Analysis of Managing Business Performance: A Financial Report

VerifiedAdded on 2023/01/12

|18

|3500

|40

Report

AI Summary

This report provides a comprehensive analysis of managing business performance, focusing on standard costing and its application in financial analysis. Part I utilizes marginal costing statements to evaluate the impact of changes in selling price and variable costs on net profit, including break-even point calculations under various scenarios. The analysis extends to margin of safety and net profit margins, offering insights into business profitability and risk. Part II delves into the concept of standard costing, explaining its meaning and the process of setting standard costs, including material and labor variances. It explores factors leading to favorable and adverse variances in labor and material costs, and critically assesses standard costing as a tool for ensuring control within a business. The report concludes with a discussion of the results and limitations of the exercises, providing a balanced perspective on the effectiveness of these financial tools.

Managing Business

Performance

Performance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

PART I.............................................................................................................................................3

1...................................................................................................................................................3

2...................................................................................................................................................3

3...................................................................................................................................................5

4...................................................................................................................................................8

PART II............................................................................................................................................9

INTRODUCTION...........................................................................................................................9

Explaining the meaning of standard costing and outlining process in setting up the standard

costs.............................................................................................................................................9

Explaining factors that results to adverse and the favourable labour & material variances ....10

Critically assessing standard costing as the tool for the purpose of ensuring control...............12

CONCLUSION .............................................................................................................................13

REFERENCES..............................................................................................................................14

PART I.............................................................................................................................................3

1...................................................................................................................................................3

2...................................................................................................................................................3

3...................................................................................................................................................5

4...................................................................................................................................................8

PART II............................................................................................................................................9

INTRODUCTION...........................................................................................................................9

Explaining the meaning of standard costing and outlining process in setting up the standard

costs.............................................................................................................................................9

Explaining factors that results to adverse and the favourable labour & material variances ....10

Critically assessing standard costing as the tool for the purpose of ensuring control...............12

CONCLUSION .............................................................................................................................13

REFERENCES..............................................................................................................................14

