Managing Business Performance: Costing Analysis of ABC Footwear

VerifiedAdded on 2023/01/13

|12

|3156

|72

Report

AI Summary

This report analyzes the performance of ABC Footwear using marginal and standard costing techniques. Part 1 focuses on marginal costing, calculating break-even points, profit margins, and margin of safety under various scenarios, including changes in selling price and variable costs. Part 2 delves into standard costing, explaining the process of setting standard costs, identifying factors that can lead to material and labor variances (both favorable and adverse), and demonstrating how standard costing serves as a tool for control. The report highlights the limitations of marginal costing, such as its short-term applicability and inability to separate costs. It concludes by emphasizing the importance of these costing methods in managing business performance and making informed decisions. The analysis includes calculations and explanations to provide a comprehensive understanding of cost management principles and their practical application within a business context, specifically for ABC Footwear.

Managing Business

Performance

Performance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

PART 1............................................................................................................................................1

1. Statement of marginal costing showing 20 % profit on selling price..........................................1

2. and 3. Statement of marginal costing showing various changes in selling price and variable

cost...................................................................................................................................................2

4. Explanation of results and limitations of the exercise:..........................................................5

PART 2............................................................................................................................................5

1. Explantation of standard costing and process of setting standard costs................................5

2. Explantation of factors that can lead to both adverse and favourable materials and labour

Variances with example.............................................................................................................7

3. explanation of standard costing as a tool for control..............................................................8

CONCLUSION ...............................................................................................................................8

REFERENCES................................................................................................................................9

INTRODUCTION...........................................................................................................................1

PART 1............................................................................................................................................1

1. Statement of marginal costing showing 20 % profit on selling price..........................................1

2. and 3. Statement of marginal costing showing various changes in selling price and variable

cost...................................................................................................................................................2

4. Explanation of results and limitations of the exercise:..........................................................5

PART 2............................................................................................................................................5

1. Explantation of standard costing and process of setting standard costs................................5

2. Explantation of factors that can lead to both adverse and favourable materials and labour

Variances with example.............................................................................................................7

3. explanation of standard costing as a tool for control..............................................................8

CONCLUSION ...............................................................................................................................8

REFERENCES................................................................................................................................9

INTRODUCTION

Managing business performance is a systematic process which helps organisation to

enhance their performance with using various techniques. In order to understand techniques of

performance management ABC footwear is taken for his report. It is newly establish business

organisation. In this report various tools of marginal costing has been identity. Uses of standard

costing and factors affecting of determining standard costing has been analysis.

PART 1

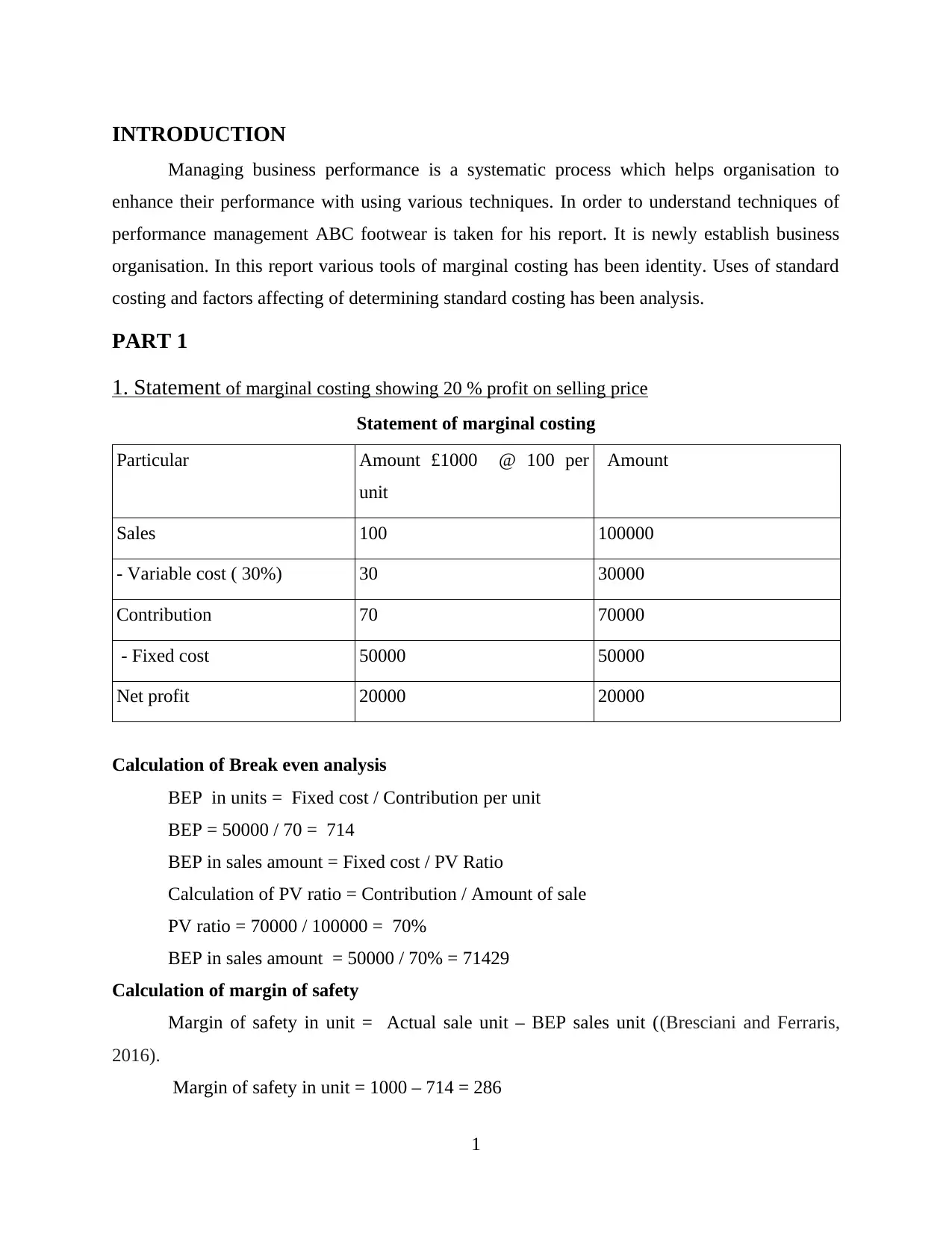

1. Statement of marginal costing showing 20 % profit on selling price

Statement of marginal costing

Particular Amount £1000 @ 100 per

unit

Amount

Sales 100 100000

- Variable cost ( 30%) 30 30000

Contribution 70 70000

- Fixed cost 50000 50000

Net profit 20000 20000

Calculation of Break even analysis

BEP in units = Fixed cost / Contribution per unit

BEP = 50000 / 70 = 714

BEP in sales amount = Fixed cost / PV Ratio

Calculation of PV ratio = Contribution / Amount of sale

PV ratio = 70000 / 100000 = 70%

BEP in sales amount = 50000 / 70% = 71429

Calculation of margin of safety

Margin of safety in unit = Actual sale unit – BEP sales unit ((Bresciani and Ferraris,

2016).

