Managerial Finance Report: Funding, Investment, and Company Evaluation

VerifiedAdded on 2020/06/04

|16

|3806

|28

Report

AI Summary

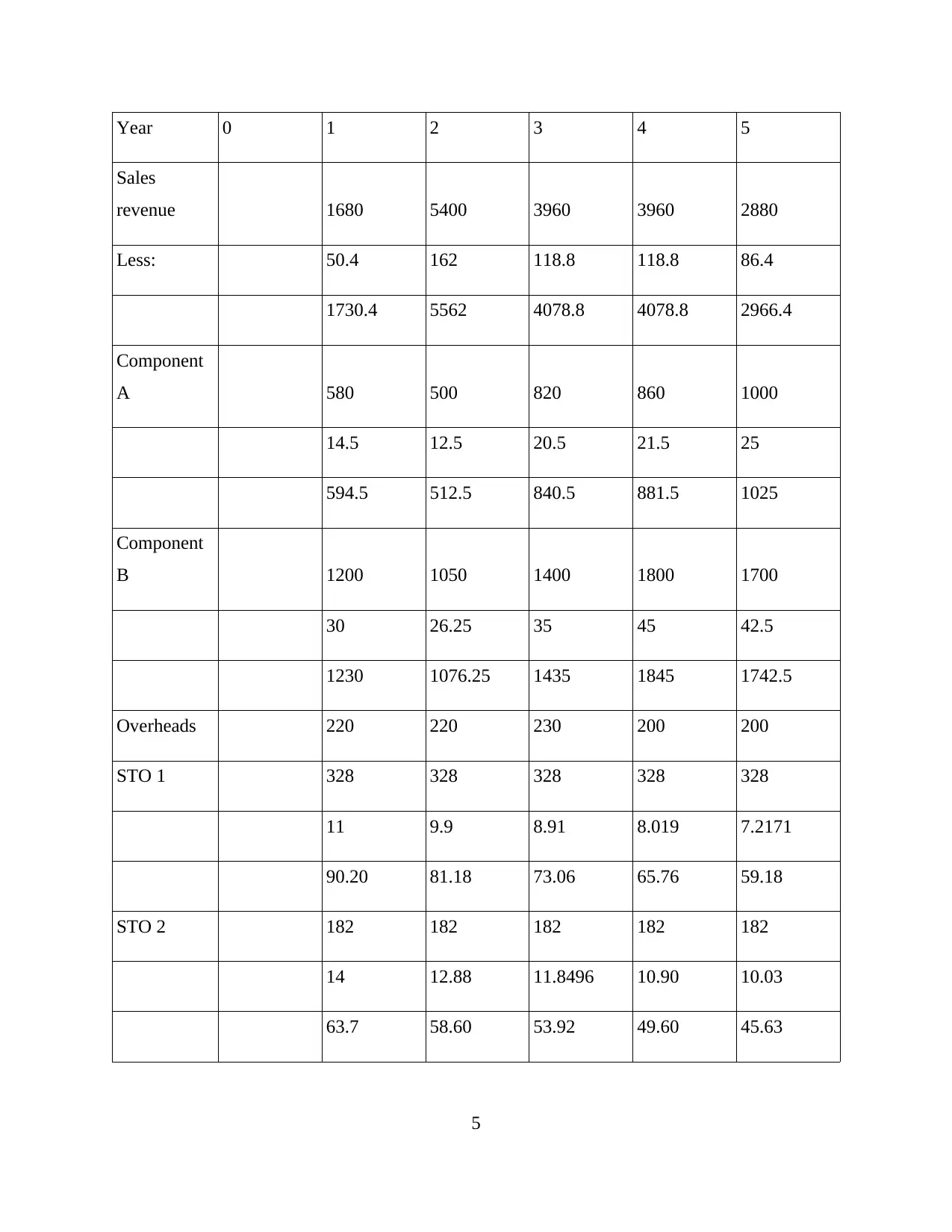

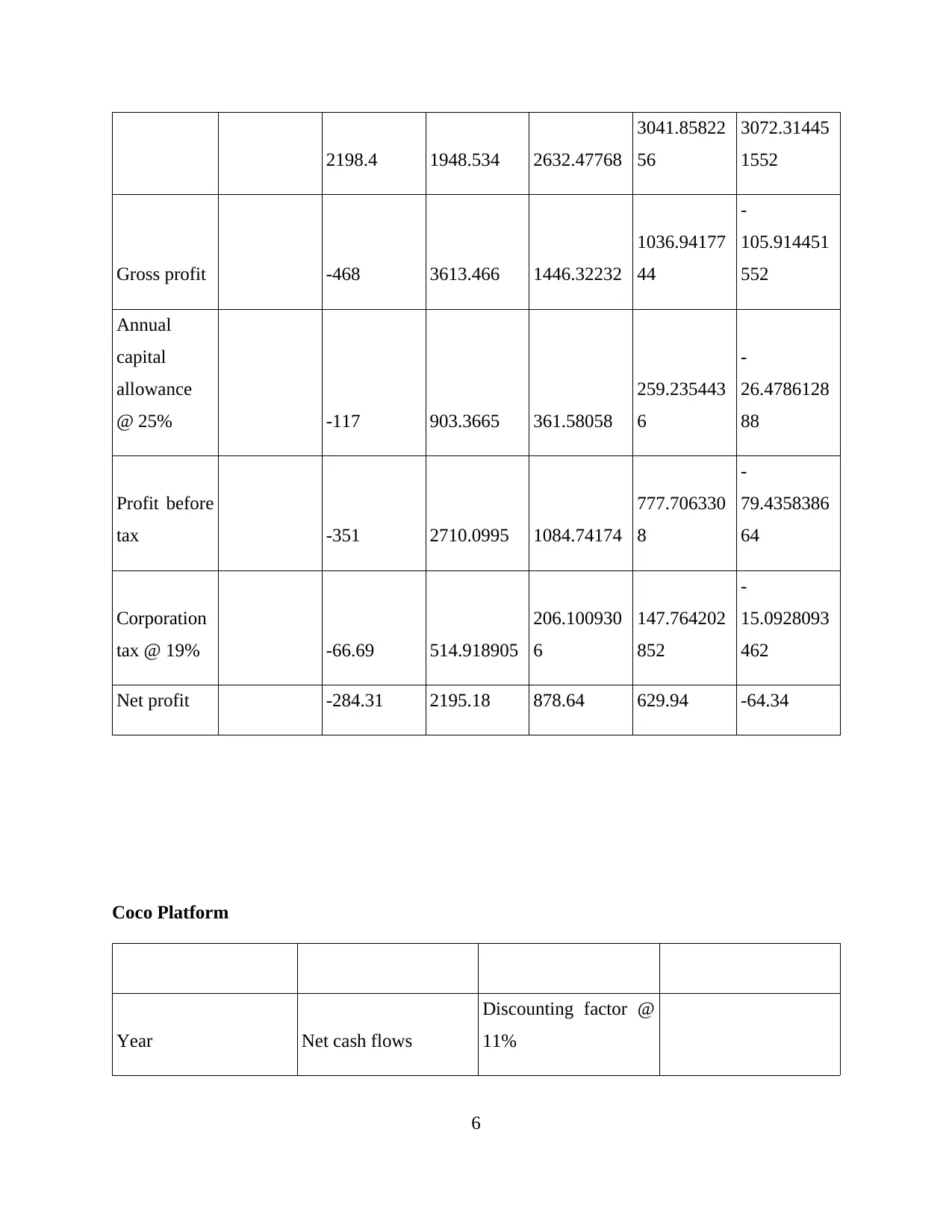

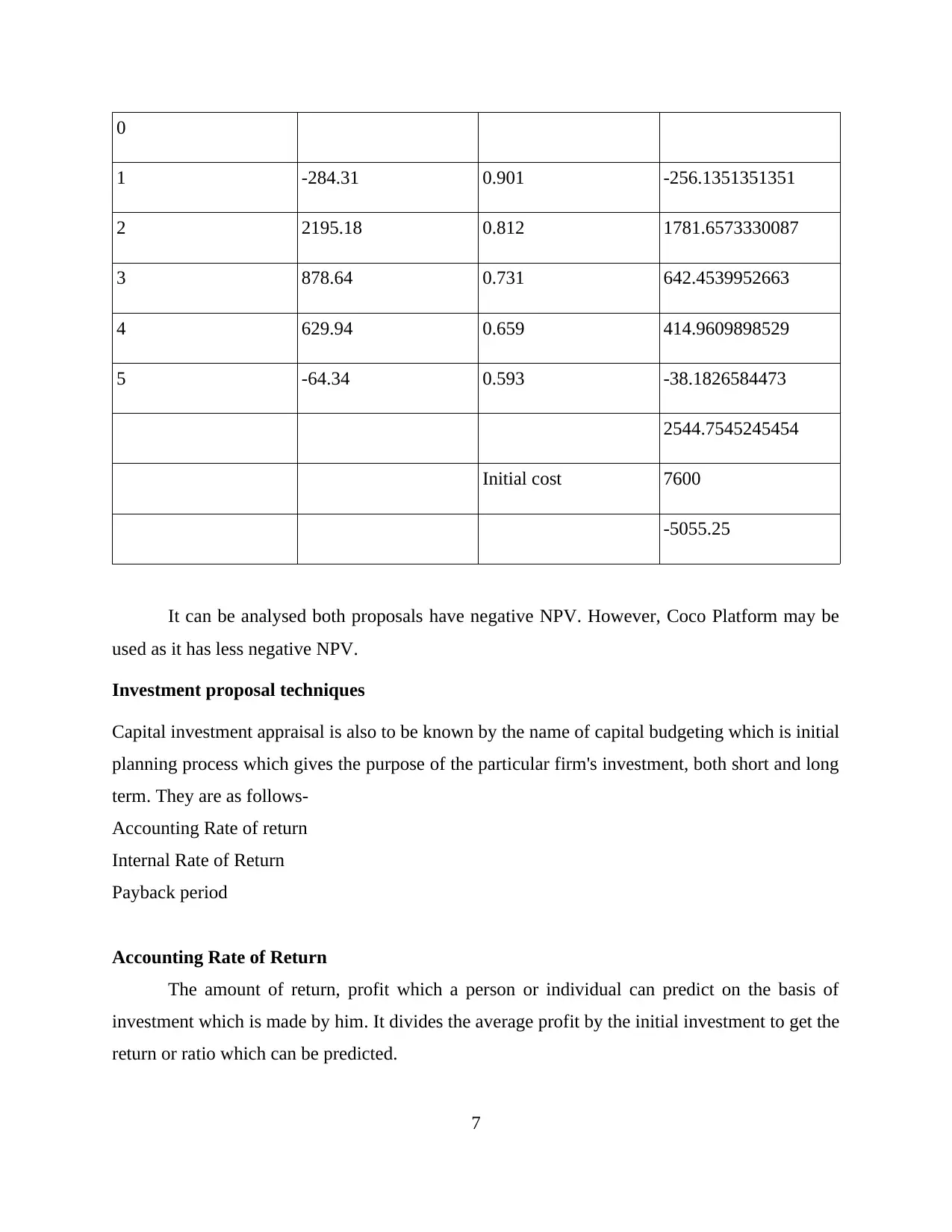

This report provides a detailed analysis of managerial finance, encompassing various critical aspects. It begins by exploring different sources of funding, both internal and external, along with their respective advantages and disadvantages. The report then delves into investment proposal techniques, including their limitations, and provides a comprehensive overview of accounting rate of return, internal rate of return, and payback period. The importance and usage of management tools such as budgets and break-even analysis are thoroughly discussed, with calculations for break-even analysis and cash budgets over a three-month period. Furthermore, the report evaluates company performance, conducts a literature review of budgets and break-even analysis, and highlights their significance to an organization. Finally, it addresses key issues that management must consider for survival and profit generation, concluding with recommendations for effective financial management.

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.