PART I

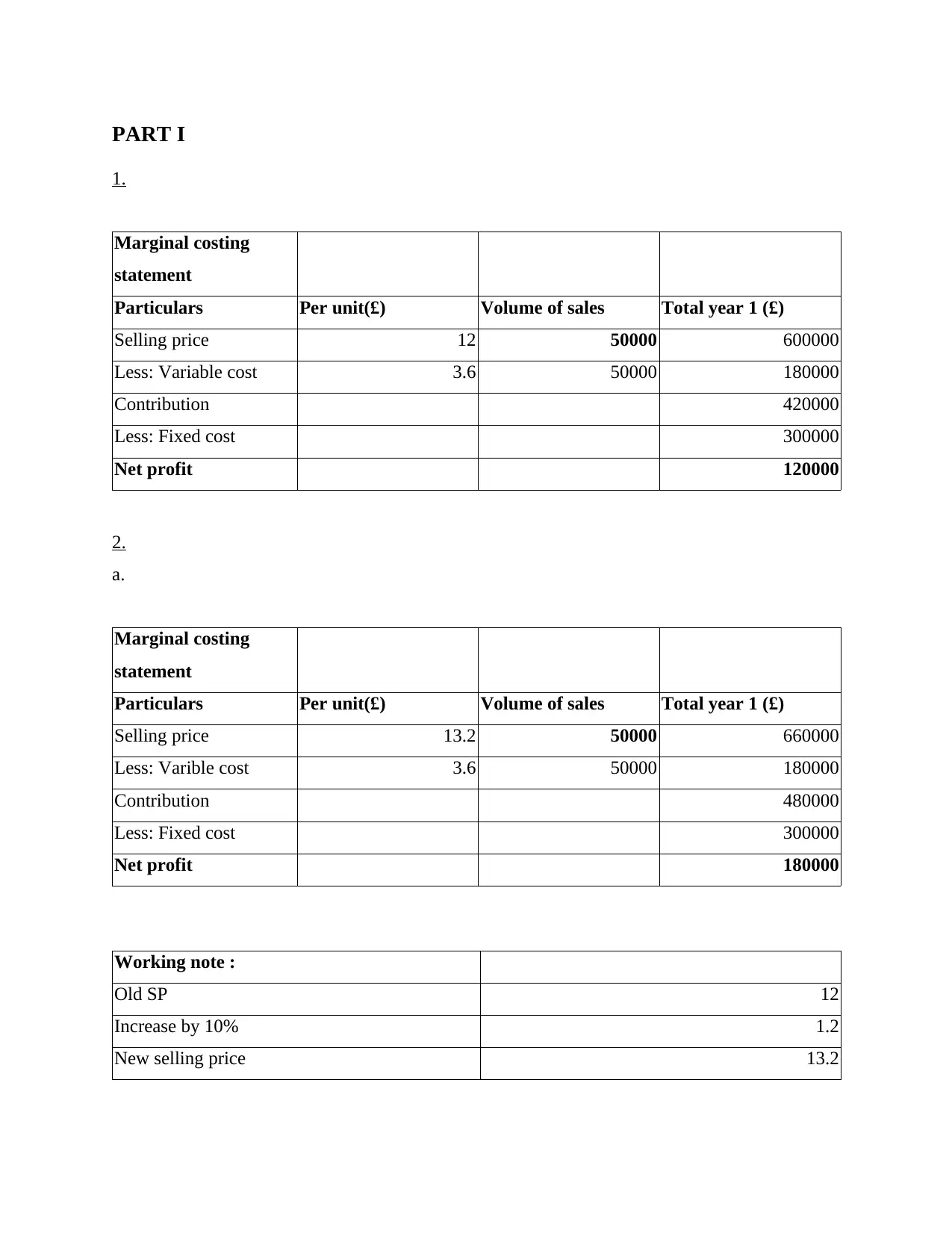

1.

Marginal costing

statement

Particulars Per unit(£) Volume of sales Total year 1 (£)

Selling price 12 50000 600000

Less: Variable cost 3.6 50000 180000

Contribution 420000

Less: Fixed cost 300000

Net profit 120000

2.

a.

Marginal costing

statement

Particulars Per unit(£) Volume of sales Total year 1 (£)

Selling price 13.2 50000 660000

Less: Varible cost 3.6 50000 180000

Contribution 480000

Less: Fixed cost 300000

Net profit 180000

Working note :

Old SP 12

Increase by 10% 1.2

New selling price 13.2

1.

Marginal costing

statement

Particulars Per unit(£) Volume of sales Total year 1 (£)

Selling price 12 50000 600000

Less: Variable cost 3.6 50000 180000

Contribution 420000

Less: Fixed cost 300000

Net profit 120000

2.

a.

Marginal costing

statement

Particulars Per unit(£) Volume of sales Total year 1 (£)

Selling price 13.2 50000 660000

Less: Varible cost 3.6 50000 180000

Contribution 480000

Less: Fixed cost 300000

Net profit 180000

Working note :

Old SP 12

Increase by 10% 1.2

New selling price 13.2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

b.

Marginal costing

statement

Particulars Per unit(£) Volume of sales Total year 1 (£)

Selling price 10.8 50000 540000

Less: Varible cost 3.6 50000 180000

Contribution 360000

Less: Fixed cost 300000

Net profit 60000

Working note :

Old SP 12

decrease by 10% 1.2

New selling price 10.8

c.

Marginal costing

statement

Particulars Per unit(£) Volume of sales Total year 1 (£)

Selling price 12 50000 600000

Less: Varible cost 3 50000 150000

Contribution 450000

Less: Fixed cost 300000

Net profit 150000

Working note :

SP 12

Marginal costing

statement

Particulars Per unit(£) Volume of sales Total year 1 (£)

Selling price 10.8 50000 540000

Less: Varible cost 3.6 50000 180000

Contribution 360000

Less: Fixed cost 300000

Net profit 60000

Working note :

Old SP 12

decrease by 10% 1.2

New selling price 10.8

c.

Marginal costing

statement

Particulars Per unit(£) Volume of sales Total year 1 (£)

Selling price 12 50000 600000

Less: Varible cost 3 50000 150000

Contribution 450000

Less: Fixed cost 300000

Net profit 150000

Working note :