Margin of safety in unit = 1000 – 714 = 286

1

Managing business performance is a systematic process which helps organisation to

enhance their performance with using various techniques. In order to understand techniques of

performance management ABC footwear is taken for his report. It is newly establish business

organisation. In this report various tools of marginal costing has been identity. Uses of standard

costing and factors affecting of determining standard costing has been analysis.

PART 1

1. Statement of marginal costing showing 20 % profit on selling price

Statement of marginal costing

Particular Amount £1000 @ 100 per

unit

Amount

Sales 100 100000

- Variable cost ( 30%) 30 30000

Contribution 70 70000

- Fixed cost 50000 50000

Net profit 20000 20000

Calculation of Break even analysis

BEP in units = Fixed cost / Contribution per unit

BEP = 50000 / 70 = 714

BEP in sales amount = Fixed cost / PV Ratio

Calculation of PV ratio = Contribution / Amount of sale

PV ratio = 70000 / 100000 = 70%

BEP in sales amount = 50000 / 70% = 71429

Calculation of margin of safety

Margin of safety in unit = Actual sale unit – BEP sales unit ((Bresciani and Ferraris,

2016).

Margin of safety in unit = 1000 – 714 = 286

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Margin of safety in % = Current sale – BEP sale / Current sale *100

Margin of safety in % = 100000 – 71429 / 100000 * 100 = 28.57 %

Calculation of net profit %

Net profit % = Net profit / Sales *100

Net profit % = 20000 /100000 *100 = 20 %

2. and 3. Statement of marginal costing showing various changes in selling price and variable

cost

Increasing original selling price by 10%, leaving the variable cost unchange

Statement of marginal costing

Particular Amount £ 1000 @ per unit Amount

Sales 110 110000

- Variable cost ( 30%) 30 30000

Contribution 80 80000

- Fixed cost 50000 50000

Net profit 30000 30000

Calculation of Break even analysis

BEP in units = Fixed cost / Contribution per unit

BEP in units = 50000 / 80 = 625 unit

BEP in sales amount = Fixed cost / PV Ratio

Calculation of PV ratio = Contribution / Amount of sale*100 (Cleary and Quinn, 2016).

PV ratio = 80000 / 110000*100 = 72.7 %

BEP in sales = 50000 / 72.7 % = 68775

Calculation of margin of safety

Margin of safety in unit = Actual sale unit – BEP sales unit

Margin of safety = 1000 – 625 = 375 units

Margin of safety in % = Current sale – BEP sale / Current sale *100

Margin of safety in % = 110000 – 68775 / 110000 *100 = 37.4 %

Calculation of net profit %

Net profit % = Net profit / Sales *100

2

Margin of safety in % = 100000 – 71429 / 100000 * 100 = 28.57 %

Calculation of net profit %

Net profit % = Net profit / Sales *100

Net profit % = 20000 /100000 *100 = 20 %

2. and 3. Statement of marginal costing showing various changes in selling price and variable

cost

Increasing original selling price by 10%, leaving the variable cost unchange

Statement of marginal costing

Particular Amount £ 1000 @ per unit Amount

Sales 110 110000

- Variable cost ( 30%) 30 30000

Contribution 80 80000

- Fixed cost 50000 50000

Net profit 30000 30000

Calculation of Break even analysis

BEP in units = Fixed cost / Contribution per unit

BEP in units = 50000 / 80 = 625 unit

BEP in sales amount = Fixed cost / PV Ratio

Calculation of PV ratio = Contribution / Amount of sale*100 (Cleary and Quinn, 2016).

