhead of the business is obtained which

8

MANAGERIAL ACCOUNTING

establishes a relationship between them6. The favorable variances are added while unfavorable

variances are deducted to get the actual overhead expenses of the company.

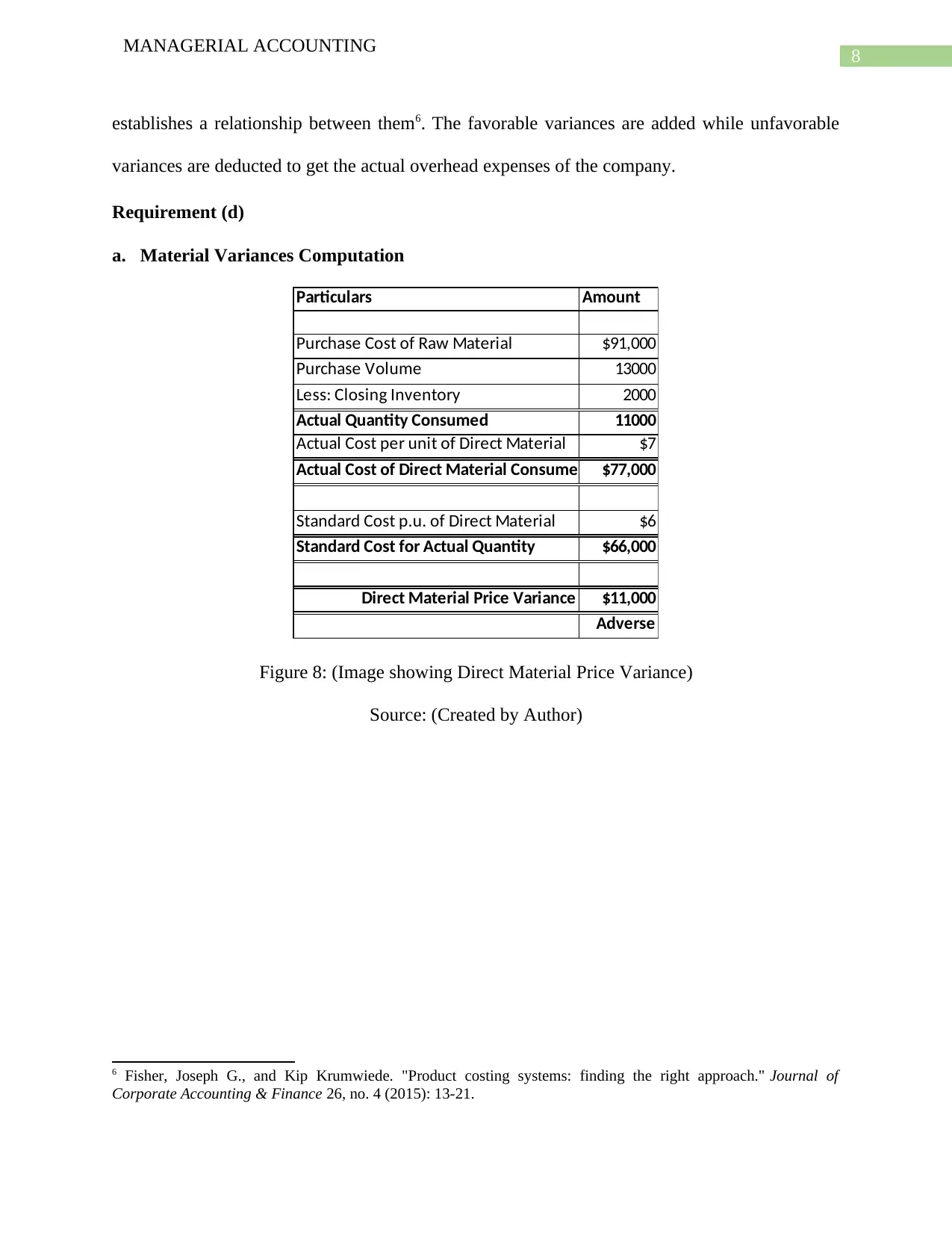

Requirement (d)