SP 12

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

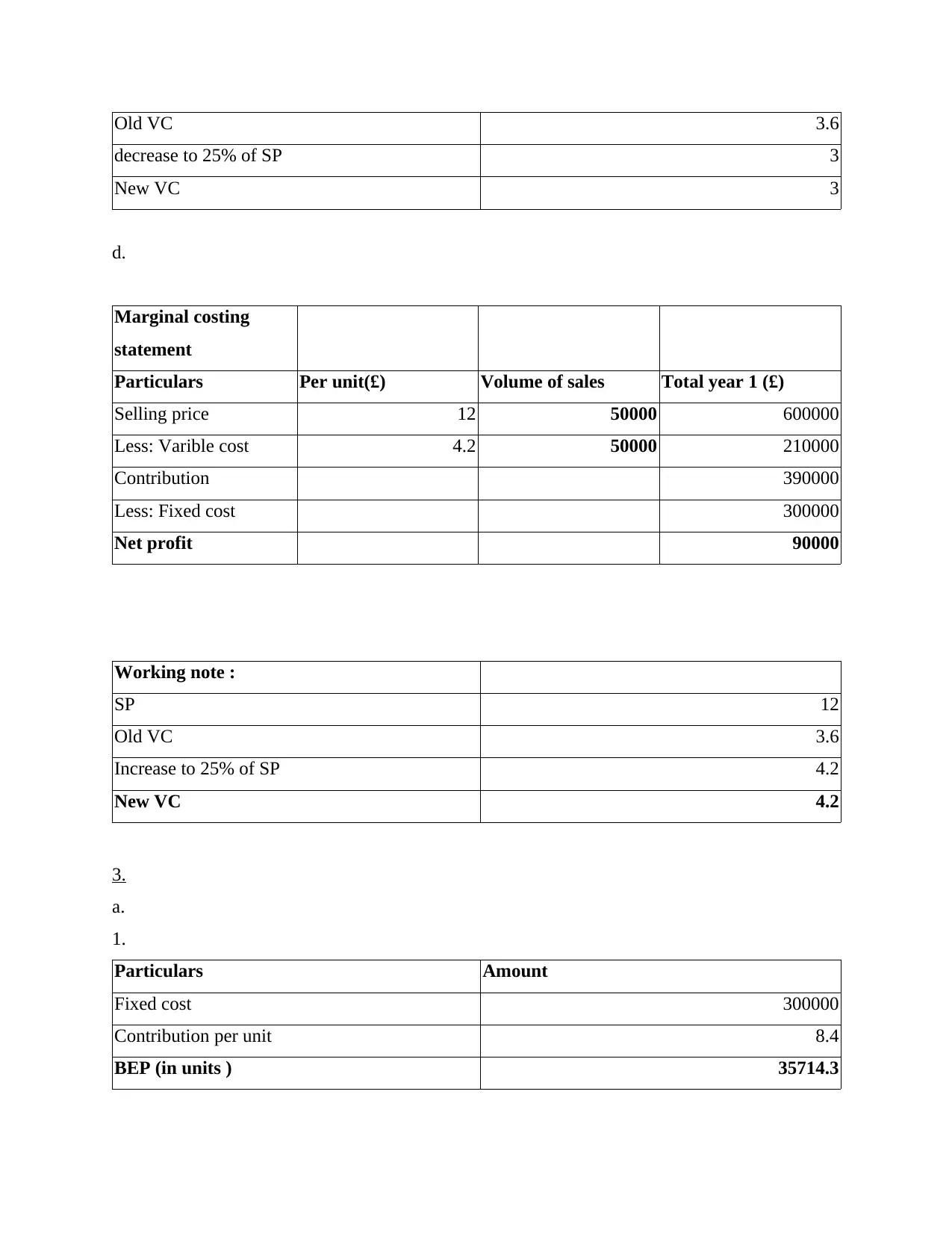

Old VC 3.6

decrease to 25% of SP 3

New VC 3

d.

Marginal costing

statement

Particulars Per unit(£) Volume of sales Total year 1 (£)

Selling price 12 50000 600000

Less: Varible cost 4.2 50000 210000

Contribution 390000

Less: Fixed cost 300000

Net profit 90000

Working note :

SP 12

Old VC 3.6

Increase to 25% of SP 4.2

New VC 4.2

3.

a.

1.

Particulars Amount

Fixed cost 300000

Contribution per unit 8.4

BEP (in units ) 35714.3

decrease to 25% of SP 3

New VC 3

d.

Marginal costing

statement

Particulars Per unit(£) Volume of sales Total year 1 (£)

Selling price 12 50000 600000

Less: Varible cost 4.2 50000 210000

Contribution 390000

Less: Fixed cost 300000

Net profit 90000

Working note :

SP 12

Old VC 3.6

Increase to 25% of SP 4.2

New VC 4.2

3.

a.

1.