PV ratio = 80000 / 110000*100 = 72.7 %

BEP in sales = 50000 / 72.7 % = 68775

Calculation of margin of safety

Margin of safety in unit = Actual sale unit – BEP sales unit

Margin of safety = 1000 – 625 = 375 units

Margin of safety in % = Current sale – BEP sale / Current sale *100

Margin of safety in % = 110000 – 68775 / 110000 *100 = 37.4 %

Calculation of net profit %

Net profit % = Net profit / Sales *100

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

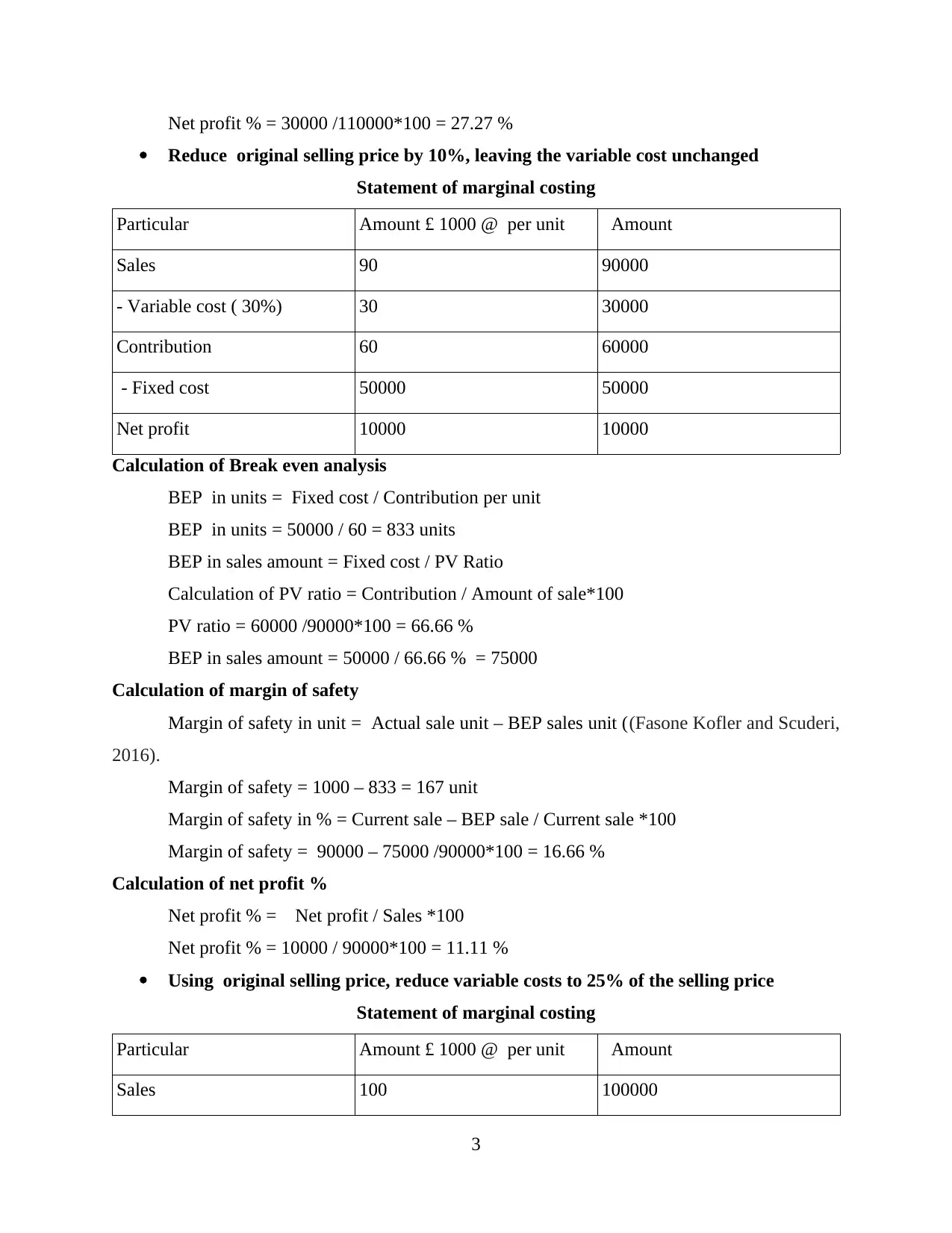

Net profit % = 30000 /110000*100 = 27.27 %

Reduce original selling price by 10%, leaving the variable cost unchanged

Statement of marginal costing

Particular Amount £ 1000 @ per unit Amount

Sales 90 90000

- Variable cost ( 30%) 30 30000

Contribution 60 60000

- Fixed cost 50000 50000

Net profit 10000 10000

Calculation of Break even analysis

BEP in units = Fixed cost / Contribution per unit

BEP in units = 50000 / 60 = 833 units

BEP in sales amount = Fixed cost / PV Ratio

Calculation of PV ratio = Contribution / Amount of sale*100

PV ratio = 60000 /90000*100 = 66.66 %

BEP in sales amount = 50000 / 66.66 % = 75000

Calculation of margin of safety

Margin of safety in unit = Actual sale unit – BEP sales unit ((Fasone Kofler and Scuderi,

2016).

Margin of safety = 1000 – 833 = 167 unit

Margin of safety in % = Current sale – BEP sale / Current sale *100

Margin of safety = 90000 – 75000 /90000*100 = 16.66 %

Calculation of net profit %

Net profit % = Net profit / Sales *100

Net profit % = 10000 / 90000*100 = 11.11 %

Using original selling price, reduce variable costs to 25% of the selling price

Statement of marginal costing

Particular Amount £ 1000 @ per unit Amount

Sales 100 100000

3

Reduce original selling price by 10%, leaving the variable cost unchanged

Statement of marginal costing

Particular Amount £ 1000 @ per unit Amount

Sales 90 90000

- Variable cost ( 30%) 30 30000

Contribution 60 60000

- Fixed cost 50000 50000

Net profit 10000 10000

Calculation of Break even analysis

BEP in units = Fixed cost / Contribution per unit

BEP in units = 50000 / 60 = 833 units

BEP in sales amount = Fixed cost / PV Ratio

Calculation of PV ratio = Contribution / Amount of sale*100

PV ratio = 60000 /90000*100 = 66.66 %

BEP in sales amount = 50000 / 66.66 % = 75000

Calculation of margin of safety

Margin of safety in unit = Actual sale unit – BEP sales unit ((Fasone Kofler and Scuderi,

2016).

Margin of safety = 1000 – 833 = 167 unit

Margin of safety in % = Current sale – BEP sale / Current sale *100

Margin of safety = 90000 – 75000 /90000*100 = 16.66 %

Calculation of net profit %

Net profit % = Net profit / Sales *100

Net profit % = 10000 / 90000*100 = 11.11 %

Using original selling price, reduce variable costs to 25% of the selling price

Statement of marginal costing

Particular Amount £ 1000 @ per unit Amount

Sales 100 100000

3

- Variable cost ( 25 %) 25 25000

Contribution 75 75000

- Fixed cost 50000 50000

Net profit 25000 25000

Calculation of Break even analysis

BEP in units = Fixed cost / Contribution per unit

BEP in units = 50000 / 75 = 667 unit

BEP in sales amount = Fixed cost / PV Ratio (Haseeb and et.al., 2019).

