Managerial Economics Assignment on Market Dynamics and Profit

VerifiedAdded on 2020/04/21

|12

|1257

|68

Homework Assignment

AI Summary

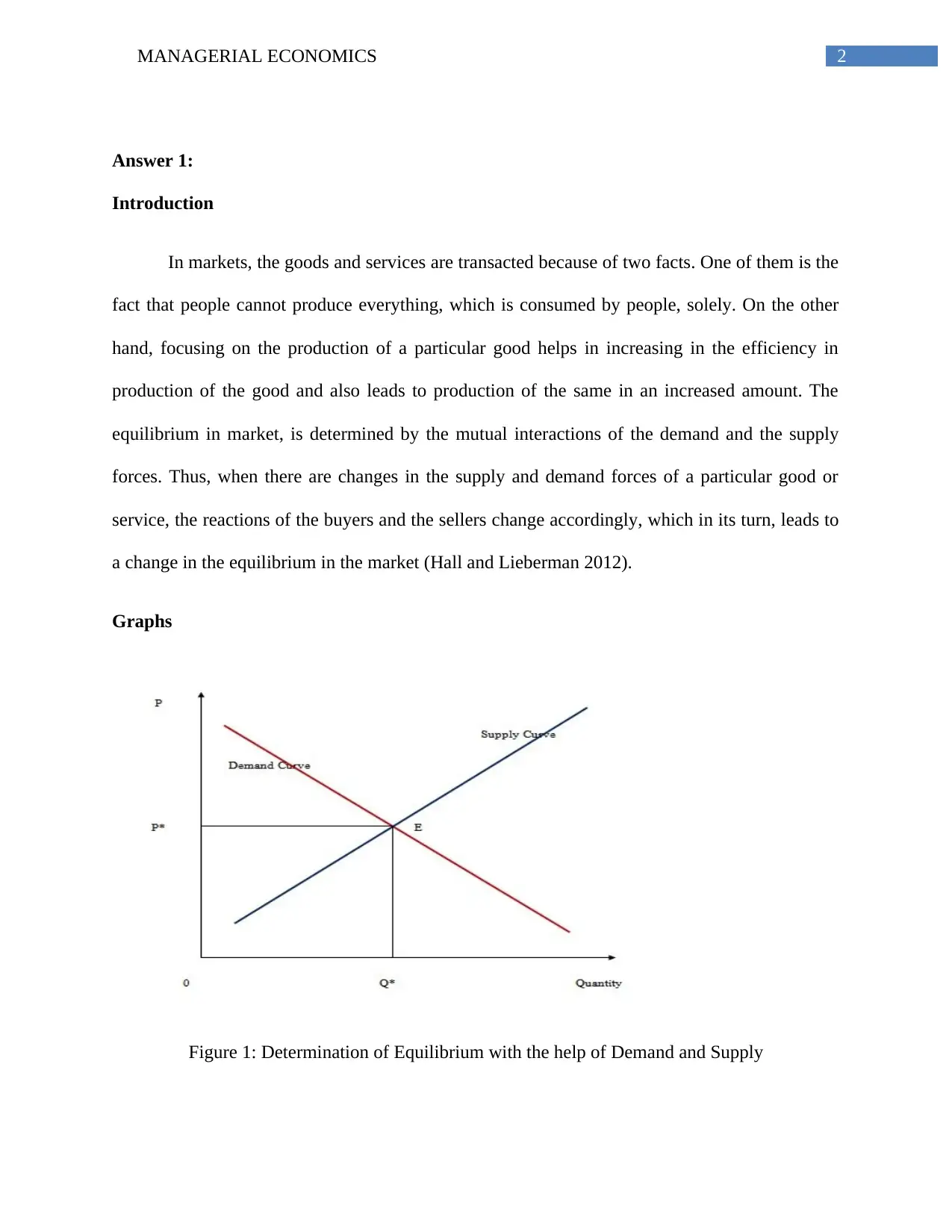

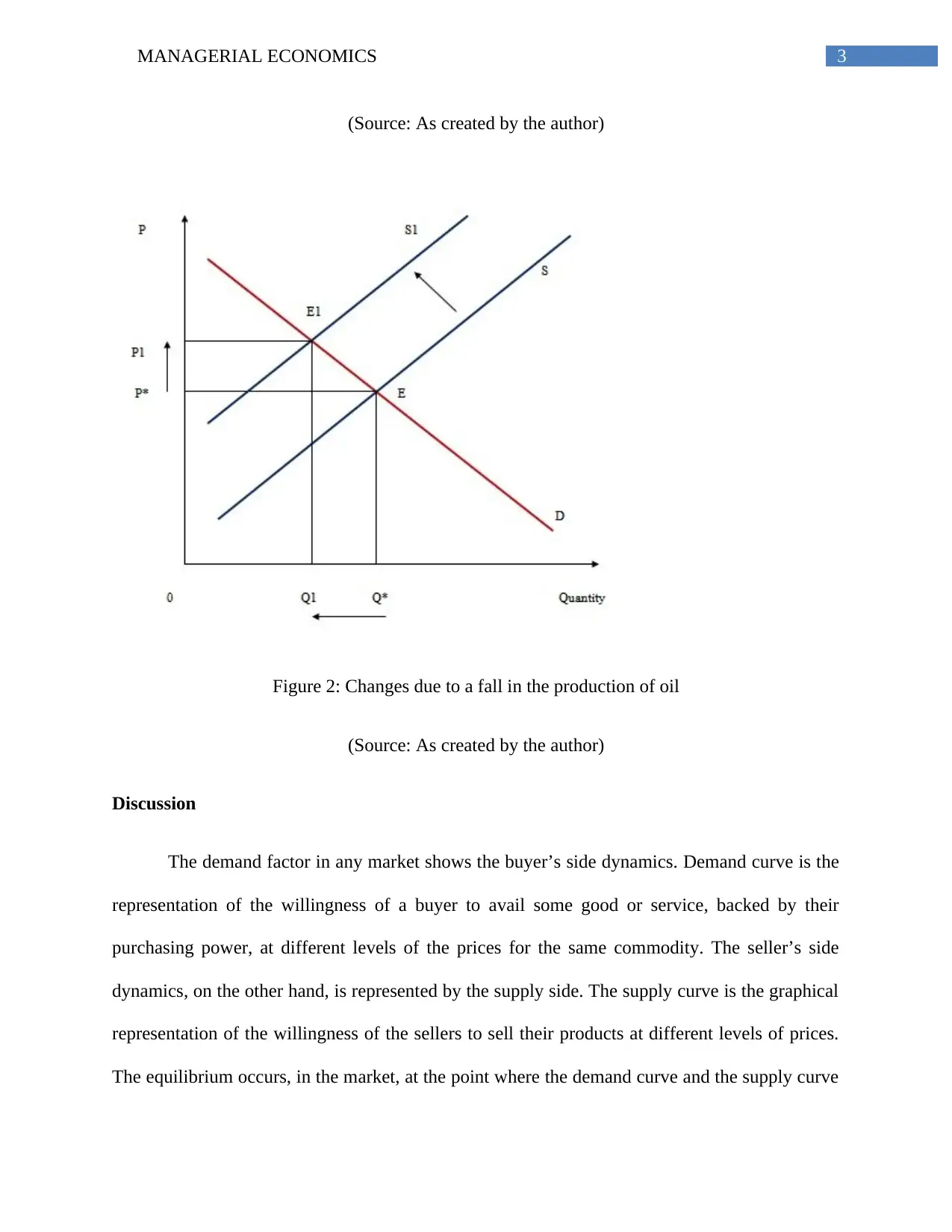