Particulars Amount

Fixed cost 300000

Contribution per unit 8.4

BEP (in units ) 35714.3

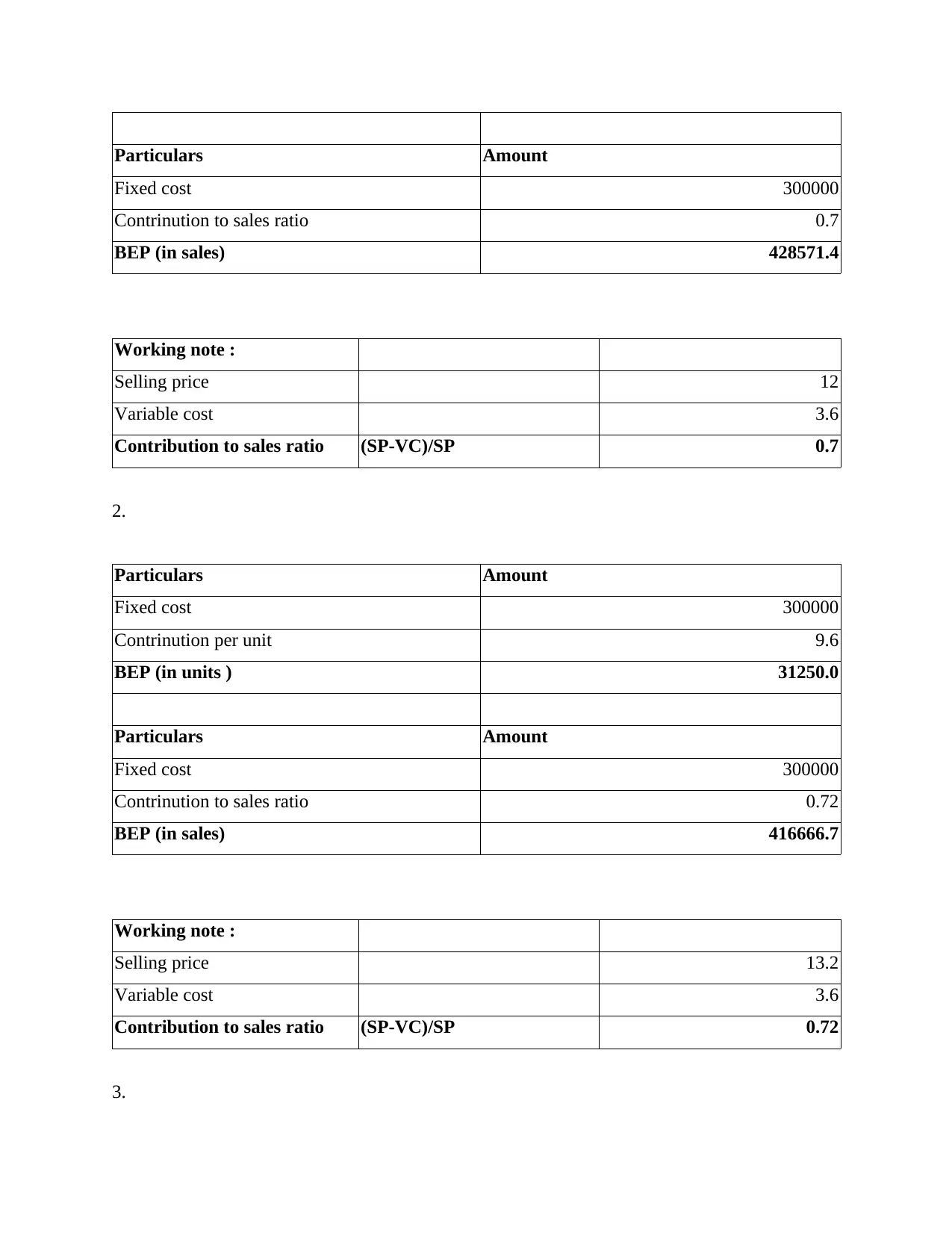

Particulars Amount

Fixed cost 300000

Contrinution to sales ratio 0.7

BEP (in sales) 428571.4

Working note :

Selling price 12

Variable cost 3.6

Contribution to sales ratio (SP-VC)/SP 0.7

2.

Particulars Amount

Fixed cost 300000

Contrinution per unit 9.6

BEP (in units ) 31250.0

Particulars Amount

Fixed cost 300000

Contrinution to sales ratio 0.72

BEP (in sales) 416666.7

Working note :

Selling price 13.2

Variable cost 3.6

Contribution to sales ratio (SP-VC)/SP 0.72

3.

Fixed cost 300000

Contrinution to sales ratio 0.7

BEP (in sales) 428571.4

Working note :

Selling price 12

Variable cost 3.6

Contribution to sales ratio (SP-VC)/SP 0.7

2.

Particulars Amount

Fixed cost 300000

Contrinution per unit 9.6

BEP (in units ) 31250.0

Particulars Amount

Fixed cost 300000

Contrinution to sales ratio 0.72

BEP (in sales) 416666.7

Working note :