Calculation of PV ratio = Contribution / Amount of sale*100

PV ratio = 75000 / 100000*100 = 75 %

BEP in sales amount = 50000 / 75% = 66667

Calculation of margin of safety

Margin of safety in unit = Actual sale unit – BEP sales unit

Margin of safety in unit = 1000 – 667 = 333 unit

Margin of safety in % = Current sale – BEP sale / Current sale *100

Margin of safety in % = 100000 – 66667 / 100000 *100 = 33.33 %

Calculation of net profit %

Net profit % = Net profit / Sales *100

Net profit % = 25000 / 100000 *100 = 25 %

Using original selling price, increase variable costs to 35% of the selling price

Statement of marginal costing

Particular Amount £ 1000 @ per unit Amount

Sales 100 100000

- Variable cost ( 35 %) 35 35000

Contribution 65 65000

- Fixed cost 50000 50000

Net profit 15000 15000

Calculation of Break even analysis

4

Contribution 75 75000

- Fixed cost 50000 50000

Net profit 25000 25000

Calculation of Break even analysis

BEP in units = Fixed cost / Contribution per unit

BEP in units = 50000 / 75 = 667 unit

BEP in sales amount = Fixed cost / PV Ratio (Haseeb and et.al., 2019).

Calculation of PV ratio = Contribution / Amount of sale*100

PV ratio = 75000 / 100000*100 = 75 %

BEP in sales amount = 50000 / 75% = 66667

Calculation of margin of safety

Margin of safety in unit = Actual sale unit – BEP sales unit

Margin of safety in unit = 1000 – 667 = 333 unit

Margin of safety in % = Current sale – BEP sale / Current sale *100

Margin of safety in % = 100000 – 66667 / 100000 *100 = 33.33 %

Calculation of net profit %

Net profit % = Net profit / Sales *100

Net profit % = 25000 / 100000 *100 = 25 %

Using original selling price, increase variable costs to 35% of the selling price

Statement of marginal costing

Particular Amount £ 1000 @ per unit Amount

Sales 100 100000

- Variable cost ( 35 %) 35 35000

Contribution 65 65000

- Fixed cost 50000 50000

Net profit 15000 15000

Calculation of Break even analysis

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

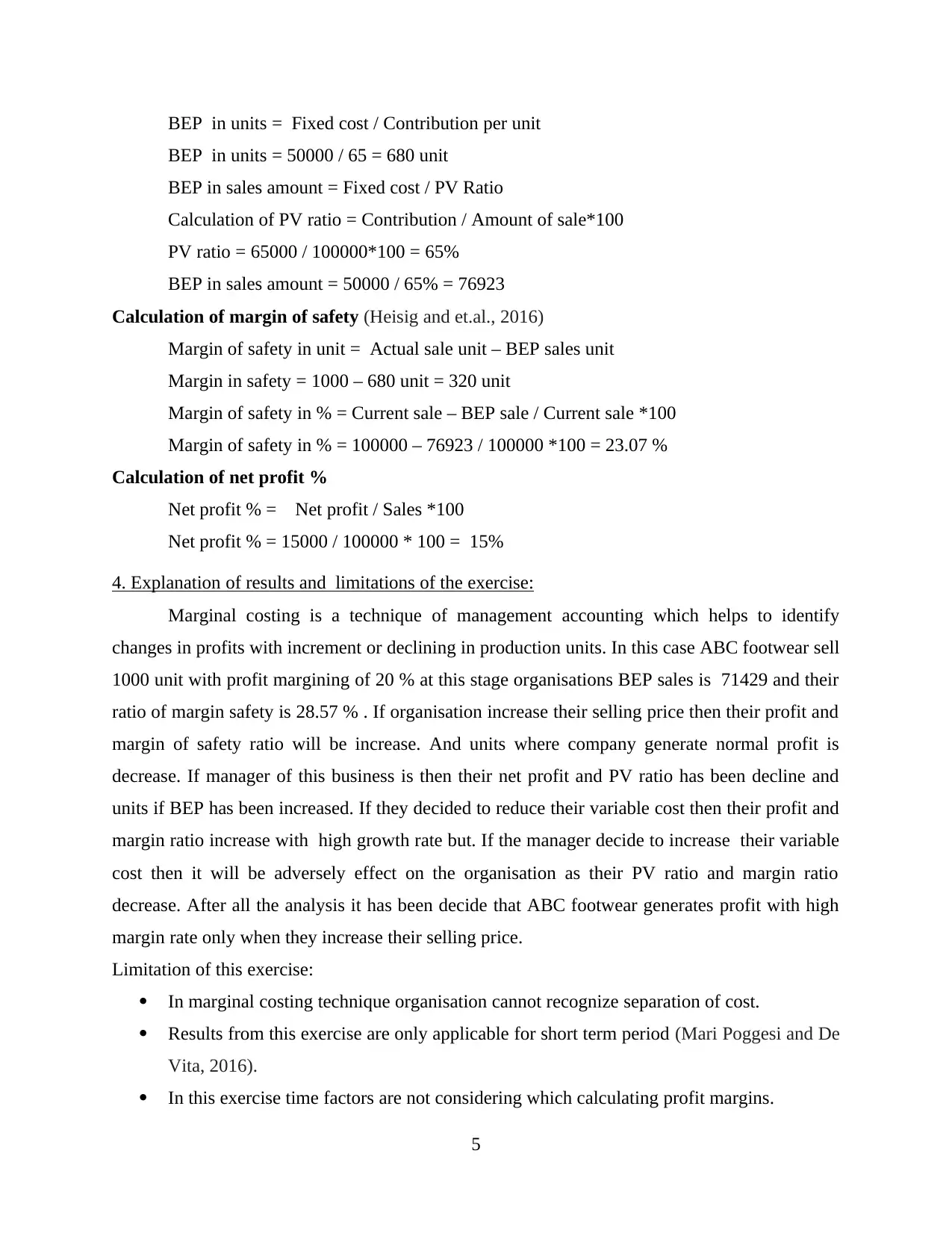

BEP in units = Fixed cost / Contribution per unit

BEP in units = 50000 / 65 = 680 unit

BEP in sales amount = Fixed cost / PV Ratio

Calculation of PV ratio = Contribution / Amount of sale*100

PV ratio = 65000 / 100000*100 = 65%

BEP in sales amount = 50000 / 65% = 76923

Calculation of margin of safety (Heisig and et.al., 2016)

Margin of safety in unit = Actual sale unit – BEP sales unit

Margin in safety = 1000 – 680 unit = 320 unit

Margin of safety in % = Current sale – BEP sale / Current sale *100

Margin of safety in % = 100000 – 76923 / 100000 *100 = 23.07 %

Calculation of net profit %

Net profit % = Net profit / Sales *100

Net profit % = 15000 / 100000 * 100 = 15%

4. Explanation of results and limitations of the exercise:

Marginal costing is a technique of management accounting which helps to identify

changes in profits with increment or declining in production units. In this case ABC footwear sell

1000 unit with profit margining of 20 % at this stage organisations BEP sales is 71429 and their

ratio of margin safety is 28.57 % . If organisation increase their selling price then their profit and

margin of safety ratio will be increase. And units where company generate normal profit is

decrease. If manager of this business is then their net profit and PV ratio has been decline and

units if BEP has been increased. If they decided to reduce their variable cost then their profit and

margin ratio increase with high growth rate but. If the manager decide to increase their variable

cost then it will be adversely effect on the organisation as their PV ratio and margin ratio

decrease. After all the analysis it has been decide that ABC footwear generates profit with high

margin rate only when they increase their selling price.

