Comprehensive Analysis of Managerial Accounting Alternatives

VerifiedAdded on 2020/05/16

|9

|1200

|423

AI Summary

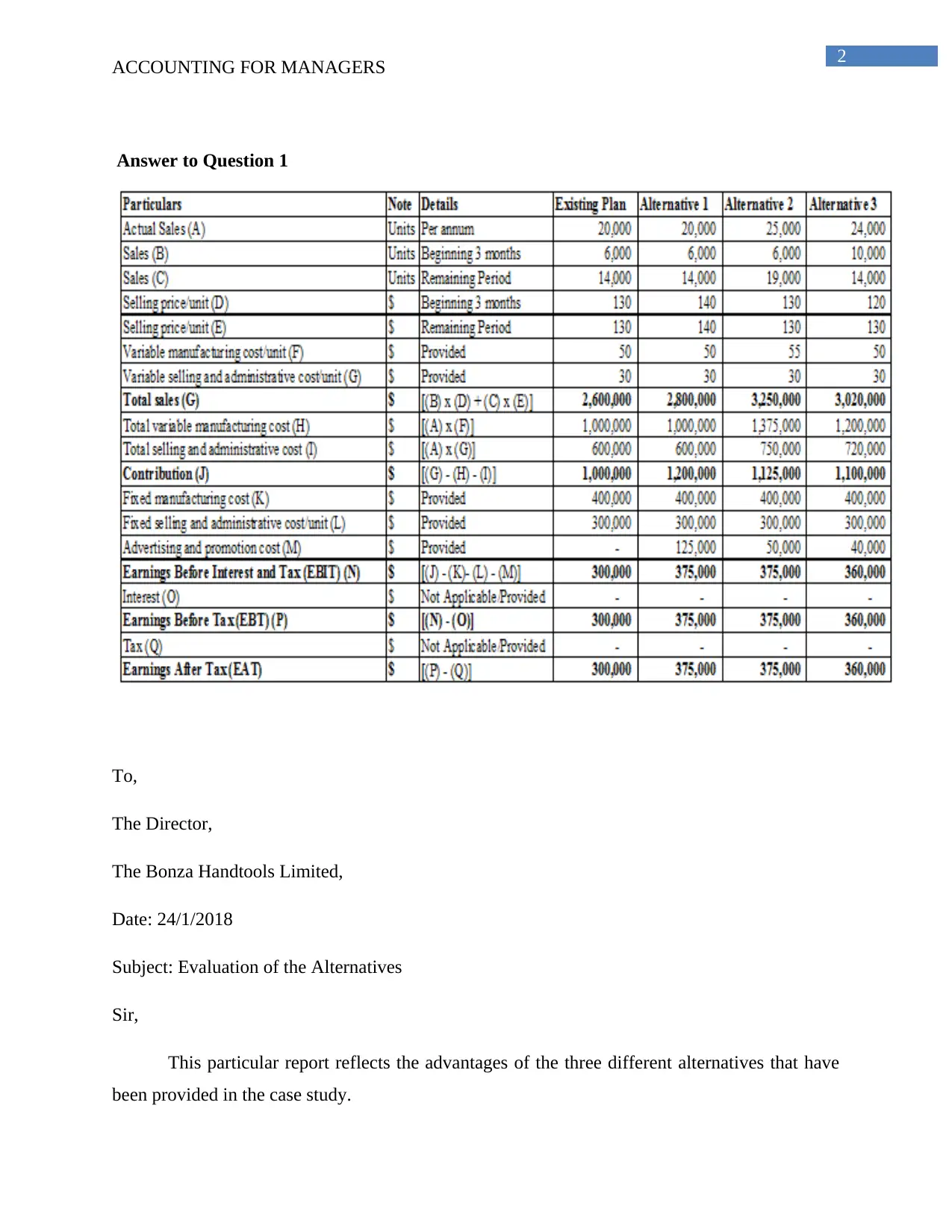

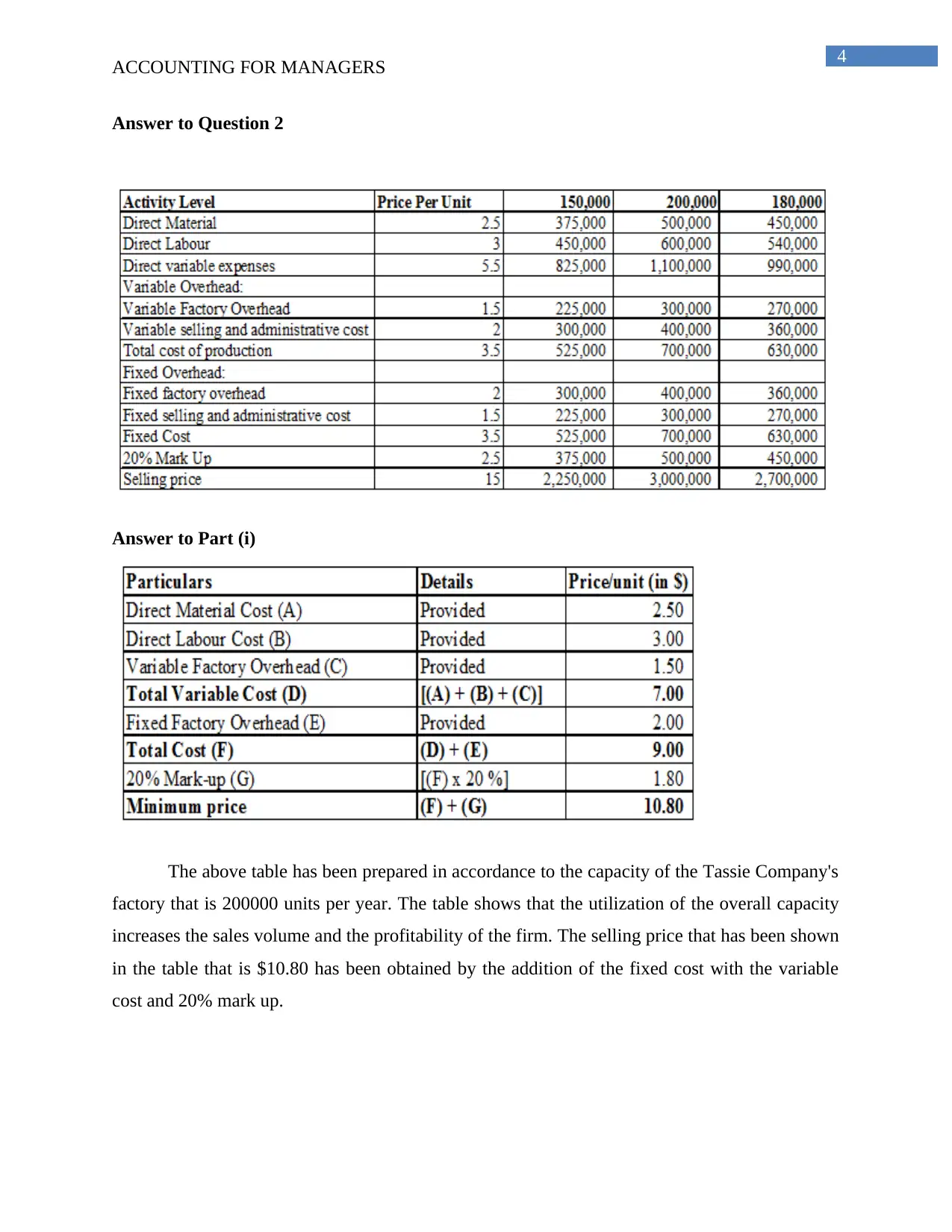

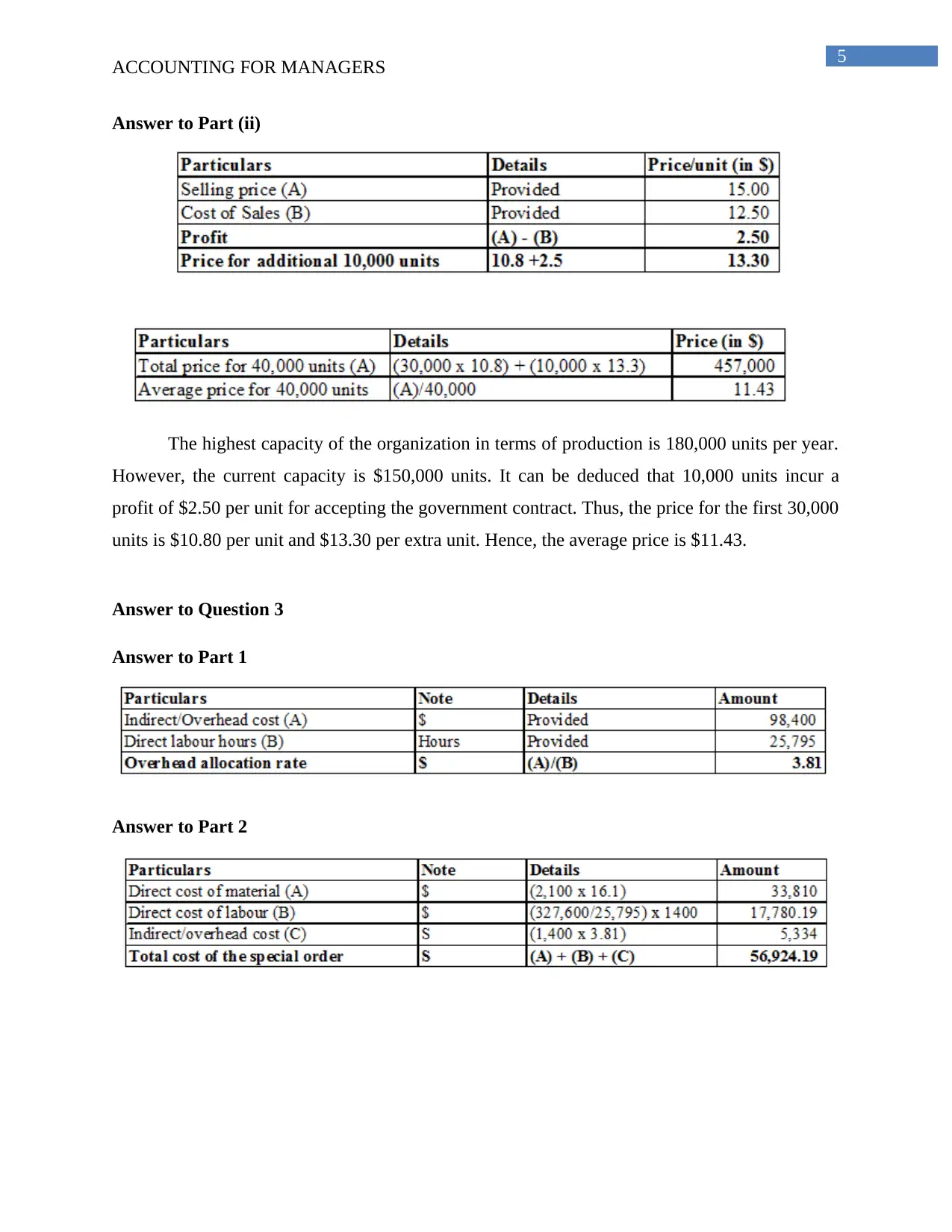

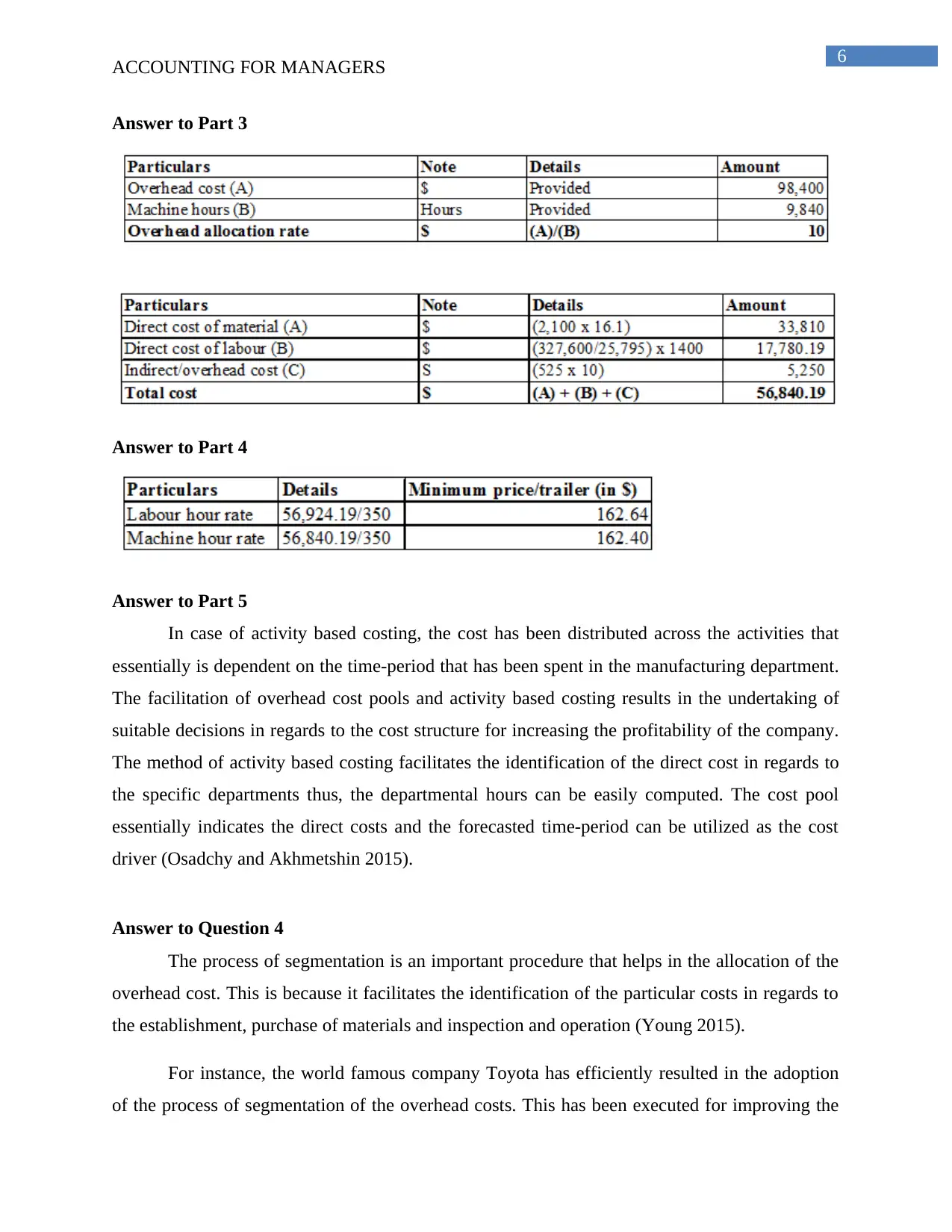

The assignment requires an evaluation of three distinct business alternatives within the context of managerial accounting. Each alternative is assessed based on its potential effects on selling prices, sales volume, variable costs, and overall profitability. The first alternative suggests increasing the product's price while incurring significant advertising expenses, posing a risk if not successful. The second alternative involves enhancing product quality and increasing sales volume, albeit with higher variable costs. The third option considers reducing the selling price temporarily to boost profitability but risks damaging perceived product quality. Ultimately, the assignment concludes that improving product quality and sales volume is recommended for optimal profitability. Additionally, activity-based costing methods are discussed to allocate overhead costs effectively, highlighting their role in enhancing decision-making processes within organizations.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.