Selling price 13.2

Variable cost 3.6

Contribution to sales ratio (SP-VC)/SP 0.72

3.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

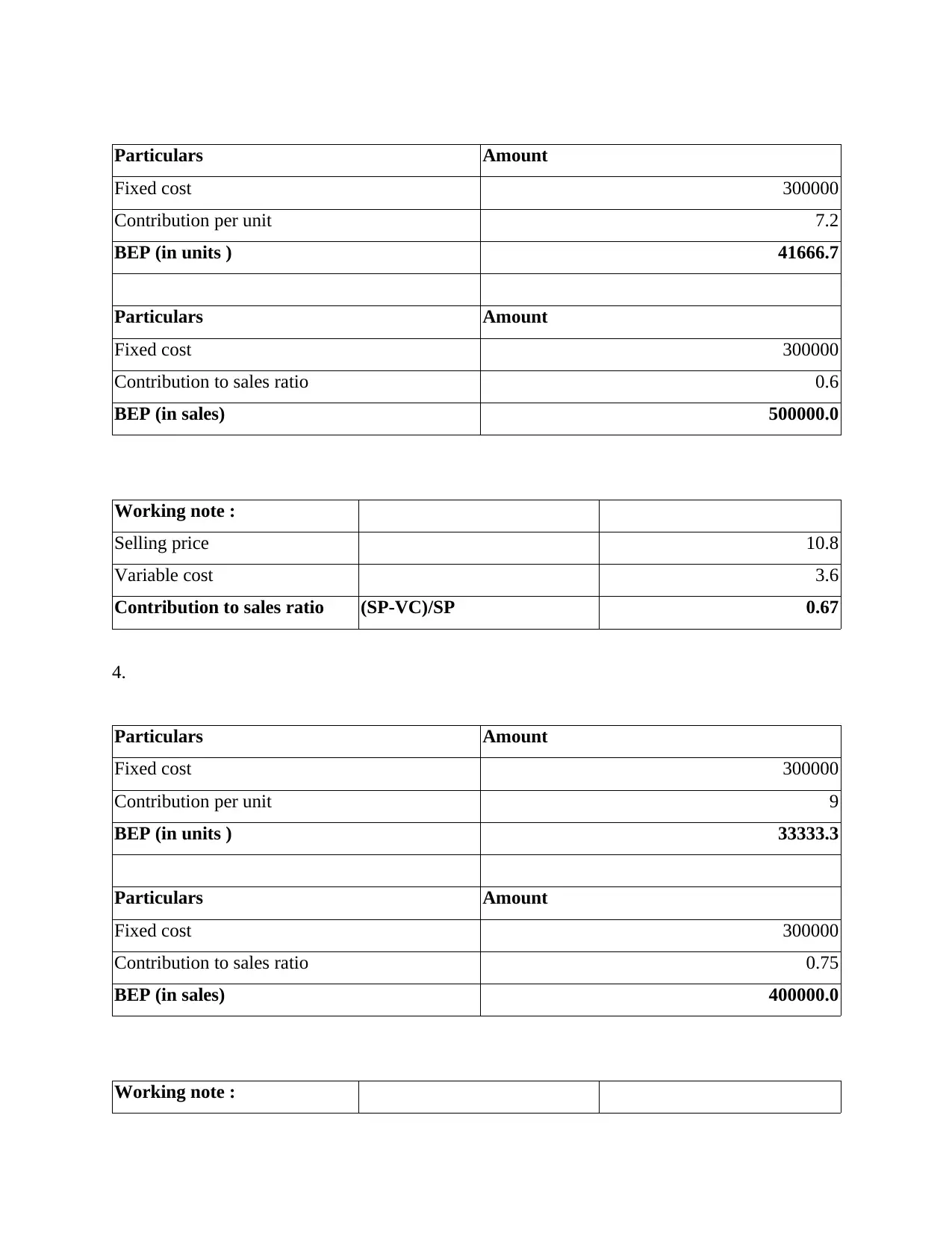

Particulars Amount

Fixed cost 300000

Contribution per unit 7.2

BEP (in units ) 41666.7

Particulars Amount

Fixed cost 300000

Contribution to sales ratio 0.6

BEP (in sales) 500000.0

Working note :

Selling price 10.8

Variable cost 3.6

Contribution to sales ratio (SP-VC)/SP 0.67

4.

Particulars Amount

Fixed cost 300000

Contribution per unit 9

BEP (in units ) 33333.3

Particulars Amount

Fixed cost 300000

Contribution to sales ratio 0.75

BEP (in sales) 400000.0

Working note :

Fixed cost 300000

Contribution per unit 7.2

BEP (in units ) 41666.7

Particulars Amount

Fixed cost 300000

Contribution to sales ratio 0.6

BEP (in sales) 500000.0

Working note :

Selling price 10.8

Variable cost 3.6

Contribution to sales ratio (SP-VC)/SP 0.67

4.

Particulars Amount

Fixed cost 300000

Contribution per unit 9

BEP (in units ) 33333.3

Particulars Amount

Fixed cost 300000

Contribution to sales ratio 0.75

BEP (in sales) 400000.0

Working note :

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Selling price 12

Variable cost 3

Contribution to sales ratio (SP-VC)/SP 0.75

5.

Particulars Amount

Fixed cost 300000

Contribution per unit 7.8

BEP (in units ) 38461.5

Particulars Amount

Fixed cost 300000

Contribution to sales ratio 0.65

BEP (in sales) 461538.5

Working note :

Selling price 12

Variable cost 4.2

Contribution to sales ratio (SP-VC)/SP 0.65

b.

Margin of safety in units and in percentage.

1 2 3 4 5

Current Sales

level 600000 660000 540000 600000 600000

Current sales

units 50000 50000 50000 50000 50000

Break even

point units 35714.29 31250.00 41666.67 33333.33 38461.54

Variable cost 3

Contribution to sales ratio (SP-VC)/SP 0.75

5.

Particulars Amount

Fixed cost 300000

Contribution per unit 7.8

BEP (in units ) 38461.5

Particulars Amount

Fixed cost 300000

Contribution to sales ratio 0.65

BEP (in sales) 461538.5

Working note :

Selling price 12

Variable cost 4.2

Contribution to sales ratio (SP-VC)/SP 0.65

b.

Margin of safety in units and in percentage.