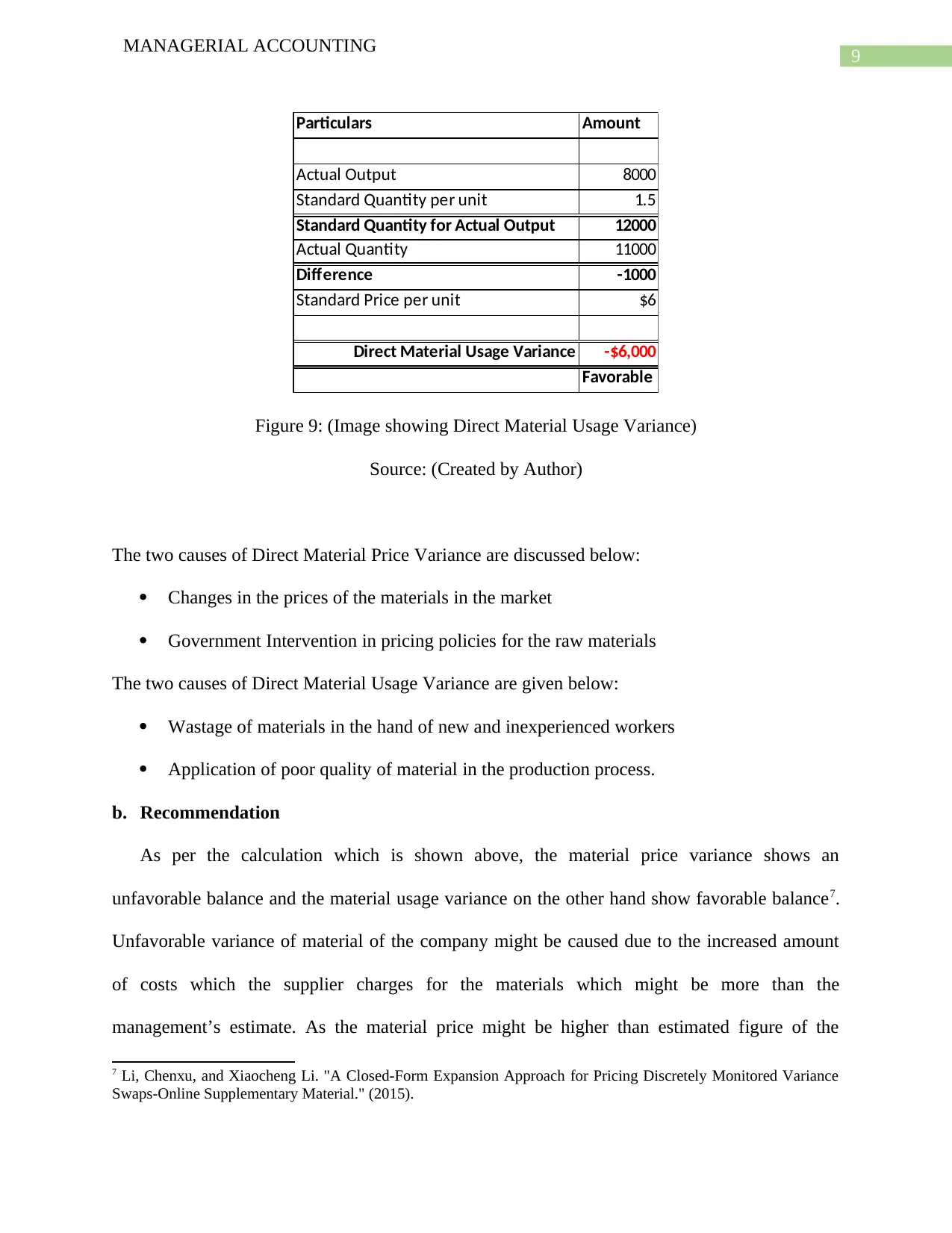

a. Material Variances Computation

Particulars Amount

Purchase Cost of Raw Material $91,000

Purchase Volume 13000

Less: Closing Inventory 2000

Actual Quantity Consumed 11000

Actual Cost per unit of Direct Material $7

Actual Cost of Direct Material Consumed $77,000

Standard Cost p.u. of Direct Material $6

Standard Cost for Actual Quantity $66,000

Direct Material Price Variance $11,000

Adverse

Figure 8: (Image showing Direct Material Price Variance)

Source: (Created by Author)

6 Fisher, Joseph G., and Kip Krumwiede. "Product costing systems: finding the right approach." Journal of

Corporate Accounting & Finance 26, no. 4 (2015): 13-21.

MANAGERIAL ACCOUNTING

establishes a relationship between them6. The favorable variances are added while unfavorable

variances are deducted to get the actual overhead expenses of the company.

Requirement (d)

a. Material Variances Computation

Particulars Amount

Purchase Cost of Raw Material $91,000

Purchase Volume 13000

Less: Closing Inventory 2000

Actual Quantity Consumed 11000

Actual Cost per unit of Direct Material $7

Actual Cost of Direct Material Consumed $77,000

Standard Cost p.u. of Direct Material $6

Standard Cost for Actual Quantity $66,000

Direct Material Price Variance $11,000

Adverse

Figure 8: (Image showing Direct Material Price Variance)

Source: (Created by Author)

6 Fisher, Joseph G., and Kip Krumwiede. "Product costing systems: finding the right approach." Journal of

Corporate Accounting & Finance 26, no. 4 (2015): 13-21.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

MANAGERIAL ACCOUNTING

Particulars Amount

Actual Output 8000

Standard Quantity per unit 1.5

Standard Quantity for Actual Output 12000

Actual Quantity 11000

Difference -1000

Standard Price per unit $6

Direct Material Usage Variance -$6,000

Favorable

Figure 9: (Image showing Direct Material Usage Variance)

Source: (Created by Author)