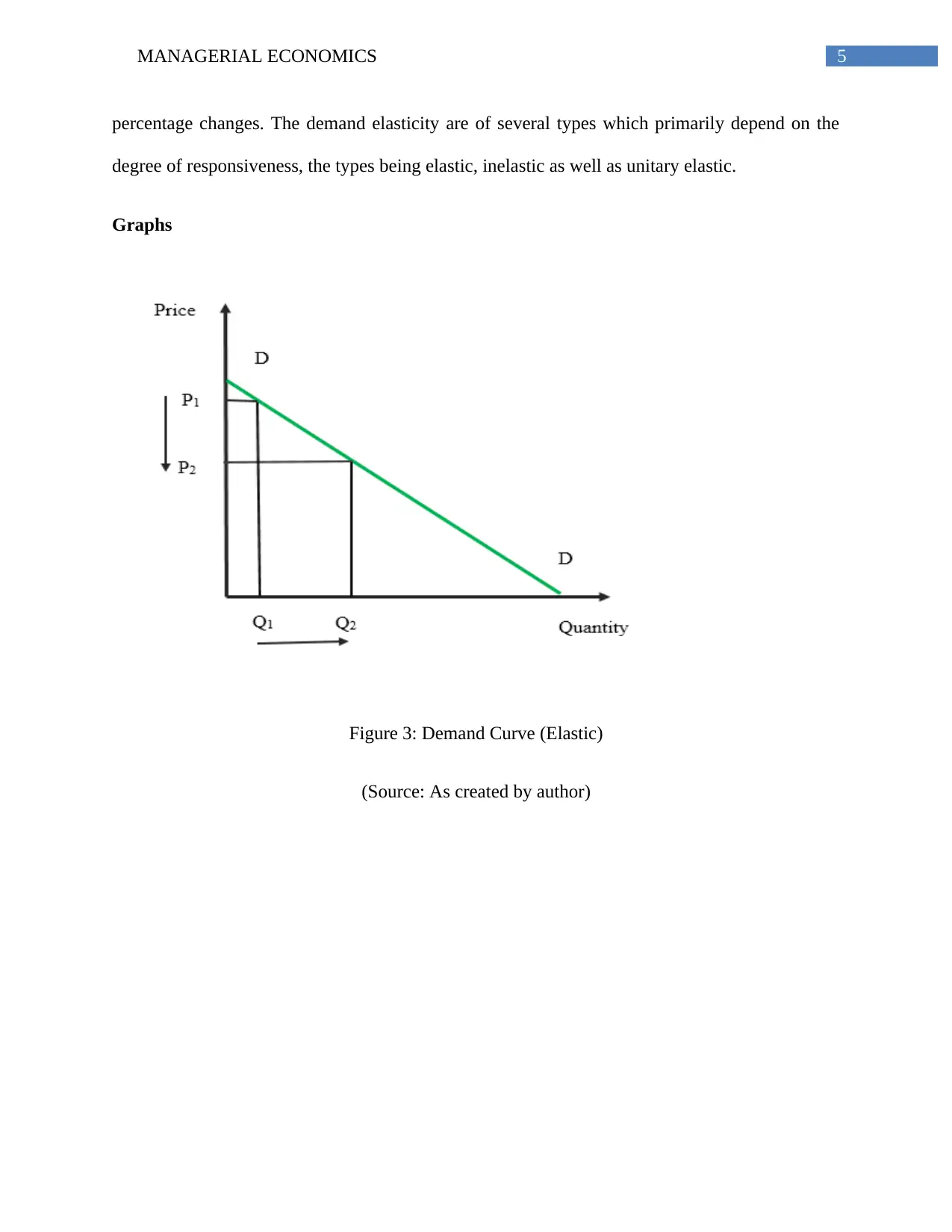

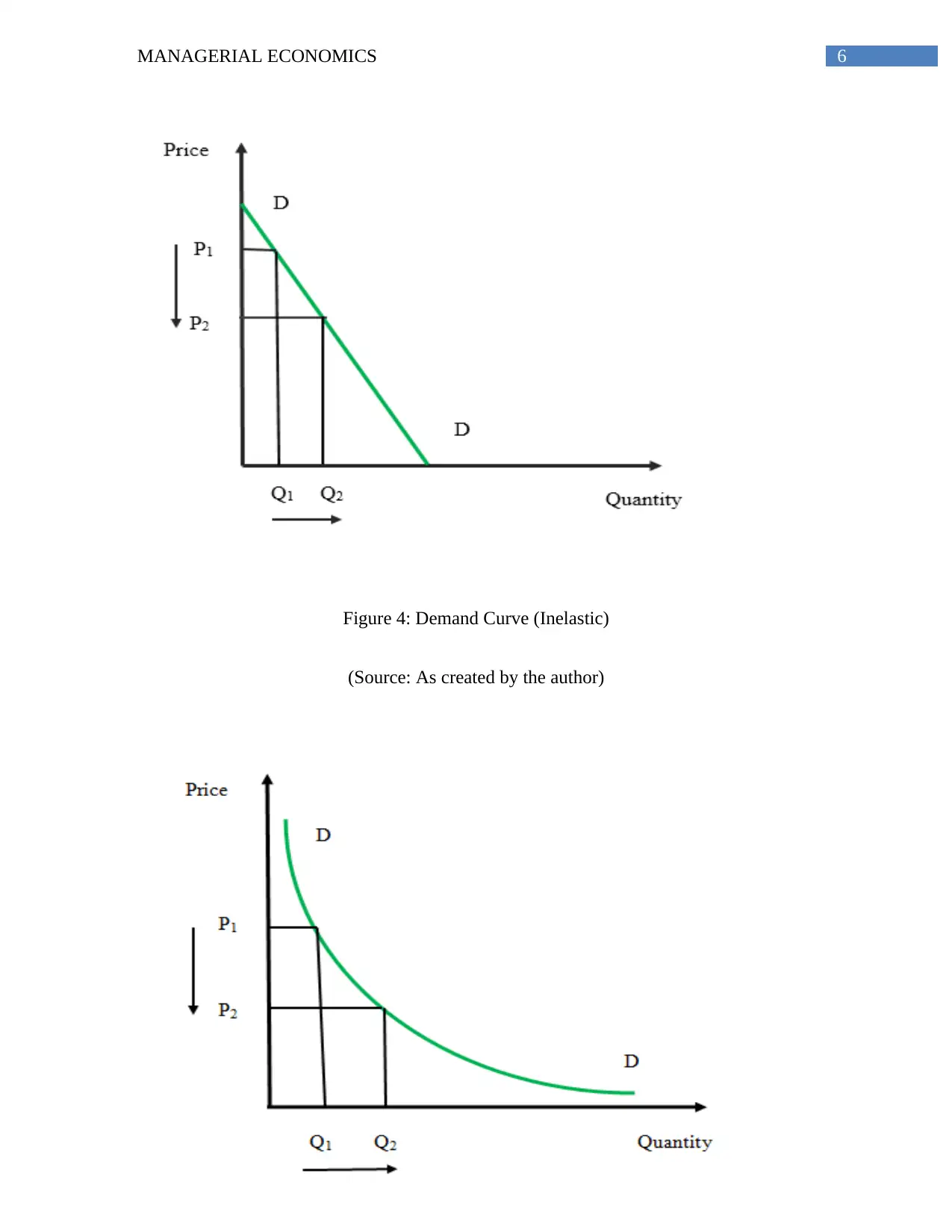

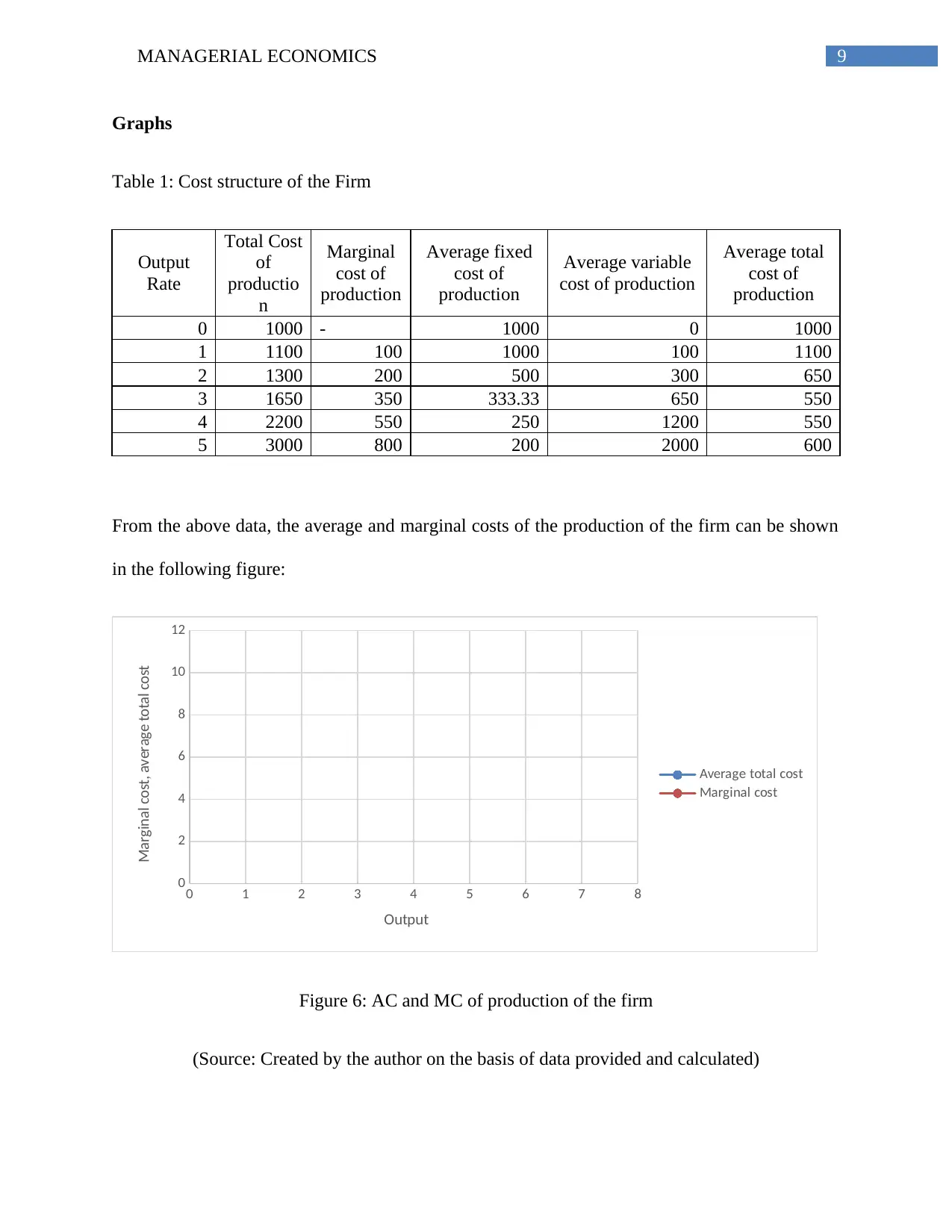

This managerial economics assignment explores core concepts including market equilibrium, elasticity of demand, and cost structures. The first section analyzes market equilibrium, illustrating how supply and demand interact to determine prices and quantities, and demonstrating the impact of shifts in supply, such as a reduction in oil production. The second section focuses on price elasticity of demand, categorizing demand as elastic, inelastic, or unitary elastic, with examples of each. The final section examines profit maximization, showing how firms aim to minimize average costs, using a cost structure table and a graph to determine the output level at which average cost is minimized. The assignment provides a comprehensive overview of these key economic principles.

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.