1 2 3 4 5

Current Sales

level 600000 660000 540000 600000 600000

Current sales

units 50000 50000 50000 50000 50000

Break even

point units 35714.29 31250.00 41666.67 33333.33 38461.54

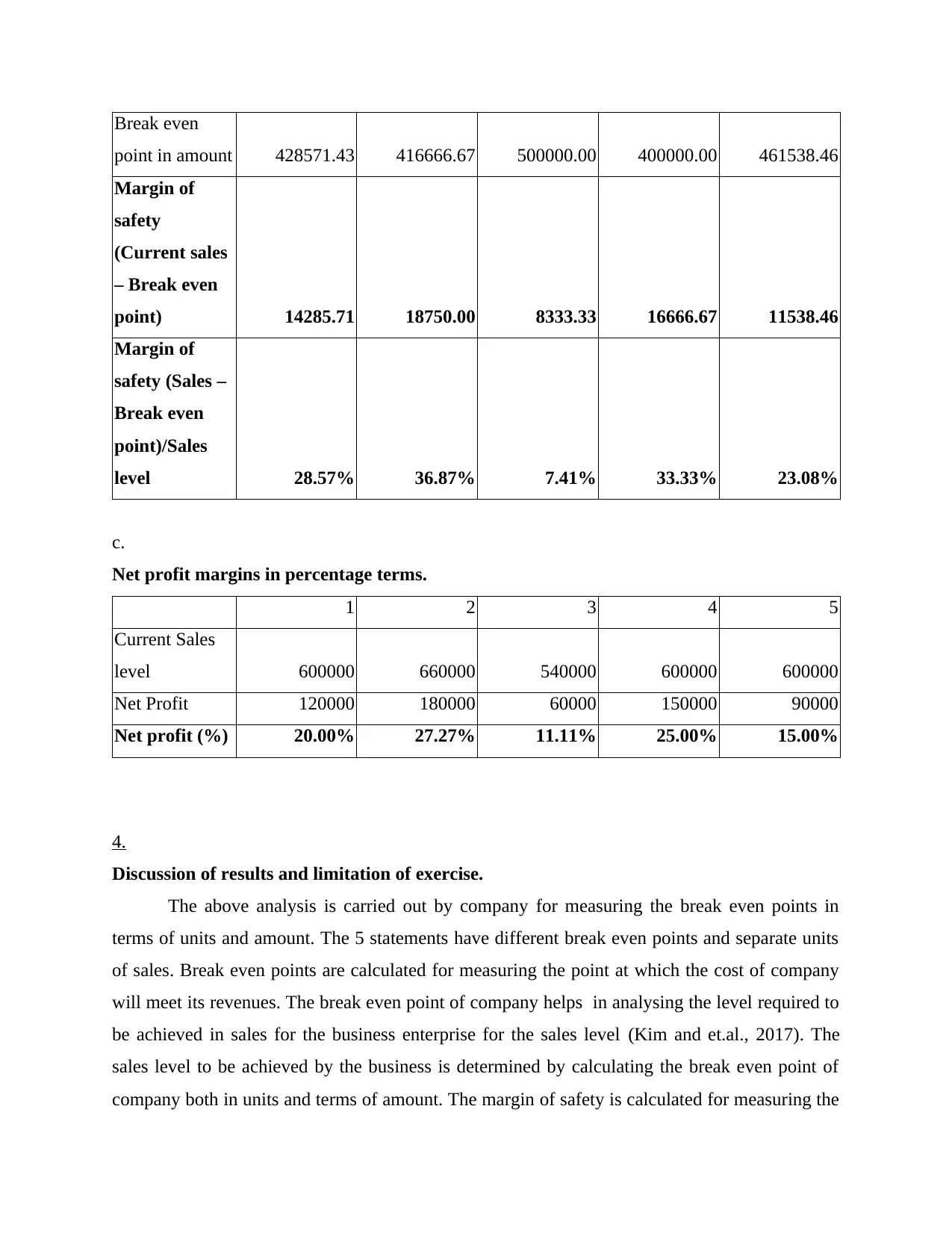

Break even

point in amount 428571.43 416666.67 500000.00 400000.00 461538.46

Margin of

safety

(Current sales

– Break even

point) 14285.71 18750.00 8333.33 16666.67 11538.46

Margin of

safety (Sales –

Break even

point)/Sales

level 28.57% 36.87% 7.41% 33.33% 23.08%

c.

Net profit margins in percentage terms.

1 2 3 4 5

Current Sales

level 600000 660000 540000 600000 600000

Net Profit 120000 180000 60000 150000 90000

Net profit (%) 20.00% 27.27% 11.11% 25.00% 15.00%

4.

Discussion of results and limitation of exercise.

The above analysis is carried out by company for measuring the break even points in

terms of units and amount. The 5 statements have different break even points and separate units

of sales. Break even points are calculated for measuring the point at which the cost of company

will meet its revenues. The break even point of company helps in analysing the level required to

be achieved in sales for the business enterprise for the sales level (Kim and et.al., 2017). The

sales level to be achieved by the business is determined by calculating the break even point of

company both in units and terms of amount. The margin of safety is calculated for measuring the

point in amount 428571.43 416666.67 500000.00 400000.00 461538.46

Margin of

safety

(Current sales

– Break even

point) 14285.71 18750.00 8333.33 16666.67 11538.46

Margin of

safety (Sales –

Break even

point)/Sales

level 28.57% 36.87% 7.41% 33.33% 23.08%

c.

Net profit margins in percentage terms.