Limitation of this exercise:

In marginal costing technique organisation cannot recognize separation of cost.

Results from this exercise are only applicable for short term period (Mari Poggesi and De

Vita, 2016).

In this exercise time factors are not considering which calculating profit margins.

5

BEP in units = 50000 / 65 = 680 unit

BEP in sales amount = Fixed cost / PV Ratio

Calculation of PV ratio = Contribution / Amount of sale*100

PV ratio = 65000 / 100000*100 = 65%

BEP in sales amount = 50000 / 65% = 76923

Calculation of margin of safety (Heisig and et.al., 2016)

Margin of safety in unit = Actual sale unit – BEP sales unit

Margin in safety = 1000 – 680 unit = 320 unit

Margin of safety in % = Current sale – BEP sale / Current sale *100

Margin of safety in % = 100000 – 76923 / 100000 *100 = 23.07 %

Calculation of net profit %

Net profit % = Net profit / Sales *100

Net profit % = 15000 / 100000 * 100 = 15%

4. Explanation of results and limitations of the exercise:

Marginal costing is a technique of management accounting which helps to identify

changes in profits with increment or declining in production units. In this case ABC footwear sell

1000 unit with profit margining of 20 % at this stage organisations BEP sales is 71429 and their

ratio of margin safety is 28.57 % . If organisation increase their selling price then their profit and

margin of safety ratio will be increase. And units where company generate normal profit is

decrease. If manager of this business is then their net profit and PV ratio has been decline and

units if BEP has been increased. If they decided to reduce their variable cost then their profit and

margin ratio increase with high growth rate but. If the manager decide to increase their variable

cost then it will be adversely effect on the organisation as their PV ratio and margin ratio

decrease. After all the analysis it has been decide that ABC footwear generates profit with high

margin rate only when they increase their selling price.

Limitation of this exercise:

In marginal costing technique organisation cannot recognize separation of cost.

Results from this exercise are only applicable for short term period (Mari Poggesi and De

Vita, 2016).

In this exercise time factors are not considering which calculating profit margins.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

PART 2

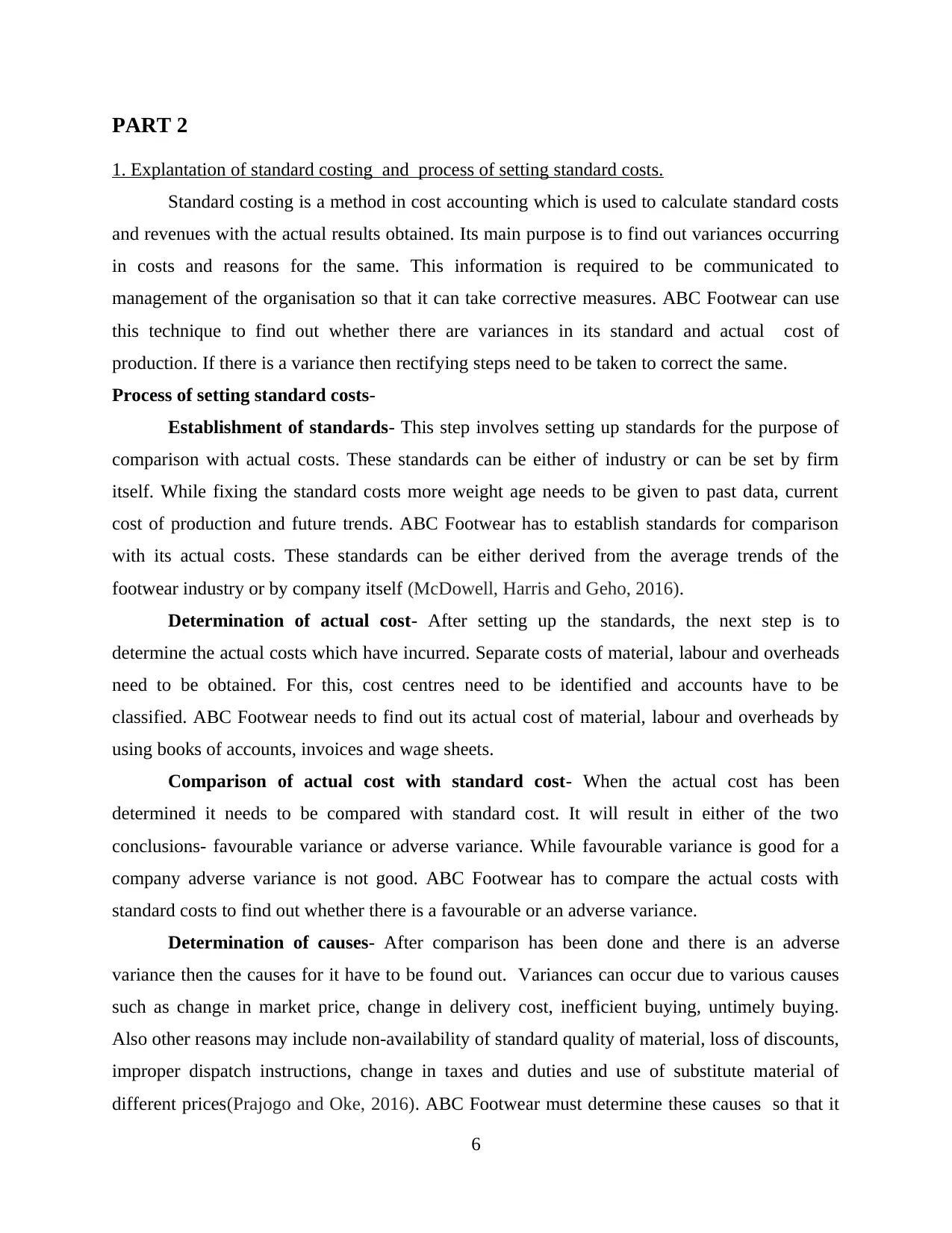

1. Explantation of standard costing and process of setting standard costs.

Standard costing is a method in cost accounting which is used to calculate standard costs

and revenues with the actual results obtained. Its main purpose is to find out variances occurring

in costs and reasons for the same. This information is required to be communicated to

management of the organisation so that it can take corrective measures. ABC Footwear can use

this technique to find out whether there are variances in its standard and actual cost of

production. If there is a variance then rectifying steps need to be taken to correct the same.