The two causes of Direct Material Price Variance are discussed below:

Changes in the prices of the materials in the market

Government Intervention in pricing policies for the raw materials

The two causes of Direct Material Usage Variance are given below:

Wastage of materials in the hand of new and inexperienced workers

Application of poor quality of material in the production process.

b. Recommendation

As per the calculation which is shown above, the material price variance shows an

unfavorable balance and the material usage variance on the other hand show favorable balance7.

Unfavorable variance of material of the company might be caused due to the increased amount

of costs which the supplier charges for the materials which might be more than the

management’s estimate. As the material price might be higher than estimated figure of the

7 Li, Chenxu, and Xiaocheng Li. "A Closed-Form Expansion Approach for Pricing Discretely Monitored Variance

Swaps-Online Supplementary Material." (2015).

MANAGERIAL ACCOUNTING

Particulars Amount

Actual Output 8000

Standard Quantity per unit 1.5

Standard Quantity for Actual Output 12000

Actual Quantity 11000

Difference -1000

Standard Price per unit $6

Direct Material Usage Variance -$6,000

Favorable

Figure 9: (Image showing Direct Material Usage Variance)

Source: (Created by Author)

The two causes of Direct Material Price Variance are discussed below:

Changes in the prices of the materials in the market

Government Intervention in pricing policies for the raw materials

The two causes of Direct Material Usage Variance are given below:

Wastage of materials in the hand of new and inexperienced workers

Application of poor quality of material in the production process.

b. Recommendation

As per the calculation which is shown above, the material price variance shows an

unfavorable balance and the material usage variance on the other hand show favorable balance7.