1 2 3 4 5

Current Sales

level 600000 660000 540000 600000 600000

Net Profit 120000 180000 60000 150000 90000

Net profit (%) 20.00% 27.27% 11.11% 25.00% 15.00%

4.

Discussion of results and limitation of exercise.

The above analysis is carried out by company for measuring the break even points in

terms of units and amount. The 5 statements have different break even points and separate units

of sales. Break even points are calculated for measuring the point at which the cost of company

will meet its revenues. The break even point of company helps in analysing the level required to

be achieved in sales for the business enterprise for the sales level (Kim and et.al., 2017). The

sales level to be achieved by the business is determined by calculating the break even point of

company both in units and terms of amount. The margin of safety is calculated for measuring the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

difference between profitability & break-even point. Margin of safety is measured in both terms

of units and also in terms of amount. Margin of safety used for assessing the level of stocks

required to be kept with the business for the production and sales. Margin of safety should not be

high as it causes company to have extra carrying cost for storing the stocks of inventory. They

are used by management in budgeting and investing decisions.

The limitations of break even point is that the fixed costs of company vary after the

certain level of operations. Also the volume of sales changes the variable costs of the company

that affects the results of business operations (Kampf, Majerčák and Švagr, 2016). This do not

allow the company to make accurate declarations for the business. Margin of safety do not give

accurate analysis of the cost information carried out by the business. This do not allow company

to make accurate results of the forecasts. The margin of safety if analysed wrongly may cause the

company to incur carrying costs.

PART II

INTRODUCTION

Standard costing is the cost accounting techniques that is adopted for computing

variances present between actual and the budgeted figures. The present report provides a deeper

insights towards concept of standard costing and the process followed in setting up the standard

cost. Moreover, it also presents the reason behind favourable and adverse variances with an

importance of standard costing in ensuring effective controlling.

Explaining the meaning of standard costing and outlining process in setting up the standard costs

Standard cost refers to an estimated unit cost that is built up of the standards for each and

every element of the cost. It is the target cost that needs to be incurred under an efficient

operating circumstances. Standard cost re identified analysing expected material price, expenses

and labour, efficiency level in using labour and material, Budgeted volume and overhead cost of

an activity.

Difference between budgeted and standard costs:

The budgeted data is reflected as the totalled of the standard cost

Budget facilitates information about cost for an overall activity

Standard represents the same info or the unit basis

In order to set standards the key aspect are taken into account that includes:

of units and also in terms of amount. Margin of safety used for assessing the level of stocks

required to be kept with the business for the production and sales. Margin of safety should not be

high as it causes company to have extra carrying cost for storing the stocks of inventory. They

are used by management in budgeting and investing decisions.

The limitations of break even point is that the fixed costs of company vary after the

certain level of operations. Also the volume of sales changes the variable costs of the company

that affects the results of business operations (Kampf, Majerčák and Švagr, 2016). This do not

allow the company to make accurate declarations for the business. Margin of safety do not give

accurate analysis of the cost information carried out by the business. This do not allow company

to make accurate results of the forecasts. The margin of safety if analysed wrongly may cause the

company to incur carrying costs.

PART II

INTRODUCTION

Standard costing is the cost accounting techniques that is adopted for computing

variances present between actual and the budgeted figures. The present report provides a deeper

insights towards concept of standard costing and the process followed in setting up the standard

cost. Moreover, it also presents the reason behind favourable and adverse variances with an

importance of standard costing in ensuring effective controlling.

Explaining the meaning of standard costing and outlining process in setting up the standard costs

Standard cost refers to an estimated unit cost that is built up of the standards for each and

every element of the cost. It is the target cost that needs to be incurred under an efficient

operating circumstances. Standard cost re identified analysing expected material price, expenses

and labour, efficiency level in using labour and material, Budgeted volume and overhead cost of

an activity.

Difference between budgeted and standard costs:

The budgeted data is reflected as the totalled of the standard cost

Budget facilitates information about cost for an overall activity

Standard represents the same info or the unit basis

In order to set standards the key aspect are taken into account that includes:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Material by purchasing department- Contracts agreed, forecast movements in the prices,

pricing related discussion with the suppliers, availability of the bulk buying discounts,

quality of material needed.

Labour- Agreements on the pay rises and reference to the payroll

Process for setting standard cost

Determining cost centre- For setting up the standard cost, it is necessary to have a cost

centre for fixing the cost and responsibility. In manufacturing enterprise, cost centres are

developed as per the no. of products manufactured & no. of the departments, divisions or the

sections are been involved in process of production. Cost centre in relation to the person known

as the cost centre of personnel and relating to equipments and the products known as impersonal

cost centre.

Classifying accounts- Cost incurs at several stages of the production process. Such costs

must be recorded adequately for making an accurate computation of the total value of the cost

incurred. Thus, there is the need for classification of the accounts for the purpose of cost control

under the system of standard costing.

Codification of the accounts- After classification of the accounts, different types of the

accounts could be codified & different symbols could be utilised for facilitating speedy

collection, reporting and communication.