Process of setting standard costs-

Establishment of standards- This step involves setting up standards for the purpose of

comparison with actual costs. These standards can be either of industry or can be set by firm

itself. While fixing the standard costs more weight age needs to be given to past data, current

cost of production and future trends. ABC Footwear has to establish standards for comparison

with its actual costs. These standards can be either derived from the average trends of the

footwear industry or by company itself (McDowell, Harris and Geho, 2016).

Determination of actual cost- After setting up the standards, the next step is to

determine the actual costs which have incurred. Separate costs of material, labour and overheads

need to be obtained. For this, cost centres need to be identified and accounts have to be

classified. ABC Footwear needs to find out its actual cost of material, labour and overheads by

using books of accounts, invoices and wage sheets.

Comparison of actual cost with standard cost- When the actual cost has been

determined it needs to be compared with standard cost. It will result in either of the two

conclusions- favourable variance or adverse variance. While favourable variance is good for a

company adverse variance is not good. ABC Footwear has to compare the actual costs with

standard costs to find out whether there is a favourable or an adverse variance.

Determination of causes- After comparison has been done and there is an adverse

variance then the causes for it have to be found out. Variances can occur due to various causes

such as change in market price, change in delivery cost, inefficient buying, untimely buying.

Also other reasons may include non-availability of standard quality of material, loss of discounts,

improper dispatch instructions, change in taxes and duties and use of substitute material of

different prices(Prajogo and Oke, 2016). ABC Footwear must determine these causes so that it

6

1. Explantation of standard costing and process of setting standard costs.

Standard costing is a method in cost accounting which is used to calculate standard costs

and revenues with the actual results obtained. Its main purpose is to find out variances occurring

in costs and reasons for the same. This information is required to be communicated to

management of the organisation so that it can take corrective measures. ABC Footwear can use

this technique to find out whether there are variances in its standard and actual cost of

production. If there is a variance then rectifying steps need to be taken to correct the same.

Process of setting standard costs-

Establishment of standards- This step involves setting up standards for the purpose of

comparison with actual costs. These standards can be either of industry or can be set by firm

itself. While fixing the standard costs more weight age needs to be given to past data, current

cost of production and future trends. ABC Footwear has to establish standards for comparison

with its actual costs. These standards can be either derived from the average trends of the

footwear industry or by company itself (McDowell, Harris and Geho, 2016).

Determination of actual cost- After setting up the standards, the next step is to

determine the actual costs which have incurred. Separate costs of material, labour and overheads

need to be obtained. For this, cost centres need to be identified and accounts have to be

classified. ABC Footwear needs to find out its actual cost of material, labour and overheads by

using books of accounts, invoices and wage sheets.

Comparison of actual cost with standard cost- When the actual cost has been

determined it needs to be compared with standard cost. It will result in either of the two

conclusions- favourable variance or adverse variance. While favourable variance is good for a

company adverse variance is not good. ABC Footwear has to compare the actual costs with

standard costs to find out whether there is a favourable or an adverse variance.

Determination of causes- After comparison has been done and there is an adverse

variance then the causes for it have to be found out. Variances can occur due to various causes

such as change in market price, change in delivery cost, inefficient buying, untimely buying.

Also other reasons may include non-availability of standard quality of material, loss of discounts,

improper dispatch instructions, change in taxes and duties and use of substitute material of

different prices(Prajogo and Oke, 2016). ABC Footwear must determine these causes so that it

6

can take a corrective action and improve the overall performance so that variances don't occur

again. It is important to determine the causes of variance so that they don't occur again.

Disposition of variances- The last step in the process is to dispose off the variances

whether adverse or favourable by using Costing P&L A/c. The amount of variance resulting

because of improper standards and conditions beyond control of management can be adjusted to

work in progress, finished goods and cost of goods sold. ABC Footwear needs to ensure proper

disposition of variances (Rajnoha, Lesnikova and Korauš, 2016).