Unfavorable variance of material of the company might be caused due to the increased amount

of costs which the supplier charges for the materials which might be more than the

management’s estimate. As the material price might be higher than estimated figure of the

7 Li, Chenxu, and Xiaocheng Li. "A Closed-Form Expansion Approach for Pricing Discretely Monitored Variance

Swaps-Online Supplementary Material." (2015).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

MANAGERIAL ACCOUNTING

management for materials therefore the company should reject the contract as the prices charged

for the material are more than the management estimated budget and such is the cause of the

material price variance as shown in the calculation above8.

Requirement (e)

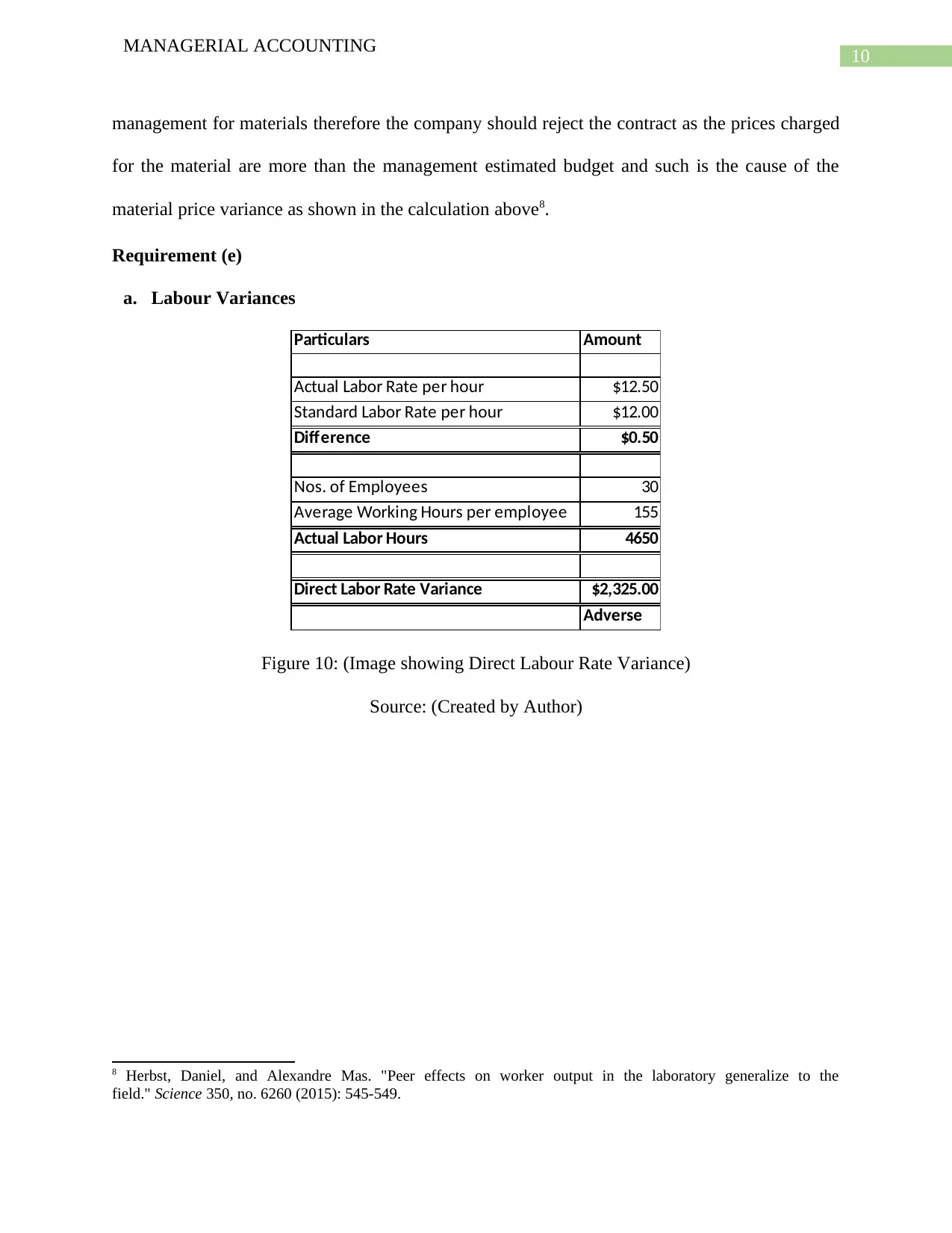

a. Labour Variances

Particulars Amount

Actual Labor Rate per hour $12.50

Standard Labor Rate per hour $12.00

Difference $0.50

Nos. of Employees 30

Average Working Hours per employee 155

Actual Labor Hours 4650

Direct Labor Rate Variance $2,325.00

Adverse

Figure 10: (Image showing Direct Labour Rate Variance)

Source: (Created by Author)

8 Herbst, Daniel, and Alexandre Mas. "Peer effects on worker output in the laboratory generalize to the

field." Science 350, no. 6260 (2015): 545-549.

MANAGERIAL ACCOUNTING

management for materials therefore the company should reject the contract as the prices charged

for the material are more than the management estimated budget and such is the cause of the

material price variance as shown in the calculation above8.

Requirement (e)

a. Labour Variances

Particulars Amount

Actual Labor Rate per hour $12.50

Standard Labor Rate per hour $12.00

Difference $0.50

Nos. of Employees 30

Average Working Hours per employee 155

Actual Labor Hours 4650

Direct Labor Rate Variance $2,325.00

Adverse

Figure 10: (Image showing Direct Labour Rate Variance)

Source: (Created by Author)

8 Herbst, Daniel, and Alexandre Mas. "Peer effects on worker output in the laboratory generalize to the

field." Science 350, no. 6260 (2015): 545-549.