Setting standards- Thereafter codification, the next step is to set standards which is an

ideal that is been anticipated and could be achieved over a future time period. Success of the

standard costing depends on reliability, genuineness and an acceptance of such standards (Tsai,

Lan and Huang, 2019). Under this three kinds of the standards are evaluated that are basic,

normal and the current standard. In this the current standard is been divided into two parts that is

ideals and an expected standard.

Establishing for the standard cost- In this step, for each and very element of the cost

separately, standard cost is been established. Generally, components of the cost is grouped as the

labour, overhead and the material. Moreover, the standard cost are also set for sales.

Preparing sheet stating standard cost- After establishing the standard cost, sheet or card

including the standard cost must be prepared separately in accordance product and process wise.

pricing related discussion with the suppliers, availability of the bulk buying discounts,

quality of material needed.

Labour- Agreements on the pay rises and reference to the payroll

Process for setting standard cost

Determining cost centre- For setting up the standard cost, it is necessary to have a cost

centre for fixing the cost and responsibility. In manufacturing enterprise, cost centres are

developed as per the no. of products manufactured & no. of the departments, divisions or the

sections are been involved in process of production. Cost centre in relation to the person known

as the cost centre of personnel and relating to equipments and the products known as impersonal

cost centre.

Classifying accounts- Cost incurs at several stages of the production process. Such costs

must be recorded adequately for making an accurate computation of the total value of the cost

incurred. Thus, there is the need for classification of the accounts for the purpose of cost control

under the system of standard costing.

Codification of the accounts- After classification of the accounts, different types of the

accounts could be codified & different symbols could be utilised for facilitating speedy

collection, reporting and communication.

Setting standards- Thereafter codification, the next step is to set standards which is an

ideal that is been anticipated and could be achieved over a future time period. Success of the

standard costing depends on reliability, genuineness and an acceptance of such standards (Tsai,

Lan and Huang, 2019). Under this three kinds of the standards are evaluated that are basic,

normal and the current standard. In this the current standard is been divided into two parts that is

ideals and an expected standard.

Establishing for the standard cost- In this step, for each and very element of the cost

separately, standard cost is been established. Generally, components of the cost is grouped as the

labour, overhead and the material. Moreover, the standard cost are also set for sales.

Preparing sheet stating standard cost- After establishing the standard cost, sheet or card

including the standard cost must be prepared separately in accordance product and process wise.

Explaining factors that results to adverse and the favourable labour & material variances

Labour variance

Labour rate variance focuses on comparing the actual hours for which the workers

worked in a particular time period with that of the proportion of cost using a standard cost for per

labour hour. Adverse labour rate variance resulted when actual cost for the hours worked

exceeds standards cost for an actual hours. However, favourable variance occurred when actual

cost for the hours worked seems as less than the standard cost for an actual hours.

Favourable labour rate variance is resulted due to many factors that are as follows-

hiring of more an more unskilled or the semi skilled labour

decrease in an overall rate of wages within the market because of an increase in supply of

the labour that caused because of an immigrants as result of relaxation of an immigration

policy

Inadequately high setting of standard cost of the direct labour that might be attributed due

to an inefficient planning.

Adverse labour rate variance caused due to several factors that includes-

Increase in national minimum wage rate

Hiring more of skilled labour than estimated in standard

Inefficient hiring process by HR department

Effective negotiations by the labour unions

Labour efficiency variance reflects comparison of an actual output produced in

comparison to standard duration. Adverse variance states that an actual production took a longer

time than the standard whereas favourable variance indicates that an actual production took very

less time than the standard.

Factors causing Favourable variance

Higher level of skilled staff

Incorrect budgeting

Improved motivation among staff

Factors causing adverse variance

Lower level of skilled staff

Decline in the motivation of staff

Inaccurate budgeting

Labour variance

Labour rate variance focuses on comparing the actual hours for which the workers

worked in a particular time period with that of the proportion of cost using a standard cost for per

labour hour. Adverse labour rate variance resulted when actual cost for the hours worked

exceeds standards cost for an actual hours. However, favourable variance occurred when actual

cost for the hours worked seems as less than the standard cost for an actual hours.

Favourable labour rate variance is resulted due to many factors that are as follows-

hiring of more an more unskilled or the semi skilled labour

decrease in an overall rate of wages within the market because of an increase in supply of

the labour that caused because of an immigrants as result of relaxation of an immigration

policy

Inadequately high setting of standard cost of the direct labour that might be attributed due

to an inefficient planning.

Adverse labour rate variance caused due to several factors that includes-

Increase in national minimum wage rate

Hiring more of skilled labour than estimated in standard

Inefficient hiring process by HR department

Effective negotiations by the labour unions

Labour efficiency variance reflects comparison of an actual output produced in

comparison to standard duration. Adverse variance states that an actual production took a longer

time than the standard whereas favourable variance indicates that an actual production took very

less time than the standard.

Factors causing Favourable variance

Higher level of skilled staff

Incorrect budgeting

Improved motivation among staff

Factors causing adverse variance

Lower level of skilled staff

Decline in the motivation of staff

Inaccurate budgeting

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.