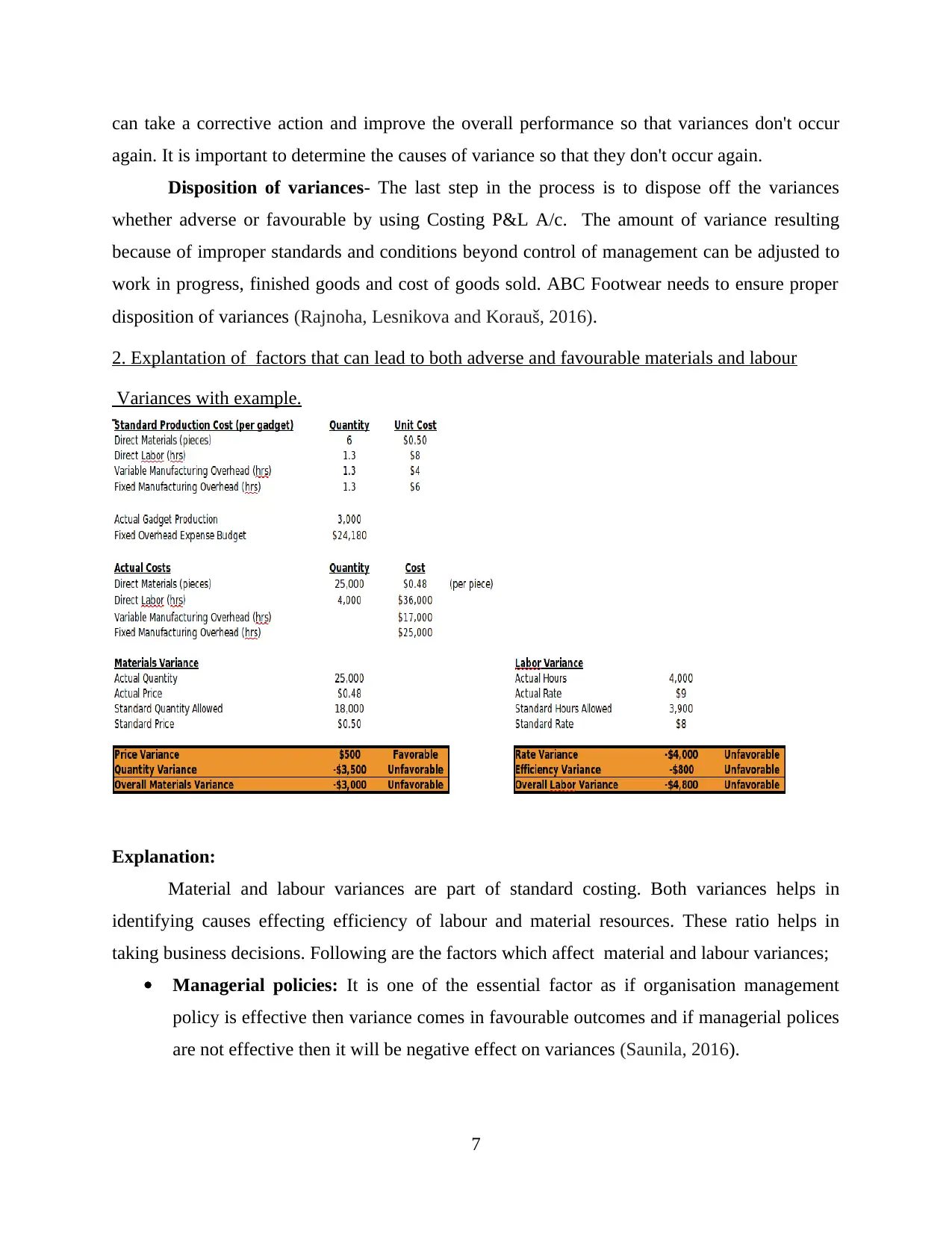

2. Explantation of factors that can lead to both adverse and favourable materials and labour

Variances with example.

Explanation:

Material and labour variances are part of standard costing. Both variances helps in

identifying causes effecting efficiency of labour and material resources. These ratio helps in

taking business decisions. Following are the factors which affect material and labour variances;

Managerial policies: It is one of the essential factor as if organisation management

policy is effective then variance comes in favourable outcomes and if managerial polices

are not effective then it will be negative effect on variances (Saunila, 2016).

7

again. It is important to determine the causes of variance so that they don't occur again.

Disposition of variances- The last step in the process is to dispose off the variances

whether adverse or favourable by using Costing P&L A/c. The amount of variance resulting

because of improper standards and conditions beyond control of management can be adjusted to

work in progress, finished goods and cost of goods sold. ABC Footwear needs to ensure proper

disposition of variances (Rajnoha, Lesnikova and Korauš, 2016).

2. Explantation of factors that can lead to both adverse and favourable materials and labour

Variances with example.

Explanation:

Material and labour variances are part of standard costing. Both variances helps in

identifying causes effecting efficiency of labour and material resources. These ratio helps in

taking business decisions. Following are the factors which affect material and labour variances;

Managerial policies: It is one of the essential factor as if organisation management

policy is effective then variance comes in favourable outcomes and if managerial polices

are not effective then it will be negative effect on variances (Saunila, 2016).

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Incentive policies: If organisations provides incentives to labours for their work

performance then their variance generates favourable results. In this example it has been

analysis that labour variance generates unfavourable result this means that their

organisation is not provides them incentive thus their efficiency ratio decrease.

Quality of raw material: If organisation use high quality of raw material then their

quality ratio of material generates result in favour of organisation. But if they uses low

quality of product then it will reduce quality level of their product.

Effective Operating cycle period: If organisations operating cycle period is take short

time in circulate their process then it will effect variance in positive way and if this

period take long time to compete their cycle then it will impact negative. In this example

material and labour variance both are unfavourable this means that their operating cycle

period take long time in their process.

3. explanation of standard costing as a tool for control.

Standard Costing as a tool of control

Standard costing can be used as a tool of control by the management. It can help the

management in taking effective decisions to reduce the overall cost which will help in

maximisation of profits. ABC Footwear's managers can use it for bringing efficiency and

effectiveness in its cost operations which will benefit it in the long-run.

Advantages of standard costing as a management tool-

Fixation of price- Standard costing can help in fixation of price of inventory as well as

finished goods for sale. Managers of ABC Footwear can use it to fix the price of their stock and

finished goods.

Framing of production policy- Production policy can be framed using standard costs as

a parameter. ABC Footwear can frame its production policy using price and quantity, standard

hours and standard output (Vij and Bedi, 2016).

Comparison and analysis of data- Standard costing helps in comparison of actual

results obtained with the set standards. If the variances are obtained then corrective measures

need to be taken. ABC Footwear can use this technique to compare the data and analysing it for

the purpose of interpretation.

8

performance then their variance generates favourable results. In this example it has been

analysis that labour variance generates unfavourable result this means that their

organisation is not provides them incentive thus their efficiency ratio decrease.

Quality of raw material: If organisation use high quality of raw material then their

quality ratio of material generates result in favour of organisation. But if they uses low

quality of product then it will reduce quality level of their product.

Effective Operating cycle period: If organisations operating cycle period is take short

time in circulate their process then it will effect variance in positive way and if this

period take long time to compete their cycle then it will impact negative. In this example

material and labour variance both are unfavourable this means that their operating cycle

period take long time in their process.

3. explanation of standard costing as a tool for control.

Standard Costing as a tool of control

Standard costing can be used as a tool of control by the management. It can help the

management in taking effective decisions to reduce the overall cost which will help in

maximisation of profits. ABC Footwear's managers can use it for bringing efficiency and

effectiveness in its cost operations which will benefit it in the long-run.