11

MANAGERIAL ACCOUNTING

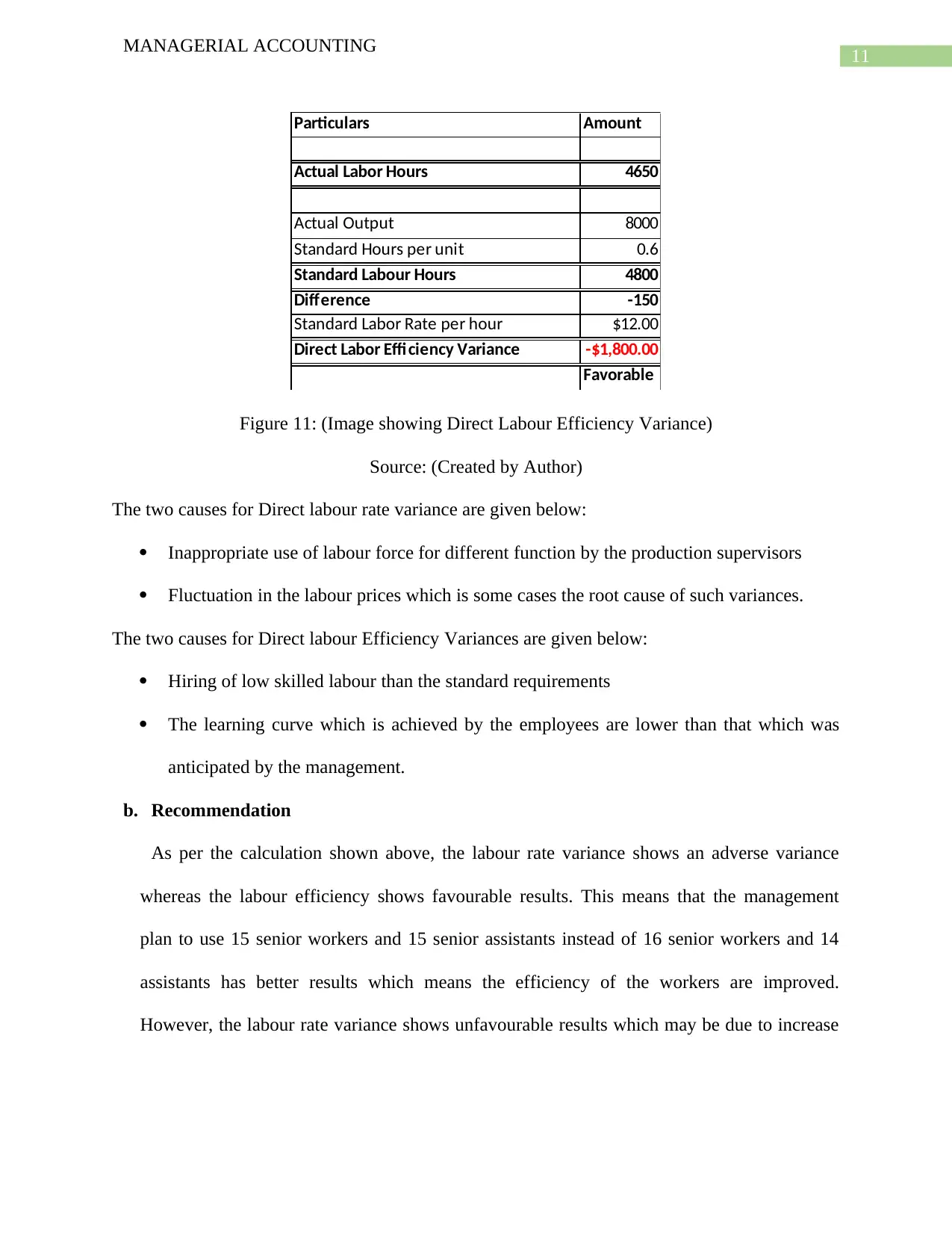

Particulars Amount

Actual Labor Hours 4650

Actual Output 8000

Standard Hours per unit 0.6

Standard Labour Hours 4800

Difference -150

Standard Labor Rate per hour $12.00

Direct Labor Efficiency Variance -$1,800.00

Favorable

Figure 11: (Image showing Direct Labour Efficiency Variance)

Source: (Created by Author)

The two causes for Direct labour rate variance are given below:

Inappropriate use of labour force for different function by the production supervisors

Fluctuation in the labour prices which is some cases the root cause of such variances.

The two causes for Direct labour Efficiency Variances are given below:

Hiring of low skilled labour than the standard requirements

The learning curve which is achieved by the employees are lower than that which was

anticipated by the management.

b. Recommendation

As per the calculation shown above, the labour rate variance shows an adverse variance

whereas the labour efficiency shows favourable results. This means that the management

plan to use 15 senior workers and 15 senior assistants instead of 16 senior workers and 14

assistants has better results which means the efficiency of the workers are improved.

However, the labour rate variance shows unfavourable results which may be due to increase

MANAGERIAL ACCOUNTING

Particulars Amount

Actual Labor Hours 4650

Actual Output 8000

Standard Hours per unit 0.6

Standard Labour Hours 4800

Difference -150

Standard Labor Rate per hour $12.00

Direct Labor Efficiency Variance -$1,800.00

Favorable

Figure 11: (Image showing Direct Labour Efficiency Variance)

Source: (Created by Author)

The two causes for Direct labour rate variance are given below:

Inappropriate use of labour force for different function by the production supervisors

Fluctuation in the labour prices which is some cases the root cause of such variances.

The two causes for Direct labour Efficiency Variances are given below:

Hiring of low skilled labour than the standard requirements

The learning curve which is achieved by the employees are lower than that which was

anticipated by the management.

b. Recommendation

As per the calculation shown above, the labour rate variance shows an adverse variance

whereas the labour efficiency shows favourable results. This means that the management

plan to use 15 senior workers and 15 senior assistants instead of 16 senior workers and 14

assistants has better results which means the efficiency of the workers are improved.

However, the labour rate variance shows unfavourable results which may be due to increase

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 30

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.