Advantages of standard costing as a management tool-

Fixation of price- Standard costing can help in fixation of price of inventory as well as

finished goods for sale. Managers of ABC Footwear can use it to fix the price of their stock and

finished goods.

Framing of production policy- Production policy can be framed using standard costs as

a parameter. ABC Footwear can frame its production policy using price and quantity, standard

hours and standard output (Vij and Bedi, 2016).

Comparison and analysis of data- Standard costing helps in comparison of actual

results obtained with the set standards. If the variances are obtained then corrective measures

need to be taken. ABC Footwear can use this technique to compare the data and analysing it for

the purpose of interpretation.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Cost emphasis- Standard costing helps in laying emphasis on cost and finding out

methods to reduce it. ABC Footwear can use it to put the emphasis of management on managing

costs incurred in production.

Better forecasting- The reasons due to which variances have occurred are taken into

consideration for doing better forecasting of budget. ABC Footwear can use standard costing for

doing better forecasting of costs which are likely to incur in the future (Wang Pauleen and

Zhang, 2016).

CONCLUSION

From the above analysis it has been concluded that managers uses various performance

management techniques which helps in expansion of their business units. Marginal costing

technique use by mangers to take decisions regarding choosing best alternative among others,

which help in generating more profit. On the other side mangers uses standard costing method

for analysing performance level of their production factors by identifying differences between

actual and standard cost. This will help managers to formulate those polices which help in

reducing gap between actual and standard cost and enhance efficiency level of production factors

of the organisation.

9

methods to reduce it. ABC Footwear can use it to put the emphasis of management on managing

costs incurred in production.

Better forecasting- The reasons due to which variances have occurred are taken into

consideration for doing better forecasting of budget. ABC Footwear can use standard costing for

doing better forecasting of costs which are likely to incur in the future (Wang Pauleen and

Zhang, 2016).

CONCLUSION

From the above analysis it has been concluded that managers uses various performance

management techniques which helps in expansion of their business units. Marginal costing

technique use by mangers to take decisions regarding choosing best alternative among others,

which help in generating more profit. On the other side mangers uses standard costing method

for analysing performance level of their production factors by identifying differences between

actual and standard cost. This will help managers to formulate those polices which help in

reducing gap between actual and standard cost and enhance efficiency level of production factors

of the organisation.

9

REFERENCES

Books and Journals:

Bresciani, S. and Ferraris, A., 2016. Innovation-receiving subsidiaries and dual embeddedness:

impact on business performance. Baltic Journal of Management.

Cleary, P. and Quinn, M., 2016. Intellectual capital and business performance. Journal of

Intellectual Capital.

Fasone, V., Kofler, L. and Scuderi, R., 2016. Business performance of airports: Non-aviation

revenues and their determinants. Journal of Air Transport Management. 53. pp.35-45.

Haseeb, M. and et.al., 2019. Industry 4.0: A solution towards technology challenges of

sustainable business performance. Social Sciences. 8(5). p.154.

Heisig, P. and et.al., 2016. Knowledge management and business performance: global experts’

views on future research needs. Journal of Knowledge Management.

Mari, M., Poggesi, S. and De Vita, L., 2016. Family embeddedness and business performance:

Evidences from women-owned firms. Management Decision.

McDowell, W. C., Harris, M. L. and Geho, P. R., 2016. Longevity in small business: The effect

of maturity on strategic focus and business performance. Journal of Business Research.

69(5). pp.1904-1908.

Prajogo, D. I. and Oke, A., 2016. Human capital, service innovation advantage, and business

performance. International Journal of Operations & Production Management.

Rajnoha, R., Lesnikova, P. and Korauš, A., 2016. From financial measures to strategic

performance measurement system and corporate sustainability: empirical evidence from

Slovakia. Economics and Sociology.

Saunila, M., 2016. Performance measurement approach for innovation capability in SMEs.

International Journal of Productivity and Performance Management.

Vij, S. and Bedi, H. S., 2016. Are subjective business performance measures justified?.

International Journal of Productivity and Performance Management.

Wang, W. Y., Pauleen, D. J. and Zhang, T., 2016. How social media applications affect B2B

communication and improve business performance in SMEs. Industrial Marketing

Management. 54. pp.4-14.

10

Books and Journals:

Bresciani, S. and Ferraris, A., 2016. Innovation-receiving subsidiaries and dual embeddedness:

impact on business performance. Baltic Journal of Management.

Cleary, P. and Quinn, M., 2016. Intellectual capital and business performance. Journal of

Intellectual Capital.

Fasone, V., Kofler, L. and Scuderi, R., 2016. Business performance of airports: Non-aviation

revenues and their determinants. Journal of Air Transport Management. 53. pp.35-45.

Haseeb, M. and et.al., 2019. Industry 4.0: A solution towards technology challenges of

sustainable business performance. Social Sciences. 8(5). p.154.

Heisig, P. and et.al., 2016. Knowledge management and business performance: global experts’

views on future research needs. Journal of Knowledge Management.

Mari, M., Poggesi, S. and De Vita, L., 2016. Family embeddedness and business performance:

Evidences from women-owned firms. Management Decision.

McDowell, W. C., Harris, M. L. and Geho, P. R., 2016. Longevity in small business: The effect

of maturity on strategic focus and business performance. Journal of Business Research.

69(5). pp.1904-1908.

Prajogo, D. I. and Oke, A., 2016. Human capital, service innovation advantage, and business

performance. International Journal of Operations & Production Management.

Rajnoha, R., Lesnikova, P. and Korauš, A., 2016. From financial measures to strategic

performance measurement system and corporate sustainability: empirical evidence from

Slovakia. Economics and Sociology.

Saunila, M., 2016. Performance measurement approach for innovation capability in SMEs.

International Journal of Productivity and Performance Management.

Vij, S. and Bedi, H. S., 2016. Are subjective business performance measures justified?.

International Journal of Productivity and Performance Management.

Wang, W. Y., Pauleen, D. J. and Zhang, T., 2016. How social media applications affect B2B

communication and improve business performance in SMEs. Industrial Marketing

Management. 54. pp.4-14.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.